Occlusion Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.68 Billion |

| Market Size (2031) | USD 4.97 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

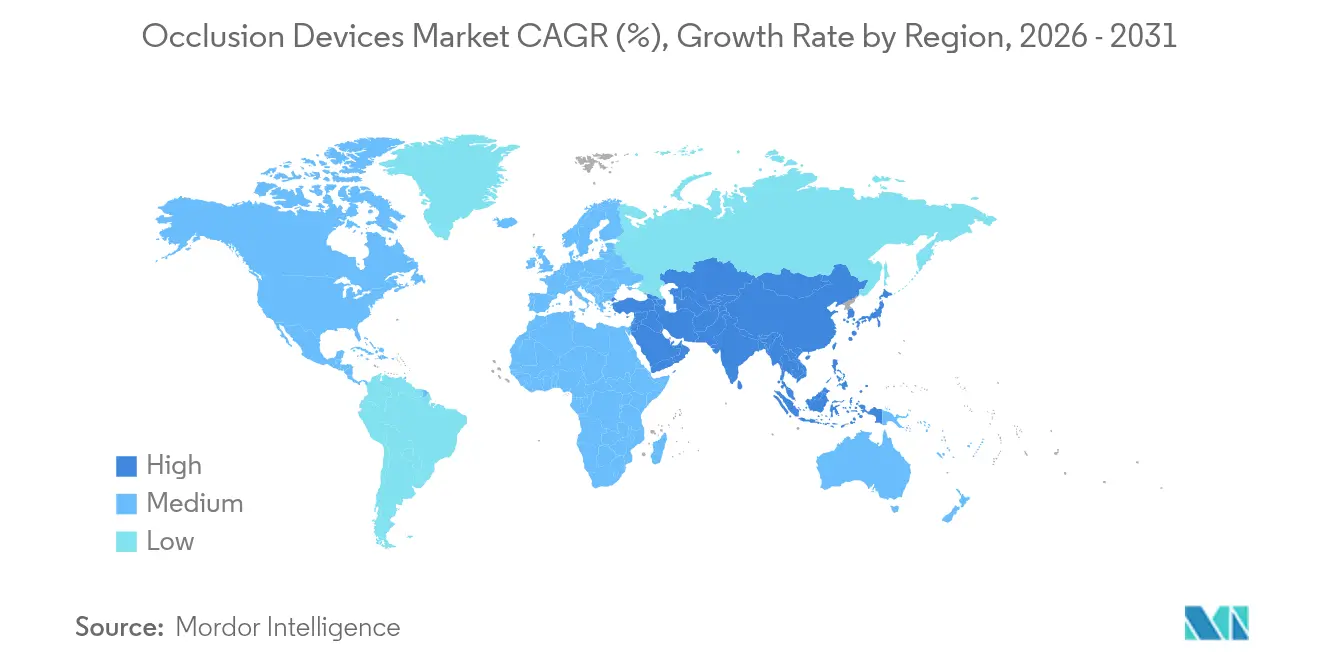

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

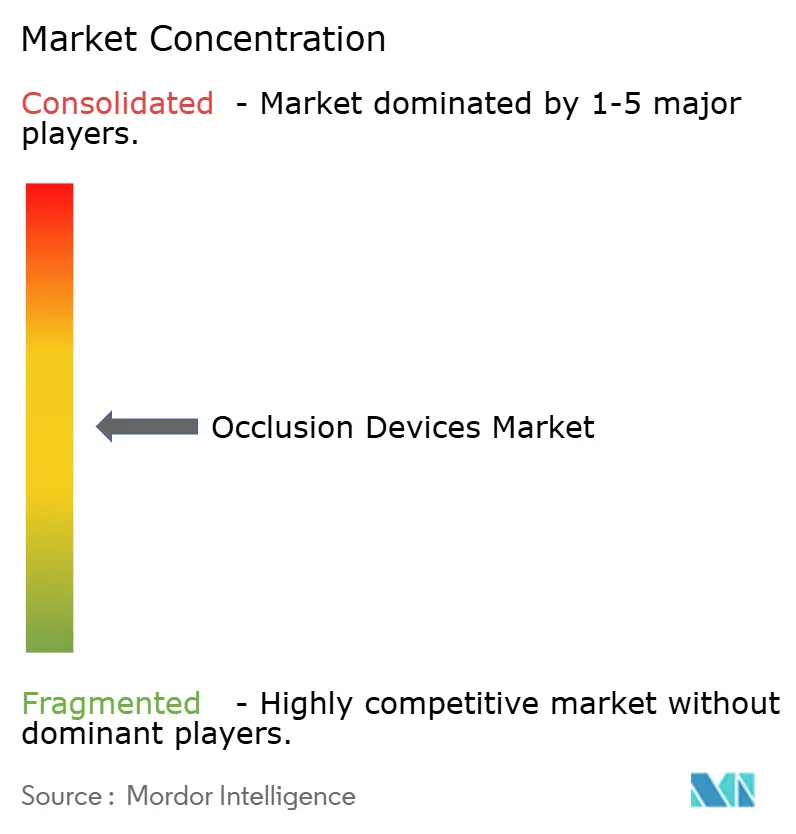

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Occlusion Devices Market Analysis by Mordor Intelligence

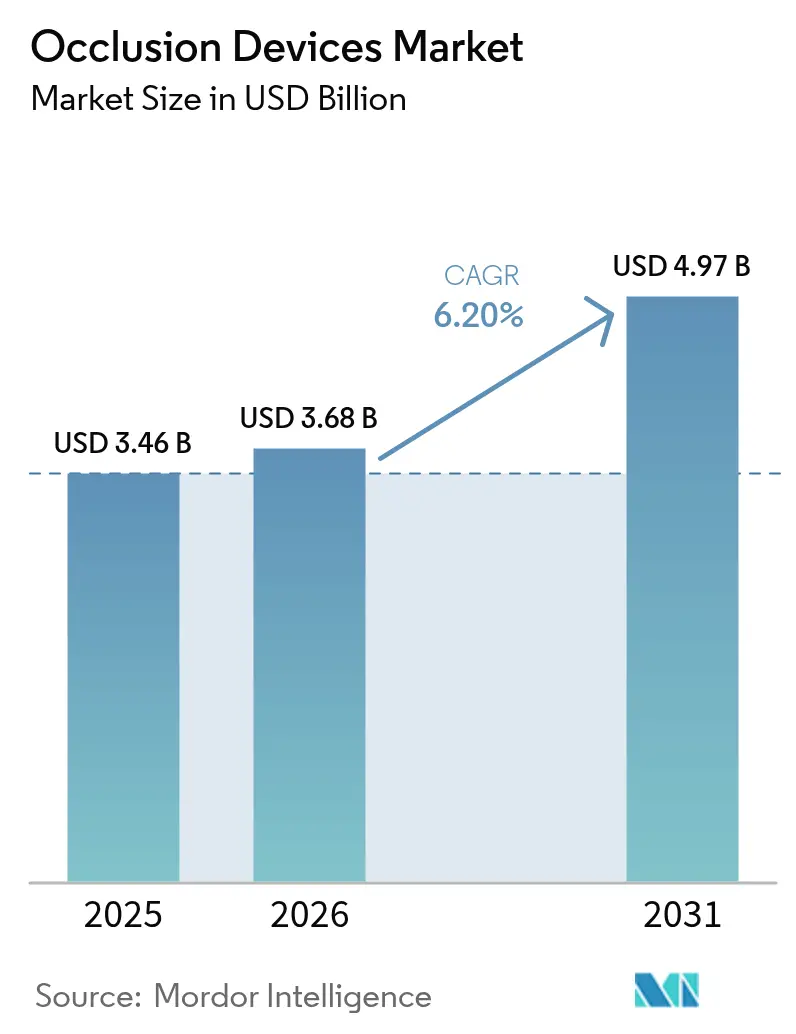

The Occlusion Devices Market size was valued at USD 3.46 billion in 2025 and estimated to grow from USD 3.68 billion in 2026 to reach USD 4.97 billion by 2031, at a CAGR of 6.20% during the forecast period (2026-2031).

Across the forecast horizon, rising demand for minimally invasive neurovascular and peripheral interventions, steady migration of complex procedures into outpatient settings, and regulatory clarity for AI-enabled devices collectively underpin expansion. Persistent pressure on providers to shorten length-of-stay, together with broader insurance coverage for stroke and aneurysm care, reinforces purchasing of next-generation occlusion systems. Material innovation centred on bio-resorbable polymers opens new commercial white spaces, while supply-chain stress around high-grade alloys and the need for specialist training temper growth in some low-resource regions. Portfolio breadth, clinical-evidence leadership, and rapid integration of AI and robotic assistance remain the core competitive levers in the occlusion devices market.

Key Report Takeaways

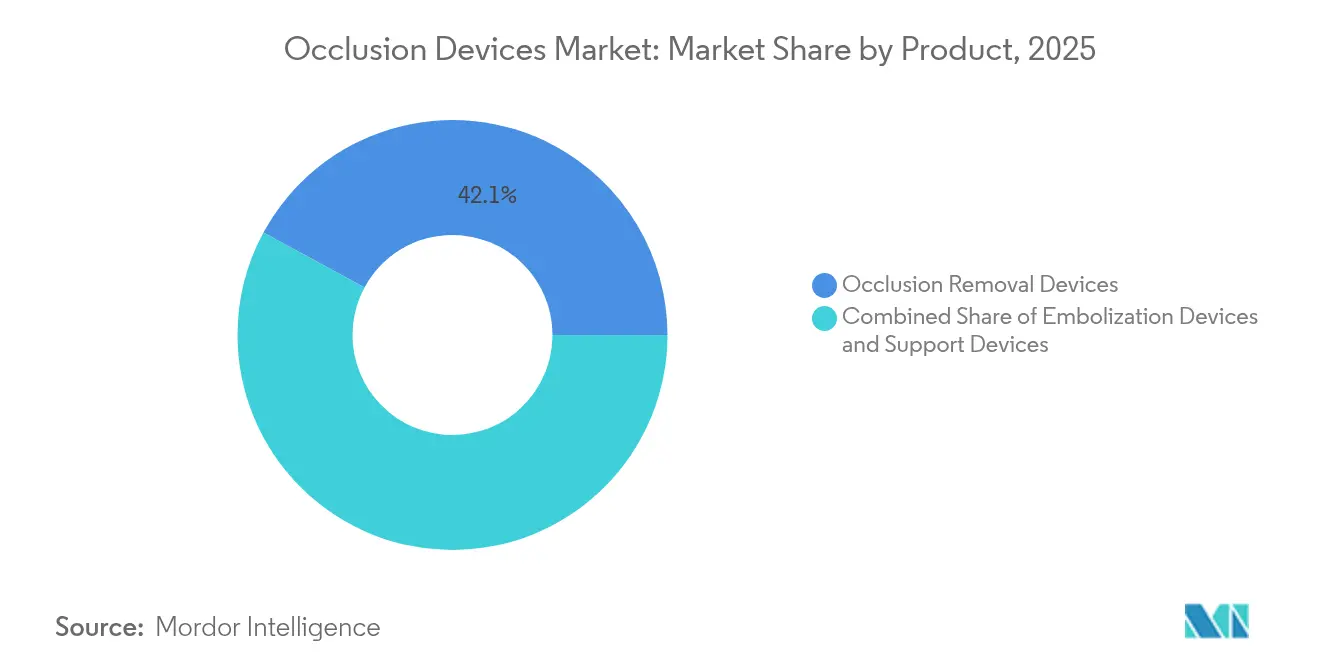

- By product type, occlusion removal devices captured 42.10% of the occlusion devices market share in 2025; embolization devices are projected to expand at an 7.88% CAGR through 2031.

- By material, nitinol accounted for 43.40% share of the occlusion devices market size in 2025, whereas bio-resorbable polymers are advancing at an 11.20% CAGR to 2031.

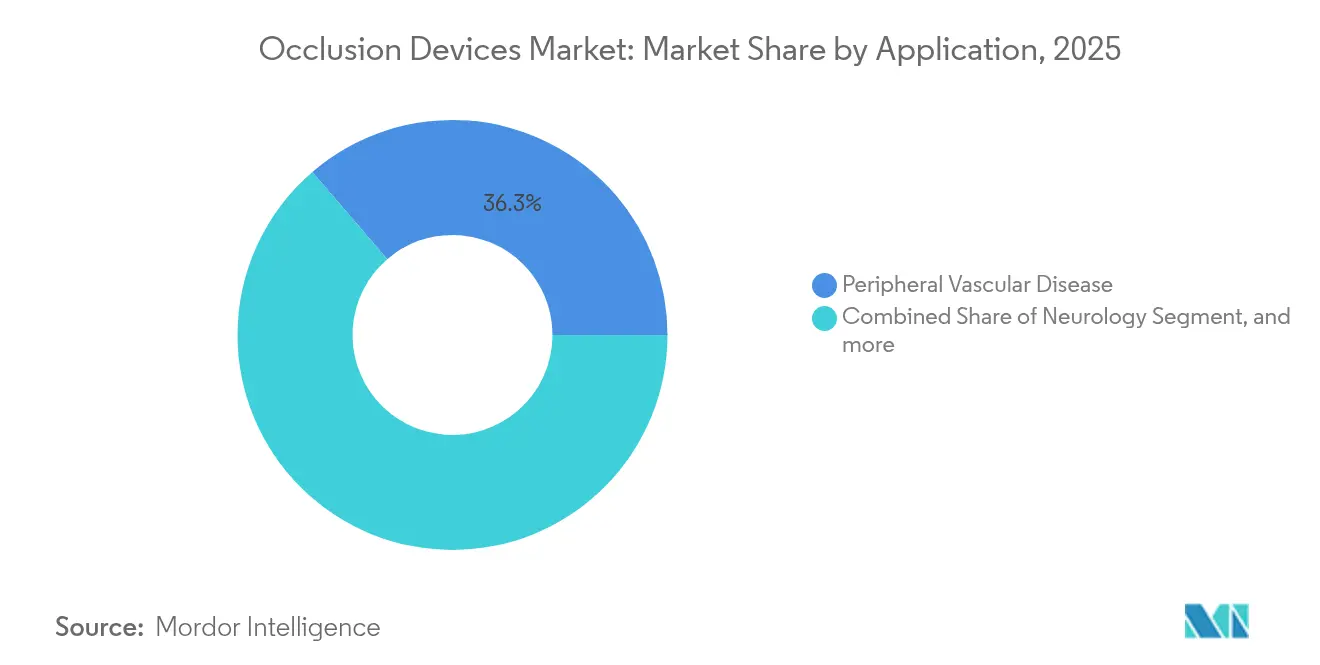

- By application, peripheral vascular disease represented 36.30% of the occlusion devices market size in 2025; oncology is forecast to grow at a 9.61% CAGR over the same period.

- By disease pathology, ischemic stroke retained 37.20% share of the occlusion devices market in 2025, while tumor embolization register a 8.33% CAGR to 2031.

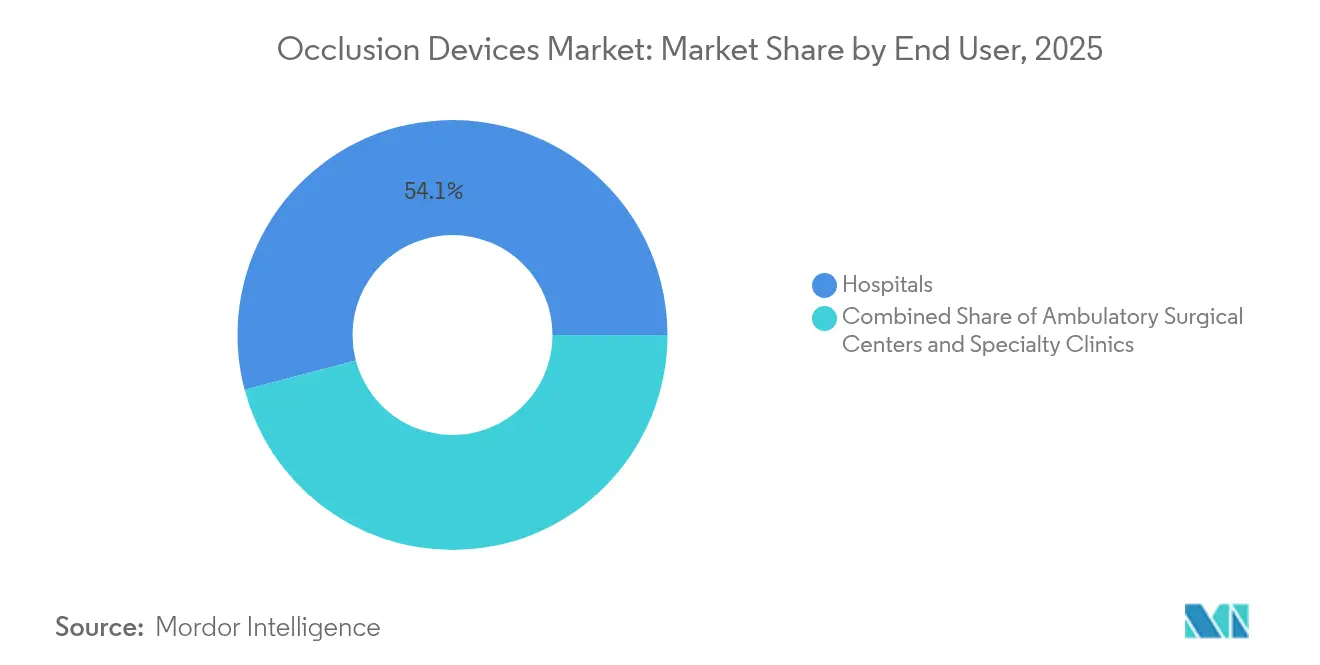

- By end user, hospitals retained 54.10% share of the occlusion devices market in 2025, while ambulatory surgical centers register a 10.63% CAGR to 2031.

- By geography, North America led with 42.60% revenue share in 2025; Asia-Pacific is the fastest-growing region at a 12.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Occlusion Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Preference for Minimally Invasive Occlusive Procedures | +1.2% | Global, strongest in North America & Europe | Medium term (2–4 years) |

| Shift Toward Ambulatory Endovascular Care Models | +0.8% | North America & EU core, expanding to Asia-Pacific | Long term (≥4 years) |

| Integration of AI-Guided Imaging & Robotic Assistance | +1.1% | Global, led by developed markets | Medium term (2–4 years) |

| Broader Insurance Coverage for Stroke Interventions | +0.9% | North America, Europe, select Asia-Pacific | Short term (≤2 years) |

| Rising Neuro-Oncology Demand Linked to SRS & Trans-Radial Techniques | +0.7% | Global, concentrated in major medical centers | Long term (≥4 years) |

| Material Innovation Toward Bio-Resorbable Polymers | +0.6% | Global, with accelerated R&D in Europe & Asia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Minimally Invasive Occlusive Procedures

Regulators cleared several next-generation systems in 2024 that improve deliverability and reduce complication rates, illustrating confidence in less-invasive approaches.[1]U.S. Food and Drug Administration, “510(k) Clearances 2024,” fda.gov Comparative studies show hospital stay reductions of 1.5–2 days and 15–20% total episode cost savings when occlusion devices replace open surgery. These clinical and economic benefits encourage provider adoption, especially in reimbursement-sensitive environments. Ambulatory centers report double-digit volume increases as minimally invasive protocols become routine, reinforcing demand for devices that support same-day discharge. With stroke and peripheral arterial disease incidence rising among ageing populations, minimally invasive occlusion solutions remain central to future treatment algorithms.

Shift Toward Ambulatory Endovascular Care Models

Updated 2025 CMS payment rules now reimburse a broader list of endovascular procedures in outpatient settings.[2]Centers for Medicare & Medicaid Services, “Hospital Outpatient Prospective Payment System 2025,” cms.gov This shift lets ASCs invest in premium occlusion platforms while maintaining cost advantages over hospitals. Data from multisite registries indicate equivalent safety profiles and 25–30% lower total costs for ASC procedures. Payers gain from reduced facility fees, prompting insurers to authorise more cases outside hospitals. Manufacturers respond with compact consoles and single-use kits engineered for smaller procedure rooms. As the outpatient share of endovascular volumes climbs, demand concentrates on devices that balance portability, ease of use, and robust clinical performance.

Integration of AI-Guided Imaging & Robotic Assistance

FDA draft guidance issued in 2025 defines clear pathways for adaptive algorithms, giving suppliers certainty to embed AI directly into occlusion systems. Clinical trials highlight 15–20% improvements in device-placement accuracy and shorter fluoroscopy times when AI-driven navigation is used. Robotic platforms further cut operator variability, expanding eligibility for patients with challenging anatomy. Early adopters document faster learning curves and lower radiation exposure for staff. Competitive advantage increasingly hinges on validated datasets and post-market surveillance infrastructure that feed algorithm refinement, creating high barriers for late entrants.

Broader Insurance Coverage for Stroke Interventions

The 2025 Medicare physician fee schedule boosts reimbursement not only for mechanical thrombectomy but also for caregiver training and follow-up services, recognising the full continuum of stroke care. Commercial insurers align policies, widening access to preventive aneurysm treatment. Emerging tele-stroke networks link community hospitals with urban stroke centres, improving time-to-treatment metrics and stimulating device demand in previously under-served areas. Similar coverage expansions across Asia-Pacific support double-digit regional growth as governments address rising cerebrovascular disease burdens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Costs in Resource-Limited Settings | -0.8% | Global, most severe in emerging markets and rural areas | Long term (≥ 4 years) |

| Training Demands for Neuro-Occlusion Techniques | -0.6% | Global, particularly acute in rural/underserved areas | Medium term (2-4 years) |

| Material Safety Concerns in Flow-Diversion | -0.4% | Global, with heightened scrutiny in EU and North America | Short term (≤ 2 years) |

| Vulnerable Supply Chains for High-Grade Alloys | -0.5% | Global, most impactful in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs in Resource-Limited Settings

Healthcare providers in emerging economies struggle to fund premium occlusion systems amid competing spending priorities. Currency volatility and EU MDR-related compliance costs that suppliers pass through to buyers raise acquisition prices by 15–25%.[3]Johnson & Johnson, “2024 Annual Report,” jnj.com Financing innovations such as leasing and shared-service models partly ease barriers, yet uptake lags in rural hospitals where stroke burden is high. Without consistent device access, these regions risk poorer outcomes and widening care disparities.

Training Demands for Neuro-Occlusion Techniques

Mastery of advanced mechanical thrombectomy or flow-diversion procedures demands 50–100 supervised cases, limiting the number of credentialed operators. Workforce shortages are pronounced outside major academic centres, creating geographic utilisation gaps. AI-guided systems shorten learning curves, but standardised certification remains uneven. Professional societies are rolling out global curricula; however, scaling mentorship programs takes time, restraining short-term growth in frontier markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Removal Devices Sustain Lead as Embolization Surges

Removal devices secured 42.10% of the occlusion devices market in 2025 owing to their indispensable role in emergency stroke care where rapid vessel recanalisation dictates outcomes. Robust clinical guidelines and favourable reimbursement sustain steady demand, while iterative design advances such as enhanced clot-engagement stent retrievers sharpen clinical performance. Emerging miniaturised coil retrievers broaden treatable anatomy, reinforcing segment resilience. Concurrently, Embolization devices post an 7.88% CAGR to 2031, propelled by growth in oncology and preventive aneurysm workflows. Providers increasingly prefer combination therapy kits that package embolic agents with delivery catheters, improving procedural efficiency. Support devices grow in tandem, supplying micro-catheters, guidewires, and ancillary tools that enable precise deployment across complex vasculature.

Clinicians report expanding utilisation of removal devices in distal stroke territories once considered unreachable, thanks to ultra-trackable stent retrievers. Manufacturers integrate radiopaque markers and kink-resistant shaft designs that maintain tactile feedback while improving deliverability. Embolization innovators focus on bio-active coils and liquid embolics that achieve definitive occlusion with lower re-canalisation rates. As oncologic and trauma indications broaden, the balance of revenue slowly tilts toward embolization, yet emergency neurovascular applications safeguard the primacy of removal systems within the occlusion devices market.

By Material: Nitinol Dominates but Bio-Resorbables Accelerate

Nitinol, with 43.40% 2025 share, remains the backbone of high-performance occlusion devices because shape-memory and super-elastic characteristics match tortuous cerebrovascular anatomy. Suppliers refine alloy purity and surface treatments to mitigate nickel ion release and enhance endothelialisation. Platinum continues serving cases requiring high radiopacity for fine anatomical visualisation. In contrast, bio-resorbable polymers record an 11.20% CAGR, mirroring clinician appetite for temporary scaffolds that avoid long-term imaging artefacts and permit future interventions. Early clinical programs demonstrate predictable degradation profiles and favourable inflammatory responses, although manufacturing yields and sterilisation protocols still add cost premiums.

Device makers explore hybrid constructions, embedding radiopaque fibres into polymer matrices to marry visibility with resorption. Regulatory bodies require stringent in-vivo degradation data, delaying market entry for some concepts. Yet once scale efficiencies materialise, bio-resorbables promise to expand indications where permanent implants pose lifetime risk management challenges. The competition between metallic durability and polymer convenience is likely to shape materials R&D budgets throughout the forecast period.

By Application: Oncology Emerges as Rapid-Growth Pillar

Peripheral Vascular Disease retained 36.30% share of the occlusion devices market size in 2025 on the back of entrenched endovascular protocols for limb salvage and chronic occlusion relief. The segment provides predictable base revenue, but its growth curve is maturing. Oncology applications, posting a 9.61% CAGR, leverage occlusion to deliver chemo-embolisation and radio-embolisation directly to tumours, shrinking systemic toxicity and recovery times. Neurovascular stroke indications stay robust as national stroke networks proliferate, whereas urology benefits modestly from increased embolisation for benign prostatic hyperplasia and arteriovenous malformations.

Interventional oncologists cite improved quality-of-life scores when targeted embolisation precedes systemic therapy. AI-assisted imaging enhances lesion targeting, further lifting clinical outcomes. Industry partnerships with drug-delivery specialists seek to co-develop combination regimens where embolic particles double as drug carriers. This blurring of device and pharmaceutical lines could accelerate future oncology-centric revenue streams within the occlusion devices market.

By Disease Pathology: Tumour Embolisation Gains Momentum

Ischaemic Stroke accounted for 37.20% of 2025 revenue, reflecting its entrenched status as the largest pathology segment requiring immediate mechanical intervention. Evidence from multicentre registries posts >85% recanalisation success with modern stent retrievers, maintaining strong demand. Tumour embolisation grows at an 8.33% CAGR as interventional radiology expands beyond palliation to curative intent in select hepatocellular and renal tumours. Cerebral aneurysm treatment benefits from prophylactic flow-diversion, while peripheral arterial occlusion volumes rise in tandem with diabetes prevalence.

The validated performance of devices like WEB 17 in ruptured and unruptured aneurysms broadens physician confidence. Meanwhile, oncology protocols adopt staged embolisation approaches to reduce operative bleeding, presenting recurring revenue opportunities as patients cycle through multiple sessions. As cancer incidence climbs with ageing populations, the tumour embolisation niche evolves into a strategic pillar underpinning overall market expansion.

By End User: ASCs Rapidly Narrow Gap with Hospitals

Hospitals delivered 54.10% of occlusion devices market revenue in 2025, leveraging comprehensive imaging suites and neuro-critical care capacity required for complex cases. Nevertheless, Ambulatory Surgical Centers are projected to post a 10.63% CAGR as revised payment incentives and portable imaging solutions empower them to handle routine stroke and embolisation procedures. Specialty clinics occupy a mid-ground, focusing on elective oncologic or peripheral interventions where narrow expertise drives referral traffic.

ASC operators cite 25–30% cost savings and high patient satisfaction owing to shorter admission cycles. Manufacturers now field compact capital equipment bundles tailored for ASC procedural rooms. Remote proctoring and AI-enabled guidance further reduce training hurdles, helping community settings match urban hospital outcomes. Over the forecast horizon, cases migrating to ASCs will reshape procurement patterns, favouring suppliers offering integrated disposables and imaging software subscriptions over heavyweight capital goods.

Geography Analysis

North America generated 42.60% of 2025 revenue, buoyed by Medicare reimbursement certainty, dense stroke-centre networks, and a mature innovation ecosystem spanning academic hospitals and industry partners. Continued FDA policy clarity around AI and bio-resorbables sustains a favourable launch environment for novel occlusion solutions. Canada’s single-payer system channels incremental funding to stroke prevention, while Mexico’s public–private hospital expansion gradually adds procedure capacity. Talent concentration and strong payer-provider alignment preserve North America’s leadership despite intensifying cost-containment pressures.

Asia-Pacific posts the fastest regional CAGR at 12.41% through 2031, underpinned by rapid hospital construction, insurance expansion, and mounting cerebrovascular disease prevalence among ageing citizens. China’s Volume-Based Procurement framework compresses price points, yet sheer procedural volume and provincial stroke-centre rollouts offset margin pressure. Japan leads research into high-precision micro-catheters and advanced alloy compositions, although demographic headwinds moderate long-term procedure growth. India, with improving neuro-interventional training pipeline and rising middle-class insurance coverage, delivers high-double-digit unit growth despite infrastructure gaps. South Korea and Australia provide stable demand anchored in high-acuity tertiary facilities and active clinical-trial participation.

Europe maintains steady, mid-single-digit growth driven by robust universal healthcare systems, continent-wide stroke care protocols, and pan-EU regulatory harmonisation that expedites multi-market launches. Germany’s engineering strengths support local manufacturing clusters, while the United Kingdom, navigating post-Brexit adjustments, remains influential in guideline development and outcomes research. Southern European markets benefit from EU Cohesion Funds funnelling capital into hospital modernisation, whereas Eastern Europe offers long-term upside as reimbursement frameworks mature. Collaborative initiatives between the European Medicines Agency and FDA accelerate evidence sharing, shortening time-to-market for cross-Atlantic product launches.

Competitive Landscape

Market concentration is moderate, with diversified conglomerates and focused neuro-vascular specialists competing across overlapping procedural domains. Stryker’s USD 4.9 billion acquisition of Inari Medical and Johnson & Johnson’s USD 13.1 billion purchase of Shockwave Medical in 2025 illustrate vertical integration strategies aimed at bundling occlusion, atherectomy, and intravascular lithotripsy to capture full episode-of-care economics. These deals enhance cross-selling into stroke and peripheral arterial disease workflows and consolidate clinical data assets critical for AI algorithm training.

Technology differentiation increasingly hinges on proprietary imaging software and robotic navigation platforms. Firms with extensive post-market registries feed machine-learning engines that optimise device selection and placement in real time. FDA guidance on adaptive algorithms confers first-mover advantage to companies with validated datasets, raising the compliance hurdle for start-ups. Meanwhile, innovators targeting bio-resorbable polymers attract venture capital eager to back disruptive materials, though scale-up challenges persist.

Supply-chain resilience emerges as a strategic priority after alloy shortages in 2024 exposed dependence on a narrow vendor base. Leading players now dual-source nitinol and invest in additive manufacturing to localise production. Training and service networks remain critical moats; vendors provide turnkey education platforms and remote proctoring to speed customer onboarding, particularly in emerging markets where operator density is low. Overall, competitors combine M&A, R&D, and service differentiation to defend share in the evolving occlusion devices market.

Occlusion Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

BTG International Ltd

Medtronic

Edwards Lifesciences

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product and indication white space continues to expand where care pathways favor minimally invasive, shorter-stay interventions and where payer policy supports migration to outpatient settings. The 2025 CMS Hospital Outpatient Prospective Payment System update broadened reimbursement for more endovascular procedures in outpatient settings, which is increasing demand for ASC-ready occlusion platforms (compact footprints, simplified setup, and single-use kits) and matching the momentum already seen in ambulatory surgical centers. For neurovascular and peripheral embolization, recent FDA clearances for new occlusion and embolization systems, including Okami Medicals LOBO Vascular Occlusion System (510(k), April 2026), point to a steady cadence of predicate-based product refreshes, with more room for differentiated deliverability, visibility, and vessel-matching design features.

Structural heart occlusion is also becoming more competitive and innovation-led, with left atrial appendage (LAA) exclusion and occlusion attracting new entrants and a widening range of devices. Edwards Lifesciences FDA 510(k) clearance for the Ecliptis LAA exclusion system (June 2026) and Genesee BioMedicals 510(k) clearance for its ATLAAS epicardial LAA occlusion device (May 2026) highlight pipeline activity beyond the established LAA incumbents. This keeps procedural efficiency, including imaging workflow, and clinical evidence generation central to hospital purchasing decisions. In parallel, targeted neurovascular innovation continues, such as MicroPort NeuroTechs FDA approval for the NUMEN Helia spring coil embolization system (May 2026), which supports opportunity in complex lesion anatomies where standard coils or plugs face delivery limits and where broader portfolio coverage can help hospitals standardize across cases.

Recent Industry Developments

- June 2026: Edwards Lifesciences received FDA 510(k) clearance for the Ecliptis left atrial appendage (LAA) exclusion system. The clearance adds a new branded option in structural-heart occlusion and increases competitive pressure in LAA therapy ecosystems where procedure workflow, imaging compatibility, and clinical evidence affect adoption.

- February 2026: Abbott shared positive 45-day results from its VERITAS Study for the Amulet 360 LAA Occluder. The update supports Abbotts iteration cycle in LAA closure by focusing on performance endpoints that can shape physician preference and contracting discussions in hospital structural-heart programs.

- October 2024: Conformal Medical began enrollment in the GLACE Study in Europe evaluating ICE-guided imaging during LAA closure using its CLAAS AcuFORM device. The trial activity extends clinical evidence generation for alternative LAA closure approaches and indicates ongoing investment in procedural simplification and imaging-guided workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers medical occlusion devices used in minimally invasive procedures to block, seal, or close a vessel or an anatomical opening, so bleeding or abnormal blood flow can be controlled. Revenue is measured at the point of device sale in the covered geographies.

Scope exclusions: We exclude procedure fees, physician services, and stand alone diagnostic imaging that may happen before or after occlusion procedures.

Segmentation Overview

- By Product

- Occlusion Removal Devices

- Coil Retrievers

- Stent Retrievers

- Other Removal Devices

- Embolization Devices

- Support Devices

- Occlusion Removal Devices

- By Material

- Nitinol

- Platinum

- Bio-resorbable Polymers

- By Application

- Peripheral Vascular Disease

- Neurology

- Oncology

- Urology

- Other Applications

- By Disease Pathology

- Ischemic Stroke

- Cerebral Aneurysm

- Peripheral Arterial Occlusion

- Tumor Embolization

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to map the demand pool and keep assumptions realistic before we started the model build. We reviewed public sources such as the US FDA device databases and safety communications, CDC health statistics, WHO Global Health Observatory indicators, and OECD health expenditure and procedure related series where available.

To make sure the model reflects how this market is actually used, we also checked peer reviewed clinical literature (such as trials and meta analyses on embolization and occlusion procedures), selected customs and trade statistics where they help explain device flow, and company filings and investor decks for product mix commentary. A paid company financials and intelligence subscription was used selectively to standardize revenue baselines and ownership changes. This list is illustrative, and many other public sources were also used for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary conversations were run with clinicians involved in interventional cardiology, neurointervention, and peripheral procedures, plus procurement staff and distributor channel contacts. We used those inputs to confirm adoption patterns, typical usage per case, and price corridors by region, then rechecked any weak secondary datapoints before the final model set.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 35% | EMEA: 37% |

| Smaller Players: 20% | Managers: 53% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where procedure demand and treated cohorts are reconstructed using indicators tied to occlusion use, and then converted into device value using realistic pricing logic. For checks, we also run selective bottom-up approximations, such as sampled average selling price multiplied by expected unit volumes for key device groups, and channel feedback on mix shifts, and then totals are adjusted when gaps are explained.

Key model inputs include interventional procedure volumes by major indication (for example stroke and aneurysm related neuro cases, peripheral embolization cases, and structural heart closures), typical devices used per case, shifts toward minimally invasive care settings, and regional pricing corridors for materials like nitinol and platinum based constructs. We also track approval and safety signals that can change utilization, along with hospital versus ambulatory site of care mix since it impacts purchasing behavior. Forecasting is mainly done using scenario analysis, where procedure growth and adoption rates are flexed around clinical guidance and capacity constraints, and the chosen path is aligned to the consensus we heard from experts. When country level case data is thin, we use proxy indicators like population age bands and disease prevalence, and then we apply conservative penetration assumptions until stronger validation is available.

Data Validation & Update Cycle

Outputs are validated by comparing modeled revenue against independent signals, such as procedure trend direction, device price ranges, and reported regional growth narratives from public sources. Any sharp step changes are flagged, worked back to input assumptions, and then reviewed again before sign off.

The model and write up go through multiple analyst checks, and follow up calls are triggered when a large variance shows up across regions, device groups, or implied pricing. Reports are refreshed annually, and interim updates are made when material events occur, such as major approvals, safety notices, or policy changes that can move volumes. Before delivery, we complete a fresh review pass so the final numbers reflect the most current information available.

Mordor Intelligence's Occlusion Devices Market Estimate Compared With Other Published Estimates

Published market numbers can look far apart even when they are talking about similar devices, because each study chooses its own inclusion list, base year, and pricing method. Differences also come from how procedure volumes are inferred when country level reporting is not consistent.

The main gap comes from whether tubal and gastrointestinal occlusion products are counted alongside embolization and vascular occlusion devices. Mordor Intelligence treats the scope around interventional occlusion and embolization use cases and avoids mixing adjacent contraceptive or broader GI device categories into the total. Variance can also be driven by how average selling prices are carried forward, whether currency is normalized to a single conversion point, and how often assumptions are refreshed after new approvals or safety updates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.46 B (2025) | |

| Industry Publisher A | USD 4.00 B (2024) | Uses an earlier base year and includes tubal occlusion within product scope, which can lift totals even when interventional procedure volumes are similar. |

| Global Publisher B | USD 6.44 B (2025) | Applies a broader product perimeter that bundles cardiac, vascular, and GI occlusion devices together, and the higher total is also sensitive to faster ASP progression assumptions. |

Looking across the table, the spread is mostly explained by what gets counted as an occlusion device market and how pricing is carried through the forecast years. Our approach stays traceable to procedure linked demand indicators, practical usage per case, and region level price corridors, which makes the final number easier to reproduce and challenge during decision making.

Key Questions Answered in the Report

What is the current size of the occlusion devices market?

The occlusion devices market size is USD 3.68 billion in 2026 and is projected to reach USD 4.97 billion by 2031 at a 6.20% CAGR.

Which product segment leads the market?

Occlusion removal devices lead with 42.10% revenue share in 2025, driven by their role in emergency stroke interventions.

Why are Ambulatory Surgical Centers important for future growth?

CMS reimbursement expansions make ASCs cost-effective venues for endovascular procedures, supporting a 10.63% CAGR for this end-user segment through 2031.

Which region is growing the fastest?

Asia-Pacific records a 12.41% CAGR, propelled by rapid healthcare infrastructure development and rising stroke prevalence.

What material innovation is shaping product development?

Bio-resorbable polymers, growing at 11.20% CAGR, address concerns over permanent implants and open new therapeutic opportunities.

How is artificial intelligence influencing occlusion device procedures?

FDA-guided AI integration improves placement accuracy by up to 20% and shortens procedure times, giving early adopters a competitive edge.

Page last updated on: