India Medical Devices Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

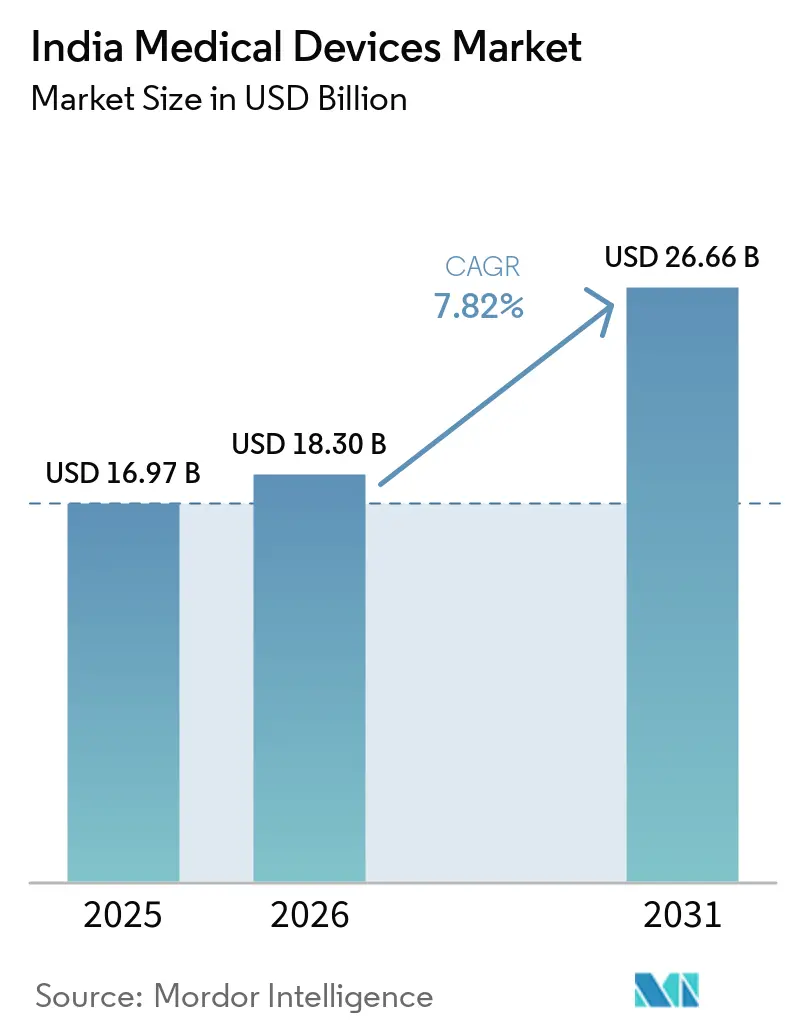

| Base Year Market Size (2025) | USD 16.97 Billion |

| Market Size (2026) | USD 18.30 Billion |

| Market Size (2031) | USD 26.66 Billion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Medical Devices Market Analysis by Mordor Intelligence

India Medical Devices Market size in 2026 is estimated at USD 18.30 billion, growing from 2025 value of USD 16.97 billion with projections showing USD 26.66 billion, growing at 7.82% CAGR over 2026-2031.

Rising chronic-disease prevalence, government production incentives, and rapid digital-health adoption are shifting the sector from a heavy reliance on imports toward an integrated domestic manufacturing base. Twenty-two greenfield plants commissioned under the Production-Linked Incentive (PLI) program have already generated INR 12,344.37 crore (USD 1.48 billion) in sales and INR 5,869.36 crore (USD 703 million) in exports, demonstrating the early success of localization mandates. Remote-patient monitoring, wearable glucose sensors, and AI-enabled imaging are expanding hospital and clinic technology budgets, while price ceilings on stents and implants are pushing manufacturers toward volume-led tier-2 and tier-3 strategies. Competitive intensity is rising as multinationals accelerate technology transfer and domestic firms leverage cost-engineering advantages, yet after-sales service gaps in smaller cities present an untapped opportunity for regional distributors.

Key Report Takeaways

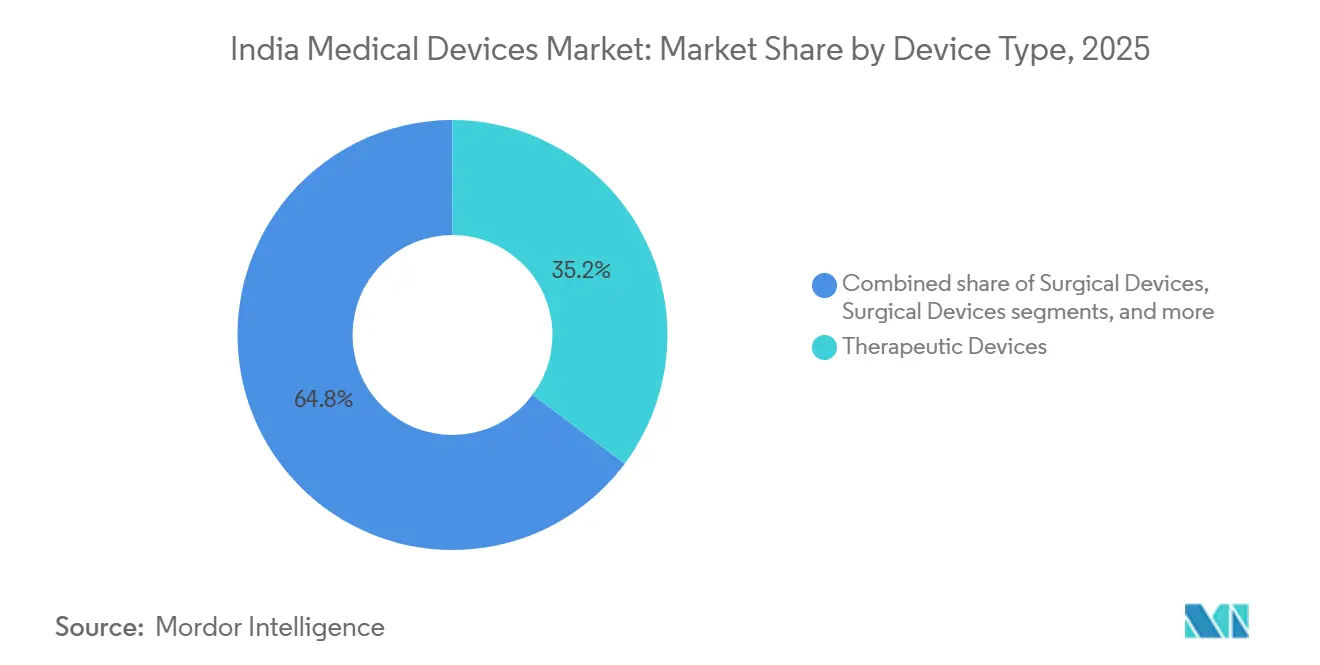

- By device type, therapeutic devices led with 35.21% revenue share in 2025, while monitoring devices are anticipated to post the fastest 8.54% CAGR through 2031.

- By technology platform, conventional electro-mechanical equipment and disposables commanded 42.32% of 2025 sales, whereas augmented/virtual-reality solutions are forecast to grow at an 8.77% CAGR during 2026-2031.

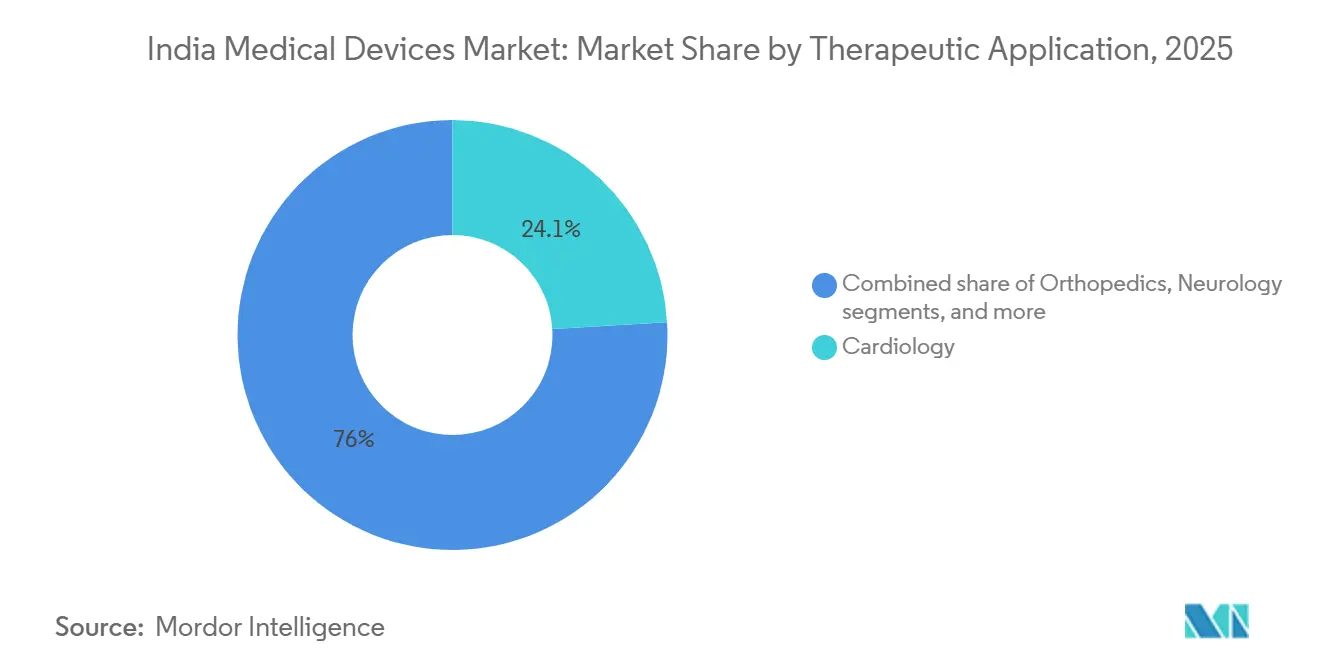

- By therapeutic application, cardiology captured 24.05% share in 2025; neurology is expected to expand at a 9.22% CAGR to 2031.

- By end-user, hospitals accounted for 65.43% of 2025 demand, while clinics are projected to register a 9.43% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Burden of Non-Communicable Diseases | +1.8% | Urban metros, tier-1 cities | Long term (≥ 4 years) |

| Government Incentives for Domestic Manufacturing | +1.5% | Tamil Nadu, Karnataka, Gujarat | Medium term (2-4 years) |

| Expansion of Healthcare Infrastructure and Insurance Coverage | +1.3% | Tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Digital Health Transformation and Telemedicine Adoption | +1.2% | Rural and remote areas | Short term (≤ 2 years) |

| Rising Medical Tourism and Demand for High-End Procedures | +0.7% | Delhi NCR, Chennai, Mumbai, Bengaluru | Medium term (2-4 years) |

| Increasing Penetration of Affordable Point-of-Care Diagnostics | +0.9% | Tier-2, tier-3, rural markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Burden of Non-Communicable Diseases

ICMR-INDIAB recorded 101.3 million diabetics, 315.5 million hypertensives, and 254.2 million people with obesity in 2024, fueling sustained demand for glucose monitors, blood-pressure cuffs, insulin pumps, and dialysis machines[1]Indian Council of Medical Research, “ICMR-INDIAB Study Highlights NCD Burden,” icmr.gov.in. Chronic kidney disease has pushed more than 300,000 patients onto maintenance dialysis, spurring investments in continuous ambulatory peritoneal dialysis systems. Cardiovascular complications are driving demand for implantable devices, yet stent price caps of INR 27,890 (USD 334) have narrowed margins. Manufacturers are therefore pursuing volume growth in tier-2 and tier-3 centers with affordable product lines. Continuous glucose monitors are gaining urban traction, but rural uptake hinges on reimbursement pathways and point-of-care infrastructure.

Government Incentives for Domestic Manufacturing

The PLI scheme earmarked INR 3,420 crore (USD 410 million) for 55 high-end devices, offering a 5% incentive on incremental sales for four years[2]Press Information Bureau, “Ayushman Bharat Digital Mission Milestones,” pib.gov.in. By September 2025, 22 greenfield projects had begun production, yet critical components like X-ray tubes and detectors remain imported, limiting value addition to 40-50%. Large players such as GE Healthcare and Siemens Healthineers have localized scanner assembly; smaller innovators struggle to absorb upfront capex. Backward integration into sensors and medical-grade polymers will require multi-year R&D and collaboration with the electronics clusters in Gujarat and Tamil Nadu.

Expansion of Healthcare Infrastructure and Insurance Coverage

The Pradhan Mantri Ayushman Bharat Health Infrastructure Mission invested INR 64,180 crore (USD 7.7 billion) between 2021 and 2026, establishing 175,338 Ayushman Arogya Mandirs and equipping 1,558 dialysis centers with 10,824 machines. Ayushman Bharat beneficiary cards exceeded 420 million, saving households INR 1.52 lakh crore (USD 18.2 billion) in out-of-pocket costs. Portable ultrasound, point-of-care analyzers, and telemedicine kiosks are now required across primary centers. However, coverage gaps for PET-CT and genetic testing limit advanced-diagnostic adoption in public hospitals, prompting device makers to maintain dual product lines for public and private sectors.

Digital Health Transformation and Telemedicine Adoption

The Ayushman Bharat Digital Mission has issued 799.1 million ABHA IDs, linked 671.9 million health records, and onboarded 418,000 facilities as of January 2025. Government telehealth platform eSanjeevani delivered 356 million consultations, highlighting demand for connected glucometers, Wi-Fi pulse oximeters, and smartphone ECG patches. Qure.ai’s AI chest-X-ray tool cuts radiology turnaround by up to 40% in Apollo and Fortis hospitals. Niramai’s thermal breast-screening system provides radiation-free diagnostics in tier-2 cities. HL7-FHIR interoperability standards are forcing device vendors to embed APIs and cloud connectivity, favoring software-centric players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory and Compliance Requirements | -0.8% | Nation-wide SMEs | Medium term (2-4 years) |

| Price Controls and Reimbursement Limitations | -0.6% | High-volume stent, implant segments | Long term (≥ 4 years) |

| Supply-Chain Dependence on Imported Components | -0.5% | Forex-sensitive inputs | Short term (≤ 2 years) |

| Fragmented After-Sales Service and Maintenance Ecosystem | -0.3% | Tier-3 cities, rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Compliance Requirements

The Medical Device Rules 2017 mandate ISO 13485-aligned QMS certification costing INR 5 lakh to INR 50 lakh depending on risk class[3]Central Drugs Standard Control Organisation, “Medical Device Rules 2017 Overview,” cdsco.gov.in. Post-market surveillance requires adverse-event reporting within 30 days, adding administrative overhead. Start-ups face 12-18 month approval cycles for Class C and D devices, while absence of FDA or EMA mutual recognition obliges duplicate trials. Ambiguity around software-as-medical-device classification slows AI solution launches.

Price Controls and Reimbursement Limitations

NPPA price caps on stents and knee implants have squeezed gross margins by up to 70%, prompting portfolio rationalization by Abbott, Boston Scientific, and Medtronic. Ayushman Bharat still excludes PET-CT, genetic panels, and liquid biopsies from reimbursement, constraining uptake in public hospitals. Rising input costs versus regulated prices challenge domestic manufacturers to sustain R&D investment, creating a two-tier ecosystem of stripped-down public-sector models and premium private-pay devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Devices Lead, Monitoring Surges

Therapeutic devices controlled 35.21% of the India medical devices market share in 2025, supported by large installed bases of dialysis machines, ventilators, and infusion pumps. Monitoring devices will post the fastest 8.54% CAGR through 2031 as wearable ECG patches and continuous glucose monitors integrate with digital health records. Diagnostic imaging, already benefiting from PLI-backed scanner assembly, is expanding mid-tier MRI and CT systems to tier-2 hospitals, while robotic surgery adoption is growing in medical-tourism hubs.

IVD demand surged post-pandemic as Truenat platforms spread into primary clinics, and assistive aids remain underpenetrated due to limited insurance. Dental devices are gaining urban traction through cosmetic procedures. Collectively, the segment mix is tilting toward chronic-disease management as the India medical devices market size for monitoring and home-care solutions expands alongside aging demographics and lifestyle disorders.

By Technology Platform: Conventional Dominates, AR/VR Accelerates

Conventional electromechanical equipment and disposables accounted for 42.32% of 2025 revenue, underscoring the enduring installed base in public and private hospitals. Augmented- and virtual-reality tools for surgical simulation are advancing at 8.77% yearly, lowering complication risk and training costs. Wearable monitors and telehealth peripherals align with ABHA data standards, enabling continuous vital capture.

Robotic surgery platforms, led by da Vinci and SSI Mantra, are expanding into urology and gynecology, though capital costs limit wider adoption. 3D-printed surgical guides in orthopedic centers deliver patient-specific accuracy. AI diagnostic algorithms, such as Qure.ai’s imaging suite, are transforming radiology workflows. Together these advances position connected platforms to command a larger slice of the India medical devices market size by 2031.

By Therapeutic Application: Cardiology Anchors, Neurology Sprints

Cardiology contributed 24.05% of therapeutic revenue in 2025, underpinned by India’s cost-advantaged bypass and angioplasty services that attract overseas patients. Neurology will grow 9.22% annually, powered by new stroke units in tier-2 hospitals equipped with CT angiography and thrombectomy systems. Orthopedic implants retain scale, although implant price ceilings limit profitability.

Ophthalmology is expanding through cataract volumes, while oncology procurement focuses on linear accelerators and brachytherapy. The India medical devices market share for chronic-care applications is expected to rise as non-communicable diseases exceed 65% of mortality, steering investments toward long-term monitoring and home-care devices.

By End-User: Hospitals Dominate, Clinics Surge

Hospitals captured 65.43% of the 2025 demand due to tertiary expansions and Ayushman Bharat empanelment of 33,000 facilities. Clinics are projected to grow at 9.43% CAGR, leveraging specialty chains to provide high-margin outpatient services in tier-2 and tier-3 cities. Primary-care Ayushman Arogya Mandirs create steady orders for portable ultrasounds and automated BP monitors, while home-care platforms accelerate wearable adoption.

Diagnostic laboratories are automating analyzers to meet test volumes for insured populations, and ambulatory surgery centers are investing in portable anesthesia and minimally invasive kits. Rehabilitation facilities are expanding in metros for post-stroke and trauma care. This diversification underlines how distributed care settings are reshaping procurement priorities within the India medical devices market.

Competitive Landscape

Multinationals—GE Healthcare, Siemens Healthineers, Philips, Medtronic, and Abbott—collectively hold about 40-45% of revenue through technology leadership and hospital partnerships. Domestic firms—Meril, Trivitron, BPL Medical, and Molbio Diagnostics—are scaling rapidly via PLI incentives and lower cost structures. Price ceilings on stents and implants have triggered stripped-down SKUs for public procurement, while premium private-pay segments retain full-featured models.

Software-centric disruptors such as Qure.ai and Niramai monetize AI services through subscription models, thereby avoiding high hardware capex. SSI Mantra’s robot illustrates indigenous innovation in complex segments at 40% lower price points. Strategic alliances—for example, GE Healthcare with IIT-Madras on algorithms and Siemens with Apollo on remote diagnostics—signal a convergence of hardware and software capabilities. The India medical devices market is thus bifurcating into premium and value tiers with distinct product portfolios and go-to-market models.

India Medical Devices Industry Leaders

Abbott Laboratories

GE Healthcare

Koninklijke Philips N.V.

Medtronic plc

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Shukra Pharmaceuticals received a Letter of Intent from the Yamuna Expressway Industrial Development Authority (YEIDA) to set up an INR 587 Cr medical devices manufacturing facility in Uttar Pradesh, for a 10-acre plot in the Medical Devices Park under the Invest UP initiative.

- September 2025: Tata Elxsi, one of the global leaders in design and technology services, announced the inauguration of the ‘Bayer Development Centre in Radiology’ at its Pune, India, facility. The centre is designed to co-develop with Bayer, a leader in key areas of Radiology, advanced radiology devices, and technology that enable early and accurate diagnosis and treatment of critical illnesses, supporting Bayer’s global mission to bring innovative, safe, and compliant solutions to patients and clinical staff worldwide.

- October 2025: Medtronic launched two advanced electrosurgical devices the Valleylab FT10 Electrosurgical Generator (VLFT10FXGEN) and the Valleylab Vessel Sealing Generator (VLFT10LSGEN) in India.

India Medical Devices Market Report Scope

According to the Scope, a medical device is a type of instrument, apparatus, appliance, machine, or implant used to diagnose, treat, monitor, or prevent diseases.

The medical devices market in India is segmented by type of device and end-users. By type of device, the market is segmented into respiratory devices, cardiology devices, orthopaedic devices, diagnostic imaging devices, endoscopy devices, ophthalmology devices, and other type of devices. Other type of devices include life support devices and dental devices, among others. By end-users, the market is segmented into hospitals, diagnostic centres, and other end users. Other end-users include clinics and ambulatory centres and home healthcare settings, among others. The report offers the value (in USD million) for the above segments.

| Diagnostic Imaging Devices |

| Therapeutic Devices |

| Surgical Devices |

| Monitoring Devices |

| In-Vitro Diagnostics (IVD) |

| Assistive & Mobility Aids |

| Dental Devices |

| Other Devices |

| Conventional Electro-Mechanical & Disposables |

| Wearable & Remote Monitoring |

| Telehealth & mHealth |

| Robotic Surgery |

| 3D Printing |

| Augmented / Virtual Reality (AR / VR) |

| Nanotechnology |

| Other Technology Platforms |

| Cardiology |

| Orthopedics |

| Neurology |

| Ophthalmology |

| General Surgery |

| Other Therapeutic Applications |

| Hospitals |

| Clinics |

| Home-Care Settings |

| Other End-Users |

| By Device Type | Diagnostic Imaging Devices |

| Therapeutic Devices | |

| Surgical Devices | |

| Monitoring Devices | |

| In-Vitro Diagnostics (IVD) | |

| Assistive & Mobility Aids | |

| Dental Devices | |

| Other Devices | |

| By Technology Platform | Conventional Electro-Mechanical & Disposables |

| Wearable & Remote Monitoring | |

| Telehealth & mHealth | |

| Robotic Surgery | |

| 3D Printing | |

| Augmented / Virtual Reality (AR / VR) | |

| Nanotechnology | |

| Other Technology Platforms | |

| By Therapeutic Application | Cardiology |

| Orthopedics | |

| Neurology | |

| Ophthalmology | |

| General Surgery | |

| Other Therapeutic Applications | |

| By End-User | Hospitals |

| Clinics | |

| Home-Care Settings | |

| Other End-Users |

Key Questions Answered in the Report

How large is the India medical devices market in 2026?

It was valued at USD 18.30 billion in 2026 and is projected to reach USD 26.66 billion by 2031.

Which device category is growing fastest?

Monitoring devices, including wearable ECG and glucose sensors, are advancing at an 8.54% CAGR through 2031.

What share do hospitals hold in overall demand?

Hospitals contributed 65.43% of 2025 revenue, reflecting their dominance in high-value equipment purchases.

How is the PLI scheme impacting local manufacturing?

Twenty-two greenfield plants have begun production, generating USD 1.48 billion in cumulative sales and accelerating component localization.

Which therapeutic area leads the market?

Cardiology remains the largest application with 24.05% share, bolstered by inbound medical tourists seeking cost-effective cardiac surgery.

What challenges do small manufacturers face?

High regulatory-compliance costs and stringent post-market surveillance requirements disproportionately strain SMEs.

Page last updated on: