HIV Self-test Kits Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

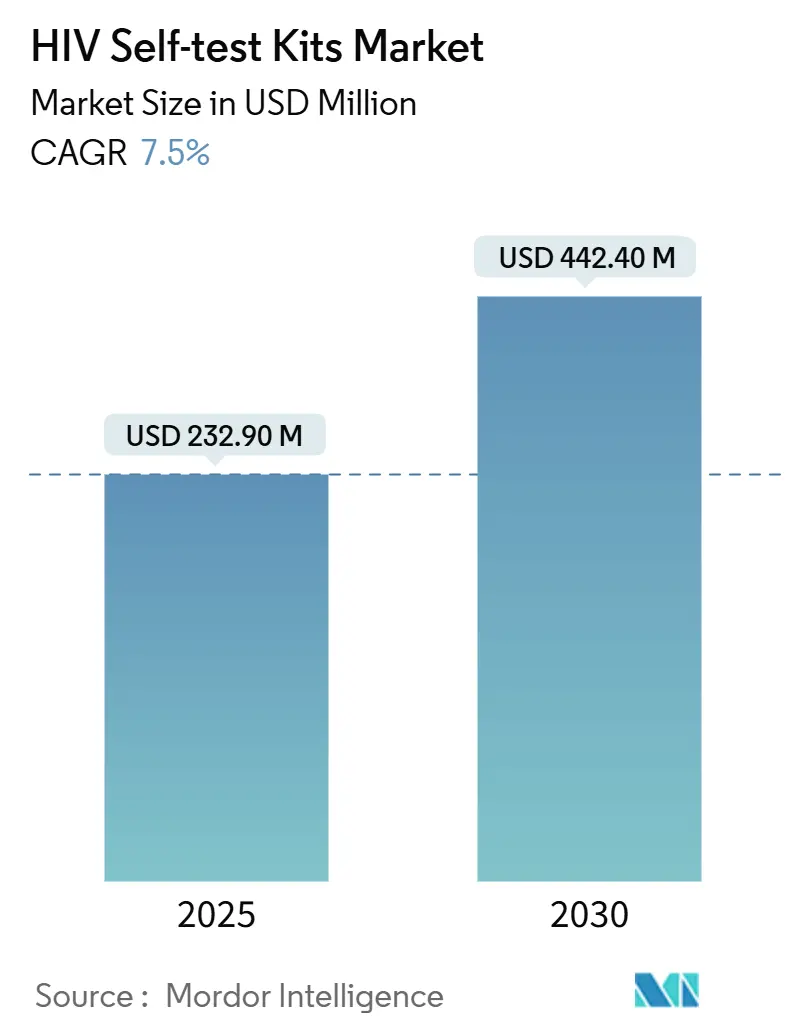

| Market Size (2025) | USD 232.90 Million |

| Market Size (2030) | USD 442.40 Million |

| Growth Rate (2025 - 2030) | 7.50% CAGR |

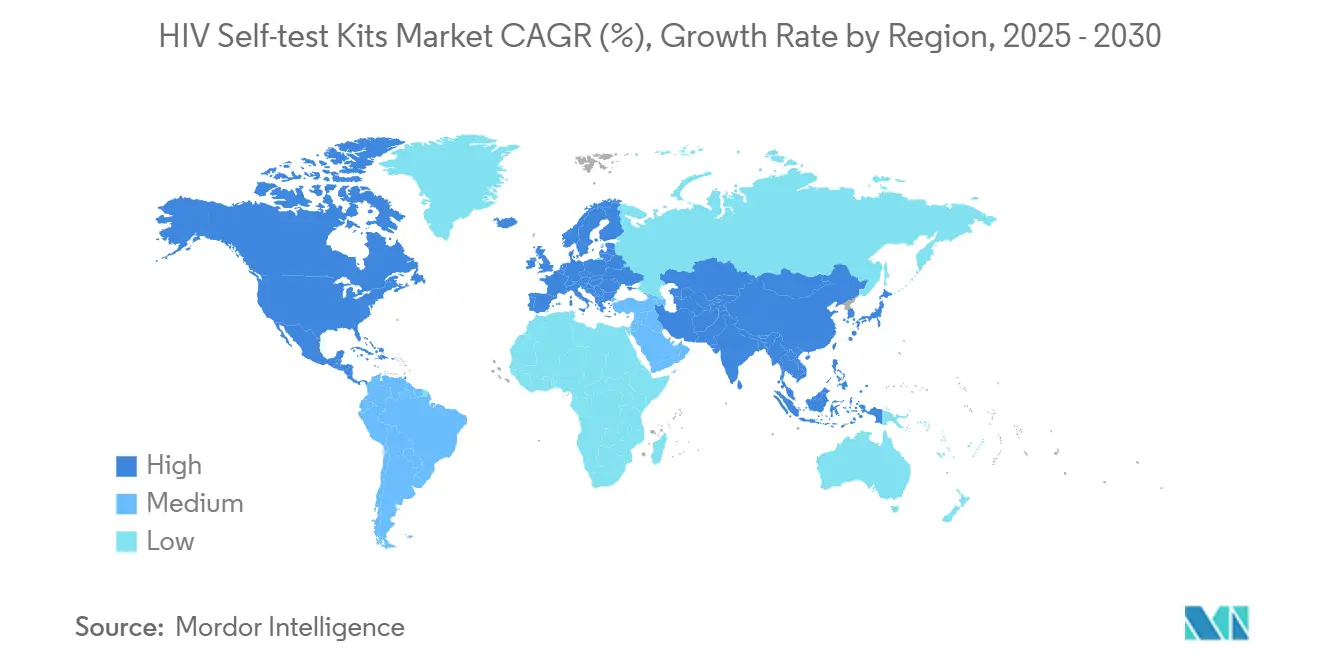

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HIV Self-test Kits Market Analysis by Mordor Intelligence

The HIV self-test kits market size is USD 232.9 million in 2025 and is projected to reach USD 442.4 million by 2030 at a 7.50% CAGR. Demand consolidation follows a shift from facility-based testing to consumer-controlled diagnostics as more platforms secure WHO prequalification and procurement agencies formalize guidelines for self-testing. Retail pharmacies and e-commerce distribution have broadened access, introduced discreet delivery, and supported subscription replenishment that fits quarterly testing schedules. Program sponsors are embedding self-testing within PrEP pathways, which improves retention and stabilizes recurring consumption patterns for the HIV self-test kits market. Reader-enabled devices and molecular formats are emerging to address early-infection detection and to integrate results into digital care systems and surveillance workflows

Key Report Takeaways

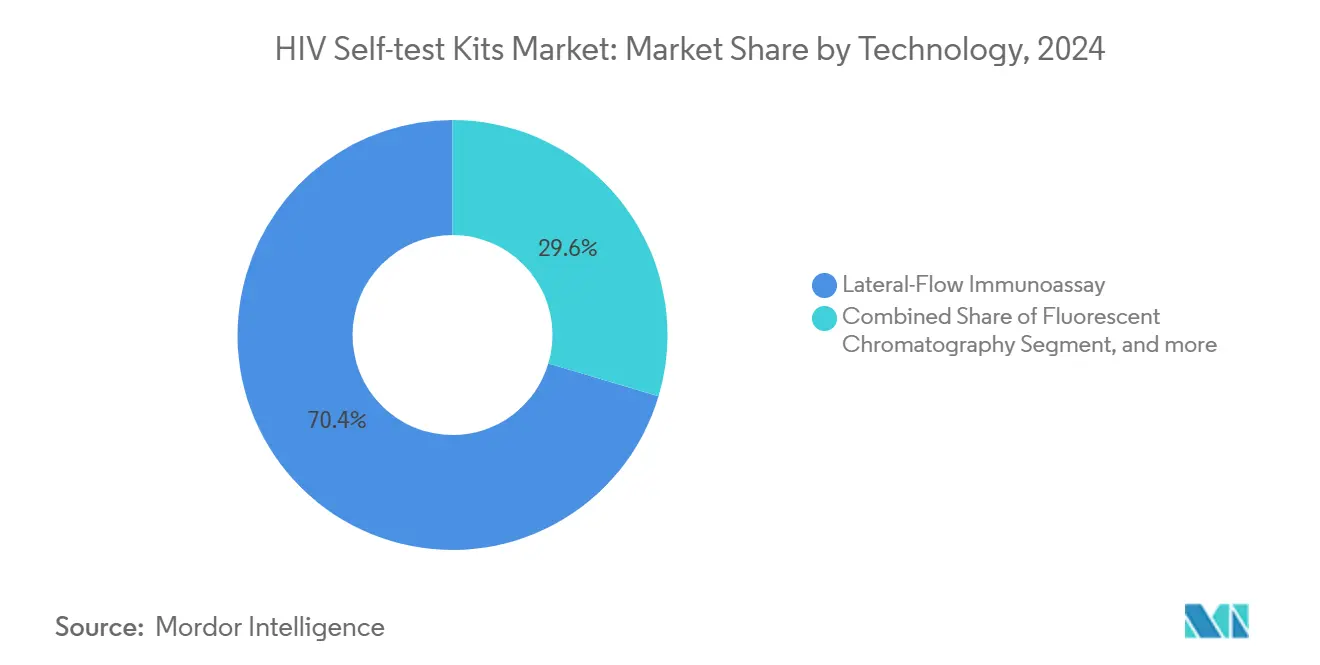

- By technology, lateral flow immunoassay led with 70.4% revenue share in 2024. Molecular and reader-enabled home tests are projected to grow at an 8.95% CAGR through 2030.

- By sample type, blood-based fingerstick devices held 55.7% share in 2024. Oral-fluid tests are forecast to expand at a 9.43% CAGR.

- By test generation, second-generation tests accounted for 58.8% share in 2024. Third-generation devices are set to grow at an 8.43% CAGR through 2030.

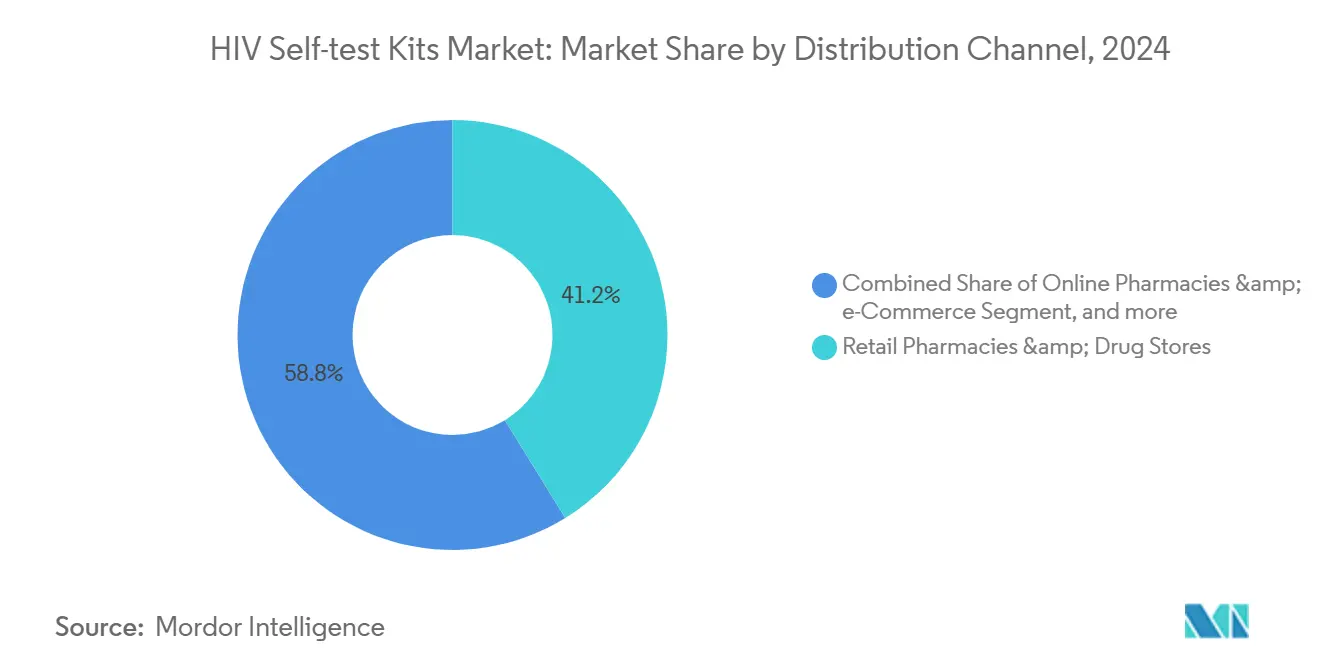

- By distribution channel, retail pharmacies and drug stores accounted for 41.2% of 2024 volume. Online pharmacies and e-commerce platforms are expected to grow at a 9.87% CAGR.

- By application, point-of-care testing held 57.7% application share in 2024. Home testing is projected to grow at an 8.78% CAGR through 2030.

- By geography, North America captured 42.5% of 2024 revenue. Asia-Pacific is projected to post the fastest regional growth at an 8.54% CAGR through 2030.

Global HIV Self-test Kits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led national HIV screening initiatives | +1.80% | Global; strongest in North America & Europe | Medium term (2–4 years) |

| Rising donor funding and global health grants for self-testing procurement | +1.20% | Sub-Saharan Africa, Asia Pacific | Long term (≥ 4 years) |

| Technological advances in rapid point-of-care immunoassays | +1.50% | Global | Short term (≤ 2 years) |

| Expanding retail & pharmacy-based distribution networks | +0.90% | North America, Europe, Asia Pacific | Medium term (2–4 years) |

| Growing public awareness campaigns on early HIV diagnosis | +0.80% | Global | Long term (≥ 4 years) |

| Integration of HIV self-testing into digital health ecosystems | +1.30% | Early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Led National HIV Screening Initiatives

Large-scale public programs are removing structural barriers to testing. England’s expansion of emergency-department opt-out screening completed almost 2 million tests in 24 months and found that 73% of those screened had never been tested before. The CDC’s Together TakeMeHome program distributed 440,000 self-tests in its first year—24.1% went to first-time testers—showing how centralized procurement and mail-order logistics can scale nationwide reach.[1]Centers for Disease Control and Prevention, “Findings from the First Year of a Federally Funded, Direct-to-Consumer HIV Self-Test Distribution Program,” cdc.gov Scotland’s 2023-26 elimination plan embeds self-testing within its stigma-reduction strategy, while updated WHO guidelines endorse self-testing to start or maintain PrEP, driving regulatory harmonization worldwide.[2]World Health Organization, “Countries Take Up New WHO Recommendations on Self-Testing for PrEP and PEP,” who.int These initiatives anchor predictable volume demand and hasten reimbursement discussions. Over the medium term, mandatory screening targets are expected to sustain kit uptake even in budget-constrained settings.

Rising Donor Funding & Global Health Grants for Self-Testing Procurement

PEPFAR’s commitment to source 15 million tests from African factories by 2025 signals a pivot to regional manufacturing that lowers freight costs and shortens lead times. The CDC Foundation’s USD 5 million injection into 53 community organizations demonstrates the catalytic effect of small grants on last-mile distribution. Unitaid’s regional manufacturing facility further diversifies supply and reduces currency risk for import-dependent countries. Yet, the Clinton Health Access Initiative warns of a USD 9.5 billion funding gap by 2025, creating pressure for blended-finance mechanisms. Sustained donor inflows remain pivotal to absorbing price premiums of molecular kits and ensuring stockpiles for humanitarian crises.

Technological Advances in Rapid Point-of-Care Immunoassays

Northwestern University’s nanomechanical platform delivers results in minutes and detects antigen in the acute phase, mitigating the traditional antibody-test window period. NIH-funded projects aim to commercialize self-tests priced below USD 5 with viral-rebound monitoring capability, promising parity with laboratory PCR sensitivity. Patterned dried-plasma spot cards cut pre-analytic errors linked to hematocrit variability, and RT-PCR lateral-flow hybrids reach 82.29 RNA copies/mL detection limits—comparable to high-throughput NAT systems. Fast-evolving miniaturization is expected to compress kit size and shipping weight, unlocking new direct-to-consumer channels.

Expanding Retail & Pharmacy-Based Distribution Networks

Walgreens partnered with KFF’s Greater Than HIV to deliver free testing at 550 stores, illustrating the potential of big-box chains to normalize testing in everyday settings. Boots’ private-label kit launch extends the model to over-the-counter retail in the U.K. Digital vending pilots in Brighton saunas give hard-to-reach groups discreet access at hours when clinics are closed. Kenya’s ePrEP pilot merges online pharmacies with teleconsultations for PrEP eligibility, a template likely to spread to other mobile-savvy markets. As pharmacies integrate telehealth kiosks, linkage-to-care gaps are expected to narrow, boosting repeat purchase rates and prescription conversions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain disruptions & limited manufacturing capacity in emerging regions | –1.1% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2–4 years) |

| Variable reimbursement policies & lack of insurance coverage for self-test kits | –0.8% | Global; acute in middle-income countries | Long term (≥ 4 years) |

| Socio-cultural stigma limiting self-test adoption in conservative communities | –0.9% | Middle East & North Africa, conservative locales worldwide | Long term (≥ 4 years) |

| Inadequate post-test linkage-to-care infrastructure | –0.7% | Rural and resource-limited settings globally | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Disruptions & Limited Manufacturing Capacity in Emerging Regions

The 2020-21 COVID-19 period revealed how import dependency can paralyze HIV test availability; freight bottlenecks caused stock-outs lasting several months in parts of East Africa. While Senegal’s diaTROPIX and Nigeria’s Codix Bio facilities add regional capacity, scalability hurdles persist, as ISO-13485 certification and WHO prequalification require years of data and capital outlays. Europe’s IVDR rule reclassifies HIV tests as high-risk, squeezing smaller manufacturers that lack the budget for notified-body audits, potentially contracting global kit diversity until 2027. These factors could widen price gaps between molecular and lateral-flow formats, straining donor budgets.

Variable Reimbursement Policies & Lack of Insurance Coverage for Self-Test Kits

U.S. Affordable Care Act preventive-service mandates do not uniformly extend to self-testing, forcing many users to pay out-of-pocket despite Medicare adding HIV/AIDS to chronic-disease management programs in 2025.[3]Federal Register, “Medicare Program; Changes to the Medicare Advantage and the Medicare Prescription Drug Benefit Program,” federalregister.gov Middle-income economies face steeper barriers; Kenyan purchasers in an online PrEP study were willing to pay USD 11.77 per month, a figure exceeding local daily-wage earnings. Western-Kenya cost models reveal non-kit expenses—like community mobilizers—represent 30% of total distribution budgets, costs rarely covered by insurance. Inconsistent payment pathways undercut retailer incentives to stock higher-margin molecular kits, slowing technology diffusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Molecular Convergence Challenges Lateral-flow Dominance

Lateral flow immunoassay technology held 70.4% share in 2024, anchored by low production cost, short time to result, and ambient stability that supports last-mile distribution. These devices detect HIV-1 and HIV-2 antibodies with simple visual lines and do not require electricity or a reader, which suits donor-funded mass distribution. Molecular and reader-enabled home tests are projected to grow at an 8.95% CAGR through 2030 as buyers seek higher sensitivity and stronger digital integration. New molecular formats in late-stage development rely on isothermal amplification or CRISPR-based detection to reduce the diagnostic window to fewer than 10 days. Flow-through platforms that deliver one-minute results also gained a foothold but face pricing headwinds in donor channels. The HIV self-test kits market continues to favor designs that balance accuracy, ease of use, and documentation.

LFA incumbency is tested by the need to close early-infection gaps and to deliver auditable, time-stamped outputs that integrate into surveillance systems. Reader-enabled designs address misinterpretation errors and improve consistency in unassisted environments. Connectivity reduces reporting friction for public health teams and for PrEP programs that track quarterly testing. These preferences are visible in procurement, where tenders increasingly ask for digital features and validated performance in early infection. Manufacturers are adapting lines accordingly, while cost parity remains the threshold for mainstream adoption in the HIV self-test kits market. LFA will endure in price-sensitive settings while molecular and connected formats scale in regulated retail and managed care channels.

By Sample Type: Oral-fluid Tests Gain Despite Blood-based Incumbency

Blood-based fingerstick devices maintained 55.7% share in 2024, supported by WHO prequalification for multiple platforms and training familiarity among programs with capillary sampling. Fingerstick tests yield high sensitivity in field conditions and operate reliably across wide temperature ranges. Oral-fluid tests are set to expand at a 9.43% CAGR through 2030 as first-time testers and adolescents prefer noninvasive collection. As of 2024, OraQuick remained the sole WHO-prequalified oral-fluid self-test, which shaped donor tenders and supported premium pricing for saliva-based kits. Saliva tests still trail blood in sensitivity by a small margin due to lower antibody titers and a longer window period. Urine-based self-tests stay limited given lower antibody concentrations and sensitivity shortfalls that face regulatory barriers.

The trajectory for saliva relies on second-generation assays that add p24 antigen detection to close the window gap. If validated, these platforms could match fingerstick performance while retaining noninvasive collection, which would widen adoption among hesitant users. That shift would also support integration with telehealth flows, since noninvasive samples reduce user errors tied to lancets and collection steps. The HIV self-test kits market is responsive to such usability gains when accuracy is maintained. Until then, fingerstick platforms will remain the default in acute risk settings, such as PrEP monitoring, where earlier detection is critical. Program design will likely segment users by risk and preference with inventory strategies that cover both modalities.

By Test Generation: Third-generation Gains Reflect Window-period Pressure

Second-generation tests accounted for 58.8% share in 2024 as they remained entrenched in donor lists and are simpler to manufacture. They use single-antigen coatings and yield results later in the serological timeline, which is adequate for routine screening but less aligned with acute risk monitoring. Third-generation devices are projected to grow at an 8.43% CAGR through 2030 as tender scoring and regulatory reviews prioritize earlier detection. Regulators in the United States and European Union increasingly favor higher sensitivity profiles for premarket authorization, which steers production toward dual-antigen, IgM-capable designs. WHO’s 2024 updates to prequalification criteria also reward shorter window periods in scoring. Fourth-generation self-tests that combine antibody and p24 antigen detection are moving toward commercialization and would place pressure on legacy formats once launched.

The generation shift brings price considerations for public buyers because third-generation wholesale prices are higher than second-generation equivalents. Donor budgets will need to reconcile performance gains with per-test caps that keep programs within target spend. Manufacturers can offset price gaps by including training, digital support, or logistics services to raise tender value without raising unit price. The HIV self-test kits market will likely show mixed generational supply within multi-year framework agreements as countries phase upgrades by region or risk group. Over time, performance-based procurement should accelerate the replacement of older formats. The pace of this transition will depend on regulatory clearance timing and the willingness of manufacturers to manage margins during the upgrade cycle.

By Distribution Channel: E-commerce Disrupts Pharmacy Incumbency

Retail pharmacies and drug stores held 41.2% of 2024 distribution volume due to foot traffic, pharmacist guidance, and insurance processing for eligible buyers. Major chains placed self-tests in sexual health aisles next to condoms and emergency contraception and normalized same-day purchase without stigma. Pharmacy settings also align with PrEP dispensing, which enables opportunistic add-ons during refills. Online pharmacies and e-commerce platforms are projected to grow at a 9.87% CAGR as privacy, always-on access, and subscription models attract new users. Amazon’s marketplace, specialty e-tailers, and integrated telehealth services combine kits with counseling and broader STI panels in a single checkout. These integrated offerings raise average order value and encourage adherence through automated quarterly shipments.

Hospitals and clinics accounted for a modest share through supervised testing, which remains common in antenatal care and TB co-screening programs. Public programs, NGOs, and community distribution contributed a large share of unit volume in donor-funded countries, with periodic spikes tied to disbursement cycles. E-commerce reduces distribution cost and supports discreet purchasing, which is a priority for many first-time testers. Pharmacy and digital channels often serve different buyer motivations and can be optimized together. The HIV self-test kits market will continue to shift toward digital-first replenishment as programs implement reminder flows and enrollment-based outreach. Broad channel coverage is now an operational requirement for suppliers that sell across both insured and donor-funded contexts.

By Application: Home Testing Ascends as Reimbursement Expands

Point-of-care testing held 57.7% of application share in 2024 and reflects supervised self-testing in clinics and mobile settings with on-site counseling and confirmatory pathways. Supervised models deliver higher linkage-to-care and furnish structured data to surveillance systems. Facility self-testing also reduces staff time per test compared with venipuncture-based rapid testing. Home testing is projected to grow at an 8.78% CAGR through 2030 as payers adopt policies that reimburse mailed kits and as digital support improves adherence. Medicaid programs in multiple U.S. states expanded coverage for mailed self-test kits in 2024, which lowered total cost of testing per completed case against clinic encounters. Private insurers are piloting value-based arrangements that tie payments to quarterly adherence and documented linkage.

Home use still faces gaps in confirmatory follow-through without built-in reminders, prepaid lab vouchers, or live counseling. Programs that add these features within connected platforms report better adherence and faster next-step initiation. As more plans adopt covered home testing, logistics partnerships and digital coaching will become standard features. The HIV self-test kits market benefits when home testing is positioned as part of a supported care pathway instead of a standalone product. Over the forecast, the mix of supervised and home use is likely to rebalance as coverage expands and as post-test support tools gain adoption. The rate of change will track funding policies and the availability of integrated telehealth services that handle reactive cases.

Geography Analysis

North America’s 38.6% revenue dominance in 2024 rests on large-scale public procurement and mature reimbursement pathways, exemplified by the Together TakeMeHome target of 1 million mail-order kits over five years. FDA’s 2024 approval of adolescent use for OraQuick widened the eligible user pool by about 4 million people aged 14–17, fueling incremental kit volumes. Canada’s multi-site evaluation found 94.1% of participants could correctly perform an oral-fluid test without assistance, reinforcing the region’s readiness to migrate diagnosis into homes. As Medicare integrates HIV self-testing into chronic-disease therapy management, retailer margins are expected to expand, supporting private-label launches.

Europe follows coordinated elimination roadmaps. The U.K. allocated GBP 1.5 million to supply 20,000 self-tests as part of a wider GBP 20 million opt-out expansion across 47 emergency departments. The EU’s IVDR transition encourages common quality benchmarks but may temporarily reduce kit diversity until notified-body queues clear. Digital vending pilots and pharmacy roll-outs in urban gay venues illustrate how micro-targeted distribution complements regional public-health strategy. However, uptake remains heterogeneous; Eastern and Southern Europe trail Northern nations on the 95-95-95 cascade, signaling untapped growth for value-priced lateral-flow kits.

Asia Pacific and the Middle East & Africa provide the highest growth runway. MEA’s 11.3% CAGR through 2030 reflects a 116% rise in new infections since 2010, demanding rapid scale-up of diagnostics. Africa’s first WHO-prequalified ARV producer, Universal Corporation Kenya, points to broader localization that could cut kit lead times to weeks. India’s STAR III pilot reported 88% of users would choose self-testing next time, revealing strong latent demand poised for e-commerce fulfillment. China’s online sales surpassed 5 million kits in 2020, and regulatory pathways now allow dual HIV/syphilis self-tests, indicating room for portfolio diversification. Japan’s 2024 data show rural diagnosis shortfalls, highlighting the critical role that self-testing can play in decentralized screening.

Competitive Landscape

The HIV self-test kits market is moderately fragmented, with the top five producers accounting for an estimated 62% of annual kit shipments in 2024. OraSure’s USD 56.8 million revenue and FDA adolescent label extension strengthened its lead in oral-fluid testing, while Abbott’s Panbio kit battles for blood-based share. Roche’s acquisition of LumiraDx’s point-of-care assets signals a move toward integrated molecular platforms that could cascade into at-home formats. Trinity Biotech leverages its TrinScreen product’s inclusion in national algorithms to punch above its scale, and SD Biosensor’s WHO technology-transfer license paves the way for emerging-market manufacturing.

Strategic playbooks center on three levers: adolescent labeling, molecular accuracy, and digital ecosystem integration. OraSure tied up with telehealth providers to offer immediate linkage-to-care video consults. Abbott pilots Bluetooth-enabled cartridges that upload anonymized results to surveillance dashboards, appealing to public-health buyers. New entrants such as Linear Diagnostics are fast-tracking five-minute Exponential Amplification assays backed by GBP 1 million seed funding, an example of venture capital flowing into ultra-rapid formats. Despite this churn, regulatory hurdles remain significant; IVDR conformity and FDA 510(k) pathways require multimillion-dollar clinical validation budgets, tempering the pace of new approvals.

Digital partnerships are equally decisive. Grindr’s clickable testing banners redirect users to free kit order pages, while Amazon’s “Buy With Prime” badge on select kits accelerates checkout. Retail-pharmacy private labels, including Boots and CVS, are expected to debut within two years, further commoditizing lateral-flow products. Price competition will intensify, but higher-margin molecular assays and companion-app subscriptions offer revenue defense. Overall, competitive intensity is set to rise as localized production trims logistics costs and governments add self-tests to essential medicines lists.

HIV Self-test Kits Industry Leaders

OraSure Technologies

Abbott Laboratories

bioLytical Laboratories

Atomo Diagnostics

Chembio Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Linear Diagnosti.s received GBP 1 million to advance a five-minute STI/HIV rapid test

- February 2025: FIND and Unitaid backed the launch of diaTROPIX, a regional diagnostics plant in Dakar, to boost African kit supply.

- February 2025: OraSure Technologies secured FDA approval to lower the minimum age for OraQuick HIV Self-Test to 14 years.

Global HIV Self-test Kits Market Report Scope

As per the scope of the report, HIV self-test kits are diagnostic tools that allow individuals to check their HIV status privately at home. They typically involve collecting a small blood or oral fluid sample and providing results within minutes. These kits enable early detection and promote confidential testing, increasing access to HIV testing services.

The HIV self-test kits market is segmented by Technology (Lateral Flow Immunoassay, Immunofiltration/Flow-Through, Fluorescent Chromatography, Nascent Molecular/Reader-enabled), Sample Type (Blood, Oral Fluid, Urine), Test Generation (2nd, 3rd, 4th), Distribution Channel (Retail Pharmacies & Drug Stores, Online Pharmacies & e-Commerce, Hospitals & Clinics, Public Program/NGO & Community), Application (Home Testing, Point-of-Care Testing, Facility-based Self-testing), and Geography (North America, Europe, APAC, Middle East and Africa). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Lateral Flow Immunoassay (LFA) |

| Immunofiltration / Flow-Through (e.g., INSTI) |

| Fluorescent Chromatography |

| Nascent molecular/reader-enabled home tests |

| Blood (fingerstick) |

| Oral Fluid |

| Urine |

| 2nd |

| 3rd |

| 4th |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies & e-Commerce |

| Hospitals & Clinics |

| Public Program / NGO & Community Distribution |

| Home Testing |

| Point-of-Care Testing |

| Facility-based self-testing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Lateral Flow Immunoassay (LFA) | |

| Immunofiltration / Flow-Through (e.g., INSTI) | ||

| Fluorescent Chromatography | ||

| Nascent molecular/reader-enabled home tests | ||

| By Sample Type | Blood (fingerstick) | |

| Oral Fluid | ||

| Urine | ||

| By Test Generation | 2nd | |

| 3rd | ||

| 4th | ||

| By Distribution Channel | Retail Pharmacies & Drug Stores | |

| Online Pharmacies & e-Commerce | ||

| Hospitals & Clinics | ||

| Public Program / NGO & Community Distribution | ||

| By Application | Home Testing | |

| Point-of-Care Testing | ||

| Facility-based self-testing | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the HIV self-testing kits market today?

The market generated USD 232.9 million in 2025 and is forecast to reach USD 442.4 million by 2030.

What CAGR is projected for self-testing kits through 2030?

Revenues are expected to expand at a 7.55% CAGR.

Which technology dominates current sales?

Lateral-flow immunoassays accounted for 70.4% of 2024 revenue.

Which distribution channel is growing fastest?

Online pharmacies are expanding at a 19.3% CAGR as privacy concerns steer users to mail-order kits.

Which region offers the highest growth potential?

The Middle East & Africa is projected to grow at 11.3% CAGR through 2030 due to rising infection rates and donor funding.

What age group just gained access to a U.S.-approved self-test?

In 2024, the FDA cleared the OraQuick kit for users as young as 14, widening adolescent coverage.

Page last updated on: