Healthcare Analytical Testing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

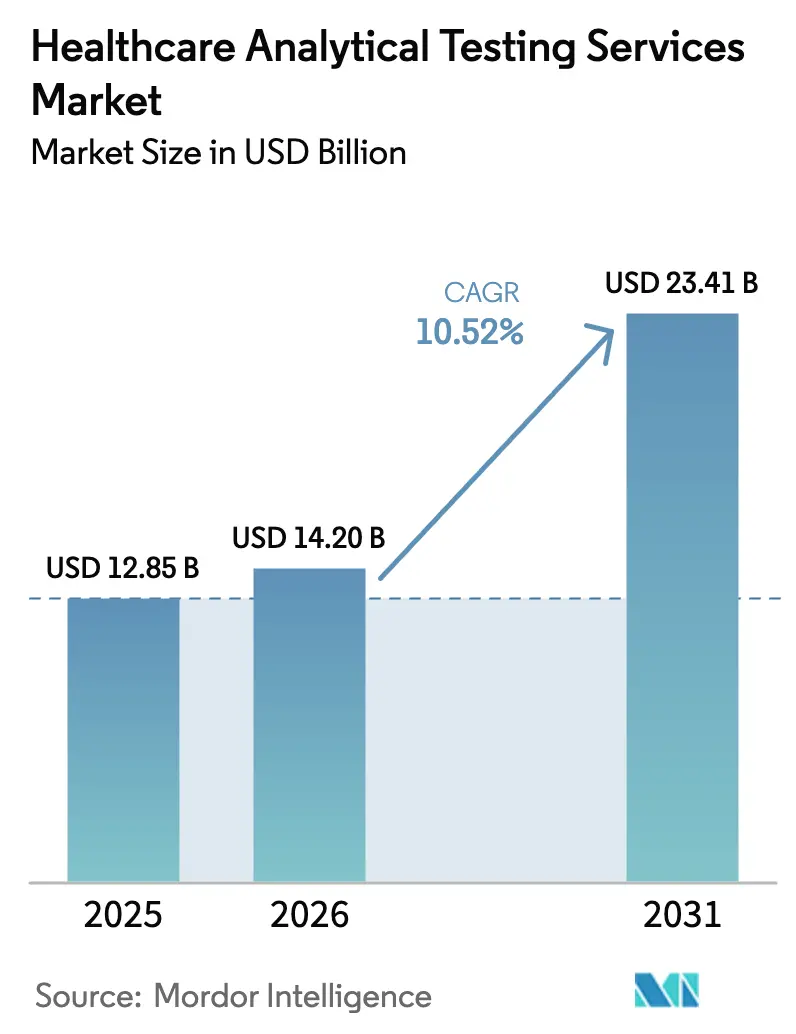

| Market Size (2026) | USD 14.2 Billion |

| Market Size (2031) | USD 23.41 Billion |

| Growth Rate (2026 - 2031) | 10.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

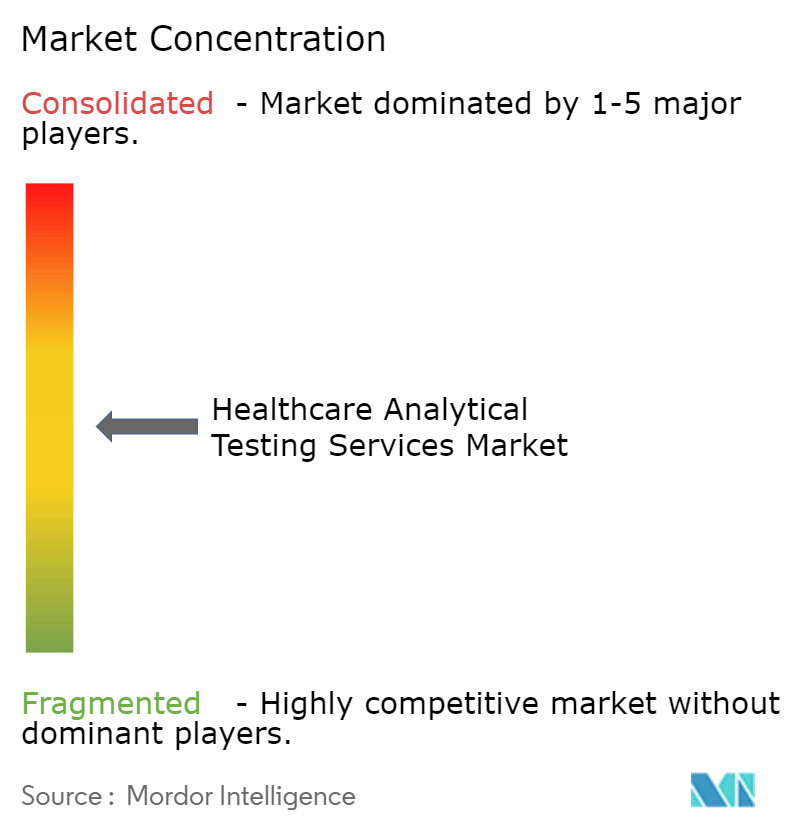

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Analytical Testing Services Market Analysis by Mordor Intelligence

The healthcare analytical testing services market size was valued at USD 12.85 billion in 2025 and estimated to grow from USD 14.2 billion in 2026 to reach USD 23.41 billion by 2031, at a CAGR of 10.52% during the forecast period (2026-2031). Growth draws momentum from the rapid expansion of biologics pipelines, the mainstreaming of personalized medicine, and increasingly stringent global regulations that demand deeper characterization of both drug substance and packaging. As drug formulations embrace higher molecular complexity, sponsors lean heavily on outsourced specialists that can supply cutting-edge mass-spectrometry, spectroscopy, and bioassay platforms without the fixed-cost burden of internal labs. Procurement departments also favour contract test houses that demonstrate audit-ready digital data integrity and robust quality-by-design (QbD) workstreams. Heightened consolidation among leading laboratories, coupled with aggressive deployment of AI-enabled method development tools, is widening the capability gap between tier-one providers and smaller regional firms.

Key Report Takeaways

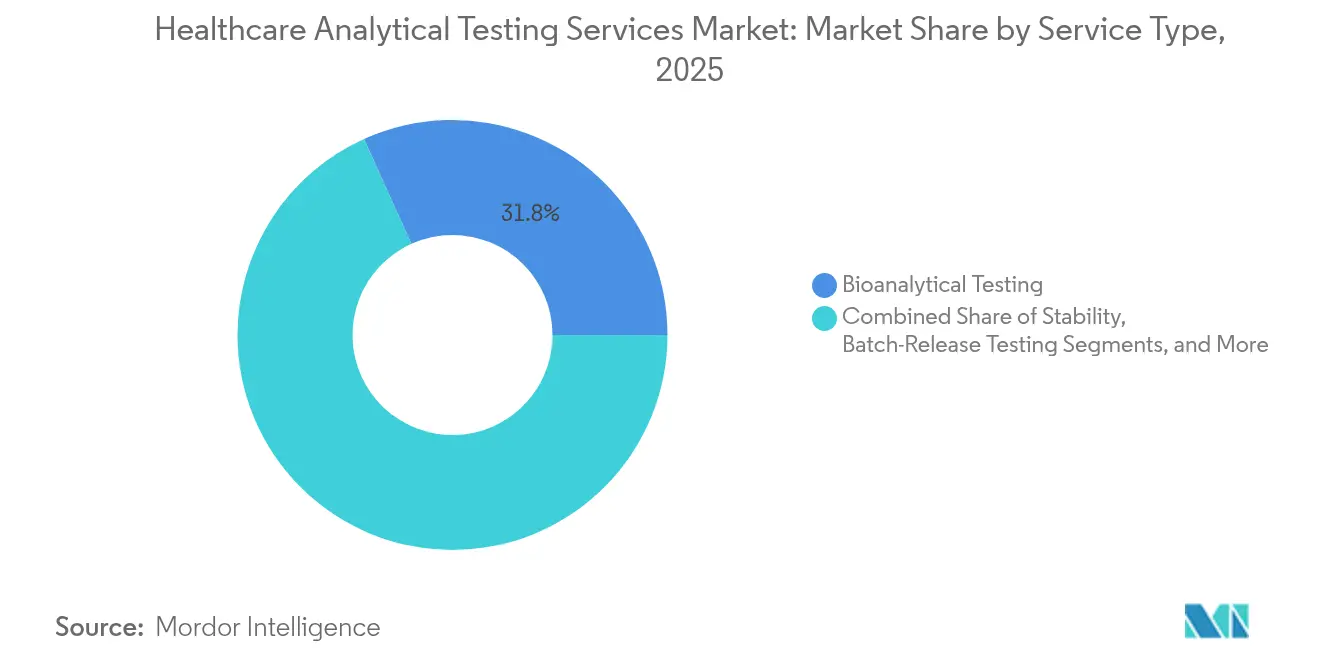

- By service type, bioanalytical testing led with 31.75% of the healthcare analytical testing services market share in 2025, while cell and gene-therapy viral vector testing is projected to expand at 14.86% CAGR through 2031.

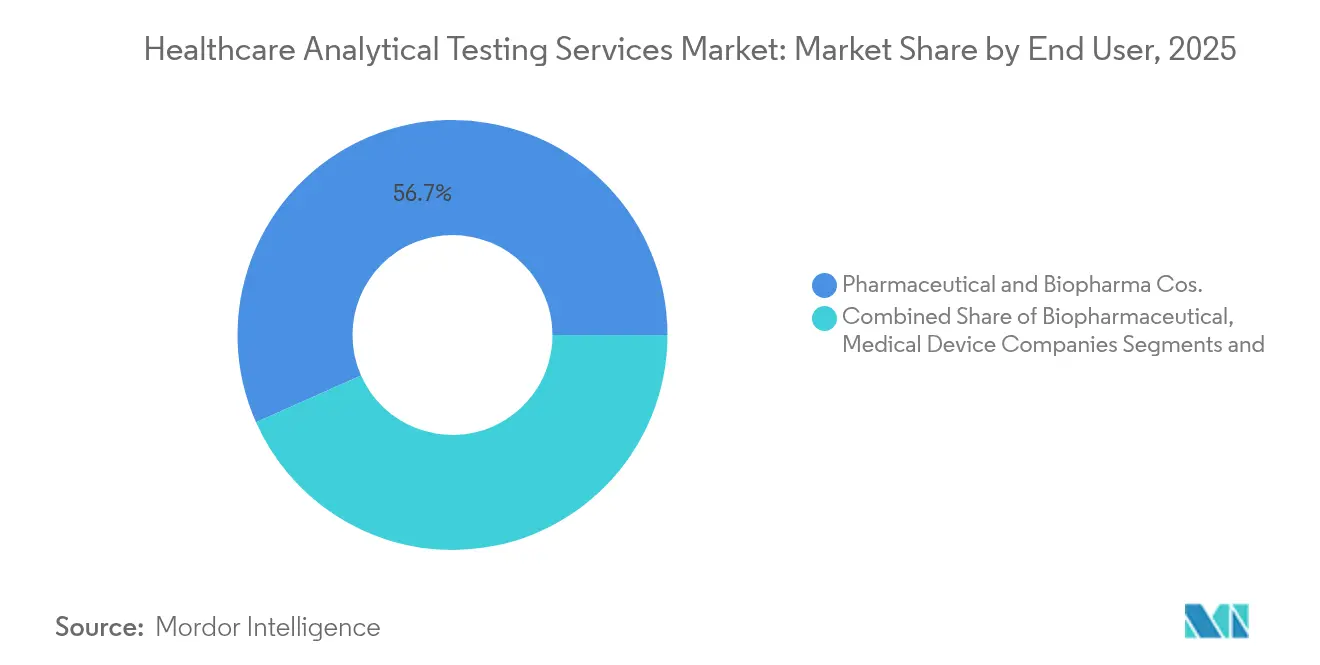

- By end user, pharmaceutical and biopharmaceutical companies accounted for 56.65% of the healthcare analytical testing services market in 2025, whereas CDMOs/CROs are forecast to grow at 10.62% CAGR to 2031.

- By development, commercial and marketed products are expected to generate the highest testing vote, pre-clinical and Phase I pipelines are expected to post the fastest 10.95% CAGR through 2031.

- By geography, North America held 41.20% of % healthcare analytical testing services market share in 2025; Asia Pacific is set to register the quickest 11.12% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Analytical Testing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing surge for complex biologics & biosimilars | +2.80% | North America & Europe, global reach | Medium term (2-4 years) |

| Adoption of quality-by-design in drug development | +1.90% | North America, EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Personalized-medicine-led biomarker demand | +2.10% | North America & Western Europe, global influence | Medium term (2-4 years) |

| Regulatory tightening on extractables & leachables | +1.40% | FDA and EMA jurisdictions, global ramifications | Short term (≤ 2 years) |

| Cell- & gene-therapy viral-vector testing boom | +1.70% | North America & Europe, emerging Asia-Pacific centers | Long term (≥ 4 years) |

| AI-enabled high-throughput method development | +0.90% | Early adoption in North America & Europe, worldwide diffusion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Outsourcing Surge for Complex Biologics & Biosimilars

Biologics and biosimilars now dominate late-stage pipelines, yet their multidimensional characterization needs, such as protein folding, aggregation, glycosylation, and potency, outstrip in-house capabilities for many sponsors. WuXi Biologics recorded RMB 18.675 billion revenue in 2024, supported by 151 new integrated projects that leaned on external analytics to handle 40–60 comparability batches per product, well beyond historical norms. Contract labs offering state-of-the-art LC-MS and orthogonal bioassays, therefore secure recurring fee streams across the product lifecycle.

Adoption of Quality-By-Design in Drug Development

ICH Q8–Q12 guidelines elevate analytical procedure development from routine compliance to a strategic lever. Sponsors increasingly insist on design-space establishment, critical quality attribute mapping, and statistical DoE during method validation. Laboratories that can provide software-driven QbD packages win earlier engagement and stickier contracts, reducing client attrition rates.[1]ISPE, “ICH Q14 – Analytical Procedure Development,” ispe.org

Personalized-medicine-led Biomarker Demand

The pivot toward precision oncology and rare-disease therapeutics fuels a surge in multi-omics biomarker discovery, validation, and companion diagnostic development. Labcorp’s FDA-cleared PGDx elio plasma focus Dx liquid biopsy accents the need for ultra-sensitive platforms that integrate genomics, proteomics, and metabolomics in a single workflow.

Regulatory Tightening on Extractables & Leachable

FDA draft guidance and EU GMP Annex 1 revisions reposition E&L testing as a critical safety assurance rather than a box-ticking exercise. Intertek and peers have expanded high-resolution GC-MS and LC-MS libraries capable of profiling low-level leachables in single-use systems, pushing throughput gains while maintaining regulatory rigor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Global Data-Integrity Regulations | -1.80% | Global, with varying enforcement intensity | Short term (≤ 2 years) |

| Shortage Of Mass-Spectrometry Talent | -1.20% | North America & Europe primarily, emerging in Asia Pacific | Medium term (2-4 years) |

| High Capex For Next-Gen Analytical Platforms | -0.90% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Intensifying IP-Ownership Disputes In Outsourced Studies | -0.60% | North America & Europe primarily, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex Global Data-Integrity Regulations

The ALCOA+ principles championed by the FDA and echoed by the MHRA oblige laboratories to deploy audit-ready electronic systems, redundant backups, and full audit trails.[2]UK MHRA, “GxP Data Integrity Guidance,” gov.uk Smaller firms struggle with capital outlays for 21 CFR Part 11-compliant LIMS and frequent re-validation exercises, narrowing their bid competitiveness.[3]FDA, “Data Integrity and Compliance With Drug CGMP,” fda.gov

Shortage of Mass-Spectrometry Talent

Vacancies for LC-MS/MS specialists linger for months as universities graduate fewer analytical chemists than the market demands. High turnover inflates labour costs and delays project onboarding, particularly for complex biologic comparability studies that need experienced personnel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Bioanalytical Testing Anchors Routine Demand While Viral-Vector Assays Accelerate

Bioanalytical Testing held 31.75% of the healthcare analytical testing services market share in 2025, driven by indispensable pharmacokinetic and immunogenicity assessments across all trial phases. The healthcare analytical testing services market size attributed to Bioanalytical Testing is projected to rise at 8.42% CAGR to 2031 as monoclonal antibodies and antibody-drug conjugates proliferate. Routine ligand-binding assays, hybrid LC-MS workflows, and immunogenicity panels, therefore, remain core revenue pillars. Complementing this base, Cell & Gene-Therapy Viral Vector Testing will expand at 14.86% CAGR, outpacing every peer segment through specialized replication-competent virus assays and next-generation sequencing-based genome integrity checks. Method development & validation services gain uplift from QbD adoption, while extractables & leachables testing sees double-digit growth as single-use manufacturing expands.

Charles River Laboratories leverages four decades of bioanalytical experience and a global network of GLP facilities to service early- and late-phase programs. Meanwhile, bioMérieux’s 3P ENTERPRISE platform automates environmental monitoring, reflecting wider digitalization inside microbiology labs. Rapid sterility methods from Nelson Labs cut incubation windows down to six days, freeing cold-chain inventory space and accelerating lot release.

By End User: CDMOs and CROs Challenge Pharmaceutical Incumbency

Pharmaceutical & Biopharmaceutical Companies captured 56.65% of the healthcare analytical testing services market in 2025. Yet, CDMOs/CROs will expand their testing demand at 10.62% CAGR as integrated development-plus-manufacturing deals become standard. The healthcare analytical testing services market size attributable to CDMOs/CROs is forecast to reach USD 7.55 billion by 2031. Medical Device Companies increasingly outsource biocompatibility, pyrogen, and E&L studies owing to tighter device regulations. Hospitals & Clinics seek specialized oncology genomic panels they cannot run in-house, whereas Academic Institutes drive new method development for multi-omics biomarker programs.

The rise of decentralised trials fuels ICON plc’s collaboration with LEO Pharma to integrate analytics and site management under one contract, signposting demand for holistic clinical-analytical packages. CDMO heavyweights are also scaling laboratory estates; Sterling Pharma Solutions added five new QC and R&D labs in 2024, boosting capacity for small-molecule testing.

By Development Phase: Commercial Lots Dominate Throughput While Pre-Clinical Studies Thrive

Commercial/Marketed products generate the most testing volume through batch release, stability, and pharmacovigilance studies. In parallel, Pre-Clinical and Phase I workstreams display the sharpest 10.95% CAGR as discovery funnels widen in cell and gene therapy. Early-phase sponsors outsource method development, forced-degradation studies,s and metabolite profiling to mitigate schedule risk. Phase III testing continues to underpin large steady-state demand because every pivotal trial, whether small molecule or biologic, still requires high-throughput bioanalysis and validated potency assays.

Adaptive designs and platform trials enlarge the analytical scope mid-study, obliging flexible labs that can rapidly broaden assay menus. As real-world evidence becomes a regulatory staple, many marketed products now undergo longitudinal biomarker surveillance, expanding commercial-phase service revenues.

Geography Analysis

North America controlled 41.20% of the healthcare analytical testing services market share in 2025, sustained by the FDA’s globally influential rulemaking, dense pharmaceutical headquarters, and a deep bench of GLP-compliant laboratories. The region also attracts heavy capital investment: Thermo Fisher inaugurated a 29,000 sq ft bioanalytical hub in Gothenburg while maintaining Boston as its command centre, signaling a trans-Atlantic footprint that prioritises proximity to sponsors.

Europe sustains robust growth due to strict GMP Annex 1 revisions that push sterility and environmental monitoring volumes. Eurofins Scientific runs 900 laboratories across 62 countries and posted EUR 6.515 billion revenue in 2023, reflecting continental breadth. SGS strengthened its biologics testing facility in Lincolnshire, supplying a one-stop microbiology and chemistry offer that resonates with European biosimilar developers.

Asia Pacific is the fastest climber, advancing at 11.12% CAGR as China, India, and South Korea absorb global manufacturing mandates. WuXi AppTec’s divestiture of its Advanced Therapies unit to Altaris highlights fluid strategic positioning around high-value analytics. Government incentives, from Singapore’s biomedical schemes to South Korea’s gene-therapy grants, attract new GLP labs that align with PIC/S GMP, propelling cross-border data acceptance. Domestic regulatory agencies are aligning with ICH and ISO standards, streamlining dossier acceptance across regions, and lowering re-testing duplication.

Competitive Landscape

The healthcare analytical testing services market displays moderate fragmentation but shows a discernible tilt toward consolidation as top players aggregate niche competencies. Eurofins Scientific has closed more than 80 acquisitions, adding Infinity Laboratories and Ascend Clinical in 2024 to deepen its biopharma and medical device portfolios. Labcorp enhances oncology analytics through the 2025 purchase of Incyte Diagnostics assets, expanding precision-medicine reach in the Pacific Northwest. Thermo Fisher earmarked USD 40–50 billion for acquisitions, signalling sustained deal flow that could recalibrate service depth among first-tier laboratories.

Technology investment is the primary battlefield. AI-guided chromatographic gradient prediction, robotic sample preparation, and auto-verification cut cycle times and reduce human error. Intertek’s risk-based quality assurance programme delivered 8.5% growth inside its health division, proving that digital lean operations convert directly into margin lift—providers lacking capital for full-stack automation risk relegation to subcontractor roles.

Specialized entrants still prosper where agility trumps scale, particularly in viral-vector genomics, continuous-manufacturing analytics, and rapid sterility testing. Nelson Labs’ six-day sterility turnaround sets a new service benchmark, compelling incumbents to accelerate innovation pipelines. Across the board, laboratory networks that can guarantee end-to-end data integrity, traceability, and global regulatory harmonization retain competitive primacy.

Healthcare Analytical Testing Services Industry Leaders

Charles River Laboratories

Laboratory Corporation of America Holdings

Intertek Group

SGS SA

Eurofins Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Labcorp announced the acquisition of select assets of Incyte Diagnostics’ clinical and anatomic pathology testing businesses, broadening oncology test coverage in the Pacific Northwest.

- April 2025: Roche committed USD 50 billion to expand U.S. pharma and diagnostics infrastructure, targeting 12,000 new jobs by 2030.

- March 2025: Labcorp completed the purchase of BioReference Health’s oncology-focused testing assets, bolstering its precision cancer portfolio.

- March 2025: Nelson Labs introduced rapid sterility testing that slashes incubation to six days at U.S. and German sites.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the healthcare analytical testing services market as fee-based laboratory analyses that evaluate the identity, purity, potency, stability, and sterility of small-molecule drugs, large-molecule biologics, cell and gene therapies, medical devices, and nutraceuticals from pre-clinical screening through post-launch surveillance.

Scope exclusion: Routine quality checks performed entirely within a sponsor's own manufacturing facility are excluded.

Segmentation Overview

- By Service Type

- Bioanalytical Testing

- Stability Testing

- Batch-Release Testing

- Raw Material & Physical Characterization

- Method Development & Validation

- Microbial & Environmental Monitoring

- Extractables & Leachables

- Biosafety & Sterility Testing

- Other Specialized Services

- By Molecule

- Small-Molecule Drugs

- Large-Molecule Biologics

- Cell & Gene Therapies

- Combination & Medical Device Products

- Nutraceuticals

- By Development Phase

- Pre-Clinical

- Phase I

- Phase II

- Phase III

- Commercial/Marketed

- By End User

- Pharmaceutical Companies

- Biopharmaceutical Companies

- Medical Device Companies

- CDMOs/CROs

- Hospitals & Clinics

- Academic/Research Institutes

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with quality heads at North American, European, and Asia Pacific contract laboratories, alongside procurement managers at mid-sized bio-pharma companies, enabled us to validate prevailing price bands, service mix shifts, and the share of batches now outsourced. Follow-up surveys with regulatory consultants clarified filing-related test volumes in emerging markets.

Desk Research

We began by pulling publicly available metrics from authoritative bodies such as the US FDA drug approval database, the European Medicines Agency clinical trial register, OECD R&D expenditure statistics, and WHO Global Health Observatory data; these set the demand backdrop we later refined. Corporate filings, investor presentations, and news retrieved through D&B Hoovers and Dow Jones Factiva helped us benchmark outsourcing ratios and average testing prices across leading contract labs.

Trade association portals (e.g., BioPharma Europe, Advanced Medical Technology Association) and peer-reviewed journals supplied prevalence data on biologics and combination products, while customs records illuminated cross-border movement of test reagents.

The sources listed are illustrative rather than exhaustive; many additional references were consulted to verify numbers and context.

Market-Sizing & Forecasting

A blended top-down view linking annual production volume, average batch size, and regulatory submission counts established the total addressable demand pool, which we further sense checked through selective supplier roll-ups of contract lab revenues. Key variables such as biologic share of pipeline assets, FDA novel drug approvals, average cost per stability study, and regional clinical trial starts shaped the model.

For forecasting, we applied multivariate regression supplemented by scenario analysis; independent drivers (R&D spend growth, new facility start-ups, and evolving GMP guidelines) were projected first, then loaded into the model to derive service revenues through 2030. Gaps where bottom-up evidence ran thin, particularly in Tier 2 Asian markets, were bridged using cross-regional outsourcing rate analogs vetted with interviewees.

Data Validation & Update Cycle

Outputs undergo variance checks against independent revenue disclosures, anomaly reviews by a senior analyst, and team sign-off. Mordor analysts refresh the dataset annually, triggering interim updates when material events, such as major regulatory changes or large M&A deals, shift market fundamentals; a final verification pass occurs just before report release.

Why Our Healthcare Analytical Testing Services Baseline Commands Reliability

Published figures vary because firms differ on whether to include device testing, how they treat inflation in average service prices, and how often they re-benchmark models.

Key gap drivers include narrower molecule scope (several sources omit cell and gene therapy panels), aggressive discounting of average selling prices, or reliance on historic revenue trajectories without cross-checking emerging trial counts and biosimilar uptake. Mordor's model, with its annual refresh cadence and dual track (regulatory data plus supplier revenue) approach, minimizes these skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.85 B | Mordor Intelligence | - |

| USD 17.01 B | Global Consultancy A | Includes in-house tests and applies uniform 3% price inflation, inflating totals |

| USD 7.48 B | Industry Publisher B | Excludes medical device panels and uses 2023 outsourcing rates without update |

In sum, the disciplined scope selection, variable level transparency, and continuous validation embedded in Mordor's methodology deliver a balanced, reproducible baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current size of the healthcare analytical testing services market?

The healthcare analytical testing services market size stands at USD 14.2 billion in 2026 and is projected to hit USD 23.41 billion by 2031.

Which service segment leads the market today?

Bioanalytical Testing leads, holding 31.75% healthcare analytical testing services market share in 2025.

Which geographic region is growing fastest?

Asia Pacific shows the highest regional CAGR, advancing at 11.12% through 2031 on the back of manufacturing scale-up and regulatory harmonization.

Why are CDMOs and CROs gaining market share?

Drug sponsors increasingly favour integrated outsourcing that combines manufacturing and advanced analytics, driving CDMOs/CROs to a forecast 10.62% CAGR through 2031.

How are regulations influencing market demand?

Tighter guidelines on QbD, extractables & leachables and data integrity compel sponsors to use specialised labs with validated, audit-ready methods, fuelling steady outsourced testing growth

What technologies are reshaping laboratory competitiveness?

AI-guided method development, robotic sample prep and rapid sterility testing shorten turnaround times and improve data quality, providing strategic differentiation for early adopters.

Page last updated on: