Medical Device Connectivity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.81 Billion |

| Market Size (2031) | USD 13.51 Billion |

| Growth Rate (2026 - 2031) | 22.95% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device Connectivity Market Analysis by Mordor Intelligence

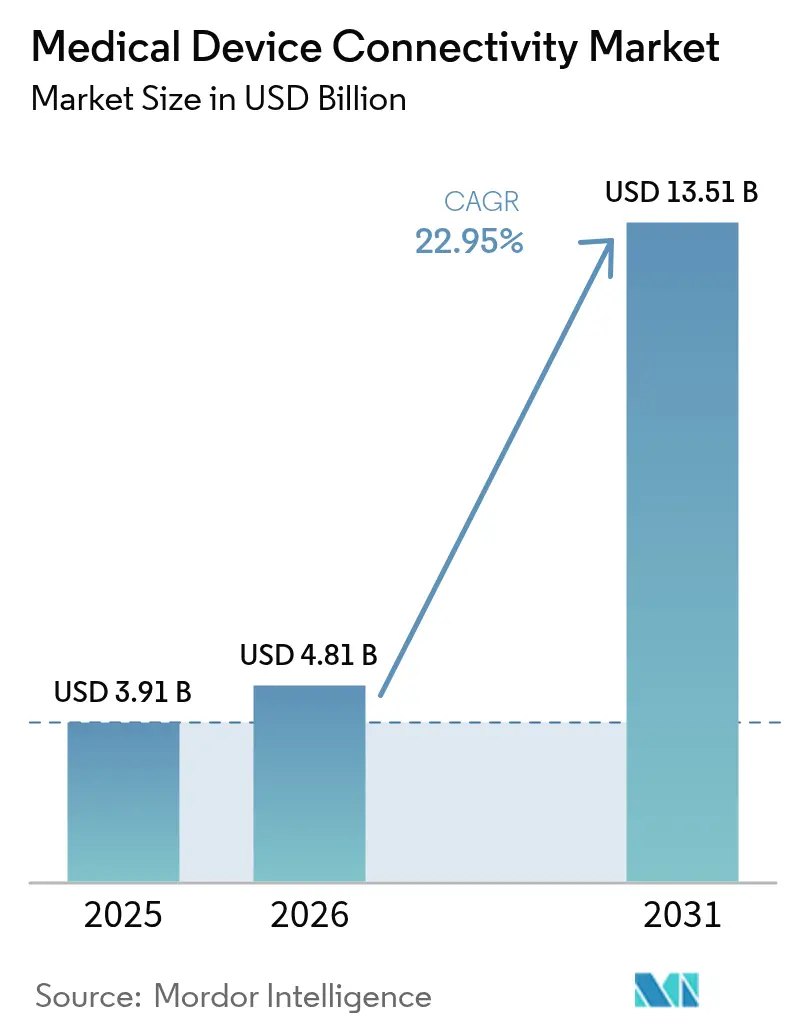

The global medical device connectivity market size was valued at USD 3.91 billion in 2025 and estimated to grow from USD 4.81 billion in 2026 to reach USD 13.51 billion by 2031, at a CAGR of 22.95% during the forecast period (2026-2031). Rapid digitization of healthcare, mounting clinician workload, and the move to value-based reimbursement are driving demand for seamless device-to-system data exchange. Healthcare providers are replacing proprietary protocols with open standards to ease information blocking penalties and reduce documentation time. Rising specialist shortages are expanding Tele-ICU programs, while continuous monitoring across acute, ambulatory, and home settings is lowering readmissions and improving care coordination. Investments in secure connectivity architectures are accelerating as regulators tighten cybersecurity oversight and 6G research promises ultra-reliable, low-latency wireless links for critical care applications.

Key Report Takeaways

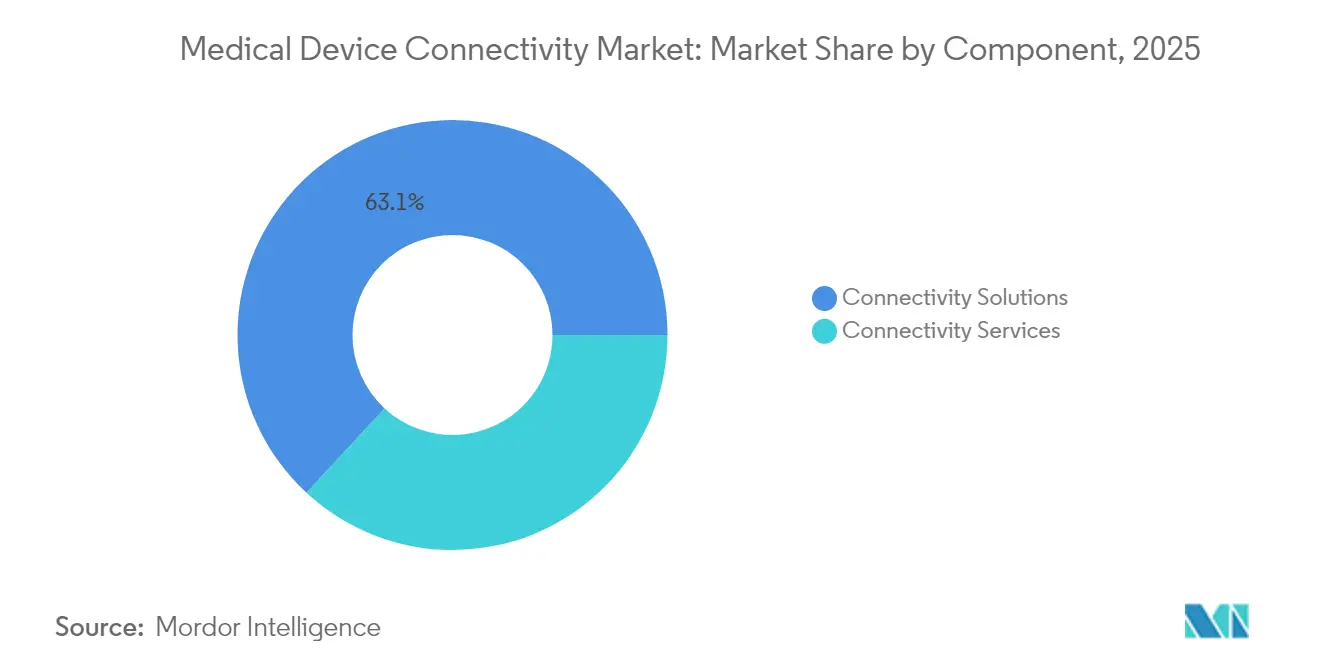

- By component, connectivity solutions led with 63.12% of the medical device connectivity market share in 2025; connectivity services are projected to advance at a 25.30% CAGR through 2031.

- By technology, wired interfaces held 57.35% of the medical device connectivity market size in 2025, while wireless technologies are expected to grow 24.95% annually to 2031.

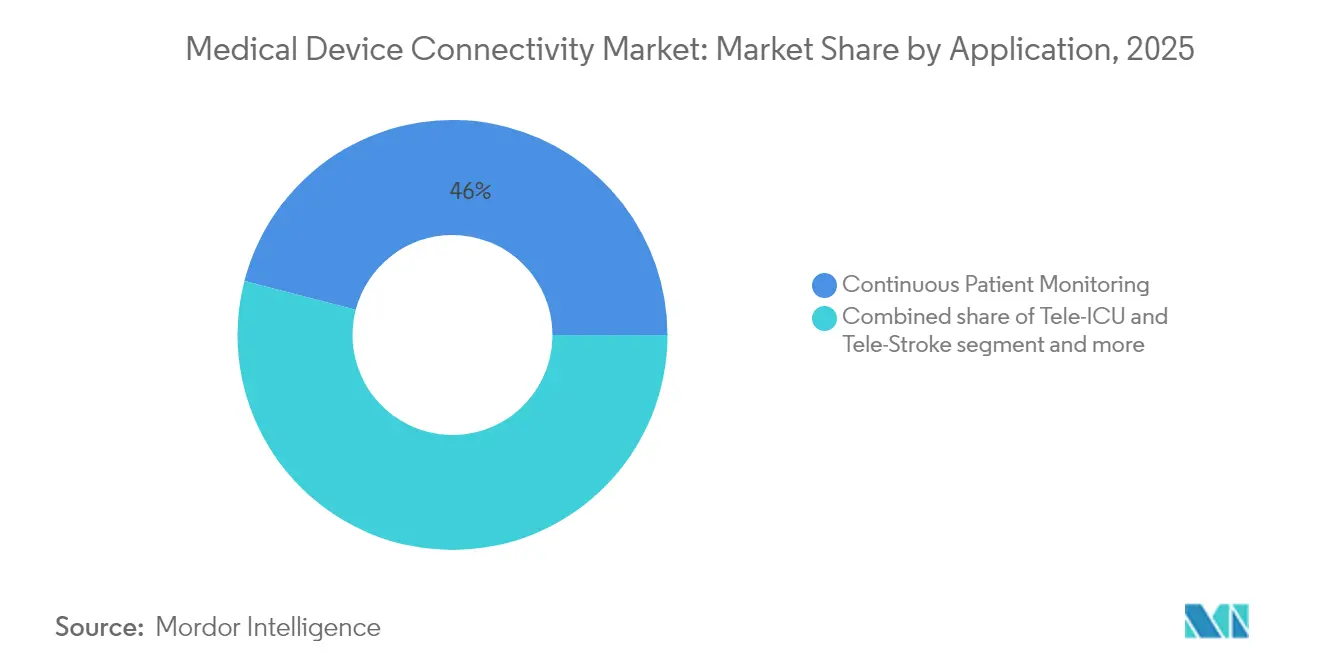

- By application, continuous patient monitoring accounted for 45.95% of the medical device connectivity market size in 2025; Tele-ICU & Tele-Stroke applications are forecast at a 26.40% CAGR.

- By end-user, hospitals & clinics commanded 66.70% of the medical device connectivity market share in 2025, whereas home healthcare is poised for 27.10% CAGR growth.

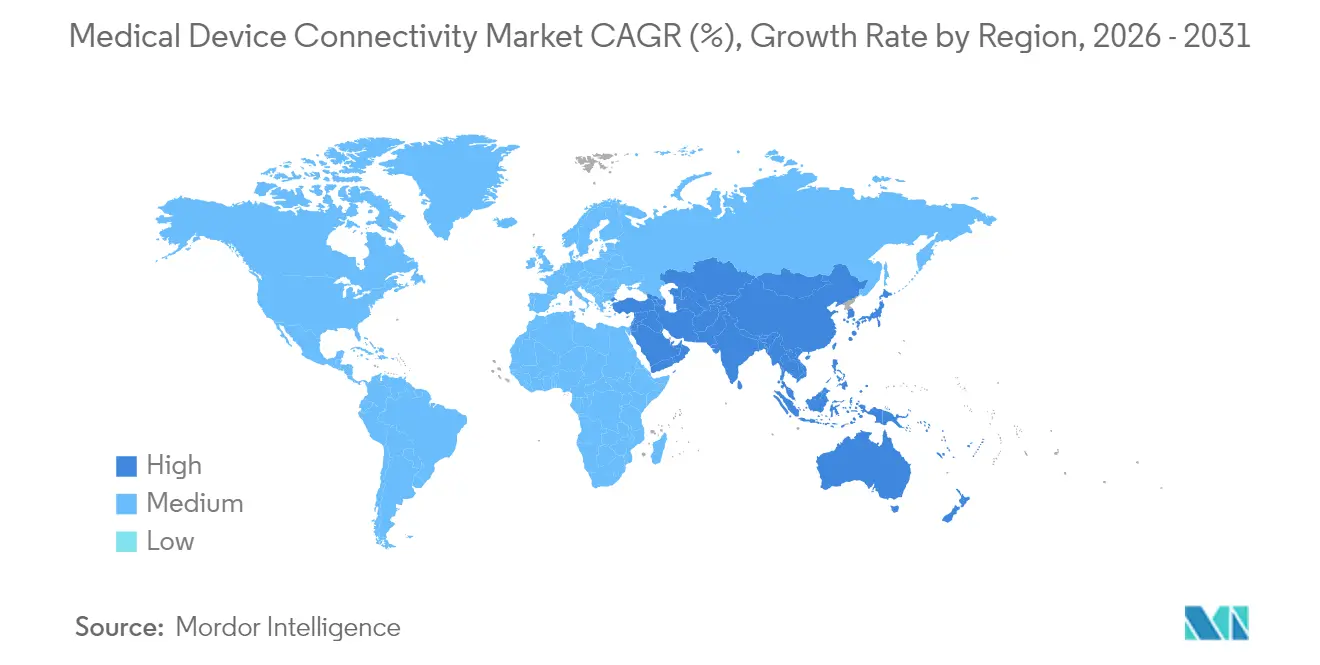

- By geography, North America led with 38.10% of revenue in 2025; Asia Pacific is set to expand at 25.90% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Device Connectivity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EMR interoperability mandates and digital-health policies | +5.9% | North America, Europe | Medium term (2-4 years) |

| Outcome-based reimbursement demanding real-time data | +5.2% | North America, Europe, emerging APAC | Medium term (2-4 years) |

| Expansion of remote and home-based chronic-care monitoring | +4.3% | Global | Short term (≤ 2 years) |

| Convergence of IoT cybersecurity frameworks | +3.6% | North America, Europe | Medium term (2-4 years) |

| Proliferation of multi-parameter wearable & implantable devices | +2.8% | North America, APAC | Short term (≤ 2 years) |

| Cloud-native analytics enabling predictive clinical insights | +2.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EMR interoperability mandates and digital-health policies

Standardized APIs mandated by the 21st Century Cures Act are forcing a shift from proprietary protocols to FHIR-based exchanges. Health systems completing compliance programs have cut documentation time by 13% and improved care coordination, encouraging broader deployment of connectivity engines. Device makers now design interoperability[1]Office of the National Coordinator for Health IT, “Interoperability,” healthit.gov into new products to avoid costly retrofit cycles and to accelerate FDA clearance processes that increasingly weigh connectivity safeguards.

Outcome-based reimbursement demanding real-time data

CMS alternative payment models link revenue to clinical outcomes, pushing hospitals to instrument beds with continuous monitoring and edge analytics that flag patient deterioration early. Health systems using connected RPM platforms have reported 24% lower readmissions for heart failure, aligning financial and quality incentives. This business case is strongest in intensive care units, stroke wards, and oncology infusion centers[2]Centers for Medicare & Medicaid Services, “CMS Interoperability and Patient Access Final Rule,” cms.gov, where preventable adverse events carry steep penalties.

Convergence of IoT cybersecurity frameworks

The FDA’s 2024 cybersecurity guidance[3]U.S. Food and Drug Administration, “Cybersecurity,” fda.gov aligns medical devices with the NIST framework, lowering integration complexity by harmonizing encryption, authentication, and patch management practices. Hospitals deploying these norms report 37% fewer security-related incidents and 42% faster onboarding of new wireless monitors, accelerating refresh cycles for legacy fleets.

Cloud-native analytics enabling predictive clinical insights

Embedding analytics within connectivity gateways converts raw waveform data into predictive scores at the bedside. Intensive care units using cloud inference engines capture early signs of sepsis or respiratory decline, giving clinicians an additional 4-hour window to intervene. Hospitals note that prior to these upgrades, 97% of device data was archived unused; repurposing it now supports early warning systems and population-level benchmarking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heterogeneous legacy device fleets without data standards | -5.9% | North America, Europe | Medium term (2-4 years) |

| High upfront integration and interface-engine costs | -4.7% | Global, emerging markets | Short term (≤ 2 years) |

| Persistent cybersecurity and patient-privacy vulnerabilities | -4.3% | Global | Medium term (2-4 years) |

| Limited workflow alignment causing clinician resistance | -3.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heterogeneous legacy device fleets without data standards

Hospitals often operate infusion pumps, ventilators, and monitors with life cycles exceeding eight years, many of which lack patchable operating systems. Interface engines must translate vendor-specific protocols, increasing project timelines and demanding continuous maintenance. Isolation networks protect vulnerable endpoints, yet duplicative wiring adds cost and complexity to expansion projects.

High upfront integration and interface-engine costs

Comprehensive connectivity deployments require hardware routers, cabling, middleware licences, and months of workflow mapping. Rural hospitals face tighter capital budgets and limited biomedical IT staff, prompting outsized reliance on managed-service vendors. This cost burden delays adoption despite proven clinical benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Interface platforms underpin end-to-end integration

Connectivity solutions held 63.12% of 2025 revenue, establishing them as the backbone for normalizing heterogeneous device data and enforcing rapidly evolving interoperability rules. These platforms translate HL7v2, FHIR, and proprietary streams into EHR-ready payloads that feed clinical decision support engines. Vendor neutral gateways such as Mirth Connect provide open-source flexibility, while enterprise suites bundle device libraries, alarm management, and analytics modules. Health systems deploy redundant server clusters to maintain near-zero downtime for high-acuity wards. As refresh cycles accelerate, the medical device connectivity market increasingly favors solutions offering out-of-the-box adapters for infusion pumps, anesthesia machines, and wireless telemetry packs.

Connectivity services are forecast to grow 25.30% annually as hospitals outsource implementation, maintenance, and cybersecurity patching. Managed-service contracts guarantee uptime, shield providers from staffing shortages, and ensure compliance documentation stays current. Small and mid-size facilities choose subscription models that convert capital expenditure into predictable operating costs. Service firms bundle interface tuning, 24 × 7 monitoring, and change-control governance across multi-vendor estates. This trend positions the services sub-segment as a key revenue accelerator within the broader medical device connectivity market.

By Technology: Wireless momentum closes the gap with entrenched wired lines

Wired links represented 57.35% of 2025 sales, anchored by shielded Ethernet backbones in critical care and surgical suites. Real-time waveform fidelity and known latency profiles keep hard-wired networks indispensable for high-bandwidth, life-support devices. Replacement cycles are slow because rewiring operating theatres disrupts clinical throughput and requires rigorous validation. Even so, hospitals upgrading core switches to support power-over-Ethernet enable future device classes without additional outlets, extending the relevance of wired infrastructure within the medical device connectivity market.

Wireless technologies are expected to rise 24.95% CAGR on the back of 5G upgrades and forthcoming 6G research that promises sub-millisecond latency. Access point density is increasing in general wards to support telemetry belts, wearable ECG patches, and smart beds transmitting posture and falls data. Wi-Fi 6E deployments carve new spectrum free of legacy interference, while private 5G slices offer deterministic quality of service for mobile CT scanners and rapid response carts. Hospitals report smoother patient transfers when IV pumps automatically switch SSIDs, eliminating manual reconnection at ward boundaries. These innovations confirm wireless as the mobility engine of the medical device connectivity market.

By Application: Continuous monitoring remains cornerstone while Tele-ICU soars

Continuous patient monitoring captured 45.95% of revenue in 2025, underscoring its centrality to deterioration detection, sepsis prevention, and ventilator weaning pathways. Central command centers aggregate feeds from bedsides, enabling fewer staff to supervise larger patient volumes and escalate only actionable alarms. Edge compute modules preprocess waveform data inside the hospital to minimize cloud egress and meet data-residency statutes. This persistent demand cements continuous monitoring as the volume anchor of the medical device connectivity market size.

Tele-ICU & Tele-Stroke services are projected at 26.40% CAGR, reflecting widescale adoption of hub-and-spoke critical care models. Rural facilities leverage high-definition cameras and shared analytics workstations to access intensivists around the clock. Stroke neurologists remotely confirm clot-retrieval eligibility within treatment windows, reducing disability rates. As reimbursement parity rules stabilize, more health systems bankroll dedicated tele-critical care networks, propelling this niche toward outsized gains within the medical device connectivity market.

By End-User: Hospitals dominate yet home care growth reshapes downstream demand

Hospitals & clinics contributed 66.70% of 2025 turnover, supported by regulatory mandates, multi-modality device fleets, and in-house biomedical informatics teams capable of sustaining complex interfaces. These institutions integrate pumps, ventilators, and hemodynamic monitors into EHR flows that feed quality dashboards and sepsis bundles. Documentation accuracy ties directly to Diagnosis-Related Group reimbursement, ensuring steady investment in the medical device connectivity market.

Home healthcare settings are on track for 27.10% CAGR, underpinned by expanded remote patient monitoring billing codes and consumer preference for aging-in-place. Cellular gateways embedded in blood pressure cuffs and spirometers overcome inconsistent broadband, automatically synchronizing data for clinician review. Analytics engines filter noise, surfacing only threshold breaches to care coordinators. This shift decentralizes demand, requiring vendors to support self-installation kits and intuitive mobile apps, and it marks a pivotal evolution in the medical device connectivity industry.

Geography Analysis

North America held 38.10% of 2025 revenue due to mature EHR penetration, strict interoperability enforcement, and early adoption of edge analytics. CMS penalties for information blocking and new API mandates compel providers to deploy standards-based gateways that seamlessly connect bedside devices with payer portals. Academic medical centers pilot AI-augmented surveillance that merges continuous monitoring with predictive scoring, accelerating procurement of high-throughput connectivity hubs. Venture investment in digital health startups further expands the regional footprint of the medical device connectivity market.

Asia Pacific is forecast to expand 25.90% annually between 2026-2031, the fastest worldwide. China scales smart hospital blueprints featuring private 5G, robotics, and cloud PACS integration, while India’s production-linked incentive schemes nurture indigenous device manufacturers embedding open-standard interfaces from inception. Japan upgrades rural clinics with tele-stroke networks, leveraging government stimulus that reimburses cross-prefecture consults over encrypted VPNs. South Korea and Australia incentivize data-centric healthcare pilots, creating fertile ground for wireless telemetry and AI triage algorithms. These dynamics are positioning the region as a critical growth engine of the medical device connectivity market.

Europe grows at a projected 21.05% CAGR, supported by the Medical Device Regulation and General Data Protection Regulation, which jointly elevate interoperability and cybersecurity bars. Germany subsidizes hospital digital maturity upgrades under its Hospital Futures Act, accelerating HL7-FHIR gateway procurements. The United Kingdom mandates digital maturity assessments for NHS trusts, unlocking funding for secure device onboarding. Nordic countries pioneer 6G research testbeds for clinical use, and pan-EU initiatives encourage cross-border data exchange via the European Health Data Space. Strong attention to privacy and security shapes vendor selection, with hospitals favoring platforms offering zero-trust designs and granular consent management, reinforcing Europe’s stature within the medical device connectivity market.

Competitive Landscape

The medical device connectivity market shows moderate concentration as multinational device makers, IT giants, and niche integrators align offerings around unified data platforms. Philips, through its Capsule acquisition, bundles bedside hubs with cloud analytics that flag early patient deterioration. GE HealthCare integrates VitalsIQ algorithms directly into monitors, shortening detection-to-intervention loops. Siemens Healthineers partners with Vivolight to launch multimodal angiography platforms that natively stream DICOM and OCT data into vascular guidance suites, exemplifying the shift from standalone connectors to workflow-centric ecosystems.

Cloud-native challengers capitalize on microservice architectures that scale elastically and simplify update roll-outs. Their subscription pricing undercuts perpetual licences, appealing to community hospitals and ambulatory networks. Start-ups embed machine learning models that classify waveforms or predict pressure-injury risk, positioning connectivity as an AI enablement layer. Security differentiation is intensifying; vendors advertise FIPS-validated encryption modules, continuous vulnerability scanning, and Software Bill of Materials disclosures to satisfy FDA premarket expectations.

Co-development and reseller agreements blur competitive boundaries. Device manufacturers white-label integration engines to speed time-to-market while connectivity specialists pre-certify libraries for hundreds of device profiles, lowering integration cost for providers. Strategic activity is expected to continue as platforms converge on end-to-end solutions that fuse device data, clinical context, and predictive analytics, redefining value capture across the medical device connectivity market.

Medical Device Connectivity Industry Leaders

Cisco Systems Inc.

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Oracle Corporation

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AVer Information Inc. showcased MD720UIS, MD120UI, and MD330U/UI cameras plus ViewCare software, bringing AI-driven fall detection and multi-device orchestration to hospital and home monitoring workflows.

- January 2025: The FDA warned of cybersecurity vulnerabilities in Contec CMS8000 and Epsimed MN-120 patient monitors and advised disconnecting remote functions until patches are applied.

- November 2024: Siemens Healthineers and Vivolight launched the ARTIS icono floor, a DSA-OCT hybrid platform delivering integrated vascular imaging via standard connectivity protocols.

- July 2024: Medprime Technologies released Micalys, an AI-enabled digital microscope offering slide-level scanning at 100× magnification with network sharing features for telepathology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical device connectivity market as the hardware, software, and associated services that move clinical data automatically between regulated bedside or ambulatory devices and hospital or cloud information systems. Components span interface engines, gateways, device-side modules, telemetry hubs, and the implementation support that keeps them interoperable. According to Mordor Intelligence, these elements form a distinct spend pool, separate from generic hospital IT budgets.

Scope Exclusion: We exclude unregulated consumer wearables, standalone electronic health record platforms, and any data-integration tools that operate only at the hospital information-system layer.

Segmentation Overview

- By Component

- Connectivity Solutions

- Interface Engines & Integration Platforms

- Connectivity Hubs & Gateways

- Device Interface Modules

- Connectivity Services

- Implementation & Integration

- Support & Maintenance

- Consulting & Training

- Connectivity Solutions

- By Technology

- Wired

- Wireless

- Hybrid

- By Application

- Continuous Patient Monitoring

- Tele-ICU & Tele-Stroke

- Imaging & PACS Connectivity

- Medication Administration & Smart IV Pumps

- Anesthesia & Ventilator

- Other Applications

- By End-User

- Hospitals & Clinics

- Ambulatory Surgery & Specialty Centers

- Home Healthcare Settings

- Other End-Users

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with biomedical engineers, clinical informaticists, and procurement heads across North America, Europe, and Asia so we could verify interface densities, refresh cycles, and service attach rates that desk sources seldom reveal. Follow-up surveys with gateway and ventilator makers let us refine price curves and future penetration assumptions.

Desk Research

Our team first compiled shipment and installed-base indicators from tier-1 sources such as the FDA Unique Device Identifier catalog, the Office of the National Coordinator for Health IT, Eurostat medical-technology files, and UN Comtrade customs codes. We then enriched figures with annual reports and AAMI connectivity briefs. Subscription feeds from D&B Hoovers and Dow Jones Factiva supplied segment revenues, while peer-reviewed papers in JAMA Network and IEEE IoT Journal explained clinical adoption pacing. These references illustrate, not exhaust, the secondary set that shaped baseline inputs.

Market-Sizing & Forecasting

A top-down build of device stock, replacement rhythms, and connectivity attach ratios anchors the 2025 baseline. Selective bottom-up roll-ups of ventilator, infusion-pump, and monitor suppliers validate totals. Key variables like installed ICU beds, remote-monitoring reimbursement codes, hospital Wi-Fi coverage, cybersecurity mandates, and average interface license fees feed a multivariate regression with scenario analysis to 2030. Gaps in bottom-up data are bridged with interview-derived ranges checked against public tender values.

Data Validation & Update Cycle

Model outputs pass variance screens against third-party shipment tallies and EHR penetration metrics before senior review. Reports refresh each year, while material events such as new FDA security rules trigger mid-cycle updates so clients receive our latest view.

Why Mordor's Medical Device Connectivity Baseline Commands Reliability

Published estimates often diverge because analysts start from different device lists, price ladders, or refresh cadences, and because attach ratios rise unevenly between regions.

The main gaps arise when other publishers fold in consumer fitness trackers that our scope omits, apply a single global ASP rather than the tiered schedule we validate through interviews, or assume near-universal wireless adoption without factoring capital-budget limits or compliance timelines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.91 B (2025) | Mordor Intelligence | |

| USD 4.30 B (2025) | Global Consultancy A | Includes consumer wearables; uses one flat ASP |

| USD 4.51 B (2025) | Industry Analyst B | Assumes 90 % wireless penetration by 2025 despite budget realities |

The comparison shows that when scope precision, attach-ratio evidence, and yearly updates are combined, our baseline delivers a balanced, transparent foundation that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the key factor motivating hospitals to upgrade legacy connectivity platforms?

Compliance with interoperability mandates is pushing hospitals to replace proprietary device interfaces with open-standard gateways that streamline data exchange and reduce clinician documentation time.

How is cybersecurity shaping vendor selection for connectivity solutions?

Providers prioritize platforms that embed zero-trust authentication and real-time vulnerability monitoring, aligning with FDA guidance that treats security as a prerequisite for device approval.

Why are wireless connectivity options gaining momentum over traditional wired links?

Wi-Fi 6E and private 5G networks support clinical mobility and easier room reconfiguration, enabling seamless monitoring as patients move between units without manual reconnection.

How are analytics changing the value proposition of device connectivity?

Edge and cloud analytics convert raw device data into predictive alerts, allowing care teams to intervene earlier and reduce preventable adverse events.

What role do managed services play in accelerating connectivity adoption?

Outsourcing implementation and maintenance helps facilities lacking in-house biomedical IT talent maintain uptime, manage patches, and meet evolving regulatory requirements more efficiently.

Outsourcing implementation and maintenance helps facilities lacking in-house biomedical IT talent maintain uptime, manage patches, and meet evolving regulatory requirements more efficiently.

Continuous data streams from wearables require scalable bandwidth management and contextual data tagging so that clinicians receive actionable insights without alert fatigue.

Page last updated on: