Maplitho Paper Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

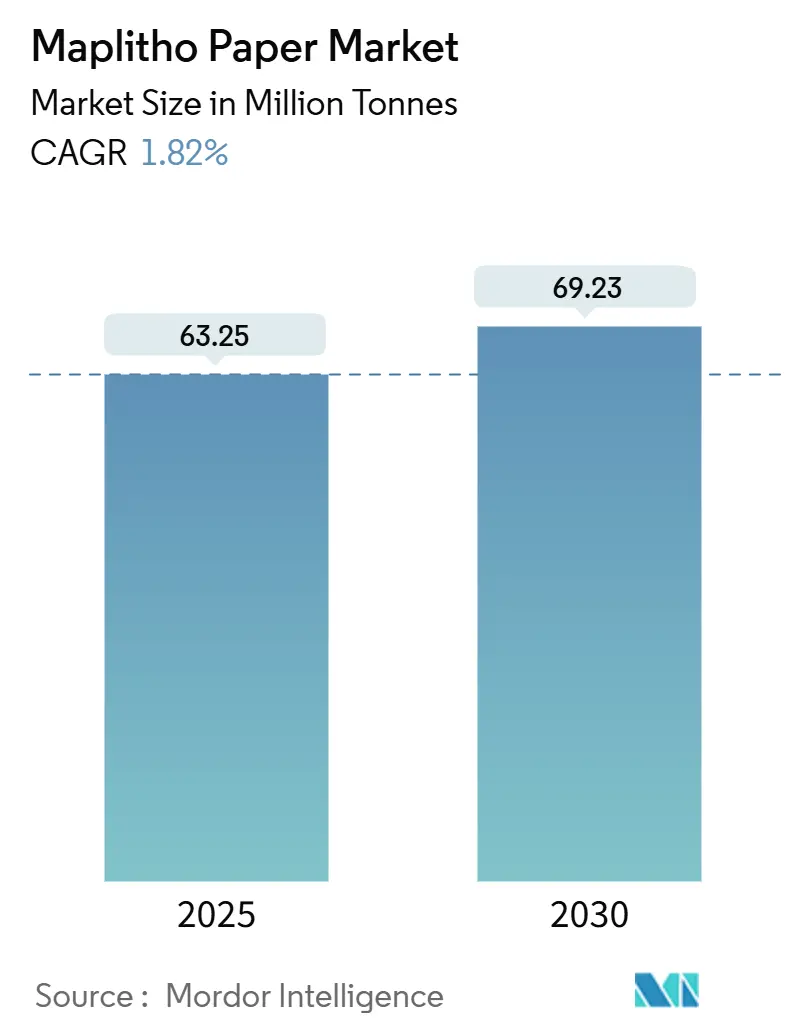

| Market Volume (2025) | 63.25 Million tonnes |

| Market Volume (2030) | 69.23 Million tonnes |

| Growth Rate (2025 - 2030) | 1.82% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Maplitho Paper Market Analysis by Mordor Intelligence

The Maplitho paper market size stands at 63.25 million tonnes in 2025 and is forecast to reach 69.23 million tonnes by 2030, advancing at a 1.82% CAGR over the period. Modest expansion reflects a maturing demand curve, yet the Maplitho paper market continues to gain incremental volumes from literacy programmes, premium print applications and expanding e-commerce documentation requirements. Asia-Pacific remains the centre of gravity as integrated mills leverage hardwood fibre proximity and scale efficiencies to buffer pulp price swings. In North America, 59 mill closures since 2014 have rebalanced supply and steadied pricing, while Europe’s tighter environmental rules drive consolidation and technology upgrades. Premium uncoated freesheet grades used on high-speed inkjet presses provide a margin hedge, encouraging capacity conversions from coated to uncoated lines and reinforcing the Maplitho paper market’s gradual shift toward higher-value niches.

Key Report Takeaways

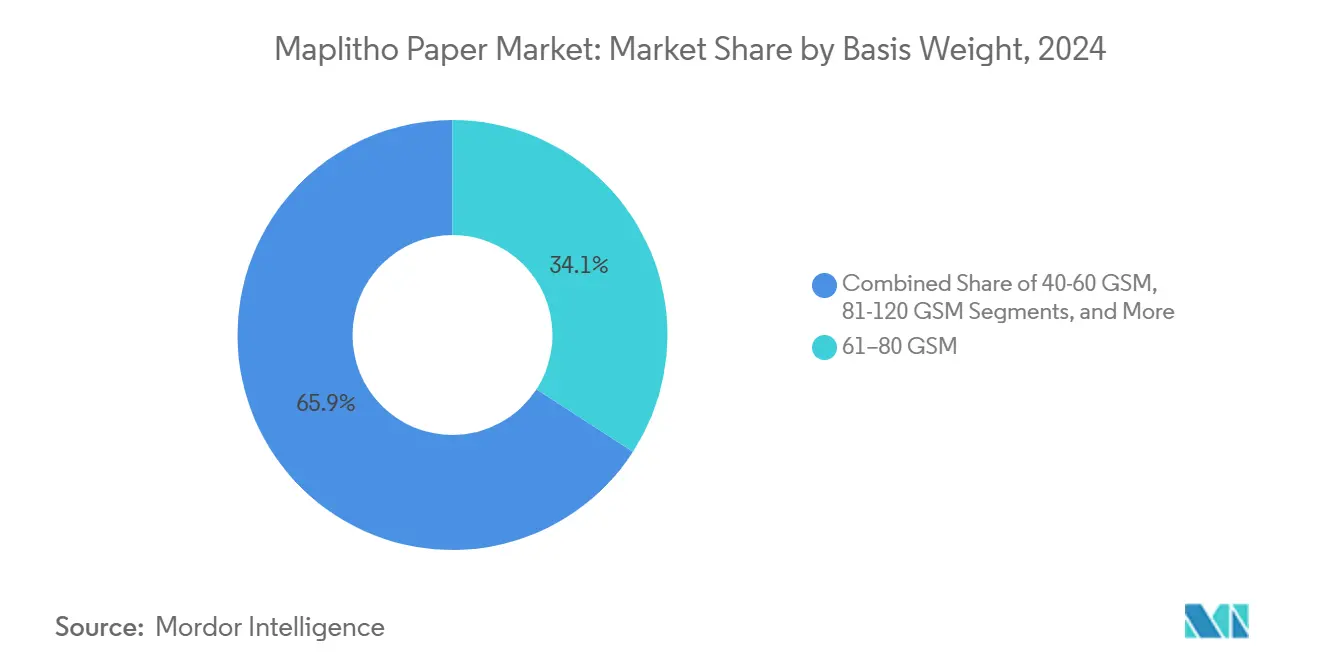

- By basis weight, the 61-80 GSM range segment held 34.14% of the Maplitho paper market share in 2024.

- By end-use application, the Maplitho paper market size for packaging inserts and manuals is projected to grow at a 2.26% CAGR between 2025-2030.

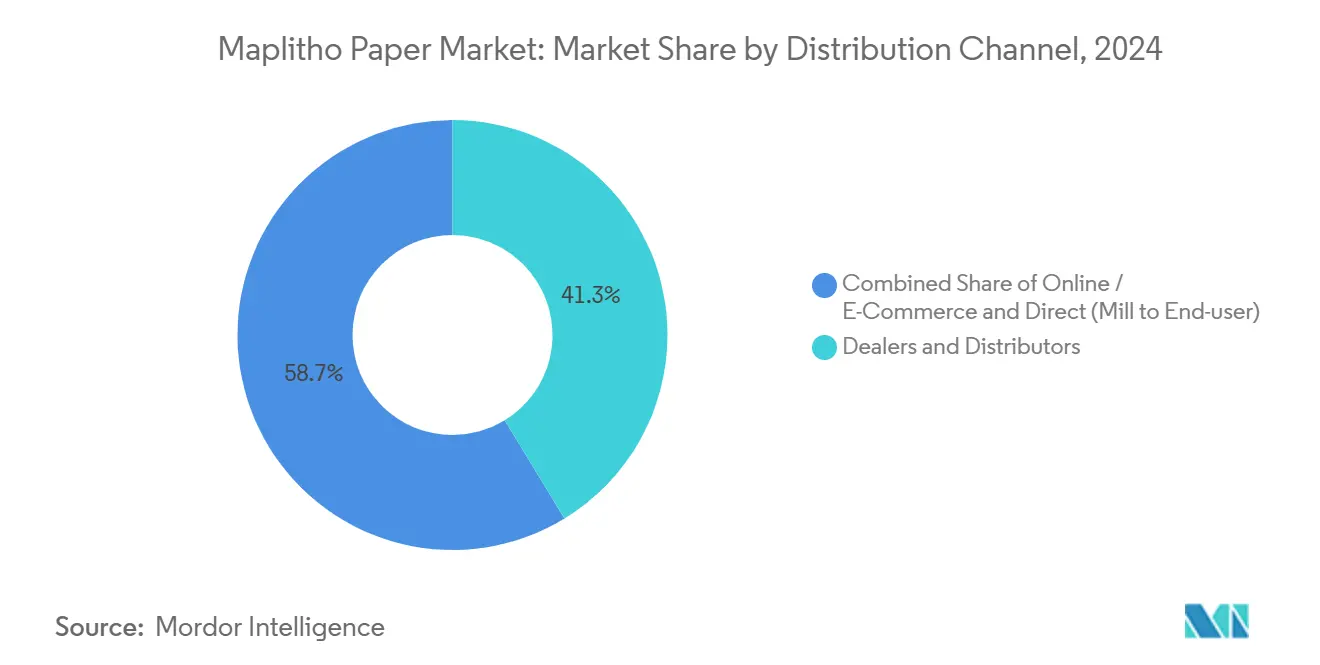

- By distribution channel, the dealer networks segment commanded 41.27% of the Maplitho paper market share in 2024.

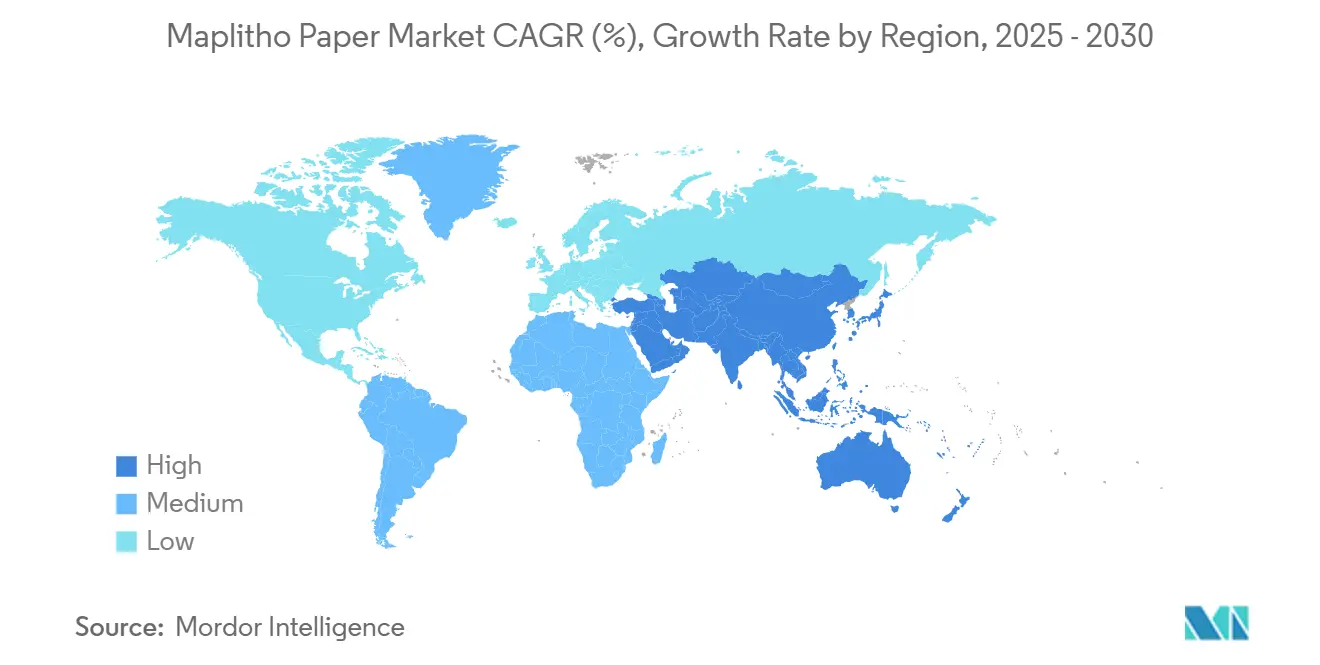

- By geography, the Maplitho paper market size for Asia-Pacific is projected to expand at a 2.56% CAGR between 2025-2030.

Global Maplitho Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising literacy rates and K-12 expenditure in emerging economies | +0.6% | Asia-Pacific, Middle East and Africa, Latin America | Long term (≥ 4 years) |

| Corporate/government shift to plastic-free documentation | +0.4% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Expansion of high-speed inkjet presses favouring premium uncoated sheets | +0.3% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Post-pandemic rebound in SME office printing volumes | +0.2% | Global, particularly developed markets | Short term (≤ 2 years) |

| Election-cycle spikes in ballot and campaign material printing | +0.1% | Democratic markets globally, cyclical impact | Short term (≤ 2 years) |

| Capacity conversions from coated to uncoated freesheet | +0.2% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising literacy rates and K-12 expenditure in emerging economies

Public investment in schools and textbooks is increasing long-term consumption of Maplitho paper market volumes. India’s sector, with more than 900 operating mills, meets expanding rural education needs by supplying examination sheets, workbooks and administrative forms. Historical FAO statistics show Asia-Pacific printing and writing paper usage rising from 2.4 million tonnes in 1962 to 20 million tonnes by 1992, illustrating the strong link between literacy drives and paper demand. China’s output growth from 25 million tonnes in 1997 to 71 million tonnes in 2007 further underscores that relationship. Because school systems reorder paper every academic year, the driver adds a structural component to Maplitho paper market demand. Mills therefore position capacity near high-growth education clusters to cut logistics costs and ensure timely deliveries.

Corporate/government shift to plastic-free documentation

Sustainability mandates are converting workflows once reliant on synthetic substrates into paper-based alternatives, reinforcing premium demand within the Maplitho paper market. HP met its zero-deforestation commitment by sourcing all brand paper from certified or recycled fibres, signalling supplier preference for eco-compliant sheets. European single-use-plastic rules now push businesses to print manuals, identification cards and certificates on uncoated freesheet instead of laminated plastic. The US Government Printing Office specification framework likewise sets strict performance attributes for federal contracts requiring archival-grade paper. Because compliance cycles run three-to-five years, mills benefit from predictable offtake that incentivises investment in higher-quality varieties. Vertical integration, coupled with forestry certification programmes, gives leading producers pricing leverage when offering plastic-replacement solutions.

Expansion of high-speed inkjet presses favouring premium uncoated sheets

Commercial printers are upgrading to inkjet equipment that runs at more than 300 metres a minute, yet these platforms require tight moisture control and refined surface formation. Consequently, premium uncoated freesheet grades command pricing at least 25% above office-copy categories, supporting margin expansion in the Maplitho paper market. Mills modifying head-box and press configurations to improve formation secure supply contracts with print service providers that value run-ability and colour fidelity. Ballot printers in California must also follow ink-penetration and opacity rules detailed by the Secretary of State, further stimulating demand for these specialised substrates. The technology-product linkage shields the segment from digital substitution because variable-data marketing, photobooks and election materials still require physical output.

Post-pandemic rebound in SME office printing volumes

Hybrid work has not eliminated the day-to-day paperwork of small business operations. The UK Longitudinal Small Business Survey found 40% of firms reported sales growth in 2023, a metric usually correlated with increased printing for invoices, HR records and contracts. OECD research shows SMEs embedded in value chains keep extensive documentation to satisfy buyer compliance chec. In the US, supply bottlenecks eased from 36.1% to 14.5% between April 2022 and July 2023, letting enterprises restock stationery and printing supplies. As SMEs expand payrolls, each new employee drives incremental printed form demand, reinforcing a base-load of Maplitho paper market consumption that digital tools have yet to displace fully.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating digitisation of workflows and e-billing | -0.8% | Global, with advanced adoption in developed markets | Long term (≥ 4 years) |

| Volatile hardwood pulp prices pressuring margins | -0.4% | Global, with acute impact in regions dependent on imported pulp | Short term (≤ 2 years) |

| Stricter effluent-/water-use regulations for integrated mills | -0.2% | North America, Europe, developed Asia-Pacific markets | Medium term (2-4 years) |

| Supply-chain risk from mill consolidation in Asia | -0.3% | Asia-Pacific, with spillover effects to global markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating digitisation of workflows and e-billing

Enterprises continue to substitute electronic document management for hard-copy processes, reducing baseline Maplitho paper market demand in sectors like banking and government services. OECD surveys confirm pandemic-driven digital adoption remains sticky, with firms expanding e-signature and cloud archiving systems that cut print volumes. Regulatory acceptance of digital invoices lowers the need for multipart stationery, while consumer preference for online statements accelerates decline in mail-based communications. Once installed, document-automation platforms create network effects that further erode paper usage. Although literacy growth offsets part of the volume loss in emerging regions, the downward pull on mature-economy tonnage persists and explains the modest overall CAGR.

Volatile hardwood pulp prices pressuring margins

Margins tighten when pulp cost spikes outpace end-product price adjustments. The US Producer Price Index for wood pulp climbed to 220.65 in January 2025, a 5.4% year-on-year rise that squeezed producers without secured fibre supply. Mills dependent on imported pulp in Europe and South Asia faced higher freight and currency expenses, aggravating cost swings. University of Georgia forecasts of plentiful salvage timber suggest near-term pulpwood prices may settle, yet structural constraints in Latin America hint at renewed upward pressure by 2027. Working-capital needs rise because manufacturers must carry inventory buffers to avoid shutdowns during price surges. The cost volatility prompts strategic hedging and pushes some mills to vertically integrate into forestry assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Basis Weight: Premium grades drive margin expansion

The >120 GSM bracket captured higher sales growth than any other category, advancing at 2.32% CAGR from 2025 to 2030 as customers sought rigid substrates for luxury packaging inserts, photobooks and high-impact marketing collateral. This slice of the Maplitho paper market benefits from durable texture and elevated brightness that withstands heavy ink coverage without distortion. In contrast, the 61–80 GSM band retains dominance, holding 34.14% of 2024 tonnage because it meets office-printer engine specifications and offers cost efficiency. Producers tweak refining and sizing parameters to lift stiffness and formation, ensuring multipurpose performance while keeping manufacturing yields high. The Maplitho paper market size for 40–60 GSM grades is likely to contract modestly as newspaper circulation wanes, prompting mills to repurpose lightweight capacity toward envelope or medical-leaflet variants. Equipment upgrades often emphasise automated moisture profiling, allowing shifts across basis weights without extended downtime, thereby improving mix flexibility. Growing demand for corporate sustainability certificates pushes buyers toward heavier, long-lasting sheets that endure archiving, supporting the strategic emphasis on premium segments.

Competitive positioning within basis weights hinges on fibre recipes and press section efficiency. Integrated players owning hardwood plantations mitigate input volatility and channel fibre with shorter lengths to achieve smooth surfaces required in the mid-to-heavy GSM categories. Capital expenditure prioritises dilution profiling, closed-loop water systems and advanced calendaring to enhance smoothness on >120 GSM grades while lowering energy intensity. International Paper earmarked USD 1.2 billion for 2025 upgrades focused on higher-margin uncoated freesheet lines, signalling confidence in the premium bracket’s profitability [1]“International Paper Annual Report 2024,” International Paper, internationalpaper.com. Mid-tier mills adopt niche strategies, such as tinted stationery or watermark security, that justify price premiums. Consequently, basis-weight mix optimisation emerges as a key lever for sustaining margins despite the Maplitho paper market’s low headline growth.

By End-use Application: Packaging inserts emerge as growth catalyst

Office printing and photocopiers, at 33.78% of 2024 demand, still anchor Maplitho paper market volumes because small enterprises and public offices maintain file copies, training manuals and compliance documents. Hybrid working stabilises run rates as employees split tasks between digital and physical formats. Simultaneously, e-commerce expansion is boosting packaging insert requirements for assembly instructions, warranty cards and safety sheets, fuelling a 2.26% CAGR through 2030 in this sub-segment. Consumer-protection regulations mandating printed multilingual instructions reinforce the trajectory, ensuring sustainable tailwinds even if transactional printing declines further. As inserts require opacities that prevent show-through, mills producing mid-weight grades with high bulk gain competitive advantage.

The Maplitho paper market size for publishing and commercial printing remains resilient in niche sectors such as religious texts, coffee-table books and local periodicals that value tactile quality. Stationery and notebooks obtain incremental gains from school enrolment, especially where government procurement absorbs large volumes for subsidised exercise books. Emerging government programmes that distribute learning kits in rural districts underpin this steady demand lane. Election material, while cyclical, adds sizable bursts to the application mix, prompting mills to build short-run flexibility and security-thread capabilities. The diversified application palette cushions overall consumption patterns, making the Maplitho paper market less sensitive to single-use declines.

By Distribution Channel: Digital procurement accelerates transformation

Dealer networks retained 41.27% of 2024 supply thanks to relationship-oriented sales, local warehousing and credit terms tailored to SMEs. Many mid-size buyers appreciate bundled services such as on-site paper testing and printer maintenance advice offered by distributers. Nevertheless, digital platforms are outpacing legacy channels, clocking a 2.43% CAGR that demonstrates a lasting procurement realignment in the Maplitho paper market. E-catalogues and live inventory feeds let corporate buyers consolidate spending, reduce transaction costs and enforce internal sustainability checks. Large mills are partnering with e-commerce portals, embedding real-time production schedules so customers can lock in volumes months ahead.

Direct mill-to-customer agreements are tightening for high-specification grades where end users stipulate colour gamut, smoothness and stiffness thresholds. Such contracts often integrate just-in-time logistics and vendor-managed inventory, shifting working-capital burdens down the chain. Meanwhile, dealers defend relevance by diversifying into branded office supplies and offering same-day delivery within metro areas. Hybrid models are emerging in the Maplitho paper market where distributors operate white-label web stores synced to mill databases, blending service depth with digital efficiency. Competitive advantage thus stems from omnichannel agility rather than exclusive channel dominance.

Geography Analysis

Asia-Pacific held 43.62% of 2024 tonnage, anchored by China’s 121.05 million-tonne output and India’s network of more than 900 mills employing 1.5 million people The region’s integrated value chain, spanning plantation forestry to converting plants, compresses logistics costs and allows rapid grade switching to meet fast-rising literacy-driven volumes. Government incentives for energy-efficient machinery further elevate competitiveness, while mill clusters around coastal ports enable export flows to South Asia and the Middle East. Japan and South Korea maintain niche specialities in archival-grade Maplitho paper, using advanced coating-free smoothening technologies that fetch price premiums.

North America’s rationalised capacity now operates at healthier utilisation rates after 59 closures over the past decade. The resultant discipline stabilised prices and encouraged investments in inkjet-grade optimisation; Sylvamo expects another 10% capacity reduction by early 2025, which should keep supply in check. Producers channel freed capital toward automation and sustainability retrofits to comply with tightening water-discharge norms under EPA 40 CFR Part 430. Demand steadies around premium office, legal and packaging grades, indicating that the region remains profitable despite low overall growth.

Europe grapples with digital substitution and stricter climate mandates, epitomised by UPM’s decision to shutter its Ettringen mill, removing 270,000 tonnes of uncoated mechanical capacity by July 2025. Yet European mills lead in renewable-energy integration and closed-loop water systems, traits that appeal to environmentally conscious buyers. The Middle East and Africa, forecast at a 2.56% CAGR, gains from government education drives and large-scale infrastructure projects requiring administrative paperwork. South America experiences moderate growth tied to textbook procurement and commercial printing, with Brazil investing in literacy campaigns that propel incremental Maplitho paper market demand.

Competitive Landscape

The Maplitho paper market exhibits moderate concentration, with the top five producers controlling an estimated 55–60% of global tonnage. International Paper allocates USD 1.2 billion in 2025 capex to debottleneck premium uncoated lines and enhance energy efficiency . UPM and Stora Enso prioritise fibre-based alternatives to plastics, using lignin-barrier technologies that open adjacencies in food service packaging. [2]“Stora Enso Interim Report Q1 2025,” Stora Enso, storaenso.comThese moves align with the sector’s broader pivot toward margin-accretive segments less exposed to transactional printing decline.

Asian leaders such as Nine Dragons and APP leverage low labour costs and integrated forestry assets to supply both domestic classrooms and export markets. Regional competitors JK Paper and ITC focus on brand recognition and wide distribution to cater to India’s fragmented downstream converters .[3]"ITC Stand-alone Financial Results Q4 FY2024,” ITC Limited, itcportal.com .High-speed inkjet compatibility is now a key differentiator; mills that can guarantee run-ability win multi-year contracts from variable-data printers seeking waste reduction. Capital intensity and stringent effluent rules form formidable entry barriers, but niche entrants exploring bamboo or bagasse fibres pose a small disruptive threat.

Strategic actions in 2024–2025 show consolidation momentum. International Paper’s combination with DS Smith extends its reach into European sustainable packaging, while Sylvamo exited a North American supply agreement to streamline operations and focus on value-added grades. UPM’s Uruguay pulp mill ramp-up underpins backward integration, giving cost control at times of pulp volatility. Stora Enso’s new board line in Finland underscores a tilt toward multi-layer packaging substrates that share process similarities with heavier Maplitho paper grades, illustrating portfolio adjacency benefits.

Maplitho Paper Industry Leaders

-

International Paper Company

-

UPM-Kymmene Corporation

-

Stora Enso Oyj

-

Mondi plc

-

Nippon Paper Industries Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: UPM-Kymmene confirmed closure of its Ettringen mill, removing 270,000 tonnes of capacity and optimising the European production base.

- February 2025: Stora Enso reported EUR 2,362 million Q1 sales and higher EBIT, supported by ramp-up of its consumer board line in Oulu, Finland.

- January 2025: International Paper finalised its business combination with DS Smith, broadening sustainable packaging capabilities in North America and Europe.

- January 2025: Sylvamo noted improved pricing after a 10% reduction in North American uncoated freesheet capacity and ended a supply agreement to sharpen its focus on core mills.

Global Maplitho Paper Market Report Scope

| 40-60 GSM |

| 61-80 GSM |

| 81-120 GSM |

| >120 GSM |

| Publishing and Commercial Printing |

| Office Printing and Photocopiers |

| Stationery and Notebooks |

| Packaging Inserts and Manuals |

| Others |

| Direct (Mill to End-user) |

| Dealers and Distributors |

| Online / E-Commerce |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Basis Weight | 40-60 GSM | ||

| 61-80 GSM | |||

| 81-120 GSM | |||

| >120 GSM | |||

| By End-use Application | Publishing and Commercial Printing | ||

| Office Printing and Photocopiers | |||

| Stationery and Notebooks | |||

| Packaging Inserts and Manuals | |||

| Others | |||

| By Distribution Channel | Direct (Mill to End-user) | ||

| Dealers and Distributors | |||

| Online / E-Commerce | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Maplitho paper market in 2025?

The Maplitho paper market size is 63.25 million tonnes in 2025.

Which region leads consumption of Maplitho paper?

Asia-Pacific accounts for 43.62% of global volume, supported by large-scale production centres in China and India.

What basis-weight segment is growing fastest?

Grades above 120 GSM are forecast to rise at 2.32% CAGR through 2030 due to premium packaging and high-quality print demand.

Why are online channels important to Maplitho paper procurement?

E-commerce platforms deliver pricing transparency and inventory visibility, helping the channel grow at 2.43% CAGR.

What is the main restraint on future Maplitho paper demand?

Accelerating digitalisation, including e-billing and electronic document workflows, is projected to reduce overall CAGR by 0.8%.

How are pulp price swings affecting producers?

A 5.4% year-on-year rise in the wood-pulp price index during 2025 tightened margins, driving mills to seek vertical integration or hedging strategies.

Page last updated on: