Paper Honeycomb Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.27 Billion |

| Market Size (2031) | USD 6.77 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

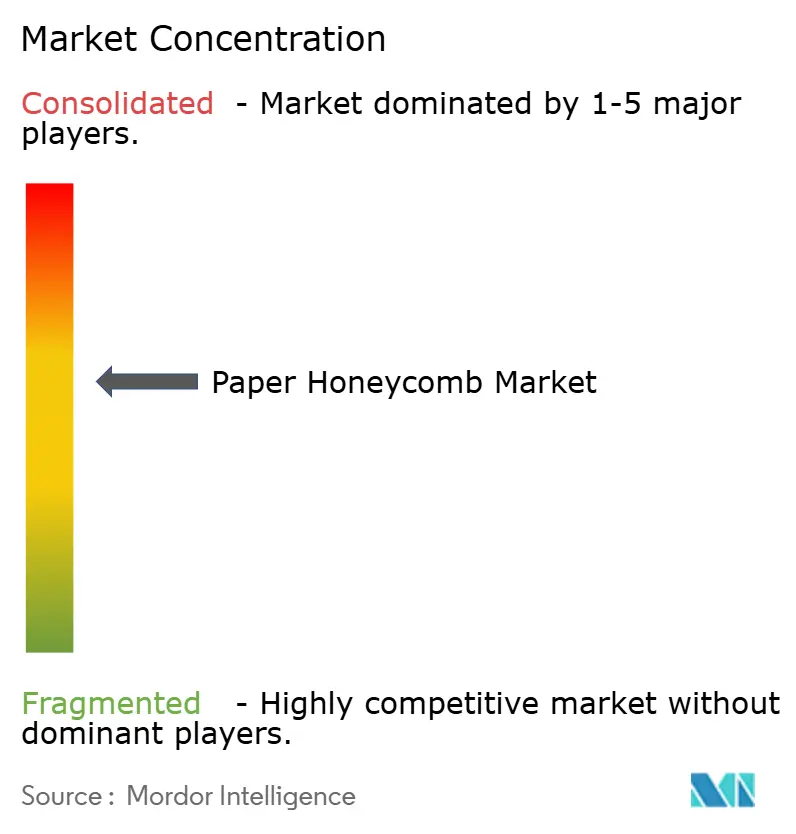

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Honeycomb Market Analysis by Mordor Intelligence

Paper Honeycomb Market size in 2026 is estimated at USD 5.27 billion, growing from 2025 value of USD 5.01 billion with 2031 projections showing USD 6.77 billion, growing at 5.14% CAGR over 2026-2031. Momentum reflects brand owners’ pivot to fiber-based formats under tightening packaging rules and corporate net-zero targets. Rising parcel volumes, automotive lightweighting programs, and accelerating single-use-plastic phase-outs collectively reinforce a healthy demand baseline. Automation in core production lines is lowering unit costs, supporting wider adoption in price-sensitive end-markets. Meanwhile, specialty barrier coatings are unlocking humidity-resistant applications that were once the domain of polymer foams. Consolidation—exemplified by Smurfit Kappa’s USD 11.2 billion merger with WestRock—signals the need for scale economies and global reach as sustainability moves to the center of procurement decisions.

Key Report Takeaways

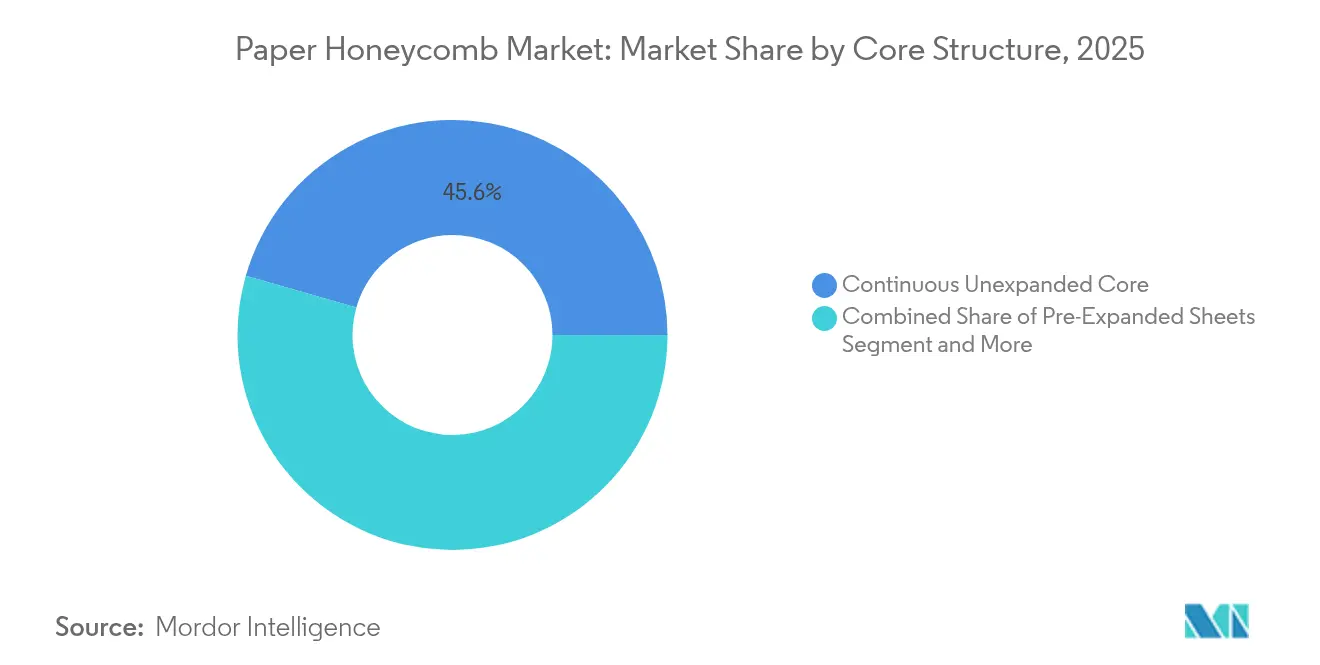

- By core structure, continuous unexpanded cores led with 45.55% of paper honeycomb market share in 2025, while micro-honeycomb cores are projected to grow at a 6.79% CAGR through 2031.

- By cell size, the 10-20 mm band accounted for 39.05% of the paper honeycomb market size in 2025; the 20-30 mm segment is forecast to expand at a 6.55% CAGR.

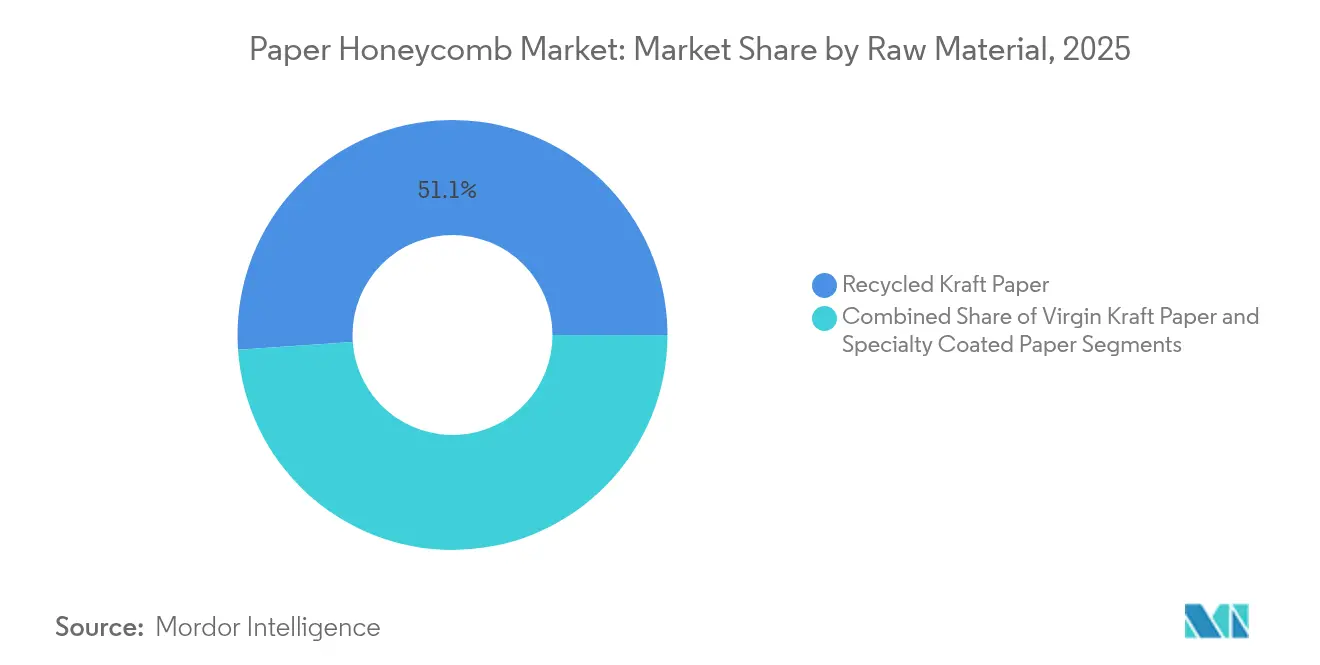

- By raw material, recycled kraft paper captured 51.10% of the paper honeycomb market share in 2025, whereas specialty coated paper is advancing at a 6.74% CAGR.

- By application, protective packaging represented 39.15% of the paper honeycomb market size in 2025; automotive components are growing fastest at 6.52% CAGR.

- By end-user industry, food and beverage held 30.15% revenue share in 2025, while automotive is projected to rise at a 6.35% CAGR to 2031.

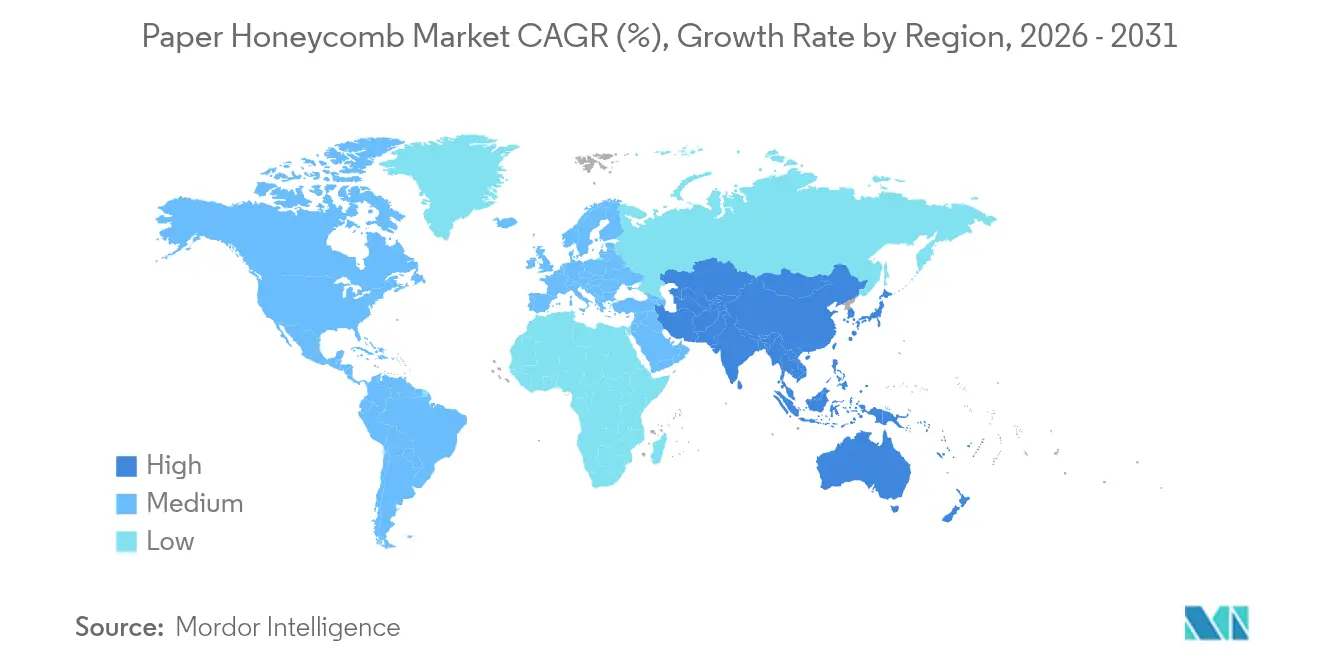

- By geography, Europe dominated with a 38.25% share in 2025; Asia-Pacific is set to register a 6.81% CAGR, the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paper Honeycomb Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-driven demand for lightweight packaging | +1.8% | Europe, North America, Global firms | Long term (≥ 4 years) |

| Explosive growth of global e-commerce parcel volumes | +1.5% | Asia-Pacific, North America, Global | Medium term (2-4 years) |

| Cost advantage vs. wood and polymer inserts | +0.9% | Emerging markets, Global | Short term (≤ 2 years) |

| Automation of honeycomb core production lines | +0.7% | North America, Europe, Developed Asia-Pacific | Medium term (2-4 years) |

| Commercialisation of micro-cell cores for electronics | +0.4% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Single-use-plastic bans accelerating void-fill substitution | +0.3% | Europe, Select US states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustainability-driven demand for lightweight packaging

Global brands view honeycomb cores as an immediate route to carbon and freight-weight reduction. Mercedes-Benz achieved 15–20% component weight cuts by embedding bionic honeycomb structures, directly supporting its 2039 carbon-neutral goal. [1]Mercedes-Benz Group, “Bionic Design: Inspired by Nature,” group.mercedes-benz.com Similar programs at DS Smith removed more than 1.2 billion plastic units from customer supply chains in 2024, confirming that fiber-based substitutes are now a procurement default for many FMCG players. Because scope 3 emissions reporting becomes mandatory across the EU and key US states after 2025, demand for verifiable low-impact packaging is expected to strengthen, particularly in automotive, appliance, and electronics verticals. Improved strength-to-weight ratios and compatibility with automated packing lines widen the addressable market beyond traditional void fill, providing a durable pull factor through 2030.

Explosive growth of global e-commerce parcel volumes

Fulfillment giants are rewriting packaging specifications to align protection, cost, and recyclability. Amazon replaced 95% of plastic air pillows in its US network with paper fillers made from 100% recycled content, eliminating nearly 15 billion plastic units annually. [2]CNBC, “Amazon’s Ditching the Plastic Air Pillows in Its Boxes,” cnbc.com The move prompted parallel conversions across leading marketplaces in Asia-Pacific and Europe, spurring suppliers to develop right-sized, curb-side-recyclable formats. Honeycomb-based padded mailers now meet drop-test and machinability standards, opening a premium avenue for small electronics and cosmetics. Temperature-controlled variants, integrating phase-change materials within the honeycomb grid, are gaining acceptance for pharmaceuticals and meal kits as cold-chain e-commerce scales.

Cost advantage vs. wood and polymer protective inserts

Honeycomb structures deliver compelling logistics savings, often cutting finished-pack weight by 30–50% compared with plywood or foam inserts. BASF’s roof-module trial for compact cars demonstrated a 30% weight reduction, converting directly to lower material spend and improved fuel economy in legacy ICE fleets as well as range extension for EVs. Producers are standardising thickness at 30 mm and automating slitting and gluing to achieve outputs above 1.7 t/hour, reducing labor intensity and allowing localised production. End-of-life recyclability further lowers the total cost of ownership as landfill levies rise, tipping procurement models in favor of paper honeycomb across construction, appliance, and furniture sectors.

Automation of honeycomb core production lines

Licensing of ThermHex continuous-forming technology enables high-speed, single-step production of consistent cores, cutting waste and reducing capital per output unit. Japanese tier-1 supplier Kotobukiya Fronte adopted the platform to produce M-Light interior panels, underscoring the automotive industry’s appetite for automated, thin-gauge cores. Advanced 5-axis machining centers now trim stacked panels to net-shape with micron tolerance, ensuring repeatability for load-bearing parts. Real-time sensor arrays monitor glue application and cell expansion, driving yield improvement and faster QA sign-off. The result is a scalable capacity capable of meeting rapid spikes in e-commerce seasonality without sacrificing unit economics or quality consistency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of recycled kraft paper prices | −0.8% | North America, Europe, Global | Short term (≤ 2 years) |

| Moisture sensitivity in high-humidity supply chains | −0.5% | Asia-Pacific, Tropical regions | Medium term (2-4 years) |

| Limited global capacity of bio-adhesive suppliers | −0.3% | Premium applications, Global | Long term (≥ 4 years) |

| Absence of heavy-duty pallet compression standards | −0.2% | Emerging markets, Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility of recycled kraft paper prices

Fluctuating pulp costs pressure converters’ margins and complicate price quotes. Kraft pulp slid to 5,060 CNY/T in June 2025, a 14.7% year-on-year drop, yet spot volatility forces short hedging cycles, raising working-capital needs. With recycled fiber supply concentrated among a handful of North American and European mills, any outage is transmitted instantly to global roll prices. Currency swings further distort landed costs for firms operating multi-regional plants. Strategies such as backward integration, long-term offtake contracts, and substitution with alternative fibers are under exploration, although each requires considerable capital or R&D investment before risk is fully mitigated.

Moisture sensitivity in high-humidity supply chains

Elevated humidity degrades compressive strength and dimensional stability in uncoated honeycomb panels. Laboratory tests show critical stress values drop markedly as relative humidity rises, constraining usage in tropical lanes and electronics shipments without supplemental barriers. Specialty water-resistant coatings are growing at a 7.1% CAGR, but costs remain higher than standard kraft options. Desiccant integration and unit-load over-wrapping partly alleviate the issue, yet climate-controlled storage can reverse freight savings. Manufacturers, therefore, focus on developing bio-based barrier chemistries that maintain recyclability while raising moisture thresholds, a field likely to see commercial breakthroughs within five years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Core Structure: Micro-Cells Drive Innovation

The continuous unexpanded core segment contributed 45.55% to 2025 revenue, anchored by mature production infrastructure that favors high-volume protective packaging. Micro-honeycomb cores, though smaller in installed capacity, are posting a robust 6.79% CAGR as electronics and precision equipment suppliers demand tighter tolerances and higher energy absorption. Wider adoption in battery housings and instrument panels underscores their crossover potential. Cost parity with legacy foams is approaching as scaling and automation progress, positioning micro-cells as a future standard for premium e-commerce and automotive applications.

Second-generation production lines now deliver cell sizes below 10 mm without sacrificing tensile strength, enabling the integration of thermal management layers critical for semiconductor packaging. Samsung’s patent portfolio indicates growing interest in honeycomb-assisted heat dissipation for chip carriers, pointing to downstream demand beyond traditional box-in-box shipping. As a result, the paper honeycomb market expects micro-cell penetration to accelerate after 2026, especially once adhesive supply constraints ease.

By Cell Size: Precision Applications Accelerate Growth

In 2025, the 10-20 mm cell size bracket represented 39.05% of value, offering the sweet-spot balance between cushioning and material usage. Demand from large consumer-electronics shippers and furniture OEMs keeps this band dominant. The adjacent 20-30 mm tier is forecast to climb at a 6.55% CAGR, paced by automotive interiors and appliance side-walls. Meanwhile, sub-10 mm formats are carving niche roles in wearables and high-value micro-electronics shipping, where vibration dampening and exact fit override cost concerns.

Modeling software now lets designers specify mixed cell architectures within one panel, improving localized energy absorption without bulk weight gains. Such versatility supports emerging omnichannel supply chains that use a single pack design for retail, direct-to-consumer, and return logistics. Consequently, the paper honeycomb market sees cell-size diversification as a route to margin expansion for converters with advanced design capabilities.

By Raw Material: Specialty Coatings Enable Premium Applications

Recycled kraft paper remains the backbone, capturing 51.10% share. Ready availability, consumer recognition, and compatibility with standard municipal recycling streams keep it the default grade for mainstream applications. Specialty coated papers, though smaller in volume, are expanding 6.74% annually as they solve moisture and grease challenges in food, pharmaceutical, and tropical logistics chains. Virgin Kraft maintains a foothold where maximum burst strength trumps cost, notably in industrial equipment crating.

Coating innovation is vibrant. Bio-polymer barriers now rival petroleum-based films in resistance while preserving repulpability, aligning with upcoming EU recyclability criteria effective 2027. The paper honeycomb market size for coated substrates is projected to cross USD 1.08 billion by 2031, reflecting both functional upgrades and shifting brand owner procurement policies toward higher-performing papers.

By Application: Automotive Components Lead Growth

Protective packaging stood at 39.15% market contribution in 2025, underpinned by e-commerce scale and industrial spare-part flows. Automotive components, at a 6.52% CAGR, outrank all others as OEMs chase fleet-wide weight cuts. Honeycomb door inners, parcel shelves, and battery trays are moving from pilot to mass production, aided by continuous-laminate processes that bond decorative skins inline.

Crash-energy absorption and thermal insulation are dual benefits propelling adoption in EV platforms. The paper honeycomb industry now supplies multi-layer sandwich solutions that meet automaker flame-spread and off-gassing standards, signaling deeper penetration. Furniture panels and pallets retain steady demand where cost and recyclability trump aesthetics, sustaining baseline volume even as premium segments accelerate.

By End-user Industry: Automotive Sector Transformation

Food and beverage users held a 30.15% slice in 2025, driven by the sector’s early embrace of recyclable secondary packaging under extended producer responsibility rules. Automotive, however, is rising fastest at 6.35% CAGR, reshaping order volumes toward higher-spec core structures. Electronics and appliance makers continue to require precision cushioning, while industrial goods benefit from pallets and dunnage that cut shipping weights.

E-commerce and retail channels constitute a cross-cutting demand layer as omnichannel brands harmonize pack designs. The increasing availability of small-cell mailers and lined cartons tailored for parcel-carrier sortation underscores this evolution. Collectively, these patterns keep the paper honeycomb market on a diversified growth path, reducing dependence on any single vertical.

Geography Analysis

Europe’s 38.25% share in 2025 reflects decades of policy support for fiber-based packaging. Germany and the United Kingdom spearhead adoption through aggressive single-use plastic bans and strong automotive export bases that consume high-performance honeycomb parts. France and Italy extend demand through luxury‐goods logistics, while Eastern Europe gains as multinationals relocate assembly lines eastward. The bloc’s 2050 carbon-neutral roadmap ensures structural demand tailwinds as brand owners align with mandatory recyclability and recycled-content thresholds.

Asia-Pacific is the fastest-growing region at 6.81% CAGR, underpinned by China’s scale, India’s manufacturing expansion, and Japan’s advanced vehicle sector. Chinese converters such as Suzhou Beecore are adding high-speed lines, boosting regional self-sufficiency, and lowering export freight costs. India’s push for domestic electronics assembly and e-commerce penetration positions it as the next mass-volume growth node. South Korea benefits from semiconductor exports requiring precision honeycomb cushioning, while ASEAN nations leverage low labor costs to attract panel and pallet production investments. Government-led bans on polystyrene food packaging across the region further reinforce conversion momentum.

North America harnesses explosive parcel growth and an accelerated EV transition. Packaging Corporation of America reported record quarterly revenue in 2025, citing strong corrugated and honeycomb shipments to e-commerce and auto accounts. Amazon’s paper-forward packaging policy galvanizes the supply base, while Mexico’s near-shoring trend attracts new honeycomb plants to serve US customers with reduced lead times. Canada’s forest product surplus supports domestic kraft supply, partially buffering regional input cost volatility.

Competitive Landscape

The paper honeycomb market remains moderately fragmented yet is moving toward greater concentration. Smurfit Westrock’s formation created a USD 34 billion revenue giant capable of integrated board-to-box supply. DS Smith’s USD 7.8 billion merger with International Paper gives the combined entity a powerful North Atlantic footprint. [4]DS Smith, “RNS Statements,” dssmith.com These tie-ups aim to capture procurement synergies, shared R&D, and unified customer contracts at a multiregional scale.

Technology licensing is another competitive lever. EconCore’s ThermHex process, adopted by Kotobukiya Fronte, highlights how proprietary continuous forming creates durable differentiation in automotive supply. Patent filings increasingly target micro-cell geometries and moisture-resistant chemistries, suggesting IP barriers may rise. Meanwhile, mid-tier converters invest in digital design suites and quick-set adhesive systems to service short lead-time e-commerce accounts. Overall, competition revolves around scale, automation, and functional upgrades rather than raw production volume alone.

Private-equity interest is notable as investors seek circular-economy assets with tangible ESG credentials. Several regional converters in Asia-Pacific and Europe are reported acquisition targets, aligning with global groups’ expansion and integration agendas. Cost leadership through local raw-paper sourcing and renewable-energy-powered mills is expected to distinguish winners in a market where downstream brands increasingly audit scope 3 emissions.

Paper Honeycomb Industry Leaders

Smurfit Kappa Group plc

DS Smith plc

Packaging Corporation of America – Hexacomb

Honicel Group B.V.

Grigeo AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smurfit Westrock reported Q1 2025 net sales of USD 7.66 billion and net income of USD 382 million, confirming post-merger performance momentum.

- April 2025: Packaging Corporation of America posted a record USD 2.14 billion in Q1 2025 revenue, up 38.7% versus 2024, driven by higher prices and volumes in packaging.

- January 2025: International Paper and DS Smith finalized their merger, targeting at least USD 514 million in annual pre-tax cash synergies.

- July 2024: Smurfit Kappa completed its USD 11.2 billion merger with WestRock, creating a global sustainable-packaging leader.

Global Paper Honeycomb Market Report Scope

Paper honeycomb packaging is a sustainable and lightweight material used for protective packaging. It consists of a series of hexagonal cells made from paper, resembling the structure of a honeycomb, which is why it is called a paper honeycomb. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The paper honeycomb packaging market is segmented by core (Continuous Unexpanded Core, and Pre-Expanded Sheets), by end- user industry (Automotive, Food and Beverages, Electronics, Household Appliances, and Other End-User Industries) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Continuous Unexpanded Core |

| Pre-Expanded Sheets |

| Corrugated-Edge Core |

| Micro-Honeycomb Core |

| ≤ 10 mm |

| 10 – 20 mm |

| 20 – 30 mm |

| > 30 mm |

| Recycled Kraft Paper |

| Virgin Kraft Paper |

| Specialty Coated Paper |

| Protective Packaging |

| Pallet and Dunnage |

| Furniture and Interior Panels |

| Automotive Components |

| Door and Partition Panels |

| Other Applications |

| Automotive |

| Food and Beverage |

| Electronics |

| Home Appliances |

| Industrial Goods |

| E-commerce and Retail |

| Furniture and Interior Design |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Core Structure | Continuous Unexpanded Core | ||

| Pre-Expanded Sheets | |||

| Corrugated-Edge Core | |||

| Micro-Honeycomb Core | |||

| By Cell Size | ≤ 10 mm | ||

| 10 – 20 mm | |||

| 20 – 30 mm | |||

| > 30 mm | |||

| By Raw Material | Recycled Kraft Paper | ||

| Virgin Kraft Paper | |||

| Specialty Coated Paper | |||

| By Application | Protective Packaging | ||

| Pallet and Dunnage | |||

| Furniture and Interior Panels | |||

| Automotive Components | |||

| Door and Partition Panels | |||

| Other Applications | |||

| By End-user Industry | Automotive | ||

| Food and Beverage | |||

| Electronics | |||

| Home Appliances | |||

| Industrial Goods | |||

| E-commerce and Retail | |||

| Furniture and Interior Design | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the paper honeycomb market?

The paper honeycomb market is valued at USD 5.27 billion in 2026 and is forecast to reach USD 6.77 billion by 2031 at a 5.14% CAGR.

Which region leads the paper honeycomb market in 2025?

Europe holds the lead with a 38.25% revenue share, supported by strict single-use-plastic bans and established recycling infrastructure.

Which application is expanding fastest within the paper honeycomb market?

Automotive components are growing quickest at a 6.52% CAGR as EV platforms demand lightweight, recyclable structural parts.

How have mergers affected competitive dynamics?

Large mergers such as Smurfit Kappa with WestRock and DS Smith with International Paper have raised concentration and accelerated technology investment across the sector.

What are the main restraints on growth?

Input-cost volatility for recycled kraft paper and moisture sensitivity in humid supply chains collectively shave roughly 1.3 percentage points off the market’s potential CAGR.

How does automation influence the industry outlook?

Automated ThermHex and 5-axis machining lines cut costs and improve quality, enabling converters to meet rising e-commerce and automotive demand while sustaining margins.

Page last updated on: