Copier Paper Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

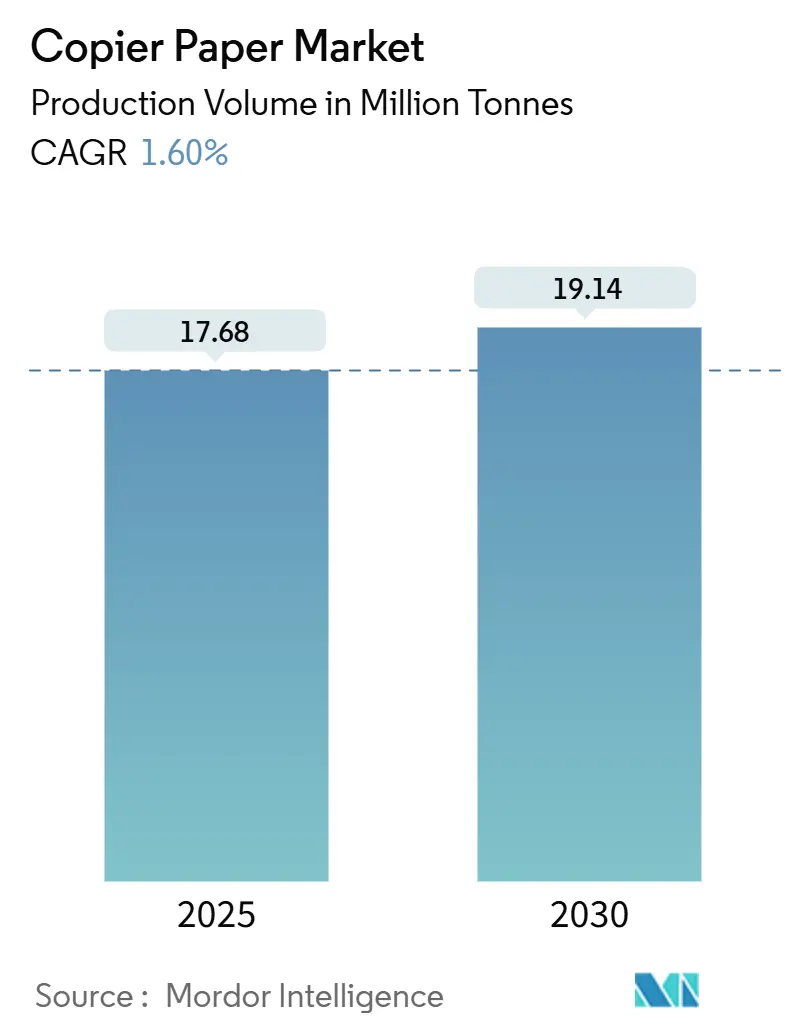

| Market Volume (2025) | 17.68 Million tonnes |

| Market Volume (2030) | 19.14 Million tonnes |

| Growth Rate (2025 - 2030) | 1.60% CAGR |

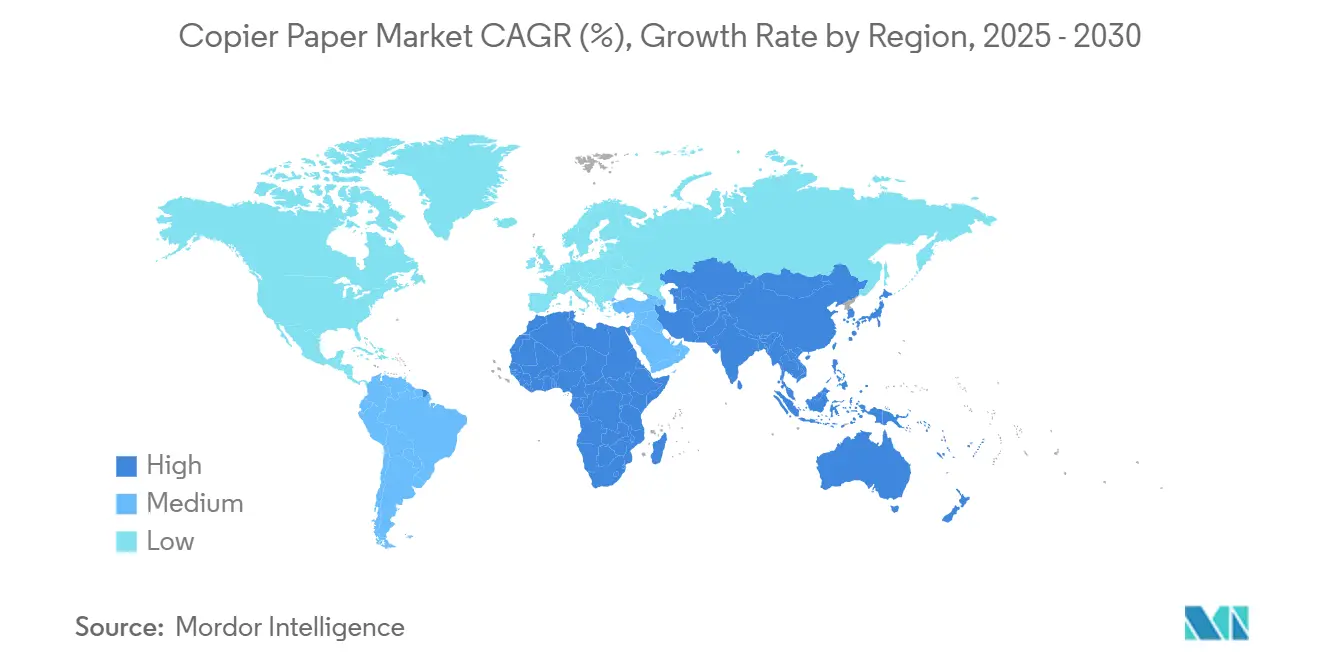

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Copier Paper Market Analysis by Mordor Intelligence

The copier paper market size sits at 17.68 million tonnes in 2025 and is projected to reach 19.14 million tonnes by 2030, reflecting a measured 1.60% CAGR over the forecast horizon. Sustained demand from office and education printing underpins baseline tonnage even as corporate digitization advances, while Asia-Pacific’s 40.15% share anchors global consumption thanks to large installed printer fleets and expanding middle-class documentation needs. [1]National Bureau of Statistics of China, “Statistical Communiqué of the People’s Republic of China on the 2024 National Economic and Social Development,” stats.gov.cn Middle East and Africa provides the fastest regional upside at 2.51% CAGR, buoyed by urban business formation and government exam printing mandates. Virgin wood pulp remains the dominant raw material at 62.73% share, yet recycled fiber volumes accelerate in response to tightening sustainability rules in the European Union and North America. Competitive dynamics stay intense as integrated producers optimise capacity and elevate sustainability credentials to defend margins in this commodity-driven copier paper market.

Key Report Takeaways

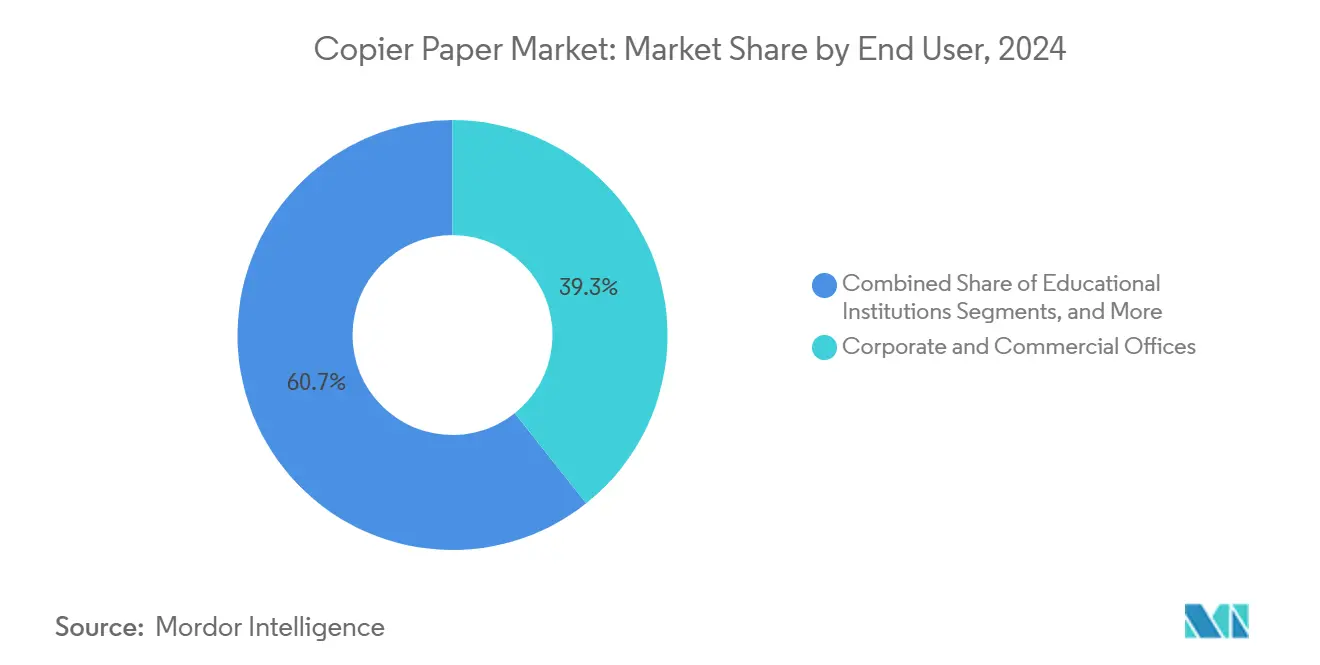

- By end user, the corporate and commercial offices segment accounted for 39.31% of the copier paper market size in 2024.

- By raw material, the copier paper market size for recycled fiber is projected to grow at a 2.46% CAGR between 2025-2030.

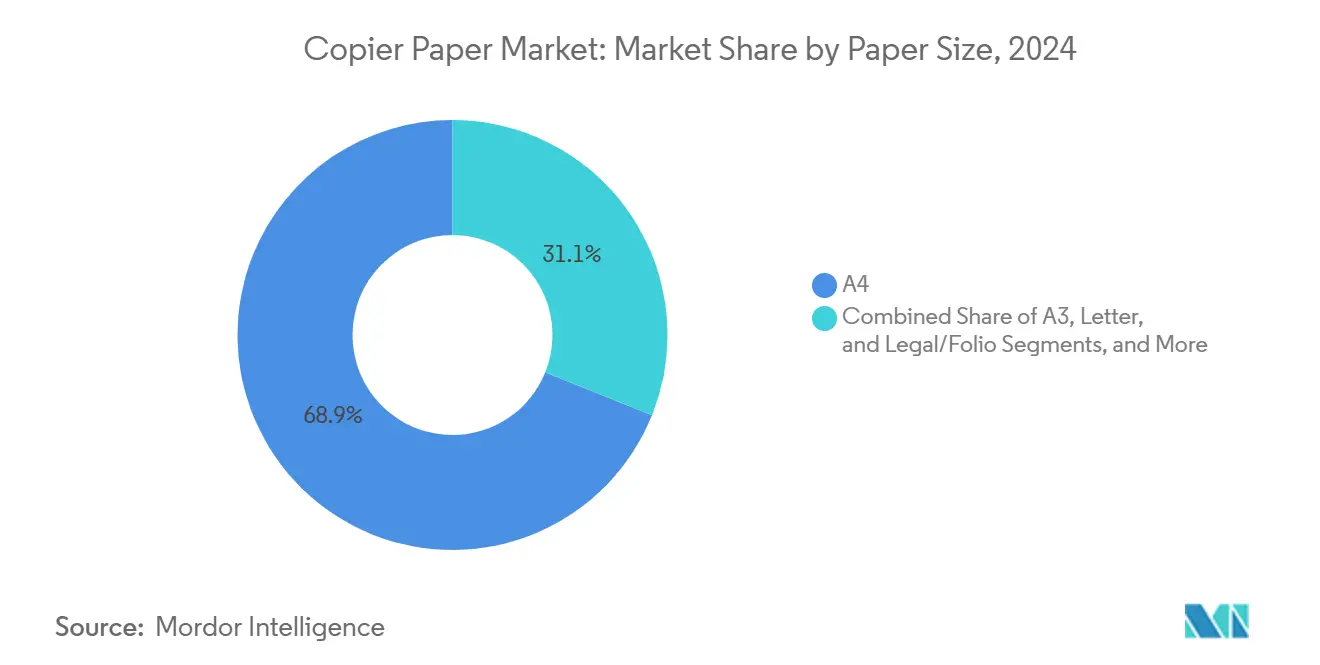

- By paper size, the A4 format segment captured 68.92% of the copier paper market share in 2024.

- By distribution channel, the copier paper market size for stationery retail stores is projected to grow at a 2.27% CAGR between 2025-2030.

- By basis weight, the 75–80 GSM segment commanded 35.67% of the copier paper market share in 2024.

- By geography, the copier paper market size for Middle East and Africa region is projected to grow at a 2.51% CAGR between 2025-2030.

Global Copier Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in office and education printing | +0.4% | Global with APAC and North America focus | Medium term (2-4 years) |

| Rapid urban middle-class expansion in APAC | +0.3% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Government exam and form printing mandates | +0.2% | India, China, Brazil, selective Africa | Short term (≤ 2 years) |

| Brand-driven premium A4 demand in Africa | +0.2% | Sub-Saharan and North Africa | Medium term (2-4 years) |

| High-speed inkjet-compatible cut-sheet launches | +0.2% | North America and EU, extending to APAC | Short term (≤ 2 years) |

| Reshoring after anti-dumping tariffs | +0.1% | North America, Australia, selective EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in office and education printing

Post-pandemic hybrid work patterns have stabilised around three to four in-office days per week, lifting run-rates on shared printers in corporate campuses. School systems have returned to in-person learning, and standardised testing regimes in China and India now schedule larger examination cohorts than before 2020, directly translating into higher sheet counts. Financial services and healthcare keep hard-copy records to satisfy compliance audits, ensuring baseline bulk orders for uncoated freesheet. Companies weigh the cost of digital transformation against familiar paper-based workflows, sustaining incremental copier paper market tonnage. Where remote printing is necessary, employees often print at the office during scheduled days, reinforcing the physical documentation cycle.

Rapid urban middle-class expansion in APAC

China’s labour productivity climbed 4.9% in 2024, signalling stronger purchasing power across tier-2 and tier-3 cities. Newly formed urban households outfit home offices with compact printers, creating fresh demand nodes for the copier paper market. India’s similar urbanisation path fuels parallel growth as service-sector employment rises and home-based tutoring and small businesses proliferate. Regulatory traditions that favour stamped physical contracts further uphold paper usage even among tech-savvy professionals. Local mills scale capacity to meet the dispersed demand, leveraging short haul logistics advantages and contributing steady volume to regional totals.

Government exam and form printing mandates

Education ministries in India and China still specify paper-based testing for high-stakes exams, making annual sheet consumption highly predictable. [2]Victorian Government, “Victorian Government Paper Procurement Guide,” buyingfor.vic.gov.au Administrative forms for business registration, tax filings and licensing also demand physical submission in many emerging economies due to limited digital infrastructure. Government procurement guidelines now prioritise FSC- or PEFC-certified sheets, linking sustainability credentials to eligibility but not reducing absolute tonnage. As bureaucratic processes expand alongside formal economies, each new official form requirement compounds baseline demand for the copier paper market. Short-lead tenders often favour local mills, boosting domestic production runs.

Brand-driven premium A4 demand in Africa

Business formalisation across Nigeria, Kenya and South Africa elevates expectations for crisp, bright documents that convey professionalism. Financial advisers and legal practices request branded reams that resist jamming and support duplex printing, moving purchases away from unbranded economy grades. Import substitution policies reward regional converters that can match international quality, opening premium niches for suppliers from Egypt and Morocco. Multinational corporations extend global stationery standards to African subsidiaries, reinforcing the transition to reputable labels. Universities and private schools increasingly specify premium paper for official transcripts and examination scripts, locking in repeat orders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate digitization and paper-less workflows | -0.5% | Global, led by North America and EU | Medium term (2-4 years) |

| Stringent sustainability regulations | -0.4% | EU, expanding to North America and APAC | Long term (≥ 4 years) |

| Managed Print Services reducing page-volumes | -0.2% | North America and EU corporate markets | Short term (≤ 2 years) |

| Blockchain-based e-invoicing mandates | -0.2% | EU, India, Brazil selective uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corporate digitization and paper-less workflows

Cloud repositories, e-signature platforms and integrated ERP modules now allow multi-department document routing without hard copies. DocuSign alone claims 93 billion sheets saved, a headline figure that illustrates how quickly digital substitutes can outstrip physical outputs. Boards push sustainability scorecards that tie executive pay to resource utilisation, sharpening focus on pages per employee. Hybrid meetings rely on shared screens, further marginalising printed decks. High adoption rates in banking and insurance demonstrate material substitution potential and the negative 0.5% pull on the copier paper market CAGR.

Stringent sustainability regulations

Regulation (EU) 2024/1781 establishes eco-design requirements that raise compliance costs for virgin pulp mills by demanding recyclability and traceability across the product lifecycle. [3]European Parliament and Council, “Regulation (EU) 2024/1781 Establishing Eco-design Requirements for Sustainable Products,” eur-lex.europa.eu Packaging rules add minimum recycled-content thresholds, pressuring uncoated freesheet producers to re-engineer furnish mixes or face restricted market access. Carbon pricing frameworks in the EU and Canada inflate energy bills, eroding cost advantage for integrated pulp-and-paper complexes. Buyers embed Scope 3 emission criteria into tenders, prompting some to substitute electronic workflows entirely. These overlapping mandates collectively remove 0.4% from the copier paper market’s prospective CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Paper Size: A4 Standardisation Strengthens Global Cohesion

A4 sheets accounted for 68.92% of copier paper market share in 2024 and are expected to grow at 2.14% CAGR, reinforcing their position as the global default for contractual and administrative documents. Multinational companies insist on uniform size across subsidiaries, reducing storage complexity and easing archival scanning workflows, which keeps re-order intervals predictable. Letter size remains significant in the United States but converging trade documentation practices motivate gradual switching, especially among exporters that must satisfy overseas customs paperwork.

ISO 216 compliance also simplifies printer design, enabling OEMs to standardise feed mechanisms worldwide. Public sector digitisation projects still print legacy forms originally laid out in A4, so the format stays entrenched even during workflow upgrades. The copier paper market benefits from this inertia, with large mill trim widths optimised for A4 ream production. Procurement managers cite fewer misfeeds and easier duplex alignment as extra reasons for staying with the format, reinforcing a virtuous cycle of demand.

By Basis Weight: Lightweight Grades Gain Cost-Efficiency Traction

The 75-80 GSM band held a 35.67% share of the copier paper market in 2024, balancing rigidity with postal savings. Yet the ≤75 GSM category is accelerating at 2.23% CAGR as mills improve formation and opacity, allowing users to trim logistics spend without sacrificing legibility. Large corporations have begun to shift internal print policies to 70 GSM for drafts and inter-office memos, replicating the practice once limited to Asia.

Marketing teams, however, still favour 80–90 GSM for outward-facing presentations where tactile quality influences client perception. Design studios deploy >90 GSM when colour density and lay-flat properties matter. Such stratification helps the copier paper market capture price-tier diversity even while average grammage edges downward. Producers use lighter grades to hedge against pulp cost spikes, maximising machine speed and yield per tonne of furnish.

By Raw Material: Recycled Fiber Narrows Performance Gap

Virgin wood pulp retained 62.73% copier paper market share in 2024 but faces rising substitution as recycled fiber grows at 2.46% CAGR under stricter procurement rules. European mills advertise carbon footprints 20–30% lower for recycled sheets, winning bids from multinationals seeking emissions credits. Investment in de-inked pulp lines improves brightness and runnability, bringing recycled grades closer to virgin benchmarks.

Premium legal firms still specify virgin pulp for archival permanence, yet mixed-source offerings now meet many mainstream office criteria. The copier paper market thus evolves into a dual-sourcing arena, allowing buyers to toggle between cost stability and environmental targets. Integrated producers hedge by operating both virgin and recycled assets to maintain customer stickiness.

By End User: Outsourcing Shifts Pages to Print-for-Pay Hubs

Corporate and commercial offices delivered 39.31% of copier paper market size in 2024, reflecting their central role in daily transactional printing. Gradual rationalisation of in-house fleets pushes non-core jobs toward external copy shops, which explains the segment’s 2.38% CAGR through 2030. Universities and schools anchor a stable education block focused on exam scripts and course packs resistant to online-only formats.

Government departments preserve steady intake through legally mandated archives and notarised records. Remote work trends redistribute some volume to home offices, but bulk purchases still flow through employer-led ordering portals. Consequently, the copier paper market sustains a multipolar demand structure where different end users compensate for each other’s cyclical swings.

By Distribution Channel: Retail Footfalls Echo Small-Business Momentum

B2B wholesalers controlled 42.38% of copier paper market size during 2024, servicing contractual accounts with predictable monthly call-offs. Stationery retailers, however, achieve the highest 2.27% CAGR as start-ups and freelancers opt for on-demand reams instead of pallet lots. Online marketplaces marry the two approaches, offering bulk tiers with last-mile parcel convenience.

Lockbox subscriptions where SMEs receive predefined quantities each quarter gain popularity, smoothing revenue for both mills and merchants. Wholesale networks respond by bundling allied supplies such as toner, widening basket size to defend share. This dynamic keeps distribution diversity alive across the copier paper market, mitigating reliance on any single sales channel.

Geography Analysis

Asia-Pacific’s 40.15% share underscores its status as the demand nucleus, with China’s 5.0% GDP uplift and 5.3% secondary-industry expansion in 2024 directly reinforcing domestic sheet usage. India adds momentum through rising service-sector documentation and centralised exam printing that chains large tender volumes to local mills. Japan and South Korea hold steady demand as mature but quality-sensitive buyers, while Indonesia and Vietnam generate incremental volume via rapid SME formation.

North America trails as the second-largest copier paper market, balancing capacity withdrawals with robust niches in healthcare and legal sectors that resist digitisation. Mexico’s maquiladora zone spurs cross-border paperwork, cushioning regional decline rates. Reshoring trends after tariff regimes entice domestic converting investments that offset some import reliance, thereby sustaining internal supply loops.

Europe navigates tighter sustainability directives by pivoting toward recycled content and eco-labels, which permits price premiums that keep mills profitable despite tepid tonnage growth. [4]Mondi Group, “Interim Results Announcement 2024,” mondigroup.com Middle East and Africa registers the fastest 2.51% CAGR, driven by business formalisation, exam-centric education models and growing premium brand awareness among corporates. South America shows stable yet currency-sensitive purchasing, with Brazil’s sizable internal market balancing Argentina’s volatility.

Competitive Landscape

The copier paper market exhibits moderate concentration; the top five producers collectively account for roughly 55% of global tonnage, enabling scale economies without tipping into oligopoly. International Paper, Sylvamo and Mondi leverage integrated pulp sourcing and extensive logistics footprints to negotiate raw-material volatility while keeping service levels high. Capacity alignment strategies dominate boardroom agendas: UPM will shutter its Ettringen mill by July 2025, eliminating 270,000 tonnes that no longer match profitable demand nodes.

Sustainability branding differentiates suppliers despite product commoditisation. Mondi promotes cradle-to-cradle certification on its premium ranges, while Stora Enso’s 17.7% EBIT growth in Q1 2025 stems in part from price realisation on eco-labelled SKUs. Consolidation appetite rises as smaller independents struggle to finance decarbonisation upgrades; acquisition pipelines therefore focus on high-efficiency converters in growth geographies such as MEA.

Technological investments skew toward energy-efficient dryers and closed-loop water systems instead of exotic paper chemistries. Mills trial AI-driven quality monitoring to cut broke rates and free up machine speed for incremental tonnes. Recycled fiber specialists expand through contract networks with municipal collection agencies, positioning themselves for future regulatory quotas. Altogether, competitive positioning hinges on balancing asset optimisation, sustainability credentials and geographic diversification within the broader copier paper market.

Copier Paper Industry Leaders

International Paper Company

Asia Pulp and Paper (Sinarmas)

Domtar Corporation

APRIL Group (Royal Golden Eagle)

Chenming Paper

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: UPM Communication Papers confirmed the permanent closure of its Ettringen mill in Germany, removing 270,000 tonnes of uncoated mechanical paper capacity and affecting 235 positions.

- February 2025: Stora Enso posted Q1 2025 sales of EUR 2.362 billion (USD 2.755 billion) and 17.7% adjusted EBIT growth, marking a fourth consecutive quarter of improvement.

- December 2024: Billerud unveiled a SEK 1.4 billion (USD 0.15 billion) investment plan for its Escanaba and Quinnesec mills to enhance graphic and specialty paper capability.

- July 2024: Australia terminated a 25.5% anti-dumping duty on Indonesian A4 copy paper imports following judicial review.

Global Copier Paper Market Report Scope

| A4 |

| A3 |

| Letter |

| Legal/Folio |

| ≤75 GSM |

| 75–80 GSM |

| 80–90 GSM |

| >90 GSM |

| Virgin Wood Pulp |

| Recycled Fibre |

| Corporate and Commercial Offices |

| Educational Institutions |

| Government and Public Sector |

| Home and SOHO |

| Print-for-Pay / Copy Shops |

| Stationery/Retail Stores |

| B2B/Wholesale |

| Online Retail and E-procurement |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Paper Size | A4 | ||

| A3 | |||

| Letter | |||

| Legal/Folio | |||

| By Basis Weight (GSM) | ≤75 GSM | ||

| 75–80 GSM | |||

| 80–90 GSM | |||

| >90 GSM | |||

| By Raw Material | Virgin Wood Pulp | ||

| Recycled Fibre | |||

| By End User | Corporate and Commercial Offices | ||

| Educational Institutions | |||

| Government and Public Sector | |||

| Home and SOHO | |||

| Print-for-Pay / Copy Shops | |||

| By Distribution Channel | Stationery/Retail Stores | ||

| B2B/Wholesale | |||

| Online Retail and E-procurement | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the global shipment volume for copier paper in 2025?

The copier paper market size equals 17.68 million tonnes in 2025.

How quickly is demand expected to grow through 2030?

Total shipments are forecast to rise at a 1.60% CAGR, reaching 19.14 million tonnes by 2030.

Which region currently purchases the most copier paper?

Asia-Pacific holds 40.15% of global consumption, driven by China and India.

What raw material leads production today?

Virgin wood pulp provides 62.73% of 2024 supply, although recycled fiber is growing faster.

Who tops the list of leading manufacturers?

International Paper, Sylvamo and Mondi Group are among the largest integrated producers worldwide.

Which distribution channel is growing the fastest?

Stationery retail stores are expanding at a 2.27% CAGR as small offices and home offices favour direct purchases.

Page last updated on: