Paper Notebook Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

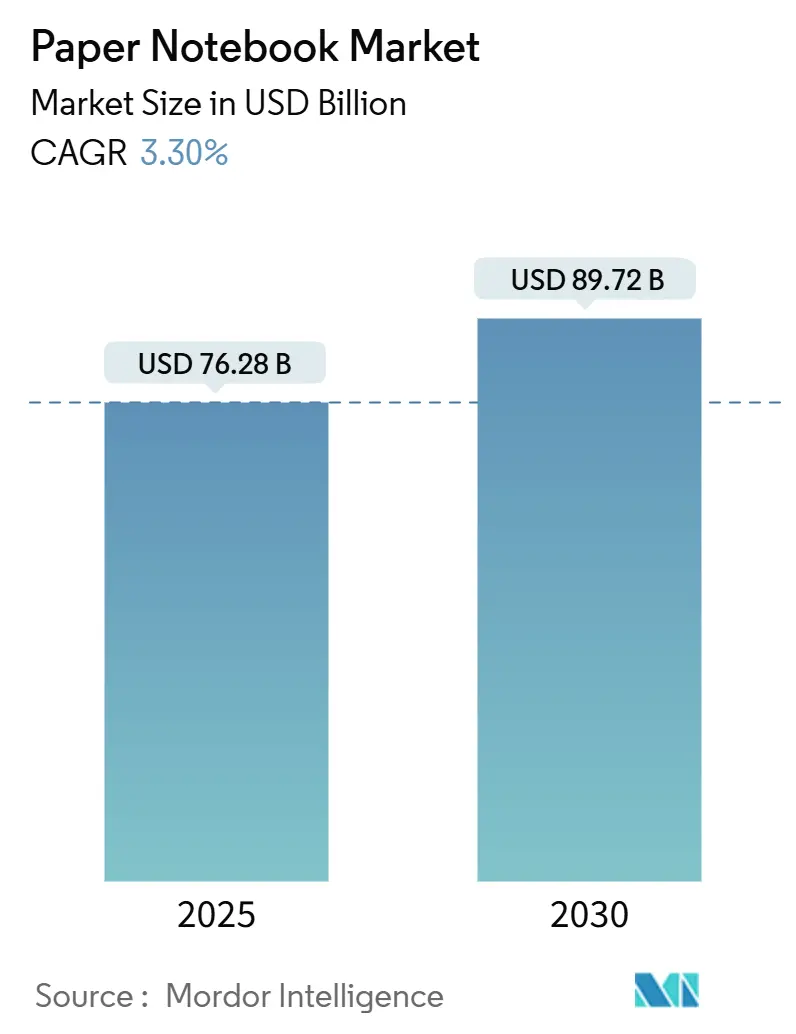

| Market Size (2025) | USD 76.28 Billion |

| Market Size (2030) | USD 89.72 Billion |

| Growth Rate (2025 - 2030) | 3.30% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Notebook Market Analysis by Mordor Intelligence

The paper notebook market size stands at USD 76.28 billion in 2025 and is projected to reach USD 89.72 billion by 2030, reflecting a 3.30% CAGR. This steady trajectory underscores the market’s ability to pivot toward premium offerings, sustainability-focused sourcing, and hybrid analog-digital formats that defend relevance despite mounting digital substitution. Absolute growth of USD 13.44 billion is fueled by resilient institutional demand, enduring consumer preference for handwriting’s cognitive benefits, and the emotional appeal of tactile planning tools. Strategic price-tier diversification shields manufacturers from raw-material volatility, while ESG-aligned innovations open premium pockets of demand. Intensifying competition in compact and specialty segments drives R&D around paper quality, binding durability, and cloud-enabled note capture, positioning leading brands to convert niche enthusiasm into mainstream adoption.

Key Report Takeaways

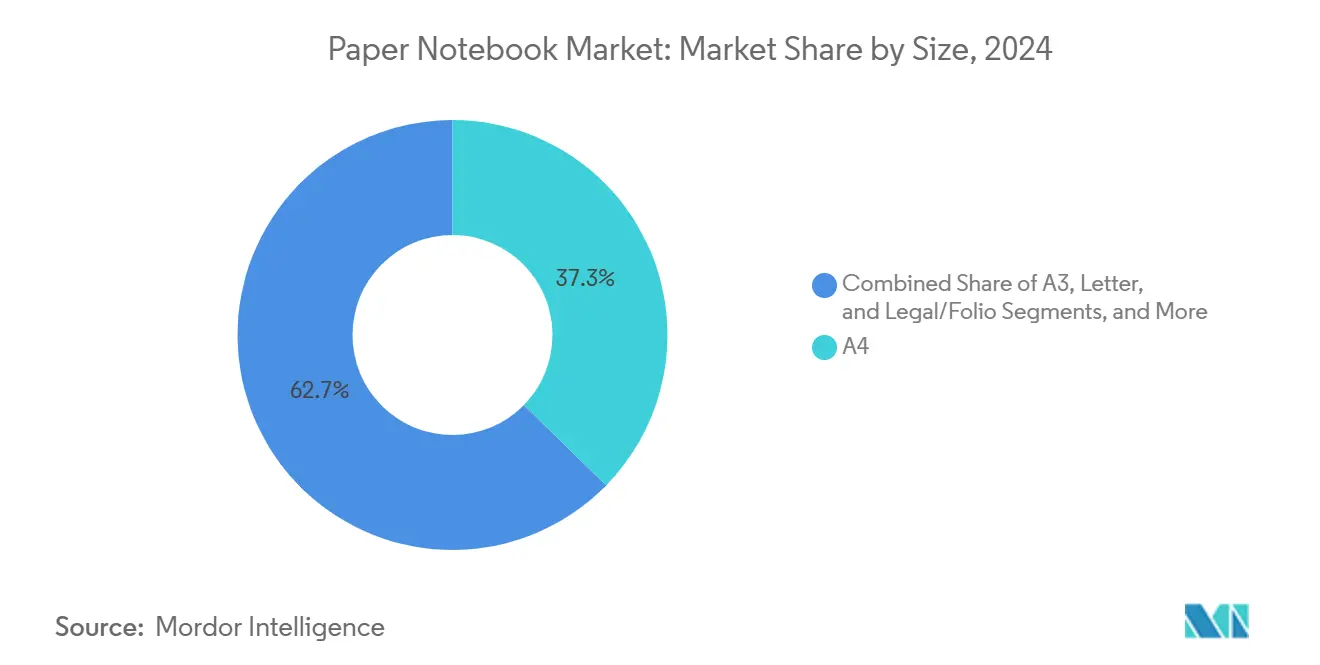

- By size, A4 notebooks held 37.33% of paper notebook market share in 2024.

- By binding type, the paper notebook market size for sewn binding is advancing at a 4.52% CAGR between 2025-2030.

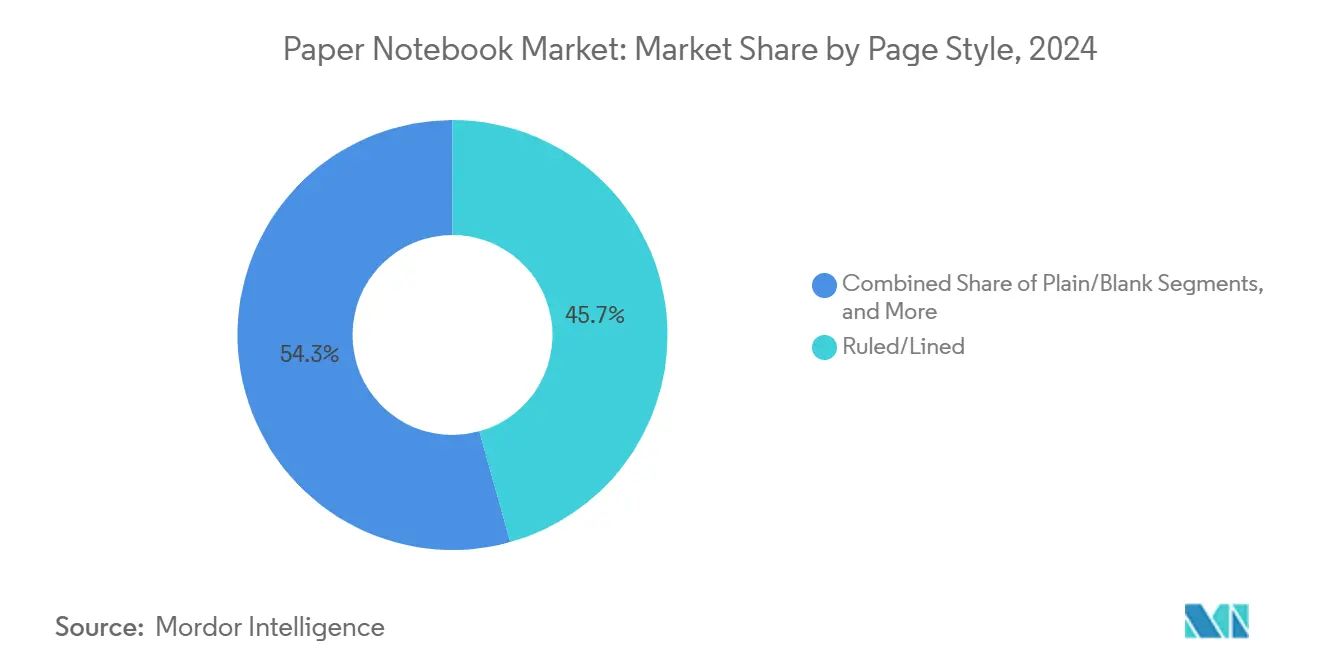

- By page style, ruled pages captured 45.67% of paper notebook market share in 2024.

- By cover material,the paper notebook market size for hardcover products is growing at a 4.27% CAGR between 2025-2030.

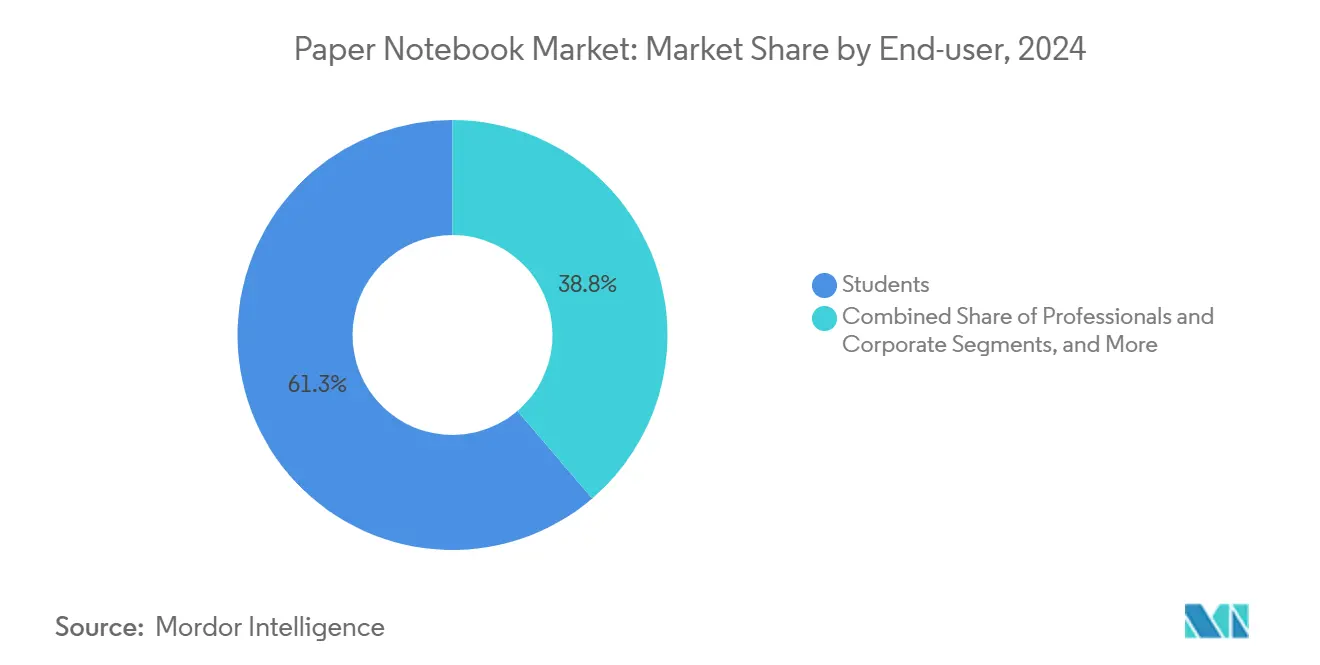

- By end-user, students generated 61.25% of paper notebook market share in 2024.

- By geography, the paper notebook market size for the Middle East and Africa region exhibits the fastest 4.05% CAGR between 2025-2030.

Global Paper Notebook Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global K-12 enrolments | +0.8% | Global, strongest in APAC and MEA | Long term (≥ 4 years) |

| Corporate gifting and promotional spend on branded notebooks | +0.6% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Premiumisation and personalisation trend in stationery | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Hybrid analog-digital notebooks with cloud integration | +0.4% | North America and EU, early adoption phase | Long term (≥ 4 years) |

| Social-media-driven bullet-journaling and planning communities | +0.5% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| ESG-aligned demand for recycled and FSC-certified paper | +0.6% | Global, regulatory-driven in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global K-12 Enrolments Drive Educational Demand

Worldwide efforts to close access gaps are lifting primary and secondary enrollment figures, especially across Asia-Pacific and Africa, sustaining baseline consumption of student notebooks as foundational learning tools. UNESCO recorded 249 million out-of-school children in 2024 yet flagged accelerated infrastructure investment that will channel new pupils into classrooms. [1]UNESCO Institute for Statistics, “World Education Statistics 2024,” uis.unesco.org In the United States, the National Center for Education Statistics projects steady K-12 expansion through 2030, a trend mirrored in India and Nigeria where youthful demographics underpin robust stationery requisitions. Procurement cycles linked to public-sector calendars stabilize order flows even when retail channels experience seasonality. As remote-learning platforms proliferate, policymakers still recognize handwriting’s developmental role, ensuring notebooks remain core to learning kits. Suppliers that tailor format, ruling, and durability to local curricula capture volume efficiencies while embedding ESG features to satisfy evolving ministry guidelines.

Corporate Promotional Spending Sustains Branded Notebook Demand

Promotional merchandise outlays hit USD 26.78 billion in 2024, with notebooks ranked among the most cost-effective impressions per dollar in marketing campaigns. [2]Promotional Products Association International, “2024 PPAI Sales Volume Report,” ppai.org Education and healthcare sectors increasingly order FSC-certified notebooks to reinforce purpose-led branding, while technology firms pair cloud-enabled pages with QR-linked onboarding media. Sustainable SKUs claimed 13.77% of promotional budgets and are expanding at double-digit rates, rewarding suppliers that can trace recycled fiber or agro-residue inputs. Minimum-order customization platforms allow small companies to participate, broadening the demand base. As hybrid work blurs professional and personal planning, branded premium books gain desktop visibility beyond a single event, extending marketing ROI and lifting average selling prices in bulk contracts.

Premiumisation Trends Reshape Product Positioning

Consumers gravitate toward notebooks that blend aesthetics, durability, and story-rich provenance, fueling above-average growth for hardcovers wrapped in fabric, cork, or vegan leather. Such upgrades carry 20–40% higher unit prices, offsetting flat volumes in mature regions. Moleskine’s resilience, despite an 8% H1 2024 revenue dip, underscores how direct-to-consumer channels and limited-edition collaborations secure loyalty from creative professionals. Bullet journaling kits, gift sets, and licensed intellectual-property covers monetize fandom among millennial and Gen Z cohorts. Premiumisation also manifests in micro-niche layouts—wellness trackers, habit planners, meeting agendas—enabling retailers to command higher shelf prices even as entry-level SKUs confront commoditization.

Hybrid Analog-Digital Notebooks with Cloud Integration

Smart paper substrates coated for erasability and paired with scanning apps bridge analog satisfaction with digital archiving, appealing to professionals who value handwriting yet need searchable records. Early adopters cluster in North America and Western Europe, where high device penetration and app familiarity lower barriers. Vendors embed NFC tags or QR codes to automate cloud sync, while enterprise IT departments welcome paper that complies with security protocols. The technology unlocks subscription revenue from companion software, shifting business models from purely one-time hardware sales. Although the segment’s volume remains small, its influence on R&D and perceived innovation raises switching costs for premium customers who demand future-proof stationery ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digital substitution (tablets, laptops) | -0.9% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Pulp-price volatility compressing margins | -0.5% | Global, supply-chain dependent | Short term (≤ 2 years) |

| Municipal "paper-waste" restrictions in select cities | -0.2% | Urban centers in developed markets | Long term (≥ 4 years) |

| Season-peak logistics bottlenecks and stock-outs | -0.3% | Global, concentrated during Q3-Q4 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Substitution Pressures Traditional Stationery Demand

School districts in Scandinavia and U.S. collegiate programs offer subsidized tablets, gradually lowering paper requisitions for coursework. ACCO Brands acknowledged in its 2024 10-K that notebook volumes face structural decline linked to device ubiquity.[3]ACCO Brands Corporation, “Form 10-K 2023,” sec.gov Corporate note-taking migrates onto collaborative platforms, shrinking office-supply budgets. While developing economies lag in infrastructure, younger populations show high digital affinity that foreshadows future down-shifts in paper consumption. Manufacturers hedge by introducing smart notebooks, but these cannibalize entry-level lines, requiring careful portfolio balance.

Pulp Price Volatility Compresses Manufacturing Margins

Producer prices for wood pulp climbed from 217.200 to 219.835 between April and May 2024, reflecting tight log supply and energy inflation. Spot spikes outpace contracted indexation, forcing mid-tier converters to absorb costs pending annual catalog resets. ITC’s paperboard division cited raw-material swings and cheap imports for a 9.5% revenue dip in Q3 FY24, illustrating sensitivity even for vertically integrated firms. Hedging tools remain limited, intensifying the search for agro-residue and recycled-fiber alternatives that dampen exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size: Compact Formats Gain Professional Traction

A4 retained 37.33% of 2024 revenue because its dimensions align with standard copier paper and institutional lesson plans. The segment benefits from automated cutting lines that reduce waste and support bulk school tenders. Pocket (≤A6) books post a 4.43% CAGR to 2030 as commuters and field technicians value portability that fits jacket pockets. Millennials employed in consulting and sales adopt A6 planners for rapid meeting notes, motivating retailers to dedicate premium shelf shares. Mid-size A5 caters to hobby journaling, while B5 preserves share in Japan and South Korea where legacy binders dictate refill compatibility. Kuantum Papers Limited scaled agro-fiber production to serve diverse trim sizes, optimizing press utilization for export and domestic customers. The paper notebook market captures incremental margins by packaging multi-size multipacks that satisfy household and remote-office users.

Demand heterogeneity obliges converters to maintain flexible cutting and binding lines. While compact-format growth outpaces overall paper notebook market, unit economics remain favorable because fewer square meters of paper generate comparable retail prices. By embedding recycled kraft bands around multipacks, brands communicate sustainability, boosting basket value. Manufacturers that partner with logistics providers to bundle diverse sizes in a single master carton lower pick-and-pack costs for online orders. Across premium channels, limited-edition micro sizes with bespoke artwork create scarcity appeal that commands double-digit mark-ups, reinforcing premiumisation’s impact on the paper notebook market.

By Binding Type: Premium Sewn Binding Attracts Quality-Conscious Users

Spiral and Wire-o formats delivered 30.41% of 2024 revenue owing to ease of use in academic and engineering settings where pages must fold flat. Large production runs and low tooling investment support aggressive pricing, making spiral dominant in mass merchants. Section-sewn volumes accelerate at a 4.52% CAGR as professionals view notebooks as archival documents needing durable spines. Luxury publishers introduce Smyth-sewn signatures with gilded edges, anchoring prices 3–4 times higher than glue-bound pads. Glue and perfect binding remain ubiquitous in low-cost exercise books, but solvent-based adhesives face regulatory scrutiny over volatile organic compounds, pushing R&D toward water-based glues.

Advances in PUR adhesives close the durability gap, enticing mid-market buyers who seek compromise between cost and longevity. Staple-stitched “exam pads” maintain niche demand among standardized-test centers that prefer 32-page count to minimize shipment weight. M&G Stationery recorded unit gains by offering spiral books with customizable poly dividers, satisfying student tabbing needs. Brands integrate recycled aluminum coils to reinforce green credentials, responding to corporate tenders that weight ESG criteria at bid evaluation. As binding choice dovetails with perceived quality, marketing copy highlights lay-flat angles and page retention to justify premium pricing within the broader paper notebook market.

By Page Style: Bullet Journaling Drives Dotted Format Growth

Ruled layouts comprised 45.67% of 2024 shipments, favored by schools for handwriting practice and by offices for meeting minutes. Gridded and squared pages cater to STEM coursework, aiding graph plotting and visual accuracy. Dotted grids grow 4.61% annually through 2030, propelled by bullet journaling’s flexibility for sketching, habit tracking, and monthly spreads. Social media tutorials recommend 120 gsm paper to prevent ghosting, raising raw-material cost but enabling higher retail points. Plain pages support sketch artists but face competition from specialized art pads with textured surfaces.

Brands invest in soy-based inks to minimize odor in heavy-ink decorative spreads common in bullet journals, appealing to health-conscious consumers. Limited-edition color-edge dotted notebooks sell out quickly during influencer collaborations, accentuating scarcity marketing. Software integrations that detect dotted layouts improve scan accuracy, bridging analog creativity with cloud backup. As dotted demand breaks into mainstream retail, shelf allocations re-balance, compelling manufacturers to rationalize slower-moving narrow-ruled variants. This shift amplifies value creation for the paper notebook industry through higher unit margins and cross-sell of markers and stencils.

By Cover Material: Hardcover Premium Positioning Gains Momentum

Softcover card boards led 52.78% of 2024 volume because they combine light weight with low material costs, fitting school budgets and trade promotions. Yet hardcovers advance at a 4.27% CAGR as gift givers and self-employed professionals seek heirloom presentation. Vegan-leather wraps resonate with eco-minded buyers, while fabric covers printed with contemporary patterns allow seasonal refreshes. Recycled PET felt emerges as an alternative that diverts plastic waste and adds tactile differentiation. ACCO Brands pledged to lift its environmentally certified products by 10 percentage points by 2025, broadening hardcover options carrying FSC or PEFC labels.

Softcover evolution continues via embossed textures and aqueous varnishes that mimic linen while remaining recyclable, balancing cost and appeal. Lay-flat cased-in books with integrated ribbons target executive planners seeking durability across multi-year projects. Manufacturers reengineer corner protectors with biodegradable polymers, keeping premium aesthetics while aligning to circular-economy mandates. Consequently, cover innovation contributes incremental value to the paper notebook market size without materially inflating shipping weights that influence e-commerce economics.

By End-user: Corporate Professional Segment Accelerates

Students supplied 61.25% of 2024 demand, with procurement locked into textbook cycles and curricular kits. Ed-tech adoption supports hybrid learning but cannot fully displace handwriting drills critical for motor-skill development. Professional segments expand 4.12% annually as meeting culture endures and privacy concerns limit open-laptop note-taking in sensitive discussions. Branded onboarding kits containing notebooks, pens, and stickers reinforce culture in distributed workforces, shifting some education-centric capacity toward B2B design teams. Household personal planners witness steady adoption during economic uncertainty as consumers track spending and wellness goals offline.

Artists and designers form a niche that values heavy-weight paper and unique bindings, providing outsized margin contribution. DOMS Industries grew stationery revenue 17.3% year over year by marketing sketch notebooks with gel-pen compatibility aimed at hobby illustrators. Cross-selling high-margin accessories such as pen loops and covers deepens share of wallet. As organizations codify ESG targets, notebooks with recycled content become default internal purchase, reinforcing volume momentum in the professional channel and broadening the addressable paper notebook market.

By Distribution Channel: Online Retail Disrupts Traditional Patterns

Stationery and book stores accounted for 39.89% of 2024 sales, benefiting from tactile product trials and immediate gratification. Yet online retail grows 4.39% annually to 2030 as consumers rely on reviews and unboxing videos to gauge quality. Direct-to-consumer portals allow brands to personalize covers, bundle accessories, and harvest first-party data. Supermarkets capture opportunistic buys during seasonal promotions, while institutional contracts stabilize baseline volumes. Fulfilment automation drives down pick costs for multi-sku orders, encouraging large notebooks marketed in reusable gift sleeves to combat perceived shipping waste.

Moleskine’s e-commerce sales lifted overall profitability despite total revenue contraction, illustrating online’s cushioning effect. Marketplaces introduce private labels competing on price, spurring incumbents to emphasize heritage and ESG transparency. Subscription models that deliver quarterly themed notebooks create predictable revenue and foster community engagement, reshaping lifetime customer value within the paper notebook market.

Geography Analysis

Asia-Pacific’s dominance in the paper notebook market stems from cost-competitive pulp, dense supplier clusters, and entrenched cultural practices that valorize handwriting. China’s M&G Stationery posted RMB 23.35 billion revenue and 16.78% growth in 2023, exemplifying domestic brand leverage over local distribution and online ecosystems. India benefits from policy initiatives such as the National Education Policy, which mandates foundational learning kits that include exercise books, further anchoring demand. Regional suppliers are progressively adopting renewable energy and agro-residue fibers, appeasing both export buyers and local regulators.

North America and Europe together contribute significant premium value even as digital devices encroach on traditional usage. Corporate gifting, bullet journaling culture, and ESG procurement criteria sustain higher net revenue per tonne of paper. California’s recycled-content mandates set procurement precedents for other states, nudging suppliers to recalibrate fiber blends without sacrificing brightness or opacity. [4]State of California, “Recycled-Content Paper Requirements,” calrecycle.ca.gov European Union directives on packaging and waste intensify design-for-recycling imperatives, prompting shift toward mono-material wraps and reduced foil stamping.

Middle East and Africa’s 4.05% CAGR arises from demographic tailwinds and government investment in classroom infrastructure. Markets such as Egypt and Kenya upgrade curriculum delivery, incorporating workbooks that require robust binding to withstand tropical climates. Retail modernization sees international stationery chains opening outlets in Gulf Cooperation Council hubs, stocking premium hardcovers aimed at expatriate professionals. South American nations observe steady, albeit slower, growth, anchored by Brazil’s large public-school network and cultural affinity for design-driven planners. Currency volatility and import tariffs create opportunities for regional paper mills to develop competitive local brands, further diversifying supply in the global paper notebook market.

Competitive Landscape

The market remains moderately fragmented. ACCO Brands, ITC Limited, Moleskine, and M&G Stationery rank among the largest suppliers, yet none exceeds 15% global revenue individually. ACCO’s 11.2% Q2 2024 sales decline illustrates exposure to North American digital substitution. Conversely, M&G leverages domestic e-commerce to achieve double-digit growth, while ITC’s Classmate capitalizes on integrated pulp sourcing to control costs in India. Premium challenger brands target niche communities with limited-edition designs and sustainability stories, eroding share of generalists among affluent consumers.

Strategic plays include capacity expansion by Kuantum Papers, from 450 TPD to 675 TPD, which strengthens supply of agro-based FSC-certified sheets for notebook converters. Firms invest in digital partnerships, embedding NFC tags that integrate with productivity apps, thus defending relevance amid software proliferation. Cost-optimization programs, such as ACCO’s USD 20 million savings target, fund R&D in smart paper and recycled fiber, mitigating margin erosion from pulp volatility.

Regional players differentiate by localizing formats, language templates, and festival-themed covers. Collaboration with influencers accelerates direct-to-consumer demand while bypassing traditional wholesale mark-ups. Moleskine’s loyalty app encourages refills and accessory bundling, increasing customer lifetime value. Competitive pressure intensifies during back-to-school, leading to tactical price promotions that compress gross margins. Nevertheless, premiumisation, ESG leadership, and smart-paper R&D remain key levers for sustaining profitability across the paper notebook market.

Paper Notebook Industry Leaders

ACCO Brands Corporation

Hamelin Group (Oxford)

Moleskine S.p.A.

Exacompta Clairefontaine S.A.

Shenzhen MandG Stationery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Oregon Department of Environmental Quality enacted the Plastic Pollution and Recycling Modernization Act, compelling notebook producers to finance enhanced recycling infrastructure, elevating compliance costs for U.S. suppliers.

- January 2025: California introduced recycled-content paper procurement rules, opening avenues for manufacturers with certified sustainable notebooks.

- September 2024: ACCO Brands released an ESG report highlighting 16.7% energy-efficiency gains and 25% CO₂ reductions while targeting a 10-point increase in certified products by 2025.

- March 2024: Forest Stewardship Council added certificate holders, expanding sustainably sourced paper pathways for notebook makers.

Global Paper Notebook Market Report Scope

| A4 |

| A5 |

| B5 |

| Pocket (≤A6) |

| Spiral/Wire-o |

| Perfect/Glue Bound |

| Sewn/Section-Sewn |

| Staple-Stitched |

| Ruled/Lined |

| Plain/Blank |

| Grid/Squared |

| Dotted/Bullet |

| Softcover (Card) |

| Hardcover (Board/Fabric/Leather) |

| Recycled/Biodegradable Covers |

| Students |

| Professionals and Corporate |

| Personal/Household |

| Creative/Art and Design |

| Supermarkets and Hypermarkets |

| Stationery and Book Stores |

| Online Retail and DTC |

| Institutional/Bulk |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Size | A4 | ||

| A5 | |||

| B5 | |||

| Pocket (≤A6) | |||

| By Binding Type | Spiral/Wire-o | ||

| Perfect/Glue Bound | |||

| Sewn/Section-Sewn | |||

| Staple-Stitched | |||

| By Page Style | Ruled/Lined | ||

| Plain/Blank | |||

| Grid/Squared | |||

| Dotted/Bullet | |||

| By Cover Material | Softcover (Card) | ||

| Hardcover (Board/Fabric/Leather) | |||

| Recycled/Biodegradable Covers | |||

| By End-user | Students | ||

| Professionals and Corporate | |||

| Personal/Household | |||

| Creative/Art and Design | |||

| By Distribution Channel | Supermarkets and Hypermarkets | ||

| Stationery and Book Stores | |||

| Online Retail and DTC | |||

| Institutional/Bulk | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the paper notebook market by 2030?

The market is expected to reach USD 89.72 billion by 2030, growing at a 3.30% CAGR.

Which region currently leads demand for paper notebooks?

Asia-Pacific accounts for 43.52% of global revenue, driven by expansive school-age populations and integrated manufacturing.

Which notebook size segment is expanding the fastest?

Pocket (²A6) notebooks are forecast to grow at a 4.43% CAGR through 2030 as professionals favor portable planning tools.

How are sustainability regulations shaping notebook specifications?

Mandates in states such as California require recycled-content paper, and FSC certifications are increasingly specified in public and corporate tenders.

What binding type is gaining share among premium buyers?

Sewn binding is advancing at a 4.52% CAGR as users prioritize durability and presentation quality for long-term reference materials.

How does digital substitution affect notebook demand?

Tablet and laptop adoption is reducing baseline paper consumption in developed markets, causing an estimated Ð0.9% impact on forecast CAGR.

Page last updated on: