Stone Paper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

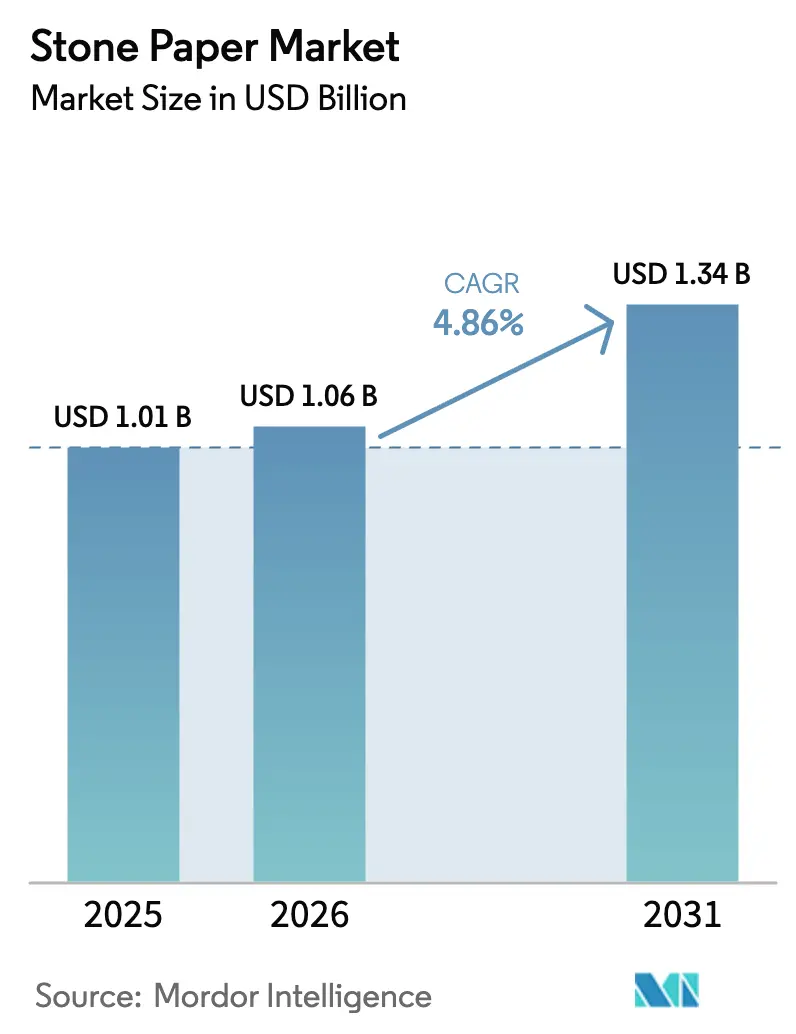

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.34 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

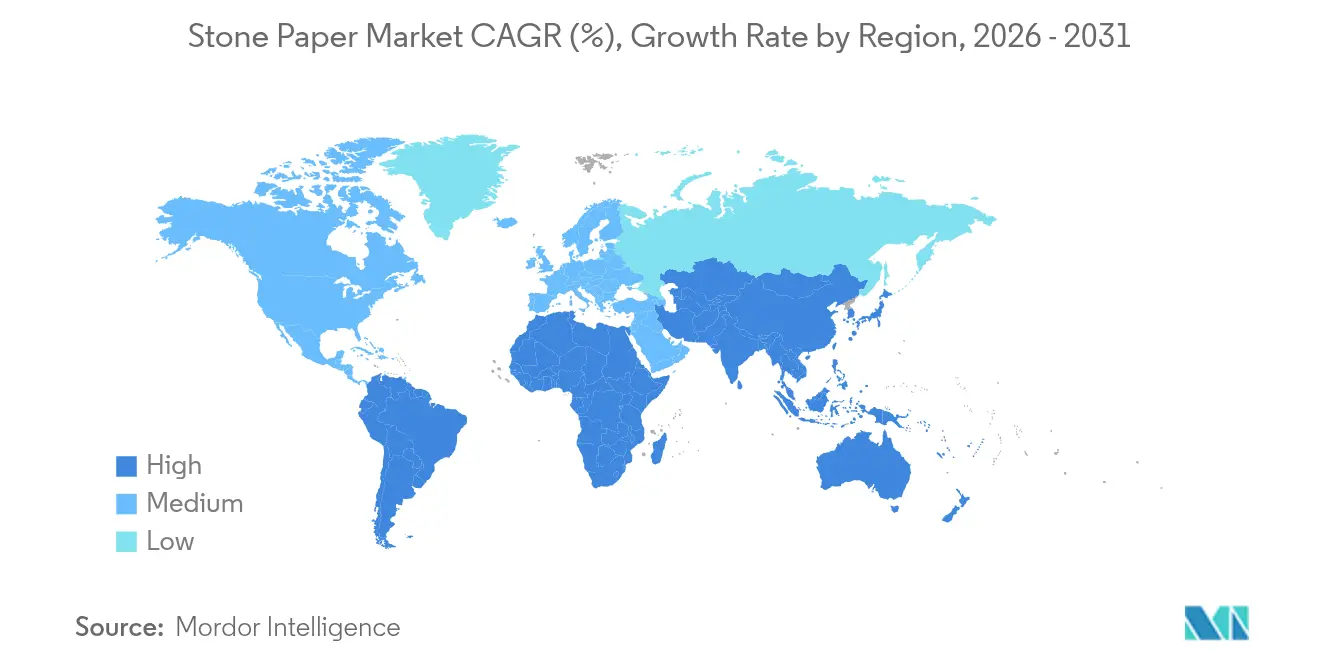

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

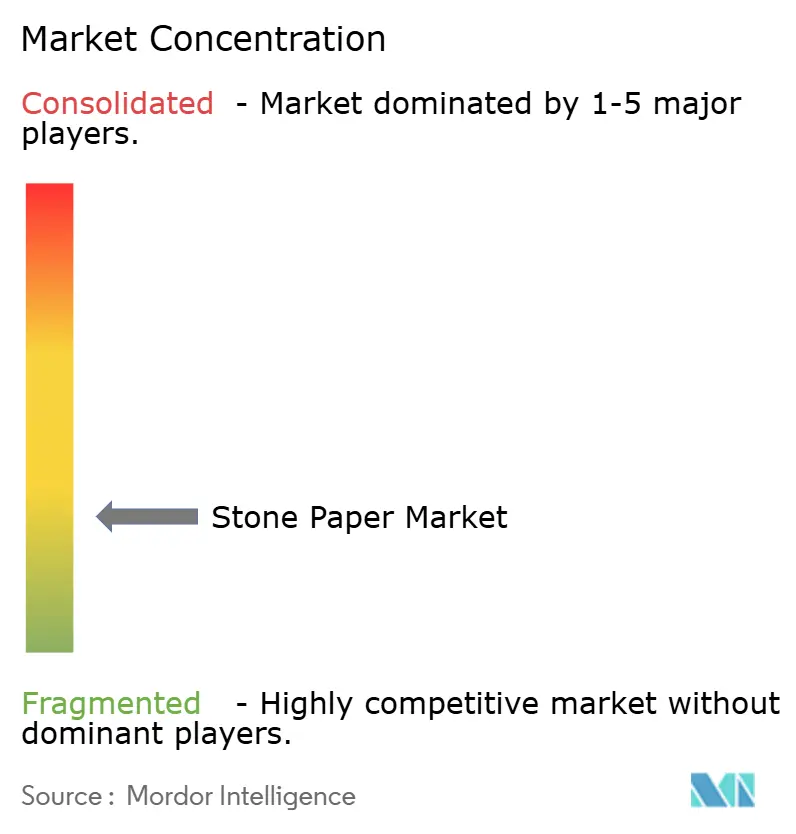

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Stone Paper Market Analysis by Mordor Intelligence

The stone paper market size is expected to grow from USD 1.01 billion in 2025 to USD 1.06 billion in 2026 and is forecast to reach USD 1.34 billion by 2031 at 4.86% CAGR over 2026-2031. Rising government bans on single-use plastics, brand-driven sustainability targets, and cost-down advances in limestone–polyethylene composites underpin this expansion. Asia-Pacific commands the largest regional position, while North America records the fastest growth as procurement teams shift toward mineral-based substrates. Technical breakthroughs such as TBM’s LIMEX and water-based dual-coat systems improve barrier performance and printability, broadening use in food contact, labels, and industrial applications. Integrated limestone-to-product supply chains protect margins amid HDPE price swings between USD 1,200–1,300 per t in early 2025. Although raw-material concentration and recycling‐system gaps introduce risk, favorable policy and corporate carbon targets continue to pull the stone paper market toward scale.

Key Report Takeaways

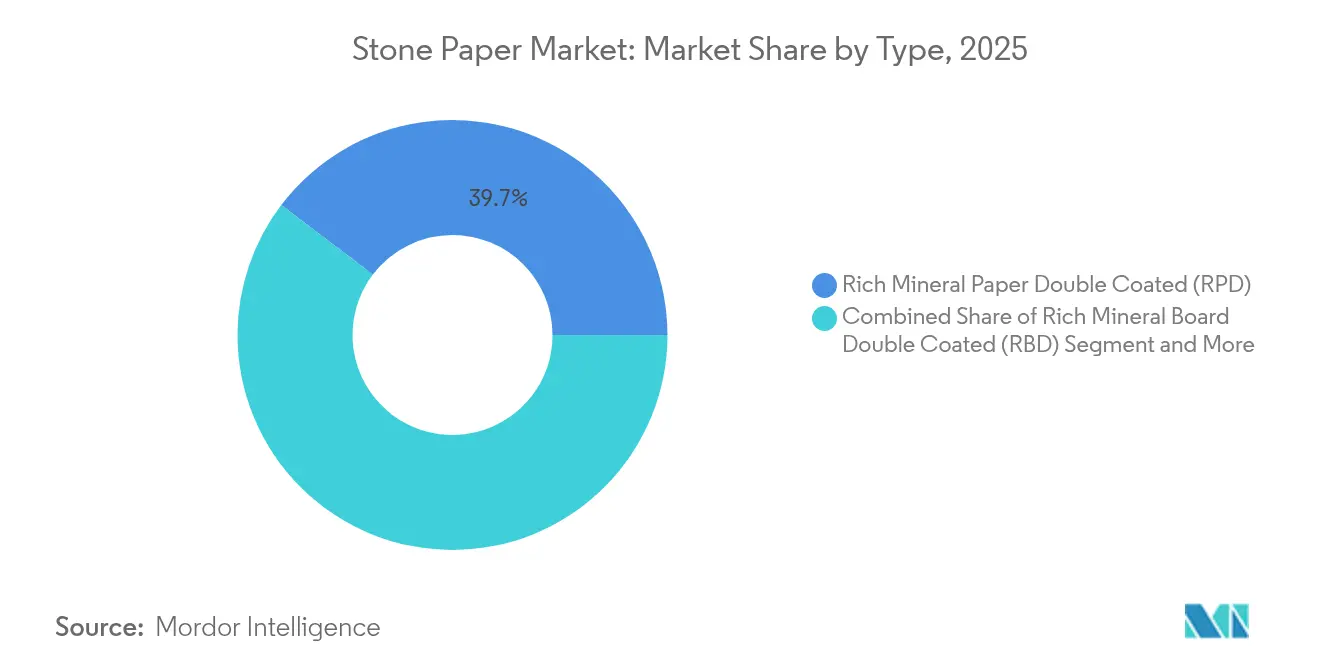

- By type, Rich Mineral Paper Double Coated led with 39.67% of stone paper market share in 2025, while Rich Mineral Paper Double Coated (RPD) the highest CAGR at 8.03% through 2031.

- By application, packaging held 37.85% of stone paper market share in 2025, while industrial labels and tags post the highest CAGR at 7.62% through 2031.

- By end-user industry, food and beverage accounted for 27.78% share of the stone paper market size in 2025; retail and e-commerce rise fastest at 8.77% CAGR to 2031.

- By Product Form, sheets held 29.65% of stone paper market share in 2025, while Flexible Films and Bags the highest CAGR at 8.18% through 2031.

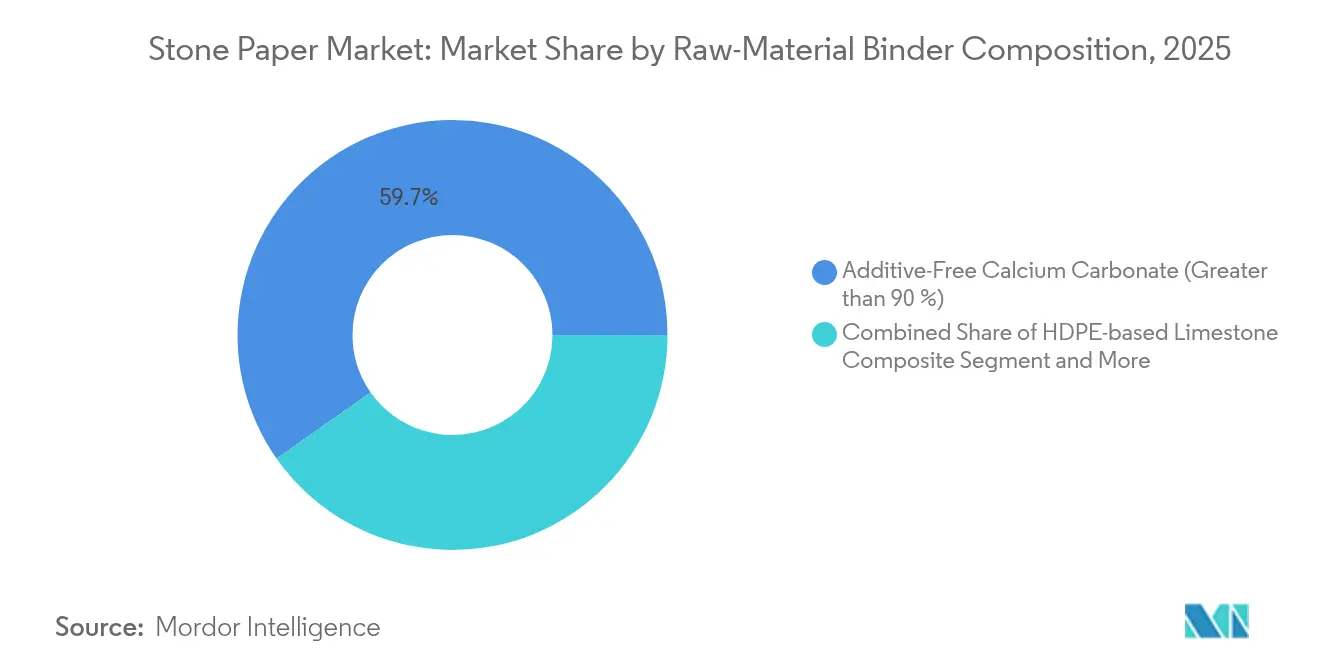

- By raw-material / binder composition, Additive-Free Calcium Carbonate (>90 %) accounted for 59.74% share of the stone paper market size in 2025; HDPE-based Limestone Composite rise fastest at 7.88% CAGR to 2031.

- By region, Asia-Pacific maintained a 39.89% revenue share in 2025, whereas North America is projected to grow at 7.74% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stone Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from flexible packaging converters | +1.2% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Mainstream corporate sustainability mandates | +0.9% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Government bans on single-use plastics | +1.5% | Global, led by EU and select Asia-Pacific markets | Short term (≤ 2 years) |

| Cost-down advances in LIMEX and mineral-polymer composites | +0.8% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Luxury brands shifting to carbon-neutral stationery (niche pull) | +0.3% | North America and EU premium markets | Medium term (2-4 years) |

| Humidity-resistant food-contact boards for tropical cold-chains | +0.4% | Asia-Pacific tropical regions, expanding to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging demand from flexible packaging converters

Converters accelerate adoption as they seek recyclable food substrates before the EU’s 2030 deadline[1]European Chemicals Agency, “Understanding the Packaging and Packaging Waste Regulation,” echa.europa.euWestRock documented a 93% plastic reduction after shifting to fiber-based trays, validating performance in ready-meal formats. Stone paper reduces ink use by 20–30%, enhancing converter economics. Waterproof and tear-resistant attributes unlock humid-climate categories, while two-layer calcium-carbonate/PE structures secure food-grade compliance at cost parity with specialty films. Brand trials in dairy lidding and detergent refill pouches confirm scalability across varied barrier requirements.

Mainstream corporate sustainability mandates

Large retailers embed life-cycle metrics in sourcing, propelling demand for substrates with lower CO2 footprints. McDonald’s and Amazon now specify paper-based packaging pathways, steering procurement toward mineral substrates that deliver 60% lower environmental impact than wood-pulp paper. Suppliers able to provide granular ESG data and end-of-life traceability rise in bid evaluations. The trend is strongest in high-visibility consumer sectors where packaging sustainability influences brand equity.

Government bans on single-use plastics

The PPWR took effect in February 2025, phasing out PFAS in food packaging by August 2026 and mandating recyclability, rapidly boosting European orders. India’s 2024 amendment banned select disposables and funded R&D for alternatives such as stone paper. [2]Ministry of Environment India, “Compulsory Ban on Polythene Bags,” pib.gov.in Australian state bans slated for 2025 reinforce a domino effect, prompting multinational suppliers to adopt globally compliant materials.

Cost-down advances in LIMEX and mineral-polymer composites

Process optimization pushes limestone content past 50%, lowering petroleum use and approaching cost parity with virgin plastics. [3]WIPO, "LIMEX – the alternative to plastic and paper made out of limestone." wipo.int Continuous calendaring removes granule pre-processing, trimming capex. patents on food-grade dual layers expand applications without compromising compliance. Regional mineral abundance further compresses delivered costs, especially in East Asia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited post-consumer recycling infrastructure | -0.7% | Global, particularly acute in developing markets | Long term (≥ 4 years) |

| Higher ex-factory price versus wood-pulp paper in price-sensitive regions | -0.5% | Price-sensitive regions in Asia-Pacific and South America | Medium term (2-4 years) |

| Concentration of high-grade limestone deposits and mining licences | -0.4% | Global, with regional supply chain vulnerabilities | Long term (≥ 4 years) |

| Brand hesitation over incomplete life-cycle data disclosures | -0.3% | North America and EU corporate markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited post-consumer recycling infrastructure

Stone paper cannot enter fiber or conventional plastic loops, requiring purpose-built recovery systems. Municipal waste networks lack scale for specialty mineral-polymer streams, muting circular-economy value propositions. Mechanical recycling to pellets or energy recovery dominates today, yet emerging mineral separation technologies show promise once volumes justify investment. Developing regions face steeper challenges as basic collection remains underfunded.

Higher ex-factory price versus wood-pulp paper

Specialized calendering, premium HDPE, and limited runs keep unit costs above uncoated pulp substrates, constraining adoption in commoditized print or school-notebook categories. However, durability, ink-saving, and reduced replacement frequency tip total cost of ownership in favor of stone paper for high-performance niches. As installed capacity rises and material formulations migrate toward locally sourced calcium carbonate, the price gap is expected to narrow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: RPD Dominance Drives Technical Innovation

Rich Mineral Paper Double Coated captured 39.67% of the stone paper market in 2025, and its 8.03% CAGR through 2031 outpaces other grades thanks to superior printability and barrier performance. The dual water-based coat minimizes show-through and boosts ink holdout, which lowers press-side rejects and supports premium food labels. Process refinements let converters run RPD at pulp-paper line speeds, reinforcing economies of scale. Rising demand in pre-made snack pouches and pharmaceutical leaflets keeps capacity additions centered on this grade.

RBD serves heavier-gauge clamshells and folding cartons that need added stiffness, while SPN targets cost-sensitive inserts where coating is unnecessary. Stone Thermoforming Board fulfills three-dimensional trays but remains niche because tooling adaptations carry higher upfront costs. Suppliers integrate limestone quarries with extrusion-coating units to stabilize mineral quality, and several firms have unveiled solvent-free coatings that cut VOCs during curing.

By Application: Packaging Leadership Amid Labels Growth

Packaging accounted for 37.85% of stone paper market revenue in 2025, anchoring demand across food service, confectionery, and personal-care goods. Regulatory bans on PFAS-lined boards channel volume to mineral substrates with comparable grease resistance yet recyclability. Flexible sachets, ice-cream tubs, and ready-meal trays showcase adoption momentum, and commercial trials confirm heat-seal integrity at production pace.

Industrial labels and tags advance fastest at 7.62% CAGR, leveraging waterproof and tear-resistant traits for outdoor chemicals, lumber, and cold-chain logistics. The stone paper market size for labels is projected to expand steadily as barcode readability remains crisp despite condensation. Decoration, graphics, and premium stationery exploit the unique velvety texture to command price premiums in art supplies and luxury notebooks.

By End-User Industry: Food Sector Stability, Retail Acceleration

Food and beverage retained 27.78% share of the stone paper market size in 2025, driven by hygienic needs and shelf-life preservation alongside aggressive plastic-reduction roadmaps. Multinationals source mineral substrates for burger clamshells and sauce sachets, with durability during freezer-to-oven cycles cited as a key benefit.

Retail and e-commerce post the fastest 8.77% CAGR to 2031 as parcel volume multiplies and brand owners pursue curbside-recyclable mailers. Folding mailer envelopes, returnable garment pouches, and luxury gift wraps adopt coated limestone sheets to uphold print vibrancy while replacing plastic laminates. Industrial logistics value scratch resistance, and education verticals pilot workbooks that withstand humidity, illustrating broader penetration.

By Product Form: Sheets Dominance, Films Innovation

Sheets represented 29.65% of 2025 demand, aligned with legacy print shops and flatbed die-cutters needing minimal equipment changeover. Continuous calendaring now enables jumbo rolls, enhancing throughput for magazine covers and wrap-around labels. Flexible films and bags display 8.18% CAGR to 2031, buoyed by TBM’s LimeAir garbage bag success that cut petroleum plastics by 27%.

Boards and cartons gain share in frozen foods and hardware blister packs that require puncture strength. Finished stationery, though smaller in volume, secures high margins as consumers pay premiums for water-proof notebooks. Suppliers collaborate with equipment OEMs to develop low-temperature sealing profiles, empowering converters to run stone paper films without extensive retrofits.

By Raw-Material Composition: Calcium Carbonate Foundation, HDPE Innovation

Additive-free calcium carbonate grades held 59.74% of 2025 volume, enabled by ample limestone reserves in China and India, the latter producing 450 million t in FY24. HDPE-based limestone composites see 7.88% CAGR through 2031 as process tweaks accommodate recycled HDPE priced near USD 1,250 /t in March 2025. Bio-PE / PLA hybrids win attention in jurisdictions offering compostability credits.

Formulators balance mineral loading, polymer grade, and coupling agents to hit target tear strength without sacrificing recyclability. Integrated players secure quarry licenses to curb feedstock volatility, while downstream converters trial PCR-HDPE blends, fostering circular value chains.

Geography Analysis

Asia-Pacific contributed 39.89% of stone paper market revenue in 2025, supported by limestone abundance, dense converter clusters, and state-level plastic bans. China leads production with integrated mines and extrusion lines, whereas India’s new capacities capitalize on low-cost feedstock. Japan anchors technology R&D; TBM’s pilot lines deliver LIMEX pellets for regional collaborators in food service and construction. Australia’s Karst scales premium stationery, validating consumer acceptance of non-wood notebooks.

North America is the fastest-growing geography, at 7.74% CAGR through 2031. Corporate ESG procurement, coupled with federal and state legislation restricting polystyrene and PFAS, accelerates substrate switches in quick-service dining and retail mailers. Local extrusion capacity remains modest; hence Asian suppliers fill early demand, yet several US converters announce retrofits to produce coated limestone sheets domestically.

Europe benefits from the PPWR and long-standing EPR schemes that reward recyclable packaging. Germany and the Nordic countries pilot closed-loop collection for mineral-paper coffee cups, while France mandates traceability labeling, which stone paper substrates accommodate via digital watermarks. Stora Enso’s USD 1 billion Oulu board line expansion signals the region’s intent to bolster renewable materials supply.

Competitive Landscape

The stone paper market remains fragmented, with regional specialists dominating supply. Technology leaders such as TBM leverage LIMEX IP and vertical integration from quarry to compounding to secure unit-cost advantages. Taiwanese and Chinese firms replicate at lower capital cost, intensifying price competition in commodity grades. European producers, including STP Stone Paper, differentiate with solvent-free coatings and FSC-aligned traceability.

Strategic moves emphasize scale synergy; several Asia-Pacific players acquire downstream converter stakes to lock in offtake and accelerate application trials. Patent filings surge for food-contact and mono-material constructs, highlighting incremental rather than disruptive innovation. Cross-industry alliances emerge: pipe-insulation developers in Japan deployed LIMEX wraps to cut installation time while boosting moisture protection.

Supply-chain robustness becomes a distinguishing factor as HDPE and freight volatility persist. Integrated limestone mining offers pricing insulation, whereas non-integrated converters form long-term quarry contracts to secure feedstock. Environmental disclosure platforms such as TBM’s ScopeX add service revenue streams and embed suppliers deeper into customer sustainability programs

Stone Paper Industry Leaders

-

Stone Paper Printing & Packaging India LLP

-

AM Packaging Co. Ltd.

-

Karst Stone Paper

-

TBM Co., Ltd.

-

Etched Stone Paper (UK)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TBM’s LIMEX Pellet adopted by Vietnam’s BioTech for detergent refill pouches, cutting petroleum plastics while maintaining price parity.

- May 2025: Shinto Tsushin and Shinryo Reihatsu launched LIMEX-based pipe-insulation exteriors with improved strength and CO2 savings.

- April 2025: TBM debuted GX Skills training linked to ScopeX CO2-tracking service, broadening its sustainability solutions.

- March 2025: Stora Enso’s Oulu packaging board line commenced ramp-up, reinforcing European supply of renewable substrates.

- February 2025: EU Packaging and Packaging Waste Regulation became effective, mandating recyclability by 2030 and banning PFAS in food packaging from Aug 2026.

Global Stone Paper Market Report Scope

The study tracks the demand for stone paper offered by various vendors operating in the market. The pricing for the raw material, along with the consumption, import, and export trends and average prices, is taken into consideration to arrive at the market revenue.

The market is segmented by type (rich mineral paper double coated (RPD) and rich mineral board double coated (RBD)), by application (packaging, printing, decoration, industrial and commercial), by geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa).The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Rich Mineral Paper Double Coated (RPD) |

| Rich Mineral Board Double Coated (RBD) |

| Synthetic Paper No-Coat (SPN) |

| Stone Thermoforming Board (ST) |

| Packaging |

| Printing and Publishing |

| Decoration and Graphics |

| Industrial Labels and Tags |

| Commercial Stationery and Notebooks |

| Food and Beverage |

| Retail and E-commerce |

| Consumer Goods (FMCG) |

| Industrial and Logistics |

| Education and Office Supplies |

| Hospitality and Events |

| Sheets |

| Rolls |

| Finished Stationery (notebooks, journals, etc.) |

| Flexible Films and Bags |

| Boards and Cartons |

| HDPE-based Limestone Composite |

| Bio-PE / PLA Hybrid Limestone Composite |

| Recycled LIMEX Grade |

| Additive-Free Calcium Carbonate (>90 %) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Type | Rich Mineral Paper Double Coated (RPD) | ||

| Rich Mineral Board Double Coated (RBD) | |||

| Synthetic Paper No-Coat (SPN) | |||

| Stone Thermoforming Board (ST) | |||

| By Application | Packaging | ||

| Printing and Publishing | |||

| Decoration and Graphics | |||

| Industrial Labels and Tags | |||

| Commercial Stationery and Notebooks | |||

| By End-User Industry | Food and Beverage | ||

| Retail and E-commerce | |||

| Consumer Goods (FMCG) | |||

| Industrial and Logistics | |||

| Education and Office Supplies | |||

| Hospitality and Events | |||

| By Product Form | Sheets | ||

| Rolls | |||

| Finished Stationery (notebooks, journals, etc.) | |||

| Flexible Films and Bags | |||

| Boards and Cartons | |||

| By Raw-Material / Binder Composition | HDPE-based Limestone Composite | ||

| Bio-PE / PLA Hybrid Limestone Composite | |||

| Recycled LIMEX Grade | |||

| Additive-Free Calcium Carbonate (>90 %) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the stone paper market?

The stone paper market is valued at USD 1.06 billion in 2026 and is projected to hit USD 1.34 billion by 2031.

Which region leads the stone paper market?

Asia-Pacific holds 39.89% of global revenue, supported by abundant limestone reserves and established manufacturing clusters.

Why is the stone paper market growing in North America?

Corporate sustainability mandates and state-level bans on single-use plastics are driving an 7.74% CAGR in North America through 2031.

Which product type commands the largest share?

Rich Mineral Paper Double Coated accounts for 39.67% of global revenue and posts an 8.03% CAGR through 2031.

What is the key restraint limiting faster adoption?

The absence of dedicated post-consumer recycling systems reduces circularity and slows acceptance in sustainability-focused applications.

Page last updated on: