Writing And Printing Paper Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Volume (2025) | 77.78 Million tonnes |

| Market Volume (2030) | 75.81 Million tonnes |

| Growth Rate (2025 - 2030) | -0.51% CAGR |

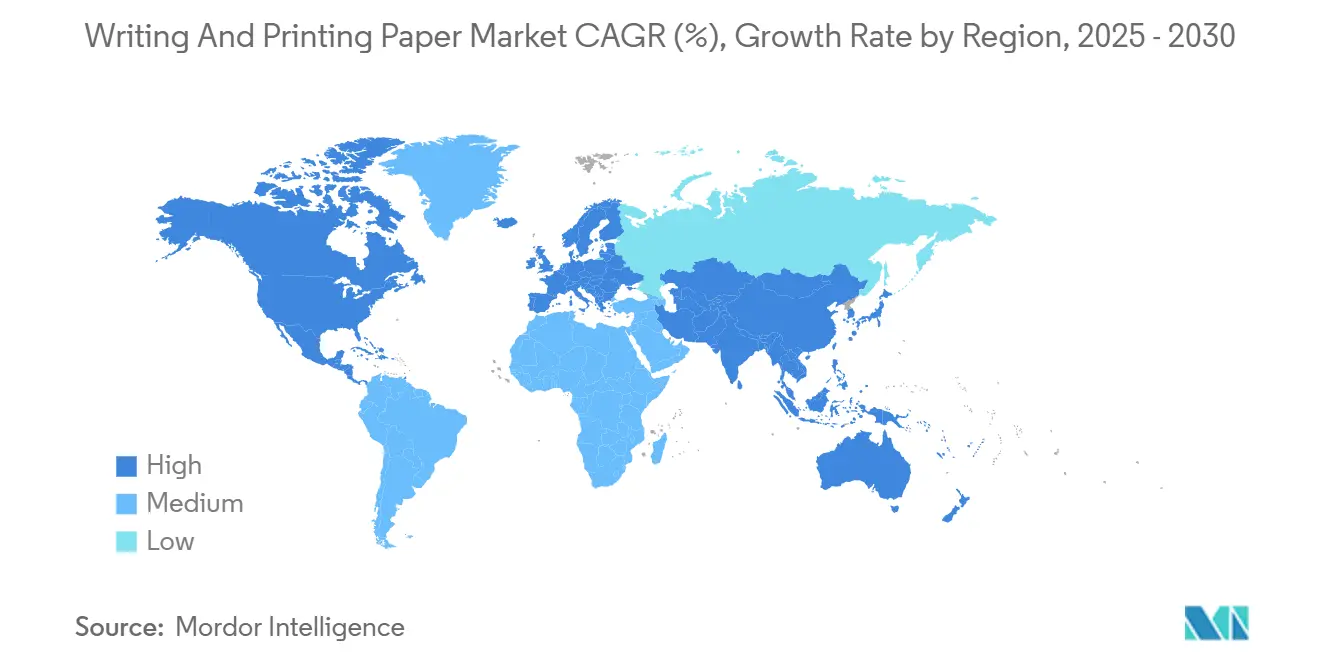

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Writing And Printing Paper Market Analysis by Mordor Intelligence

The writing and printing paper market size stands at 77.78 million tonnes in 2025 and is projected to decline to 75.81 million tonnes by 2030, translating into a –0.51% CAGR. Structural pressures from digitalization are squeezing volumes, yet the writing and printing paper market continues to find support in pockets such as examination papers, fintech security forms, and premium stationery where tactile quality matters. Specialized niches, especially those tied to government mandates and brand-driven presentation demands, create pricing resilience even as commodity grades face contraction. Asia-Pacific keeps the lead, while Middle East and Africa register the quickest advance, highlighting how emerging economies partly offset mature-market declines. Competitive strategies revolve around mill rationalization, product premiumization, and verifiable sustainability credentials, with capacity closures in Europe balanced by investments in higher-margin specialties.

Key Report Takeaways

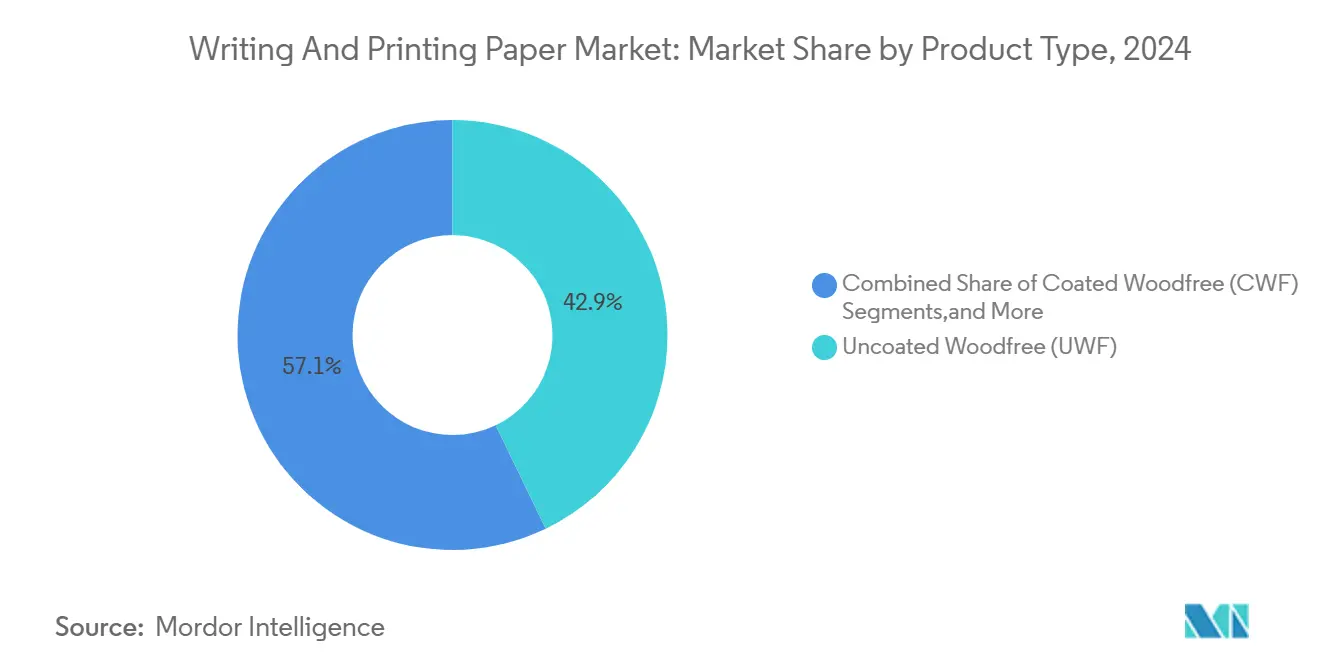

- By product type, Uncoated Woodfree captured 42.87% of the writing and printing paper market share in 2024.

- By application, the writing and printing paper market size for the Books and Journals segment is projected to grow at a 0.34% CAGR between 2025-2030.

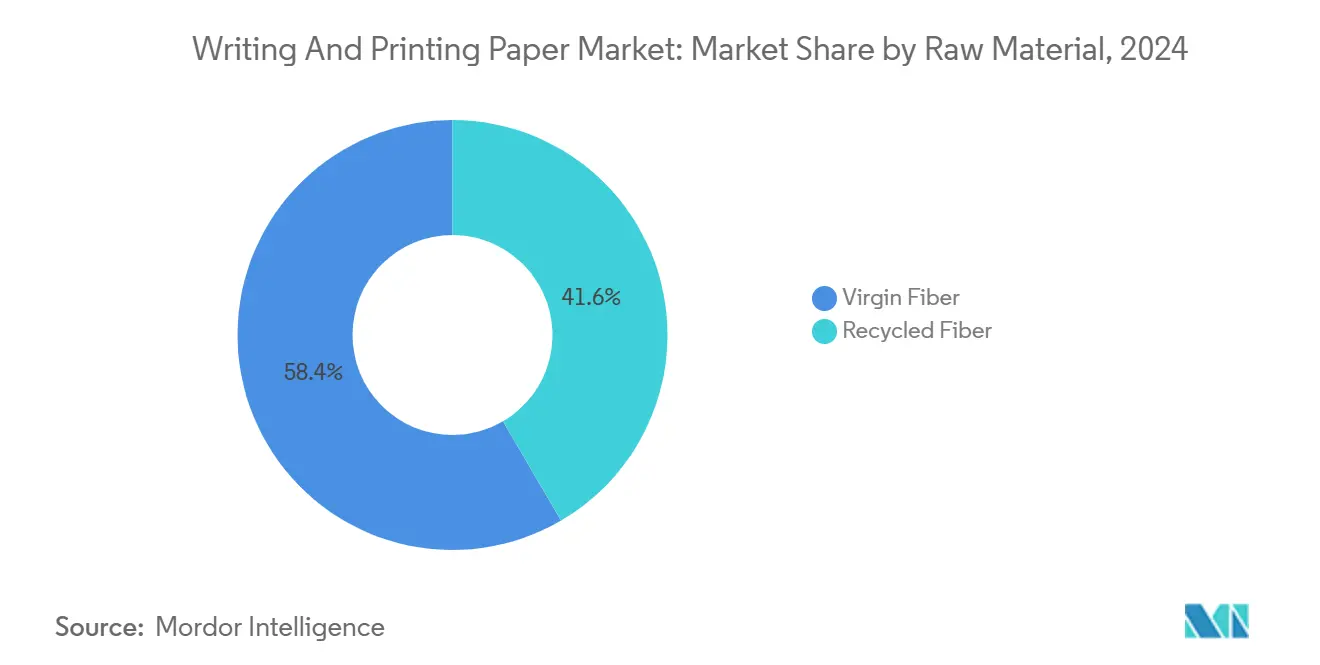

- By raw material, Virgin Fiber held 58.42% of the writing and printing paper market share in 2024.

- By distribution channel, the writing and printing paper market size for the Online B2B Platforms is projected to grow at a 0.58% CAGR between 2025-2030.

- By geography, Asia-Pacific region dominated with 56.93% of the writing and printing paper market share in 2024.

Global Writing And Printing Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising literacy and education spending in emerging economies | +0.80% | South Asia, Africa, Latin America | Long term (≥ 4 years) |

| Growth in self-publishing and short-run book printing | +0.30% | Global; North America and Europe core | Medium term (2-4 years) |

| Corporate demand for premium office stationery in Asia | +0.20% | APAC core; spill-over to MEA | Short term (≤ 2 years) |

| Government examination-paper demand in South Asia and Africa | +0.40% | South Asia, Sub-Saharan Africa | Medium term (2-4 years) |

| “BookTok”-fuelled resurgence of paperback fiction sales | +0.10% | North America, Europe, urban APAC | Short term (≤ 2 years) |

| Hybrid “code-on-paper” secure forms for fintech KYC | +0.10% | Global financial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising literacy and education spending in emerging economies

Government education budgets in South Asia and Sub-Saharan Africa are expanding, creating steady orders for textbooks and examination sheets where digital alternatives remain costly[1]World Bank, “Adequacy of Public Education Spending,” worldbank.org . Infrastructure constraints such as unreliable electricity and limited device access preserve paper’s role in large-scale assessments. National literacy campaigns further amplify volumes as adult education programs prefer low-cost printed materials. Suppliers positioned near growth markets enjoy freight advantages and preferential procurement terms. As fiscal capacity rises, higher-quality grades also gain traction, boosting mix-driven revenue despite flat tonnage.

Growth in self-publishing and short-run book printing

Advances in digital presses make single-copy economics viable, enabling authors to bypass conventional runs and order bespoke quantities. The pattern shifts demand toward diverse trim sizes and specialty coatings that enhance shelf appeal. Paper converters that can manage small batches profit from higher margins and reduced inventory risk. North America and Western Europe remain hubs for self-publishing platforms, yet uptake is visible in urban Asia. The trend diversifies consumption away from blockbuster titles to a long-tail configuration that cushions overall volatility in the writing and printing paper market.

Corporate demand for premium office stationery in Asia

Financial, legal, and consulting firms in Asian business centers reinforce brand stature through heavyweight watermarked sheets and matching envelopes. Presentation kits, investment reports, and ceremonial contracts command premium uncoated woodfree grades. Vendors offering flawless whiteness, consistent formation, and rapid delivery service secure framework agreements. Although per-capita sheet use is falling, the value per tonne sold in this niche is rising, supporting profitability amid shrinking commodity volumes across the broader writing and printing paper market.

Government examination-paper demand in South Asia and Africa

High-stakes testing regimes typically print millions of answer booklets each season, often embedding security features such as watermarks or bar codes. Ministries issue multi-year tenders providing visibility to mills capable of guaranteeing on-time deliveries. Seasonal peaks require ample warehousing and flexible capacity scheduling. Because alternate digital platforms risk connectivity failures, policymakers continue to prioritize paper-based exams, ensuring a baseline demand stream that stabilizes the writing and printing paper market through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital substitution and remote work reduce copy-paper volumes | –1.2% | Global, especially developed markets | Short term (≤ 2 years) |

| Volatile pulp prices and energy inflation squeeze margins | –0.4% | Global; exposure highest in energy-intense regions | Medium term (2-4 years) |

| Fortune-500 zero-paper ESG mandates | –0.3% | North America, Europe, multinationals | Medium term (2-4 years) |

| EU Deforestation Regulation compliance costs | –0.2% | Europe with global supply impacts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital substitution and remote work reduce copy-paper volumes

Hybrid workplaces cut per-capita consumption by up to 60% as cloud collaboration eliminates most internal print jobs. Office closures shrink centralized print hubs, and electronic signature platforms replace multi-page contracts. The fall-off is most pronounced in North America and Western Europe, yet spill-overs appear in urban Asia. Resulting excess capacity triggers mill shutdowns, lifting unit costs for remaining producers.

Volatile pulp prices and energy inflation squeeze margins

Geopolitical shocks tighten fiber supply and boost power tariffs, eroding profitability even for integrated mills. Spot electricity rates in Europe surged above EUR 200/MWh during 2024, while hardwood pulp touched USD 950/tonne, forcing some producers to idle lines. Passing costs downstream proves difficult as commodity grades face fierce import competition. Mills with captive biomass boilers or long-term fiber contracts enjoy a cushion, but independents endure margin compression.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Shifts Reshape the Mix

Uncoated Woodfree holds 42.87% of the writing and printing paper market share in 2024, underpinned by versatility across office, educational, and transactional uses. Yet its tonnage dips as corporate digitization advances. The segment still benefits from exam paper orders and premium stationery specifications, anchoring a sizeable base despite contraction. Competitive focus is on cost optimization through larger rolls, faster machines, and regional mill clustering.

Coated Woodfree is projected to post a 0.11% CAGR to 2030, outperforming every other grade as image-intensive books, art publications, and luxury catalogs privilege surface smoothness. Converters add value via gloss, matte, and silk finishes that enhance color depth. Strategic mill conversions prioritize this grade to capture stability amid shifting demand. Uncoated Mechanical and Coated Mechanical together shrink as advertising migrates online, yet regional newspaper campaigns in Southeast Asia preserve a portion of the base.

By Application: Educational and Cultural Niche Growth

Office and Home Printing contributes 35.38% to the writing and printing paper market size in 2024, but faces persistent erosion due to electronic workflow acceleration. Manufacturers respond with ultra-high-yield grades to cut basis-weight while preserving opacity, squeezing fiber costs.

Conversely, Books and Journals is forecast to grow 0.34% CAGR through 2030 in a selective revival of printed reading, aided by social-media driven trend surges. Educational printing remains vital as infrastructure gaps limit e-learning in emerging economies. Magazine and catalog demand continues to decline, yet fashion and luxury titles retain print editions as brand beacons.

By Raw Material: Sustainability Drives Recycled Uptake

Virgin Fiber covers 58.42% of 2024 volumes, reflecting unmet brightness and durability requirements in archival, exam, and corporate applications. Nevertheless, supply chain scrutiny and cost pressures push buyers toward higher recycled content, lifting Recycled Fiber at a 0.62% CAGR.

The writing and printing paper market size attributed to recycled grades gains as mills upgrade de-inking lines and optical sorting to reach 90+ ISO brightness. EU regulations and corporate ESG scorecards accelerate substitution, though full replacement remains unlikely where strength and longevity are critical.

By Distribution Channel: Digital Platforms Challenge Legacy Networks

Distributors and Wholesalers maintain a 40.74% sales share owing to warehousing, credit provision, and last-mile deliveries to SMEs. Still, Online B2B Platforms are rising at 0.58% CAGR as price transparency and streamlined ordering attract procurement officers.

Large corporate buyers increasingly place blanket orders directly with mills, bypassing intermediaries for cost savings. Hybrid models emerge: distributors integrate e-commerce storefronts, while mills deploy regional depots to shorten lead times. Channel dynamics thus become a critical differentiator in the writing and printing paper market.

Geography Analysis

Asia-Pacific controls 56.93% of global volume thanks to integrated supply chains, expanding literacy, and scale economies in China and India. China alone produced over 121 million tons of paper and board in 2024, supplying both domestic and export needs while benefiting from efficient logistics networks. India’s National Education Policy intensifies textbook demand, and Southeast Asia’s vocational training programs sustain steady orders for exam stock. Regional producers also leverage proximity to fiber plantations in Indonesia, enhancing cost competitiveness.

Middle East and Africa, though smaller, posts the quickest 0.75% CAGR to 2030 as governments invest in schooling, administrative capacity, and diversification agendas. Gulf countries expand secure document printing for fintech corridors, while African states standardize centralized examinations. Import flows dominate supply, offering opportunities for regional converters to establish in-market capacity that reduces freight costs. Rising urbanization stimulates premium stationery niches in metropolitan centers such as Lagos and Nairobi.

North America and Europe continue to contract in tonnage, yet remain crucial for high-margin grades and innovation leadership. UPM’s 2025 Ettringen mill closure removes 270,000 tonnes of uncoated mechanical capacity, illustrating ongoing rationalization. Mills that remain operational pivot toward specialty grades with certified sustainability attributes for discerning buyers. Despite volume decline, profitability can improve where value-added features offset lower output.

Competitive Landscape

Industry concentration is moderate: the top five producers hold roughly 55% of worldwide capacity, leaving room for regional challengers. International Paper, UPM, Stora Enso, Billerud, and Suzano pursue selective investments in specialty lines while shuttering underperforming assets. Recent deals include Suzano’s USD 3.4 billion tissue joint-venture with Kimberly-Clark, signaling diversification into adjacent fiber-based categories. [2]Suzano, “Global Tissue Company Announcement,” suzano.com

Operational efficiency remains a critical battlefield. Mills automate roll handling, deploy AI for predictive maintenance, and adopt energy-saving refiners to trim per-tonne costs. Sustainability credentials further distinguish market leaders: Life-cycle analysis, FSC or PEFC certification, and full Scope 1-3 emissions disclosure are now standard expectations among Fortune 500 buyers. Companies demonstrate compliance with the EU Deforestation Regulation through blockchain traceability or remote sensing data, locking in preferred-supplier status for European clients. [3]European Parliament & Council, “Regulation 2023/1115,” eur-lex.europa.eu

Emerging players in South Asia and MEA leverage proximity to growth markets and lower labor costs. However, capital intensity and stringent environmental norms limit unchecked expansion, favoring joint ventures with established technology partners. Innovation focuses on recycled-content optimization, barrier-coated papers for food contact, and secure substrates for digital hybrid forms, providing new revenue streams beyond conventional grades.

Writing And Printing Paper Industry Leaders

UPM-Kymmene Corporation

Stora Enso Oyj

Sappi Limited

Nippon Paper Industries Co., Ltd.

Oji Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Suzano and Kimberly-Clark formed a USD 3.4 billion tissue joint venture with 1 million tonnes annual capacity, aiming for EUR 2 billion revenue by 2030

- May 2025: Irving Pulp and Paper announced a USD 1.1 billion modernization at Saint John to lift pulp output 66% and add green energy generation

- March 2025: UPM Communication Papers confirmed the permanent closure of its Ettringen mill, removing 270,000 tonnes of capacity and saving EUR 39 million annually

- December 2024: Billerud unveiled SEK 1.4 billion investment plans to convert Escanaba and Quinnesec mills toward paperboard

Global Writing And Printing Paper Market Report Scope

| Uncoated Woodfree (UWF) |

| Coated Woodfree (CWF) |

| Uncoated Mechanical (UM) |

| Coated Mechanical (CM) |

| Office and Home Printing |

| Books and Journals |

| Magazines and Catalogs |

| Advertising and Promotional Materials |

| Stationery and School Supplies |

| Virgin Fiber |

| Recycled Fiber |

| Direct (Mill to Printer / Publisher) |

| Distributors and Wholesalers |

| Online B2B Platforms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Uncoated Woodfree (UWF) | ||

| Coated Woodfree (CWF) | |||

| Uncoated Mechanical (UM) | |||

| Coated Mechanical (CM) | |||

| By Application | Office and Home Printing | ||

| Books and Journals | |||

| Magazines and Catalogs | |||

| Advertising and Promotional Materials | |||

| Stationery and School Supplies | |||

| By Raw Material | Virgin Fiber | ||

| Recycled Fiber | |||

| By Distribution Channel | Direct (Mill to Printer / Publisher) | ||

| Distributors and Wholesalers | |||

| Online B2B Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Thailand | |||

| Indonesia | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the global writing and printing paper market?

The writing and printing paper market size is 77.78 million tonnes in 2025.

Is the writing and printing paper market growing?

No, it is expected to contract at a –0.51% CAGR, reaching 75.81 million tonnes by 2030.

Which region holds the largest share of the writing and printing paper market?

Asia-Pacific leads with 56.93% market share in 2024, driven by large-scale education and manufacturing demand.

Which segment is growing fastest within the writing and printing paper market?

Coated Woodfree by product type and Books and Journals by application have the highest CAGRs at 0.11% and 0.34%, respectively.

Who are the key players in the writing and printing paper industry?

International Paper, UPM, Stora Enso, Billerud, and Suzano rank among the largest, together accounting for about 55% of global capacity.

How are sustainability trends influencing raw material choices?

Recycled Fiber is gaining at a 0.62% CAGR as regulators and buyers push for higher recycled content and deforestation-free sourcing.

Page last updated on: