Europe Paper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

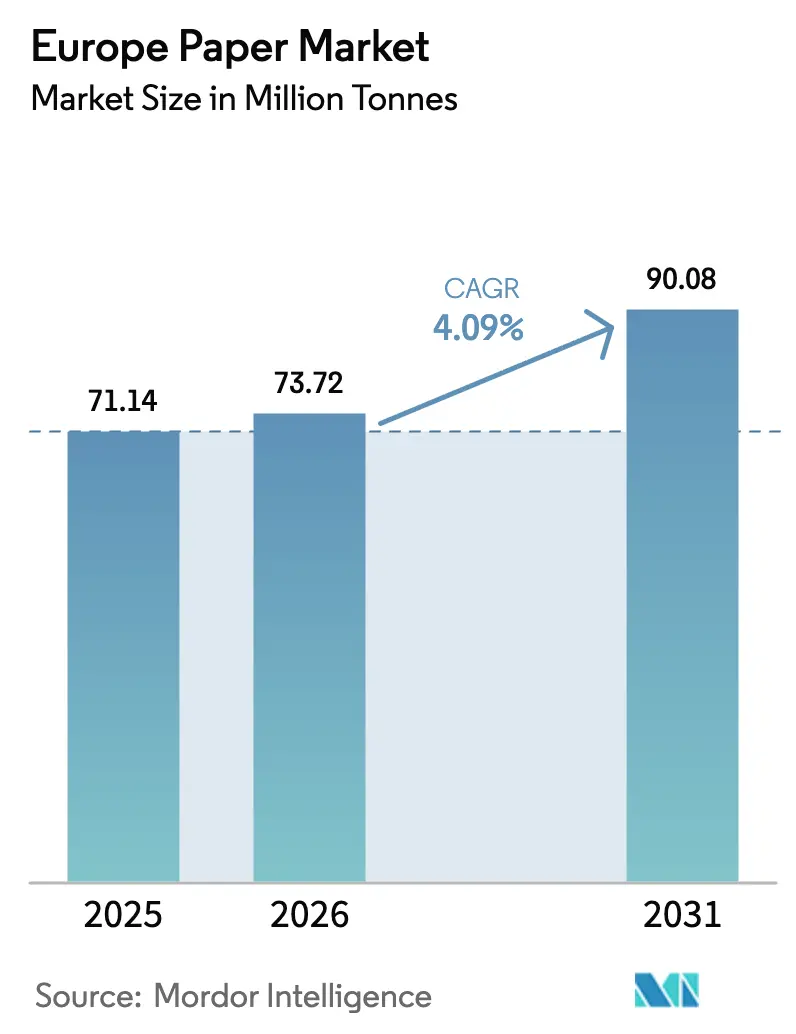

| Base Year Market Size (2025) | 71.14 Million tonnes |

| Market Volume (2026) | 73.72 Million tonnes |

| Market Volume (2031) | 90.08 Million tonnes |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Paper Market Analysis by Mordor Intelligence

The Europe paper market size is projected to be 71.14 million tonnes in 2025, 73.72 million tonnes in 2026, and reach 90.08 million tonnes by 2031, growing at a CAGR of 4.09% from 2026 to 2031. An accelerated swing toward fiber-based packaging, reinforced by the European Union’s Packaging and Packaging Waste Regulation, is the primary structural driver. Rising e-commerce volumes, expanding bans on single-use plastics, and a recycling rate already above 70% are strengthening demand for containerboard, molded-fiber foodware, and barrier-coated specialty papers. Capacity conversions away from newsprint and uncoated free-sheet continue to tighten supply in declining graphic grades while simultaneously adding momentum to containerboard and specialty substrates. Intensifying energy-price volatility and high pulp costs pressure margins, yet mills that invest in de-inking, closed-loop water systems, and bioenergy remain comparatively insulated. The merger that created Smurfit Westrock, along with Stora Enso’s and UPM’s ongoing retooling, signals deeper integration and scale economics across the supply chain.

Key Report Takeaways

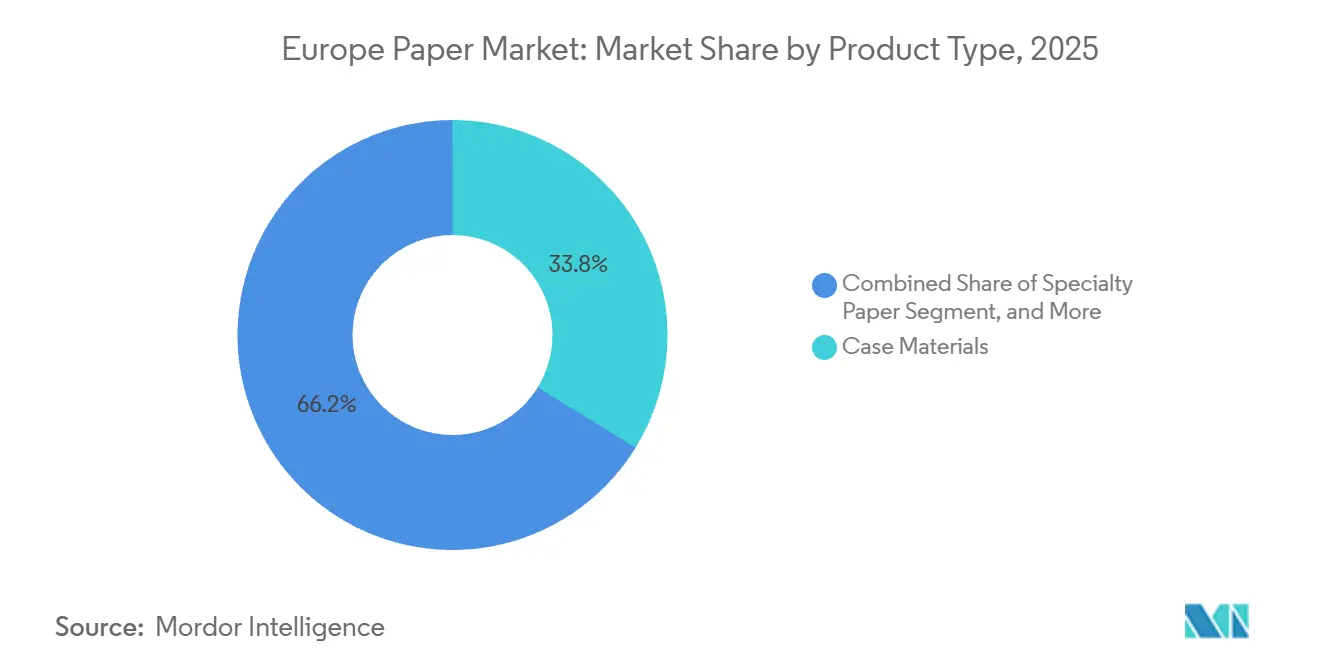

- By product type, case materials commanded 33.78% of 2025 volume, whereas specialty papers are forecast to record the fastest growth at a 5.16% CAGR through 2031.

- By raw-material source, recycled fiber accounted for 60.32% of volume in 2025, while agro-residue fiber is projected to expand at a 6.03% CAGR to 2031.

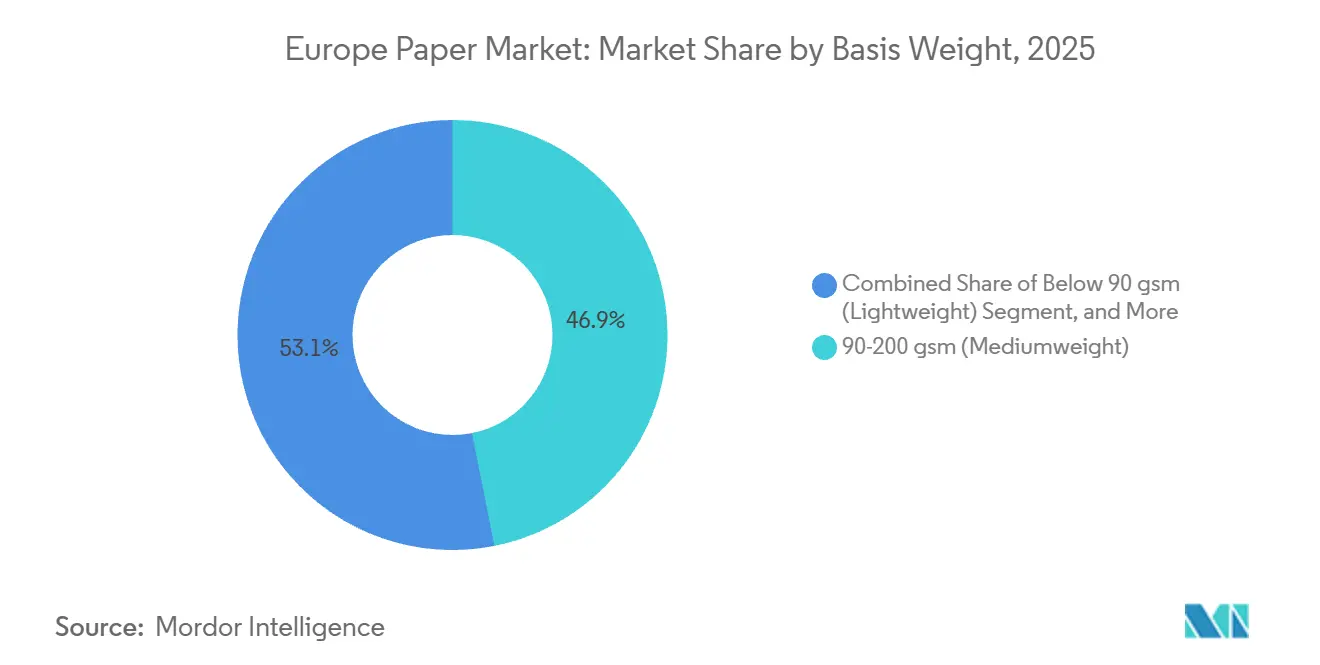

- By basis weight, the 90-200 gsm segment held 46.88% of 2025 tonnage, and grades below 90 gsm are expected to post a 5.67% CAGR over the forecast period.

- By end use, packaging and industrial applications accounted for 40.12% of volume in 2025, whereas food-service disposables are anticipated to grow the fastest at a 5.48% CAGR through 2031.

- By country, Germany captured 24.12% of regional tonnage in 2025, while Spain is projected to register the highest country-level expansion at a 6.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Use of Sustainable Packaging | +1.2% | Pan-European, with intensity in Germany, France, Netherlands | Medium term (2-4 years) |

| Expansion of E-commerce and Food-service Demand | +1.5% | Pan-European, concentrated in Germany, UK, France, Spain | Short term (≤ 2 years) |

| EU Circular-Economy Mandates on Fiber Packaging | +0.9% | EU-27, with stricter enforcement in Western Europe | Long term (≥ 4 years) |

| Rising Hygiene-Paper Consumption Post-COVID | +0.6% | Pan-European, with elevated demand in Southern Europe | Medium term (2-4 years) |

| Commercialization of 3-D Molded-Fiber Packaging | +0.4% | Early adoption in Germany, Netherlands, Scandinavia | Long term (≥ 4 years) |

| On-demand Ink-jet Corrugated Printing Adoption | +0.3% | Germany, Italy, Spain logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Use of Sustainable Packaging

Brand owners in fast-moving consumer goods and e-commerce are migrating to fully recyclable fiber packaging to comply with the EU requirement that all packaging be recyclable by 2030. Germany’s VerpackG assigns lower extended producer responsibility fees to paper solutions, tilting procurement economics toward containerboard and specialty grades certified for recyclability.[1]German Environment Agency, “VerpackG Guidelines,” UBA.DE Mondi’s MailerBAG, adopted by major e-retailers in 2024, showcases paper substrates engineered with water-based barrier chemistry that rivals polyethylene mailers in tear resistance.[2]Mondi, “MailerBAG Launch,” MONDIGROUP.COM Producers are therefore scaling de-inking, contaminant removal, and barrier-coating assets, accepting higher capital intensity to secure long-run competitiveness. Mills that close the loop with retailers gain a stable recovered-fiber supply and preferential shelf placement with sustainability-minded consumers.

Expansion of E-commerce and Food-service Demand

Online retail accounted for 23% of total European sales in 2024, boosting corrugated-box demand because single-item parcels consume more containerboard per dollar of merchandise than palletized store deliveries.[3]Eurostat, “Digital Economy and Society Statistics,” EUROSTAT.EC.EUROPA.EU Simultaneously, the Single-Use Plastics Directive eliminated polystyrene take-out ware, steering quick-service restaurants toward molded-fiber clamshells and paper straws. Huhtamaki’s 2024 Spanish capacity addition of 15,000 tonnes for molded-fiber disposables positions it to serve multinational chains as they standardize fiber formats across Europe. The combined pull from parcel logistics and food service reallocates machine time away from legacy graphic lines, widening the Europe paper market demand pool for containerboard and functional specialty papers. E-commerce’s tendency to favor variable-data printing further underpins the higher margins of digital pre-print rolls.

EU Circular-Economy Mandates on Fiber Packaging

The PPWR limits non-cellulosic components in paper packs to 5%, privileging monomaterial substrates over plastic-laminated hybrids. Member states must deploy separate collection systems for paper and cardboard by 2025, thereby improving feedstock purity and increasing the effective supply of OCC for recycled-fiber containerboard. Extended-producer-responsibility fees now scale with recyclability scores in Germany, France, and Italy, rewarding brands that strip out metalized barriers and polyethylene windows. Producers that can guarantee closed-loop chains gain a price premium, while mills without recycling operations face mounting competitive pressure. The PPWR’s scheduled PFAS limits catalyze R&D on starch- and chitosan-based barrier technologies, favoring integrated players with coating expertise.

Rising Hygiene-Paper Consumption Post-COVID

European tissue use remains 3% above 2019 per-capita levels, buoyed by hybrid work patterns that shift consumption from offices to homes. Tourism recovery returned away-from-home tissue volumes to growth in 2024, lifting demand in Spain, Italy, and Greece. Retail private labels upgraded converting lines for premium softness and embossing, intensifying competition with branded tissue leaders such as Essity. Forest-certification labels like FSC and PEFC are now table stakes, prompting mills to secure certified fiber streams or deepen de-inking for hygiene-grade recycled inputs. A resilient, premiumizing tissue segment smooths cash flow volatility for diversified producers battered by pulp price gyrations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Wood-Pulp and Recovered Paper Prices | -0.8% | Pan-European, acute in Nordic and Central European mills | Short term (≤ 2 years) |

| Digital Media Substitution of Graphic Papers | -1.1% | Pan-European, concentrated in Germany, UK, France | Long term (≥ 4 years) |

| Energy and Carbon-credit Price Inflation | -0.5% | Pan-European, severe in Germany, Poland, Czech Republic | Medium term (2-4 years) |

| Tighter Water-Use Regulations for Mills | -0.3% | Scandinavia, Germany, Austria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Wood-Pulp and Recovered Paper Prices

Northern bleached softwood kraft traded between USD 1,000 and USD 1,100 per tonne in 2024 as Canadian wildfires and Brazilian logistics hiccups disrupted supply. Recovered OCC in Germany swung from EUR 80 to EUR 120 per tonne (USD 86.4-129.6) as export demand from Asia ebbed and flowed. Cost whiplash compresses spreads for mills lacking captive pulp, forcing short-term margin sacrifice or abrupt price pass-throughs that risk customer churn. Capital-heavy vertical integration into pulp assets insulates large incumbents but raises balance-sheet leverage. Smaller independents without pulp self-sufficiency face existential risk whenever the input-cost cycle spikes.

Digital Media Substitution of Graphic Papers

CEPI logged an 8% drop in European graphic paper output in 2024, accelerating a decade-long slide as advertisers reallocate budgets to digital channels. Norske Skog shuttered its Austrian Bruck mill, removing 220,000 tonnes of newsprint and confirming the wave of closures sweeping Europe. Demand erosion leaves stranded assets, forcing costly conversions or write-downs, and drags pulp prices as mechanical and high-brightness chemical demand contracts. While diversified majors pivot to containerboard, pure-play graphic mills struggle to fund necessary retrofits, deepening regional overcapacity in a shrinking segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Case Materials Anchor Volume Growth

Case materials held 33.78% of 2025 volume within the Europe paper market, reflecting corrugated boxes’ central role in e-commerce and industrial shipping. Specialty papers are forecast to pace the field at a 5.16% CAGR to 2031, catalyzed by food-contact barrier liners, silicone-coated release carriers, and filtration media. Graphic papers slumped further in 2024, with an 8% production contraction, underscoring secular decline. Innovations such as digital pre-print on containerboard, plus PFAS-free coatings, keep specialty grades attractive for brand owners.

Sappi’s USD 43.2 million barrier-coating line in Germany exemplifies mills’ offensive push into higher-margin niches. EU recyclability caps on non-cellulosic constituents reward monomaterial cartons, fortifying demand for case materials. Containerboard also benefits from warehousing automation that favors unitized corrugated solutions. Conversely, graphic-paper lines face closure or retrofits, while sanitary grades hold steady on premium tissue demand.

By Raw-Material Source: Recycled Fiber Dominates Supply

Recycled fiber contributed 60.32% of tonnage in 2025, leveraging Europe’s mature 71.4% recycling rate. Agro-residue fiber, though a small base, is projected to expand 6.03% CAGR as mills trial wheat-straw and hemp blends to buffer pulp-price risk. Virgin fiber use persists in hygiene and high-strength grades but loses share under circular-economy directives.

Germany’s VerpackG fee matrix grants recycled-fiber packaging a clear cost edge, while Stora Enso’s Oulu conversion pivots half-a-million tonnes into recycled containerboard. Agro-residue pilots in Spain blend 20% straw with OCC without compromising box compression, signaling future scalability. Persistent NBSK volatility keeps the spotlight on diversified feedstocks, but hygiene-grade brightness and strength requirements ensure virgin kraft remains a crucial component in the Europe paper market size allocation.

By Basis Weight: Lightweighting Drives Below 90 gsm Growth

Substrates in the 90-200 gsm band controlled 46.88% of 2025 volume, valued for versatility in folding cartons and office papers. Yet grades below 90 gsm are the fastest climbers at 5.67% CAGR as shippers slice weight to curb freight emissions. Above 200 gsm stock maintains relevance where rigidity is paramount, such as beverage carriers and industrial wraps.

Digital inkjet technology improves ink lay-down, enabling converters to run 120 gsm liners in place of 150 gsm without graphic compromise. EU recyclability metrics further motivate thinner monomaterial solutions that need fewer coatings. Mondi’s 80 gsm barrier-paper, launched in 2024, delivers moisture protection equal to 120 gsm polyethylene-laminated sheets, pointing to future down-gauging potential. The Europe paper market share of sub-90 gsm grades therefore stands to widen as coating chemistries and fiber bonding advance.

By End-use Industry: Packaging Leads, Food-service Accelerates

Packaging and industrial applications absorbed 40.12% of 2025 volume, driven by containerboard, sack kraft, and industrial wraps. Food-service disposables, lifted by the plastic-ban tailwind, are poised to rise at 5.48% CAGR, shining as the fastest end-use. Printing and publishing retreat, while hygiene products provide steady ballast through premium tissue offerings.

Huhtamaki’s additional 15,000 tonnes in Spanish molded-fiber plates answers quick-service restaurants’ region-wide fiber substitution. Parcel proliferation keeps containerboard machines at high utilization. Shift toward take-away dining compounds per-meal packaging intensity, adding momentum. Graphic-paper decline remains irreversible, steering capital toward board and specialty plants that backstop future Europe paper market size expansion.

Geography Analysis

Germany accounted for 24.12% of 2025 tonnage, underpinned by 19.2 million tonnes of output and robust industrial packaging demand. Spain, however, is forecast to log a 6.11% CAGR, leveraging Saica’s USD 194.4 million Zaragoza expansion and proximity to North African export routes. France, Sweden, and Italy grow at mid-single-digit rates, while Eastern Europe benefits from nearshoring supply chains.

Southern, Western, and Northern Europe contribute distinct demand profiles. In Western Europe, Germany, France, and the Netherlands lead in containerboard throughput, benefiting from strong e-commerce logistics corridors. Policy frameworks such as Germany’s VerpackG anchor high recycling rates, ensuring a stable OCC stream for mills. Municipal collection upgrades across France raise feedstock purity, supporting specialty and hygiene grades.

Southern Europe’s growth is anchored in Spain and Italy. Spain’s Zaragoza and Valencia corridors support containerboard capacity catering to export-oriented produce and seafood sectors. Italy’s vibrant food and luxury goods industry underwrites premium folding cartons and label stock demand. Rising adoption of molded-fiber disposable tableware, combined with high tourist arrivals, accelerates tonnage gains in the region.

Northern Europe leverages an integrated forestry supply chain, allowing Finland and Sweden to feed virgin kraft into high-strength packaging and tissue. Bio-powered turbines and district heating schemes moderate energy cost exposure, partially offsetting carbon-credit expenses. The region also pilots enzymatic pulping and lignin by-product valorization, hinting at future value pools that could bolster the Europe paper market share of high-performance substrates.

Competitive Landscape

The market is signifying moderate concentration. Smurfit Westrock’s USD 34 billion union increases its clout over recovered-paper procurement and retail contracts, streamlining a Europe-wide mill-and-box-plant network. Stora Enso, UPM-Kymmene, Mondi, and Metsa Group focus on high-return conversions and specialty assets, progressively pruning legacy graphic capacity.

Investment patterns gravitate toward recycled-fiber containerboard, PFAS-free barrier specialty lines, and energy-efficient drying systems. Sappi’s USD 43.2 million German barrier-coating line taps into premium, non-plastic food wraps. Saica, a privately held challenger, expands its Spanish recycled linerboard, capturing share in fast-growing Iberian and export niches. Technology adoption around closed-loop water, AI-driven quality control, and on-demand corrugated printing is becoming a differentiator for margin resilience.

Startups pursuing agricultural-residue pulping and molded-fiber electronics cushioning inject competitive dynamism but must scale to compete on cost. Patent filings emphasize starch-based barrier chemistries, enzymatic pulping, and hybrid flexo-digital presses. Overall, capability to meet tightening environmental rules while keeping costs contained defines the trajectory for winners in the Europe paper market.

Europe Paper Industry Leaders

Stora Enso Group

UPM-Kymmene Corporation

Mondi plc

Metsa Group

Smurfit Westrock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Mondi committed EUR 120 million (USD 129.6 million) to expand its Ružomberok mill in Slovakia, adding 150,000 tonnes of annual kraft-paper capacity and a biomass energy plant, with start-up slated for Q4 2027.

- January 2026: UPM earmarked EUR 150 million (USD 162 million) to convert its Nordland mill in Germany from graphic papers to 200,000 tonnes of barrier-coated specialty packaging, targeting plastic-free food applications.

- December 2025: Smurfit Westrock finished a EUR 90 million (USD 97.2 million) upgrade at its Nettingsdorf mill in Austria, adding 250,000 tonnes of recycled containerboard capacity and advanced de-inking systems for food-grade output.

- November 2025: Stora Enso entered a strategic partnership with Finnish biotech firm Spinnova to commercialize wood-based textile fibers, with pilot production scheduled for Q2 2026 at the Enocell mill in Finland.

Europe Paper Market Report Scope

The Europe Paper Market encompasses the production, and consumption of various paper products across the region. It includes a wide range of product types, raw-material sources, basis weights, and end-use industries, catering to diverse applications such as packaging, printing, hygiene, and food-service disposables.

The Europe Paper Market Report is Segmented by Product Type (Graphic Papers, Case Materials, Sanitary and Household, Wrappings, Carton Board, and Specialty Papers), Raw-Material Source (Virgin Fiber, Recycled Fiber, and Agro-Residue Fiber), Basis Weight (Below 90 gsm, 90-200 gsm, and Above 200 gsm), End-use Industry (Packaging and Industrial, Printing and Publishing, Hygiene and Sanitary, Food-service Disposables, and Other End-use Industries), and Country (Germany, France, Sweden, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tonnes).

| Graphic Papers | Newsprint |

| Other Graphic Papers | |

| Case Materials | |

| Sanitary and Household | |

| Wrappings | |

| Carton Board | |

| Specialty Papers |

| Virgin Fiber |

| Recycled Fiber |

| Agro-Residue Fiber |

| Below 90 gsm (Lightweight) |

| 90-200 gsm (Mediumweight) |

| Above 200 gsm (Heavyweight) |

| Packaging and Industrial |

| Printing and Publishing |

| Hygiene and Sanitary |

| Food-service Disposables |

| Other End-use Industries |

| Germany |

| France |

| Sweden |

| Italy |

| Spain |

| Rest of Europe |

| By Product Type | Graphic Papers | Newsprint |

| Other Graphic Papers | ||

| Case Materials | ||

| Sanitary and Household | ||

| Wrappings | ||

| Carton Board | ||

| Specialty Papers | ||

| By Raw-Material Source | Virgin Fiber | |

| Recycled Fiber | ||

| Agro-Residue Fiber | ||

| By Basis Weight | Below 90 gsm (Lightweight) | |

| 90-200 gsm (Mediumweight) | ||

| Above 200 gsm (Heavyweight) | ||

| By End-use Industry | Packaging and Industrial | |

| Printing and Publishing | ||

| Hygiene and Sanitary | ||

| Food-service Disposables | ||

| Other End-use Industries | ||

| By Country | Germany | |

| France | ||

| Sweden | ||

| Italy | ||

| Spain | ||

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe paper market be by 2031?

The market is forecast to reach 90.08 million tonnes by 2031, supported by steady 4.09% CAGR growth in recycled containerboard and specialty papers.

Which product segment is expanding the fastest?

Specialty papers, particularly barrier-coated and release-liner grades, are projected to grow at a 5.16% CAGR through 2031.

Why is Spain the fastest-growing country in European paper?

New recycled-containerboard capacity, favorable EPR incentives, and access to North African export channels lift Spains expected 6.11% CAGR.

How are EU regulations shaping material choices?

The PPWR caps non-cellulosic content at 5% and mandates recyclability, which tilts converters toward monomaterial fiber packs and boosts demand for containerboard.

What strategies help mills manage pulp-price volatility?

Vertical integration into pulp assets, long-term OCC supply contracts, and diversification into agro-residue fiber blends mitigate input-cost swings.

Which technologies are redefining competitiveness?

Closed-loop water systems, PFAS-free starch barriers, and on-demand inkjet corrugated printing cut costs, meet stricter ESG rules, and unlock higher-margin digital customization.

Page last updated on: