Manual Toothbrush Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

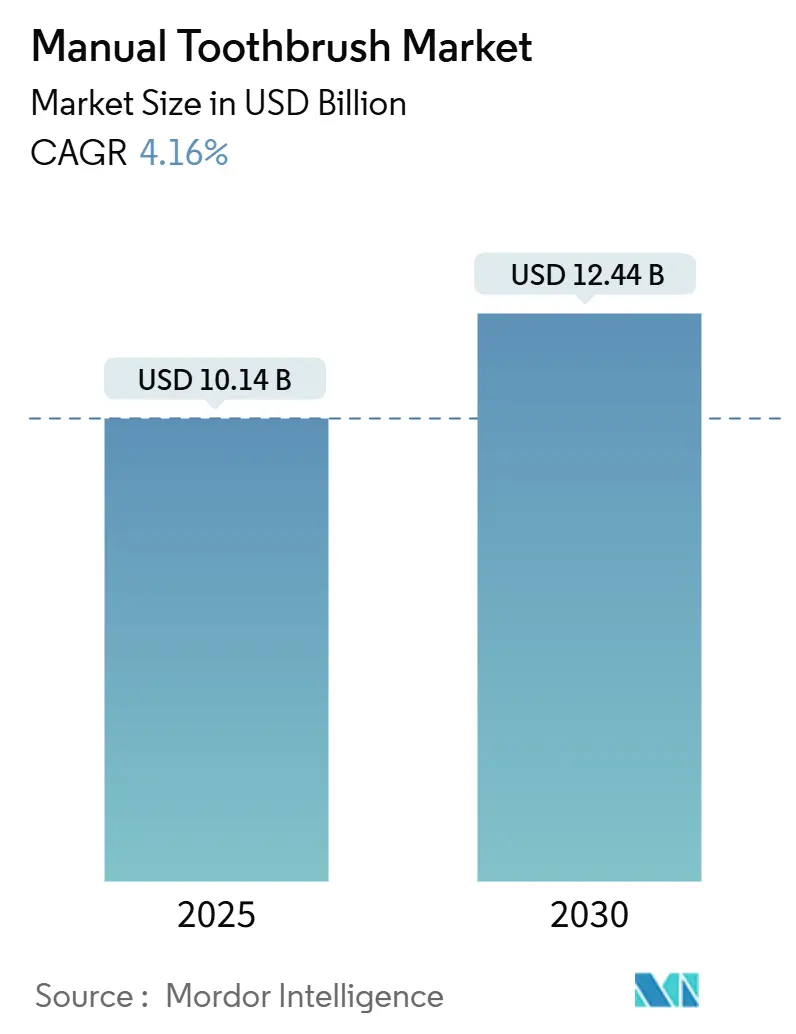

| Market Size (2025) | USD 10.14 Billion |

| Market Size (2030) | USD 12.44 Billion |

| Growth Rate (2025 - 2030) | 4.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Manual Toothbrush Market Analysis by Mordor Intelligence

The global manual toothbrush market size is valued at USD 10.14 billion in 2025 and is projected to reach USD 12.44 billion by 2030, exhibiting a CAGR of 4.16% during the forecast period. Driven by essential oral hygiene needs and cost-effectiveness, the global manual toothbrush market is witnessing steady growth, solidifying its status as a staple in both developed and emerging markets. Even with the surge of electric alternatives, manual toothbrushes hold their ground, thanks to their affordability, user-friendliness, and innovations in bristle design and eco-friendly materials. The World Health Organization (2024) highlights a pressing need for oral hygiene: in the Western Pacific Region, about 800 million people, or 42% of the population, grapple with oral diseases, from untreated dental caries to gum diseases and tooth loss [1]Source: World Health Organization, “Oral Health Western Pacific Region,” who.int. This urgency is particularly pronounced in lower- and middle-income regions, where cost-sensitive consumers seek basic yet effective dental care. Consumer preferences are evolving: there's a rising inclination towards soft-bristled toothbrushes, driven by heightened awareness of gum sensitivity. While plastic toothbrushes currently dominate the market, sustainability concerns are prompting manufacturers to rethink materials and designs. Adults remain the primary users, but products tailored for children are swiftly capturing market share, owing to preventive dental initiatives and heightened parental awareness.

Key Report Takeaways

- By bristle type, hard bristles captured 58.15% of the manual toothbrush market share in 2024, whereas soft bristles are forecast to expand at a 4.76% CAGR through 2030.

- By material, plastic accounted for 95.43% of the manual toothbrush market size in 2024, and wood/bamboo options are poised for a 6.63% CAGR between 2025-2030.

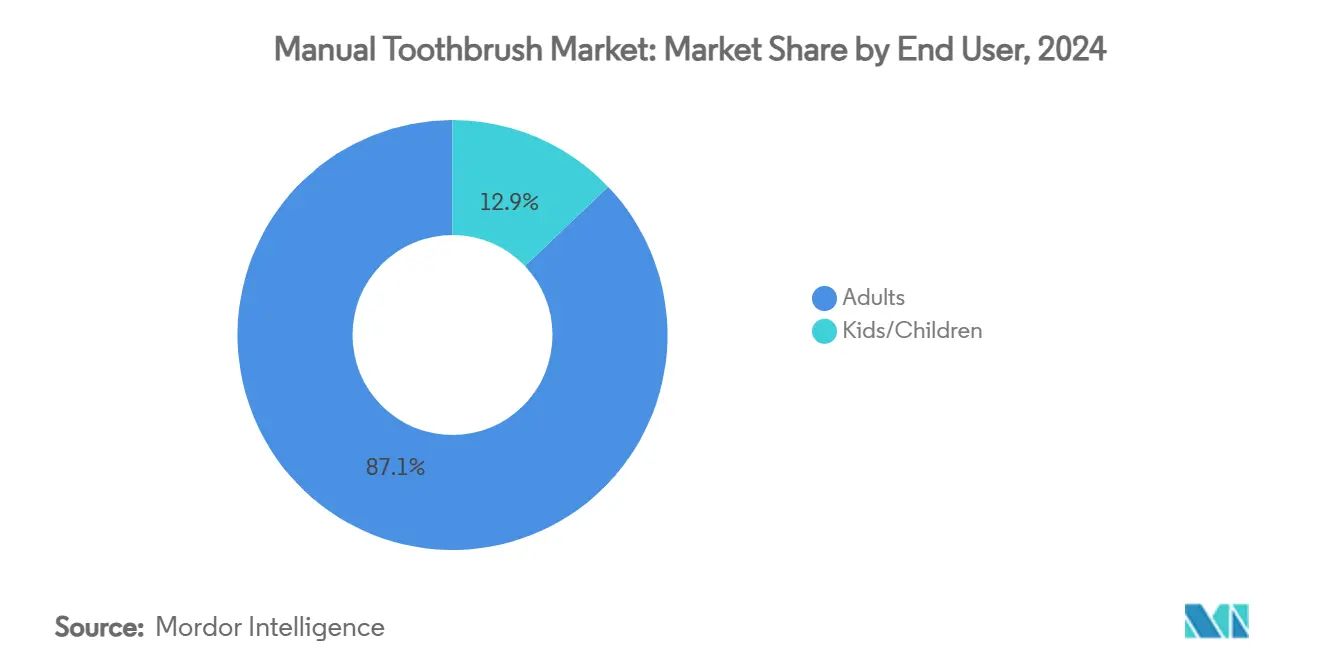

- By end-user, adults held 87.12% of the manual toothbrush market share in 2024, while the children segment records the highest projected CAGR at 5.72% to 2030.

- By distribution channel, supermarkets/hypermarkets represented 39.72% of the manual toothbrush market size in 2024, and online retail is advancing at a 5.84% CAGR through 2030.

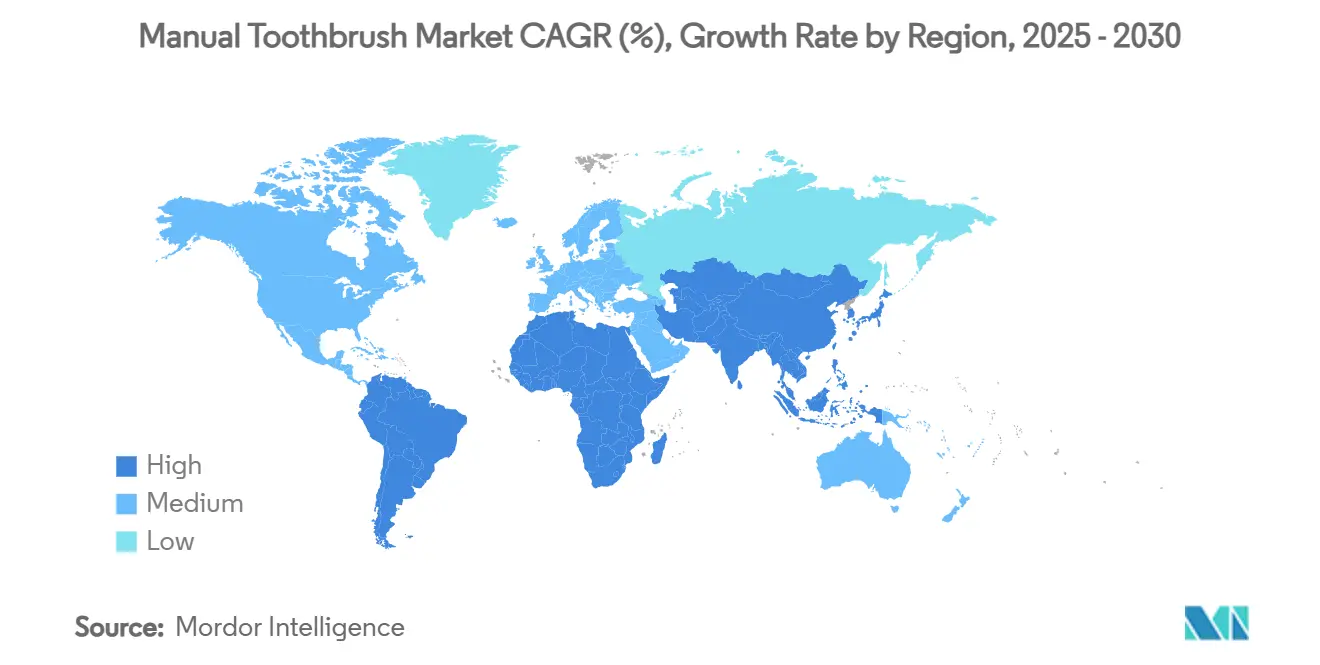

- By geography, Asia-Pacific commanded 35.76% of the manual toothbrush market share in 2024 and is also the fastest-growing region with a 4.87% CAGR to 2030.

Global Manual Toothbrush Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer awareness of oral hygiene | +0.8% | Global; stronger in Asia-Pacific and South America | Medium term (2-4 years) |

| Rising prevalence of dental disorders | +0.6% | Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Demand for eco-friendly toothbrushes | +0.4% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Government initiatives on oral hygiene | +0.3% | United Kingdom, Brazil, India, Pacific islands | Short term (≤ 2 years) |

| Aggressive marketing and advertising | +0.2% | Global competitive markets | Short term (≤ 2 years) |

| Affordability and accessibility | +0.5% | Emerging Asia-Pacific, South America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Awareness of Oral Hygiene

Heightened consumer awareness of the connection between oral and systemic health is propelling the growth of the manual toothbrush market. Public health data and targeted campaigns are directly shaping consumer behavior and purchase choices. According to Delta Dental’s 2024 State of America’s Oral Health Report, a significant 92% of adults recognize the link between oral and overall health. Furthermore, 91% deem dental visits crucial, leading to a commendable 74% adherence to suggested oral hygiene practices [2]Source: Delta Dental Plans Association, “State of America’s Oral Health Report 2024,” deltadental.com. Global initiatives echo this sentiment: the World Health Organization warns that by 2025, 3.5 billion individuals will grapple with oral diseases, highlighting the critical need for daily care [3]Source: World Health Organization, “Oral Health Fact Sheet 2025,” who.int. In light of this, parents from underserved regions are increasingly turning to preventive measures, opting for fluoride toothbrushes and educational resources. Colgate’s 2023 initiative, “Bright Smiles, Bright Futures,” underscores this trend. The campaign not only broadened school-based oral health education but also provided free toothbrushes to underprivileged communities in the U.S. Such initiatives not only enhance access but also cultivate enduring habits, solidifying the role of manual toothbrushes in healthcare and broadening their market reach across diverse socioeconomic groups.

Rising Prevalence of Dental Disorders

Growing dental health concerns among all age groups are driving a surge in demand for both basic and advanced manual toothbrushes, leading to market innovations and targeted product developments. In 2024, 47% of U.S. adults aged 30 and older reported suffering from periodontitis, steering the market towards gum-care-focused manual toothbrushes[4]Source: American Dental Association, “2024 Adult Periodontal Evaluation Report,” ada.org. These specialized brushes boast ultra-soft bristles, contoured heads, and ergonomic handles, all designed to alleviate pressure on inflamed areas. Meanwhile, oral health challenges in children are prompting a notable diversification in products. In the 2023–24 dental screening cycle, 22.4% of five-year-olds in the UK exhibited visible tooth decay [5]Source: Office for Health Improvement and Disparities, “Oral Health Survey of 5-Year-Old Schoolchildren: 2024,” gov.uk. This statistic has intensified the demand for child-friendly manual toothbrushes, which now come with engaging features like vibrant designs, timers, and easy-grip handles to boost compliance. Brands such as Jordan and Colgate have swiftly adapted, launching dedicated lines for children. Colgate’s "Kids Extra Soft" series, for instance, showcases animal-shaped brushes paired with brushing guides. As these consumer expectations evolve in light of heightened oral health concerns, the manual toothbrush market is witnessing simultaneous growth in both volume and value, spanning both mass and premium segments.

Increasing Demand for Eco-Friendly and Sustainable Toothbrushes

In the manual toothbrush market, a surge in demand for eco-friendly products is reshaping consumer behavior, spurring product innovation and expanding market segments. Millennials and Gen Z consumers are increasingly shunning plastic hygiene tools, opting instead for biodegradable or recyclable alternatives, thereby aligning their oral care choices with broader environmental values. In 2024, The Humble Co. announced a 32% year-over-year surge in global sales of its bamboo manual toothbrushes, underscoring a rising preference for compostable materials. Major retailers, including Target and Boots, have responded by expanding shelf space for sustainable toothbrush brands, buoyed by strong sales and positive consumer feedback. In India, the 2023 “Swachh Smiles” initiative, championed by local NGOs and state governments, advocated for plastic-free oral hygiene in rural regions. This push resulted in heightened demand for neem-wood and bamboo toothbrushes at community health centers. On the global stage, manufacturers like Colgate are amplifying their eco-conscious offerings, introducing products like the Colgate Keep and Colgate Bamboo Charcoal series, which prioritize minimal plastic use and recyclable packaging. These industry shifts are further bolstered by policy measures, notably the EU’s directive on curbing single-use plastics, nudging manufacturers to rebrand their manual toothbrush lines with a sustainability focus.

Aggressive Marketing and Advertising

In the manual toothbrush market, aggressive and innovative marketing strategies are reshaping consumer behavior and fueling growth. Campaigns that effectively bridge the gap between awareness and action stand out. Colgate India’s 2025 “Indianis Dentris” campaign addressed the common oversight of infrequent toothbrush replacements. They introduced a new flower species resembling a frayed toothbrush, emphasizing the 3-month replacement rule through engaging storytelling and dynamic social media activations. This fresh tactic not only heightened engagement but also directly impacted replacement frequency. On another front, premium D2C brand Perfora has engaged India’s younger urbanites. Through influencer-led promotions, they spotlighted the Perfora Soft Manual Brush, packaged with oral care kits, targeting Gen Z's aesthetic and preventive care priorities. Such strategies have nudged consumers towards premium, design-centric manual toothbrushes. Colgate-Palmolive, not to be outdone, segments the market psychographically. Their promotion of the Charcoal Clean Manual Brush resonates with health-conscious consumers seeking natural solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High competition and market saturation | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Shift toward electric toothbrushes | -0.5% | High-income segments worldwide | Medium term (2-4 years) |

| Environmental concerns around plastic waste | -0.2% | EU; spreading to North America | Medium term (2-4 years) |

| Traditional tooth-cleaning practices | -0.4% | Rural Sub-Saharan Africa, South Asia, Middle East | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

High Competition and Market Saturation

In mature and price-sensitive regions, growth in the manual toothbrush segment faces mounting constraints due to heightened competition and market saturation. The commoditized nature of manual toothbrushes, coupled with low entry barriers, has spurred a surge of brands offering nearly identical products at slight price differences, amplifying downward pricing pressures. In saturated markets like North America and Western Europe, dominant players such as Colgate-Palmolive and Oral-B command shelf space, restricting opportunities for smaller or newer entrants to carve out a niche. Moreover, consumer fatigue with undifferentiated products has stunted volume growth; a trend evident in Japan, despite nationwide hygiene campaigns, toothbrush replacement rates have plateaued. While demand continues to rise in emerging markets, local manufacturers have flooded the low-end segment, igniting fierce price wars that squeeze margins and curtail investments in product innovation. E-commerce giants like Amazon and Flipkart are inundated with generic manual toothbrush listings, complicating brand visibility without hefty advertising expenditures. Collectively, these dynamics foster a crowded competitive landscape characterized by weak brand loyalty, minimal product differentiation, and squeezed profitability, ultimately hindering long-term market growth.

Shift towards Electric Toothbrushes

Electric toothbrushes are swiftly overtaking their manual counterparts, both in market share and innovation. As consumers, especially the younger urban crowd, link oral care quality to tech advancements, manual brushes are often seen as relics of the past. Brands such as Oral-B and Perfora are seizing this sentiment, directing their research and developments, ad budgets, and influencer collaborations predominantly towards electric toothbrushes, sidelining manual ones. Take Oral-B, for instance: while it promotes its sustainable manual variant, the Clic, the brand's primary focus remains on its AI-driven electric models, drawing both consumer interest and retail shelf space away from manual options. This strategic pivot is tightening the price elasticity of manual brushes, challenging brands to either raise margins or introduce premium features without being overshadowed by the perceived clinical edge of electric brushes. Moreover, the aspirational allure of electric brushes, bolstered by social media buzz and endorsements from dentists, is redefining consumer loyalty, particularly among premium and health-focused buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bristle Type: Soft Bristles Gain Clinical Endorsement

In 2024, hard/medium bristle manual toothbrushes jointly captured 58.15% of the market share. Consumers, especially in regions with limited dental literacy or a cultural tilt towards vigorous brushing, often believe that firmer bristles offer superior cleaning. Medium bristles strike a balance, merging effectiveness with gentleness. For instance, Oral-B’s “Shiny Clean Medium” line enjoys robust retail success in South America, a region where medium bristles are the go-to choice. Brands like Close-Up and Dento have tailored their offerings, ensuring they resonate within these lucrative segments.

Conversely, soft bristle toothbrushes are the segment to watch, boasting a 4.76% CAGR, owing to endorsements from professionals and a growing awareness of gum health. Colgate, in 2024, unveiled its “Gum Expert UltraSoft” line in Southeast Asia, bolstered by influencer campaigns that spotlighted its safe, daily use. The momentum is further fueled by social media, with dentists advocating soft bristles to mitigate gum recession and enamel wear. While features like indicator bristles and ergonomic handles are found across all bristle types, the rising preference for soft bristles underscores a significant shift towards preventive oral care and tailored product choices.

By Material: Sustainability Drives Wood/Bamboo Surge

In 2024, plastic manual toothbrushes command a dominant 95.43% market share, buoyed by their cost efficiency, extensive distribution networks, and established manufacturing bases. Their stronghold is particularly evident in regions sensitive to pricing and those with limited infrastructure. A pivotal factor bolstering this supremacy is the advent of hybrid manual toothbrush designs. Innovations like recyclable bristles and reusable handles cater to the rising environmental consciousness, all while keeping affordability intact. A case in point is Colgate’s Keep manual toothbrush, which boasts a reusable aluminum handle paired with replaceable plastic heads, showcasing brands' responsiveness to the demand for sustainable yet budget-friendly manual options.

Meanwhile, bamboo and wooden manual toothbrushes are on a rapid ascent, charting a 6.63% CAGR. This surge is fueled by heightened environmental awareness and a growing appetite for plastic-free choices. Pioneering this movement, brands such as The Humble Co. and Brush with Bamboo are introducing biodegradable handles and compostable packaging, directly appealing to eco-aware consumers. Additionally, the “Others” segment, spotlighting innovations like neem-fiber and wheat-straw handles, underscores a trend. Especially in regions like India, there's a burgeoning emphasis on local materials, marrying sustainability with traditional health practices in product development.

By End-User: Children's Segment Accelerates

In 2024, adults dominated the manual toothbrush market, accounting for 87.12% of the share. This stronghold is attributed to ingrained oral care habits and a wide array of product choices. Premium brands, such as Colgate's SlimSoft Charcoal and Sensodyne’s soft-bristle variants, cater to adults, addressing concerns like sensitivity and plaque. By incorporating features like ergonomic handles and ultra-fine bristles, these brands carve out a niche in a crowded market, bolstering adult loyalty through specialization and trust.

Meanwhile, the kids/children's segment is witnessing the fastest growth, boasting a 5.72% CAGR. This surge is bolstered by proactive government measures and innovations tailored for young users. A case in point is the UK’s Supervised Toothbrushing Programme, which mandates daily brushing in nurseries of underprivileged areas, driving consistent demand for children's manual toothbrushes (Department of Health and Social Care, 2025). To further engage the young audience, brands like Colgate and Jordan have rolled out age-tailored brushes adorned with vibrant characters, equipped with suction bases and timers.

By Distribution Channel: Online Retail Transforms Access

In 2024, supermarkets and hypermarkets accounted for a dominant 39.72% share of manual toothbrush sales. This preference stems from consumers wanting to personally assess bristle texture, handle grip, and price. Retailers, including DMart in India and Tesco in the UK, have seen mass-market plastic toothbrushes command significant shelf space, especially during oral care discount cycles and bundled offers. Highlighting this trend, Tesco's 2024 consumer insights revealed that over 70% of manual toothbrushes were purchased in-store during regular grocery trips, with a particular emphasis on multi-pack plastic options. This widespread availability is especially pronounced in lower-income and suburban markets.

Online retail, witnessing a robust 5.84% CAGR, emerges as the fastest-growing channel. This surge is fueled by a growing appetite for sustainable manual toothbrushes and the allure of convenient repeat purchases. Brands such as The Humble Co. and Mamaearth have adeptly tapped into this momentum, rolling out bamboo toothbrush subscription packs on platforms like Amazon and their proprietary websites. Meanwhile, Hubble Hygiene, a startup championing biodegradable toothbrushes, reported a notable 30% uptick in quarterly sales in 2024. This was achieved through strategic sales on Flipkart and Nykaa, specifically targeting eco-conscious millennials and Gen Z. E-commerce not only allows brands to sidestep the traditional shelf-space tussle but also facilitates direct engagement with consumers in search of eco-friendly options, bolstering market growth in both premium and niche segments.

Geography Analysis

In 2024, Asia-Pacific dominates with a 35.76% market share and leads with a 4.87% CAGR growth rate through 2030. Factors like population density, proactive oral health campaigns, and the penetration of affordable products drive this surge. India's National Oral Health Program has begun distributing manual toothbrushes in school hygiene kits. Meanwhile, Colgate's "Bright Smiles, Bright Futures" initiative has successfully reached over 160 million children, promoting early adoption. Systema, a brand under Japan's Lion Corporation, dominates the premium manual toothbrush market in Asia. With a focus on ergonomic handle designs and ultra-fine bristles, Systema addresses the needs of consumers with sensitive gums.

North America and Europe, despite their maturity, are leveraging premiumization and sustainability for growth. Brands like Switzerland's Curaprox and Sweden's TePe are broadening their eco-friendly manual toothbrush lines, incorporating recycled plastic and bioplastic handles. Regulatory measures further bolster these trends. For instance, France's prohibition on specific non-recyclable dental products has catalyzed innovation, leading to the emergence of biodegradable manual brushes. This positions Europe at the forefront of material transformation and lucrative high-margin growth.

Moderate yet promising growth is evident in the Middle East and South America, driven by public health initiatives and the expansion of urban retail. In Brazil, the Ministry of Health's "Brasil Sorridente" program is distributing free oral hygiene kits, including manual toothbrushes. This initiative aims to enhance access in underserved areas. Meanwhile, the 2024 Dubai Dental Conference in the United Arab Emirates highlighted innovations in manual toothbrushes from regional startups. These startups are catering to Islamic oral care traditions, introducing products like miswak-infused brushes. Such initiatives illustrate how public policy, cultural traditions, and urban growth are cultivating consumer bases in niche or previously underserved oral care markets.

Competitive Landscape

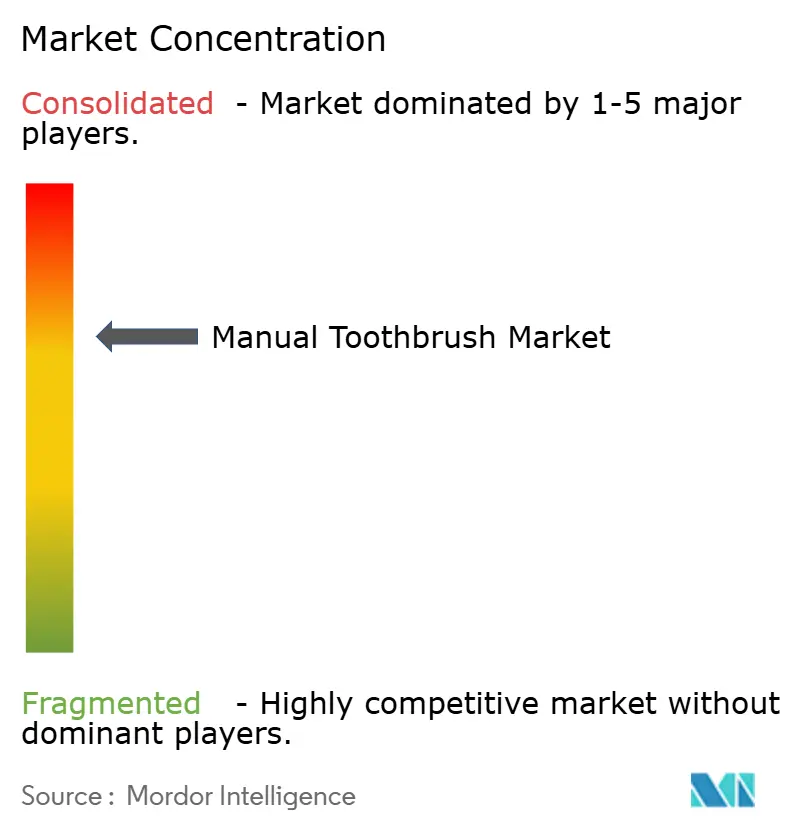

The market exhibits moderate consolidation. The established players in the manual toothbrush market, such as Colgate, leverage strong brand equity, endorsements from dental professionals, and prominent retail visibility to maintain their dominance. Colgate caters to diverse income groups, marketing both mass-market brushes and premium lines like Colgate SlimSoft. In Europe, brands like TePe and Curaprox, backed by dental endorsements, highlight sustainability to appeal to eco-conscious consumers.

In a market often seen as commoditized, technology-driven product enhancements emerge as key differentiators. Innovations in bristle shape, density, and handle ergonomics create perceptions of clinical superiority. For instance, Perfora's premium line, featuring antibacterial silver bristles, appeals to Gen Z and millennials. Some brands are even exploring sensor-embedded manual toothbrushes that sync with mobile apps, blending traditional brushing with digital hygiene tracking.

Brands are honing in on underserved markets, championing sustainability, and pioneering direct-to-consumer (D2C) strategies. Procter & Gamble’s Oral-B, with its 60% less plastic "Clic" model, epitomizes the industry's pivot towards eco-design without compromising brand identity.

Manual Toothbrush Industry Leaders

Colgate‑Palmolive Company

Procter & Gamble Company

Unilever PLC

Sunstar Suisse SA

Haleon plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Woongjin Thinkbig introduced an eco-friendly bamboo manual toothbrush to extend its personal-care range.

- August 2024: The Humble Co. rolled out a bamboo brush using fully recyclable paper packaging to deepen its sustainable offering.

Global Manual Toothbrush Market Report Scope

| Hard/Medium Bristle |

| Soft Bristle |

| Plastic |

| Wood/Bamboo |

| Others |

| Adults |

| Children/Kids |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Pharmacies/Drug Stores |

| Online Retaile Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| By Bristle Type | Hard/Medium Bristle | |

| Soft Bristle | ||

| By Material | Plastic | |

| Wood/Bamboo | ||

| Others | ||

| By End-User | Adults | |

| Children/Kids | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Pharmacies/Drug Stores | ||

| Online Retaile Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current manual toothbrush market size?

The manual toothbrush market size stood at USD 10.14 billion in 2025 and is projected to reach USD 12.44 billion by 2030.

Which region leads the manual toothbrush market?

Asia-Pacific holds the lead with 35.76% share in 2024 and posts the fastest 4.87% CAGR through 2030.

Why are soft-bristled toothbrushes gaining popularity?

Soft bristles reduce gum abrasion and align with dental-professional guidance, fueling a 4.76% CAGR that outpaces harder variants.

What distribution channel is growing fastest?

Online retail shows a 5.84% CAGR, driven by subscription models and influencer-led direct-to-consumer brands.

Page last updated on: