Household Cleaners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 170.47 Billion |

| Market Size (2031) | USD 213.76 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

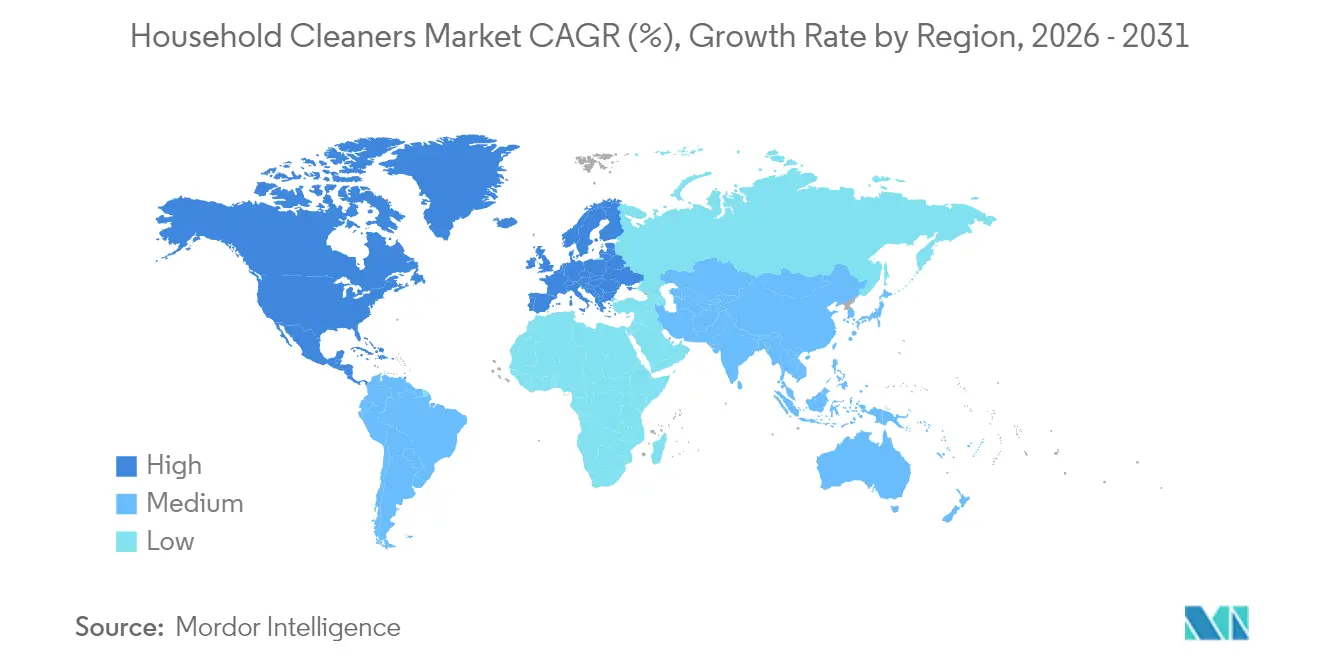

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Household Cleaners Market Analysis by Mordor Intelligence

The household cleaners market size in 2026 is estimated at USD 170.47 billion, growing from 2025 value of USD 162.93 billion with 2031 projections showing USD 213.76 billion, growing at 4.63% CAGR over 2026-2031. The pandemic heightened hygiene awareness, ensuring essential cleaning items remain staples on shopping lists, even amidst tighter household budgets. This trend is further bolstered by rising health concerns, notably malaria and dengue. For instance, the World Health Organization reported in 2023 that the Western Pacific region saw approximately 1.75 million malaria cases, with Nigeria alone representing 30.9% of global malaria deaths[1]Source: World Health Organization, "World Malaria Report 2024", who.int. Moreover, leading brands are now incorporating probiotic and plant-based formulas, meeting both efficacy and sustainability demands, allowing premium brands to maintain their price points. While Asia-Pacific leads in volume demand, Europe is making swift strides, propelled by stringent biodegradability laws favoring concentrated, low-impact surfactants. The rise of online retailers, subscription models, and smart home devices is not only ensuring predictable replenishment cycles but also strengthening consumer-brand loyalty.

Key Report Takeaways

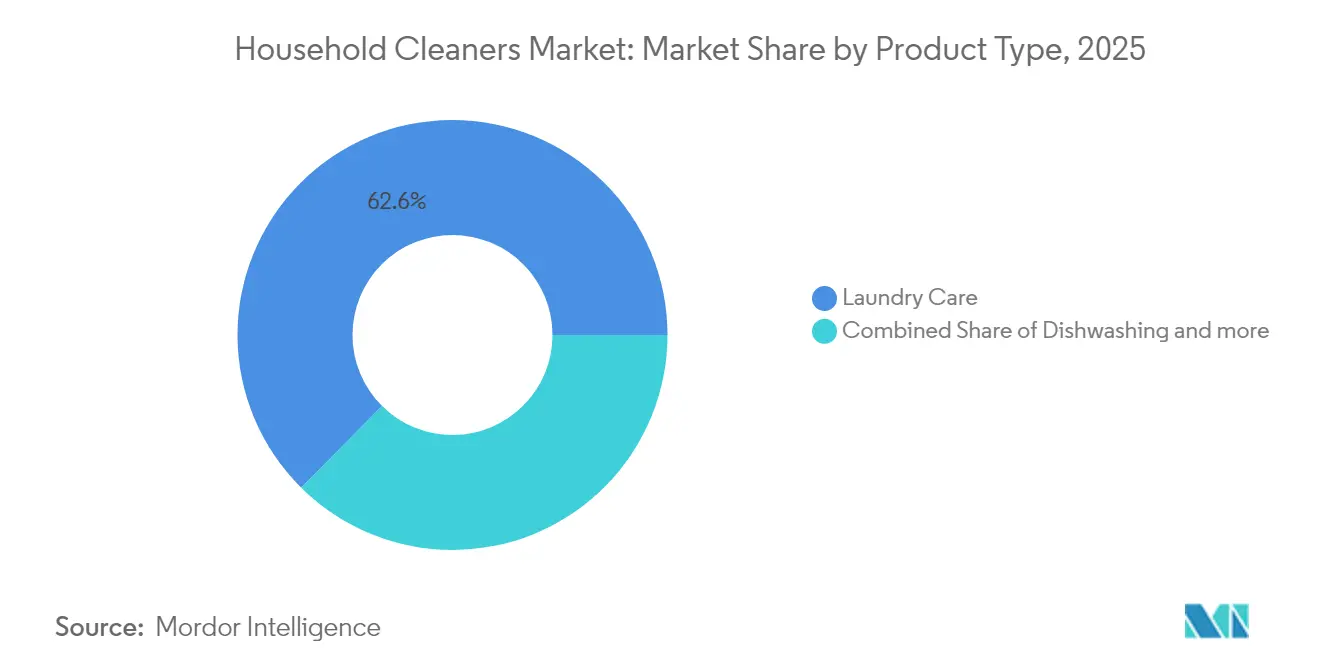

- By product type, laundry care accounted for 62.58% of the household cleaners market share in 2025, while dishwashing products recorded the highest projected CAGR at 6.08% through 2031.

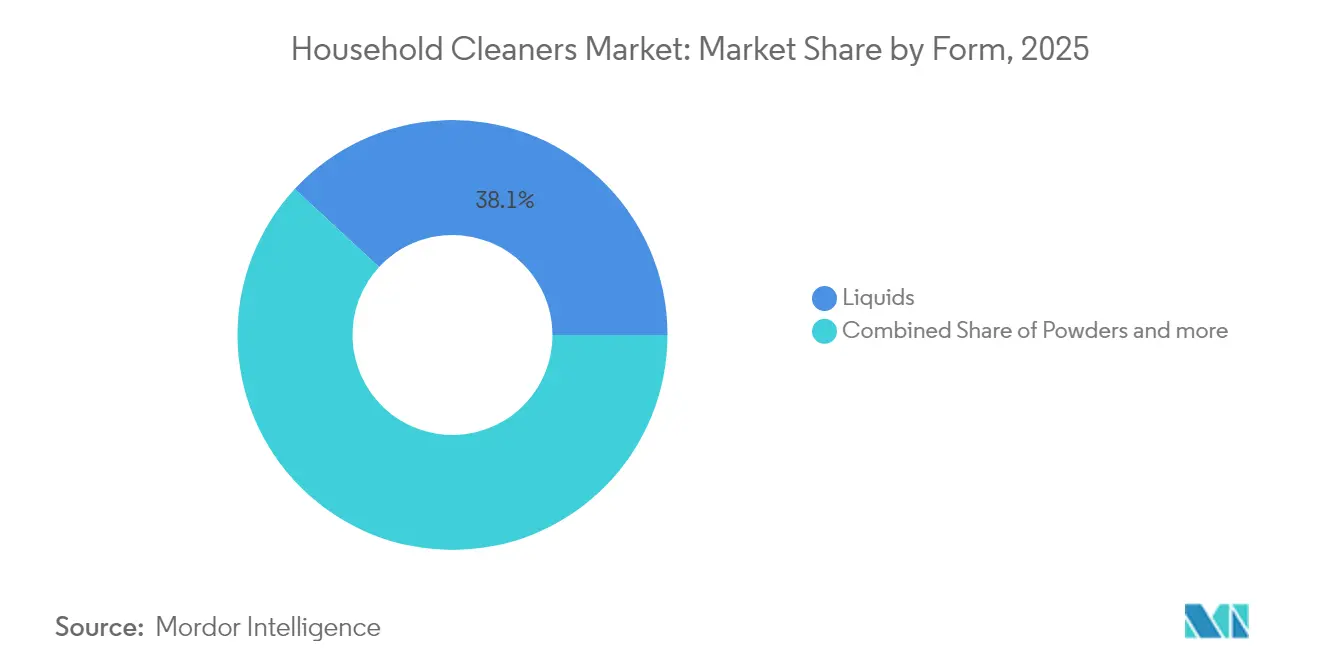

- By form, liquids led with 38.12% revenue share in 2025; powders are forecast to expand at a 6.15% CAGR to 2031, driven by value-seeking shoppers in emerging economies.

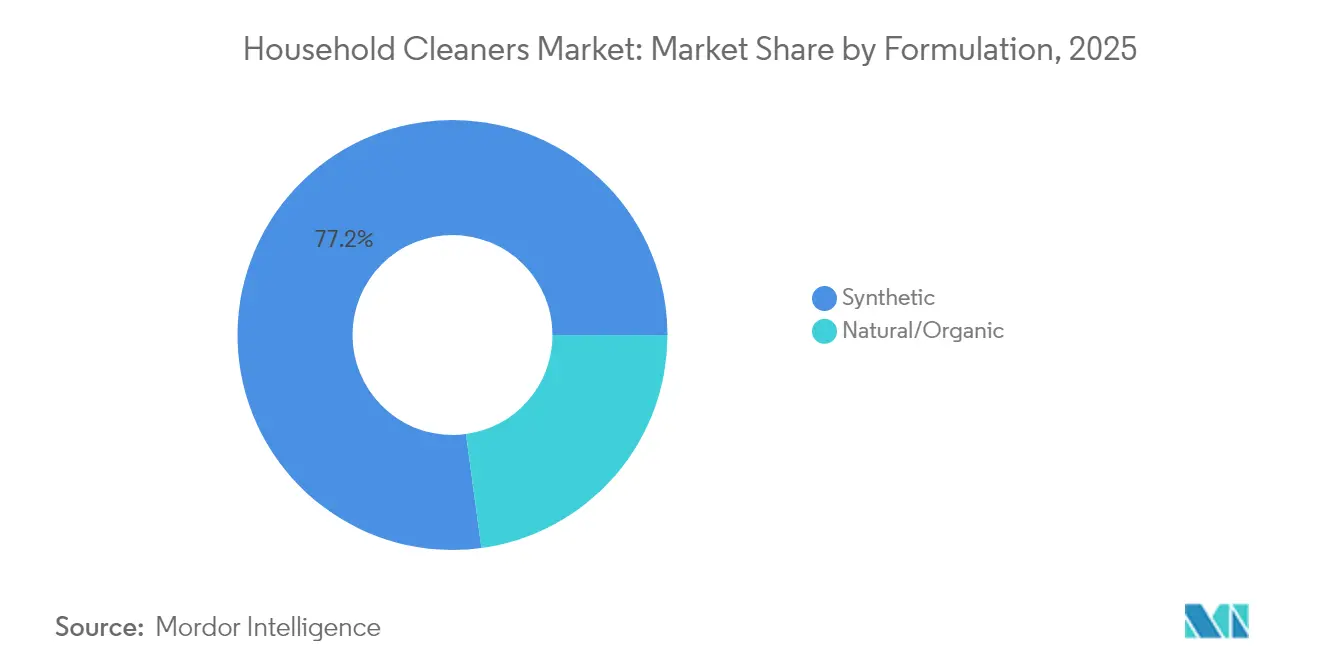

- By formulation, synthetic offerings retained a 77.15% share in 2025, but natural/organic products are growing at a 6.39% CAGR as eco-labels gain trust.

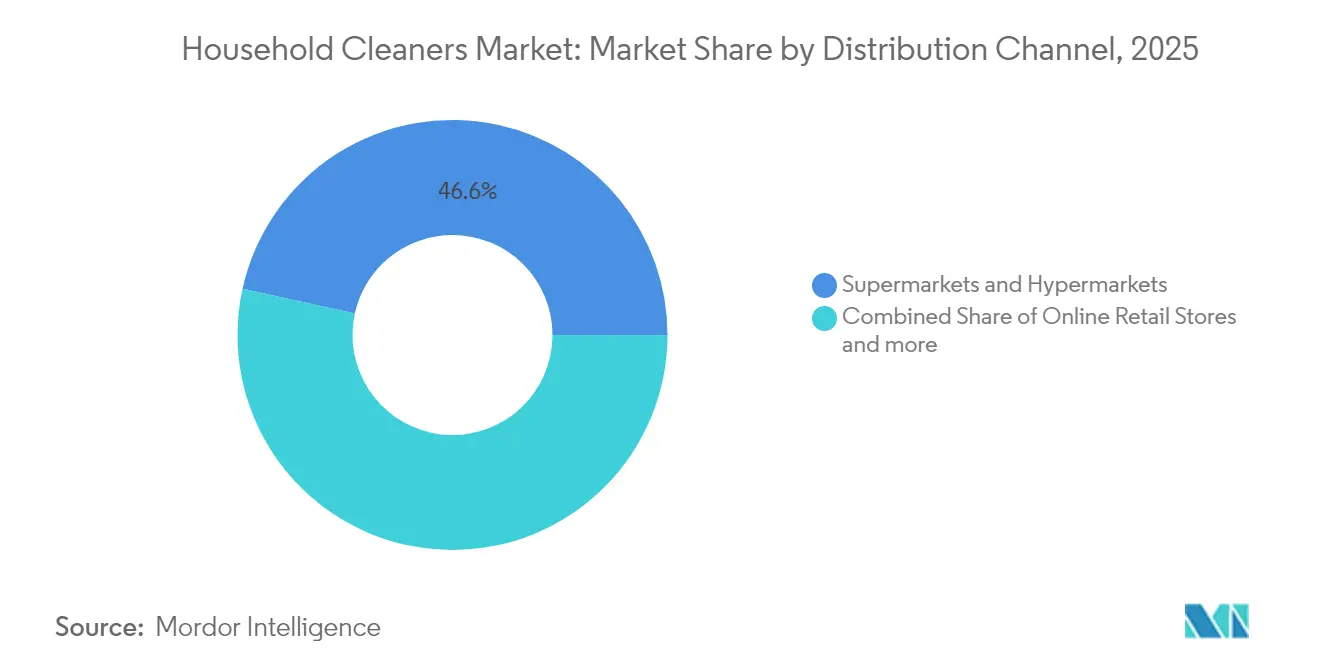

- By distribution channel, supermarkets and hypermarkets accounted for 46.55% of the household cleaners market size in 2025, while online retail is projected to advance at a 6.27% CAGR through 2031.

- By geography, Asia-Pacific commanded a 30.92% share in 2025; Europe exhibits the quickest regional CAGR at 6.03% to 2031, thanks to regulatory tailwinds.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Household Cleaners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened hygiene and sanitation awareness | +1.2% | Global, with peak impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Demand for eco-friendly and sustainable products | +0.9% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Product innovation and specialty cleaners | +0.8% | Global, led by developed markets | Medium term (2-4 years) |

| Technological integration in cleaning devices | +0.6% | North America and Europe, with gradual Asia-Pacific adoption | Long term (≥ 4 years) |

| Public health campaigns and awareness drives | +0.7% | Global, government-led initiatives | Short term (≤ 2 years) |

| Premiumization trend | +0.5% | Developed markets, urban centers in emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened hygiene and sanitation awareness

Post-pandemic hygiene consciousness fundamentally altered consumer cleaning behaviors. This behavioral shift extends beyond immediate pandemic concerns, as 85% of consumers indicate they will maintain heightened cleaning practices long-term. As of July 2025, the Centers for Disease Control and Prevention highlighted that 2.3 billion people worldwide still lack access to basic handwashing facilities with soap and water at home. This underscores significant market expansion opportunities, particularly in developing regions.[2]Source: Centers for Disease Control and Prevention, "Global Water, Sanitation, and Hygiene (WASH)", cdc.gov. Moreover, healthcare facility protocols increasingly influence household cleaning standards, with professional-grade disinfectants gaining traction in residential applications. Furthermore, the WHO's guidelines on sanitation and health reinforce the critical role of cleaning products in disease prevention, supporting sustained demand growth across all product categories.

Demand for eco-friendly and sustainable products

Environmental consciousness drives accelerating demand for sustainable cleaning solutions, with the U.S. Environmental Protection Agency's Safer Choice program certifying nearly 2,000 products that meet stringent health and environmental criteria. Along the same line, the 2024 updates to the Safer Choice Standard introduced enhanced packaging sustainability requirements and new energy efficiency criteria, creating competitive advantages for compliant manufacturers. European markets lead this transition, with the EU Ecolabel criteria revision emphasizing concentrated products and plant-based ingredients to reduce environmental impact. Moreover, Ecocert's natural cleaning product certification allows manufacturers to market globally with two labeling levels: 'Ecodetergents' (maximum 5% synthetic ingredients) and 'Ecodetergents made with Organic' (minimum 95% natural ingredients, minimum 10% organic). Furthermore, consumer willingness to pay premium prices for environmentally responsible products sustains higher margins while driving innovation in bio-based formulations.

Product innovation and specialty cleaners

Innovation cycles accelerate as manufacturers differentiate through specialized formulations and delivery mechanisms, with Unilever's April 2025 launch of Cif Infinite Clean probiotic cleaning spray exemplifying the bioscience revolution in home care. The company's ground-breaking bioscience initiatives leverage natural microorganisms to enhance cleaning efficacy while reducing chemical dependency. Patent activity in toilet bowl cleaner formulations demonstrates ongoing research and development investment, with biodegradable pad systems and effervescing compositions addressing both performance and environmental concerns. Additionally, specialty applications gain traction as consumers seek targeted solutions for specific cleaning challenges, moving beyond generic all-purpose formulations. The integration of antimicrobial technologies becomes particularly relevant as healthcare-associated infection prevention drives demand for products with proven pathogen elimination capabilities. Innovation timelines compress as digital consumer feedback loops enable rapid product iteration and market testing.

Technological integration in cleaning devices

Governments, health organizations, and nonprofits globally have intensified education on the importance of effective cleaning practices as a frontline defense against infectious diseases, creating heightened demand for cleaning products across categories such as dishwashing, laundry care, surface care, and toilet care. For example, nonprofit initiatives like the Hope and Comfort Hygiene Hub in Massachusetts distribute millions of hygiene products annually to address hygiene insecurity and promote health and dignity in vulnerable populations, reinforcing the societal value of accessible cleaning essentials. The U.S. Environmental Protection Agency, for instance, encourages safer household product initiatives that spur manufacturers to prioritize health-conscious and green formulations. These awareness efforts align closely with product developments in 2024 and 2025 that combine efficacy with sustainability and sensory appeal. Clorox has introduced innovations like the Lavender and Jasmine Scented Bleach (September 2024), while Pine-Sol’s Cherry Blossom Scent Multi-Surface Cleaner (February 2025) and Branch Basics’ all-purpose natural concentrate reflect consumer demand for natural, multi-functional, and eco-friendly cleaning solutions, encouraged greatly by ongoing hygiene education campaigns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense market competition | -0.8% | Global, particularly acute in mature markets | Short term (≤ 2 years) |

| Environmental regulations on packaging waste | -0.6% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Environmental and health concerns | -0.5% | Global, consumer-driven in developed markets | Long term (≥ 4 years) |

| Stringent regulatory requirements | -0.7% | Europe and North America core, Asia-Pacific following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense market competition

Market saturation in developed regions intensifies competitive pressures, with private-label alternatives capturing an increasing share from branded manufacturers through aggressive pricing strategies. The Federal Trade Commission's antitrust enforcement activities, including the Amazon case alleging monopolistic behavior in online retail, highlight competitive concerns that affect household cleaner distribution channels. Similarly, Turkish Competition Authority findings reveal high market concentration among major retailers, creating buyer power dynamics that pressure supplier margins and limit pricing flexibility. Along the same line, promotional intensity escalates as manufacturers compete for shelf space and consumer attention, eroding profitability across the value chain. Furthermore, digital disruption enables new entrants to bypass traditional distribution channels, challenging established players' market positions. The commoditization of basic cleaning functions forces manufacturers to invest heavily in innovation and marketing to maintain differentiation.

Environmental regulations on packaging waste

The U.S. Environmental Protection Agency's National Strategy to Prevent Plastic Pollution aims to eliminate plastic waste from land-based sources by 2040, directly impacting cleaning product packaging design and material selection. PFAS regulations affect 863 consumer products, including household cleaners, with 20 states adopting policies to prohibit PFAS in food packaging and expanding restrictions to other consumer applications. Moreover, the EPA's 2024 updates to Safer Choice packaging requirements mandate higher recycled content levels, increasing material costs and supply chain complexity. Extended Producer Responsibility regulations require manufacturers to plan for product disposal at production, develop appropriate disposal systems, and educate consumers on recycling practices. Thus, compliance costs escalate as regulatory frameworks evolve, particularly affecting smaller manufacturers with limited resources for regulatory adaptation and sustainable packaging development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Laundry Care Dominance Faces Dishwashing Disruption

Laundry Care commands 62.58% market share in 2025, reflecting its essential role in household maintenance and the category's broad product portfolio spanning liquid detergents, powder formulations, and specialty additives. Dishwashing emerges as the fastest-growing segment at 6.08% CAGR through 2031, driven by convenience innovations like single-use pods and concentrated formulations that simplify usage while reducing packaging waste. Surface care and toilet care segments maintain steady growth trajectories, supported by increased hygiene awareness and specialized product development for targeted cleaning applications.

The powder detergent resurgence in developing markets contrasts with liquid dominance in developed regions, as Chemical and Engineering News reports that powders lead by volume globally despite liquids' value share advantage. Unilever's January 2024 introduction of laundry sheets represents mass market innovation that addresses sustainability concerns while maintaining cleaning efficacy. Thus, the dishwashing segment benefits from premiumization trends as consumers invest in specialized formulations for different surface types and soil conditions, while regulatory compliance factors influence product development, with EPA Safer Choice certifications becoming increasingly important for market access and consumer acceptance.

By Form: Powder Renaissance Challenges Liquid Leadership

Liquids maintain a 38.12% market share in 2025, supported by consumer preference for convenience and ease of use in developed markets. However, Powders experience remarkable growth at 6.15% CAGR through 2031, driven by cost advantages in emerging economies and environmental benefits from reduced packaging requirements. The powder revival reflects economic pressures in developing regions where consumers prioritize value over convenience, particularly as appliance ownership increases and enables effective powder usage.

Bars and other alternative forms capture niche segments focused on specific applications or environmental considerations. The form preference varies significantly by geography, with powders remaining popular in Africa, India, and parts of Europe where economic factors outweigh convenience considerations. Procter & Gamble's research indicates similar market shares by value between liquids and powders globally, though powders lead in volume terms. Innovation in powder formulations addresses traditional limitations such as dissolution rates and residue concerns, making them more competitive with liquid alternatives. The 2% annual growth projection for powdered detergents reflects increasing appliance ownership in developing countries and sustained cost advantages over liquid formulations.

By Formulation: Natural/Organic Surge Disrupts Synthetic Dominance

Synthetic formulations dominate with 77.15% market share in 2025, leveraging established supply chains and proven performance characteristics across diverse cleaning applications. Natural/Organic alternatives accelerate at 6.39% CAGR through 2031, reflecting consumer willingness to pay premiums for environmentally responsible products and health-conscious formulations, which is driving the growth in the number of organic products. For instance, according to the Bundesanstalt für Landwirtschaft und Ernährung, as of December 2024, a total of 109,567 products in Germany carried organic labels. This was another increase compared to the previous year (102,170). This growth trajectory positions natural products to capture increasing market share as sustainability concerns intensify and regulatory frameworks favor bio-based ingredients.

The transition toward natural formulations faces technical challenges in matching synthetic performance while maintaining cost competitiveness. European markets lead natural product adoption, supported by regulatory frameworks that encourage sustainable ingredient sourcing and restrict harmful chemical usage. ECOS's sustainability initiatives, including 100% renewable energy usage and zero waste certification, demonstrate the operational commitments required to compete in the natural segment. Plant-based formulations gain traction as manufacturers develop bio-based alternatives that match synthetic performance while reducing environmental impact. The natural segment's premium positioning enables higher margins that offset increased ingredient costs and specialized manufacturing requirements.

By Distribution Channel: Online Retail Transforms Traditional Commerce

Supermarkets and Hypermarkets maintain a 46.55% market share in 2025, leveraging established consumer shopping patterns and the tactile nature of cleaning product selection. Additionally, the growing number of supermarket and hypermarket stores is further supporting the segment's growth. For instance, as of March 1, 2025, there were 1,454 Sainsbury stores in the United Kingdom. Online Retail Stores surge at 6.27% CAGR through 2031, driven by subscription services, bulk purchasing convenience, and the integration of smart home technologies that enable automated replenishment. Convenience stores and other retail channels serve specific geographic and demographic segments with tailored product assortments.

The digital transformation accelerates during pandemic-driven behavioral changes, with consumers embracing online purchasing for essential household items. Amazon's alleged monopolistic practices in online retail, including anti-discounting strategies and forced bundling with fulfillment services, highlight the competitive dynamics shaping digital distribution channels. Subscription models are gaining popularity as consumers seek convenience and cost savings through automated delivery services. The online channel's growth benefits from data analytics that enable personalized product recommendations and targeted marketing campaigns. Traditional retailers invest in omnichannel strategies to compete with pure-play digital platforms while maintaining their physical presence advantages.

Geography Analysis

Asia-Pacific held 30.92% of category value in 2025, anchored by the scale of China and India, rising middle-class incomes, and rapid urbanization that elevates hygiene priorities. Manufacturers localize production to skirt import duties and respond quickly to scent and packaging preferences unique to each sub-region. Retail infrastructure modernizes via discount chains and e-commerce super-apps, expanding product reach beyond tier-one cities. Government sanitation campaigns, particularly in India, lift penetration of branded cleaners in rural districts previously reliant on bar soap.

Europe is the fastest-growing territory, advancing at a 6.03% CAGR toward 2031 as the EU Detergents Regulation’s biodegradability clause reshapes procurement toward greener inputs. Consumers routinely scrutinize label disclosures, rewarding transparent brands with repeat purchases and word-of-mouth advocacy. Concentrated pods and water-free tablets lower transport emissions, aligning with corporate net-zero pledges and unlocking retailer preferential shelf plans. The household cleaners market size for Europe is on track, buoyed by premium pricing architectures that offset modest volume growth.

North America benefits from entrenched brand loyalty and high per-capita consumption, ensuring baseline stability even in economic slowdowns. EPA Safer Choice revisions push formulators to excise contentious preservatives, raising reformulation costs but differentiating compliant SKUs on the shelf. South America and the Middle East and Africa show mixed prospects; currency volatility and fragmented logistics hinder rapid scale-up, yet urban migration and retail formalization create long-term upside. Regional joint ventures and micro-distribution partnerships help multinationals manage political risk while gaining local insights.

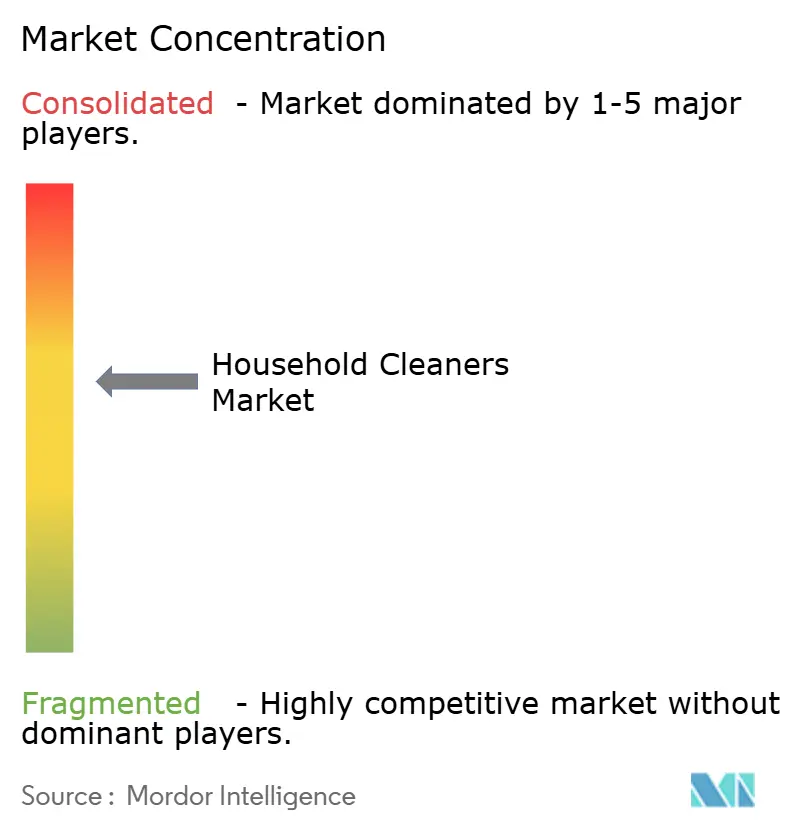

Competitive Landscape

The global household cleaners market is moderately consolidated and primarily driven by major multinational corporations, including Procter & Gamble (P&G), Unilever, Reckitt Benckiser, SC Johnson & Son, Inc., The Clorox Company, and Henkel AG & Co. KGaA. These industry leaders leverage their extensive brand portfolios, vast distribution networks (spanning physical retail and growing e-commerce platforms), and robust research and development capabilities to maintain and expand their market shares. A central strategy for growth is continuous product innovation focused on efficacy, convenience, and health-consciousness. For example, in 2025, P&G launched Tide Power PODS with Downy, offering 50% more cleaning power than their original liquid detergent, and the Cascade Platinum Plus pods, designed to eliminate the need for pre-rinsing dishes. P&G also introduced innovations in 2024, such as the Mr. Clean Magic Eraser Ultra Foamy and Magic Eraser Ultra Thick, addressing the need for powerful and convenient multi-surface cleaning solutions. Concurrently, Unilever introduced the Home Care innovation Persil Wonder Wash (also known as OMO/Surf Excel), a liquid laundry detergent specifically engineered for rapid, short-cycle washes (as quick as 15 minutes) and cold washes, in response to consumer demand for speed and energy efficiency.

Another critical growth strategy is a strong emphasis on sustainability and ingredient transparency. Companies are increasingly investing in the development of eco-friendly, natural, and organic products with biodegradable ingredients and sustainable, often refillable, packaging to appeal to environmentally conscious consumers. In a significant move in April 2025, Unilever launched Cif Infinite Clean, an all-in-one cleaner that uses pioneering bioscience technology and probiotics to offer a longer-lasting clean, available with 'Re-load' packs that reduce plastic waste. SC Johnson continues its focus on this area, highlighting in its 2024 report that over 99% of Windex PET bottles in North America are made from post-consumer recycled (PCR) resins.

Beyond innovation, major players also engage in strategic portfolio management and geographical expansion. In July 2024, Reckitt Benckiser announced plans to offload a portfolio of non-core home care brands by the end of 2025 (now called "Essential Home," including Air Wick and Cillit Bang) to sharpen its focus on its high-growth health and hygiene power brands, such as Lysol and Harpic. Mergers, acquisitions, and strategic partnerships (such as Unilever's collaboration with Samsung on laundry solutions) are also common tactics to expand product lines and improve operational efficiencies. Smaller, niche players specializing in green cleaning solutions, such as Seventh Generation and Method (owned by SC Johnson), continue to gain market share, further driving the competitive dynamics. Overall, the market is highly dynamic, driven by urbanization, increased disposable incomes, and the growth of e-commerce, forcing companies to continuously adapt their strategies to evolving consumer preferences.

Household Cleaners Industry Leaders

-

Henkel AG & Co. KGaA

-

Reckitt Benckiser Group plc

-

Procter & Gamble Co.

-

Unilever plc

-

S. C. Johnson & Son Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Reckitt unveiled Harpic DrainXpert, a new formulation in its drain cleaner lineup. The brand promised to redefine convenience, boasting the title of India's fastest drain cleaner, asserted to be capable of unclogging kitchen drains in a mere 15 minutes.

- May 2025: Air Wick unveiled a revamped air freshener formula, asserted to be double the essential oil content, emphasizing the allure of its scents. In its promotional spot, the brand showcased animals drawn to the new fragrances.

- April 2025: Surf launched a laundry liquid trio designed for short wash cycles. The fragrance-focused Magnifi-Scent Wash was made available in floral fusion, sunshine blossom, and Aqua bliss across 31 wash and 55 wash formats.

- April 2025: Unilever PLC launched Wonder Wash (short-cycle laundry liquid) in 2024, followed by new variants Dazzling Whites and Sensitive in April 2025, gaining large market adoption and share due to unmatched speed and gentleness. High repeat purchase rates and segment-creating innovation.

Global Household Cleaners Market Report Scope

Household cleaners are chemicals used to keep the house clean and maintain hygiene. The household cleaners market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into surface cleaners, glass cleaners, toilet cleaners, dishwashing detergents, and other product types. The market is segmented based on distribution channels: supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. The report also covers a detailed geographical analysis, which includes North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The report also offers the market size and forecasts for household cleaners across the five major regions. For each segment, the market sizing and forecasts have been done based on the value of USD billion.

| Dishwashing |

| Laundry Care |

| Surface Care |

| Toilet Care |

| Liquids |

| Powders |

| Bars |

| Others |

| Synthetic |

| Natural/Organic |

| Supermarkets & Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Venezuela | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| Middle East and Africa | South Africa |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Dishwashing | |

| Laundry Care | ||

| Surface Care | ||

| Toilet Care | ||

| By Form | Liquids | |

| Powders | ||

| Bars | ||

| Others | ||

| By Formulation | Synthetic | |

| Natural/Organic | ||

| By Distribution Channel | Supermarkets & Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Venezuela | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the household cleaners’ market?

Global sales reached USD 170.47 billion in 2026 and are on pace to hit USD 213.76 billion by 2031.

Which product segment is growing fastest?

Dishwashing cleaners are expanding at a 6.08% CAGR through 2031, outpacing all other product categories.

Why are natural and organic cleaners gaining share?

Consumer demand for eco-labels and health-oriented ingredients is pushing natural formulas to a 6.39% CAGR, narrowing the gap with synthetics.

How are online channels affecting distribution?

Online retail, including subscription programs, is rising at a 6.27% CAGR and is projected to account for about one-quarter of category sales by 2031.

Which region shows the highest future growth?

Europe leads future expansion with a 6.03% CAGR, driven by stringent biodegradability laws and premium product preferences.

What is the main regulatory challenge facing manufacturers?

Expanding packaging-waste rules and PFAS bans require costly material substitutions and create compliance hurdles, especially for smaller brands.

Page last updated on: