Herbal Toothpaste Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

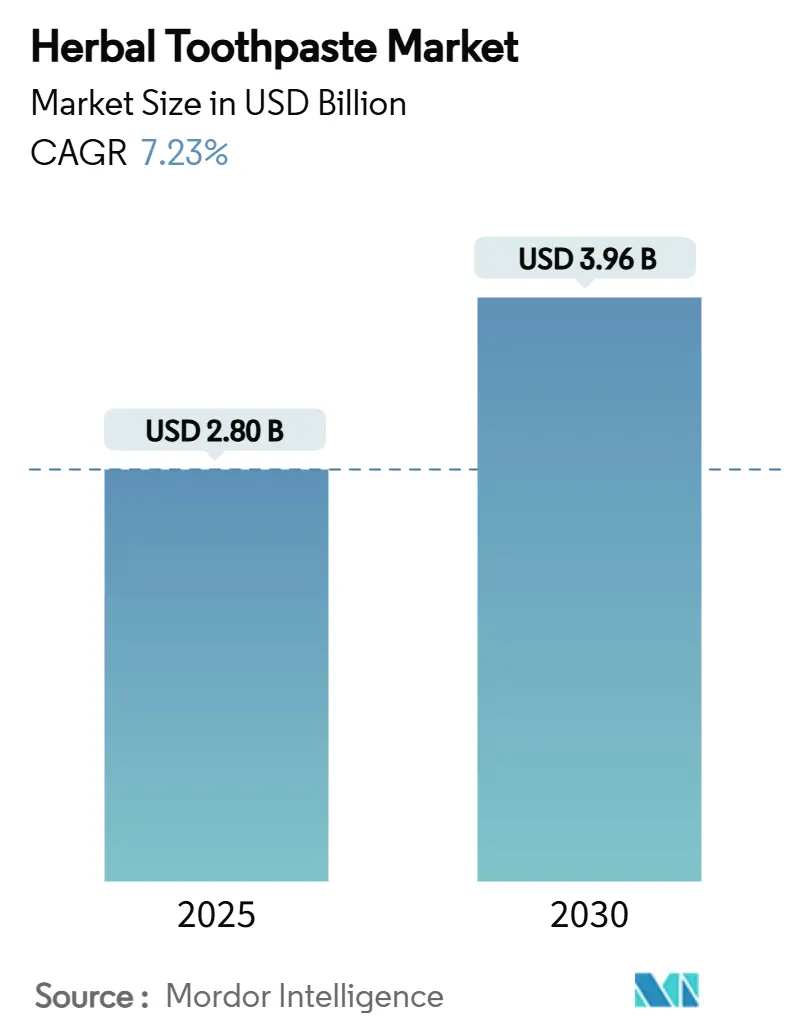

| Market Size (2025) | USD 2.80 Billion |

| Market Size (2030) | USD 3.96 Billion |

| Growth Rate (2025 - 2030) | 7.23% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Herbal Toothpaste Market Analysis by Mordor Intelligence

The global herbal toothpaste market size reached USD 2.8 billion in 2025 and is projected to expand to USD 3.96 billion by 2030 at a 7.23% CAGR, reflecting a decisive consumer shift toward natural oral-care solutions. Heightened scrutiny of synthetic additives, notably sodium lauryl sulfate (SLS) and triclosan, encourages manufacturers to highlight botanically derived actives that satisfy both efficacy and safety expectations. Asia-Pacific leads category revenue, helped by deep cultural affinity for traditional medicine and government endorsement of Ayurvedic and Traditional Chinese Medicine practices. Europe’s policy-driven restrictions on triclosan and SLS accelerate substitution trends, while North American consumers drive premiumization by gravitating to fluoride-free, plant-based propositions. Digital-first direct-to-consumer brands reinforce market dynamism by narrowing the education gap, enabling rapid adoption of innovative delivery formats such as tablets and strips. Intensifying competition is balanced by fragmented share distributions that leave ample headroom for differentiated positioning around sustainability, whitening, and pediatric safety.

Key Report Takeaways

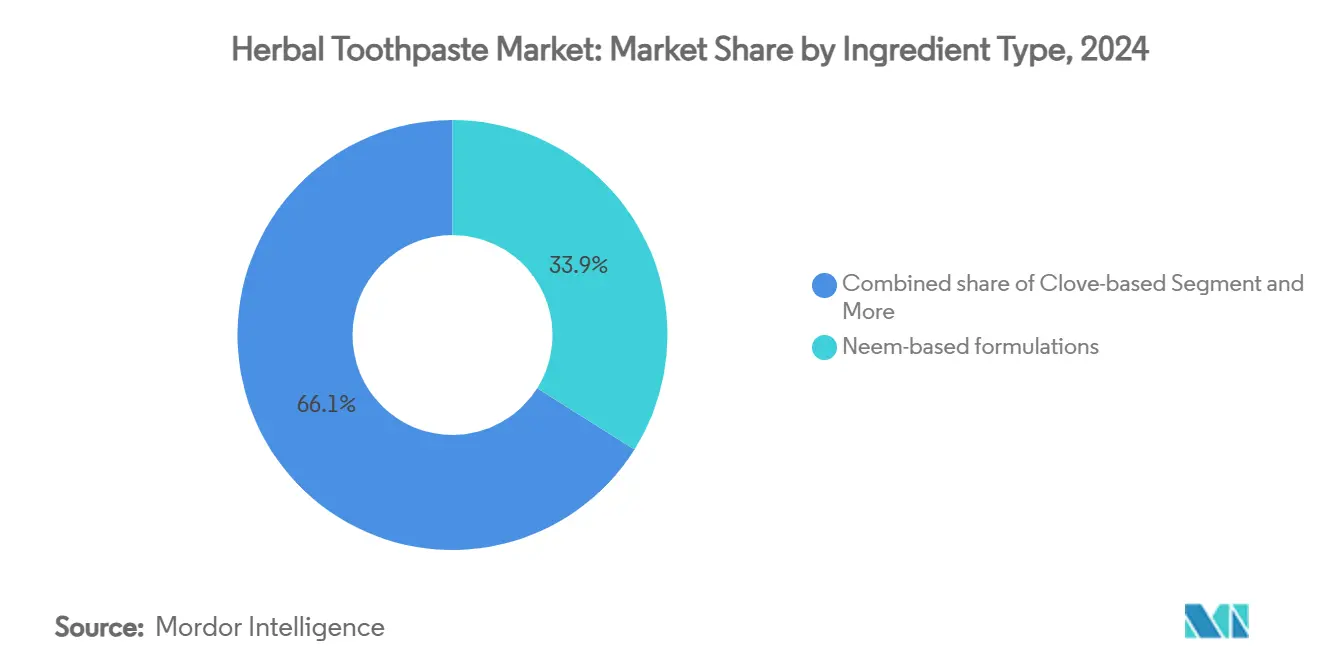

- By ingredient type, neem dominated with 34.27% of the herbal toothpaste market share in 2024; charcoal and bamboo-salt herbals are advancing at an 8.10% CAGR through 2030.

- By form, conventional paste held 65.13% of the herbal toothpaste market size in 2024, whereas tablets and strips are scaling at a 9.37% CAGR to 2030.

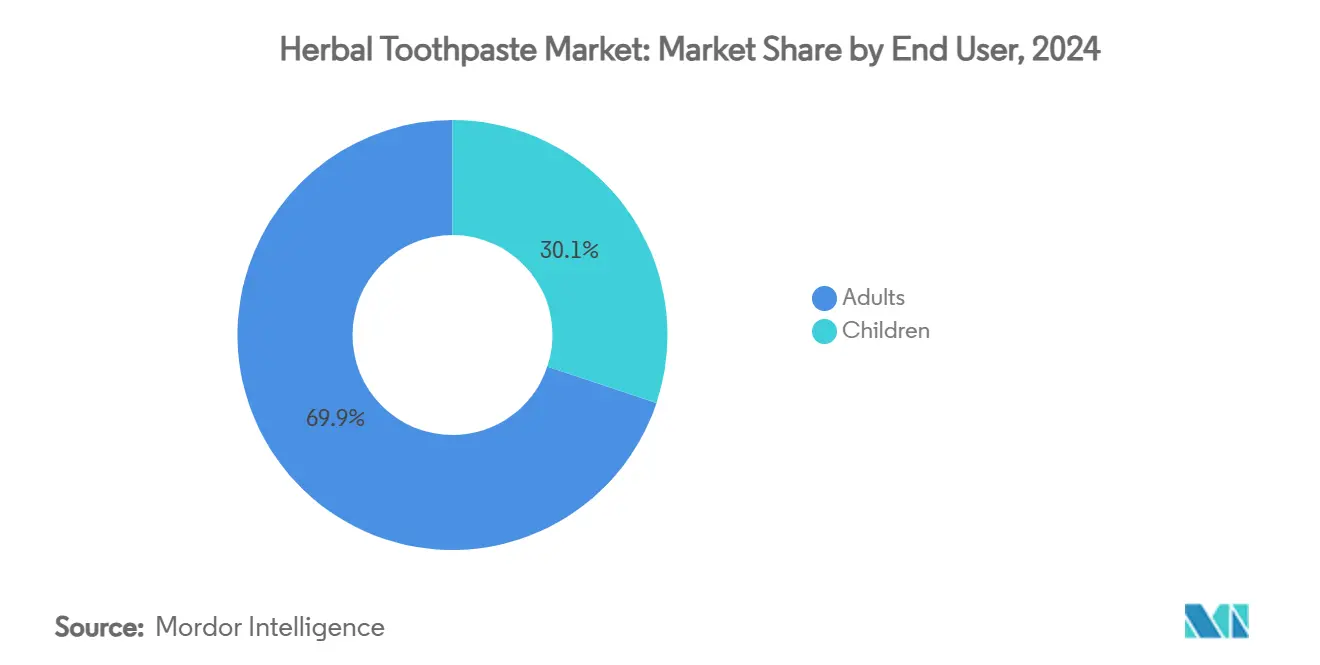

- By end-user, adults captured 70.58% revenue in 2024; the children’s segment is on track for a 7.63% CAGR to 2030, buoyed by mounting fears around pediatric fluoride exposure.

- By distribution channel, hypermarkets and supermarkets secured 44.37% of category sales in 2024, yet online retail is expanding fastest at 8.64% CAGR as D2C models proliferate.

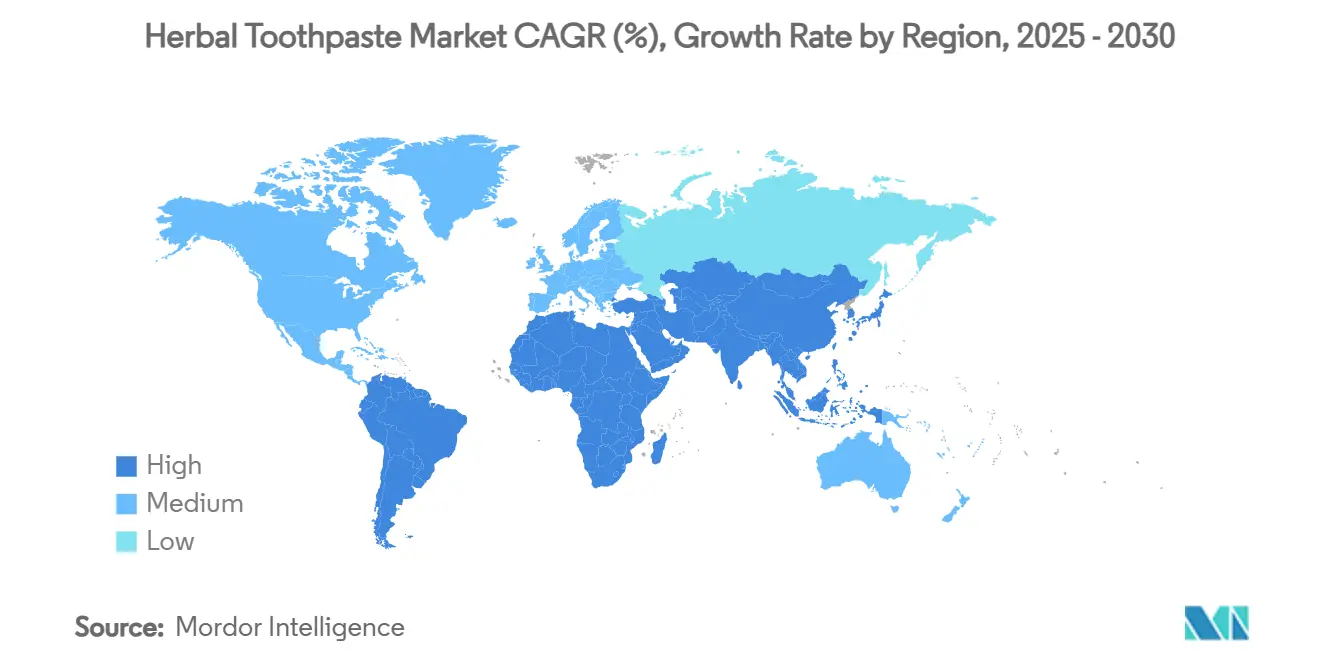

- By geography, Asia-Pacific held 51.97% regional share in 2024, while the Middle East and Africa led regional growth at 7.52% CAGR, propelled by rising disposable income and entrenched acceptance of herbal remedies.

Global Herbal Toothpaste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluoride-free demand surge | +1.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Plant-based/vegan preferences | +1.2% | Global urban centers | Long term (≥ 4 years) |

| Crack-down on SLS and triclosan | +1.5% | Europe, North America | Short term (≤ 2 years) |

| E-commerce-enabled D2C push | +1.1% | North America, Europe | Medium term (2-4 years) |

| Bio-active herb innovations are supporting the market growth | +0.9% | Asia-Pacific core; global spillover | Long term (≥ 4 years) |

| Cultural trust in traditional medicine | +0.8% | Asia-Pacific, Middle East, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for fluoride-free oral-care products

As the FDA held a public meeting in June 2025 to discuss fluoride safety for children, a growing number of parents and health-conscious consumers began questioning traditional dental care practices. Clinical studies reveal that herbal alternatives, such as neem-based formulations, can effectively reduce plaque. Notably, one study highlighted a 97.6% reduction in Enterococcus faecalis colony counts within just 7 days[1]Samah S. Abdeltawab et al., “Biocompatibility and Antibacterial Action of Salvadora persica Extract,” pubmed.ncbi.nlm.nih.gov. This shift in dental care goes beyond merely swapping ingredients; it underscores a deeper consumer skepticism towards synthetic additives and a heightened demand for transparency in personal care products. Furthermore, dental professionals are increasingly endorsing SLS-free alternatives for patients with oral mucosal irritation, lending clinical credibility to herbal formulations. This trend is gaining momentum, especially in markets where regulatory bodies voice concerns over fluoride accumulation, positioning herbal alternatives as not only safer but also more in tune with preventive healthcare philosophies.

Growing consumer preference for plant-based/vegan ingredients

Vegan consumers are now prioritizing toothpastes devoid of animal-derived ingredients and testing, marking a significant shift in the plant-based oral care revolution[2]"Veganism and Dentistry – for Dentists and Dental Professionals", December 2023, vegandentist.uk. Backing this trend, clinical studies highlight the potency of plant-based antimicrobials. For instance, herbal toothpastes featuring Salvadora persica have shown pronounced antibacterial effects against Streptococcus mutans and Lactobacillus. Millennials and Gen Z, champions of environmental sustainability and ethical consumption, are propelling this trend forward, spurring innovations in botanical sourcing and eco-friendly packaging. Urban dental professionals report a surge in patient inquiries about vegan oral care, especially in cities where plant-based lifestyles thrive. This demographic is not just vocal; they're also willing to pay a premium for products that resonate with their values, presenting a lucrative opportunity for specialized herbal brands to challenge conventional manufacturers.

Regulatory crack-down on SLS and triclosan in conventional toothpastes

European regulatory authorities spearhead global initiatives to curb the use of potentially harmful synthetic ingredients. The European Commission enacted a regulation capping triclosan concentrations at 0.3% in toothpastes and 0.2% in mouthwashes. Adding to the scrutiny, the Scientific Committee on Consumer Safety flagged triclosan as a potential endocrine disruptor, amplifying the push towards herbal alternatives. Clinical studies have shown that SLS can lead to oral mucosal desquamation and worsen recurrent aphthous ulcers, bolstering the case for regulatory restrictions. This regulatory landscape offers a competitive edge to herbal formulations, which sidestep these contentious ingredients yet retain antimicrobial potency through botanical compounds. Established herbal brands, armed with traditional use documentation and clinical studies, stand to gain significantly in this environment, showcasing their safety profiles.

E-commerce-enabled D2C brands accelerating category penetration

Direct-to-consumer (D2C) oral care brands are harnessing digital platforms to educate consumers about herbal ingredients, fostering brand loyalty beyond traditional retail channels. Notably, online retail is emerging as the fastest-growing distribution segment, projected to expand at a CAGR of 8.64% through 2030. Take Happy Tabs, for instance. Founded in 2019, the company exemplifies how D2C models can drive sustainable innovation, boasting compostable packaging and natural formulations that challenge the norm of conventional tube-based products. This digital-first strategy empowers specialized herbal brands to hone in on specific consumer segments, delivering tailored messages that highlight ingredient benefits and sustainability credentials. E-commerce platforms level the playing field, allowing smaller brands to vie with multinational giants, granting them direct access to health-conscious consumers who are often willing to pay a premium for natural alternatives. For herbal toothpaste brands, the D2C model is a boon, facilitating subscription-based purchases. This not only enhances customer lifetime value but also ensures predictable revenue streams, fueling ongoing product innovation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical-evidence gap versus fluoride benchmarks | -1.4% | Global, particularly in developed markets with established dental practices | Medium term (2-4 years) |

| Higher retail price points limiting rural uptake | -0.8% | Developing markets in Asia-Pacific, Africa, and South America | Long term (≥ 4 years) |

| Supply-chain volatility of key botanicals (e.g., neem oil) | -0.6% | Global, with acute impact in Asia-Pacific sourcing regions | Short term (≤ 2 years) |

| Intellectual-property barriers for traditional-knowledge ingredients | -0.4% | Global, with strongest impact in Western markets seeking IP protection | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clinical-evidence gap versus fluoride benchmarks

Despite emerging clinical evidence supporting herbal alternatives, dental professionals remain skeptical about the efficacy of natural ingredients in matching fluoride's proven ability to prevent caries. A systematic review highlighted that while herbal dentifrices can effectively reduce plaque and gingivitis, none outperformed fluoride-based products in caries prevention. This gap in evidence hampers professional endorsements and limits insurance coverage, curtailing market penetration in healthcare systems that emphasize evidence-based treatments[3]Syed Zubair Atif and S. M. Shahidulla, “An Overview on Herbal Tooth Powder,” researchgate.net. The challenge is even more pronounced in pediatric markets, where professionals are hesitant to recommend fluoride alternatives, especially given established caries prevention protocols for children. Yet, there's a glimmer of hope: emerging research on nano-hydroxyapatite as a fluoride substitute is gaining traction. The Scientific Committee on Consumer Safety has even approved concentrations of up to 29.5% in toothpastes, hinting at a potential bridge over the efficacy gap for herbal formulations.

Higher retail price points limiting rural uptake

Herbal toothpaste manufacturers' premium pricing strategies create accessibility barriers in price-sensitive rural markets, especially in developing economies where conventional toothpastes are significantly cheaper. This challenge is pronounced in countries like India, where 24% of families opt for tooth powder as a budget-friendly alternative, highlighting the price sensitivity that herbal brands must navigate. The complexities of sourcing botanical ingredients lead to elevated manufacturing costs for herbal formulations, which demand specialized sourcing, stringent quality control, and unique preservation methods, unlike their synthetic counterparts. While rural consumers often prioritize basic oral hygiene over premium natural ingredients, this creates segmentation challenges for herbal brands aiming for wider market penetration. This pricing challenge is especially pronounced in the children's segment in developing markets. Here, parents, despite concerns over synthetic ingredients, often gravitate towards conventional alternatives, curtailing the growth potential of herbal formulations in this demographic.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Neem Dominance Faces Charcoal Disruption

Neem-based offerings commanded 34.27% of the herbal toothpaste market share in 2024, underpinned by centuries of clinically documented antimicrobial performance. Studies reveal a 99.3% reduction in Enterococcus faecalis colonies after seven-day exposure, sustaining consumer confidence and dentist recommendations. Clove-infused lines retain sizeable volume by leveraging natural analgesic properties that address sensitivity, while mint blends thrive on breath-freshening familiarity. Ayurvedic multi-herb formulas appeal to holistic buyers, bundling synergistic anti-inflammatory and whitening traits within a single SKU. Close competitors, including tea tree and propolis-based pastes, differentiate through targeted gum-health claims, expanding choice without eroding neem’s frontrunner status.

Consumer fascination with visible whitening propels charcoal and bamboo-salt herbals, the fastest-growing subcategory at an 8.10% CAGR to 2030. Despite data linking charcoal abrasiveness to heightened enamel roughness, demand persists, highlighting perceived trade-offs between aesthetics and long-term dental integrity. LG H&H's patented bamboo-salt process shows how proprietary technology can turn traditional remedies into premium SKUs with defensible positioning. Value propositions that integrate whitening, remineralization, and lower abrasion could realign future growth curves while sustaining consumer excitement.

By Form: Paste Supremacy Challenged by Sustainable Innovations

Conventional paste still controls 65.13% of the herbal toothpaste market size, due to global familiarity with tube delivery and economies of scale in production. Gel derivatives cater to texture-seeking consumers and enable even dispersion of botanical actives. Consumers tend to choose conventional toothpastes due to their established brand trust, extensive product variants, and often lower cost compared to herbal alternatives. Powder formats remain relevant in markets where price sensitivity is acute and cultural practices favor concentrated, water-free application, supporting cost-effective oral hygiene for rural demographics.

Sustainability priorities elevate tablets and strips, which are expanding at a 9.37% CAGR. Brands such as TANITABS pair nano-hydroxyapatite remineralization with plastic-free packs, meeting dual goals of oral health and environmental stewardship. Clinical data confirm that chewable tablet efficacy equals that of conventional pastes in plaque control, giving consumers a practical on-the-go alternative. As airport security and travel convenience hurdles persist, formats that eliminate liquid restrictions position strongly for incremental share gains.

By End-User: Adult Stability, Children’s Upswing

Adult consumers contributed 70.58% of 2024 revenue, buoyed by healthcare consciousness and greater willingness to invest in premium, botanically rich SKUs. This demographic seeks effective and safe oral care solutions, driving the demand for herbal toothpastes made from ingredients like neem, clove, and mint. Sensitivity to SLS-related irritation drives dentist referrals toward herbal options, cementing repeat purchase among patients seeking gentle formulations. Adults also experiment with high-efficacy whitening herbals, reinforcing brand loyalty via measurable cosmetic results.

Parents’ fluoride concerns underpin the children’s segment’s 7.63% CAGR out to 2030. China’s CNY 5.4 billion pediatric category underscores how supportive policy and e-commerce retail converge to accelerate household trial. Successful formulators adopt milder flavors, lower abrasiveness, and cartoon branding to convert young users while assuaging safety anxieties. Regulatory dialogues on ingestible fluoride further tilt demand toward herbal options that balance remineralization with low systemic exposure risk.

By Distribution Channel: Traditional Retail Dominance Faces Digital Disruption

Hypermarkets and supermarkets accounted for 44.37% of 2024 sales, offering competitive pricing and one-stop shopping benefits for mainstream households. Their well-established retail infrastructure supports the broad distribution of multiple product variants, helping herbal toothpaste companies expand their reach and visibility globally. These outlets also attract customers through promotional offers and bundled deals, making herbal toothpastes easily accessible alongside other personal care products. Pharmacies capture health-positioned shoppers seeking professional reassurance, while convenience stores fulfill immediate replacement needs in urban cores.

Online retail is the fastest-climbing sales avenue at 8.64% CAGR. D2C pioneers leverage algorithmic targeting and content marketing to personalize ingredient education, prompting informed trial and subscription continuity. Perfora and Hello Products illustrate how storytelling and refill programs boost lifetime value while shrinking plastic footprints. As smartphone penetration deepens across emerging economies, click-to-cart immediacy could pivot volume away from brick-and-mortar, reshaping merchandising strategies across the herbal toothpaste market.

Geography Analysis

Asia-Pacific retained 51.97% of 2024 revenue, reflecting entrenched reliance on Ayurveda and Traditional Chinese Medicine, robust botanical supply chains, and government policy alignment. India’s fast-growing consumer base rewards heritage brands such as Dabur and Patanjali that blend traditional formulations with modern QC protocols. China adds scale, with children’s oral-care spend hitting CNY 5.4 billion in 2023 as parents embrace fluoride-free solutions amid rising health literacy. Japan and South Korea showcase premiumization, where discerning consumers pay elevated prices for eco-friendly packs and clinically backed botanicals. Indonesia, Thailand, and Vietnam lean on domestic herb cultivation and rising disposable income to broaden addressable bases. In Australia, upper-middle-income households gravitate toward organic, cruelty-free substitutes, sustaining niche margin pools.

The Middle East and Africa record the highest forecast CAGR at 7.52%. In Saudi Arabia, 61.8% of residents deploy herbs like clove for toothache, indicating an ingrained trust in botanicals. Gulf Cooperation Council nations pair high purchasing power with growing sustainability mindfulness, creating premium pockets for eco-labeled SKUs. Nigeria, Egypt, and South Africa benefit from sizeable youth demographics and expanding retail infrastructure that expose households to branded herbal innovations. Turkey and Morocco bridge European and African influences, sustaining double-digit import growth for natural oral-care lines.

Europe's stringent cosmetic regulations, which limit the use of triclosan and SLS, are nudging consumers towards herbal alternatives. Germany and the United Kingdom are at the forefront, driven by eco-conscious shopping and a robust online market. Nordic countries are rapidly adopting recyclable packaging and vegan products, further embedding these trends. The European Scientific Committee on Consumer Safety has endorsed nano-hydroxyapatite, giving herbal brands a fluoride-free edge in remineralization. In North America, while the market is mature, tastes are shifting: about 25% of Americans are now leaning towards natural toothpaste, energizing both established and new brands. Colgate-Palmolive's USD 100 million acquisition of Tom's of Maine underscores the industry's pivot towards natural care. Meanwhile, Mexico's burgeoning middle class and its traditional inclination towards plant-based remedies are driving a surge in demand.

Competitive Landscape

The herbal toothpaste market exhibits moderate fragmentation, evident from a concentration score of 4 out of 10. While multinationals like Colgate-Palmolive and Unilever harness global distribution and marketing prowess to secure shelf space, regional stalwarts such as Dabur, Patanjali, and Himalaya Wellness adeptly defend their territories. They achieve this by intertwining cultural narratives with large-scale manufacturing. Colgate's acquisition of Tom's of Maine not only broadens its natural-care footprint but also underscores a dedicated push towards clean-label Research and Development. Meanwhile, LG H&H's patenting of bamboo-salt processing across 14 countries underscores the potential of intellectual property strategies in safeguarding localized formulations while pursuing global expansion.

D2C innovators like Hello Products, Perfora, and Happy Tabs carve out a niche with their vegan offerings and evolving flavor profiles, leveraging subscription models to ensure steady revenue streams. Their partnerships with dentists and hygienists for clinical endorsements bolster consumer trust, mitigating any professional skepticism. Sustainability in packaging emerges as a key differentiator, with recyclable tubes and compostable pouches gaining traction both on shelves and in online searches.

Companies harnessing nano-hydroxyapatite to rival fluoride's effectiveness, all while championing an herb-centric narrative, successfully target both premium consumers and those demanding evidence. The market favors nimble players who adeptly navigate the interplay of heritage, safety, eco-conscious design, and a robust omnichannel strategy.

Herbal Toothpaste Industry Leaders

-

Colgate-Palmolive

-

Dabur India Ltd.

-

Procter & Gamble

-

Himalaya Wellness Company

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Dabur India has made its debut in the kids' toothpaste segment, unveiling the Dabur Herb'l Kids Toothpaste, designed specifically for children aged three and older. Setting itself apart from many fluoride-based competitors, Dabur's new offering is free from added chemicals. The toothpaste, boasting a delightful strawberry flavor, features popular characters: Iron Man for boys and Elsa from Frozen for girls.

- July 2024: Patanjali Dant Kanti has unveiled its latest offering: the Dant Kanti Fresh Active Gel. Crafted from a blend of natural ingredients, including cooling mint crystals, clove, cinnamon, anise, mentha, eucalyptus, and black pepper, the gel ensures a long-lasting freshness.

Global Herbal Toothpaste Market Report Scope

| Neem-Based |

| Clove |

| Mint |

| Ayurvedic Blends |

| Charcoal and Bamboo-Salt |

| Others (Tea-Tree, Aloe, Propolis, etc.) |

| Paste |

| Gel |

| Powder |

| Others (Tablet, Strip) |

| Adults |

| Children |

| Hypermarkets/Supermarkets |

| Pharmacies and Drug Stores |

| Convenience Stores |

| Online Retail |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient Type | Neem-Based | |

| Clove | ||

| Mint | ||

| Ayurvedic Blends | ||

| Charcoal and Bamboo-Salt | ||

| Others (Tea-Tree, Aloe, Propolis, etc.) | ||

| By Form | Paste | |

| Gel | ||

| Powder | ||

| Others (Tablet, Strip) | ||

| By End-User | Adults | |

| Children | ||

| By Distribution Channel | Hypermarkets/Supermarkets | |

| Pharmacies and Drug Stores | ||

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which region currently leads sales of herbal toothpastes?

Asia-Pacific commanded 51.97% share in 2024 owing to traditional medicine acceptance and strong supply chains.

What drives the fastest-growing ingredient segment?

Whitening demand propels charcoal and bamboo-salt formulations at an 8.10% CAGR despite enamel safety debates.

How quickly is online retail for herbal toothpaste expanding?

E-commerce and direct-to-consumer sales are growing at 8.64% CAGR as digital education lowers trial barriers.

Why is the children’s segment gaining momentum?

Parental concern about fluoride safety plus milder herbal flavors push children’s toothpaste sales at 7.63% CAGR.

Page last updated on: