HR SaaS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

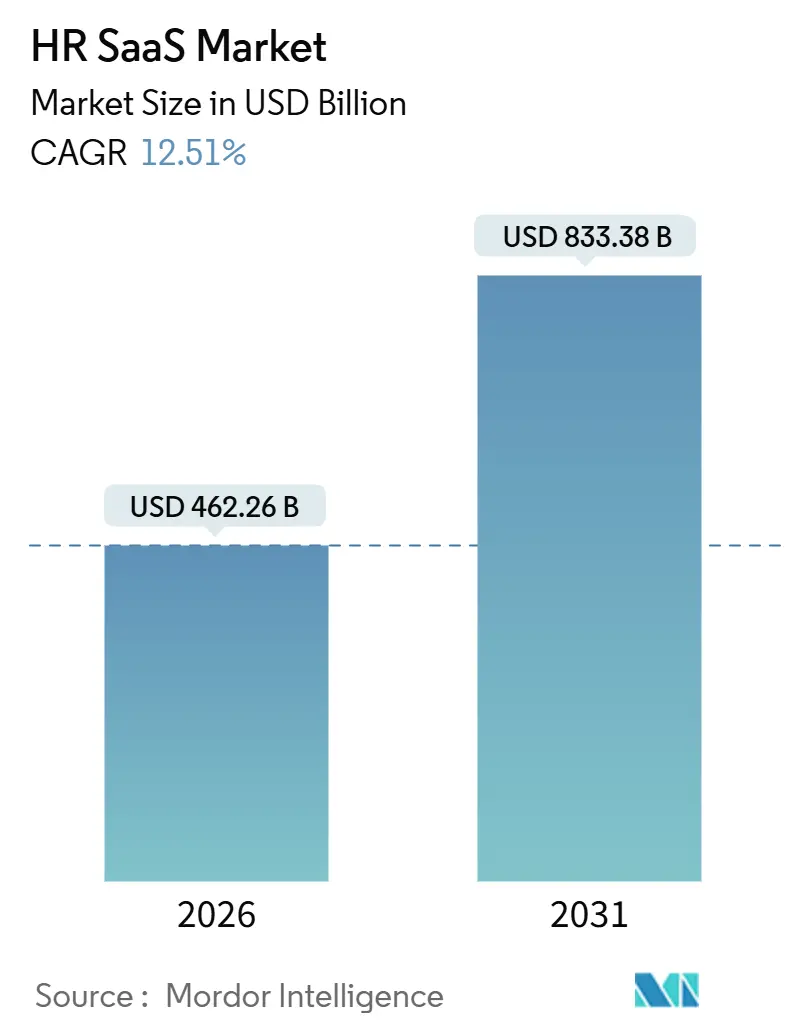

| Market Size (2026) | USD 462.26 Billion |

| Market Size (2031) | USD 833.38 Billion |

| Growth Rate (2026 - 2031) | 12.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR SaaS Market Analysis by Mordor Intelligence

The HR SaaS market size is projected to reach USD 833.38 billion by 2031, growing at a 12.51% CAGR from USD 462.26 billion in 2026. Demand is driven by the twin priorities of automating talent processes and embedding AI in decision-making, both of which require cloud delivery at a global scale. Vendors are redeploying capital into large-language-model training that can be amortized across thousands of tenants, a dynamic that sharply tilts economics away from on-premise software. Multi-country compliance, once a peripheral add-on, has become a core buying criterion as enterprises expand remote hiring. In parallel, consolidation among the top platforms is creating suites that cover payroll, analytics, and employee experience in one contract, lowering switching costs for mid-market buyers.

Key Report Takeaways

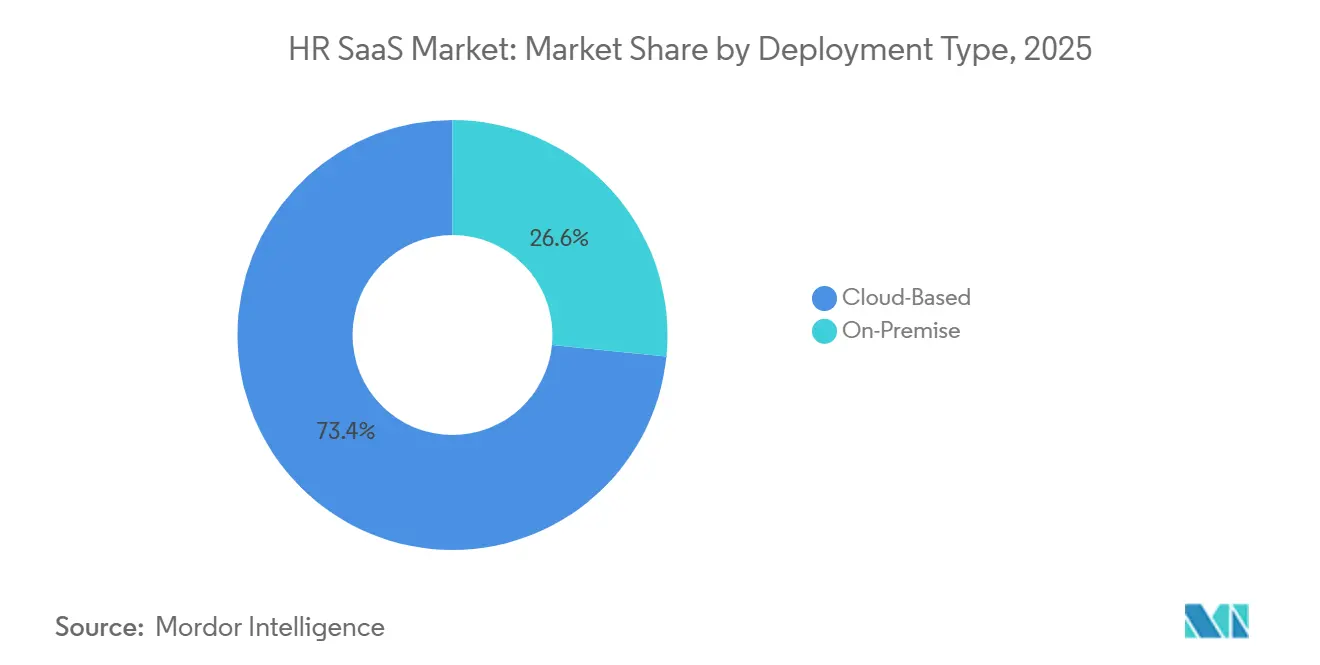

- By deployment type, cloud-based deployment led with 73.41% of the HR SaaS market share in 2025; the same segment is projected to expand at a 12.89% CAGR through 2031.

- By application, core HR captured a 32.67% share in 2025; workforce analytics is anticipated to register the highest CAGR at 13.73% through 2031.

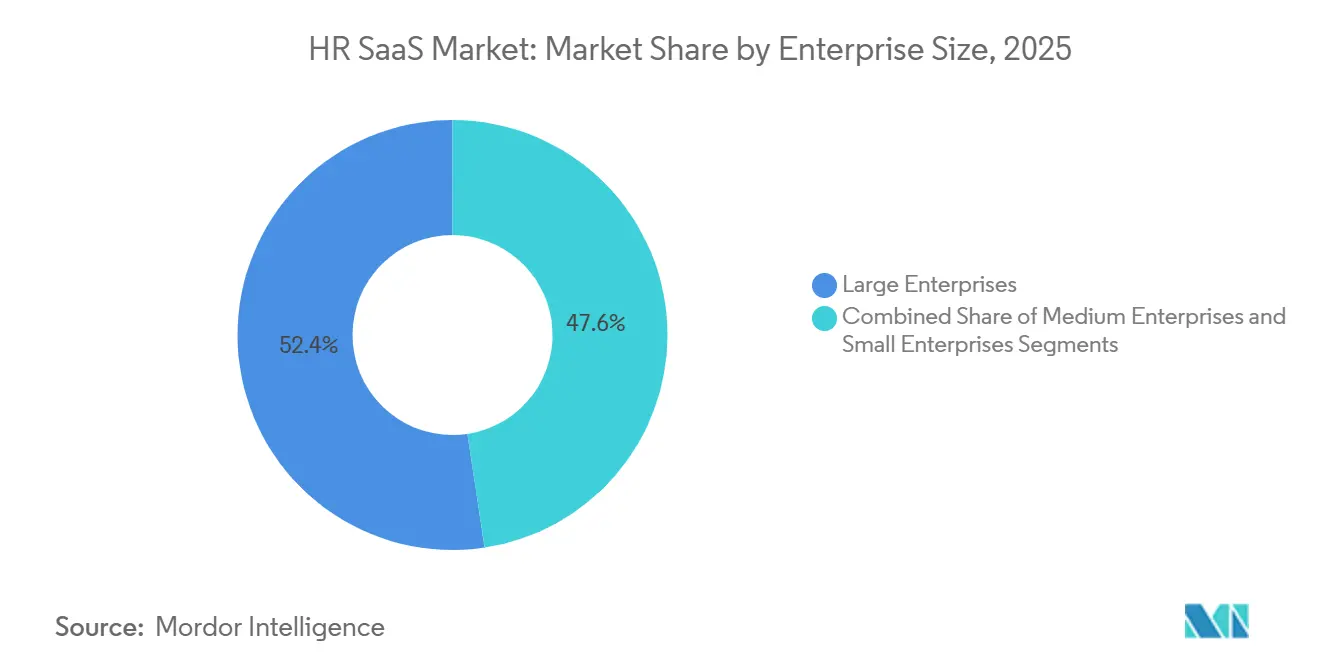

- By enterprise size, large enterprises accounted for 52.38% share of the HR SaaS market size in 2025; medium enterprises are projected to grow at 13.11% CAGR to 2031.

- By end-use industry, IT and telecom held 27.72% revenue share in 2025; healthcare is forecast to advance at 13.84% CAGR through 2031.

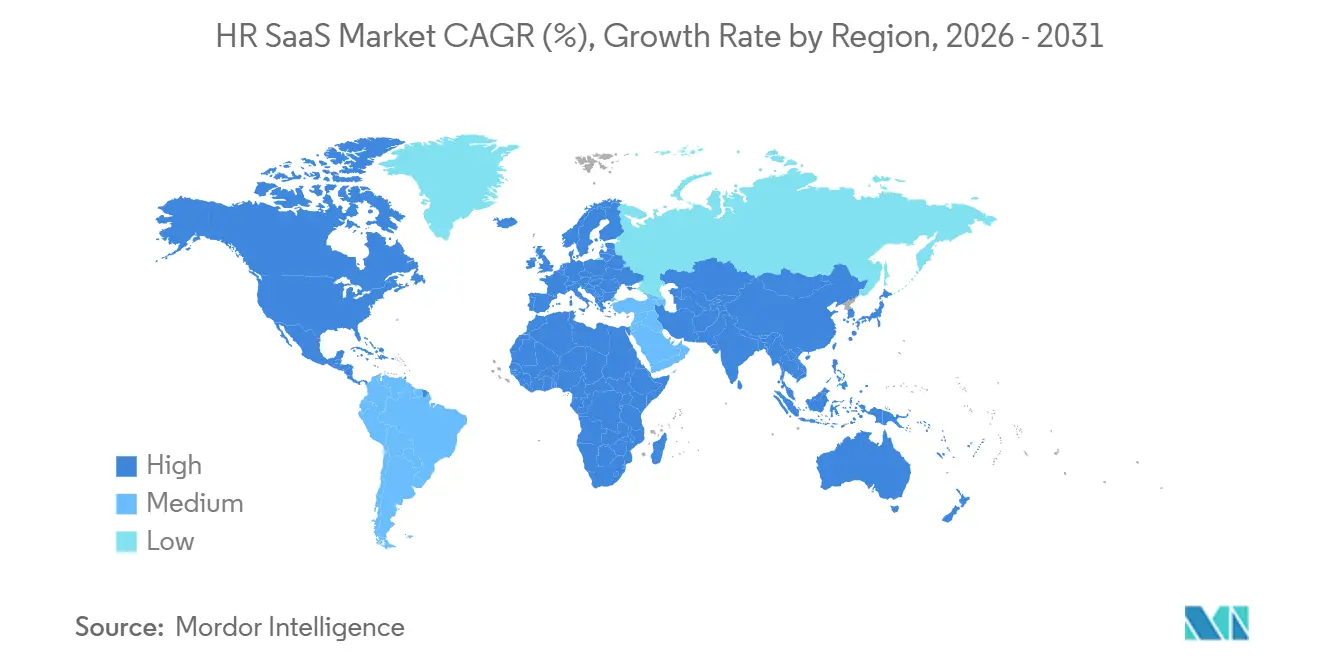

- By geography, North America contributed 39.83% of the global revenue in 2025; Asia Pacific is expected to grow at a 13.57% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR SaaS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud-Based HR Platforms | +3.2% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Need for Real-Time Workforce Analytics | +2.8% | Global, particularly strong in North America, Asia Pacific | Medium term (2-4 years) |

| Rising Compliance Complexity Across Jurisdictions | +2.1% | Global, acute in EU, UK, GCC states, Brazil | Long term (≥ 4 years) |

| Expansion of Hybrid and Remote Work Models | +1.9% | Global, led by North America, Western Europe, Australia | Short term (≤ 2 years) |

| AI-Driven Personalization of Employee Experience | +1.7% | North America, Europe, Asia Pacific urban centers | Medium term (2-4 years) |

| Demand for Unified Talent Lifecycle Management | +1.4% | Global, strongest in large enterprises across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Based HR Platforms

Cloud systems controlled 73.41% of deployment in 2025 and are advancing at a 12.89% CAGR, reflecting buyer preference for continuous feature drops that deliver AI capabilities without capital projects.[1]ISG Research, “HR Technology Trends 2025 Survey,” isg-one.com Vendor economics accelerate the cycle because each release improves models for every tenant simultaneously, slashing per-customer cost curves. ServiceNow’s USD 2.9 billion acquisition of Moveworks in March 2025 crystallized the value of agentic AI that cuts tier-1 HR ticket volume by up to 60% in pilots. Real-time compliance updates arrive in hours rather than quarters, an advantage as the EU and Saudi Arabia enforce live payroll reporting. On-premise stacks now persist mainly in defense and other air-gapped environments, though even these enclaves are adopting hybrid approaches that route analytics to sovereign clouds.

Need for Real-Time Workforce Analytics

Workforce analytics is the fastest-growing application, expanding at a 13.73% CAGR as enterprises shift from static dashboards to predictive models that flag attrition risk 90 days in advance. Average HR AI budgets reached USD 1.6 million in 2026, up tenfold from 2023. Early adopters report 15-25% reductions in regrettable turnover and 8-12% lower labor costs through the use of automated shift optimization.[2]Wall Street Journal Staff, “Predictive Analytics Reduce Employee Turnover,” wsj.com Skills ontologies embedded in these platforms help managers map internal talent to fast-emerging roles, such as prompt engineering, thereby bridging gaps created by the adoption of generative AI. Integrations with retail and healthcare scheduling deliver immediate ROI where demand volatility is highest.

Rising Compliance Complexity Across Jurisdictions

The jurisdictional patchwork is adding 2.1 percentage points to growth as fines for non-compliance increase. GDPR penalties reached a record EUR 1.5 billion (USD 1.62 billion) in 2025, prompting budgets to shift toward automated compliance engines.[3]European Data Protection Board, “GDPR Fines Reach Record Levels,” edpb.europa.eu Saudi Arabia’s Nitaqat and the UAE's Emiratization quotas require real-time nationality reporting, spurring the adoption of API-first payroll systems that can ingest rule changes within 48 hours. Brazil’s 900-plus labor statutes further highlight the need for localized engines capable of daily tax updates. Providers that cannot update rulesets quickly cede share to rivals able to deliver compliance as code.

Expansion of Hybrid and Remote Work Models

Hybrid work contributes 1.9 percentage points to growth as platforms evolve into digital headquarters that surface HR actions inside Teams and Slack. Global employment-of-record providers, such as Deel, grew to 35,000 customers by 2024, driven by remote hiring, which enabled firms to onboard talent in over 150 countries without local subsidiaries. Pulse surveys and sentiment analysis modules identify burnout before attrition manifests, a pressing issue as digital nomad visas proliferate. Real-time cost analytics enabled professional services firms to redeploy consultants to lower-cost jurisdictions while still complying with overtime regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Sovereignty Concerns | -1.8% | Global, acute in EU, China, Russia, localized in GCC states | Long term (≥ 4 years) |

| Integration Challenges with Legacy Systems | -1.5% | Global, particularly in large enterprises with ERP installations | Medium term (2-4 years) |

| Shortage of HR Tech Implementation Skills | -0.9% | Global, most severe in Asia Pacific and Latin America | Medium term (2-4 years) |

| Economic Slowdowns Curtailing IT Budgets | -0.7% | Global, cyclical impact varies by region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Sovereignty Concerns

Conflicting localization mandates subtract 1.8 percentage points from expansion, forcing multinational vendors to build in-country data centers or exit certain markets. China’s Personal Information Protection Law and Russia’s localization rules prohibit cross-border storage of employee data, driving up infrastructure costs by 15-25%. Schrems II further tightened EU-U.S. data transfers, compelling the use of encryption and pseudonymization layers that erode cloud efficiency. Separate AI models trained per jurisdiction reduce predictive accuracy, while granular consent rules create friction in deploying sentiment analytics.

Integration Challenges with Legacy Systems

Integrations with decades-old ERP stacks trim 1.5 percentage points from growth as enterprises wrestle with brittle point-to-point connectors. The average large company manages 15-20 HR-adjacent systems, many of which lack modern APIs. Middleware raises annual licensing costs by USD 50,000-200,000 and demands scarce talent fluent in both HR and API scripting. ADP’s USD 1.2 billion purchase of WorkForce Software in 2024 illustrates a move toward pre-integrated suites that lower total implementation time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Reshapes Vendor Economics

Cloud platforms held a 73.41% share in 2025 and are growing at a 12.89% CAGR, confirming that multi-tenant delivery is now the default among global firms. Vendors leverage usage telemetry to push weekly feature releases, including conversational AI that reaches every tenant overnight. The HR SaaS market benefits from this flywheel because marginal innovation cost approaches zero once training is complete. Conversely, the shrinking on-premise cohort is concentrated in defense and financial services, where air-gapped policies remain.

Hybrid models bridge the gap: core employee records stay on-premises, while analytics workloads burst to sovereign clouds that are compliant with data-residency laws. Providers offering containerized microservices capture accounts that must straddle both worlds. As regulations evolve, the HR SaaS market may see regulated sectors migrate piecemeal, lifting subscription revenues without a hard cutover event.

By Application: Workforce Analytics Outpaces Core HR

Core HR maintained a 32.67% share in 2025 as the system of record for headcount, pay, and time-off data. Yet, analytics revenues are rising fastest at a 13.73% CAGR because predictive models are finally generating tangible cost savings. Attrition warnings, skills adjacency mapping, and shift optimization move beyond pilots into budgeted programs, anchoring upsell for every core HR vendor.

Talent management suites capitalize on this momentum by embedding skills ontologies to screen applicants based on competencies rather than credentials. Payroll growth remains tied to the geographic rollout, with API-first, multi-country engines absorbing rule changes within 48 hours, an edge that legacy ERP cannot match. Learning platforms incorporate generative AI tutors that draft personalized upskilling paths, converting compliance-driven training into career mobility programs that boost engagement.

By Enterprise Size: Medium Enterprises Drive Incremental Growth

Large enterprises accounted for 52.38% of 2025 spending, reflecting their multi-jurisdictional footprints and strict security baselines. However, medium-sized enterprises are scaling fastest at a 13.11% CAGR, as modular suites lower the threshold for sophisticated functionality. Vendors court this cohort with implementation wizards, industry templates, and fixed-price setups that go live in 4-8 weeks.

The HR SaaS market size for medium-sized businesses expands further as unified bundles combine HR, payroll, and IT provisioning into a single invoice, aligning with limited back-office staff. Small-enterprise demand remains fragmented, but volume compensates for churn when acquisition costs are controlled through self-service onboarding.

By End-Use Industry: Healthcare Surges on Staffing Crisis

IT and telecom led adoption with 27.72% share in 2025, leveraging cloud-native systems to coordinate distributed engineering talent. Healthcare, however, is advancing at a 13.84% CAGR as chronic nurse shortages prompt hospitals to adopt predictive scheduling, which reduces burnout. Credential-tracking modules automate compliance with state boards and reduce exposure to six-figure fines.

Manufacturers deploy deskless-worker apps connected to robotics maintenance logs, while BFSI institutions integrate audit trails that satisfy SOX and Basel III requirements. Retail faces a 60-70% annual turnover rate, prompting the need for real-time scheduling and gig integration to scale seasonal workforces fourfold during peak weeks. Professional services firms prize project-level time tracking that aligns billable utilization with labor law limits.

Geography Analysis

North America accounted for 39.83% of 2025 revenue and is expected to maintain steady growth as enterprises channel AI budgets, averaging USD 1.6 million in 2026. The region’s mature cloud stack, combined with California’s privacy statutes, drives procurement toward platforms with encryption-at-rest and zero-trust architectures. Consolidation deals such as Paychex-Paycor reinforce suite strategies that appeal to mid-market buyers.

Asia Pacific, expanding at 13.57% CAGR, overtakes other regions in momentum. India’s 2024 labor-code consolidation mandates electronic wage filings, accelerating cloud adoption. GCC nationalization quotas similarly require real-time workforce nationality reports, creating pull for multi-country engines. China remains a high-demand yet restricted market; foreign vendors must deploy local data centers or partner with domestic players to comply with localization rules.

Europe continues to grow steadily as GDPR enforcement becomes tighter. Mid-market specialists such as Personio, which raised EUR 200 million (USD 216 million) in January 2024, fill a gap for localized compliance modules. The Middle East and Africa benefit from Vision 2030 projects that integrate public-sector digitization with HR modernization. South America’s growth centers on Brazil, where frequent tax updates and hyperinflation require daily payroll recalculations, making cloud agility indispensable.

Mordor Intelligence provides coverage of the hr saas market across other key regional markets. Detailed country-level analysis extends to Thailand incorporating local coverage and market participation, as required.

Competitive Landscape

The top five vendors captured approximately 40% of the global revenue in 2025, leaving the remaining 60% fragmented across more than 200 providers. Mergers intensified: Paychex acquired Paycor for USD 4.1 billion in January 2025, Dayforce accepted a USD 12.3 billion take-private offer in August 2025, and Workday closed its USD 1.1 billion Sana purchase in November 2025. Each deal targets the rapid infusion of conversational AI that resolves employee questions without human intervention.

Strategic differentiation now hinges on federated-learning patents that train AI across tenants without pooling raw data, thereby meeting privacy rules while retaining the benefits of scale. Vertical specialists like Darwinbox and Personio exploit localized compliance to defend regional strongholds, buoyed by funding rounds that finance product depth. Rippling’s March 2024 USD 200 million raise validated a unified HR-and-IT bundle that resonates with firms under 2,500 staff, while Deel’s USD 425 million round in April 2024 underscored demand for employment-of-record services.

White-space persists in construction, hospitality, and agriculture, where shift variability and seasonal hiring complicate standard HR workflows. Providers that embed industry taxonomies and achieve checklist-level compliance win contracts, even against larger horizontal suites. Mobile-first usability for deskless workers remains a decisive factor in manufacturing and retail wins, pushing vendors to refine sub-10-second task flows and offline sync.

HR SaaS Industry Leaders

Workday Inc.

SAP SE

Oracle Corporation

Automatic Data Processing

Ceridian HCM Holding Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Workday completed its acquisition of Sana for USD 1.1 billion, integrating conversational AI that is expected to cut service-desk costs by up to 60% in early adopter accounts.

- August 2025: Dayforce agreed to be taken private by Thoma Bravo for USD 12.3 billion, with closing targeted for early 2026.

- September 2025: Oracle enhanced Fusion Cloud HCM with AI-driven candidate screening that lowered time-to-hire 30% in pilot deployments.

- June 2025: SAP added skills intelligence to SuccessFactors, enabling gap analysis against future role demands.

Global HR SaaS Market Report Scope

The HR SaaS Market Report is Segmented by Deployment Type (Cloud-Based, and On-Premise), Application (Core HR, Talent Management, Payroll, Workforce Analytics, Learning and Development, Other Applications), Enterprise Size (Large Enterprises, Medium Enterprises, Small Enterprises), End-Use Industry (IT and Telecom, BFSI, Healthcare, Manufacturing, Retail and E-commerce, Professional Services, Other Industries), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Core HR |

| Talent Management |

| Payroll |

| Workforce Analytics |

| Learning and Development |

| Other Applications |

| Large Enterprises |

| Medium Enterprises |

| Small Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare |

| Manufacturing |

| Retail and E-commerce |

| Professional Services |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Type | Cloud-Based | ||

| On-Premise | |||

| By Application | Core HR | ||

| Talent Management | |||

| Payroll | |||

| Workforce Analytics | |||

| Learning and Development | |||

| Other Applications | |||

| By Enterprise Size | Large Enterprises | ||

| Medium Enterprises | |||

| Small Enterprises | |||

| By End-Use Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Professional Services | |||

| Other End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the HR SaaS market in 2031?

It is expected to reach USD 833.38 billion, reflecting a 12.51% CAGR from 2026 to 2031.

Which deployment model leads current spending?

Cloud-based platforms accounted for 73.41% of 2025 revenue and continue to expand fastest.

Why is Asia Pacific growing more quickly than other regions?

Digital-first labor regulations in India and nationalization mandates in GCC states are accelerating adoption, driving a 13.57% CAGR through 2031.

How are healthcare providers using HR SaaS platforms?

Hospitals deploy predictive scheduling and automated credential tracking to ease staffing shortages and avoid regulatory fines.

What integration challenges do enterprises face?

Many still run 15-20 legacy HR-adjacent systems without modern APIs, leading to costly and brittle point-to-point connectors.

Which factor most limits market growth?

Data privacy and sovereignty laws that require in-country data storage add complexity and cost, trimming the overall growth rate.

Page last updated on: