Human Resource Information System (HRIS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

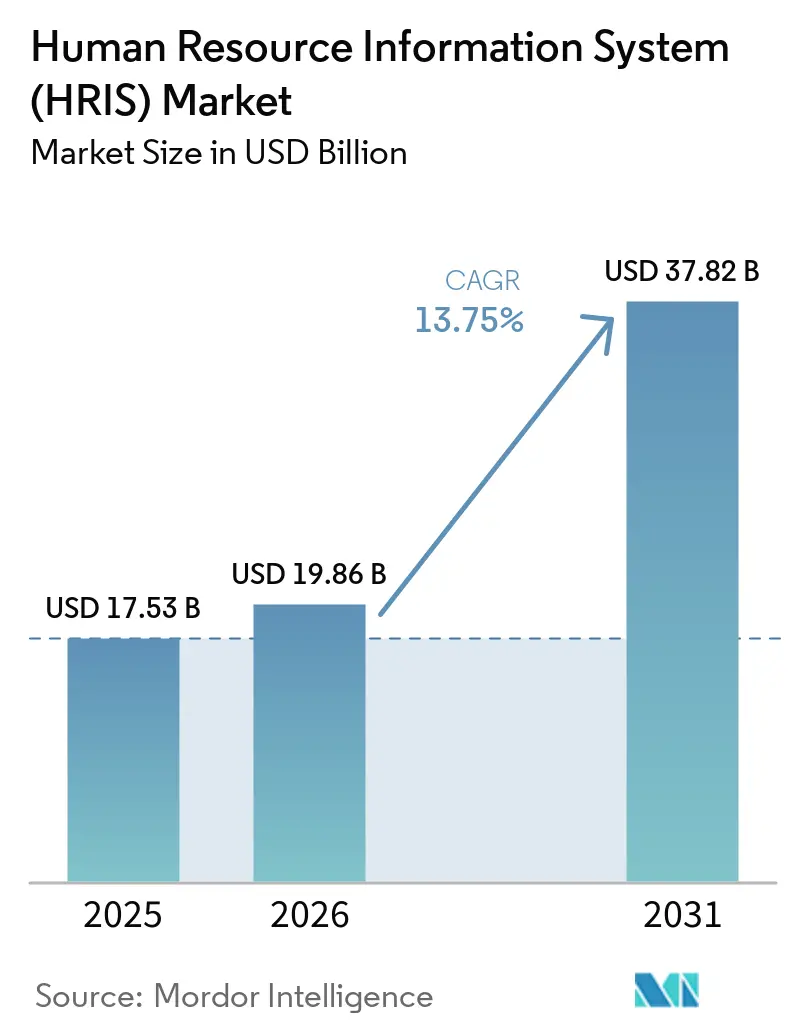

| Market Size (2026) | USD 19.86 Billion |

| Market Size (2031) | USD 37.82 Billion |

| Growth Rate (2026 - 2031) | 13.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Resource Information System (HRIS) Market Analysis by Mordor Intelligence

The human resource information system (HRIS) market size is expected to increase from USD 17.53 billion in 2025 to USD 19.86 billion in 2026 and reach USD 37.82 billion by 2031, growing at a CAGR of 13.75% over 2026-2031. Enterprises are accelerating cloud migrations to convert fixed infrastructure costs into variable subscriptions, regulators across Europe and Asia-Pacific are tightening audit-trail mandates that legacy databases cannot meet, and hybrid work models are exposing the inability of on-premise tools to monitor distributed teams. Early adopters in North America are now layering analytics and AI assistants onto core payroll engines, while Asia-Pacific start-ups are leapfrogging to mobile-first bundles that bundle local-language chatbots with e-filing of social-insurance data. Private-equity roll-ups are consolidating mid-tier vendors to assemble end-to-end human-capital suites, raising competitive stakes for incumbents while widening product choice for buyers. At the same time, the shortage of HR-tech administrators is pushing small and midsize enterprises toward pre-configured workflows that can be activated in weeks rather than quarters.

Key Report Takeaways

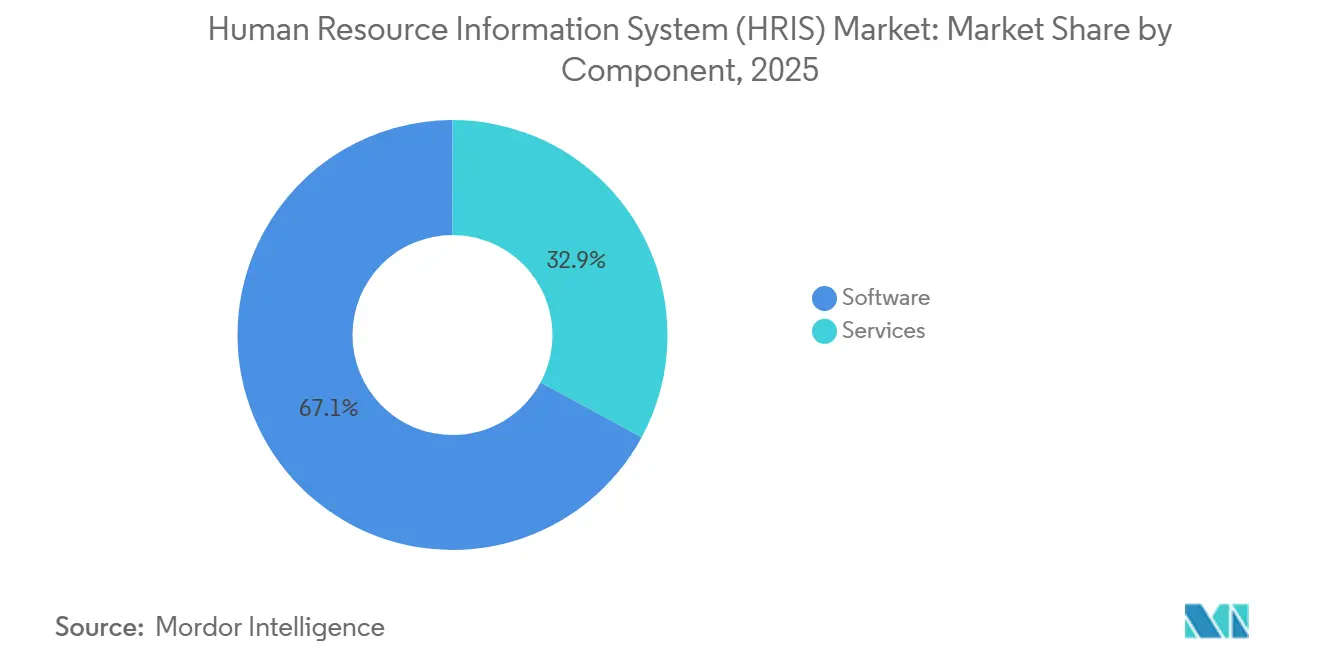

- By component, software led with 67.12% of the human resource information system (HRIS) market share in 2025, while services are advancing at a 16.21% CAGR through 2031.

- By deployment model, on-premise installations retained 71.05% of spending in 2025 but cloud solutions are expanding at a 16.55% CAGR to 2031.

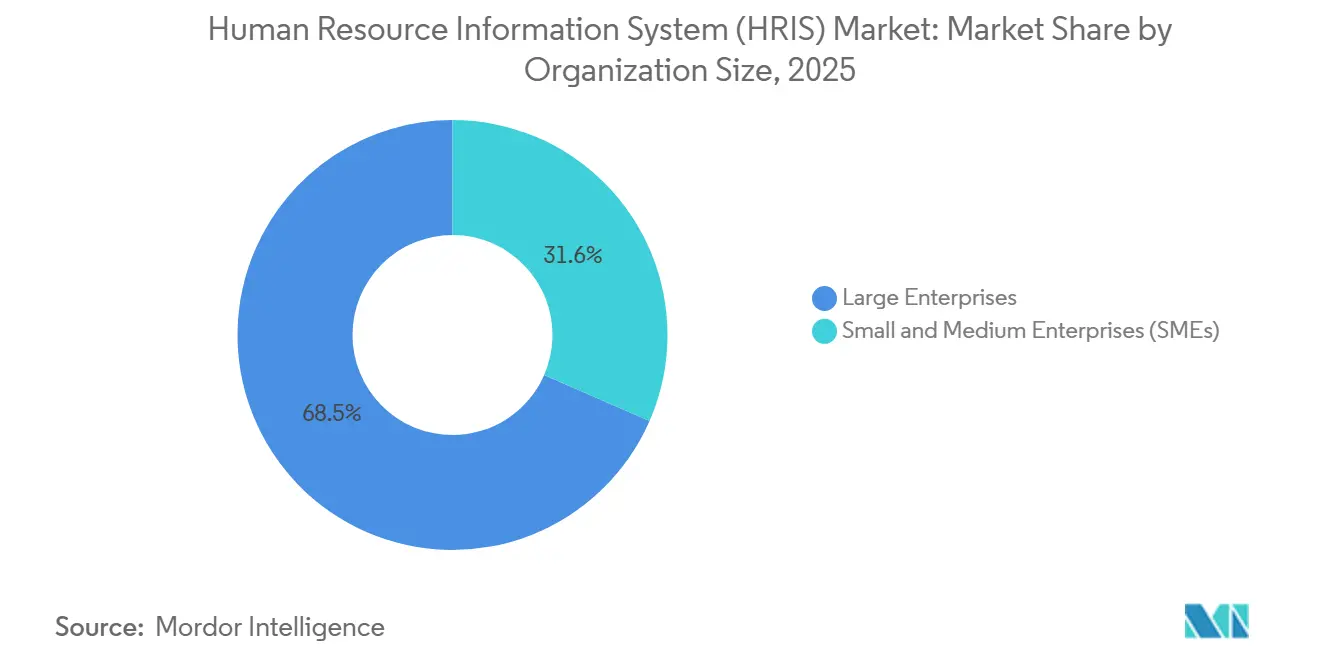

- By organization size, large enterprises commanded 68.45% of 2025 revenue of HRIS market, whereas small and medium enterprises are projected to grow at a 15.76% CAGR.

- By end-user industry, information technology and telecom captured 28.54% of revenue in 2025, while healthcare is poised to expand at a 14.89% CAGR to 2031.

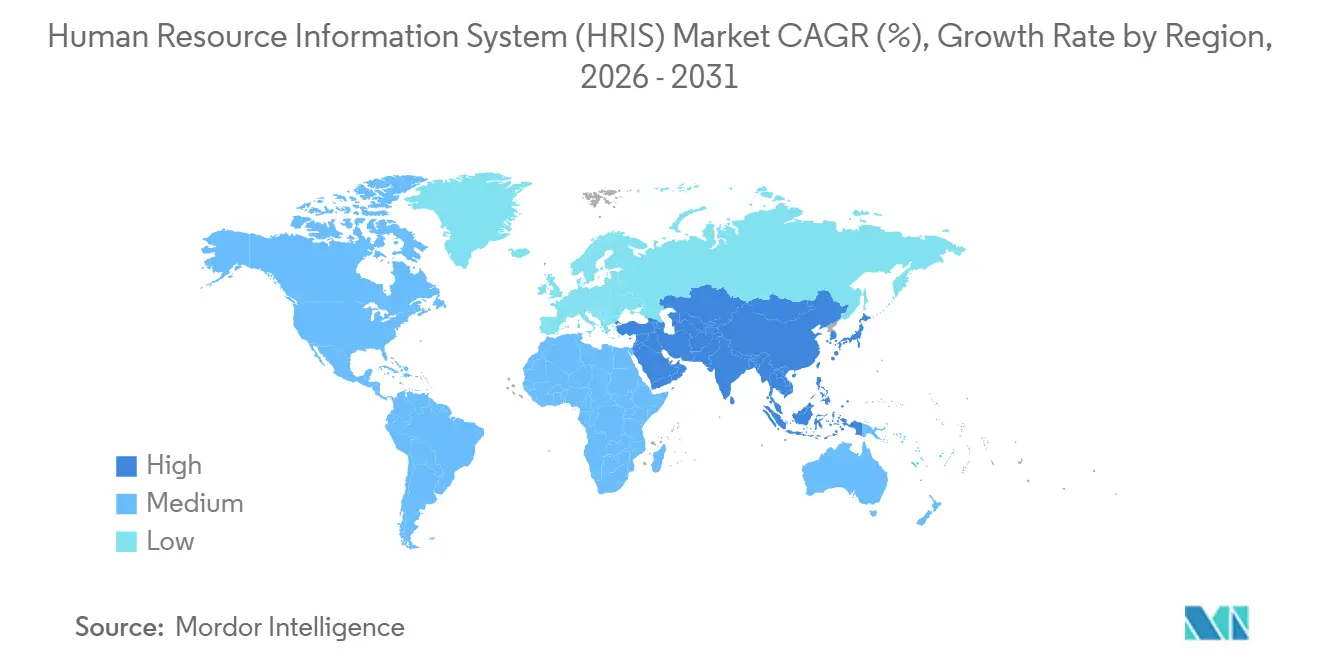

- By geography, North America held 38.02% of 2025 sales and Asia-Pacific is forecast to register a 15.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Human Resource Information System (HRIS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Cloud-Based HR Platforms | +3.2% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Workforce Analytics | +2.8% | North America and Europe, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of Remote and Hybrid Work Models | +2.5% | Global, concentrated in IT, telecom, and BFSI | Short term (≤ 2 years) |

| Integration of AI-Powered Chatbots | +2.3% | North America and Europe, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Increasing Regulatory Complexity | +1.9% | Europe, Asia-Pacific, and North America | Long term (≥ 4 years) |

| Emergence of Industry-Specific Verticals | +1.5% | Healthcare and manufacturing in the West, retail in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Cloud-Based HR Platforms

Cloud subscriptions are growing 16.55% annually, outpacing overall human resource information system market expansion as organizations offload infrastructure ownership and gain real-time global data consolidation. In 2025, 69% of employers had moved at least one core module to software-as-a-service and 83% expect full cloud adoption by 2027. Asia-Pacific enterprises, despite fragmented data centers, report 70% intent to deploy AI-enabled HR tools by 2026, stimulated by government e-filing mandates and low-cost broadband. Vendors are responding with mid-market bundles such as Workday GO, which ships pre-built workflows that cut launch times from nine months to four.

Rising Demand for Workforce Analytics

Predictive dashboards that forecast attrition, optimize overtime, and model labor costs are shifting from premium add-ons to baseline expectations. Organizations deploying AI-driven HR modules in 2026 budgeted an average of USD 1.6 million for analytics, a tenfold rise since 2023. Healthcare illustrates results: a 400-bed hospital cut nurse overtime by 18% after embedding scheduling algorithms into its HRIS. Yet only 9% of employers possess enterprise-wide AI expertise, making low-code query tools and natural-language interfaces critical adoption levers.

Expansion of Remote and Hybrid Work Models

Permanent hybrid schedules require systems that capture location-agnostic time, attendance, and productivity metrics. UKG’s 2025 pact with IFS links technician skills to equipment maintenance, letting field-service teams assign jobs irrespective of base office location. The European Union’s AI Act forces vendors to embed consent notices for any algorithm that tracks remote employees, raising development overhead but creating a compliance differentiator.[1]European Commission, “Regulatory Framework on AI,” DIGITAL-STRATEGY.EC.EUROPA.EU

Integration of AI-Powered Chatbots for Employee Self-Service

Chatbots are resolving basic HR questions in seconds and lowering help-desk workloads by 25-40%. BambooHR’s 2026 “Ask BambooHR” assistant delivers payslips and leave balances via plain-English prompts, slashing average resolution times from 48 hours to under two minutes. Regulatory scrutiny remains high: the EU treats hiring chatbots as high-risk, obligating full audit trails and human override, requirements that many start-ups struggle to satisfy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Security and Privacy in Multi-Tenant Clouds | -2.1% | Global, most acute in Europe and Asia-Pacific | Short term (≤ 2 years) |

| High Switching Costs From Legacy Systems | -1.8% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Shortage of Skilled HR-Tech Administrators | -1.4% | Global, severe in emerging markets | Long term (≥ 4 years) |

| Limited Budgets Among SMEs in Emerging Regions | -1.2% | Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy in Multi-Tenant Clouds

GDPR fines surged to EUR 2.92 billion (USD 3.11 billion) in 2024 for breaches linked to inadequate tenant segregation. Asia-Pacific data-localization laws compel vendors to spin up national data centers, diluting the economies of scale that make public clouds attractive. Single-tenant options with customer-managed encryption keys mitigate risk but lift subscription fees by as much as 50%.

High Switching Costs From Legacy Systems

Moving a 10,000-employee enterprise from an on-premise HRIS to the cloud costs USD 2-4 million and takes up to two years, largely because payroll outputs must match penny-for-penny before auditors sign off. Cultural inertia compounds expense: HR teams resist abandoning heavily customized workflows, and IT departments dread unplugging connectors that feed pension providers and tax portals. Tools promised by UKG’s pending Inova Payroll acquisition aim to automate data mapping yet still demand manual validation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand as Deployments Grow Complex

Services revenue is projected to rise 16.21% a year through 2031, surpassing overall human resource information system (HRIS) market growth as buyers seek integration, change-management, and managed-perations expertise. Software retained the largest slice 67.12% in 2025, yet commoditization of payroll engines is shifting value toward analytics, AI, and user experience enhancements. Pre-built connectors from ADP, funded by USD 1.27 billion in 2024 research spending, have compressed mid-market rollouts from nine months to four, highlighting the premium buyers place on speed. In Asia-Pacific, where 63% of system owners have fewer than three years of HR-tech experience, training and support contracts are bundled into multiyear deals to sustain adoption momentum.

Consulting budgets increasingly emphasize user adoption rather than code customization, reflecting Deloitte findings that top-quartile engagement scores correlate with 40% higher spend on change management. Cloud subscriptions blur the classic software-versus-services line because hosting, patches, and tier-one support are baked into monthly fees. Nevertheless, enterprises customizing approval chains or complex union work rules still purchase white-glove services to guard against post-upgrade breakage.

By Deployment Model: Cloud Subscriptions Redefine Procurement Strategy

Cloud instances grew 16.55% in 2025-2026, chipping away at the sizable on-premise installed base that once held 71.05% of the human resource information system market. Small and medium enterprises gravitate to subscription bundles that eliminate capex and deliver immediate compliance updates. Multinationals favor cloud single-instance architectures to enforce common job codes, compensation bands, and review cycles across borders. The European Banking Authority’s outsourcing guidelines, however, push many continental banks to retain on-premise payroll cores paired with cloud talent add-ons, creating hybrid topologies that vendors are starting to de-support.[2]European Banking Authority, “Outsourcing Guidelines,” EBA.EUROPA.EU

On-premise persistence stems from audit latency control and upgrade timing. Yet Deloitte pegs IT staffing needs for on-premise HRIS at 2.5 × those of cloud, making total cost of ownership tilt decisively toward hosted options over a five-year horizon. As a result, many regulated buyers are negotiating sovereign-cloud carve-outs rather than sticking indefinitely to in-house data centers.

By Organization Size: SMEs Propel Incremental Growth

Small and medium enterprises contribute the fastest incremental dollars in HRIS market, growing at 15.76% through 2031 as vendors unbundle advanced functions into tiered price points often below USD 10 per employee monthly. Gusto’s 2026 expansion of employer-of-record services lets start-ups pay global contractors, file local taxes, and arrange benefits across 120 countries, capabilities once limited to large multinationals. Large enterprises still account for most spending but are entering replacement cycles more slowly, focusing instead on rationalizing multiple niche tools into a single human capital platform.

Barriers for SMEs are chiefly financial and educational. Only 21% of Asia-Pacific organizations maintain stand-alone HR-tech budgets, forcing HR leaders to win internal funding that often favors front-office software. Vendors mitigate sticker shock with freemium tiers, yet stripped-down modules exclude predictive analytics and multi-country payroll, limiting appeal once a firm scales beyond 250 staff.

By End-User Industry: Healthcare Surges Ahead

Information technology and telecom held 28.54% revenue in 2025, but healthcare is the high-growth star, projecting a 14.89% CAGR as hospitals embed shift-bidding, credential tracking, and acuity-based staffing algorithms. Scientific Reports documented a 34% reduction in nurse schedule conflicts and 18% lower overtime at a 400-bed facility after deploying an AI-infused HRIS. Banking and insurance prioritize robust audit trails to satisfy regulators, while manufacturing ties workforce planning to production lines through integrations exemplified by the UKG-IFS alliance.

Retail emphasizes time-and-attendance across dispersed outlets, with demand peaking during seasonal hiring. Government agencies lag due to budget cycles and data-residency strictures. Nevertheless, e-government drives in the Middle East and Africa are nudging public bodies to modernize payroll and pension calculations to meet digital wage-payment laws.

Geography Analysis

North America secured 38.02% of 2025 revenue thanks to early Fortune 500 adoption and a dense ecosystem of payroll bureaus. Growth now concentrates in mid-market firms of 500-2,500 staff that historically relied on outsourced payroll and spreadsheets. Workday GO, introduced in November 2025, speaks to this gap by bundling standardized workflows into packages that implement in under six weeks.[3]Workday Investor Relations, “Europe Data-Center Expansion,” INVESTOR.WORKDAY.COM Compliance complexity, from California pay-transparency to Colorado job-posting mandates, nudges buyers toward configurable rule engines rather than hard-coded logic.

Asia-Pacific is the fastest climber, with a projected 15.34% CAGR that will lift its slice of the human resource information system market by 2031. India typifies the leapfrog effect: two-thirds of SMEs show digital readiness, yet the vast majority limit purchases to payroll and attendance, underscoring the need for vendor education. China’s electronic social-insurance filing requirement is pulling manufacturers into the cloud, while Japan and South Korea tiptoe away from on-premise toward sovereign-cloud models. Australia and New Zealand exhibit North American-style saturation but remain growth targets for vendors that can guarantee Fair Work Commission compliance.

Europe’s trajectory is defined by aggressive enforcement of GDPR and the EU AI Act. Fines ballooned nine-fold between 2023 and 2024, prompting companies to invest in consent-management dashboards and documentation of algorithmic logic. Workday’s EUR 175 million (USD 186 million) expansion of Frankfurt and Dublin data centers in November 2025 addresses customers that demand EU-based residency. Southern markets, Spain, Italy, and Greece, remain fragmented, with local payroll outsourcers defending share against cloud newcomers. South America, the Middle East and Africa contribute smaller slices but post double-digit growth as governments digitize labor registries and multinationals standardize global HR platforms.

Competitive Landscape

The five largest vendors, Workday, SAP, Oracle, ADP, and UKG, control roughly 45-50% of the human resource information system (HRIS) market, leaving room for disruptors specializing in verticals, mid-market speed, or unified IT-HR consoles. Thoma Bravo’s USD 12.3 billion take-private of Dayforce in 2025 signals that private equity sees long-term value in assembling full-suite offerings that cross-sell payroll, learning, and analytics. Workday’s 2025 purchases of Paradox and Sana plug conversational recruiting and AI-generated learning into its stack, while SAP’s SmartRecruiters deal shores up its applicant tracking.

Hungry challengers raise substantial capital: Rippling collected USD 450 million at a USD 16.8 billion valuation in 2025 to fuse HR, IT, and spend management within a single interface. Vertical specialists thrive, too; healthcare-focused platforms squeeze overtime by algorithmically matching credentialed nurses to demand curves, and manufacturing suites integrate with MES to forecast labor needs alongside machinery utilization.

Compliance acumen increasingly separates winners from stragglers. The EU AI Act brands HR algorithms “high risk,” compelling exhaustive documentation and human override. Large incumbents allocate dedicated legal and engineering teams to meet these mandates, while bootstrapped start-ups pivot toward lower-risk use cases such as expense tracking. Open-API strategies form another moat: platforms that ship 1,000-plus certified connectors to benefits, background-check, and productivity apps expedite rollouts and minimize costly custom code.

Human Resource Information System (HRIS) Industry Leaders

Workday, Inc.

SAP SE

Oracle Corporation

Automatic Data Processing, Inc.

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Workday introduced Workday GO, a turnkey mid-market package that reduces deployments to four weeks.

- November 2025: Workday purchased Sana, an AI-driven learning tool that auto-generates personalized courses.

- September 2025: Workday unveiled Workday Data Cloud, a cross-functional analytics layer queried through natural language.

- August 2025: Thoma Bravo finalized the USD 12.3 billion acquisition of Dayforce to accelerate international growth.

Global Human Resource Information System (HRIS) Market Report Scope

Human Resource Information System (HRIS) platforms are revolutionizing how organizations handle employee data and HR tasks. These integrated software solutions streamline essential functions, from payroll and attendance to compliance tracking and organizational reporting. By centralizing workforce information, HRIS not only boosts accuracy and reduces manual workloads but also ensures companies stay compliant with regulations. As businesses increasingly digitize their HR operations and lean towards cloud-based systems for enhanced scalability and interoperability, the HRIS market is witnessing robust growth.

The Human Resource Information System (HRIS) Market Report is Segmented by Component (Software, and Services), Deployment Model (On-Premise, and Cloud), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (IT and Telecom, BFSI, Healthcare, Manufacturing, Retail and E-Commerce, Government, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-Premise |

| Cloud |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| IT and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Manufacturing |

| Retail and E-Commerce |

| Government |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | On-Premise | |

| Cloud | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-User Industry | IT and Telecom | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Government | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current human resource information system (HRIS) market size?

As of 2026, the human resource information system (HRIS) market size stands at USD 19.86 billion and is on track to reach USD 37.82 billion by 2031.

Which segment is growing fastest within HRIS deployments?

Cloud-based solutions are expanding at a 16.55% CAGR because subscription pricing eliminates capex and supplies instant compliance updates.

Why is healthcare adopting HRIS faster than other industries?

Hospital systems require shift-bidding, credential tracking, and AI workforce planning to mitigate nursing shortages, driving a projected 14.89% CAGR in healthcare HRIS spend.

How are regulations shaping vendor roadmaps?

GDPR penalties and the EU AI Act compel providers to add audit trails, explainable algorithms, and regional data centers, forcing smaller vendors either to specialize or exit.

Which regions will contribute the most incremental HRIS revenue by 2031?

Asia-Pacific will lead incremental growth with a projected 15.34% CAGR, bolstered by digital-first start-ups in India and mandatory e-filing reforms in China.

Page last updated on: