Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Managed Hosting Market Report is Segmented by Service Type (Network Hosting, Application Hosting, Database Hosting, Web Hosting, Email Hosting, Other Service Types), Deployment Model (On-Premise, Cloud-Based, Hybrid), Organization Size (Small and Medium Enterprises, Large Enterprises), Industry Vertical (IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

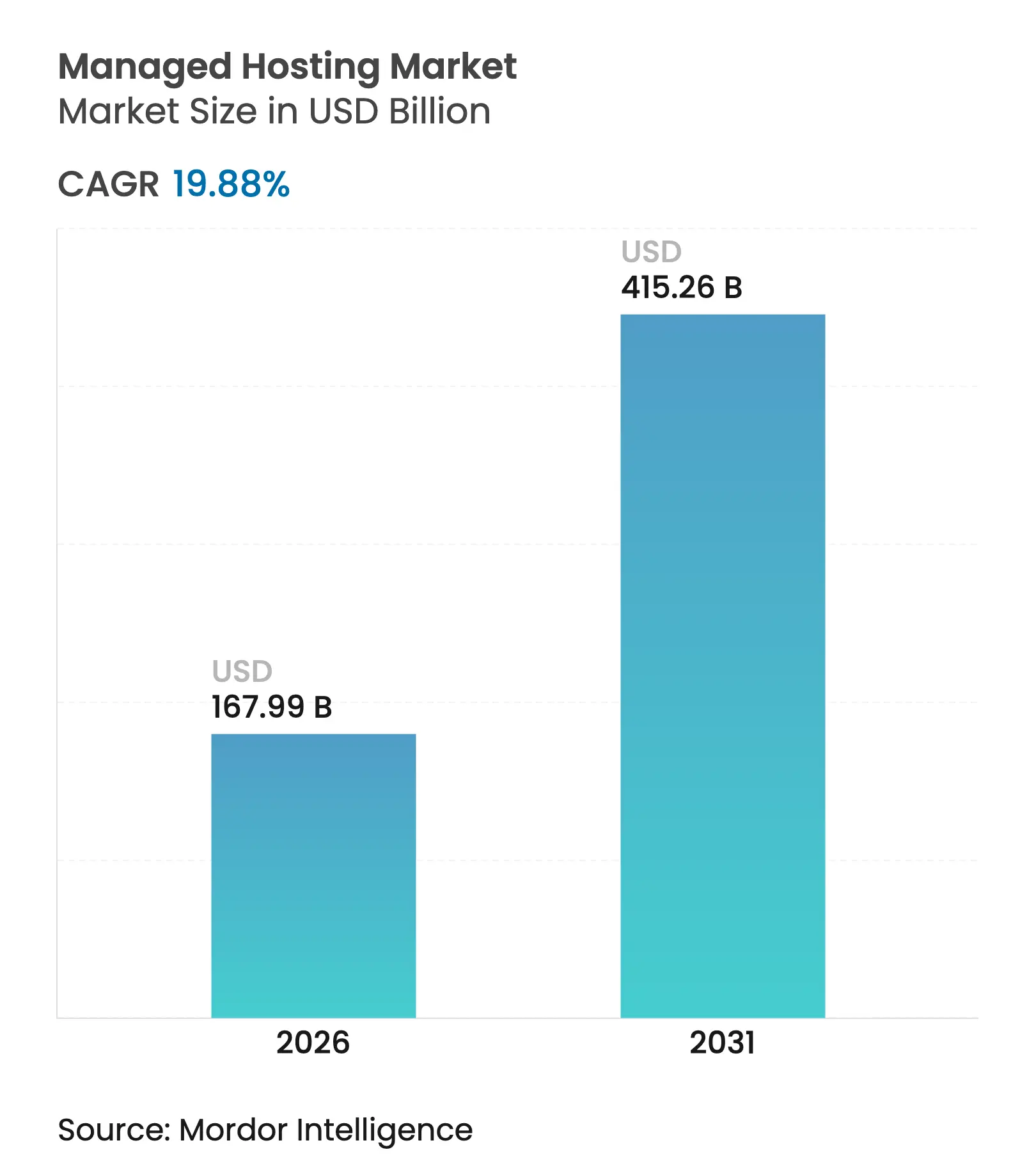

| Market Size (2026) | USD 167.99 Billion |

| Market Size (2031) | USD 415.26 Billion |

| Growth Rate (2026 - 2031) | 19.88 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The managed hosting market size was valued at USD 140.11 billion in 2025 and estimated to grow from USD 167.99 billion in 2026 to reach USD 415.26 billion by 2031, at a CAGR of 19.88% during the forecast period (2026-2031). Robust growth reflects enterprises’ decision to externalize infrastructure management as AI workloads demand specialized compute architectures that internal IT teams struggle to provision and maintain. Expansion is also propelled by sovereign-cloud mandates, edge-computing roll-outs and AI-driven cost-optimization tools that unlock operational efficiencies previously out of reach. Hyperscale capital expenditure, illustrated by AWS’s multi-trillion-yen investment in Japan, signals long-term confidence in outsourced infrastructure, while mid-market customers adopt managed services to gain enterprise-grade uptime and security without large capital outlays. Meanwhile, data-center power constraints are emerging as a strategic bottleneck as AI racks draw 50-100 kW compared with the historical 10-15 kW envelope, prompting vendors to explore advanced cooling and power-distribution innovations.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for cloud-based solutions Rising demand for cloud-based solutions | +4.2% | Global | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+4.2% | Geographic Relevance:Global | Impact Timeline:Medium term (2-4 years) |

Heightened focus on data security and compliance Heightened focus on data security and compliance | +3.8% | North America and EU, Asia-Pacific core | Short term (≤ 2 years) | |||

Digital-commerce expansion among SMEs Digital-commerce expansion among SMEs | +3.1% | Global, with concentration in Asia-Pacific and Latin America | Medium term (2-4 years) | |||

Edge-data-center proliferation enabling low-latency hosting Edge-data-center proliferation enabling low-latency hosting | +2.9% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) | |||

AI-driven TCO optimization of managed stacks AI-driven TCO optimization of managed stacks | +2.7% | Global | Short term (≤ 2 years) | |||

Sovereign-cloud mandates in emerging economies Sovereign-cloud mandates in emerging economies | +2.4% | Asia-Pacific, MEA, selective EU markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Cloud-Based Solutions

Enterprises are moving decisively toward multicloud architectures, with survey data showing that 86% plan to run diversified cloud portfolios within two years. Manufacturing firms underscore the operational urgency: every minute of unplanned downtime can cost millions, leading them to prioritize redundant cloud deployments that safeguard production lines. Generative-AI workloads intensify the shift; AWS’s Project Rainier clusters deliver roughly five-fold compute density versus previous generations, making in-house parity unrealistic for most enterprises. [1]aboutamazon.com, “AWS’s Project Rainier: the world’s most powerful computer for training AI,” aboutamazon.com As a result, cloud migration is framed less as a cost-cutting measure and more as a prerequisite for AI-enabled product innovation, especially in real-time risk analytics for financial institutions. The driver therefore underpins sustained demand for high-performance managed hosting environments that guarantee low latency, compliance and rapid scalability.

Heightened Focus on Data Security and Compliance

Regulatory scrutiny is reshaping hosting strategies as 40% of large organizations are expected to re-host at least 10% of workloads on sovereign-cloud platforms this year. [2]Telefonica Tech, “What is sovereign cloud (and why it’s important for your business),” telefonicatech.com Central-bank initiatives such as India’s forthcoming national cloud illustrate governments’ direct entry into the infrastructure arena. Healthcare providers highlight the compliance advantage: Seattle Children’s Hospital achieved 99.999% uptime via HIPAA-ready private clouds, removing the complexity of managing public-cloud compliance controls internally. The security imperative now encompasses operational resilience, identity-centric defense and zero-trust frameworks, which managed hosting vendors bundle as turnkey services. Providers that can blend sovereign-data assurances with enterprise-grade SLAs are therefore positioned for outsized growth in the managed hosting market.

Digital-Commerce Expansion Among SMEs

SMEs are increasingly capturing digital-commerce opportunities by leveraging managed platforms that deliver enterprise-class performance without heavy capital expenditure. Latin America saw cloud spending jump 85% year-on-year as mid-market merchants embraced scalable hosting to address traffic spikes during flash sales. User-experience stakes are high; research shows 47% of shoppers abandon carts when pages exceed two-second load times, pressing businesses to secure low-latency infrastructure. Managed hosting vendors now offer edge-node deployments in populous cities, cutting latency by as much as 60% and giving small retailers the responsiveness that once only global players could afford. As these capabilities spread, SMEs’ share of the managed hosting market is climbing, fueling broader market diversification.

Edge-Data-Center Proliferation

Sub-millisecond response targets for AI inference, gaming and industrial IoT drive enterprises toward localized compute footprints. Asia-Pacific leads the build-out, with EdgeConneX’s entry into Japan signaling the region’s appetite for near-user infrastructure. 5G roll-outs push traffic to the edge, reducing backhaul and shaving costs. Manufacturers adopt on-site micro-data-centers that support real-time quality control algorithms, avoiding bandwidth-hungry round-trips to distant clouds. Managed hosting providers that integrate edge nodes into their core offerings stand to differentiate on latency guarantees and geographic reach, reinforcing long-term demand in the managed hosting market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High total cost of ownership for premium tiers High total cost of ownership for premium tiers | -2.1% | Global, particularly North America and EU | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-2.1% | Geographic Relevance:Global, particularly North America and EU | Impact Timeline:Short term (≤ 2 years) |

Vendor lock-in and migration complexity Vendor lock-in and migration complexity | -1.8% | Global | Medium term (2-4 years) | |||

Shortage of skilled cloud architects in developing regions Shortage of skilled cloud architects in developing regions | -1.4% | Asia-Pacific emerging markets, MEA, Latin America | Long term (≥ 4 years) | |||

Data-centre power-supply constraints Data-centre power-supply constraints | -1.2% | Global, acute in established markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Total Cost of Ownership for Premium Tiers

Enterprises often underestimate cloud fee structures: granular charges across thousands of SKUs inflate bills and make forecasting difficult. Case studies show firms slashing costs by up to 500% by switching from hyperscale on-demand instances to specialized managed hosting contracts that bundle compute, storage and bandwidth at fixed rates. AI training intensifies the issue because GPU hours priced for elasticity become untenable for sustained workloads. Vendors that provide transparent pricing, reserved-instance arbitrage and continuous rightsizing analytics are therefore winning share as buyers seek predictable economics in the managed hosting market.

Vendor Lock-In and Migration Complexity

When applications become tightly coupled to proprietary platform services—queues, databases, event buses—exit costs soar. CIO surveys reveal multiyear migration timelines and extensive refactoring budgets when leaving a primary cloud. [3]CIO, “Switching Cloud Providers Is No Cakewalk, but Do Your Users Know That?” cio.comLegal, data-protection and contractual hurdles further complicate exits. Managed hosting providers that architect portability through Kubernetes, open APIs and multi-cloud abstractions can reduce lock-in risks, but the inertia still curbs switching and slows overall expansion rates.

By Service Type: Database Hosting Accelerates Enterprise Modernization

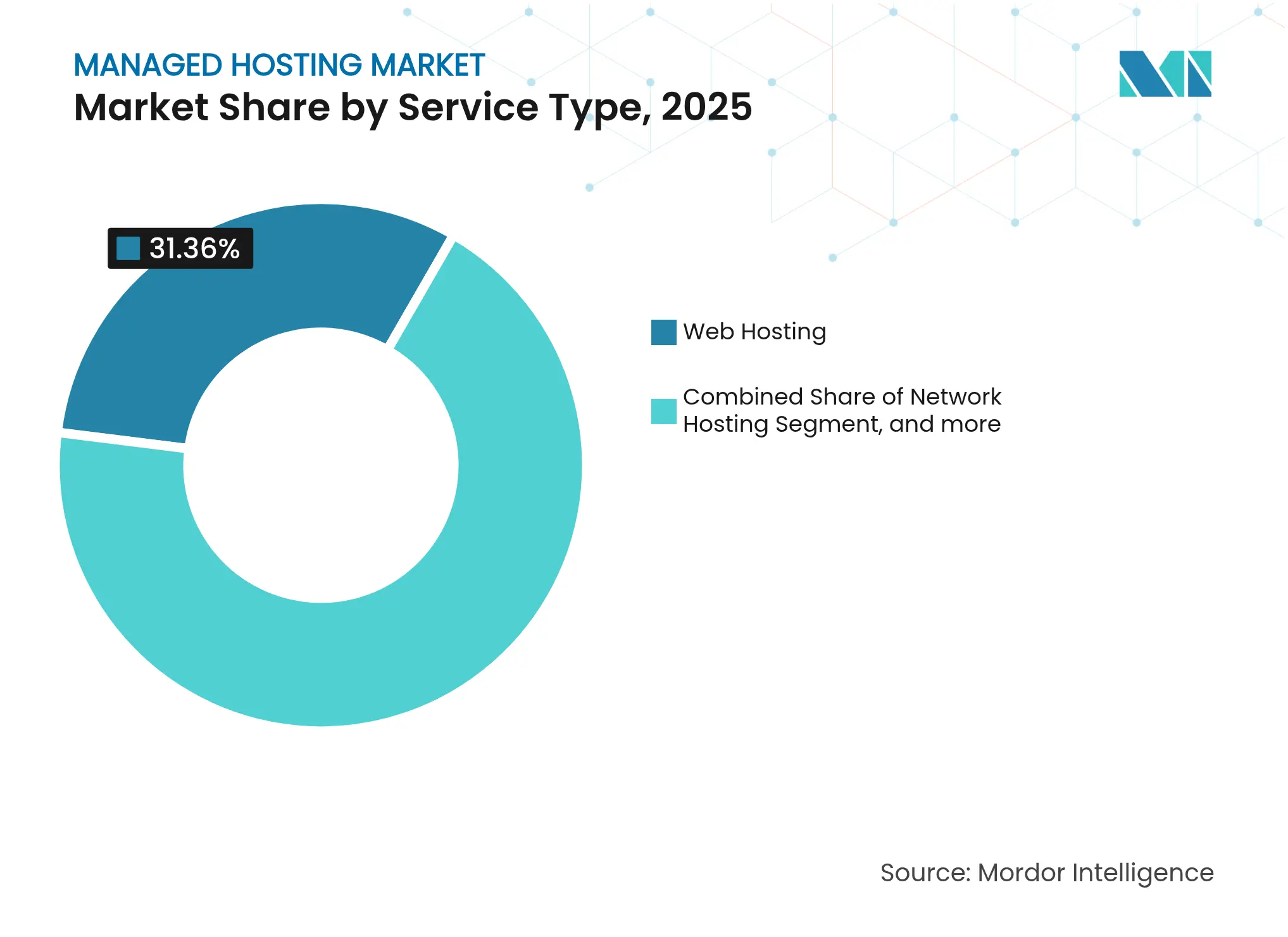

Database hosting captured heightened attention as enterprises sought specialized tuning that trims Oracle licensing fees by up to 50% while unlocking 321% higher IOPS versus generic cloud offerings. The segment is projected to log a 20.42% CAGR, becoming a central growth engine for the managed hosting market. Web hosting remains the largest slice, retaining 31.36% of managed hosting market share in 2025 thanks to legacy footprints and SME website demand. Application hosting rides container adoption, giving developers portable microservices environments, while network-hosting services support dedicated links and secure VPNs across hybrid estates.

Continued expansion in database hosting is also catalyzed by AI workloads that rely on vector databases for similarity search and real-time analytics. Providers bundle managed backup, patching and performance-optimization, relieving in-house teams from complex maintenance. Meanwhile, email-hosting customers are migrating away from on-premises servers toward unified collaboration suites, reinforcing the managed hosting market’s shift to subscription economics.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Model: Hybrid Architectures Offer Optimal Flexibility

On-premise environments held 44.92% of the managed hosting market size in 2025, reflecting the inertia of sunk investments and compliance requirements. Yet hybrid deployments are forecast to surge at 20.31% CAGR as enterprises pursue “right-workload, right-location” strategies that safeguard sensitive data while exploiting public-cloud elasticity. Cloud-only footprints expand steadily, especially among digitally native SMEs.

Hybrid adoption is fueled by standardized orchestration layers that provide single-pane-of-glass management across colocation spaces and hyperscale regions. Generative-AI guardrails, for example, often require on-premise data residency with burst-to-cloud training phases, a pattern that hybrid managed hosting seamlessly supports. Providers offering integrated networking, identity federation and uniform observability across locations gain a competitive edge as enterprises converge on multi-environment operations.

By Organization Size: SMEs Narrow the Capability Gap

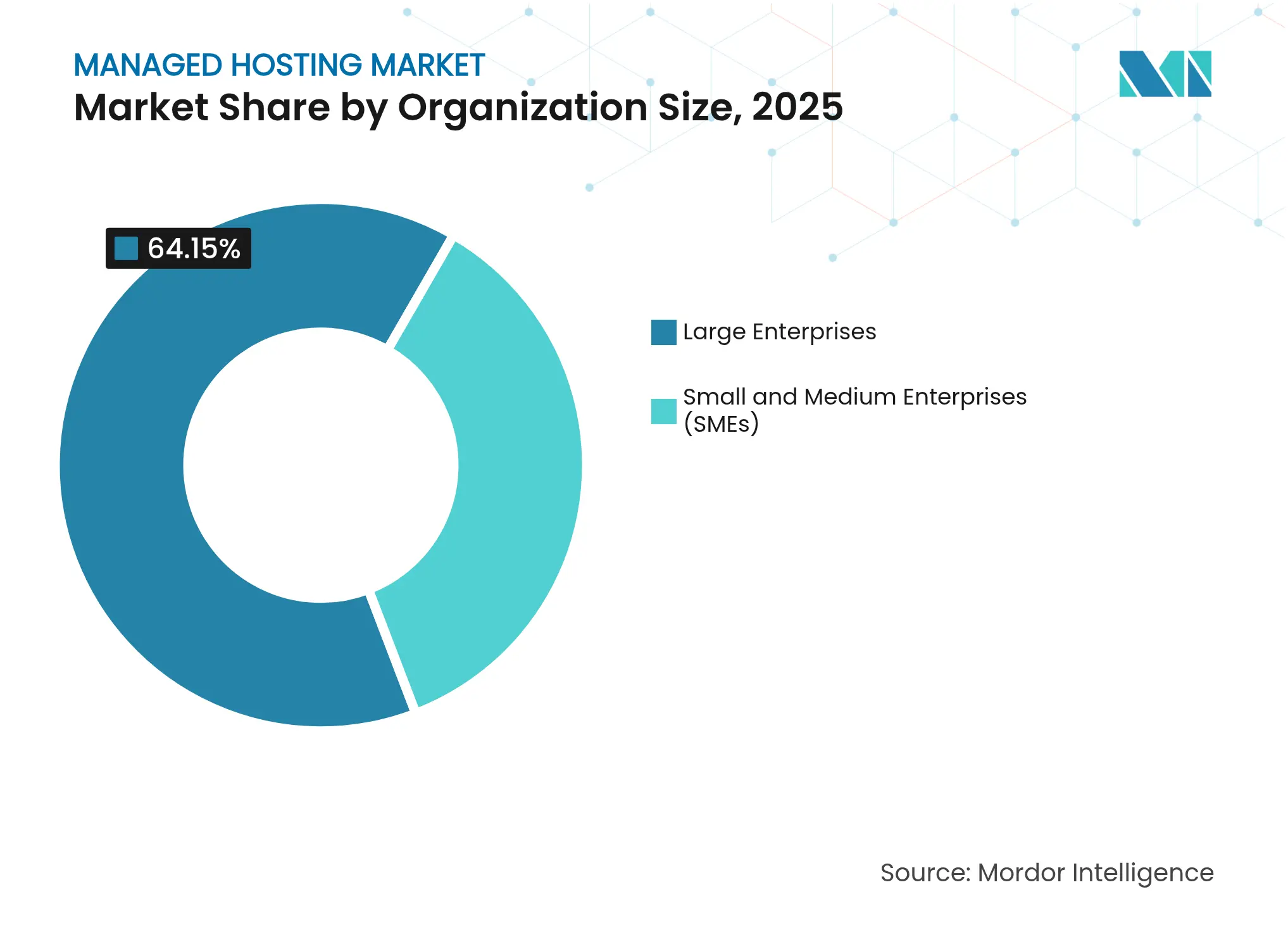

Large companies still dominate revenue, accounting for 64.15% of managed hosting market demand in 2025, but SMEs are the fastest growers at 20.22% CAGR. Falling entry costs and packaged services allow smaller firms to deploy globally distributed resources without hiring specialized talent. Evolve Media’s switch from self-managed colocation to AWS-backed managed services yielded a 30% cost drop upfront, expanding to 50% after optimization rounds.

As managed hosting providers introduce tiered offerings with predictable monthly fees, SMEs secure enterprise-grade SLAs for latency, backup and security, leveling the playing field. Meanwhile, large enterprises remain key contributors, using managed solutions to refocus scarce engineers on product development rather than infrastructure upkeep. This dual-segment momentum underscores durable growth prospects for the managed hosting market.

Note: Segment shares of all individual segments available upon report purchase

By Industry Vertical: Healthcare Surges on Compliance-Driven Digitization

BFSI retains the top spot with 23.12% of managed hosting market share, underpinned by real-time trading algorithms and stringent uptime mandates. Healthcare, however, leads on growth, advancing at 20.28% CAGR as hospitals digitize patient journeys and deploy AI-driven diagnostics on HIPAA-compliant clouds. Retail and eCommerce capitalizes on holiday peaks with auto-scaling storefronts, while manufacturing embraces edge nodes for predictive maintenance.

Telecom players modernize OSS/BSS stacks in preparation for 5G monetization, and government agencies move to sovereign-cloud setups to address data-residency statutes. Education institutions adopt cloud VDI solutions to support hybrid learning, but budget constraints temper pace relative to commercial sectors. Across industries, regulatory compliance and AI readiness are the twin catalysts driving expansion of the managed hosting market.

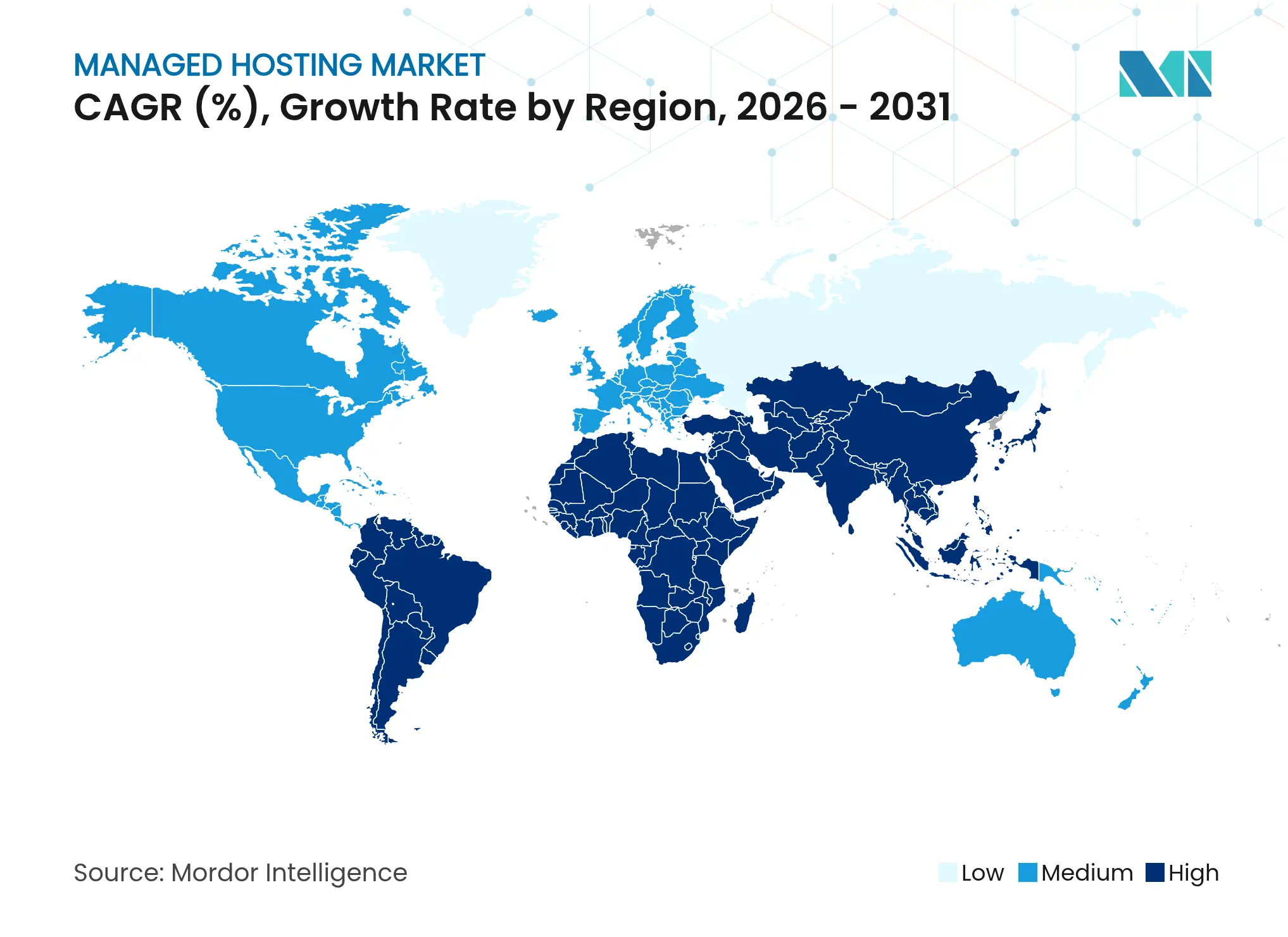

North America controlled 40.76% of the managed hosting market in 2025, a lead built on early cloud adoption, mature enterprise IT budgets and a robust ecosystem of hyperscale and colocation facilities. Power-availability challenges are becoming acute as AI GPUs push rack densities beyond 100 kW, prompting data-center operators to invest in advanced cooling and micro-grid solutions. Continued earnings acceleration—AWS posted USD 10 billion quarterly operating profit demonstrates sustained regional demand, yet expansion increasingly hinges on securing grid capacity and renewable energy supply.

Asia-Pacific stands out as the fastest-growing territory, projected at 20.47% CAGR to 2031. Factors include sovereign-cloud mandates, accelerating AI initiatives and heavy infrastructure spending such as AWS’s USD 15.1 billion Japan investment. China’s cloud expenditure is set to hit USD 11.1 billion in 2025 and continues to benefit domestic champions that dominate 71% of local share. Regional service providers, however, still treat managed services as adjunct revenue lines, leaving room for specialists to capture unmet demand.

Europe, South America and the Middle East and Africa display mixed trajectories. European enterprises grapple with GDPR and emerging data-sovereignty laws, stimulating demand for regionally partitioned cloud zones. Latin American data-center value is projected to double to USD 8-10 billion by 2029 on the back of AI use-cases and cloud-native commerce. African markets have posted 30% annual cloud-revenue growth over the past three years, yet face bandwidth costs and skills shortages that temper broader market penetration. These divergences affirm a multi-speed expansion pattern that will shape provider localization strategies.

Market Concentration

The managed hosting market remains moderately consolidated; AWS, Microsoft Azure and Google Cloud capture roughly 64% of enterprise cloud infrastructure revenue, but specialized vendors are carving out profitable niches. AWS leads with about 30% share and quarterly cloud revenue of USD 28.8 billion, followed by Azure at 21% and USD 25.5 billion, and Google Cloud at 12% and USD 12 billion. Differentiation has shifted toward verticalized offerings: Tessell’s managed-database platform, for example, claims a 250% three-year ROI over conventional SQL deployments.

Strategic alliances underpin competitive moves. Intel and AWS co-invested in custom Xeon and AI-fabric chips to secure U.S. semiconductor supply chains. Usage AI equips providers with optimization algorithms that cut on-demand compute spending by up to 55%, adding a cost-leadership lever. Microsoft is integrating Copilot agents into Azure administration to automate routine tasks and free engineers for higher-value projects. Players that marry AI-driven automation with compliance-aware architectures are expected to outperform as buyers seek both cost savings and governance assurances.

Edge and sovereign clouds constitute emerging battlegrounds. Providers like EdgeConneX are scaling geographically distributed micro-facilities to serve latency-sensitive industrial and media applications. In parallel, regional telcos and government-backed entities launch national clouds, creating procurement rules that favor local operators. These shifts reduce hyperscale lock-in and expand the addressable base for mid-tier managed hosting specialists.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The managed hosting market refers to services where a third-party provider manages the infrastructure required to host websites, applications, and data for businesses. These services typically include server management, security, data backup, monitoring, and software updates. Managed hosting allows businesses to focus on their core operations while outsourcing IT infrastructure responsibilities. The market is driven by the growing demand for secure, scalable, and reliable hosting solutions across various industries.

The Managed Hosting Market is segmented by service type (network hosting, application hosting, database hosting, web hosting, email hosting, and other service types), deployment model (on-premise, cloud-based, hybrid), organization size (small and medium enterprises (SMEs), large enterprises), industry vertical (IT & telecom, BFSI (banking, financial services, and insurance), healthcare, retail, media & entertainment, manufacturing, government, education, and other industry verticals), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.