Hospitality Property Management Software (PMS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

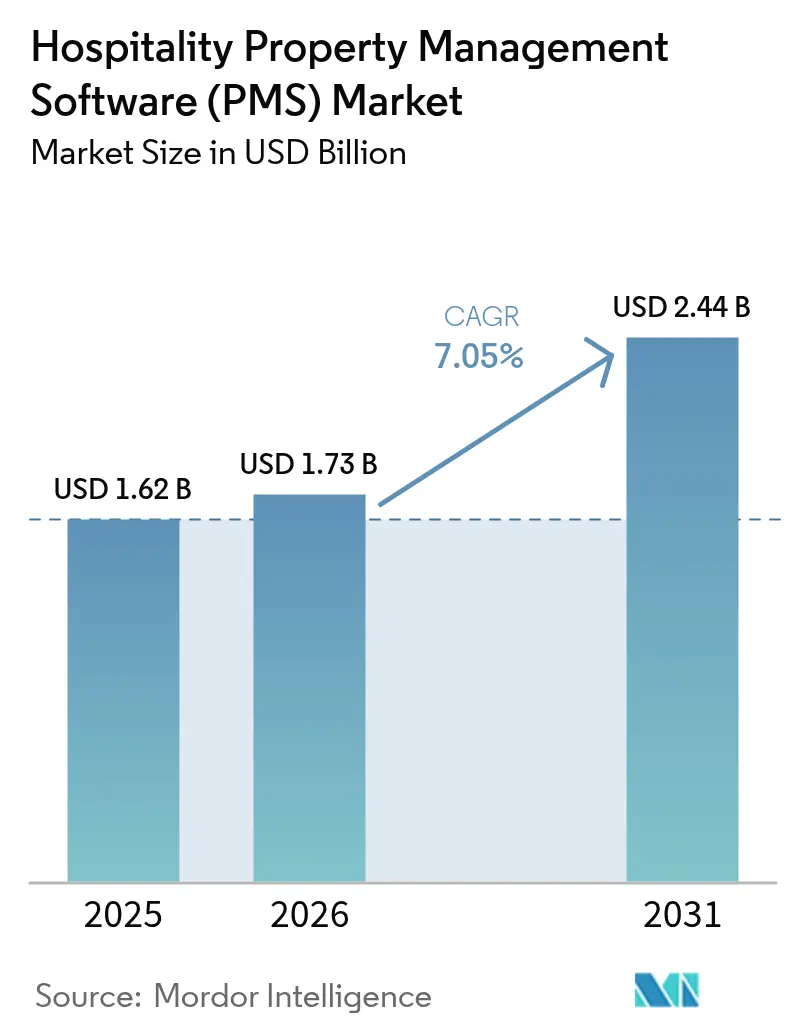

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

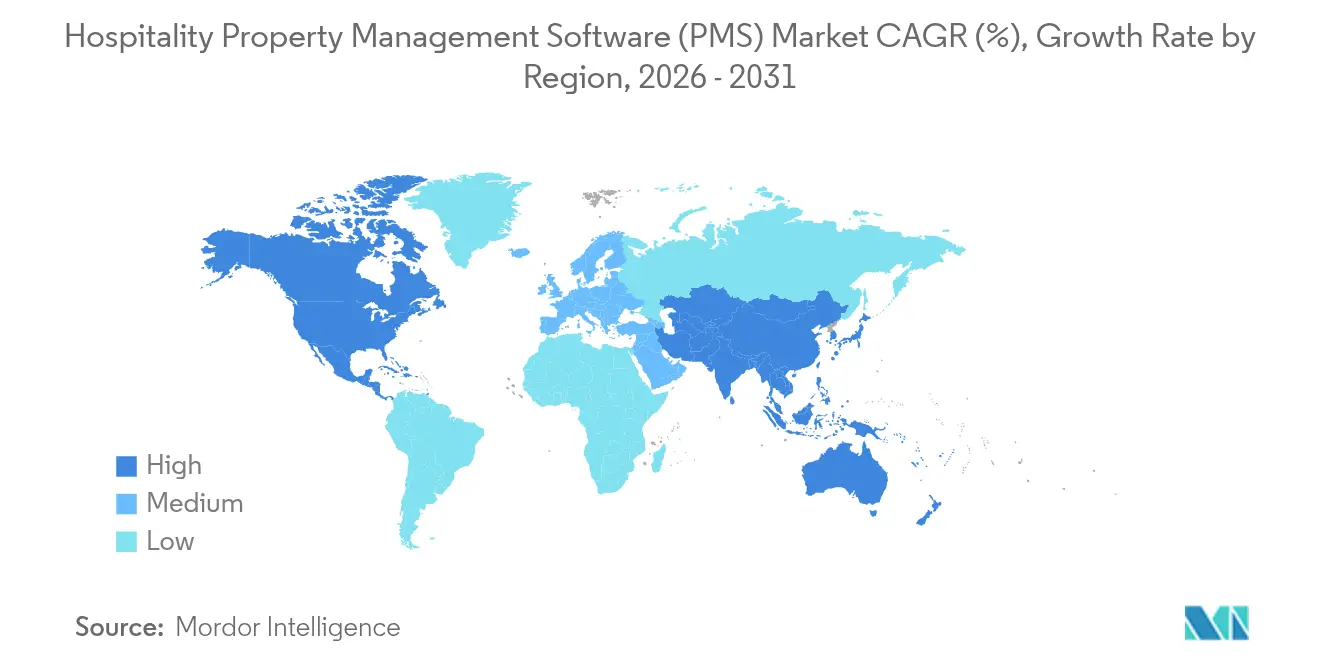

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players-Market-ML.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospitality Property Management Software (PMS) Market Analysis by Mordor Intelligence

Hospitality Property Management Software market size in 2026 is estimated at USD 1.73 billion, growing from 2025 value of USD 1.62 billion with 2031 projections showing USD 2.44 billion, growing at 7.05% CAGR over 2026-2031. Growing replacement of legacy systems, accelerated cloud migration, and the embedding of artificial-intelligence revenue tools underpin this steady value expansion. Cloud deployment continues to reshape cost structures by removing on-premise hardware, while API-first architectures cut integration time and open new revenue-sharing partnerships. Independent hotels and homestay operators now adopt sophisticated modules once limited to global chains, widening the total addressable pool and boosting competitive intensity. Meanwhile, region-specific digitalization programs in Asia-Pacific position emerging markets as outsized contributors to future license growth, even as North America focuses on advanced feature uptake.

Key Report Takeaways

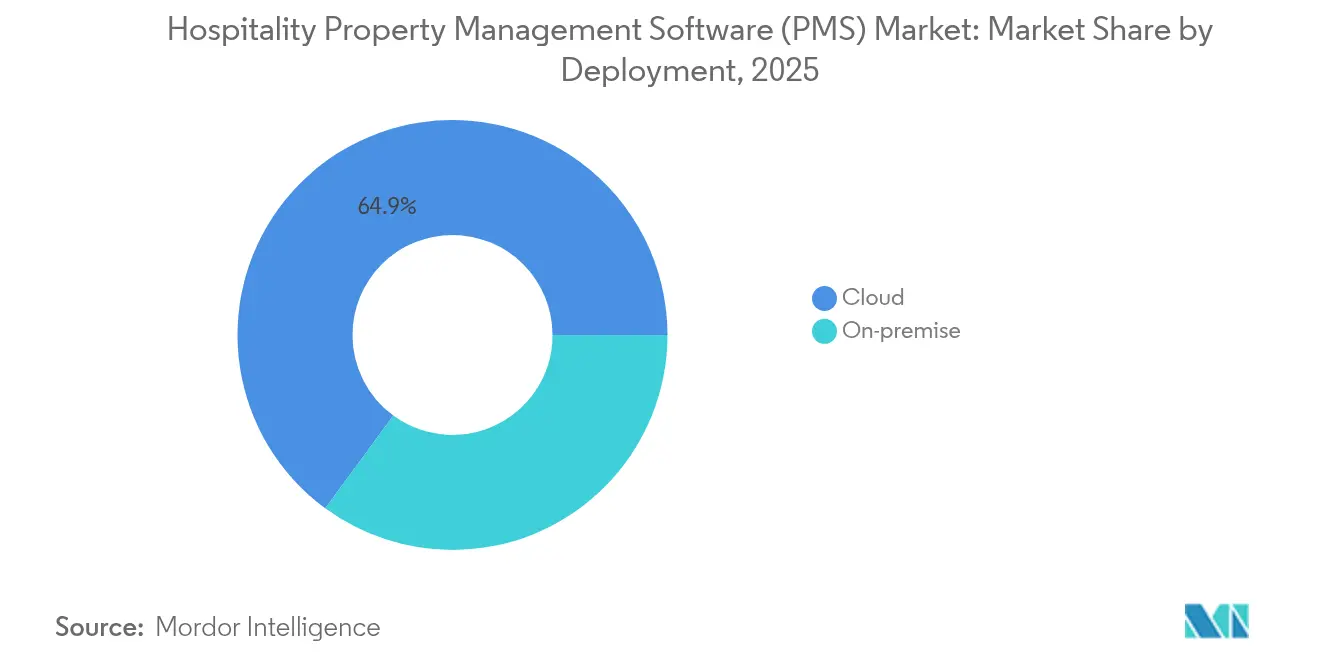

- By deployment, cloud accounted for 64.92% of the Hospitality Property Management Software market share in 2025; on-premise is contracting while cloud is expanding at a 12.38% CAGR through 2031.

- By property size, small and medium enterprises captured 57.05% share of the Hospitality Property Management Software market size in 2025 and are advancing at an 11.07% CAGR to 2031.

- By property type, hotels and resorts held 47.65% revenue share in 2025; homestay accommodations are forecast to grow at a 12.84% CAGR to 2031.

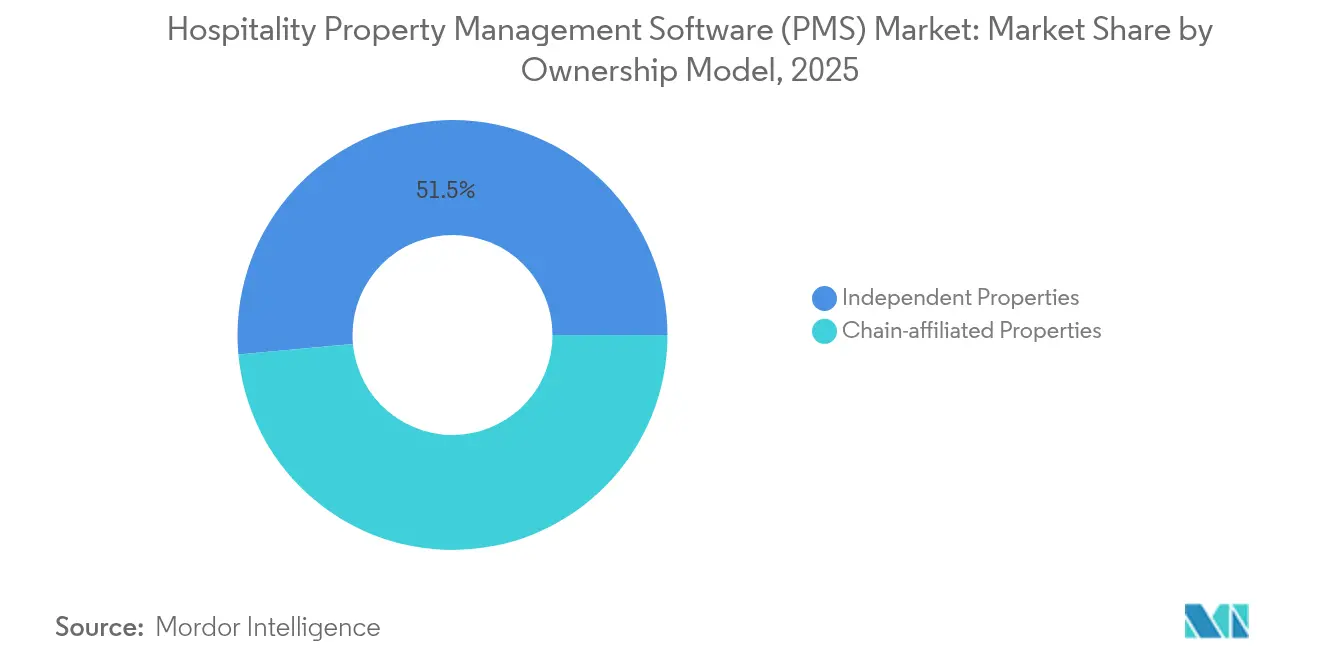

- By ownership model, independent properties commanded 51.45% of the Hospitality Property Management Software market share in 2025, while the same segment is progressing at an 11.62% CAGR through 2031.

- By functionality module, front-desk and operations led with 41.20% share of the Hospitality Property Management Software market size in 2025; revenue-management modules are expanding at a 14.02% CAGR to 2031.

- By geography, North America contributed 34.20% of 2025 revenue; Asia-Pacific is registering the fastest 12.18% CAGR and will narrow the gap by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hospitality Property Management Software (PMS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption among small- and medium-scale properties | +1.8% | Global, Asia-Pacific and Europe | Medium term (2-4 years) |

| Rapid shift from on-premise to cloud-based SaaS models | +2.1% | Global, led by North America and Asia-Pacific | Short term (≤2 years) |

| Expansion of OTA/meta-search integrations | +1.2% | Europe and North America | Medium term (2-4 years) |

| API-first, composable PMS architectures | +0.9% | North America and Europe | Long term (≥4 years) |

| AI-driven revenue-management add-ons | +1.4% | Global, early adoption in developed markets | Medium term (2-4 years) |

| ESG-reporting mandates | +0.6% | Europe, spreading to North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing adoption among small- and medium-scale properties

Small operators now view modern PMS solutions as strategic necessities rather than discretionary upgrades, a shift enabled by subscription pricing and simplified onboarding. Independent hotels report double-digit revenue lifts after implementing cloud PMS that bundle channel management and guest-experience functions. Lower upfront cost structures let SMEs redirect capital toward marketing and service innovation, strengthening brand visibility. Vendors reciprocate by releasing self-service implementation wizards that cut deployment time from months to weeks. The result is a virtuous cycle in which feature uptake accelerates across thousands of lower-tier properties, broadening the Hospitality Property Management Software market footprint.

Rapid shift from on-premise to cloud-based SaaS models

Cloud-native suites eliminate hardware refresh cycles and provide automatic version updates that keep properties secure and compliant. Large migrations such as citizenM’s 7,500-room rollout demonstrate that even enterprise portfolios can convert in weeks. Real-time access to analytics supports granular decision-making across geographically dispersed teams. Multitenant architectures also centralize disaster-recovery protocols, easing audit burdens and insurance premiums. With recurring subscription fees replacing lumpy capex, CFOs gain predictability, further propelling Hospitality Property Management Software market adoption.

AI-driven revenue-management add-ons boosting ROI

Dynamic pricing engines embedded in PMS platforms now react to demand signals drawn from competitor rates, flight searches, and local events, raising room revenue by up to 10% [1]Apaleo GmbH, “CitizenM PMS Migration,” hospitalitynet.org . Guestline’s AI module automates forecasting, freeing staff to focus on experiential upgrades. Machine-learning models also recommend ancillary offers that increase total guest spend, reinforcing cross-selling capabilities. Adoption is fastest where labor shortages constrain manual revenue teams, notably in North America. As predictive accuracy improves, properties embed AI dashboards into daily briefings, making algorithmic insights a routine input to management meetings within the Hospitality Property Management Software market.

API-first, composable PMS architectures unlocking ecosystem innovation

Open APIs let hotels cherry-pick best-of-breed modules without risking data silos, a core requirement for chains pursuing personalized guest journeys. Technology suppliers certify integrations in sandboxes, trimming engineering backlogs and accelerating go-live dates. The approach reduces vendor lock-in and fosters continuous experimentation with niche solutions—ranging from automated energy controls to spa scheduling. Start-ups entering adjacent domains can tap ready demand by publishing connectors, widening the Hospitality Property Management Software market partner network. Over time, the composable trend shifts evaluation criteria toward interoperability as much as feature depth.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity with legacy systems | -1.1% | Global, pronounced in mature markets | Short term (≤2 years) |

| Heightened data-security / privacy compliance costs | -0.8% | Europe (GDPR), expanding globally | Medium term (2-4 years) |

| Escalating OTA API-fee structure | -0.7% | Global, stronger impact in Europe | Medium term (2-4 years) |

| Shortage of skilled IT talent | -0.5% | Global, acute in developed economies | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Integration complexity with legacy and third-party systems

Many heritage properties still operate bespoke booking engines and point-of-sale modules built two decades ago, hampering smooth data exchange. Custom connectors frequently exceed budget and extend timelines, prompting some hotels to delay upgrades despite clear ROI. Dual-running old and new stacks inflates training needs and risks operational errors. Vendors respond by expanding low-code integration toolkits, yet gaps persist where proprietary data schemas remain undocumented. Until legacy attrition accelerates, this friction will temper near-term growth in segments of the Hospitality Property Management Software market.

Escalating OTA API-fee structure inflating total cost of ownership

Booking platforms now impose layered commissions that can surpass 40% when marketing surcharges are included, compressing net RevPAR for smaller hotels. Revenue-management algorithms must factor variable commission tiers, adding complexity and potential mispricing. Properties increase direct-booking incentives, but doing so demands higher spend on web-experience tools and search-engine marketing. Consequently, the total technology outlay rises even as operators aim to cut distribution costs, muting absolute margin gains within the Hospitality Property Management Software market. Vendors that embed real-time fee tracking into PMS dashboards are gaining favor among budget-conscious hoteliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud dominance accelerates digital transformation

Cloud platforms represented 64.92% of 2025 value and are forecast to widen their lead as properties prioritize scalability and lower upkeep. The Hospitality Property Management Software market size for cloud deployments is on track to reach USD 2.02 billion by 2031, reflecting the 12.38% CAGR cited earlier. Properties benefit from global content-delivery networks that sustain rapid response times, even in remote locations. Vendors bundle continuous feature updates into subscription tiers, pushing security patches without human intervention. Moving workloads off-site also facilitates multi-property consolidation, allowing regional groups to share data warehouses that power uniform guest profiles.

On-premise installations continue in jurisdictions with strict data-sovereignty laws, yet the cost differential widens as hardware ages. Cloud elasticity proves invaluable during seasonal swings, letting resorts scale instances in peak months and downgrade afterward to conserve cash. Enhanced API ecosystems around leading cloud PMS suites enable straightforward integrations with chatbots and IoT room controls, unlocking new service combinations. Ultimately, capital-light cloud economics underpin the fastest expanding channel of the Hospitality Property Management Software market.

By Property Size: SME segment drives market democratization

SMEs held 57.05% revenue in 2025, and their share of the Hospitality Property Management Software market size is expected to surpass USD 1.68 billion by 2031. Easier set-up wizards and freemium trials lower adoption hurdles for operators lacking in-house technologists. Training modules often include micro-learning content in multiple languages, aligning with the diverse talent pool typical of small hotels. SMEs also value device-agnostic interfaces that staff can run from personal smartphones, circumventing PC shortages.

Large enterprises display slower yet steady upgrades as they phase out proprietary platforms in favor of global standards. However, complex brand standards can prolong procurement cycles and integration testing. As SMEs accumulate data across customer touchpoints, they leverage loyalty plug-ins and targeted email campaigns previously reserved for chains, reinforcing the democratization thesis. This shift contributes substantial volume to the Hospitality Property Management Software market, even if absolute ticket sizes are smaller.

By Property Type: Homestay segment leads alternative-accommodation revolution

Although traditional hotels and resorts delivered 47.65% of 2025 turnover, homestay accommodations are set to register the fastest 12.84% CAGR. This portion of the Hospitality Property Management Software market share is being reshaped by individual hosts who professionalize through centralized dashboards that manage availability across multiple OTAs. APIs to smart-lock vendors automate key exchange, permitting frictionless check-ins.

Motels, lodges, and serviced apartments maintain steady demand yet require niche features such as long-stay billing or mixed dorm inventory. Vendors respond with modular add-ons, avoiding bloated, one-size-fits-all deployments. As leisure travelers seek authentic experiences, homestay hosts scale operations from single units to micro-portfolios, driving recurring license revenue. Their rising expectations push PMS providers to harden uptime guarantees and mobile-first designs, injecting new momentum into the Hospitality Property Management Software market.

By Ownership Model: Independent properties challenge chain dominance

Independent hotels captured 51.45% of 2025 revenue and will widen their lead as flexible contract terms let them negotiate best-fit solutions. The Hospitality Property Management Software market size tied to independents is projected to climb at an 11.62% CAGR, outpacing chain affiliates. Lacking corporate IT mandates, owners iterate quickly, piloting AI concierge chatbots or green-energy monitors before chain brands can clear governance hurdles.

Chain-affiliated properties retain scale advantages in loyalty ecosystems and procurement discounts, yet many now permit local tech substitution if interfaces meet group data standards. Hybrid franchise-management models further blur lines, granting operators autonomy in tool selection while preserving brand consistency through open-API data exchanges. This fluidity enlarges the overall Hospitality Property Management Software market by attracting previously reticent franchisees.

By Functionality Module: Revenue management drives optimization focus

Front-desk and operations modules remained indispensable, contributing 41.20% sales in 2025. Nonetheless, revenue-management tools will log a 14.02% CAGR and could cross the USD 540 million threshold by 2031, signaling rising sophistication across user cohorts. The Hospitality Property Management Software market size for these analytics-heavy add-ons reflects hoteliers’ need to offset labor inflation with yield gains.

Channel-management, housekeeping, and mobile-guest-journey features also exhibit solid demand as properties coordinate real-time updates across multiple systems. Integration with point-of-sale and spa scheduling under a single data schema boosts staff productivity and guest personalization. As data maturity grows, revenue algorithms increasingly consider ancillary spend probability rather than room price alone, deepening the strategic role of PMS suites within the broader Hospitality Property Management Software market.

Geography Analysis

North America contributed 34.20% of 2025 value because of long-standing vendor relationships, high cloud penetration, and mature distribution networks. Hotels now focus on advanced feature utilization, such as attribute-based selling and energy-consumption dashboards, to enhance margin resilience . The region’s regulatory stability also speeds third-party certification, shortening time-to-market for emerging modules.

Asia-Pacific is the fastest growing at 12.18% CAGR, propelled by expanding mid-scale hotel pipelines in Southeast Asia and government-funded digital programs. Philippines-based independents alone added more than 10,000 active users to cloud platforms in 2025, validating leapfrog adoption dynamics. Local operators often bypass on-premise entirely, installing mobile-first PMS versions that synchronize seamlessly with QR-code payment ecosystems popular in the region.

Europe remains sizable but heterogeneous, with ESG reporting and data-privacy regulations shaping purchase decisions. Multi-currency support and strong offline access matter in cross-border ski or island markets that experience patchy connectivity. While legacy interface challenges persist, EU sustainability directives are catalyzing upgrades as properties need granular utility tracking embedded in PMS workflows, driving incremental opportunity within the Hospitality Property Management Software market.

Competitive Landscape

The Hospitality Property Management Software market is moderately fragmented: the top five vendors account for roughly 45% of 2024 revenue, leaving headroom for specialty entrants. Oracle and Agilysys leverage deep ERP roots to bundle back-office accounting and analytics, reinforcing account stickiness [3]Agilysys, “Record Revenue Q2 2025,” agilysys.com . Cloud-native challengers such as Mews, Cloudbeds, and Apaleo emphasize open-integration catalogs, resonating with digital-first independents.

M&A momentum continues; Mews’ purchase of Atomize introduced native revenue algorithms, while Agilysys’ USD 150 million spa-software buyout broadened wellness coverage. Funding rounds are equally robust: Lighthouse secured USD 370 million to acquire The Hotels Network, signaling investor confidence in end-to-end commercial platforms. Private-equity stakes—illustrated by Blackstone’s backing of M3—inject capital for international expansion and R&D.

Competitive differentiation increasingly revolves around AI depth, ESG reporting suites, and time-to-deploy metrics. Vendors offering sandbox environments and certified plug-in marketplaces shorten onboarding, earning favor among resource-constrained SMEs. Cyber-security posture is now a gating criterion in RFPs, prompting SOC 2 and ISO-27001 accreditation races. As convergence with adjacent travel-tech segments accelerates, market participants that balance reliability with rapid innovation will capture outsized share of future Hospitality Property Management Software market growth.

Hospitality Property Management Software (PMS) Industry Leaders

Oracle Corporation

Booking Ninjas

Clock Software Ltd.

Infor Equity Holdings LLC

Stayntouch, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hotelogix surpassed 10,000 Philippine users after accelerated cloud rollouts.

- April 2025: Lighthouse acquired The Hotels Network following a USD 370 million Series C raise.

- April 2025: Duetto purchased HotStats, integrating PandL benchmarks into its revenue engine.

- March 2025: DerbySoft bought Arise to streamline travel-agency communication workflows.

Global Hospitality Property Management Software (PMS) Market Report Scope

The hospitality property management software (HPMS) market is defined based on the revenues generated from the software and services used in various property types, such as hotels and resorts, motels and lodges, homestay accommodations, service apartments, and other property types. The analysis is based on the market insights captured through secondary research and primary. The market also covers the major factors impacting the market’s growth in terms of drivers and restraints.

The hospitality property management software (PMS) market is segmented by deployment (on-premises and cloud), by property size (small and medium enterprises and large enterprises), by property type (hotels and resorts, motels and lodges, homestay accommodations, and service apartments, other property types), and geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Italy, and Rest of Europe], Asia Pacific [China, Japan, India, Australia, and Rest of Asia Pacific], Rest of the World [Latin America and Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the given segments.

| On-premise |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Hotels and Resorts |

| Motels and Lodges |

| Homestay Accommodations |

| Serviced Apartments |

| Other Property Types |

| Independent Properties |

| Chain-affiliated Properties |

| Front Desk and Operations |

| Booking and Reservations |

| Revenue Management |

| Channel Management |

| Housekeeping |

| Other Modules |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment | On-premise | ||

| Cloud | |||

| By Property Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Property Type | Hotels and Resorts | ||

| Motels and Lodges | |||

| Homestay Accommodations | |||

| Serviced Apartments | |||

| Other Property Types | |||

| By Ownership Model | Independent Properties | ||

| Chain-affiliated Properties | |||

| By Functionality Module | Front Desk and Operations | ||

| Booking and Reservations | |||

| Revenue Management | |||

| Channel Management | |||

| Housekeeping | |||

| Other Modules | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Hospitality Property Management Software market by 2031?

The market is expected to reach USD 2.44 billion by 2031, expanding at a 7.05% CAGR over 2026-2031.

Which deployment model is growing fastest in Hospitality Property Management Software?

Cloud deployment is advancing at a 12.38% CAGR as hotels prioritize scalability and lower IT overhead.

Why are small and medium hotels adopting Hospitality Property Management Software rapidly?

Subscription pricing, quick onboarding, and AI revenue tools help SMEs boost revenue while reducing operational complexity.

How is artificial intelligence used in Hospitality PMS platforms?

AI modules automate dynamic pricing, forecast demand, and recommend upsell offers, lifting room revenue by up to 10%.

Which region offers the highest growth opportunity for PMS vendors?

Asia-Pacific is registering a 12.18% CAGR due to rapid hotel construction and leapfrog cloud adoption.

Page last updated on: