Venezuela Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.12 Billion |

| Market Size (2030) | USD 1.29 Billion |

| Growth Rate (2025 - 2030) | 2.91% CAGR |

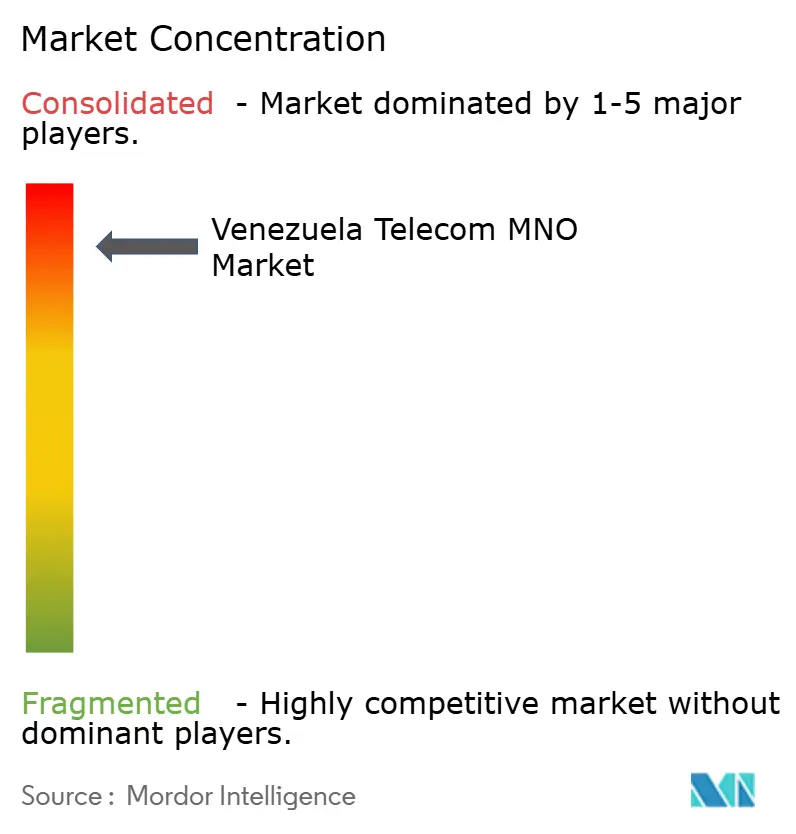

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Venezuela Telecom MNO Market Analysis by Mordor Intelligence

The Venezuela Telecom MNO Market size is estimated at USD 1.12 billion in 2025, and is expected to reach USD 1.29 billion by 2030, at a CAGR of 2.91% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 15.90 million subscribers in 2025 to 18.48 million subscribers by 2030, at a CAGR of 3.05% during the forecast period (2025-2030). The growth outlook hinges on the combined effects of dollarization-led average revenue per user (ARPU) stabilization, accelerating fiber deployment, and early 5G monetization, although persistent macroeconomic and security headwinds temper the expansion trajectory. Data and Internet demand, surging IoT uptake among industrial customers, and remittance-funded broadband upgrades create revenue headroom that partially offsets capex pressure caused by inflation and sanctions. Competitive intensity remains limited to three nationwide operators, allowing for disciplined pricing strategies and measurable service quality improvements in major cities. The extensive fiber footprint now spanning 99% of municipalities underpins cost-efficient 5G backhaul, while spectrum policy that privileges deployment over fiscal maximization shortens the time-to-market for next-generation services. The primary downside risks revolve around network vandalism, unreliable power supply, and constrained vendor financing that collectively erode margins and lengthen payback periods.

Key Report Takeaways

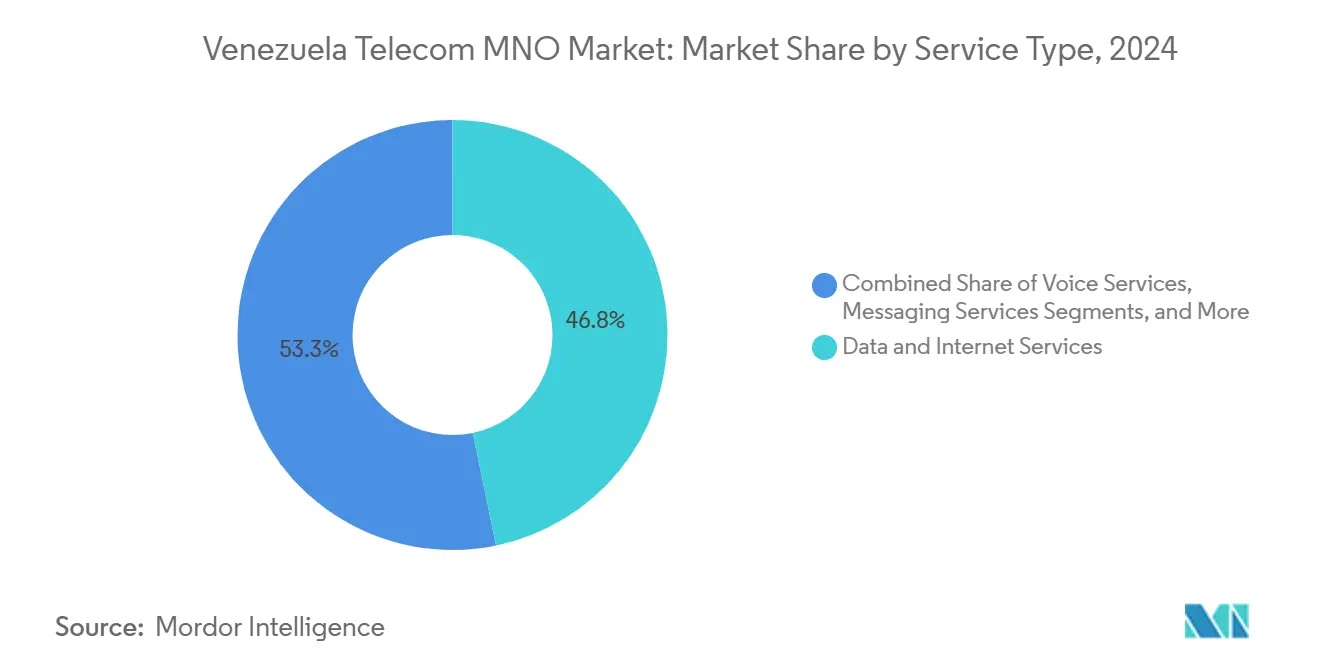

- By service type, data and internet services captured 46.75% of the Venezuelan telecom MNO market share in 2024, whereas IoT and M2M Services show the fastest momentum with a 3.15% CAGR through 2030.

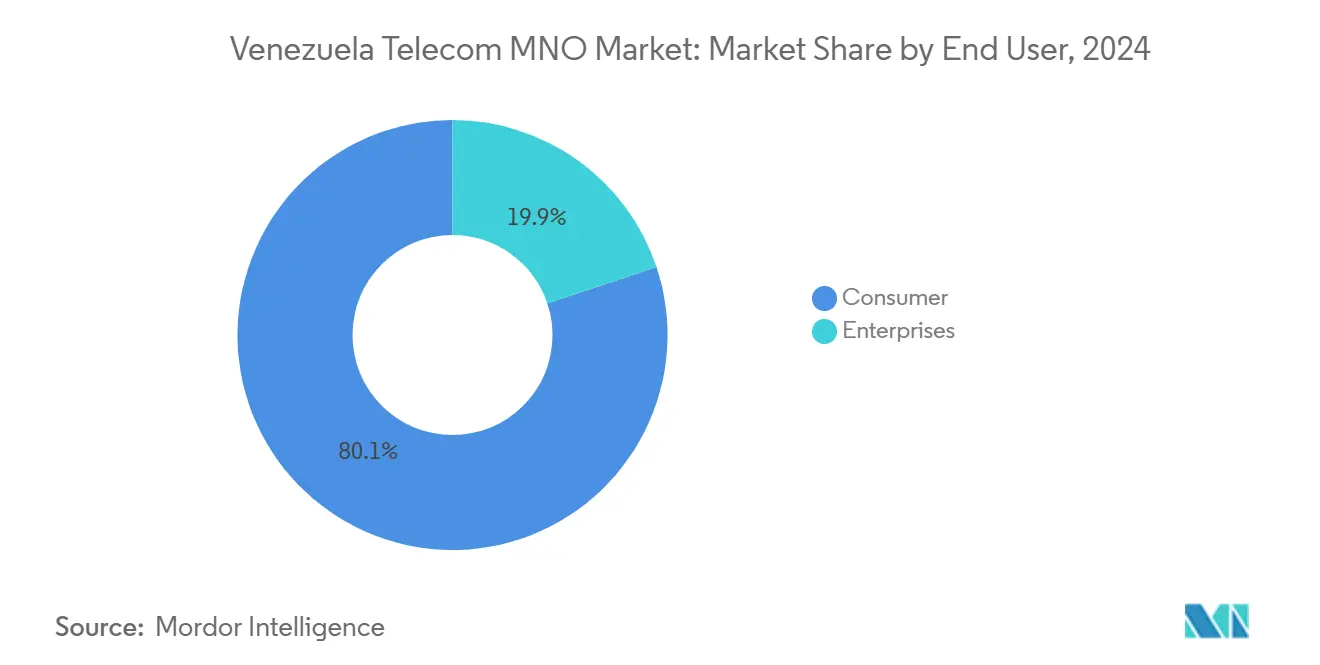

- By end user, the Consumer segment accounted for an 80.12% share of the Venezuelan telecom MNO market size in 2024, while the Enterprise segment is projected to advance at a 3.78% CAGR to 2030.

Venezuela Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dollarization-led ARPU Stabilization | +0.8% | National, with early gains in Caracas, Maracaibo, Valencia | Medium term (2-4 years) |

| Fiber-optic Footprint Expansion | +0.6% | National, prioritizing urban centers and industrial corridors | Long term (≥ 4 years) |

| Spectrum Auctions Unlocking 5G Monetization | +0.5% | National, concentrated in major metropolitan areas | Medium term (2-4 years) |

| Enterprise Digitalization Boosting IoT Demand | +0.4% | National, focused on oil, mining, and manufacturing hubs | Long term (≥ 4 years) |

| Remittance-funded Household Broadband Upgrades | +0.3% | National, particularly in diaspora-connected communities | Short term (≤ 2 years) |

| Cross-border Roaming Pacts Lowering CAPEX | +0.2% | Border regions with Colombia and Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dollarization-led ARPU Stabilization

The de facto dollarization of Venezuela’s economy has reanchored telecom pricing, reversing hyperinflation’s destructive impact on revenue integrity. Operators now quote tariffs in United States dollars, regaining pricing power and enabling multi-year investment planning free from sudden currency shocks. Movistar’s pledge to inject USD 500 million into network modernization highlights renewed confidence in predictable returns. Dollar-denominated vendor contracts improve cost visibility, while stabilized ARPU trajectories signal progressive value recapture after years of forced price caps. As purchasing power gradually realigns with digital consumption patterns, operators anticipate sustained month-over-month revenue accretion, provided political and economic reforms stay on track.

Fiber-optic Footprint Expansion

A nationwide fiber backbone now reaches 99% of municipalities, defying broader economic adversity and giving Venezuela an atypically dense fixed infrastructure relative to Latin American peers. This connectivity bedrock slashes 5G backhaul costs, facilitates competitive fixed-wireless access, and supports enterprise data services. SimpleTV’s entry into fiber-to-the-home illustrates how the expanded backbone lures non-traditional players into broadband. [1]Hernán Amaya, “Venezuela: SimpleTV Launches Fiber Optic Fixed Internet Service,” TAVI, tavilatam.com Operators are complementing aerial lines with underground routes and community security programs to curb rampant cable theft. Once vandalism risks abate, the extensive fiber grid can elevate service quality across consumer and business segments.

Spectrum Auctions Unlocking 5G Monetization

Regulators prioritized swift deployment over fiscal gains by releasing mid-band spectrum at prices conducive to operator participation. Telefónica secured 2,600 MHz frequencies enabling dynamic spectrum sharing across 805 planned nodes, while Digitel activated the country’s first 5G fixed-wireless product that delivers up to 400 Mbps in early markets. [2]Ignacio del Castillo, “Telefónica Logra Espectro y Anuncia la Inversión de 487 Millones en Venezuela,” Expansión, expansion.com Seven additional assignments in 2024 signal a multi-operator framework likely to heighten competition. Early rollouts focus on bridging broadband gaps rather than mobile premium tiers, expediting uptake among underserved households and small businesses.

Enterprise Digitalization Boosting IoT Demand

Industrial firms seek sensor-based asset monitoring and predictive maintenance to cushion operational volatility. Oil, mining, and manufacturing installations increasingly embed IoT modules that require low-latency, high-reliability links, allowing operators to upsell managed connectivity bundles. Telefónica’s regional IoT portfolio recorded 40% revenue growth, underscoring enterprise appetite for turnkey platforms. Diaspora-financed manufacturing upgrades and trans-border supply chains add to demand, positioning IoT as a sticky, high-margin revenue stream relative to legacy voice.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-inflation Curbing CAPEX | -0.7% | National, particularly affecting rural and peripheral areas | Medium term (2-4 years) |

| Aging Power Infrastructure Causing Outages | -0.5% | National, concentrated in industrial zones and rural areas | Long term (≥ 4 years) |

| Theft of Copper/Fiber and Fuel | -0.4% | National, highest impact in remote and border regions | Short term (≤ 2 years) |

| US Sanctions Restricting Vendor Financing | -0.3% | National, affecting all major infrastructure projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Theft of Copper/Fiber and Fuel

Organized vandalism has become the foremost operational headache, with more than 2,000 antenna attacks recorded in three years. Movistar alone lost 536 sites to theft in one year, compelling operators to redesign networks using underground conduits and reinforced shelters that inflate deployment budgets. Fuel siphoning undermines backup-generator reliability during power cuts, amplifying service downtime. Though community patrols and police alliances offer partial relief, the security threat still diverts capital from expansion toward asset protection.

Aging Power Infrastructure Causing Outages

Chronic electricity shortages force carriers to maintain extensive diesel generator fleets, elevating operating expenses and environmental risks. Grid instability often knocks out data centers and radio access nodes simultaneously, triggering cascading service failures that erode customer trust. [3]Yevgeniy Sverdlik, “Hard-Knock Life Gets Harder in Venezuela With Internet Near Bust,” Data Center Knowledge, datacenterknowledge.com Fuel scarcity exacerbates downtime, especially outside Caracas where refueling logistics are cumbersome. Operators therefore favor energy-efficient radio kit, distributed architectures, and renewable micro-grids, though these upgrades prolong payback horizons in a low-ARPU setting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Market Evolution

Data and Internet Services held the largest revenue slice at 46.75% in 2024, validating operators’ pivot toward digital-centric propositions that bundle generous data volumes with OTT content add-ons. Streaming and social media usage doubled average monthly traffic to 3.9 GB per user, compelling carriers to repurpose spectrum from 2G voice to LTE and 5G capacity. The growth of IoT and M2M at a 3.15% CAGR positions the niche as the fastest-expanding component of the Venezuelan telecom MNO market.

Voice Services, while declining in absolute minutes, retain utility in rural communities where smartphone penetration lags. Operators deploy VoLTE to free up bandwidth and enhance call quality, mirroring 18 Latin American peer networks that migrated to IP voice. Messaging revenue continues to shrink as WhatsApp and Telegram dominate, spurring carriers to trial rich-communication services. OTT video and PayTV bundles leverage the broad fiber network to tap into incremental household spending, whereas roaming and enterprise value-added services benefit from price stabilization, enabling premium tiers that were not viable under hyperinflation.

By End User: Consumer Dominance with Enterprise Upside

The consumer market commands an 80.12% revenue share, sustained by the affordability of prepaid services and the indispensability of mobile connectivity for remittance reception and digital payments. Despite economic adversity, households prioritize airtime purchases, often allocating remittance inflows to data top-ups. Operators structure tiered prepaid offers that monetize high-usage social media packages without overexposing budgets to inflation.

The Enterprise segment, although smaller, outpaces overall growth at a 3.78% CAGR, driven by industrial IoT mandates, supply chain digitalization, and cloud adoption in oil and manufacturing clusters. Bundled secure connectivity suites, fixed-wireless access, and managed IoT platforms allow carriers to diversify beyond price-sensitive consumer prepaid lines. Government agencies, though cash-strapped, still procure nationwide connectivity for critical services, adding a modest but stable revenue layer.

Geography Analysis

Caracas and the central industrial corridor enjoy the densest cell site coverage and the country’s highest median download speeds, benefitting from concentrated investment and comparatively resilient power infrastructure. Zulia state, anchored by Maracaibo, leverages cross-border trade with Colombia to sustain premium data uptake and robust network performance. Nueva Esparta, a tourism hub, posts 18.97 Mbps median mobile speeds and served as Digitel’s pilot 5G fixed-wireless market, underlining its strategic value for high-end service launches.

Border municipalities exhibit unique roaming traffic patterns that justify infrastructure pooling and bilateral spectrum-use agreements, though elevated theft risk complicates large-scale rollouts. Rural regions, despite physical fiber presence, still lag in service quality because unstable power and limited back-haul redundancy dilute throughput.

Satellite partnerships and experimental 5G trials with Chinese vendors demonstrate the regulator’s intention to narrow the urban-rural digital divide. As remittances lift disposable income outside Caracas, operators are reassessing expansion economics in secondary towns where latent demand aligns with modest capex outlays supported by the existing fiber grid.

Competitive Landscape

Venezuela telecom MNO market functions as a three-player oligopoly, granting Movistar, Digitel, and state-owned Movilnet collective pricing leverage yet exposing them to similar macro and security risks. Subscriber bases compressed by 10 million lines between 2013 and 2018, prompting a strategic pivot from volume growth to ARPU optimization and customer-experience differentiation.

Movistar’s USD 500 million modernization campaign spans 805 multiservice nodes and integrates dynamic spectrum sharing for expedited 5G coverage. Digitel leads early 5G execution through a USD 50 million plan to scale fixed-wireless stations from 2,400 to 5,000 by 2026. Movilnet struggles with budget limitations that hamper nationwide LTE upgrades, leaving quality gaps exploitable by rivals.

All operators intensify site-sharing agreements and jointly fund security patrols to mitigate vandalism, reflecting a shift toward cooperative cost containment over aggressive market-share grabs. Enterprise IoT services and cross-border data offerings represent the most contested white spaces, where early mover advantage could yield defensible revenue streams amid otherwise sluggish overall growth.

Venezuela Telecom MNO Industry Leaders

Movistar (Telefónica Venezuela)

Digitel

Movilnet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Digitel launched Venezuela’s first 5G Fixed Wireless Internet service, offering speeds up to 400 Mbps in Barinas and Nueva Esparta and outlining a USD 50 million expansion to 5,000 stations by 2026.

- April 2025: Movistar Venezuela suffered a data breach affecting 3.2 million users, triggering industry-wide security protocol upgrades.

- February 2025: Movistar committed USD 500 million over two years after obtaining 2,600 MHz spectrum, planning 805 nodes to enable nationwide 5G via dynamic spectrum sharing.

Venezuela Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Venezuela telecom MNO market in 2025?

The Venezuela telecom MNO market size is USD 1.12 billion in 2025 and is projected to reach USD 1.29 billion by 2030.

What is the forecast CAGR for Venezuelan mobile network revenue?

Market revenue is anticipated to grow at a 2.91% CAGR between 2025 and 2030.

Which service type currently generates the most revenue?

Data and Internet Services contribute the largest share at 46.75% of 2024 revenue.

Which segment is expanding the fastest?

IoT and M2M Services lead growth with a 3.15% CAGR forecast to 2030.

Why has ARPU begun to recover?

Dollarization allows operators to price plans in stable currency, restoring purchasing power and revenue predictability.

What are the main barriers to network reliability?

Widespread theft of network assets and chronic power outages are the principal operational constraints.

Page last updated on: