Japan IT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

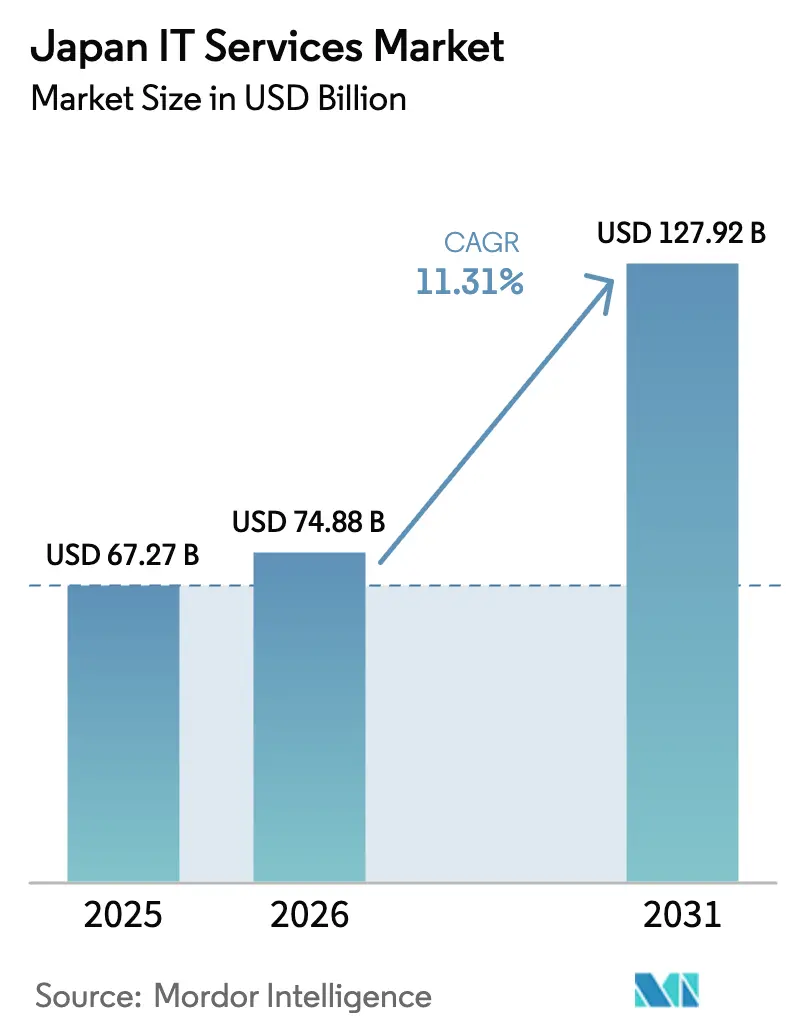

| Base Year Market Size (2025) | USD 67.27 Billion |

| Market Size (2026) | USD 74.88 Billion |

| Market Size (2031) | USD 127.92 Billion |

| Growth Rate (2026 - 2031) | 11.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan IT Services Market Analysis by Mordor Intelligence

The Japan IT Services market size was valued at USD 67.27 billion in 2025 and estimated to grow from USD 74.88 billion in 2026 to reach USD 127.92 billion by 2031, at a CAGR of 11.31% during the forecast period (2026-2031). Surging demand for core-system renewals ahead of the “2025 Digital Cliff,” strong government backing for Society 5.0 initiatives, and cloud-first procurement rules for public agencies are sustaining double-digit expansion. Large enterprises are renewing mainframes, while small and medium enterprises (SMEs) are capitalizing on tax credits that subsidize up to 75% of software costs. Hyperscale datacenter buildouts and edge-computing rollouts are broadening the service mix toward platform and managed security offerings, and currency-driven cost pressures are accelerating offshore delivery adoption. Intensifying competition among traditional system integrators, cloud hyperscalers, and specialized cybersecurity vendors is reshaping pricing, margins, and consolidation strategies.[1]Digital Agency, “Japan's Digital Transformation Strategy,” DIGITAL.GO.JP

Key Report Takeaways

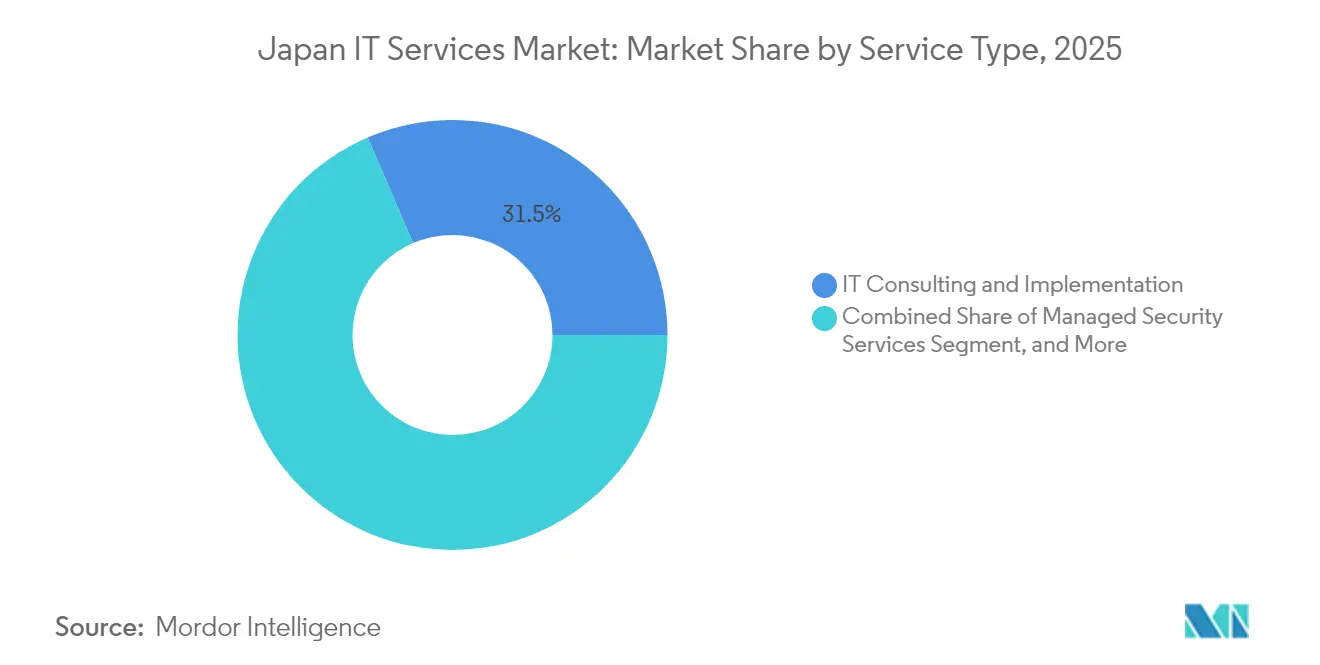

- By service type, IT consulting and implementation led with 31.45% revenue share in 2025, while cloud and platform services are projected to record a 15.73% CAGR to 2031.

- By enterprise size, large enterprises held 67.25% of the Japan IT Services market share in 2025, while SMEs are expected to expand at a 12.98% CAGR through 2031.

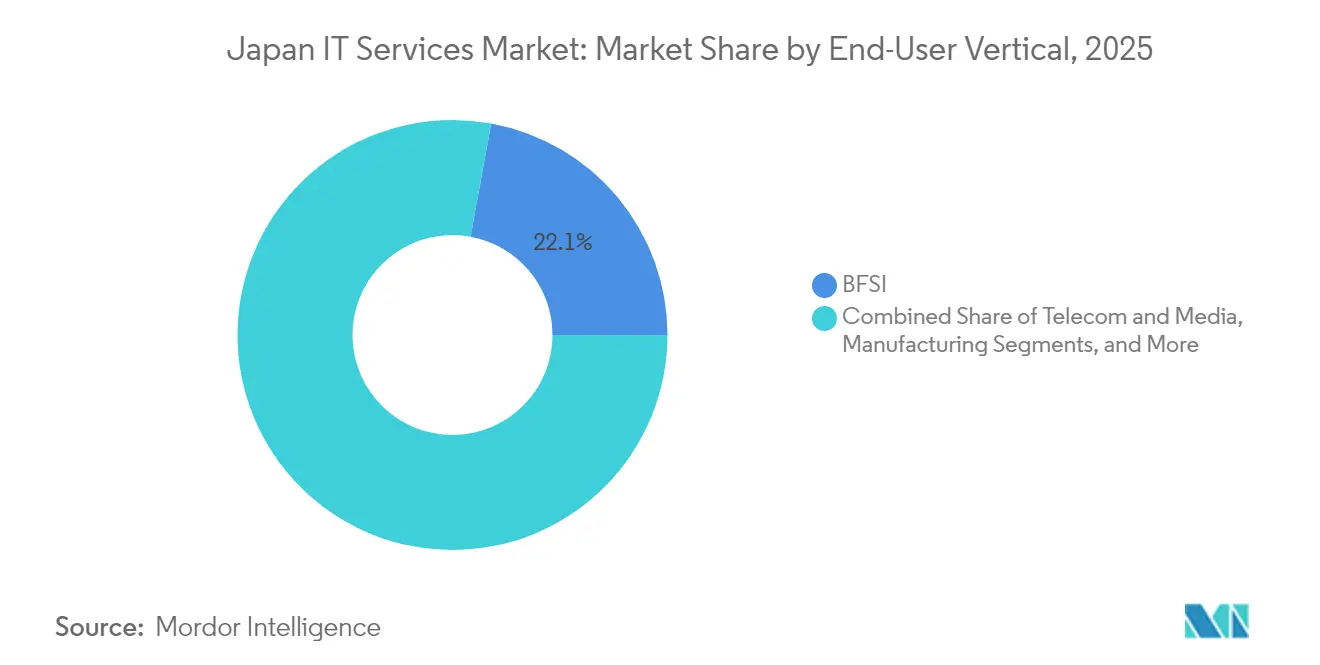

- By end-user vertical, BFSI captured 22.12% share of the Japan IT Services market size in 2025, whereas healthcare and life sciences are advancing at a 15.12% CAGR.

- By deployment model, onshore delivery maintained 64.35% share in 2025, but offshore delivery is projected to grow at a 15.95% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DX acceleration under Society 5.0 vision | +2.80% | National, with concentration in Tokyo-Osaka corridor | Long term (≥ 4 years) |

| Cloud-first procurement by central and municipal agencies | +2.10% | National, with early adoption in major metropolitan areas | Medium term (2-4 years) |

| SME tax incentives for SaaS adoption (2024-2027) | +1.70% | National, with higher uptake in manufacturing regions | Short term (≤ 2 years) |

| Surge in hyperscale and edge-DC build-outs | +1.90% | Concentrated in Kanto, Kansai, and Kyushu regions | Medium term (2-4 years) |

| Managed security demand amid cyber-insurance premium hikes | +1.40% | National, with priority in BFSI and critical infrastructure | Short term (≤ 2 years) |

| Under-reported: "2025-Cliff" legacy risk forcing core-system renewal | +2.60% | National, with highest impact in BFSI and manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

DX Acceleration Under Society 5.0 Vision

Japan’s Society 5.0 roadmap shifts enterprises from pilot-level automation to full-scale digitalization, creating large, multi-year transformation programs. Manufacturers such as Toyota linked 30,000 data points across 370 machines to streamline predictive maintenance, multiplying demand for systems integration services and edge analytics platforms.[2]IIJ Corporation, “Toyota Motor Hokkaido IoT Implementation,” IIJ.AD.JP Service contracts are increasingly outcome-based, and consulting partners must deliver productivity gains without displacing labour, aligning with human-centric policy goals.

Cloud-First Procurement by Central and Municipal Agencies

The Digital Agency mandates that all new public-sector workloads adopt a cloud-first stance, removing on-premises default biases. Early movers have cut document handling times by 60%, proving the fiscal benefits of platform-as-a-service models.[3]Ministry of Internal Affairs and Communications, “Digital Transformation Case Studies,” SOUMU.GO.JP Multi-cloud rules lower vendor lock-in risk, boosting demand for orchestration and FinOps services and allowing mid-tier integrators to bid for government workloads previously gated by legacy procurement norms.

SME Tax Incentives for SaaS Adoption (2024-2027)

The IT Subsidy Program 2025 covers up to three-quarters of eligible software spend, prompting fast follower behaviour in a segment historically slow to digitize. Subsidized firms show 40% higher productivity versus non-participants. Providers are productizing fixed-price bundles that satisfy subsidy guidelines, adding embedded cybersecurity modules to comply with program mandates.

2025-Cliff” Legacy Risk Forcing Core-System Renewal

METI warns that postponing modernization beyond 2025 could impose JPY 12 trillion in annual economic losses, galvanizing banks and manufacturers to replace COBOL cores. Resona Group cut terminal counts by 50% and trimmed IT spend by 25% via low-code re-platforming. Scarce COBOL-to-modern skills are priced at premiums, favouring incumbents with rostered legacy specialists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural shortage of 800k IT engineers by 2030 | -2.30% | National, with acute shortages in Tokyo and Osaka | Long term (≥ 4 years) |

| JPY weakness inflating imported IaaS costs | -1.80% | National, with higher impact on cloud-dependent services | Medium term (2-4 years) |

| On-prem lock-in within keiretsu supply chains | -1.20% | Concentrated in traditional manufacturing regions | Long term (≥ 4 years) |

| Under-reported: rising green-datacentre power curbs in Kanto | -0.90% | Kanto region, with spillover effects to neighboring prefectures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Structural Shortage of 800k IT Engineers by 2030

An aging workforce and limited STEM graduates produce a widening talent gap, raising salary costs and elongating project lead times. Large providers are scaling offshore centers in India and Vietnam, achieving up to 40% cost relief and reallocating scarce domestic engineers to client-facing roles.

JPY Weakness Inflating Imported IaaS Costs

US-dollar-denominated IaaS pricing climbed in yen terms, pressuring profit margins for cloud service intermediaries. Domestic carriers with JPY-priced clouds gain temporary advantage, but capability gaps sustain a multi-cloud approach that keeps foreign hyperscale demand intact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Consulting Dominates, Cloud Platforms Surge

IT consulting and implementation secured 31.45% of the Japan IT Services market share in 2025, reflecting enterprises’ need for strategic road-mapping ahead of major legacy sunsets. Japan IT Services market size for cloud and platform services is projected to expand at a 15.73% CAGR as hyperscale data centers multiply and government workloads shift to multi-cloud frameworks. Contract structures are pivoting from labour-based billing to value-based models that embed service-level outcomes, boosting average deal sizes. Aggressive transformation agendas at Fujitsu and NEC illustrate how incumbents’ re-skill toward advisory and platform integration.

Standardization of cloud environments compresses margins in traditional IT outsourcing, but fuels cybersecurity and FinOps add-ons. Managed security services grow above 12% annually as cyber-insurance premiums spike and regulators mandate threat-monitoring baselines for critical infrastructure. Service providers packaging consulting, migration, and run operations into single contracts gain wallet share through lifecycle ownership.

By Enterprise Size: Large Budgets Rule, SMEs Accelerate Under Incentives

Large organizations accounted for 67.25% of 2025 spending and drive complex, multi-year renewal projects focused on AI, analytics, and mainframe re-platforming. SMEs, energized by the IT Subsidy Program, post a 12.98% CAGR, unlocking pent-up demand for cloud ERP, HR, and security suites. Japan IT Services market size for SME projects is still comparatively small, yet the subsidy compresses adoption cycles and makes standardized delivery economical for vendors.

Providers targeting SMEs build productized, fixed-scope offerings that simplify procurement. Those reliant on subsidy leads face potential revenue cliffs after 2027 unless they transition clients to self-funded renewals. Large enterprises, meanwhile, deepen partnerships with a select roster of global and domestic integrators, driving vendor consolidation and longer contract tenures.

By End-User Vertical: BFSI Leads, Healthcare Accelerates

BFSI preserved its leadership with 22.12% share of the Japan IT Services market size in 2025 as banks raced to overhaul core banking stacks and comply with Financial Services Agency guidelines. Healthcare and life sciences, energized by digital therapeutics approvals and electronic medical records mandates, register the fastest 15.12% CAGR, opening a multi-billion-dollar opportunity for clinical data interoperability, tele-health, and cybersecurity services.

Manufacturing maintains robust demand for factory IoT and predictive maintenance, while public-sector spending concentrates on e-government portals that align with Society 5.0. Retail and logistics implement computer-vision and robotics solutions to offset labour shortages. Energy utilities invest in smart-grid analytics, leveraging AI to balance intermittent renewable inputs.

By Deployment Model: Onshore Preferred, Offshore Gains Momentum

Onshore engagements dominated at 64.35% in 2025, reflecting cultural affinity and stringent data-sovereignty requirements. Offshoring grows at 15.95% CAGR as yen weakness boosts relative cost advantages of Indian and Southeast Asian centers. Hybrid models blend local program management with remote development, enabling cost reductions without compromising compliance. Japan IT Services market share for near-shore hubs in Malaysia and the Philippines is rising, aided by similar time zones and language programs supported by the Japan Foundation.

Regulated industries such as BFSI and healthcare keep critical workloads domestic, yet pilot agile pods offshore non-sensitive modules to alleviate talent shortages. Providers mastering cross-border DevSecOps processes differentiate through secure coding and data-masking frameworks that satisfy Japan’s Personal Information Protection Act.

Geography Analysis

Tokyo and the wider Kanto region accounted for roughly 59.40% of 2025 spending, propelled by the headquarters of banks, insurers, and government agencies. Osaka and the Kansai corridor contribute high-single-digit growth as manufacturers integrate cyber-physical systems and elevate cloud adoption. Kyushu emerges as a semiconductor and datacenter hotspot, drawing hyperscale investments that stimulate local consulting and infrastructure contracts. Hokkaido and Tohoku show rising adoption of smart-agriculture and renewable energy management tools under regional revitalization funds.

Power constraints in Kanto limit new datacenter footprints, pushing edge computing to secondary prefectures and spurring demand for orchestration services. Urban migration keeps IT talent clusters in metro areas, yet remote-work norms enable regional providers to serve national clients. Government grants targeting the digital divide encourage service providers to pilot low-touch deployment templates adaptable to rural municipalities.

Regulatory heterogeneity affects public-cloud usage, particularly in healthcare where prefectural authorities govern sensitive data hosting. Providers offering standardized compliance accelerators gain share. Cross-border data flow policies linked to Free and Open Indo-Pacific initiatives position Japan as a potential regional data hub, contingent on power-grid upgrades and green-energy sourcing to meet ESG commitments.

Competitive Landscape

The top five vendors command roughly 35% of the Japan IT Services market, indicating moderate concentration. NTT DATA, NEC, and Fujitsu leverage entrenched client relationships and nationwide support networks, while Accenture and IBM apply global delivery frameworks and deep vertical know-how. Hyperscalers such as AWS and Microsoft increase direct enterprise footprints via co-selling programs with telecom operators. Specialized cybersecurity players like Netskope and Trend Micro carve out fast-growing niches by automating threat intelligence and zero-trust architectures.

Consolidation accelerates NTT’s USD 16.3 billion buy-out of NTT DATA unifies telecom and IT services assets, while KKR’s bid for Fuji Soft signals private-equity appetite for platform plays. Providers shift from body-shopping to platform-centric models, embedding IP in repeatable automation assets. Patent races in AI operationalization, sovereign cloud tooling, and quantum-resistant encryption highlight future battlegrounds.

Edge-computing orchestration, AI model operations (MLOps), and multi-cloud FinOps represent white spaces where nimble entrants can out-innovate incumbents. Talent scarcity elevates employee value propositions and propels wage inflation, spurring investment in low-code platforms that democratize development. Vendors emphasizing sustainability accreditations win datacenter contracts as clients pursue Scope 3 emission reductions.[4]NTT DATA Corporation, “Market Position and Strategy 2024,” NTTDATA.COM

Japan IT Services Industry Leaders

NTT DATA Group Corporation

NEC Corporation

Fujitsu Limited

Hitachi Ltd. (Digital Services BU)

IBM Japan Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: NTT Corporation finalized its USD 16.3 billion acquisition of NTT DATA Group, creating Japan’s largest integrated tech-services provider and aligning telecom infrastructure with digital consulting and cloud delivery.

- December 2024: KKR launched a USD 4.1 billion tender for Fuji Soft, the largest private-equity deal in Japan’s IT services segment, providing growth capital for AI and cloud expansion.

- November 2024: ITOCHU partnered with Technologent to enhance North American infrastructure services reach, granting Technologent an entry point to Japan.

- October 2024: SoftBank and NEC teamed on biometric authentication services for smart-city rollouts, merging telecom reach with facial-recognition IP.

Japan IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| Onshore Delivery |

| Near-shore Delivery |

| Offshore Delivery |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Deployment Model | Onshore Delivery |

| Near-shore Delivery | |

| Offshore Delivery |

Key Questions Answered in the Report

What is the current value of Japan's IT services sector and its expected size by 2031?

Spending reached USD 74.88 billion in 2026 and is forecast to grow to USD 127.92 billion by 2031 at an 11.31% CAGR.

Which service category is expanding fastest in Japan?

Cloud and platform services post the highest 15.73% CAGR through 2031 as public cloud mandates and hyperscale datacenters multiply.

How large is the talent shortfall facing providers?

METI projects a shortage of 800,000 IT engineers by 2030, pushing firms to offshore development and invest in automation.

Why are SMEs accelerating technology adoption?

The IT Subsidy Program reimburses up to 75% of qualifying software costs through 2027, pushing SME spending to a 12.98% CAGR.

Which customer vertical is showing the fastest spending growth?

Healthcare and life sciences lead with a 15.12% CAGR, driven by electronic medical record roll-outs and digital therapeutics approvals.

How concentrated is the competitive landscape?

The top five vendors control roughly 35% of total spend, indicating room for specialists and emerging players to gain share.

Page last updated on: