Malaysia Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

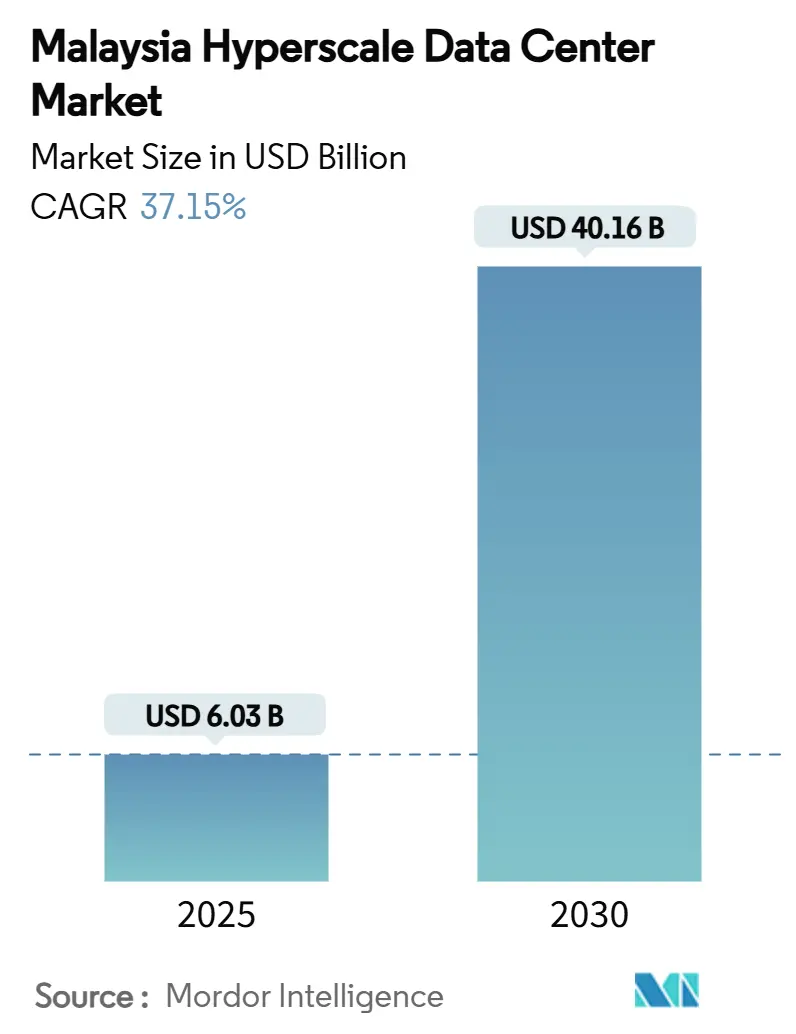

| Market Size (2025) | USD 6.03 Billion |

| Market Size (2030) | USD 40.16 Billion |

| Growth Rate (2025 - 2030) | 37.15% CAGR |

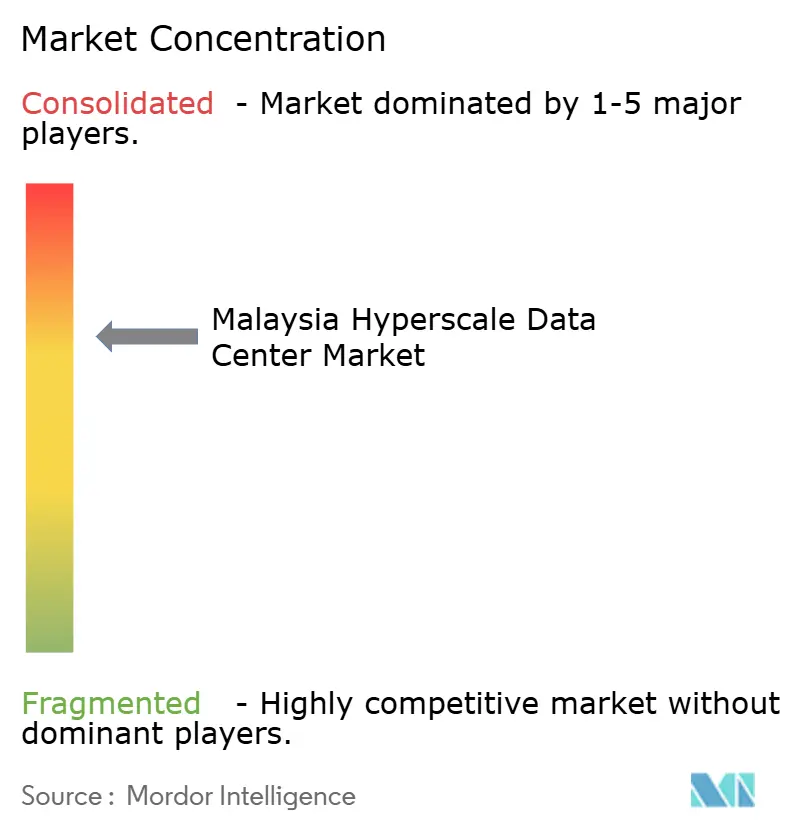

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Hyperscale Data Center Market Analysis by Mordor Intelligence

The Malaysia hyperscale data center market size is valued at USD 6.03 Billion in 2025 and is forecast to reach USD 40.16 Billion by 2031, expanding at a 37.15% CAGR. Ongoing hyperscaler capital-expenditure announcements, government tax incentives and a rapid shift toward AI-ready facilities are accelerating deployments, while connectivity improvements and abundant green-power prospects amplify investor appetite. Self-build campuses still dominate capacity but high-density, multi-tenant colocation is growing faster, propelled by smaller cloud platforms seeking quick, capital-light entry. Mechanical infrastructure—especially liquid and immersion cooling—outpaces all other component spends as operators retrofit for GPU clusters. Regionally, Johor’s proximity to Singapore and lower land costs spur the fastest expansion, though the Klang Valley retains critical mass for talent and network density.

Key Report Takeaways

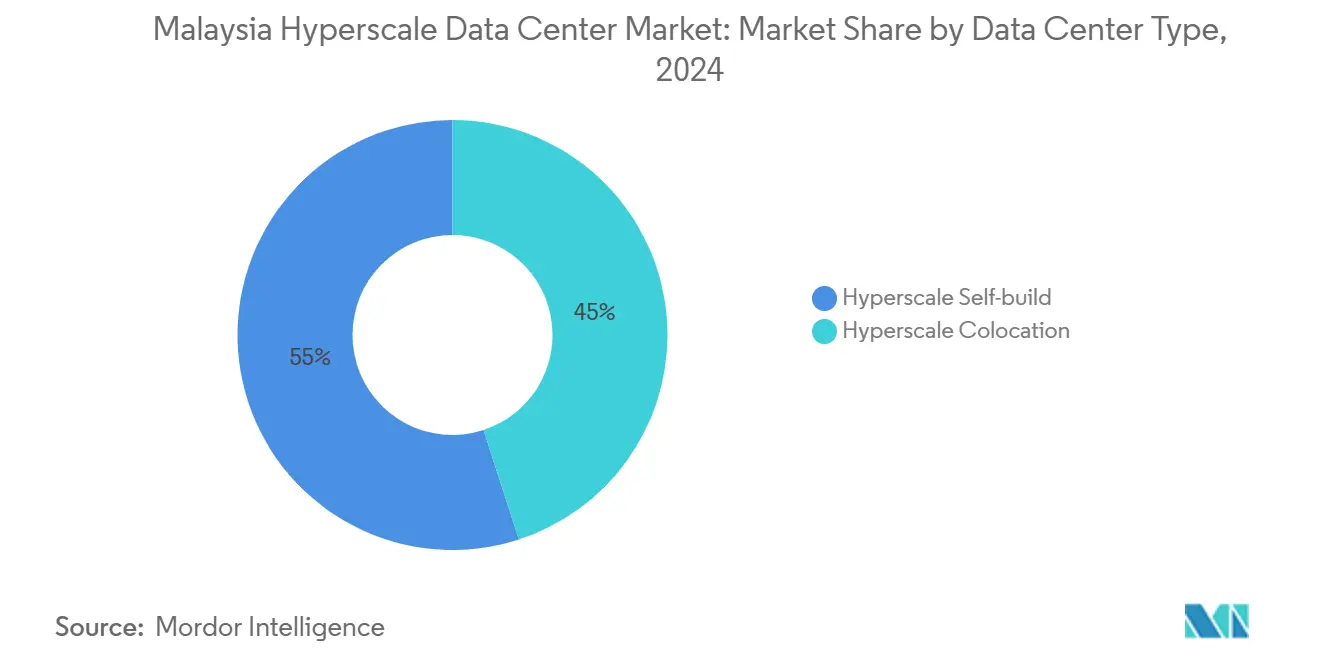

- By data center type, hyperscaler self-build facilities held 55% of the Malaysia hyperscale data center market share in 2024; hyperscale colocation is advancing at a 38.4% CAGR to 2030.

- By component, IT infrastructure accounted for 40% of the Malaysia hyperscale data center market size in 2024, and mechanical infrastructure is projected to rise at a 38.1% CAGR through 2030.

- By tier standard, Tier III deployments commanded 73% share of the Malaysia hyperscale data center market size in 2024, while Tier IV facilities are expanding at a 37.5% CAGR between 2025-2030.

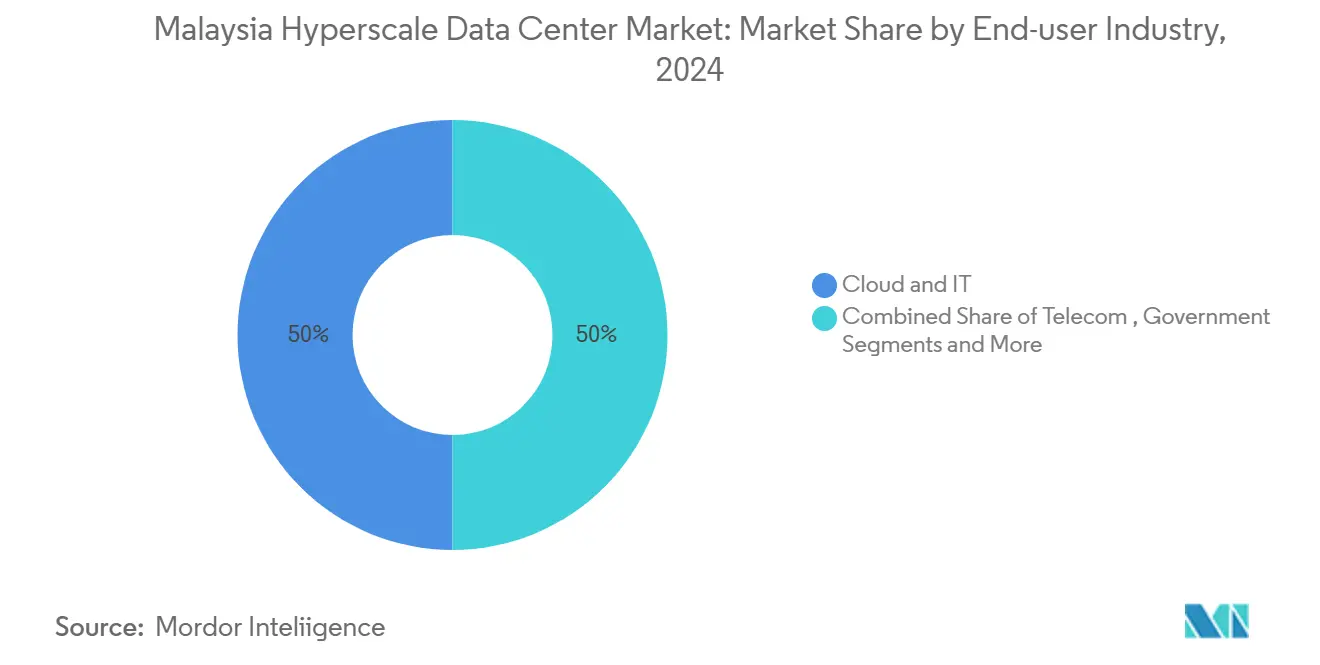

- By end-user industry, cloud and IT services represented 50% of the Malaysia hyperscale data center market size in 2024, and media and entertainment is forecast to grow at a 38.3% CAGR through 2030.

- By data center size, massive facilities captured 45% of capacity in 2024 and mega-scale campuses are growing at a 39.0% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

No country-level or regional dataset alone defines global value; it is assembled from all contributing countries and geographies, including Malaysia. Our global hyperscale data center market size reflects this full aggregation.

Malaysia Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscaler CAPEX announcements | +12.5% | National, Klang Valley and Johor | Medium term (2-4 years) |

| Rapid adoption of e-commerce and digital banking | +8.2% | Urban centres; spill-over to secondary cities | Short term (≤ 2 years) |

| Government incentives under MyDIGITAL and Green Lane | +6.8% | National; early gains in Cyberjaya and Johor Bahru | Medium term (2-4 years) |

| New international subsea cable landings | +4.1% | Coastal regions, Johor and Penang | Long term (≥ 4 years) |

| Green Electricity Tariff enabling 24×7 PPAs | +3.2% | National; strongest in Sarawak and Sabah | Long term (≥ 4 years) |

| Hydropower surplus in Sarawak and Sabah | +2.2% | East Malaysia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Hyperscaler CAPEX Announcements Drives Market Expansion

An unprecedented USD 14.7 billion pipeline from Google, AWS, Oracle and Microsoft has repositioned the Malaysia hyperscale data center market as a top-tier regional hub within 18 months.[1] Google Cloud Press Corner, “Advancing Malaysia Together: Google Announces US$2 Billion Investment in Malaysia,” googlecloudpresscorner.com These investments dwarf Singapore’s decade-long tally, sparking parallel spending on power distribution, liquid-cooling systems and inter-campus fiber rings. Competitive dynamics among the “big four” are elevating design standards, prompting 300 MW-plus campuses built for AI training clusters. Secondary suppliers—from switchgear to chilled-water modules—have accelerated footprint expansions inside Malaysia, reinforcing a virtuous supply-chain cycle for the sector.

E-commerce and Digital Banking Transformation Accelerates Cloud Adoption

Digital-economy output will exceed 25% of national GDP in 2025, propelled by e-commerce peaks and newly licensed digital banks that demand sub-10 ms latency. Shopping festivals 11.11 and 12.12 push transaction volumes that only hyperscale facilities can absorb, while TikTok Shop’s regional surge underscores the importance of AI-driven content moderation nodes. Digital-bank applicants such as GXBank cite Tier IV mandates for uninterrupted ledger processing.[3]Ministry of Investment, Trade and Industry, “Digital Economy in Malaysia,” miti.gov.my Although 5G monetisation trails expectations, forthcoming edge-zones tied to national stand-alone 5G roll-outs will lift utilisation rates across distributed clusters.

Government Policy Framework Provides Competitive Advantages

The MyDIGITAL blueprint, Malaysia Digital (MD) Status incentives and a streamlined Digital Investment Office slash approval windows by months, cutting time-to-market compared with regional peers.[2] Ministry of Investment, Trade and Industry, “Digital Economy in Malaysia,” miti.gov.my Corporate tax allowances and investment tax credits enhance internal-rate-of-return calculations for new builds, while October 2024’s National Cloud Policy offers clarity on data sovereignty and cybersecurity requirements. The Corporate Renewable Energy Supply Scheme launched in 2024 permits direct green-power procurement, aligning projects with corporate decarbonisation pledges.

International Subsea Cable Infrastructure Enhances Connectivity

Cable projects such as SEA-ME-WE 6 and the USD 300 million MIST system diversify routes and trim latency to critical APAC hubs. Malaysia’s waiver on cabotage for repair vessels curbs downtime risks and maintenance costs. Greater route diversity also reduces reliance on Singapore as a transit node, permitting direct interconnects to regional cloud availability zones and boosting the Malaysia hyperscale data center market’s attractiveness to content providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited on-grid renewable energy | -4.8% | National; most acute in Peninsular Malaysia | Medium term (2-4 years) |

| High construction costs from imported MEP and land premiums | -3.2% | Urban centres, especially Klang Valley | Short term (≤ 2 years) |

| Water-stress restrictions in Selangor | -2.1% | Selangor; major conurbations | Short term (≤ 2 years) |

| Slow 5G monetisation delaying edge usage | -1.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Renewable Energy Supply Constrains Hyperscaler Expansion

Grid renewables cover just 19% of national generation, well below hyperscalers’ 100% carbon-free targets. Coal and gas still represent 81% of supply, limiting issuance of corporate PPAs despite the 2024 Green Electricity Tariff. Tenaga Nasional Berhad’s USD 10.3 billion grid-modernisation plan aims to integrate more renewables, but timelines risk lagging new AI workloads scheduled for 2026-2027. Sarawak’s hydropower surplus offers a workaround, yet transmission bottlenecks to Peninsular load centres remain unresolved.

Rising Construction and Operational Costs Challenge Profitability

Imported chillers, generators and switchgear are priced in strong foreign currencies, while prime-site land in Cyberjaya and Johor Bahru has appreciated sharply. The July 2025 electricity-tariff reclassification moves data centers into an ultra-high-voltage band, lifting power costs by 10-15% and eroding margins. For a 100 MW campus, annual operating expenses may climb by RM63 million, compelling operators to seek long-term renewable PPAs and phase-in liquid cooling that improves power-usage effectiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Self-build Dominance Faces Colocation Challenge

Self-built campuses held 55% of the Malaysia hyperscale data center market share in 2024 as hyperscalers prioritised bespoke layouts and direct control over mechanical-electrical-plumbing systems. The Malaysia hyperscale data center market size linked to self-build projects is supported by Google’s USD 2 billion Klang Valley campus and AWS’s USD 6.2 billion tri-availability-zone commitment. Oracle’s USD 6.5 billion pledge further entrenches the model, ensuring anchor tenants for upstream power-distribution upgrades. Yet self-builds face land scarcity and lengthy grid connection lead times.

Colocation, expanding at 38.4% CAGR, offers rapid turn-up through shared power and cooling blocks. Princeton Digital Group’s 150 MW AI-ready JH1 campus in Johor illustrates how large-scale colocation can secure green financing aligned with hyperscaler sustainability clauses. Digital Edge and STT GDC leverage multi-tenant cost amortisation to deploy immersion-cooling racks at scale. Over 2025-2031, rising AI inference-zone demand and capital-budget flexibility are expected to erode the self-build share, although both models will coexist across workload tiers.

By Component: IT Infrastructure Leads While Mechanical Systems Accelerate

IT stacks—servers, storage and networking—absorbed 40% of 2024 spending as GPU-dense nodes and 400G/800G switches powered AI and high-frequency analytics. The Malaysia hyperscale data center market benefits from persistent-memory adoption that reduces read-latency for e-commerce peak loads. Electrical systems, the next largest cost block, increasingly employ modular, containerised UPS strings to shorten build times.

Mechanical infrastructure rises fastest at 38.1% CAGR because liquid-cooling and single-phase immersion solutions are essential for racks surpassing 70 kW. Operators trial direct-to-chip cold-plate loops that lower facility PUE by up to 0.15 points. Sustainable Metal Cloud demonstrates 50% energy savings in comparative trials, nudging peers toward similar designs. As mechanical capex rises, service-life extension strategies—such as refrigerant-free adiabatic systems for Sarawak’s hydropower-backed campuses—gain traction.

By Tier Standard: Tier III Dominance Challenged by Tier IV Growth

Tier III sites remain 73% of installed capacity, balancing cost and 99.982% availability. Enterprises migrating SAP HANA or low-latency SaaS workloads accept Tier III redundancy, and most content-delivery nodes follow suit. Government cloud baselines currently mirror this tier for general-purpose compute.

Tier IV, however, grows at 37.5% CAGR as digital-banking regulations and real-time AI training require 99.995% uptime. The Cyber Security Act 2024 classifies banking, telecom and transport systems as Critical Information Infrastructure, effectively mandating Tier IV for many new deployments. Oracle’s forthcoming Kedah campus targets this standard with dual power feeds and fault-tolerant switchgear. The Malaysia hyperscale data center market size allocated to Tier IV builds is therefore set to climb sharply within banking, healthcare and sovereign workloads.

By End-User Industry: Cloud Services Dominate Amid Media Growth

Cloud and IT services consumed 50% of 2024 demand as hyperscalers expanded ASEAN service portfolios from Malaysian availability zones. SaaS providers use Johor sites as redundant DR locations, reinforcing the Malaysia hyperscale data center market’s reputation for regional resilience. Telecommunications carriers, the next-largest slice, integrate edge nodes for 5G network-slicing trials.

Media and entertainment posts the highest 38.3% CAGR on the back of regional content-localisation policies and rising over-the-top streaming subscribers. ByteDance anchors GPU clusters in Johor to transcode short-form video at millisecond latencies. Government workloads increase steadily as ministries consolidate on a sovereign-cloud framework, while BFSI players leverage new digital-bank licences to capture under-banked segments.

By Data Center Size: Massive Facilities Lead While Mega-scale Accelerates

Massive sites between 25 MW and 60 MW hold 45% of installed load, reflecting hyperscalers’ preference for modular, multi-building campuses. These footprints balance scale economies with staged capex releases, making them the workhorse format of the Malaysia hyperscale data center market.

Mega-scale projects above 60 MW grow fastest at 39.0% CAGR, catalysed by GPU-cluster density and renewable-power purchase leverage. NTT’s 290 MW Johor campus and Vantage’s 256 MW Cyberjaya site epitomise this trend. STACK Infrastructure’s 220 MW expansion couples direct-liquid cooling with on-site battery storage to shave peak loads. Land-bank strategies now aim at 100-hectare zones to future-proof expansion corridors amid accelerating AI compute requirements.

Geography Analysis

The Klang Valley retains the country’s largest cluster owing to mature fiber backbones, skilled workforce and government proximity. Google’s selection of Elmina Business Park for its first campus underpins continued investor confidence despite water-stress cautions in Selangor. Microsoft’s three Greater Kuala Lumpur builds deepen the supply pipeline, yet escalating electricity tariffs push operators toward efficiency upgrades or partial off-grid solar-plus-storage solutions.

Johor emerges as the fastest-growing node in the Malaysia hyperscale data center market, fuelled by land priced at discounts of up to 60% versus Singapore. JPMorgan forecasts capacity may top 5 GW by 2035, a scenario buttressed by Princeton Digital Group’s and NTT’s multi-hundred-megawatt commitments. State authorities, however, rejected 30% of January-May 2024 applications to preserve power and water reserves, signalling stricter sustainability gating that could elongate approval cycles for latecomers.

East Malaysia’s Sarawak leverages its 6.2 GW hydropower base to court carbon-neutral campuses. Transmission bottlenecks to Peninsular load centres curtail export potential, but local demand for AI model-training farms supports green mega-campus concepts. Penang and Kedah maintain moderate share; semiconductor ecosystems there reduce spare-part lead times and enable frictionless trucking of prefabricated modules to new sites.

The hyperscale data center market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Africa, South America, and Asia, along with detailed country-level analysis for Indonesia, Thailand, South Africa, Argentina, Hong Kong, and Israel.

Competitive Landscape

Competition is moderate-fragmented as no operator exceeds a one-quarter share of installed IT load. Global hyperscalers, self-building core regions, rely on colocation for surge demand, ensuring diverse revenue per square-foot ratios across facilities. Equinix and Digital Realty employ global platform consistency to lure financial-services tenants adhering to cross-border transfer guidelines.

Regional specialists like YTL Data Center and Princeton Digital Group exploit local land banks and utility partnerships for speed-to-power advantages. Digital Edge pilots hybrid super-capacitor storage with Donghwa ES to reduce generator run-time and thereby shrink Scope 1 emissions. Sustainable Metal Cloud’s immersion technology wins proof-of-concept deals with AI-focused research firms, offering 50% energy savings on comparable workloads.

Innovation around renewable-energy hedging, edge-location fire sprinklers designed for immersion tanks and AI-driven DCIM is emerging as key differentiation. White-space opportunities persist in East Malaysia where hydropower-linked green attributes enable premium pricing for 24×7 clean-energy-matching contracts.

Malaysia Hyperscale Data Center Industry Leaders

Microsoft Corporation

Amazon Web Services

Google (Alphabet Inc.)

NTT Ltd.

Keppel Data Centres

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Malaysia’s tariff restructure places data centers in an ultra-high-voltage band, lifting power costs by 10-15%.

- May 2025: Google awards Gamuda a RM 1 billion construction package and purchases 389 acres in Negeri Sembilan.

- April 2025: Malaysia issues Cross-Border Personal Data Transfer Guidelines defining adequacy standards.

- March 2025: Microsoft confirms three Malaysian data centers launching by Q2 2025, projected to add 37,575 new jobs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Malaysia hyperscale data center market as the annual revenue earned from self-built or wholesale facilities engineered to operate beyond 10 MW of critical IT load. Figures are expressed in U.S. dollars and cover cloud operators' internal usage as well as contracted wholesale leases.

Scope Exclusions: Retail colocation suites, sites below 10 MW, edge micro-sites, and managed service revenues are excluded.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Power Distribution Units

- Transfer Switches and Switchgear

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning Services

- Design Engineering

- Fire Detection, Suppression and Physical Security

- DCIM / BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-user Industry

- Cloud and IT Services

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End-users

- By Data Center Size

- Large ( Less than or equal to 25 MW)

- Massive (Greater than 25 MW and Less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with facility developers, utility engineers, and cloud architects across Johor, Klang Valley, and Penang confirmed achievable PUE bands, contract pricing, and capacity ramp-up curves, closing gaps left by desk sources.

Desk Research

We compiled baseline data from the Malaysian Communications and Multimedia Commission, Energy Commission power statistics, Bank Negara capital-flow tables, and Malaysia Digital Economy Corporation investment trackers. Trade insights from the Asia Pacific Data Centre Association, customs import logs for servers, public filings archived in D&B Hoovers, and news captured through Dow Jones Factiva supplemented the picture. These sources illustrate, not exhaust, the reference pool used.

Market-Sizing and Forecasting

A top-down reconstruction begins with operational and announced MW capacity, reconciled with grid-connection data, then multiplied by average utilization and price per kW to reach 2025 revenue. Select bottom-up checks, sampled land-bank roll-ups and disclosed lease rates, calibrate totals. Core variables include grid tariffs, capacity additions, hyperscaler cloud bookings, subsea-cable upgrades, and renewable-quota uptake. A multivariate regression supported by ARIMA extensions projects the market to 2030; regional averages agreed during expert calls resolve missing datapoints.

Data Validation and Update Cycle

Outputs pass multi-layer variance checks; anomalies trigger re-work, and every assumption is re-signed before publication. The model refreshes yearly, with interim updates for major capacity or tariff shocks.

Why Mordor's Malaysia Hyperscale Data Center Baseline Commands Reliability

Published estimates diverge because each firm chooses different scopes, pricing bases, or refresh cadences.

Mordor Intelligence counts revenue from both self-build and wholesale hyperscale assets, applies constant 2024 exchange rates, and revisits drivers every twelve months, whereas other studies may track only CapEx, omit Johor's surge pipeline, or freeze rates for the entire study term.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.03 B (2025) | Mordor Intelligence | - |

| USD 4.04 B (2024) | Global Consultancy A | Tracks total investment across all data-center types; measures CapEx, not revenue |

| USD 1.55 B (2024) | Regional Consultancy B | Blends hyperscale with managed and edge sites; excludes self-build capacity |

| USD 0.30 B (2025) | Industry Association C | Focuses on the Kuala Lumpur cluster; omits Johor mega-campus builds |

Once differing scopes and metrics are reconciled, our disciplined model offers the most balanced and repeatable baseline for decision-makers.

Key Questions Answered in the Report

What is the current size and growth outlook of the Malaysia hyperscale data center market?

The market stands at USD 6,035.12 million in 2025 and is projected to reach USD 40,167.84 million by 2031, registering a 37.15% CAGR

Which Malaysian region is expanding fastest for hyperscale capacity?

Johor is the country’s fastest-growing data-center cluster, with capacity expected to exceed 5 GW by 2035 thanks to lower land costs and direct links to Singapore

What government incentives are attracting data-center investors?

MyDIGITAL tax breaks, Malaysia Digital (MD) Status benefits and streamlined approvals through the Digital Investment Office shorten project lead times and cut corporate tax burdens for qualifying operators

How does limited renewable energy supply affect hyperscale expansion plans?

On-grid renewables cover only 19% of national generation, creating a shortfall against hyperscalers’ 100% clean-power goals and adding complexity to long-term power-purchase agreements

On-grid renewables cover only 19% of national generation, creating a shortfall against hyperscalers’ 100% clean-power goals and adding complexity to long-term power-purchase agreements

Mechanical systems—particularly liquid and immersion cooling designed for GPU-dense racks—are expanding at a 38.1% CAGR as operators retrofit for high-thermal AI workloads

What financial impact will the July 2025 electricity-tariff change have on operators?

Reclassification into the ultra-high-voltage band is expected to raise data-center power bills by 10-15%, adding roughly RM 63 million in annual costs for a 100 MW facility

Page last updated on: