Hong Kong Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

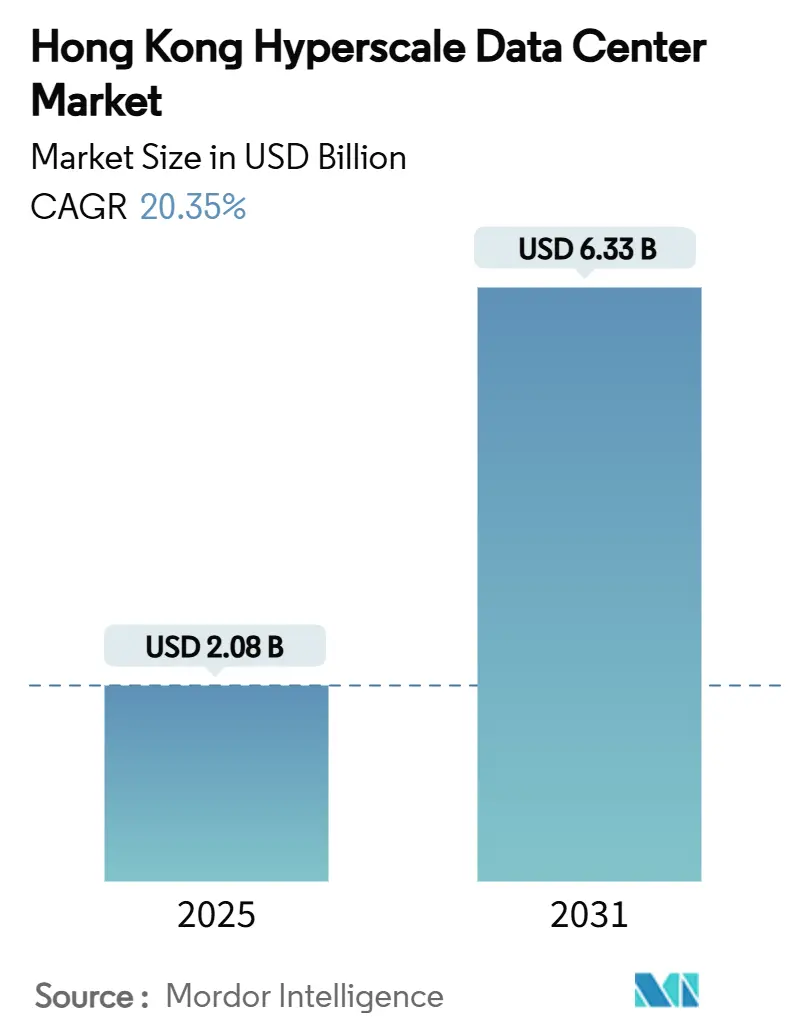

| Market Size (2025) | USD 2.08 Billion |

| Market Size (2031) | USD 6.33 Billion |

| Growth Rate (2025 - 2031) | 20.35% CAGR |

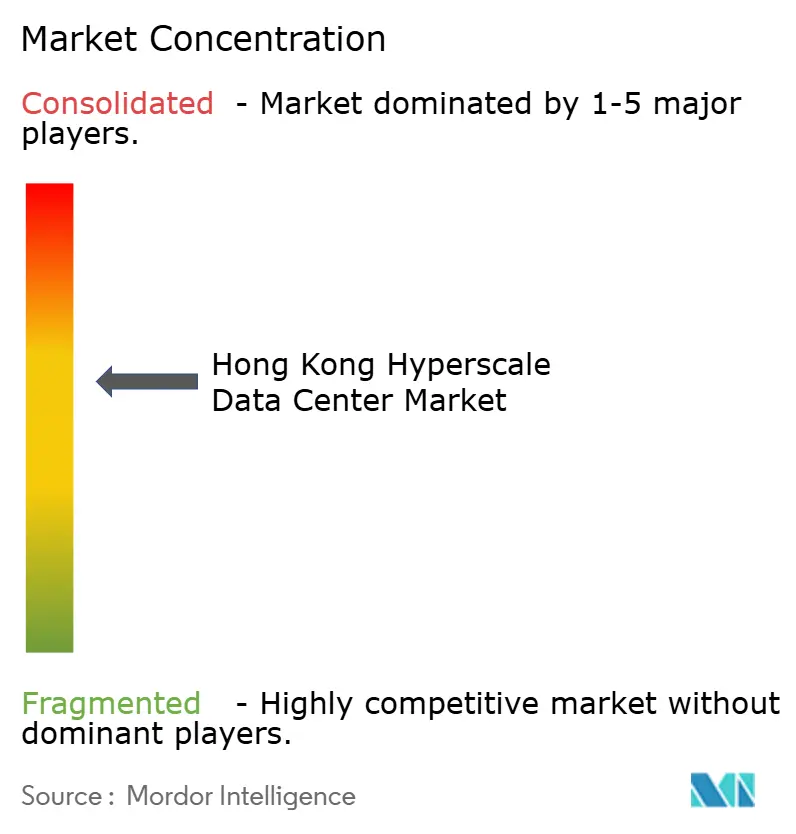

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Hyperscale Data Center Market Analysis by Mordor Intelligence

The Hong Kong hyperscale data center market size stands at USD 2.08 billion in 2025 and is forecast to reach USD 6.331 billion by 2031, expanding at a 20.35% CAGR during 2025-2031. Installed IT load is projected to rise from 1,211.83 MW to 2,057.94 MW at a 9.23% CAGR, signalling a decisive tilt toward premium, AI-ready capacity rather than sheer floor area. Rapid uptake of liquid- and immersion-based cooling, escalating GPU rack densities that breach 70 kW, and generous Northern Metropolis land-grant policies are reshaping investment priorities. Mega facilities above 60 MW are attracting hyperscaler budgets, while cross-border fintech workloads demanding sub-millisecond links accelerate facility clustering near landing stations. The Hong Kong hyperscale data center market is also benefiting from HK Electric’s first 150 MW green-hydrogen PPA, which reduces carbon-intensity risk premiums for long-term power contracts.

Key Report Takeaways

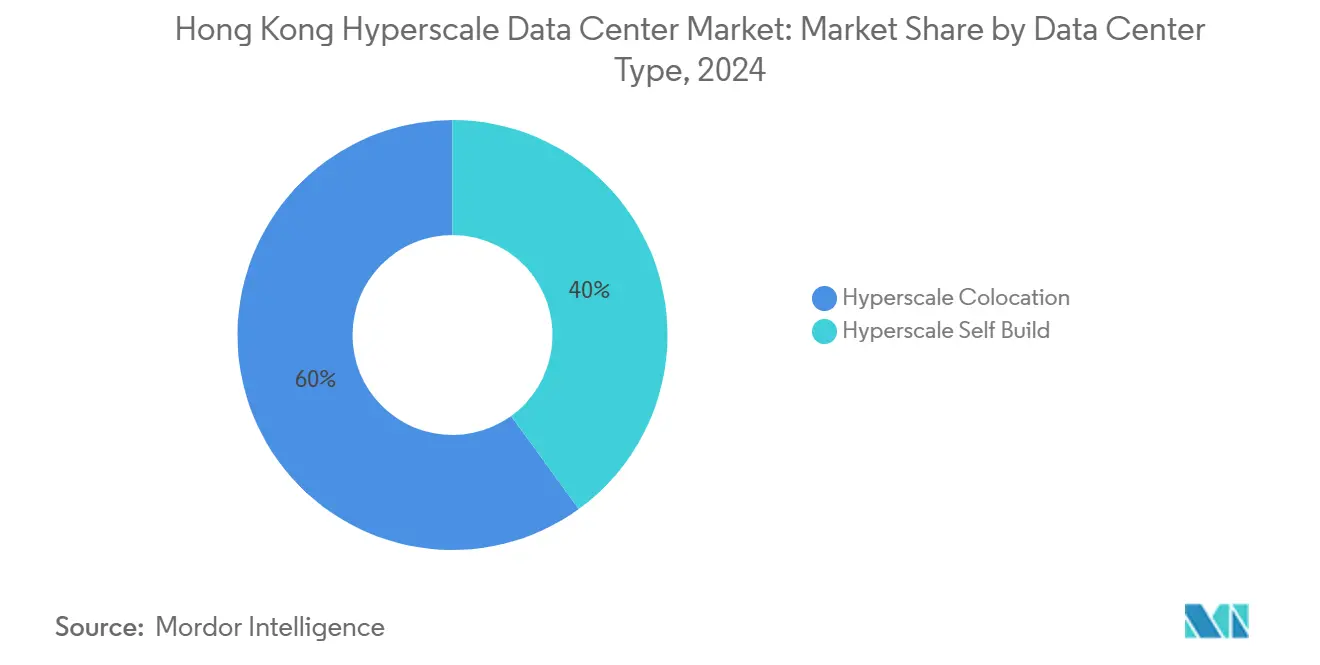

- By data center type, colocation led with 60% of Hong Kong hyperscale data center market share in 2024, whereas hyperscaler self-builds are advancing at a 22.5% CAGR to 2030.

- By component, IT infrastructure accounted for 56% share of the Hong Kong hyperscale data center market size in 2024, while immersion cooling is projected to expand at a 22.7% CAGR through 2030.

- By tier standard, Tier III facilities held 75% share in 2024; Tier IV is the fastest-growing category at 21.8% CAGR.

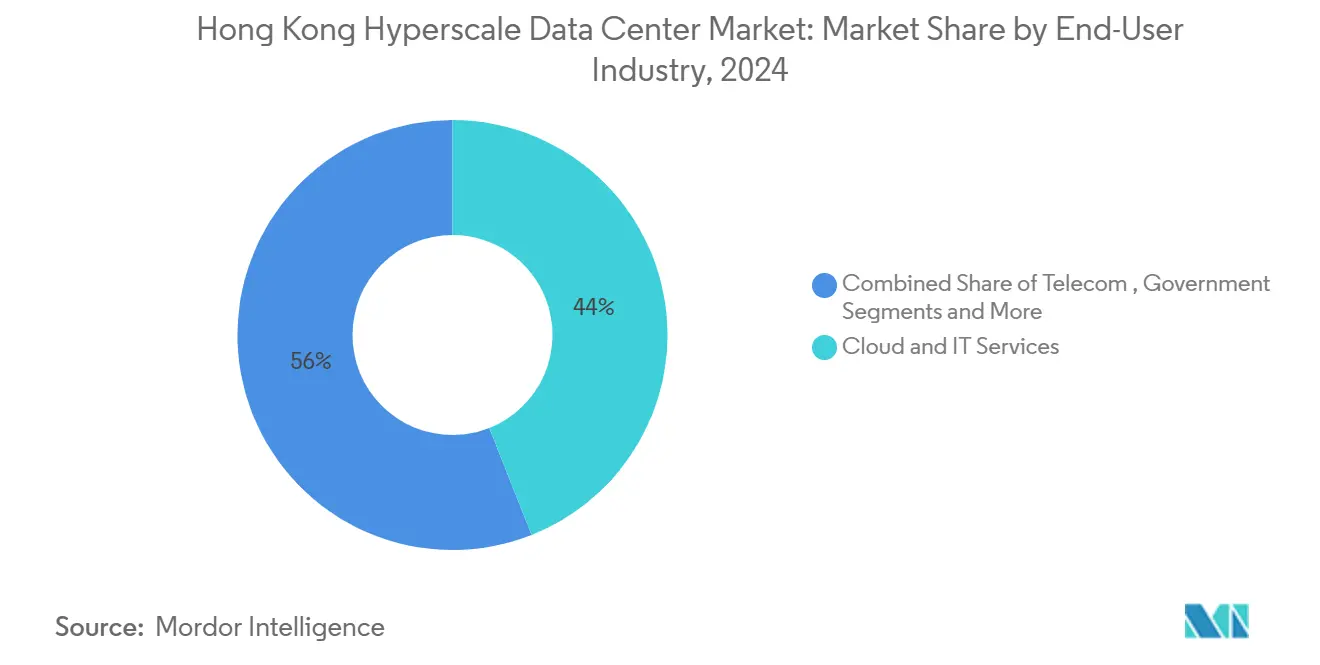

- By end-user industry, cloud and IT services captured 44% share in 2024, yet AI/ML cloud platforms are set to grow at 22.6% CAGR.

- By data center size, large facilities (≤25 MW) represented 50% share in 2024, whereas mega facilities (greater than 60 MW) are forecast to climb at a 21% CAGR.

The competitive field in Hong kong extends beyond its borders, connecting regional dynamics to a global strategic environment. Our market research on global hyperscale data center industry outlines that broader, worldwide structure.

Hong Kong Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI/ML GPU rack densities greater than70 kW accelerating new-build demand | +4.2% | Hong Kong core, spill-over to GBA | Medium term (2-4 years) |

| China-GBA “Northern Metropolis” land-grant incentives for DCs | +3.8% | Hong Kong, Shenzhen border areas | Long term (≥ 4 years) |

| Cross-border RMB-based fintech platforms needing ultra-low-latency colo | +3.1% | Hong Kong financial district, Tseung Kwan O | Short term (≤ 2 years) |

| HK Electric’s first 150 MW green-hydrogen PPA for DCs | +2.4% | Hong Kong island, Kowloon | Long term (≥ 4 years) |

| Harbourfront subsea-cable landing expansion driving carrier-neutral hubs | +2.8% | Hong Kong core, coastal areas | Medium term (2-4 years) |

| Retro-fit of high-rise industrial blocks with modular liquid-cooling suites | +2.1% | Kwai Chung, Fanling industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI/ML GPU Rack Densities Accelerating Infrastructure Transformation

GPU-intensive AI training has rendered legacy air-cooled halls uneconomical, pushing Hong Kong operators toward direct-to-chip and immersion cooling that comfortably handles 70-100 kW per rack. Global Switch’s direct liquid-cooling retrofit cut cooling energy use by 95% and delivered a record 1.02 PUE, elevating the Hong Kong hyperscale data center market as a regional testbed for thermal innovation.[1]Nicholas Gooding, “Global Switch Brings Direct Liquid Cooling to Hong Kong,” Data Center Dynamics, datacenterdynamics.com Operators equipped for liquid cooling can monetize premium AI footprints rapidly, while sites without retrofit budgets risk stranded assets. Supermicro is now shipping over 100,000 GPUs per quarter inside rack-scale liquid-ready enclosures, making liquid cooling part of baseline RFPs. The widespread adoption of high-density racks thus lifts revenue per square foot, even as total white-space growth moderates.

Cross-Border RMB Fintech Platforms Driving Ultra-Low-Latency Requirements

RMB-denominated fintech flows have normalised real-time settlement horizons, forcing data-center site selection to prioritise fibre distance to eastern Pearl River Delta exchanges. HSBC’s PayMe scaled from six-hour to six-second analytics windows after its cloud-native rebuild, reinforcing demand for hyperscale colocation in Tseung Kwan O for proximity to submarine cable gateways. ICBC Asia similarly upgraded to 24/7 video-enabled wealth-management platforms that rely on latency-optimised interconnects. China Telecom Americas now bundles dedicated <1 ms cross-border circuits with colo space, skewing new capacity toward harbourfront carrier-neutral hubs. The Cross-boundary Wealth Management Connect scheme compounds these latency mandates, anchoring colocation demand in select corridors.

China-GBA Northern Metropolis Land-Grant Incentives Reshaping Development Patterns

Policy alignment has become a structural cost advantage. The Hetao cooperation zone dedicates almost 4 km² to tech infrastructure, drawing over 150 R&D projects that presubscribe compute blocks from neighbouring Hong Kong hyperscale data center market operators. Hong Kong earmarked HKD 2 billion for research clusters inside the same corridor, allowing data-center developers to negotiate discounted land premiums. Tseung Kwan O’s 75-hectare InnoPark provides purpose-built power and fibre backbones, lowering build-out timelines for Tier IV projects.[3]Hong Kong Science and Technology Parks Corporation, “Tseung Kwan O InnoPark,” hkstp.org Hung Shui Kiu’s 10-hectare IT parcel further disperses capacity, mitigating single-district congestion while spreading risk. Collectively, these incentives compress development cycles and tilt long-run supply in favour of mega-campuses.

HK Electric’s Green-Hydrogen PPA Pioneering Sustainable Power Solutions

Decarbonisation mandates now influence hyperscaler site approvals more than headline rent. HK Electric’s 150 MW green-hydrogen PPA provides emission-free baseload and caps long-term carbon pricing exposure for incoming facilities. CLP’s ambition to cut carbon intensity to 0.26 kg CO₂e/kWh by 2030 tightens efficiency benchmarks across the Hong Kong hyperscale data center market.[2]Eric Ng, “Hong Kong Energy Giant CLP Takes the Nuclear Option,” South China Morning Post, scmp.com ECL’s off-grid hydrogen-powered prototype proved PUE 1.1 and 75 kW racks are commercially feasible, validating future hydrogen micro-grids for Kowloon brownfield redevelopments. Hitachi Energy’s HyFlex generator roadmap offers diesel-free backup that meets Hong Kong’s impending Air Quality Ordinance revisions. Early adopters thus gain compliance head-start and unlock green-finance discounts.

Restraints Impact Analysis Table*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 35% real-estate cost inflation since 2021 | -2.8% | Hong Kong core, industrial areas | Short term (≤ 2 years) |

| Scarce 132 kV power-feeder slots—3-year queue at CLP and HK Electric | -3.2% | Hong Kong island, Kowloon, New Territories | Medium term (2-4 years) |

| Proposed 2026 water-usage levy on evaporative cooling towers | -1.4% | Hong Kong core facilities | Short term (≤ 2 years) |

| National-security data-sovereignty scrutiny delaying foreign licences | -2.1% | Hong Kong financial district | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power Infrastructure Bottlenecks Creating Development Constraints

Only three new 132 kV feeds were allocated to data-center applicants in 2024, lengthening grid connection queues to three years at both major utilities. While CLP plans HKD 52.9 billion in network upgrades through 2028, most capex funds reliability rather than additional megawatts, compelling developers to phase builds into ≤10 MW blocks aligned with feeder release schedules. The district cooling plant at Kai Tak proves shared chilled-water loops can shave 20% peak power draw, yet similar projects require multi-agency coordination rarely achieved within hyperscaler timeframes. As a result, operators in the Hong Kong hyperscale data center market increasingly adopt modular edge pods that ride on existing 11 kV spurs until full-scale feeders arrive. Delays inflate financing costs and threaten SLA commitments for AI tenants that demand turnkey power reserves.

Data Sovereignty Regulations Creating Licensing Uncertainties

Hong Kong’s first cybersecurity statute, effective 2026, obliges critical-infrastructure operators to grant log-level visibility to regulators within set timeframes. Amazon and Google flagged broad access clauses that could expose proprietary AI models, prompting cautious licence-application pacing. Although floor space is still projected to climb 34% to 14 million ft² by 2025, the approval cycle for foreign hyperscalers lengthened to nine months, versus six previously. A Hong Kong-Beijing memorandum on cross-border data flows offers a framework, yet operators await granular protocols on encryption-key escrow before committing new self-builds. Consequently, some new entrants hedge with Singapore or Johor options, tempering near-term capacity take-up in the Hong Kong hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Self-Build Momentum Challenges Colocation Dominance

The Hong Kong hyperscale data center market size attributed to colocation reached USD 1.25 billion in 2024, equal to 60% of overall revenue, whereas hyperscaler self-builds logged USD 0.65 billion and are pacing a 22.5% CAGR toward 2030. Colocation’s scale stems from real-estate prices of USD 3,000-4,000/ft², making shared campuses financially rational for enterprises and mid-market cloud nodes. SUNeVision enlarged its Mega-Plus park to 470,000 ft², winning long-term AI tenants that prefer cost-predictable lease models. Nonetheless, Amazon’s USD 100 billion global self-build program highlights a pivot toward full-stack control where specialised cooling and renewable PPAs underpin AI roadmaps. Operators that excel in power-density engineering and sovereign-cloud compliance are positioned to capture wallet share from hyperscalers seeking certainty on both fronts.

Second-generation self-build blueprints increasingly feature hydrogen-ready gensets, 100% liquid-cooled white space, and software-defined power, compressing deployment times below 20 months. Colocation incumbents respond by offering “build-to-suit” halls and in-rack liquid-cooling add-ons to retain anchor tenants. Should real-estate inflation persist, hybrid models mixing powered-shell leases with tenant-specific fit-outs could rebalance the competitive field within the Hong Kong hyperscale data center market.

By Component: Immersion Cooling Disrupts Traditional Infrastructure Hierarchy

IT hardware still commanded 56% of 2024 spend, reflecting the primacy of servers, flash storage, and 400G switching fabrics. Yet immersion cooling is registering the market’s fastest 22.7% CAGR, capturing capex that formerly flowed to CRAC units and raised-floor plenums. Two-phase tanks deliver 87% cooling energy cuts and free up 30% floor footprint, letting operators increase revenue density per MVA. Electrical infrastructure—PDUs, UPS, and busways—must likewise evolve; liquid-to-air CDUs by Delta support 115 kW racks and integrate directly with BMS platforms to pre-empt thermal excursions. Suppliers offering integrated server-to-switch-to-tank ecosystems therefore gain strategic leverage over standalone component vendors inside the Hong Kong hyperscale data center industry.

General-construction contractors are redesigning shells with 1,500 kg/m² load-bearing floors and shortened plenums, lowering clear height requirements and unlocking more vertical conversions across Kwai Chung industrial stock. As the Hong Kong hyperscale data center market size for mechanical-cooling shrinks, contractors pivot toward scaled prefabrication and fire-suppression systems compatible with dielectric fluids.

By Tier Standard: Tier IV Acceleration Reflects AI Uptime Requirements

Tier III continues to dominate with 75% share, yet Tier IV is compounding at 21.8% as financial-trading and AI-model training penalise every minute of downtime. Equinix HK6’s USD 124 million project embeds Tier IV topology with liquid cooling to deliver 26.3 minutes annual downtime tolerance, a feature now demanded by leading quant-trading desks. Operators unable to finance N+2 redundancy risk migration of premium tenants to Tier IV rivals, even if rack rents run 20-30% higher. For cost-sensitive SaaS or content-distribution workloads, Tier III remains sufficient, ensuring a dual-tier ecosystem persists within the Hong Kong hyperscale data center market.

Regulators indicate forthcoming Basel III + cyber-resilience addendums may push financial institutions to mandate Tier IV for core-banking workloads, a scenario that could lift Tier IV’s Hong Kong hyperscale data center market share above 35% by 2030.

By End-User Industry: AI/ML Platforms Reshape Demand Patterns

Cloud and IT services held 44% revenue share in 2024, but AI/ML cloud platforms are growing 22.6% annually as banks, telcos, and media firms offload model-training tasks. HSBC’s Google-Cloud risk grid expanded to 40 global sites with 10× faster compute, driving incremental GPU cluster orders in Hong Kong. Telecom operators layer 400G fabric extensions onto existing dark-fibre rings, positioning their PoPs inside hyperscale halls to monetise traffic spikes from streaming and gaming launches. Government transformation projects, such as digital ID and smart-city dashboards, siphon legacy on-prem workloads into certified Hong Kong hyperscale data center market capacity that fulfils data-sovereignty and cybersecurity rules.

Meanwhile, Manufacturing 4.0 pilots at Hong Kong’s Advanced Manufacturing Centre rely on edge-AI gateways that backhaul telemetry to Tseung Kwan O GPU farms for digital-twin analytics. This long-tail diversity stabilises utilisation rates across operators even as AI heavyweights set the growth tempo.

By Data Center Size: Mega Facilities Challenge Large-Scale Dominance

Large sites still account for 50% utilisation owing to Hong Kong’s dense real-estate grid. However, mega buildings greater than 60 MW are sprinting at 21% CAGR, anchored by multi-year take-or-pay contracts from US and mainland hyperscalers. SUNeVision’s six-storey, 64-MVA block, now under construction, exemplifies the mega-trend inside the Hong Kong hyperscale data center market. Funding flows validate the thesis: Vantage Data Centers secured an extra USD 13 billion to scale regional footprints, including twin 68 MW builds earmarked for Tseung Kwan O and Fanling.

Massive sites serve as interim steps for cloud firms balancing capital discipline with latency goals, yet could face cannibalisation once power-feeder queues ease. Smaller edge-facilities capitalise on urban latency niches, but rising land levies pressure their economics unless paired with mixed-use real-estate yields.

Geography Analysis

Tseung Kwan O dominates new capacity additions after CLP commissioned a dedicated substation feeding more than 400 MVA solely to the district’s data-center cluster. The zone hosts SUNeVision’s Mega-Plus campus, GDS’s newly pre-committed 40 MW hall, and Equinix HK6, collectively anchoring over half of the Hong Kong hyperscale data center market size slated for delivery through 2028. Direct fibre spurs into the Asia-Pacific Gateway and PLCN cable systems shorten international round-trip times, making the area a natural hub for real-time AI inferencing workloads.

Kwai Chung and Tsuen Wan benefit from the government’s industrial-building revitalisation policy that waives change-of-use premiums for telecoms and compute facilities. Vantage’s 18 MW Kwai Chung site went live in 2025 after an 11-month retrofit—half the time needed for greenfield and enjoys 99.999% utility reliability on existing 11 kV feeders. These districts target enterprise tenants that value rapid move-in over Tier IV redundancy, sustaining colocation fill-rates even as hyperscalers gravitate toward mega campuses.

Northern Metropolis sub-districts Fanling and Sheung Shui are emerging as cost-effective plots averaging 20% lower land premiums. Hetao science-park tenants pre-leased 12 MW of liquid-ready capacity scheduled for 2027 to support cross-border analytics engines integrating Shenzhen supply-chain telemetry. Government plans for direct rail extensions and expedited customs lanes could unlock further captive demand, but grid upgrades remain the gating item. By 2031, Northern Metropolis facilities are projected to claim nearly 15% of installed Hong Kong hyperscale data center market load, diversifying the geographical risk profile previously concentrated along the eastern seaboard.

Mordor Intelligence tracks the hyperscale data center market across other major regions such as Asia, Europe, and North America, with additional country-level coverage spanning Japan, China, Norway, United States, France, and Sweden, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Market fragmentation persists: the five largest operators control roughly 28% of installed IT load, conferring moderate competitive pressures. SUNeVision exploits brownfield conversions and local permitting fluency to court enterprise colocation, while Equinix and Digital Realty lean on global interconnection fabrics to serve multi-cloud routing needs. Liquid-cooling IP portfolios are fast becoming strategic differentiators; Global Switch’s immersion rollout cut tenant power bills by double digits, attracting GPU farm deployments that demand guaranteed 100 kW racks.

Capital markets favour scale plays: Vantage’s USD 9.2 billion equity infusion and Digital Edge’s USD 1.6 billion raise empower multi-site land-banking that smaller peers cannot match. Conversely, niche innovators such as LiquidStack or Hitachi Energy monetise proprietary cooling and hydrogen-gen-set solutions via OEM or JV routes, embedding themselves in build-specs of mega-campuses. Regulatory agility distinguishes local incumbents; those ready for 2026 cybersecurity audits market compliance as a competitive moat, leveraging local SOC expertise to reassure fintech clients wary of data-sovereignty probes.

Acquisition chatter centres on ready-to-retrofit industrial towers and partial-shell assets whose power entitlements have already cleared utility queues. Consolidation could accelerate once Northern Metropolis greenfield plots reach critical mass, enabling portfolio players to arbitrage construction costs, optimise PUE across mixed-vintage assets, and cross-sell BMS analytics layers throughout the Hong Kong hyperscale data center market.

Hong Kong Hyperscale Data Center Industry Leaders

SUNeVision Ltd (iAdvantage)

Equinix Inc.

Digital Realty Trust Inc

China Mobile international

Amazon Web Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Vantage Data Centers completed a USD 9.2 billion equity investment led by DigitalBridge and Silver Lake.

- January 2025: Digital Edge raised over USD 1.6 billion in new equity and debt capital to fund platform expansion.

- March 2025: GDS Holdings reported Q4 2024 revenue of RMB 2,690.7 million (USD 368.6 million) and a committed area of 629,997 m².

- August 2024: Equinix announced a USD 124 million investment for its HK6 facility with liquid-cooling cabinets targeting AI workloads.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Hong Kong hyperscale data center market as the annual revenue generated from purpose-built or retrofitted facilities that deliver at least 4 MW of contiguous IT load to a single tenant or a cloud platform through self-builds or wholesale colocation agreements. This includes compute, storage, and network infrastructure charges, power, cooling, cross-connect fees, and managed facility services.

Scope exclusion: edge micro-sites below 4 MW, enterprise on-premise rooms, and carrier hotels that do not meet hyperscale density thresholds are excluded.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Unit

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning

- Design Engineering

- Fire, Security and DCIM/BMS

- DCIM / BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-user Industry

- Cloud and IT Services

- Telecom

- Banking, Financial Services and FinTech

- Media and Entertainment

- Government and Public Sector

- E-commerce and Retail

- Other End Users

- By Data Center Size

- Large ( Less than or equal to 25 MW)

- Massive (Greater than 25 MW and Less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

We interviewed data center developers, cloud platform capacity planners, facility engineering consultants, and procurement leads across Hong Kong, Shenzhen, Singapore, and Sydney. Their insights on lease terms, GPU rack densities, and land-premium hurdles filled data gaps and calibrated escalation curves that desk sources could not fully explain.

Desk Research

Mordor analysts began with factual datasets from tier-one public sources such as the Census and Statistics Department of Hong Kong, OfCA spectrum and submarine-cable filings, CLP and HK Electric power-feeder approvals, and Hong Kong Monetary Authority fintech registries. Trade associations such as the Hong Kong Internet Exchange, Uptime Institute case libraries, and IEEE Xplore papers on immersion-cooling economics offered engineering baselines. Company 10-Ks, REIT presentations, and press releases were mined for rack counts, pre-lets, and disclosed megawatt pipelines. Subscription databases D&B Hoovers and Dow Jones Factiva supported operator financial splits and deal tracing. This list is illustrative; many additional secondary references informed our desk work.

Market-Sizing & Forecasting

The base year value is built with a top-down "installed IT-load × blended ASP" construct that reconstructs hyperscale revenue from government power draw records and inbound-outbound traffic tallies, and is then sense-checked through operator roll-ups of announced megawatt additions. Key variables like average rack density (kW), new cable landing slots, brownfield land premiums, renewable PPA uptake, and GPU cluster share inform both the historical series and the 2025-2031 forecast. A multivariate regression with ARIMA error-correction captures the impact of those drivers; bottom-up lease samples adjust for outliers before lock-in.

Data Validation & Update Cycle

Outputs pass three-layer variance checks, senior peer review, and anomaly re-contacts. Models refresh annually, with interim updates when utility tariffs, zoning rules, or ≥25 MW project announcements materially shift assumptions. A final analyst pass occurs just before client delivery.

Why Mordor's Hong Kong Hyperscale Data Center Baseline Inspires Greater Confidence

Published estimates often diverge because firms choose dissimilar workload thresholds, pricing baskets, and refresh cadences.

Key gap drivers in our field include whether self-built hyperscale halls are counted, how GPU rack premiums are layered, the currency-conversion month used, and how quickly brownfield sites are rolled into supply.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.08 Bn (2025) | Mordor Intelligence | - |

| USD 2.50 Bn (2025) | Regional Consultancy A | excludes power pass-through charges, uses fixed 18 kW density |

| USD 3.20 Bn (2024) | Global Consultancy B | mixes investment outlay with operating revenue, partial Tier II sites |

| USD 13.99 Bn (2025) | Trade Journal C | aggregates all data center types, employs broad APAC pricing proxies |

The comparison shows that once differences in scope, density assumptions, and revenue recognition are stripped out, Mordor's disciplined bottom-up cross-check against power-meter data gives decision-makers a balanced, transparent baseline that can be traced back to measurable variables and repeated with confidence.

Key Questions Answered in the Report

What is the current size of the Hong Kong hyperscale data center market?

The market is valued at USD 4.39 billion in 2025 and is projected to grow to USD 9.68 billion by 2030.

Which segment dominates the Hong Kong hyperscale data center market?

Hyperscale colocation leads with 60% market share in 2024 due to rapid, turnkey deployment needs.

Why is Hong Kong attractive for mainland Chinese cloud providers?

Its “China-neutral” regulatory setting lets providers serve both domestic and global customers from a single PoP with low-latency routes.

What is the main growth restraint facing operators?

A 150 MW annual power-quota cap delays energisation of new halls, pushing companies toward phased roll-outs and power-efficiency upgrades.

How are data-center operators addressing sustainability targets?

They purchase Renewable Energy Certificates via CLP Power’s green-tariff programme, deploy liquid cooling to cut PUE, and trial HVO for backup generators.

Which geographic zones in Hong Kong see the most data-center development?

Tseung Kwan O remains the largest hub, while Tsuen Wan–Kwai Chung shows the fastest pipeline growth; the Northern Metropolis is an emerging cluster aimed at future expansion.

Page last updated on: