Singapore Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

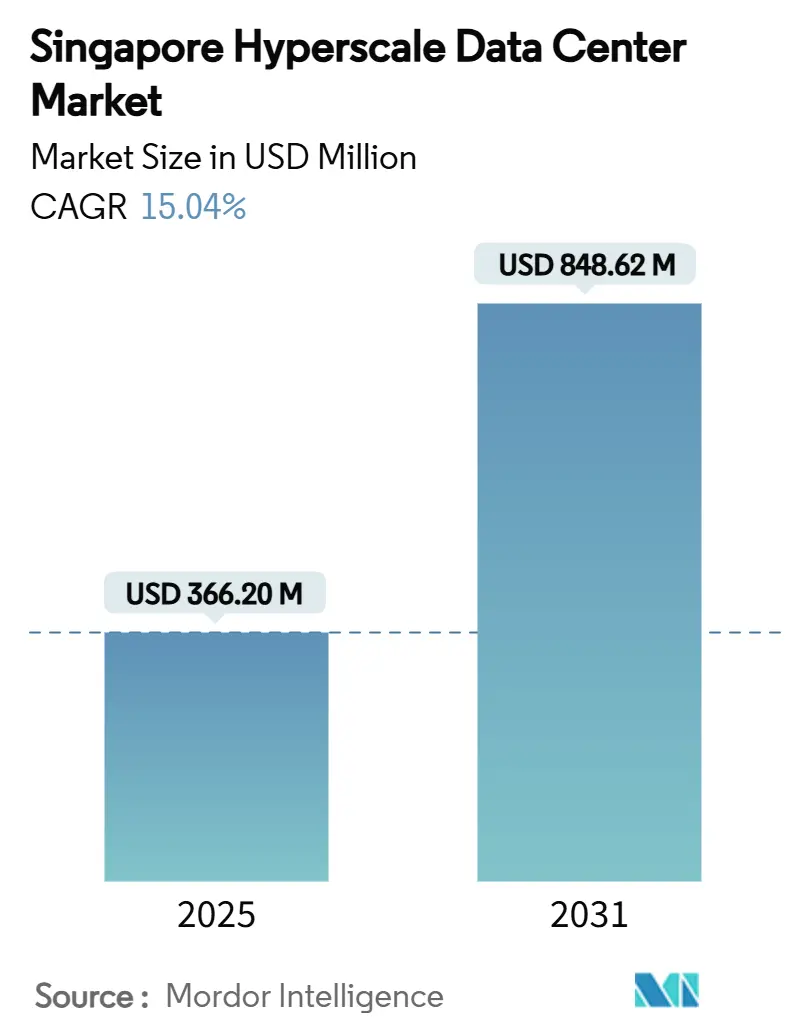

| Market Size (2025) | USD 366.20 Million |

| Market Size (2031) | USD 848.62 Million |

| Growth Rate (2025 - 2031) | 15.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Hyperscale Data Center Market Analysis by Mordor Intelligence

Singapore Hyperscale Data Center Growth Factors

The Singapore hyperscale data center market size stood at USD 366.20 million in 2025 and is forecast to reach USD 848.62 million by 2031, reflecting a 15.04% CAGR. The value growth far outpaces the 2.18% volume CAGR, indicating that density optimization, next-generation cooling, and premium uptime certifications are creating greater economic value per installed megawatt. Government policies such as the Green Data Centre Roadmap, the imminent carbon-tax escalation, and explicit water-usage caps continue to favor operators that deploy liquid-cooling and renewable-energy solutions. Rising AI and machine-learning workloads are pushing rack densities beyond 50 kW, spurring unprecedented demand for immersion and direct-to-chip cooling technologies. The entry of hyperscalers with USD 20 billion in committed investments and a cluster of floating data-center pilots underscore Singapore’s role as a testbed for sustainable megascale infrastructure. Strategic alliances between cloud providers, telecom operators, and real-estate majors signal a competitive shift from pure capacity provision toward integrated AI-ready campuses that bundle connectivity, GPUs, and sovereign-cloud zones.

Key Report Takeaways

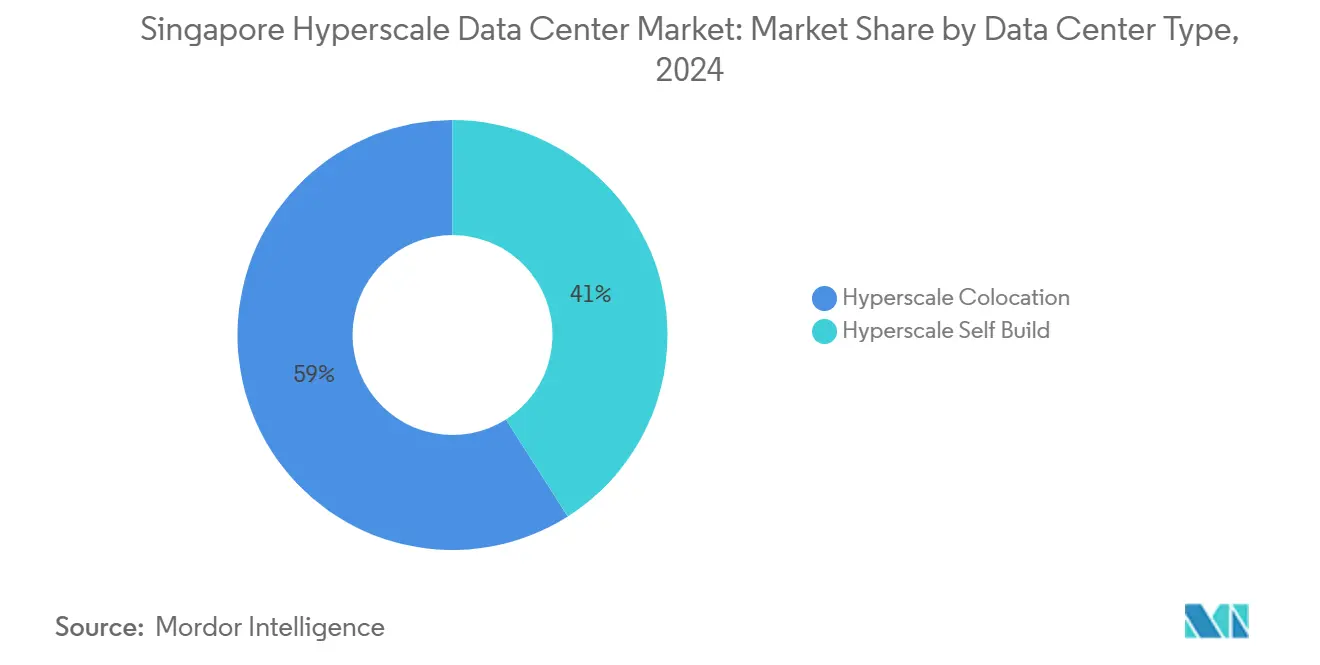

- By data center type, Hyperscale colocation led with 59% of the Singapore hyperscale data center market share in 2024; hyperscaler self-build is projected to post a 15.1% CAGR through 2030.

- By component, Mechanical infrastructure accounted for the fastest component growth at 16.1% CAGR, while IT infrastructure held a 44% revenue share in 2024.

- By tier standard, Tier III facilities commanded 66% of the market in 2024; Tier IV capacity is forecast to expand at a 17.2% CAGR to 2030.

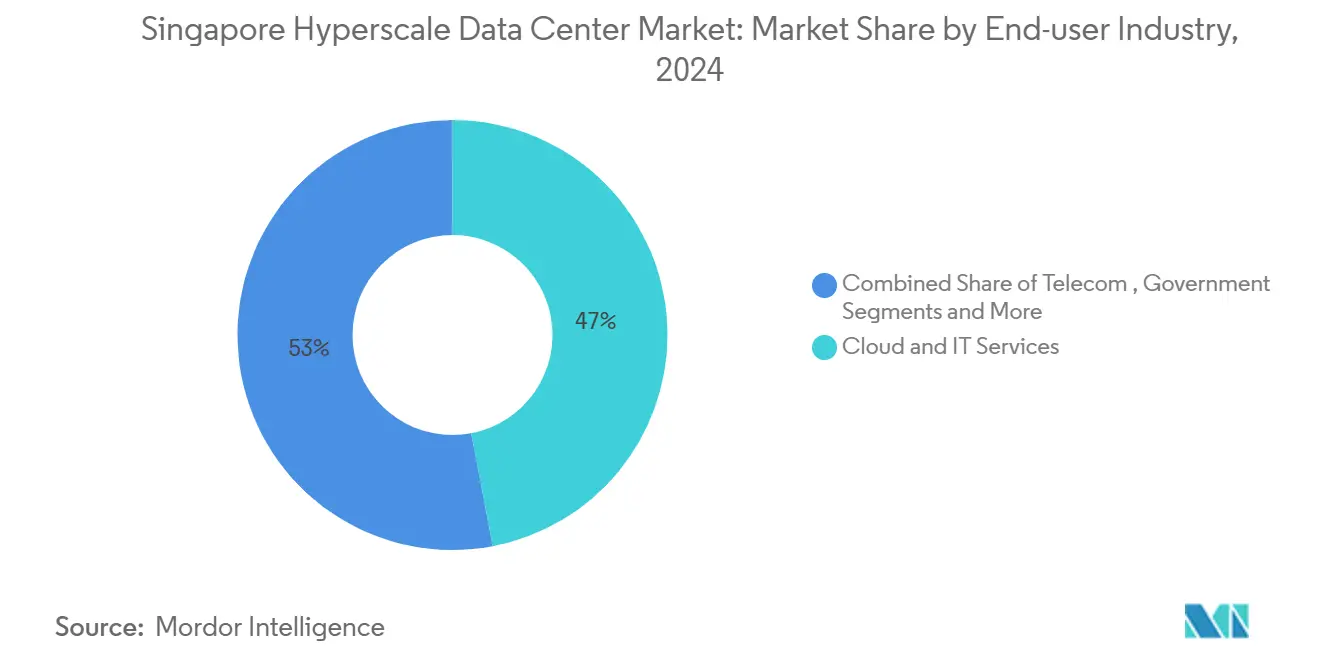

- By end-user industry, Cloud and IT end users generated 47% of 2024 demand, whereas e-commerce workloads are expected to advance at 15.7% CAGR through 2030.

- By data center size, Massive-scale sites (25-60 MW) held 50% of 2024 deployments; mega-scale builds above 60 MW are set to grow at 17.5% CAGR.

Singapore occupies a certain position within a broader, global distribution that spans multiple countries and geographies. Our hyperscale data center market share data maps worldwide allocation.

Singapore Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI / ML spill-over driving greater than 50 kW GPU racks | +3.2% | Singapore core; ripple to regional hubs | Medium term (2-4 years) |

| Real-time payment mandates raise Tier IV need | +2.8% | Nationwide; ASEAN cross-border networks | Short term (≤ 2 years) |

| 5G edge–core consolidation | +2.1% | National footprint with regional connectivity | Medium term (2-4 years) |

| ASEAN digital-sovereignty initiatives | +1.9% | Singapore hub with region-wide influence | Long term (≥ 4 years) |

| GenAI liquid-cooling campuses | +1.8% | Singapore core; export potential worldwide | Medium term (2-4 years) |

| Floating green-DC pilot projects | +1.4% | Coastal waters; template for other dense city-states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI / ML Spill-Over Driving greater than 50 kW GPU Racks

GPU-intensive AI training clusters are elevating typical rack densities from 15 kW to beyond 50 kW, compelling operators to adopt immersion and direct-to-chip cooling. Sustainable Metal Cloud demonstrated a power-usage-effectiveness below 1.03 and 50% energy savings with its HyperCube solution, validating the commercial viability of liquid cooling at scale.[1]CNBC, “Nvidia Partner Says It Can Cut Data Center Energy Use by 50% as AI Boom Strains Power Grid,” cnbc.com Singtel’s partnership with NVIDIA to roll out GPU clusters across its Nxera facilities from 2026 further normalizes AI-optimized colocation footprints. Component vendors now bundle 400 G and 800 G Ethernet fabrics with cooling-as-a-service contracts, turning infrastructure into a managed utility rather than a capital expense.

Real-Time Payment Mandates Raise Tier IV Need

The Monetary Authority of Singapore is unifying FAST, PayNow, and SGQR under a single entity, while linking the rails to India’s UPI for cross-border instant payments.[2]Channel Asia, “StarHub and HPE Team Up to Trial 5G Powered Edge Computing in Singapore,” channelasia.tech Sub-second transaction finality demands 99.995% uptime, prompting banks and payment processors to shift workloads into Tier IV certified rooms. AWS already hosts the cross-border clearing interface, illustrating hyperscaler alignment with financial-service uptime targets. Institutions such as DBS have logged SGD 370 million in cost efficiencies from AI and data analytics, adding further compute pressure. The payments revamp therefore couples fintech innovation with premium infrastructure demand.

5G Edge–Core Consolidation in City-State

Singapore’s compact landmass allows edge nodes and core data centers to operate inside the same metropolitan fiber ring. StarHub and HPE cut latency for industrial computer-vision workloads by 50% using 5G multi-access edge computing.[3]Monetary Authority of Singapore, “MAS and ABS to Establish New Payments Entity,” mas.gov.sg PSA’s Tuas Mega Port confirmed similar gains for automated guided vehicles, underscoring logistics use cases. To backhaul edge traffic, SG.GS deployed 400 G metro optics scalable to 800 G, anchoring the bandwidth needed for city-wide edge-core convergence.

ASEAN Digital-Sovereignty Initiatives

Singapore invested USD 740 million in AI governance to act as a neutral regional data steward. The Digital Connectivity Blueprint aims to double submarine-cable landings from 26 in 2023 to more than 40 by 2028, reinforcing resilience against single-point cable failures. Government clouds already host over 80% of eligible systems, demonstrating policy alignment with sovereignty objectives.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-usage caps on evaporative cooling | -2.4% | Singapore national, tropical climate regions | Short term (≤ 2 years) |

| GPU / optical-component bottlenecks | -1.6% | Global supply chain, Singapore procurement hub | Short term (≤ 2 years) |

| Carbon and heat taxes (Singapore 2024+) | -1.8% | Singapore national, policy export risk | Medium term (2-4 years) |

| Grid-draw curtailment greater than 30 MW | -1.2% | Singapore national, urban grid constraints | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water-Usage Caps on Evaporative Cooling

Singapore targets water-usage-effectiveness of 2.0 m³/MWh by 2034, effectively capping high-water evaporative chillers. Digital Realty’s tie-up with CoolestDC recorded a 29% power cut and USD 25,000 annual savings per rack after switching to liquid cooling. Smaller providers, however, often lack capital for rapid retrofit, accelerating consolidation in the Singapore hyperscale data center market.

Carbon and Heat Taxes (Singapore 2024+)

The carbon tax will rise from SGD 5 per tonne to between SGD 50 and SGD 80 by 2030, a 10-fold cost jump that reshapes site PandLs. Grants partially offset upgrades, but non-compliant operators risk eroding margin or relocating capacity. Equinix’s green-bond program shows how large incumbents front-load sustainability spend to ease future tax exposure. Operators unable to decarbonize may divert expansion to Johor or Batam, tempering near-term volume growth in the Singapore hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Commands Density Gains

In 2024, hyperscale colocation captured 59% of the Singapore hyperscale data center market share, reflecting long-standing relationships between global clouds and local facility specialists. The model remains attractive because providers like Equinix and Digital Realty deliver immediate permits, carrier-neutral connectivity, and compliance support that accelerate time-to-compute. Conversely, hyperscaler self-build is forecast to post a 15.1% CAGR through 2030 as Amazon, Google, and Microsoft pursue proprietary layouts optimized for AI liquid cooling and on-site renewable integration. The dual-track strategy underlines how the Singapore hyperscale data center market accommodates both turnkey and custom megacampus demand.

Self-build projects now emphasize vertical stacking and campus zoning to comply with land rationing. Meta’s 150 MW blueprint, the largest single-tenant site in the city-state, epitomizes mega-scale ambitions. Yet even hyperscalers retain up to 30% leased capacity to mitigate construction delays and secure multi-cloud interconnects, creating a fluid colocation–self-build mix that boosts total service depth across the Singapore hyperscale data center market.

By Component: Mechanical Infrastructure Catalyzes Innovation

Mechanical systems posted a 16.1% CAGR, outpacing all other components, as liquid and immersion cooling shifted from pilot to production. IT kits nonetheless held a 44% spending stake in 2024, driven by GPU server refresh cycles tied to generative-AI demand. Electrical topologies now feature 2N distributed redundant UPS and lithium-ion batteries that support step-load changes from high-density racks. Parallel network upgrades to 400 G and 800 G Ethernet maximize east-west traffic inside AI training clusters, anchoring the Singapore hyperscale data center market size gains in supporting infrastructure.

General-construction budgets increasingly cover recycled steel, solar façades, and low-carbon concrete to meet BCA Green Mark Platinum ratings. DCIM and AI-enabled building-management software are the fastest-rising subsegment after ST Telemedia Global Data Centres validated 10% thermal savings through real-time neural controllers.

By Tier Standard: Tier IV Drives Premium Resilience

Tier III still prevails with 66% installed capacity, delivering 99.982% uptime suited to most workloads. However, Tier IV is forecast to surge at 17.2% CAGR to 2030, propelled by real-time payments, algorithmic trading, and sovereign-cloud mandates. A 0.013-point uptime delta triggers dual-fed power, full fault-tolerance, and 24×7 remote NOC staffing, lifting capital cost by 30-40% yet ensuring regulatory compliance for critical industries. Uptime Institute awards to 1-Net North, China Mobile International Singapore 1, and multiple Equinix suites illustrate the city-state’s operational rigor. Hybrid-tier campuses hosting both Tier III and Tier IV halls in a single perimeter now dominate new blueprints, letting clients mix resilience tiers without cross-campus latency penalties

By End-User Industry: E-Commerce Accelerates Digital Transformation

Cloud and IT workloads generated 47% of 2024 demand as regional SaaS and gaming firms adopt Singapore for latency-balanced hub deployments. E-commerce, however, is projected to register a 15.7% CAGR on surging cross-border retail traffic amid Southeast Asia’s consumer-internet boom. Banking, financial services, and insurance rely on AI to cut fraud and personalize services, exemplified by DBS Bank’s 350 production-level models that cut costs by SGD 370 million. Government, manufacturing, media, and telecom segments each deepen cloud adoption through Smart Nation and Industry 4.0 policies, reinforcing base-load demand in the Singapore hyperscale data center industry.

By Data Center Size: Mega-Scale Facilities Optimize Economics

Massive sites between 25 MW and 60 MW held 50% of 2024 deployments, balancing scalability with grid-connection ease. Mega-scale campuses above 60 MW are forecast to grow at 17.5% CAGR, aided by vertical builds that raise watts per square-meter and by floating modules that circumvent land scarcity. Equinix SG6 will add 20 MW of liquid-ready IT hall capacity in a single tower, underscoring demand for concentrated high-density blocks. Operators nonetheless continue to deploy < 25 MW edge nodes near 5G clusters for latency-sensitive robotics and autonomous-vehicle use cases, adding granular points of presence that knit together the broader Singapore hyperscale data center market.

Geography Analysis

Singapore hosts more than 50 operational hyperscale facilities totaling more than 900 MW, representing roughly 55% of Southeast Asia’s installed capacity. The island’s network density, political stability, and low business-interruption risk make it the preferred landing point for 25 subsea cables. Despite intensive land use, strategic reclamation and high-rise architectures sustain new supply corridors near the eastern aviation zone.

Johor’s hyperscale corridor, situated 30 km from Singapore’s CBD, has added 1.8 GW of pipeline capacity, offering electricity tariffs up to 30% lower. The Johor-Singapore Special Economic Zone will allow renewable-power wheeling, potentially easing Singapore’s grid constraints while keeping latency sub-2 ms on dark fiber cross-links. Batam’s growth mirrors Johor’s, with Indonesian authorities marketing flexible data-sovereignty rules to multinational operators. Still, disaster recovery requirements, sovereign credit ratings, and mature interconnection ecosystems anchor core deployments within the Singapore hyperscale data center market.

Singapore differentiates by embedding climate-specific R and D into policy. The tropical data centre testbed demonstrates 18% energy savings by raising water supply temperatures to 32 °C, proving that efficient operation is achievable without compromising uptime. Mandatory carbon disclosures and granular metering create transparency that many enterprises need to meet scope-3 targets. Consequently, even as neighboring markets absorb cost-sensitive workloads, Singapore retains mission-critical and highly regulated applications.

Mordor Intelligence examines the hyperscale data center market across diverse other regional markets as well, including South America, Asia, and Europe, while also offering granular country-level perspectives for Japan, China, Chile, Hong Kong, France, and Netherlands and more.

Competitive Landscape

Global cloud platforms including AWS, Microsoft, and Google occupy self-build campuses exceeding 30 MW each, creating a moderately concentrated market. Colocation incumbents Equinix, Digital Realty, and STT GDC operate carrier-dense hubs that attract interconnect-focused enterprises. Local champions such as Keppel DC REIT and AirTrunk leverage REIT funding mechanisms to scale quickly, keeping asset turnover high within the Singapore hyperscale data center market.

Differentiation now hinges on sustainability and AI readiness. Equinix sources 100% renewable electricity and secured a 58.5 MWp solar PPA that trims 30,275 tons of CO₂ annually. Digital Realty pilots heat-recovery loops that distribute 900 kW of waste heat to adjacent horticulture facilities. SG.GS’s backbone upgrade to 800G ethernet positions it as a network fabric partner for AI cluster operators. Iron Mountain Data Centers and Lendlease Data Centre Partners expand brownfield portfolios, signaling heightened M and A activity.

REITs enhance capital efficiency. Keppel DC REIT reported Q1 2025 gross revenue of USD 102.2 million, a 22.9% uplift, driven by a 96.5% occupancy rate across 25 facilities. REIT structures lower cost of capital, enabling faster adoption of liquid-cooling retrofits. Over the next five years, participants expect asset recycling into private funds focused on edge-node development, broadening the Singapore hyperscale data center market investment universe

Singapore Hyperscale Data Center Industry Leaders

Amazon Web Services

Microsoft Corporation

Meta Platforms, Inc

Alibaba cloud

Google Cloud

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Equinix has unveiled plans for its sixth International Business Exchange data center, dubbed SG6, in Singapore, backed by an initial investment of USD 260 million. SG6 is set to bolster Singapore's data center capabilities and align with the nation's sustainability ambitions, notably the Green Plan 2030. The facility is poised to handle demanding workloads, including artificial intelligence, by leveraging renewable energy and advanced liquid cooling technologies.

- August 2024: Singtel's Digital InfraCo unit, Singtel, and Hitachi, Ltd. have inked a Memorandum of Understanding (MOU) to jointly develop next-generation data centers and a GPU Cloud in Japan, with sights set on the broader Asia Pacific region. This strategic alliance melds Singtel's vast expertise in data centers and connectivity with Hitachi's unique strengths, which encompass comprehensive data center integration, green power solutions, advanced cooling systems, robust storage infrastructure, and adept data management.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Singapore hyperscale data center market as the annual value of new-build or fully fitted facilities exceeding 4 MW of contiguous IT load that are designed for, or leased in wholesale blocks to, global cloud and social-media platforms, AI cloud providers, and similar scale-out workloads. Capacity upgrades carried out inside pre-existing hyperscale halls are included when they add incremental power or white space.

Scope exclusion: edge, enterprise, and sub-4 MW colocation suites are not part of this sizing.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- PDUs

- Switches and Switchgear

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning

- Design Engineering

- Safety and Security Systems

- DCIM / BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End Users

- By Data Center Size

- Large ( Less than or equal to 25 MW)

- Massive (Greater than 25 MW and Less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

Multiple interviews and web conferences with design consultants, liquid-cooling OEMs, power-utilities planners, and hyperscale leasing managers across Singapore, Johor, Japan, and Virginia helped us validate load-density assumptions, sustainability scorecard thresholds, and current all-in build costs. Insights from these sessions bridged gaps in desk data and steered scenario ranges.

Desk Research

Mordor analysts mined open datasets issued by agencies such as Singapore's Energy Market Authority, Infocomm Media Development Authority, and the National Environment Agency, together with customs-coded import values for servers and switchgear available in UN Comtrade and Volza shipment trackers. Trade-body white papers from the Asia Cloud Computing Association and Tier IV design filings lodged with Uptime Institute enriched architecture trends, while company 10-Ks and SGX filings revealed hyperscaler capex run rates. Paid intelligence, chiefly D&B Hoovers for tenant revenue signals and Dow Jones Factiva for project press releases, tightened our investment timelines. The sources named are illustrative; many additional publications and datasets fed our evidence base.

Market-Sizing & Forecasting

We anchored a top-down model that reconstructs total hyperscale value from grid-approved megawatt allocations and median turnkey cost per MW, then corroborated it with selective bottom-up checks on announced site pipelines and sampled contract rates. Key variables, like median rack power density, AI GPU shipment share, submarine-cable bandwidth growth, cloud spending elasticity, and Singapore's rising carbon-tax ladder, drive annual adjustments. A multivariate regression fed into an ARIMA overlay projects each variable to 2031; outliers are tempered through expert consensus gathered in primary work. Where tenant roll-ups underreport spend, proportional allocation against grid allotments closes gaps.

Data Validation & Update Cycle

Before sign-off, outputs pass anomaly screens versus CBRE vacancy benchmarks and EMA energy statistics; variances above three percentage points trigger rework. Reports refresh yearly, and material events such as new power-quota releases prompt mid-cycle revisions.

Why Our Singapore Hyperscale Data Center Baseline Commands Dependability

Published estimates seldom match because firms pick dissimilar load cut-offs, apply divergent build-cost curves, or freeze exchange rates at different points.

Key gap drivers here include: a) Mordor captures only >4 MW halls while some publishers fold in enterprise rooms; b) we factor Singapore's 1.3 PUE sustainability capex premium that others ignore; and c) our annual refresh contrasts with multi-year static baselines elsewhere, leading to sharper currency and cost updates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 366 m (2025) | Mordor Intelligence | - |

| USD 640 m (2023) | Regional Consultancy A | Includes enterprise and edge builds; older FX rates |

| USD 1.5 bn (2024) | Trade Journal B | Uses announced investment pledges, not completed capacity; excludes PUE-linked cost inflation |

In sum, by tying value strictly to live grid allocations, verified turnkey costs, and annually refreshed variables, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can readily trace and replicate.

Key Questions Answered in the Report

What is the current value of the Singapore hyperscale data center market?

The Singapore hyperscale data center market size reached USD 366.20 million in 2025 and is forecast to hit USD 848.62 million by 2031.

Which deployment model dominates Singapore’s hyperscale data centers?

Hyperscale colocation led with 59% market share in 2024, although self-build projects are growing at a 15.1% CAGR.

How fast is Tier IV capacity expanding in Singapore?

Tier IV infrastructure is projected to grow at 17.2% CAGR through 2030 due to real-time payment and financial-service demands.

Why are liquid-cooling solutions important for Singapore data centers?

AI and ML workloads push rack densities above 50 kW, and liquid cooling delivers up to 50% energy savings while meeting strict water-usage caps.

How will Singapore’s carbon tax affect data-center operators?

The tax rise from SGD 5 to up to SGD 80 per tonne by 2030 will pressure margins and speed the adoption of renewable energy and high-efficiency designs.

What role do floating data centers play in the market?

Floating modules offer 10-73 MW capacity cooled by seawater, helping expand supply despite land constraints and qualifying for green-capacity quotas.

Page last updated on: