Malaysia Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

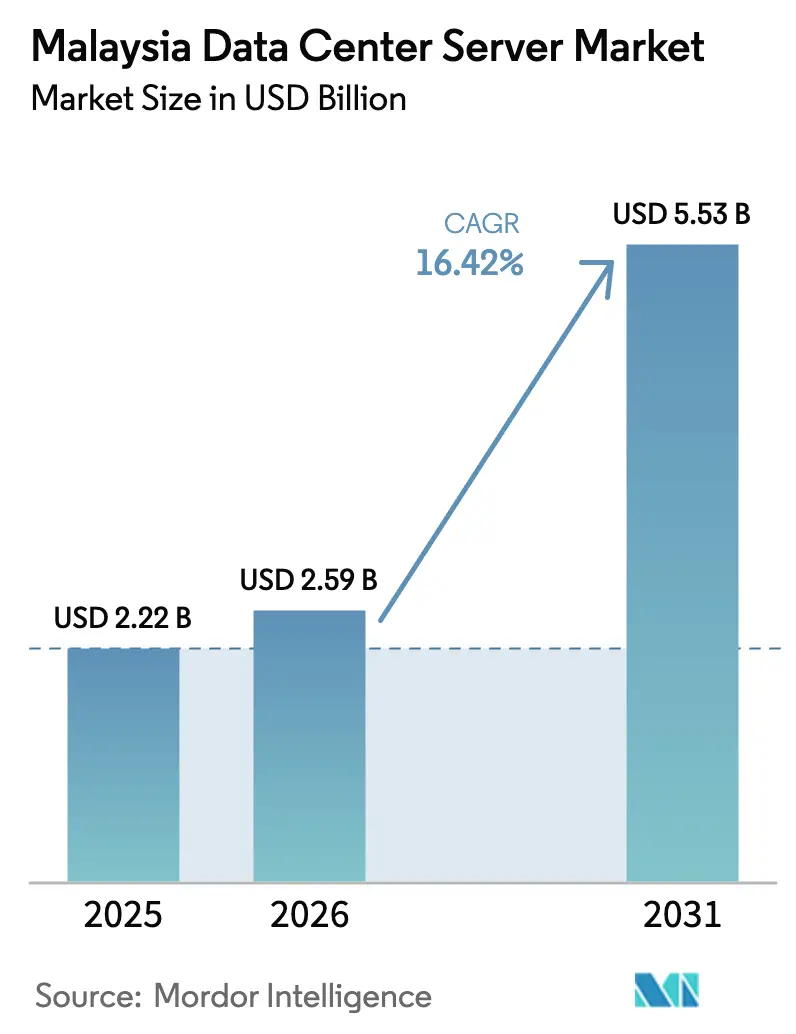

| Base Year Market Size (2025) | USD 2.22 Billion |

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 5.53 Billion |

| Growth Rate (2026 - 2031) | 16.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Data Center Server Market Analysis by Mordor Intelligence

The Malaysia data center server market size was valued at USD 2.22 billion in 2025 and estimated to grow from USD 2.59 billion in 2026 to reach USD 5.53 billion by 2031, at a CAGR of 16.42% during the forecast period (2026-2031). Growing hyperscale footprints, a national cloud-first mandate, and targeted renewable-energy incentives are invigorating server refresh cycles, particularly for high-density AI configurations. Johor’s rapid rise to 1.6 GW of live capacity, favourable land prices, and streamlined permitting make the state the focal point for new server installations. Concurrently, electricity-tariff reforms elevate power-efficiency considerations, sharpening vendor competition around performance-per-watt. Finally, ongoing submarine-cable projects strengthen Malaysia’s role as an interconnection hub, driving incremental server demand for content caching and traffic transit.

Key Report Takeaways

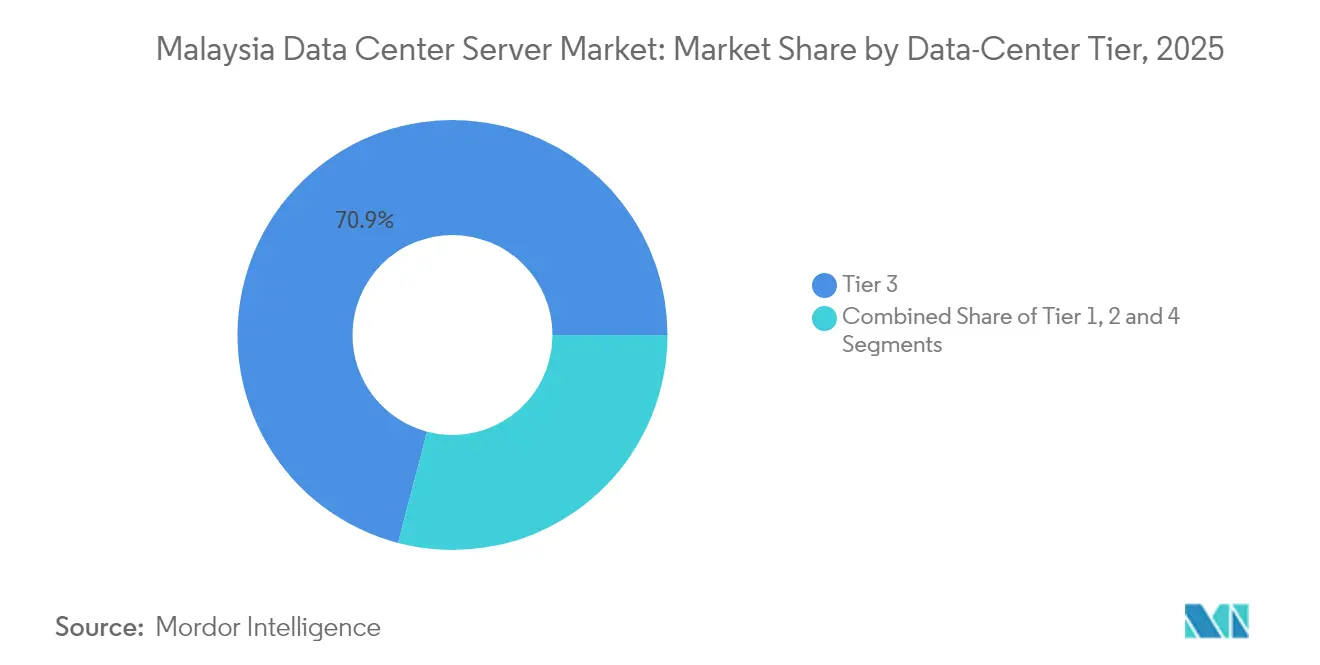

- By data-center tier, Tier 3 facilities held 70.92% of Malaysia's data center server market share in 2025, while Tier 4 is advancing at an 18.33% CAGR through 2031.

- By form factor, half-height blades led with 62.54% revenue share in 2025; quarter-height micro-blades are projected to expand at a 16.61% CAGR to 2031.

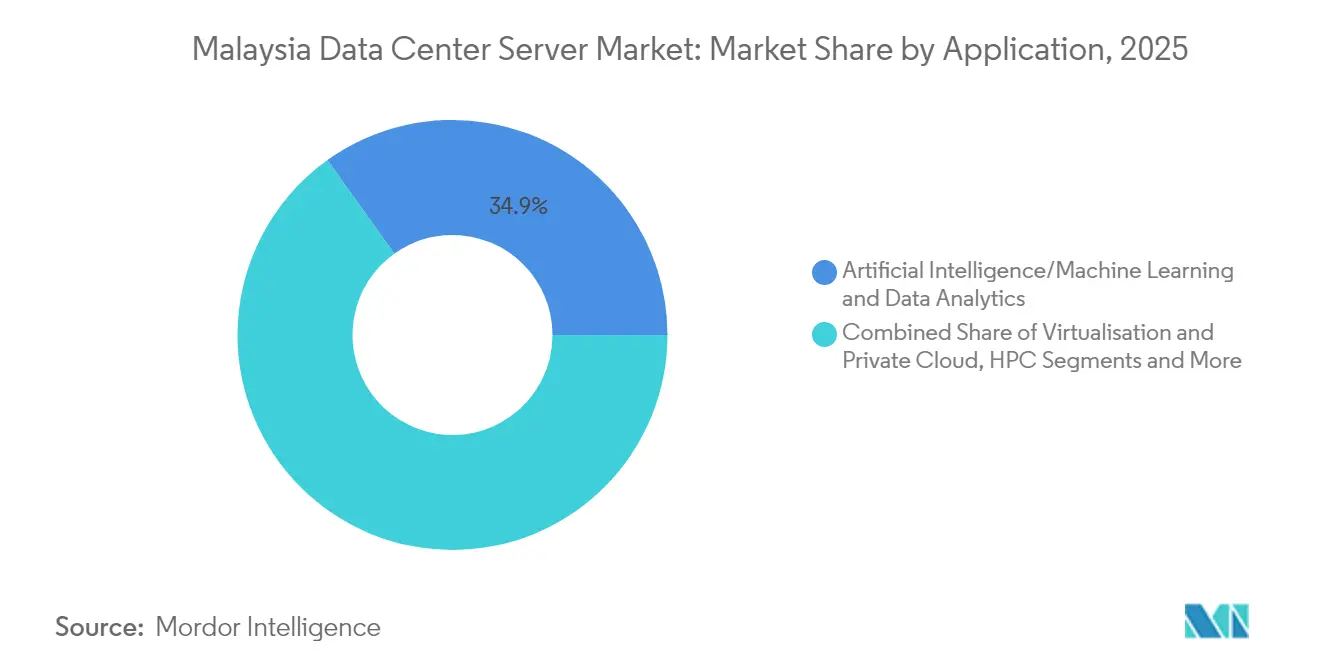

- By application, AI/ML workloads accounted for 34.88% of the Malaysia data center server market size in 2025 and command the highest absolute spending; virtualization and private-cloud workloads are the fastest-growing at 16.94% CAGR to 2031.

- By data-center type, colocation sites captured 56.62% of the Malaysia data center server market size in 2025, whereas hyperscaler deployments are growing at an 18.21% CAGR.

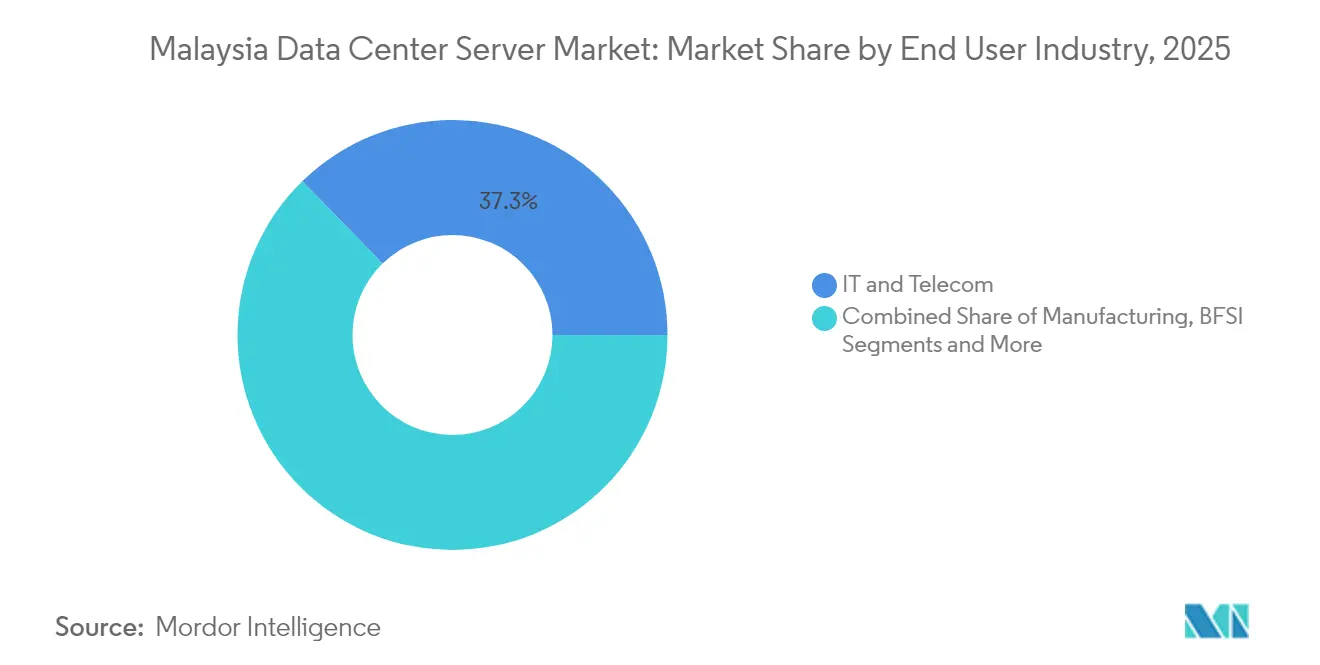

- By end-use industry, IT & telecom led with 37.32% revenue share in 2025; manufacturing and Industry 4.0 workloads are forecast to post a 17.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Understanding the full system requires moving beyond Malaysia boundaries into a wider international view. Mordor Intelligence captures the global data center server market scope in its worldwide coverage.

Malaysia Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscale & colocation data-center investments | +4.2% | National, concentrated in Johor and Selangor | Medium term (2-4 years) |

| Expansion of internet infrastructure and new submarine cables | +2.8% | National, with spillover to ASEAN region | Long term (≥ 4 years) |

| Government cloud-first & Digital Economy incentives | +3.1% | National, early gains in Cyberjaya and Putrajaya | Short term (≤ 2 years) |

| Rising adoption of cloud, AI/ML & IoT-driven workloads | +3.9% | Global demand, localized in Malaysia | Medium term (2-4 years) |

| Entry of sovereign-fund-backed edge micro-hubs in Tier-2 cities | +1.7% | Regional, focusing on Penang, Johor Bahru, Kuching | Long term (≥ 4 years) |

| Introduction of 2026 green-tax credit for high-efficiency servers | +1.3% | National, with early adoption in major facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Hyperscale & Colocation Data-Center Investments

Major cloud providers pledged more than USD 15 billion in 2024 alone, led by Google’s USD 2 billion first Malaysian region in Greater Kuala Lumpur and Microsoft’s three-site rollout scheduled for Q2 2025.[1]Google Cloud, “Google Announces First Malaysia Cloud Region,” cloud.google.comJohor’s comparative land affordability and close distance to Singapore accelerate campus-scale builds such as Vantage’s 256 MW Cyberjaya complex and Princeton Digital Group’s 150 MW AI-ready JH1 site. The resulting spike in rack demand concentrates orders for liquid-cooled GPU servers optimized for AI inference, reinforcing the Malaysia data center server market.

Government Cloud-First & Digital-Economy Incentives

The MyDIGITAL blueprint targets a 22.6% GDP share from digital activities by 2025 and requires 80% of public-sector workloads to migrate to hybrid cloud environments.[2]The Edge Markets, “TNB Tariff Hike and Data-Center Impact,” theedgemarkets.com Conditional approvals worth RM 12-15 billion allow hyperscalers to build locally, while the Cloud Framework Agreement steers procurement toward domestic partners. Ministries upgrading from legacy three-tier stacks to hyper-converged architectures report faster data access and stronger resiliency, cementing ongoing server refresh cycles.

Rising Adoption of Cloud, AI/ML and IoT-Driven Workloads

AI/ML already consumes 35.3% of server cycles, propelled by Malaysia’s roll-out of a sovereign AI stack based on Huawei Ascend chips and an in-country large-language-model program. Nvidia’s USD 4.3 billion venture with YTL Power adds GPU-dense clusters that draw over 40 kW per rack, making liquid cooling a necessity. Smart-hospital deployments and nationwide MEC pilots further diversify load profiles, encouraging purchases of edge-specific micro-blades designed for low-latency processing.

Expansion of Internet Infrastructure and New Submarine Cables

Malaysia’s participation in SEA-ME-WE 6 and other cable systems strengthens its interconnection profile, creating server demand for transit traffic and CDN nodes.[3]Submarine Networks, “SEA-ME-WE 6 Cable Route Update,” submarinenetworks.comTelekom Malaysia’s fiber expansion and DE-CIX’s peering fabric enhance route diversity and drive purchases of high-throughput network servers needed for traffic aggregation

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx for facility & server procurement | -2.1% | National, particularly affecting SME adoption | Short term (≤ 2 years) |

| FX-linked cost risk from imported hardware | -1.8% | National, with higher impact on price-sensitive segments | Medium term (2-4 years) |

| 2027 electricity-tariff reform cutting industrial subsidies | -2.3% | National, concentrated in energy-intensive facilities | Medium term (2-4 years) |

| Land scarcity in Greater Kuala Lumpur inflating real-estate costs | -1.4% | Regional, primarily affecting Klang Valley developments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

2027 Electricity-Tariff Reform Cutting Industrial Subsidies

TNB lifted the base tariff 14.2% to 45.62 sen/kWh from July 2025, while future fuel-cost pass-throughs compound uncertainty. Data-center loads could constitute 38.37% of peak-demand growth by 2030, so operators now prioritise server models with higher performance-per-watt and explore direct renewable-energy contracts under CRESS.[4]U.S. Department of Commerce, “Corporate Renewable Energy Supply Scheme Explained,” trade.gov Vendors offering liquid-cooled, high-efficiency systems stand to benefit.

High CapEx for Facility & Server Procurement

Advanced AI servers such as Nvidia’s GB300 NVL72 can cost between USD 3.7-4 million per node, while liquid-cooling retrofits add up to 30% to build costs. Semiconductor tightness prolongs lead times, pushing some buyers to dual-source from Taiwanese ODMs setting up Johor factories. Green financing—exemplified by Princeton Digital’s USD 280 million sustainability-linked loan—offers partial relief but not enough to offset capital barriers for smaller entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Tier: Mission-Critical Tier 4 Drives Growth

Tier 3 facilities dominated the Malaysia data center server market share at 70.92% in 2025, supported by banking, telecom, and public-sector workloads that demand high availability. Parallelly, Tier 4 sites are outpacing overall growth at an 18.33% CAGR, reflecting hyperscaler insistence on five-nines uptime for AI training clusters. Vantage’s Cyberjaya and Princeton Digital’s JH1 campuses exemplify the Tier 4 blueprint, featuring redundant power and chilled-water loops to sustain racks exceeding 70 kW.

The Malaysia data center server market is thus bifurcating: Tier 1-2 footprints meet edge and disaster-recovery needs, whereas Tier 3-4 facilities capture long-term, mission-critical demand. Tier 4’s momentum also aligns with the 2026 green-tax credit that rewards high-efficiency hardware, nudging enterprises toward the latest processor generations and cooling techniques.

By Form Factor: Micro-Blades Gain Edge-Computing Traction

Half-height blades held 62.54% revenue in 2025 courtesy of their familiarity, balanced thermals, and integration ease into legacy racks. Yet quarter-height micro-blades are expanding at a 16.61% CAGR, propelled by 5G backhaul rollouts and regional MEC nodes that require compact, ruggedised servers. Intel’s 5G Digital School venture in Penang showcases micro-blade edge clusters providing AI-enabled educational content with minimal latency.

Within hyperscale halls, full-height blades and GPU trays dominate AI training, but operators simultaneously procure micro-blades for latency-sensitive inference tasks. Consequently, server vendors increasingly market unified chassis able to host mixed-blade heights, lowering spares inventories and accelerating deployment—an advantage in Malaysia data center server market procurement cycles.

By Application/Workload: AI Dominance Reshapes Server Requirements

Artificial-intelligence workloads captured 34.88% of the Malaysia data center server market size in 2025 as sovereign-AI investments converged with private-sector adoption. NVIDIA-Blackwell-based racks slated for late-2025 delivery will intensify GPU attachment ratios, driving power densities past 40 kW per rack. Virtualization and private-cloud stacks nevertheless register the quickest 16.94% CAGR, fuelled by enterprises modernising ERP and productivity suites.

Smart hospitals, industrial IoT, and BFSI analytics join the demand queue, dictating heterogeneous server fleets blending GPU-rich, CPU-dense, and storage-heavy nodes. This workload mix shifts purchasing priorities toward configurable motherboards, higher memory bandwidth, and front-serviceable NVMe drives that enhance uptime in Malaysia data center server market deployments.

By Data-Center Type: Hyperscalers Accelerate Market Transformation

Colocation operators retained 56.62% of the Malaysia data center server market size in 2025, offering enterprises scale minus ownership risks. Hyperscalers, however, are marching at an 18.21% CAGR as Google, Microsoft, Oracle, and Chinese cloud giants secure multibillion-dollar land banks around Johor and Cyberjaya. Dedicated halls outfitted for liquid cooling, single-phase immersion, and 21-inch OCP racks make hyperscaler campuses the bellwether for next-generation server specs.

Edge and enterprise self-builds continue in verticals such as manufacturing where low-latency control loops are mission-critical. The coexistence of colocation and hyperscale footprints creates a layered market structure in which vendors must cater simultaneously to turnkey colocation SKUs and highly customised hyperscale bill-of-materials.

By End-Use Industry: Manufacturing Digitisation Drives Server Demand

IT & telecom remained top buyers with 37.32% share in 2025, investing in NFV, 5G core, and content-delivery nodes. Manufacturing workloads tied to Industry 4.0 and predictive-maintenance initiatives are forecast to climb 17.21% CAGR as semiconductor fabs, E&E clusters, and automotive suppliers adopt AI-powered quality control. Malaysia’s social-security agency PERKESO’s shift to Red Hat platforms illustrates how public services reduce manual processes and increase online interaction for citizens.

Healthcare posts double-digit growth through telehealth and smart-hospital roadmaps, while BFSI continues to refresh servers for real-time fraud analytics and open-banking APIs. Government ministries, under MyDIGITAL, increasingly stipulate domestic data-residency, thereby channeling fresh spend into local server halls.

Geography Analysis

Johor dominates new-build momentum, courtesy of abundant land and a one-stop approval desk that shortens project timelines. Mega-campuses from ByteDance, Microsoft, and Oracle substantiate the region’s transition from manufacturing hub to global digital-infrastructure node. Larger parcels also permit on-site solar arrays and battery-energy storage, aligning with ESG mandates.

Selangor, anchored by Cyberjaya and Greater Kuala Lumpur, remains Malaysia’s flagship data-center corridor. High dark-fiber density and proximity to governmental agencies keep utilisation high, though land scarcity inflates plot prices and nudges expansions toward the fringes of Klang Valley. Sustainability programs aimed at achieving carbon neutrality by 2030 attract operators seeking credible green-power pathways.

Penang, Sarawak, and other Tier-2 cities emerge as edge-centric zones. Penang leverages its semiconductor ecosystem to pilot low-latency education and industrial IoT workloads, while Sarawak’s first wholesale facilities cater to Borneo’s connectivity uplift. Lower real-estate costs and fresh renewable-energy potential open the door for sovereign-fund micro-hubs that feed regional redundancy needs.

Mordor Intelligence examines the data center server market across diverse other regional markets as well, including Americas, Europe, and Asia, while also offering granular country-level perspectives for Singapore, Japan, Brazil, Switzerland, Hong Kong, and South Africa and more.

Competitive Landscape

Competition is moderate. Dell Technologies, Hewlett-Packard Enterprise, and Cisco Systems still command large enterprise refresh cycles. Yet AI workloads grant share gains to Supermicro, Wiwynn, and other ODMs that offer GPU-dense, liquid-ready chassis at aggressive lead times.

Chinese vendors Huawei, Inspur, and Lenovo gain traction through cost-advantaged offers and local assembly commitments, dovetailing with Malaysia’s sovereign-AI agenda. Nvidia’s reference designs influence BOM choices among hyperscalers, pushing x86 CPU vendors toward accelerator-friendly motherboards.

Supply-chain localisation intensifies: Wiwynn’s Johor plant and potential module lines from Inventec lower shipping costs and buffer geopolitical risk for operators sourcing servers in Malaysia data center server market deployments. Energy-efficiency regulations further shape vendor line-ups, rewarding those who meet next-gen performance-per-watt thresholds.

Malaysia Data Center Server Industry Leaders

Dell Technologies

Hewlett Packard Enterprise

Cisco Systems

Huawei Technologies

Lenovo Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Malaysia unveiled a sovereign full-stack AI platform built on Huawei Ascend, targeting deployment of 3,000 GPUs by 2026

- March 2025: Nvidia launched the Blackwell Ultra AI Factory platform, shipping GB300 NVL72 racks via partners in H2 2025.

- March 2025: Microsoft Malaysia confirmed three data centers launching by Q2 2025.

- February 2025: Vantage Data Centers broke ground on a 256 MW Cyberjaya campus.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study describes the Malaysia data-center server market as all new x86 and non-x86 compute nodes, rack, blade, micro-blade, and tower, deployed inside colocation, hyperscale, enterprise, and edge facilities across the country. Revenue is captured at factory gate in USD and excludes refurbished hardware and white-box boards shipped for non-data-center use.

Scope exclusions, networking switches, storage arrays, and services are not counted.

Segmentation Overview

- By Data-Center Tier

- Tier 1 and 2

- Tier 3

- Tier 4

- By Form Factor

- Half-height Blades

- Full-height Blades

- Quarter-height / Micro-blades

- By Application / Workload

- Virtualisation and Private Cloud

- High-Performance Computing (HPC)

- Artificial Intelligence/Machine Learning and Data Analytics

- Storage-centric

- Edge / IoT Gateways

- By Data Center Type

- Hyperscalers/Cloud Service Provider

- Colocation Facilities

- Enterprise and Edge

- By End-use Industry

- BFSI

- IT and Telecom

- Healthcare and Life-Sciences

- Manufacturing and Industry 4.0

- Energy and Utilities

- Government and Defence

- Other End Users

Detailed Research Methodology and Data Validation

Primary Research

Across two recruitment waves, we interviewed regional facility operators, OEM product managers, and procurement leads from BFSI, telecom, and manufacturing clusters in Klang Valley, Johor, and Penang. These conversations clarified live rack densities, GPU attach rates, and average refresh cycles, letting us tighten cost-per-unit curves and validate shipment estimates derived from secondary data.

Desk Research

Mordor analysts began with public datasets from the Malaysian Communications and Multimedia Commission, Department of Statistics Malaysia trade tables (HS 8471), the Energy Commission's data-center power disclosures, and customs import alerts for server chassis. We layered in association insights from the Malaysia Digital Economy Corporation, the Asia Cloud Computing Association, and peer-reviewed work on hyperscale build-outs published in IEEE Xplore. Company filings, prospectuses, and investor decks helped anchor purchase prices, while news archives on Dow Jones Factiva and financial snapshots from D&B Hoovers supplied vendor revenue splits. The sources cited here illustrate, not exhaust, the wider desk-research pool our team reviewed to ground assumptions.

Market-Sizing & Forecasting

A top-down construct starts with national IT-load capacity in megawatts, reconciling MCMC licensed power, import volumes, and average watts-per-server to back-calculate unit demand. Select bottom-up checks, OEM sell-in by channel and sampled ASP × volume, temper the totals before final reconciliation. Key variables inside the model include planned hyperscale capex pipeline, average rack density (kW/rack), server price erosion, GPU penetration share, import tariff movements, and sectoral demand indices. Multivariate regression with ARIMA overlays projects each driver forward to 2030, and scenario bands are stress-tested with our primary-research panel. Assumption gaps, such as missing edge-site shipments, are patched with conservative proxy ratios drawn from adjacent ASEAN markets.

Data Validation & Update Cycle

Outputs pass three-layer scrutiny, automated variance flags, peer review, and lead-analyst sign-off. Before every annual refresh, we revisit major OEMs and power utilities; extraordinary events, for example, a fresh hyperscale campus approval, trigger an interim update so clients receive the most current view.

Why Mordor's Malaysia Data Center Server Baseline Commands Reliability

Published estimates diverge because firms pick different form-factor mixes, price points, and refresh cadences.

Key gap drivers include whether tower servers for enterprise closets are counted, if integrated services are bundled, currency translation timing, and how fast price erosion is modeled for AI-ready nodes. Our cadence, annual refresh with mid-cycle triggers, and our explicit exclusion of services reduce volatility others often embed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.22 B | Mordor Intelligence | - |

| USD 2.16 B (2024) | Global Consultancy A | Uses prior year as proxy, blends storage hardware, applies single ASP across all tiers |

| USD 5.80 B (2025) | Industry Analytics B | Bundles server integration services and power shells, counts in-flight purchase orders, no price erosion curve |

In sum, our disciplined scope, dual-track validation, and timely refreshes give decision-makers a balanced baseline that is traceable, reproducible, and free from hidden inclusions others may carry.

Key Questions Answered in the Report

What is the current size and growth outlook for the Malaysia data center server market?

The market stands at USD 2.59 billion in 2026 and is projected to reach USD 5.53 billion by 2031, registering a 16.42% CAGR over the forecast period.

Which workloads are driving the highest demand for servers in Malaysia?

AI and machine-learning workloads lead with 34.88% share in 2025, while virtualization and private-cloud workloads are the fastest-growing at a 16.94% CAGR through 2031.

Why is Johor emerging as Malaysia’s primary data-center hub?

Johor offers lower land costs, streamlined approvals, and proximity to Singapore, helping it reach 1.6 GW live capacity and making it the focal point for hyperscale projects.

What government incentives support continued server investment?

The MyDIGITAL cloud-first policy, green tax credits for high-efficiency servers starting 2026, and the Corporate Renewable Energy Supply Scheme collectively encourage sustained infrastructure upgrades.

Page last updated on: