Taiwan Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

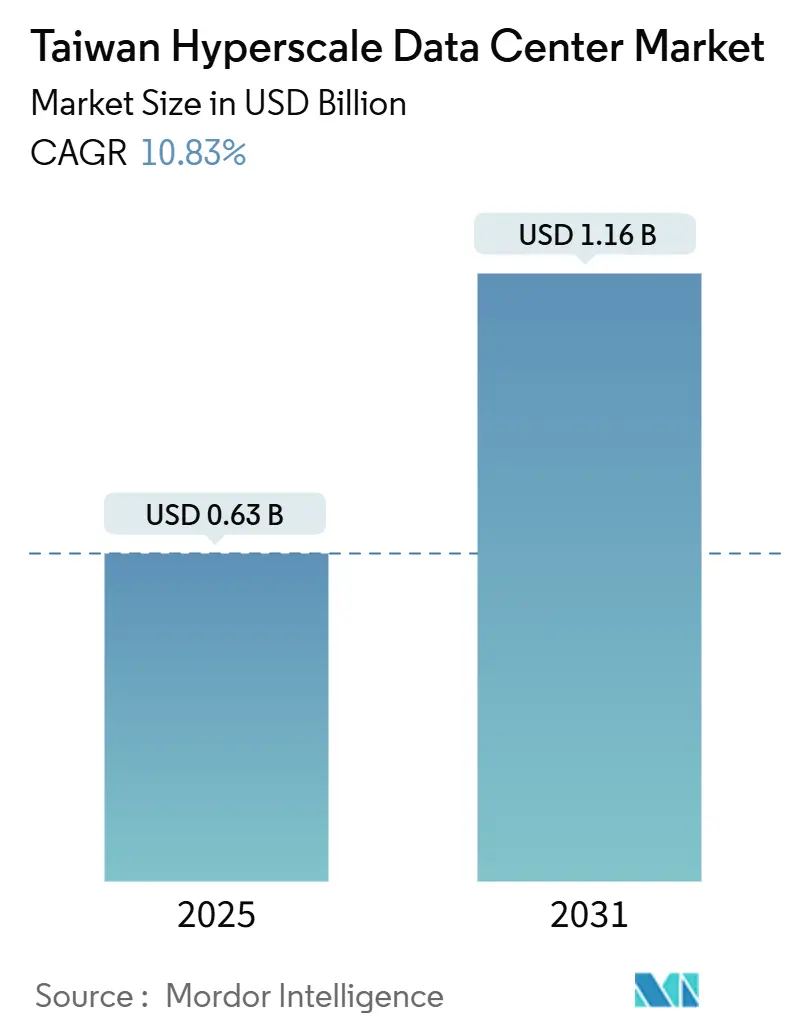

| Market Size (2025) | USD 0.63 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2025 - 2031) | 10.83% CAGR |

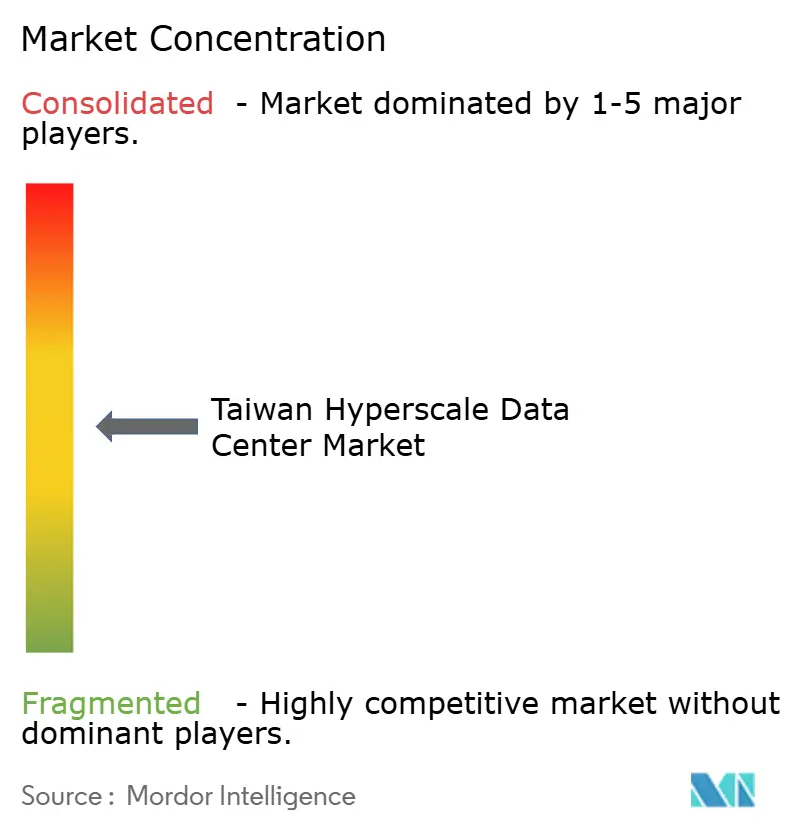

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Hyperscale Data Center Market Analysis by Mordor Intelligence

The Taiwan hyperscale data center market size stood at USD 626.32 million in 2025 and is forecast to expand to USD 1,160.55 million by 2031 at a 10.83% CAGR, accompanied by installed IT load growth from 344.91 MW to 660.75 MW. Taiwan’s position at the crossroads of Asia-Pacific subsea cables, its sovereign artificial-intelligence programs, and more than USD 5 billion of hyperscaler commitments underpin this trajectory. Hyperscaler self-build facilities dominate current capacity, yet liquid-cooled colocation suites aimed at GPU clusters are scaling rapidly. Green-energy power-purchase agreements, real-time payment regulations, and semiconductor industry synergies are reshaping site-selection logic and facility design. Operators are adopting modular construction, direct-to-chip cooling, and battery storage to navigate power-grid caps, water-recycling mandates, and persistent GPU supply shortages

Key Report Takeaways

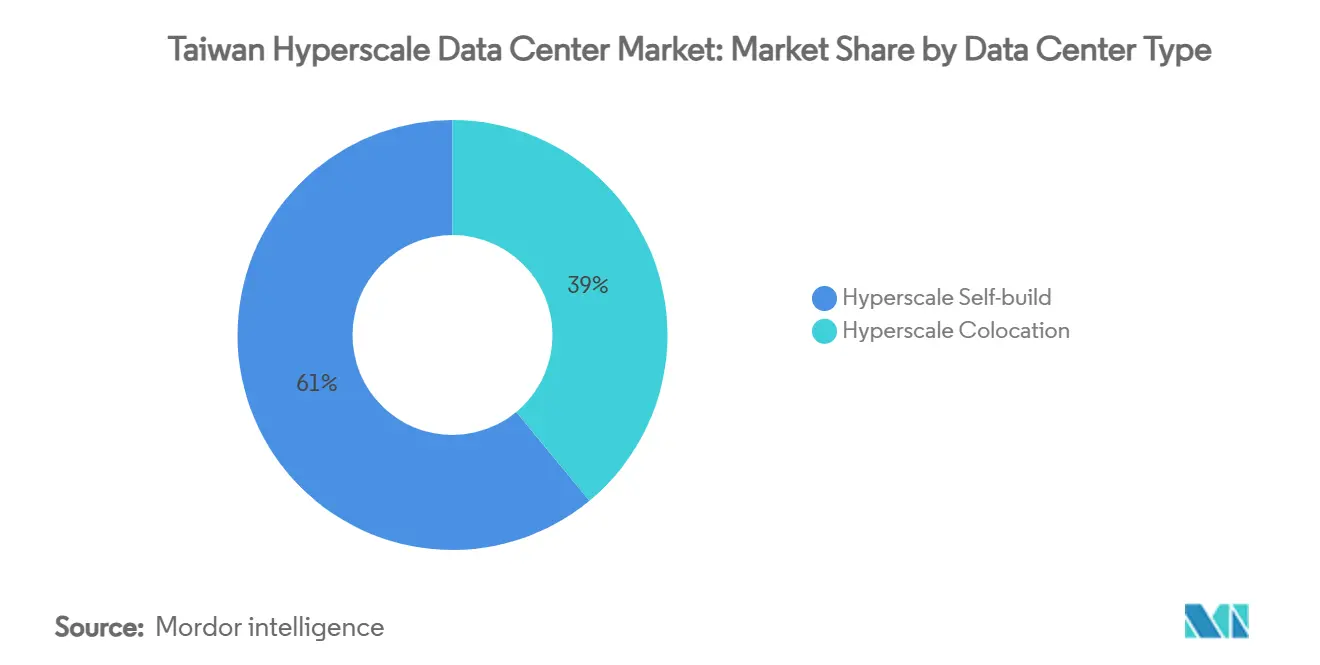

- By data center type, hyperscale self-builds led with 61% of the Taiwan hyperscale data center market share in 2024, while hyperscale colocation is projected to grow at 21.40% CAGR through 2031.

- By component, IT infrastructure accounted for 43.50% of the Taiwan hyperscale data center market spending in 2024; liquid-cooling systems are advancing at a 32.80% CAGR.

- By tier standard, Tier III facilities captured 68% share of the Taiwan hyperscale data center market size in 2024; Tier IV nodes are expanding at an 18.20% CAGR.

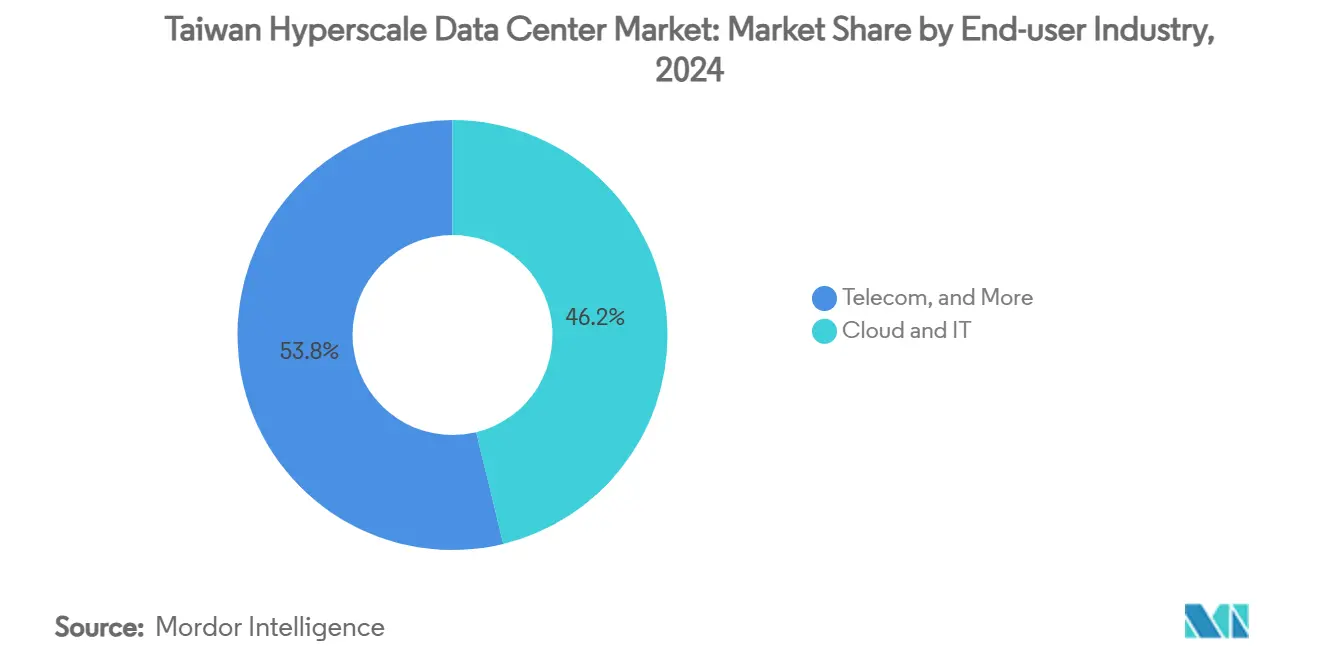

- By end-user industry, cloud and IT services represented 46.20% share of the Taiwan hyperscale data center market in 2024, while AI start-ups are set to post a 27.60% CAGR.

- By data center size, massive (greater than 25 MW and less than or equal to 60 MW) facilities commanded a 49.70% share of the Taiwan hyperscale data center market size in 2024, and mega (greater than 60 MW) sites are projected to grow at a 24.90% CAGR.

Worldwide industry scale is not derived from any single country or region but from the combination of national and regional inputs. The hyperscale data center market size of Mordor Intelligence integrates these into one global valuation.

Taiwan Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding GPU-centric AI/ML workloads (Greater than 50 kW racks) | +2.80% | Global, concentrated in Taipei-Taoyuan, Hsinchu-Miaoli | Medium term (2-4 years) |

| Rapid rollout of sovereign-cloud zones by U.S. hyperscalers | +2.10% | National, with early gains in Taipei-Taoyuan, Taichung-Changhua | Short term (≤ 2 years) |

| Government incentives on green-energy PPAs for new builds | +1.40% | National, strongest in Taichung-Changhua, Tainan-Kaohsiung | Long term (≥ 4 years) |

| Taiwan-wide real-time payment mandate driving Tier IV nodes | +1.20% | National, concentrated in financial districts | Medium term (2-4 years) |

| GenAI inference campuses requiring liquid-cooling clusters | +1.80% | Global, focused on major city clusters | Short term (≤ 2 years) |

| Surplus 5G-edge telco space converted to hyperscale core | +0.90% | National, urban concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exploding GPU-centric AI/ML Workloads Drive Infrastructure Transformation

GPU racks exceeding 50 kW are increasing average power density fourfold compared to legacy enterprise deployments. Direct-to-chip liquid cooling is attaining sub-1.33 PUE levels in production facilities.[1] Taiwan’s server ODMs, such as Foxconn, are shipping AI systems ata 60% year-on-year growth rate, yet TSMC’s advanced CoWoS packaging capacity remains fully booked through 2025, delaying GPU deliveries and forcing phased fit-outs. Hyperscale layout standards are shifting toward GPU ‘pods’ clustered around shared coolant manifolds, and facility planners now reserve 40-50% of floor area for auxiliary power and thermal equipment. The workload surge solidifies Taiwan’s role as both a semiconductor foundry and a sovereign AI computing hub. Converging chip production and data-center demand are attracting upstream suppliers of liquid cold plates, immersion tanks, and fluorinated coolants.

Rapid Rollout of Sovereign-Cloud Zones Accelerates Market Growth

AWS, Microsoft, and Google are deploying sovereign cloud zones that meet Taiwan’s data-localization rules without ceding operational control, creating hybrid facilities with isolated control planes and dedicated key-management systems.[2] AWS has earmarked three availability zones for early-2025 launch, each designed for Tier IV fault tolerance. This model satisfies cybersecurity regulations while supplying the low-latency links that local enterprises need for AI training and inference. Sovereign zones are also positioned as springboards for serving regulated workloads across emerging Asia-Pacific markets with similar residency laws. Linux-based confidential-computing stacks, hardware-root-of-trust modules, and AI-specific accelerators are standard features, reinforcing demand for specialized GPU colocation halls.

Government Green-Energy Incentives Reshape Power Procurement Strategies

Taiwan’s net-zero roadmap compels data-center operators to source 30% renewable energy by 2024 and 80% by 2028. Google’s 500 MW offshore-wind PPA in central Taiwan exemplifies the long-term contracts hyperscalers are signing to lock in clean electricity. Location decisions increasingly prioritize sub-stations close to wind-farm landing points, prompting a southward shift of new builds toward Taichung–Changhua. Battery energy-storage systems are being dimensioned for 2-hour discharge windows to buffer wind variability, and some operators are experimenting with micro-nuclear feasibility studies. Renewable mandates are therefore catalyzing investments in advanced energy-management software, high-efficiency rectifiers, and grid-interactive UPS systems

Taiwan-wide Real-Time Payment Mandate Drives Tier IV Demand

The island-wide instant-payment system requires financial transactions to clear within 10 seconds at 99.995% uptime. Banks have responded by migrating payment engines to Tier IV hyperscale nodes equipped with dual utility feeds, concurrently maintainable cooling loops, and geographically diverse recovery sites. The regulation is stimulating retrofit projects that upgrade legacy Tier III halls to full fault tolerance, boosting demand for switchgear, generators, and isolation valves. Financial firms are doubling their leased power footprints to house low-latency analytics clusters that detect fraud in real time. The payment mandate is also driving AI-enabled risk models, creating incremental GPU demand inside the same Tier IV envelopes

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic GPU / optical-transceiver supply bottlenecks | -2.30% | Global supply chain, Taiwan assembly | Medium term (2-4 years) |

| Tight water-usage rules for evaporative cooling | -1.60% | National, acute in Northern Taiwan | Short term (≤ 2 years) |

| Rising carbon-tax pilot in Northern Taiwan industrial parks | -0.80% | Northern Taiwan industrial parks | Medium term (2-4 years) |

| Local-grid draw cap of greater than 30 MW in Hsinchu Science Park | -0.70% | Hsinchu Science Park, spillover to adjacent areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight Water-Usage Rules Constrain Traditional Cooling Methods

Mandatory 30% water-recycling thresholds introduced in 2024 and rising to 80% by 2028 have rendered open-loop evaporative towers economically unviable for new hyperscale data centers. Northern sites now pay tiered fees per cubic meter once the monthly draw exceeds 9,000 m³, pressuring operators to adopt closed-loop liquid systems and adiabatic dry coolers. These alternatives reduce water draw by up to 40% but increase capital costs and require larger heat-exchanger footprints.[3] Technical skill shortages in fluid handling and corrosion control create integration risks, while semiconductor fabs compete for the same recycled water streams. The constraint is prompting the co-location of data centers with wastewater treatment plants and the wider uptake of heat-recovery chillers that feed nearby district heating loops.

Chronic GPU and Optical-Transceiver Supply Bottlenecks Limit Expansion

Lead times for NVIDIA H100 and upcoming H200 boards exceed six months due to advanced packaging bottlenecks and shortages of high-bandwidth memory. Spot prices are often 50% above the list, forcing operators to stagger rack energization and inflate working capital budgets. Shortfalls extend to 400G and 800G optical modules, with Taiwanese suppliers ramping up production but still facing a 1.45 million-unit backlog. Earthquake-related disruptions and geopolitical risks further accentuate the vulnerability of localized packaging clusters. Operators mitigate this by multi-sourcing accelerators, placing non-cancelable orders, and provisioning advance transceiver inventory in bonded warehouses; however, construction timelines nevertheless slip, and financing costs rise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Gains Traction against Self-Build Dominance

Self-build campuses controlled 61% of the Taiwan hyperscale data center market share in 2024 as global cloud firms optimized custom layouts for AI workloads. In value terms, the segment added USD 5 billion of cumulative investment commitments through 2025. The Taiwan hyperscale data center market size for colocation, however, is set to expand at 21.40% CAGR as enterprises seek rapid, capex-light access to GPU clusters. Colocation providers are differentiating through sovereign-cloud compliance zones, on-site renewable PPAs, and sub-1.33 PUE guarantees. Strategic alliances such as Taiwan Mobile and Vantage Data Centers combine telco fiber backbones with global colocation design playbooks. Revenue models are shifting toward high-density per-rack pricing, while service catalogs now include managed Kubernetes, model-training sandboxes, and inter-campus cloud fabrics.

The Taiwan hyperscale data center industry also witnesses telecom incumbents converting underutilized 5G edge shelters into regional core nodes that backhaul traffic to hyperscale colocation hubs. Such hybrid topologies lower latency for AI inference at the last mile and improve asset monetization of legacy telco estates. Colocation’s growth is constrained by grid connection queues and land scarcity in Greater Taipei, so operators increasingly pre-lease space in central and southern science parks where renewable capacity is abundant. Investor confidence is seen in the first greenfield project financing for hyperscale colocation executed in 2024, signaling maturing capital-market appetite for long-dated data-infrastructure assets.

By Component: Liquid-Cooling Systems Surge within Hardware-Dominant Spend

IT hardware captured 43.50% of 2024 spend, reflecting USD 200,000 plus price tags for fully-populated 8-GPU servers. The Taiwan hyperscale data center market size allocated to mechanical and cooling systems is climbing rapidly, with liquid-cooling solutions forecast to grow at 32.80% CAGR. Operators pivot to direct-to-chip plates, rear-door exchangers, and immersion baths to support 50-100 kW racks. Liquid loops reduce hot-aisle delta-T, enabling higher chip clocks and improved energy efficiency. Electrical systems remain core, with integrated-busway power distribution and 98%-efficient UPS topologies supporting Tier IV redundancy requirements. Commoditized air handlers are being displaced by coolant distribution units and smart leak-detection arrays.

Supply-chain realignment favors Taiwanese ODMs that bundle servers, coolant manifolds, and power skids into factory-integrated modules. Component demand also encompasses high-speed fiber, silicon photonics switches, and precision environmental sensors. The Taiwan hyperscale data center industry is therefore evolving toward a vertically integrated supply ecosystem where OEMs, component vendors, and construction contractors collaborate on design-for-manufacture principles.

By Tier Standard: Tier IV Ascends alongside Established Tier III Base

Tier III halls accounted for 68% of installed capacity in 2024, delivering N+1 redundancy suited to general cloud workloads. Regulatory trends, however, push mission-critical applications into Tier IV nodes that guarantee 99.995% availability. Tier IV’s 18.20% CAGR is anchored by fintech and real-time payment mandates and by AI inferencing for fraud analytics that cannot tolerate downtime. The Taiwan hyperscale data center market size tied to Tier IV is further buoyed by sovereign-cloud zones demanding physically separate and concurrently maintainable power and cooling paths. Operators justify higher capital intensity through premium pricing and multi-year take-or-pay contracts with banks and ministries.

Tier-IV builds emphasize fault-tolerant switchgear, cross-campus dark-fiber rings, and 2N mechanical infrastructure. Adoption of modular prefabricated power rooms accelerates time to market and simplifies maintenance. As Tier IV footprints expand, some providers retain a blended portfolio of Tier III and Tier IV halls within the same campus to match workload criticality with appropriate cost structures.

By End-User Industry: AI Start-Ups Outpace Core Cloud Segment

Cloud and IT services contributed 46.20% of 2024 revenue as international hyperscalers and domestic IaaS vendors provisioned mainstream enterprise workloads. The Taiwan hyperscale data center market size serving AI start-ups is projected to rise at 27.60% CAGR, gaining government fund that subsidizes domestic AI research. Start-ups require burstable GPU capacity and favor opex pricing, driving up demand for shared colocation pods. Telecom operators are embedding AI in network-operations analytics and customer-experience engines, converting legacy central offices to mini-data centers. Government demand stems from smart-city projects and language-model initiatives under the TAIDE program. BFSI institutions anchor Tier IV capacity expansions, while manufacturers leverage edge-to-core AI loops for predictive maintenance across fab lines.

E-commerce and media workloads remain growth pockets, yet their share is overtaken by compute-intensive model training, simulation, and digital-twin applications. Cross-sector collaborations are emerging: semiconductor fabs exchange waste heat with adjacent data centers, and banks co-locate compute near telco MEC nodes to cut payment latency.

By Data Center Size: Mega-Scale Sites Surface while Massive Campuses Prevail

Massive campuses between 25 MW and 60 MW represented 49.70% of capacity in 2024, reflecting optimal economies of scale within Taiwan’s grid-connection limits. Mega-scale facilities exceeding 60 MW, exemplified by Foxconn’s planned 100 MW AI supercomputer, are set to grow at 24.90% CAGR. The Taiwan hyperscale data center market size for mega-sites is constrained by 30 MW single-feeder caps in Hsinchu Science Park, so operators aggregate adjacent feeders or build dual-site campuses interconnected over fiber. Mega-scale economics revolve around shared coolant-distribution, bulk gas-insulated switchgear, and on-site high-voltage substations.

Large installations below 25 MW continue to serve edge and enterprise colocation but face slower growth. Site-selection models now weigh available renewable-energy quotas and seismic profiles over mere metropolitan proximity. Consequently, Taichung–Changhua attracts mega-scale developers due to offshore wind landing points and ample land parcels.

Geography Analysis

The Taipei–Taoyuan corridor held 55.40% revenue share in 2024 owing to its carrier-hotel density, subsea cable gateways, and proximity to the island’s technology headquarters. AWS’s three-zone sovereign-cloud region anchors additional network builds and stimulates anchor-tenant demand from semiconductor design houses. Land scarcity and grid congestion, however, are lengthening entitlement cycles, prompting developers to reserve capacity years in advance. Municipal authorities now require power-purchase balance sheets before granting construction permits, adding complexity to expansion plans.

Hsinchu–Miaoli capitalizes on its semiconductor cluster and mature 161 kV grid, hosting national supercomputing centers and advanced-packaging vendors. Individual data-center feeders are capped at 30 MW to prioritize fab expansions, forcing operators to deploy modular blocks across multi-building campuses. Fiber-dense routes between Hsinchu Science Park and Taipei create low-latency corridors that benefit AI inferencing workloads supporting chip design automation.

Taichung–Changhua is the fastest-growing region with 19.30% CAGR as offshore-wind PPAs unlock abundant renewable power. Google’s 500 MW wind agreement catalyzes additional data-center interest and attracts supply-chain partners. Tainan–Kaohsiung in the south offers large land parcels and emerging geothermal resources. Chunghwa Telecom’s first AI power center in Tainan signals accelerating southern deployments. Infrastructure gaps such as limited dark-fiber routes are being closed through new submarine-cable landing points and terrestrial backbones funded by telecom-utility joint ventures.

Mordor Intelligence tracks the hyperscale data center market across other major regions such as Africa, South America, and Asia, with additional country-level coverage spanning Malaysia, India, South Africa, Argentina, Hong Kong, and Saudi Arabia, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Competition is moderate, with global hyperscalers, domestic telcos, and specialist colocation firms sharing the addressable market. International cloud providers differentiate through custom silicon, sovereign-cloud compliance, and renewable PPAs. Domestic operators leverage existing metro fiber, licensed spectrum, and government relationships.

Foxconn partners with NVIDIA to build a 100 MW GPU cluster, blending manufacturing prowess with cloud service aspirations. Vantage Data Centers collaborates with Taiwan Mobile, bringing Western development standards and securing the island’s first greenfield project financing from local banks. Emerging disruptors such as Giga Computing bundle servers, coolant, and racks into turnkey modules that cut deployment cycles by 30%.

Strategic moves include long-dated offshore wind PPAs, multi-cloud interconnect fabrics, and sovereign-AI sandbox services that allow government agencies to build classified models. Competitive advantages increasingly hinge on securing GPU allocations and renewable-energy quotas rather than on traditional real-estate considerations. M and A activity remains limited but interest in edge-facility takeovers is growing as hyperscalers extend inference close to users

Taiwan Hyperscale Data Center Industry Leaders

Amazon Web Services

Microsoft Corporation

Alphabet Inc. (Google)

Chunghwa Telecom Co.

Chief Telecom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Foxconn subsidiary Ingrasys leased a 15,875 m² Taoyuan facility to scale AI-server production.

- June 2025: AWS inaugurated its Taiwan cloud region backed by USD 5 billion investment.

- June 2025: Taiwan Mobile and Vantage Data Centers began construction of a 16 MW AIDC in Taoyuan.

- May 2025: NVIDIA and Foxconn unveiled plans for a 100 MW AI supercomputing center.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Taiwan hyperscale data center market as all capital and operational revenues linked to facilities that deliver at least 10 MW of IT load or house roughly 5,000 servers for a single cloud, AI, or digital-content provider. The definition spans land acquisition, power and cooling infrastructure, IT hardware integration, and recurring managed-service fees generated within Taiwan's borders.

Scope exclusion: Enterprise on-premises server rooms, micro or edge sites below 1 MW, and pure network points of presence fall outside this study.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Unit

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning

- Design Engineering

- Fire, Security and Safety Systems

- DCIM / BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End Users

- By Data Center Size

- Large (Less than equal to 25 MW)

- Massive (Greater than 25 MW and less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured calls with facility engineers in Taipei, colocation sales managers in Taoyuan, power-equipment vendors, and local regulators. These discussions validated commissioning schedules, average selling price (ASP) trends, and PUE targets, and they filled gaps left by sparse public disclosures, especially on self-build capacity additions.

Desk Research

We first mapped Taiwan's hyperscale pipeline using open government sources such as the Ministry of Economic Affairs' power-permit bulletins, National Communications Commission spectrum releases, and DC tax-incentive filings, which indicate location, design load, and go-live year. Industry associations, such as the Asia Cloud Computing Association and Taiwan Computer Association, offer deployment counts, while grid-mix data from Taipower clarifies sustainability baselines.

Annual reports, 20-F filings, and investor decks from US hyperscale operators supplement spend patterns, and patent analytics drawn from Questel help benchmark rack-density roadmaps. News archives on Dow Jones Factiva track land purchases and equipment contracts. This list is illustrative; many additional public and paid sources informed the desk work.

Market-Sizing & Forecasting

A top-down model starts with announced and operating megawatt capacity, converted to revenue through average capex per MW and recurring opex ratios observed in interviews. Results are cross-checked with selective bottom-up roll-ups of server shipments and sampled ASP times rack counts before adjustments. Key variables include approved grid connection capacity, rack-density progression, power purchase agreement prices, land cost inflation, regulatory cooling efficiency mandates, and semiconductor export momentum. A multivariate regression forecasts each driver to 2031, then an ARIMA layer smooths short-term volatility. Missing bottom-up inputs, for confidential projects, are gap-filled using peer averages from comparable projects in Seoul and Tokyo.

Data Validation & Update Cycle

Outputs pass three rounds of analyst review that compare totals against independent grid-load series and import data. Material variances trigger re-contact of interviewees. We refresh the model annually, and then issue interim updates if a ≥5 MW project is announced or canceled.

Why Mordor's Taiwan Hyperscale Data Center Baseline Commands Reliability

Published figures differ because firms pick unique scopes, apply divergent ASP ladders, or refresh at uneven cadences.

Key gap drivers include: some publishers blend enterprise colocation and wholesale segments, others roll in full facility investment rather than monetized revenue, and rapid currency swings inflate totals when locked to budget-year NT$ exchange rates. Mordor reports only monetizable hyperscale revenue and uses quarterly NT$/USD averages, which limits such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 626.3 million | Mordor Intelligence | - |

| USD 1.84 billion (2024) | Global Consultancy A | Includes capital investment and enterprise colocation revenue, assumes 20% higher ASP ladder |

| USD 1.85 billion (2024) | Trade Journal B | Tracks total investment value, not realized revenue; scope covers all data center types |

| USD 643.7 million (2023) | Regional Consultancy C | Uses earlier base year and mixes micro, edge, and hyperscale sites, leading to lower estimate |

In sum, while external estimates swing widely, Mordor's disciplined scope, dual-approach modeling, and annual refresh cadence yield a balanced, transparent baseline that decision-makers can trace to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Taiwan hyperscale data center market?

The market reached USD 626.32 million in 2025 and is projected to surpass USD 1.16 billion by 2031.

Which segment is growing fastest in Taiwan’s hyperscale data center landscape?

Hyperscale colocation is forecast to grow at 21.40% CAGR through 2031 as enterprises seek rapid access to AI-optimized capacity.

Why are liquid-cooling systems gaining traction?

GPU racks over 50 kW require direct-to-chip or immersion cooling, driving 32.80% CAGR in liquid-cooling spend and enabling sub-1.33 PUE efficiency.

How are renewable-energy mandates affecting site selection?

Operators prioritize regions like Taichung–Changhua that offer offshore-wind PPAs, shifting development southward to secure 80% renewable mixes by 2028.

What are the key challenges facing hyperscale expansion in Taiwan?

Stringent water-recycling rules, 30 MW feeder caps, and chronic GPU and optical-module shortages are lengthening deployment timelines and raising costs.

Which companies are leading new AI infrastructure projects?

AWS, Foxconn with NVIDIA, and Chunghwa Telecom headline recent mega-scale initiatives, underscoring a convergence of global hyperscalers and domestic telcos.

Page last updated on: