Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

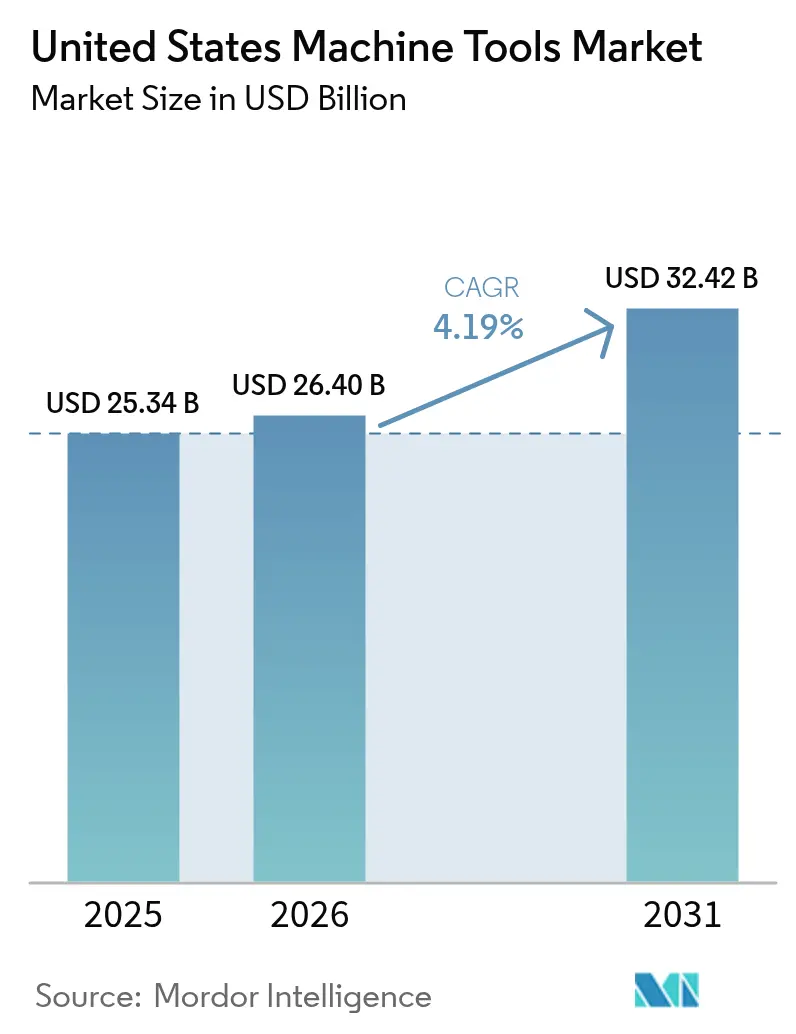

| Base Year Market Size (2025) | USD 25.34 Billion |

| Market Size (2026) | USD 26.40 Billion |

| Market Size (2031) | USD 32.42 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Machine Tools Market Analysis by Mordor Intelligence

The United States machine tools market size was valued at USD 25.34 billion in 2025 and is estimated to grow from USD 26.40 billion in 2026 to reach USD 32.42 billion by 2031, at a CAGR of 4.19% during the forecast period (2026-2031). Federal legislation, the Infrastructure Investment and Jobs Act, CHIPS and Science Act, and Inflation Reduction Act have already triggered more than USD 2 trillion in authorized outlays, doubling manufacturing construction spending between 2021 and 2024 and sharply lifting demand for precision equipment across semiconductor, battery, and defense corridors.[1]U.S. Department of the Treasury, “Manufacturing Construction Spending Data,” TREASURY.GOVSuppliers are responding with AI-enabled retrofit kits that shorten cycle times by up to 12%, helping buyers justify capex even as policy rates soften only gradually. Wage inflation for skilled machinists, which ran 1.8 percentage points ahead of average factory pay in 2024, is adding urgency to labor-saving automation but is also lengthening payback horizons where financing costs remain high.[2]U.S. Bureau of Labor Statistics, “Occupational Employment and Wage Statistics: Machinists,” BLS.GOVCommodity swings compound the picture: tungsten-carbide inputs rose 22% year-over-year in early 2025, forcing OEMs to alter toolholder compositions and push fixed-price service contracts to stabilize margins.[3]U.S. Geological Survey, “Mineral Commodity Summaries 2025,” USGS.GOV

Key Report Takeaways

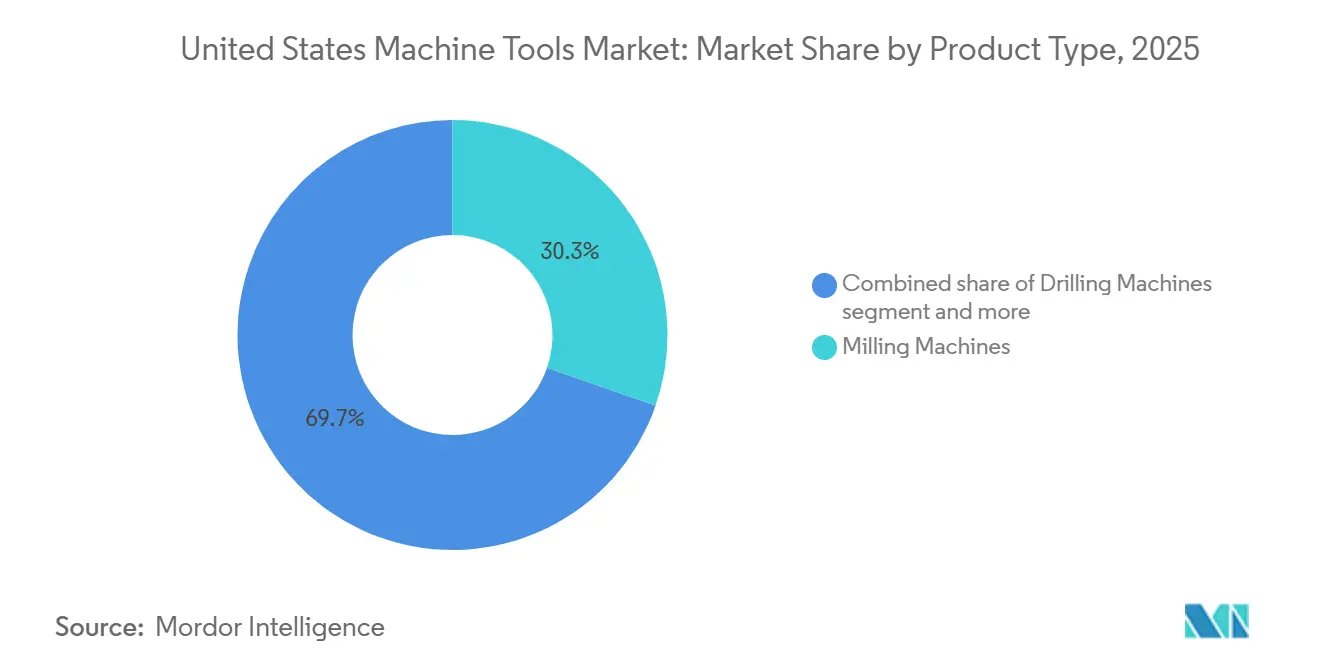

- By product type, milling machines led with 30.32% of the United States machine tools market share in 2025, while multi-axis machining centers are projected to expand at a 5.41% CAGR through 2031.

- By technology, CNC platforms captured 66.56% of the United States machine tools market in 2025 and are forecast to grow at a 5.19% CAGR through 2031.

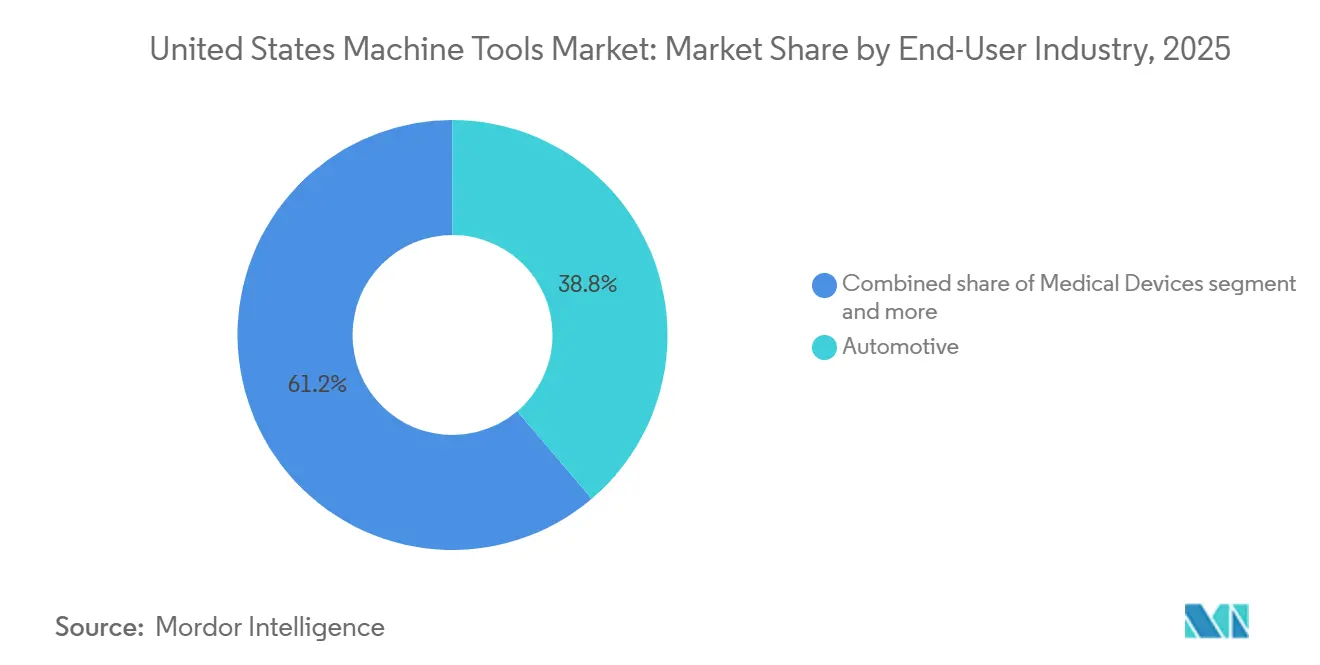

- By end-user, automotive commanded 38.78% of 2025 revenue; aerospace and defense is the fastest-growing segment at a 5.21% CAGR through 2031.

- By sales channel, direct sales held 56.56% share of the United States machine tools market size in 2025, while online and e-commerce is set to grow at 6.41% CAGR to 2031.

- Haas Automation, DMG MORI, Mazak, TRUMPF, and Okuma together accounted for roughly 42% of 2025 revenue, underscoring a moderately concentrated field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Machine Tools Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IRA, CHIPS & IIJA CapEx stimulus | +1.2% | Arizona, Ohio, Texas, New York | Medium term (2-4 years) |

| EV & battery-gigafactory precision-tooling demand | +0.9% | Michigan, Georgia, Tennessee, Kentucky | Medium term (2-4 years) |

| Commercial & defense aerospace titanium-machining rebound | +0.7% | Washington, Texas, California, Connecticut | Short term (≤ 2 years) |

| Industry 4.0 retrofit acceleration | +0.6% | Great Lakes, Southwest | Long term (≥ 4 years) |

| Generative-AI adaptive tool-path ROI | +0.5% | Medical-device and precision hubs nationwide | Long term (≥ 4 years) |

| DoD hypersonic-materials machining niche | +0.4% | Alabama, California, Virginia, Florida | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IRA, CHIPS & IIJA CapEx Stimulus

Federal incentives front-loaded what would have been a decade of capital spending into a three-year window. Semiconductor and battery corridors ordered advanced grinders, EDM units, and 5-axis centers capable of wafer and electrode processing. While early disbursements peaked in 2024-2025, suppliers tying payment terms to grant milestones stand to hold share until private follow-on funds materialize. The possibility of midstream supply-chain gaps, especially in battery separators and foils, could moderate tooling orders after 2027.[4]Congressional Research Service, “The CHIPS and Science Act: Implementation Status,” CRS.GOV Success will depend on synchronizing product roadmaps with the remaining CHIPS Act tranches.

EV and Battery-Gigafactory Precision-Tooling Demand

Gigafactories have driven brisk sales of laser welders and high-speed presses, yet lower-than-expected onsite machining intensity has curbed orders for general-purpose lathes and mills. Automakers remain cautious, weighing in-house cell production against joint-venture supply pacts. Vendors highlighting reconfigurable cells and IATF 16949 documentation gain traction because cell formats and chemistries evolve quickly. Positioning modular equipment as a hedge against chemistry shifts is central to capturing delayed orders in 2026-2028.

Commercial and Defense Aerospace Titanium-Machining Rebound

Rising orders for 737s, F-35s, and the B-21 stealth bomber revived demand for rigid, high-torque 5-axis machines that handle work-hardening titanium. With USD 205 billion earmarked for defense procurement in fiscal 2026, suppliers offering AS9100-ready service packages and predictive-maintenance layers meet stringent traceability needs. The segment’s urgency favors firms with secure service crews who can install and qualify machines inside classified cells without disrupting schedules.

Industry 4.0 Retrofit Acceleration

Job shops squeezed by high rates yet battling wage inflation see value in retrofitting legacy CNCs with sensors, edge controllers, and digital twins. TRUMPF’s AI Cutting Assistant, for instance, boosts yield without new hardware. Uptake is uneven, however, as many small firms fear cybersecurity liabilities and training gaps. Pairing retrofit kits with CMMC 2.0 documentation and subsidized operator upskilling is emerging as a win-win pathway.[4]https://www.trumpf.com/en_IN/

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-machinist wage inflation | -0.8% | Midwest, Southeast aerospace belt | Short term (≤ 2 years) |

| High interest-rate-driven payback extension | -0.6% | Nationwide | Medium term (2-4 years) |

| Volatile steel / rare-earth cost inflation | -0.4% | Nationwide | Short term (≤ 2 years) |

| CMMC 2.0 compliance-cost burden | -0.3% | Defense subcontractors nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Machinist Wage Inflation

Median machinist pay hit USD 24.82 per hour in 2024, outpacing general factory wages and compressing margins for low-pricing-power job shops. While higher pay pushes firms toward automation, the same cost pressure raises ROI hurdles, slowing orders. Suppliers bundling turnkey robotic cells with performance guarantees cushion the wage shock and rebuild buyer confidence.

High Interest-Rate-Driven Payback Extension

Although policy rates began easing in late 2024, a USD 500,000 5-axis center financed at 7% still accrues roughly USD 99,000 of interest over five years. Tighter bank standards have trimmed credit availability, leading many shops to favor retrofits or leases. OEMs clinching captive-finance deals deferred first payments, and usage-based billing sustains order flow in this climate.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Axis Centers Lead Precision Shift

Milling machines accounted for 30.32% of 2025 revenue, the largest slice of the United States machine tools market share. However, multi-axis machining centers are projected to grow at 5.41% annually through 2031, the fastest-rising subcategory. Their single-setup capability aligns with FDA validation guidance for patient-specific implants and with ASME B5.54 performance benchmarks. Laser, EDM, waterjet, and plasma units jointly hold roughly 20% of sales and gain traction where contactless processing reduces tool wear. As supply chains shorten and batch sizes shrink, buyers value flexibility over raw throughput, favoring multi-axis and laser solutions.

Multi-axis adoption also spreads fixed costs across varied workpieces, an important hedge against demand volatility. Companies like DMG MORI and Mazak bundle digital twins with new machines to prove ROI via virtual commissioning, while TRUMPF’s bevel-cut laser series cuts weld-prep time by up to 40%. Collectively, these features are steering capital away from single-purpose drills or grinders, reinforcing a premium position for configurable platforms within the United States machine tools market.

By Technology: CNC Dominance Sustained by Retrofit AI

CNC machines commanded 66.56% of 2025 technology sales, reflecting decades of installed-base advantages in the United States machine tools market. The segment is still forecast to advance at a robust 5.19% CAGR through 2031 as generative-AI add-ons lift productivity without requiring chassis replacement. Conventional manual equipment lingers in schools and repair shops but faces attrition as wages rise and safety regulations tighten. Hybrid additive-subtractive units, although below 10% of volume, are carving a niche in aerospace prototypes and medical implants where near-net shapes curb waste.

Competitive dynamics are intensifying. Several Asian entrants now match positional accuracy at 20-30% lower list prices. Incumbents therefore bundle proprietary software ecosystems, tool-wear prediction, cloud dashboards, and pay-per-use analytics to lock in service revenue. This service-centric stance helps defend margins even as hardware commoditizes within the broader United States machine tools industry.

By End-User Industry: Aerospace Outpaces Automotive

Automotive stamped a hefty 38.78% imprint on 2025 demand, yet aerospace and defense is on course for a 5.21% CAGR to 2031, the quickest among end-users. Rising output of 737 narrow-bodies, F-35 fighters, and B-21 bombers pulls in titanium-capable 5-axis centers and adaptive fixtures. Meanwhile, EV uncertainty is delaying non-battery tooling in automotive, trimming short-term spend.

Industrial machinery, electronics, and medical devices combine for roughly 30% of purchases, with hospital-side implant machining giving medical an extra lift. Shipyards, aided by submarine-yard modernization money, are placing multi-axis orders to replace aging lathes. Suppliers that master AS9100 audit trails, in-machine probing, and encryption for design files gain a defensible edge in the fastest-moving cohort of the United States machine tools market.

By Sales Channel: E-Commerce Gains on Digital Tools

Direct OEM sales captured 56.56% of 2025 turnover, proving buyers still rely on factory applications teams for complex installs. Yet online and e-commerce portals are projected to grow 6.41% yearly to 2031, taking bites from traditional dealers. TRUMPF, DMG MORI, and Haas now let customers configure options, run ROI models, and arrange financing in one web session. Dealers still account for 30% of revenue through local service and spares, but must integrate data dashboards and remote diagnostics to retain loyalty.

Refurbished machines, about 10-12% of unit volume, answer cash-flow constraints, especially among job shops facing higher rates. OEM-backed rebuild centers certify geometry to factory specs, reducing perceived risk. With digital quoting and embedded lease calculators, the United States machine tools market is inching toward the self-service norms already standard in other industrial verticals.

Geography Analysis

Regional demand continues to cluster where federal dollars and legacy clusters intersect. Great Lakes states such as Michigan, Ohio, and Indiana anchor EV powertrain and stamping investments, keeping orders flowing for presses and 3-axis mills even as non-EV lines idle. Southwest corridors in Arizona and Texas, buoyed by CHIPS grants, are absorbing high-precision grinders and EDM units essential for wafer and package fabrication. In the Southeast, aerospace giants assemble commercial jets and fighters, triggering titanium-capable 5-axis installations.

California’s mix of space launch, electronic defense, and high wages makes lights-out automation particularly attractive, while New York’s expanded fab projects create satellite demand for tool-and-die shops. Wage disparity also shapes adoption: states with USD 30-plus hourly machinist rates see faster ROI on automation, reinforcing a north-south equipment divide.

Looking forward, the regional winners will be those transitioning from construction to production. If battery midstream remains an import, Midwest gigafactories may buy fewer forming machines after 2027. Conversely, Arizona and Texas, already hosting operational fabs, could sustain above-average growth. OEMs that stock spares locally and field-service crews cleared for defense facilities will win share where unplanned downtime costs are measured in lost sortie rates or wafer starts.

Competitive Landscape

Competitive intensity in the United States machine tools market is moderate. The top five vendors control roughly 42% of sales, leaving room for niche specialists. DMG MORI deepened its federal footprint by securing USD 45 million in orders across at least 15 government sites, replacing fleets of legacy units with space-saving multi-axis centers. Haas leverages domestic assembly and short lead times, while Mazak’s Kentucky plant capitalizes on Buy-America preferences.

Strategic moves emphasize digital layers. TRUMPF invested USD 560 million in R&D in fiscal 2025, channeling 12% of revenue into AI tool-path engines, networked factory suites, and subscription monitoring. Lincoln Electric’s “RISE” program couples welding automation with CNC ecosystems, positioning the firm for turnkey cell sales rather than discrete components. Okuma introduced open-architecture controls to court third-party app developers, aiming for an industrial “app store” model that monetizes data services.

Challengers pursue agile niches. Hurco showcased INSPIRE+ intuitive controls and ProCobots packages targeting small job shops seeking rapid programming setups. Waterjet and hybrid additive-subtractive players tout material-agnostic capability, winning orders where exotic alloys defeat traditional cutters. Across the board, financing partnerships, retrofit AI modules, and CMMC-ready security layers are emerging as differentiators that may matter more than raw horsepower through 2031.

United States Machine Tools Industry Leaders

Haas Automation

TRUMPF Inc.

DMG MORI USA

Mazak Corp.

Okuma America

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Lincoln Electric outlined its “RISE” transformation with 2030 targets for margin expansion and digital-service growth.

- October 2025: TRUMPF’s Annual Report revealed USD 560 million in R&D and plans to finish its Munich HQ expansion by 2026.

- April 2025: DMG MORI opened a 20,000 m² automation hall at its Nara campus to supply global multi-axis demand.

- February 2025: DMG MORI completed its tender offer for TAIYO KOKI, boosting its turning-center lineup in North America.

United States Machine Tools Market Report Scope

The machine tools industry can be classified into metal-cutting machines and metal-forming machines. A complete background analysis of the United States Machine Tools Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The United States Machine Tools Market is Segmented by Type (Metalworking Machines, Parts and Accessories, and Installation, Repair, and Maintenance) and by End User (Automotive, Fabrication, and Industrial Machinery Manufacturing, Marine and Aerospace & Defense, Precision Engineering, and Other End Users). The report offers the market sizes and forecasts for the United States Machine Tools market in value (USD) for all the above segments.

By Product

| Metal Cutting Tools | Milling Machines |

| Drilling Machines | |

| Turning (Lathe) Machines | |

| Grinding Machines | |

| Laser Cutting Machines | |

| Electrical Discharge Machines (EDM) | |

| Waterjet Cutting Machines | |

| Plasma Cutting Machines | |

| Multi-Axis Machining Centres | |

| Others (Boring, etc.) | |

| Metal Forming Tools | Presses (Mechanical, Hydraulic, Servo) |

| Forging Machines | |

| Bending Machines | |

| Others (Shearing, Extrusion, Rolling, etc.) |

By Technology

| Conventional Machines (Manually or Semi-Manually) |

| CNC Machines |

| Additive Manufacturing / Hybrid Machines |

By End-User Industry

| Automotive |

| Aerospace & Defence |

| Electrical & Electronics |

| Industrial Machinery & Equipment |

| Medical Devices |

| Shipbuilding & Marine |

| Precision Engineering |

| Energy & Power |

| Metal Fabrication (Job Shops, etc.) |

| Other Industries (Railway, Other General Manufacturing, etc.) |

By Sales Channel

| Direct Sales (OEMs to End Users) |

| Dealers & Distributors |

| Online / E-commerce |

| Others (System Integrators, Events & Exhibitions, Rebuilders & Refurbished, etc.) |

| By Product | Metal Cutting Tools | Milling Machines |

| Drilling Machines | ||

| Turning (Lathe) Machines | ||

| Grinding Machines | ||

| Laser Cutting Machines | ||

| Electrical Discharge Machines (EDM) | ||

| Waterjet Cutting Machines | ||

| Plasma Cutting Machines | ||

| Multi-Axis Machining Centres | ||

| Others (Boring, etc.) | ||

| Metal Forming Tools | Presses (Mechanical, Hydraulic, Servo) | |

| Forging Machines | ||

| Bending Machines | ||

| Others (Shearing, Extrusion, Rolling, etc.) | ||

| By Technology | Conventional Machines (Manually or Semi-Manually) | |

| CNC Machines | ||

| Additive Manufacturing / Hybrid Machines | ||

| By End-User Industry | Automotive | |

| Aerospace & Defence | ||

| Electrical & Electronics | ||

| Industrial Machinery & Equipment | ||

| Medical Devices | ||

| Shipbuilding & Marine | ||

| Precision Engineering | ||

| Energy & Power | ||

| Metal Fabrication (Job Shops, etc.) | ||

| Other Industries (Railway, Other General Manufacturing, etc.) | ||

| By Sales Channel | Direct Sales (OEMs to End Users) | |

| Dealers & Distributors | ||

| Online / E-commerce | ||

| Others (System Integrators, Events & Exhibitions, Rebuilders & Refurbished, etc.) | ||

Key Questions Answered in the Report

How large is the United States machine tools market in 2026?

The United States machine tools market size is valued at USD 26.40 billion in 2026.

What is the expected growth rate through 2031?

Revenue is projected to grow at a 4.19% CAGR from 2026 to 2031.

Which product segment is expanding the fastest?

Multi-axis machining centers are forecast to post the highest 5.41% CAGR through 2031.

Who holds the largest share among end-users?

Automotive manufacturers led with 38.78% of 2025 demand, though aerospace is growing faster.

How are high interest rates affecting purchases?

Elevated financing costs are lengthening payback periods, prompting many shops to favor retrofit upgrades or OEM-backed leasing.

What role does e-commerce play in new machine sales?

Online portals are the fastest-growing channel, expected to rise 6.41% per year as buyers embrace self-service configuration and financing tools.

Page last updated on: