Lysosomal Storage Disease Treatment Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

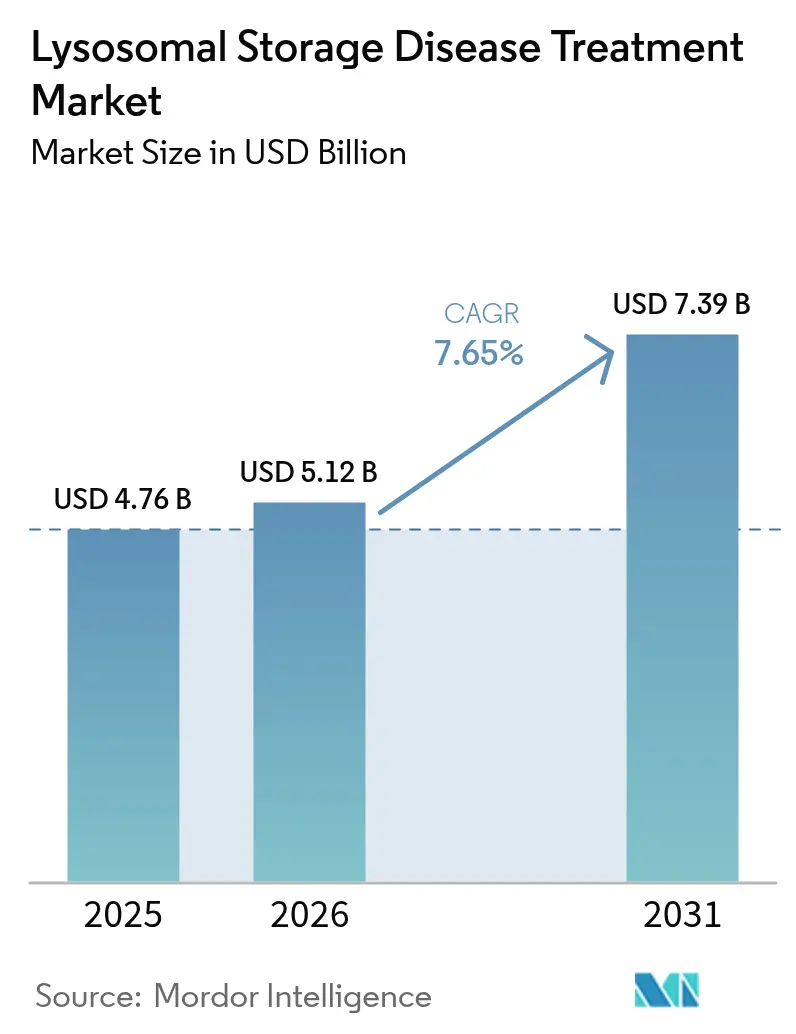

| Market Size (2026) | USD 5.12 Billion |

| Market Size (2031) | USD 7.39 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

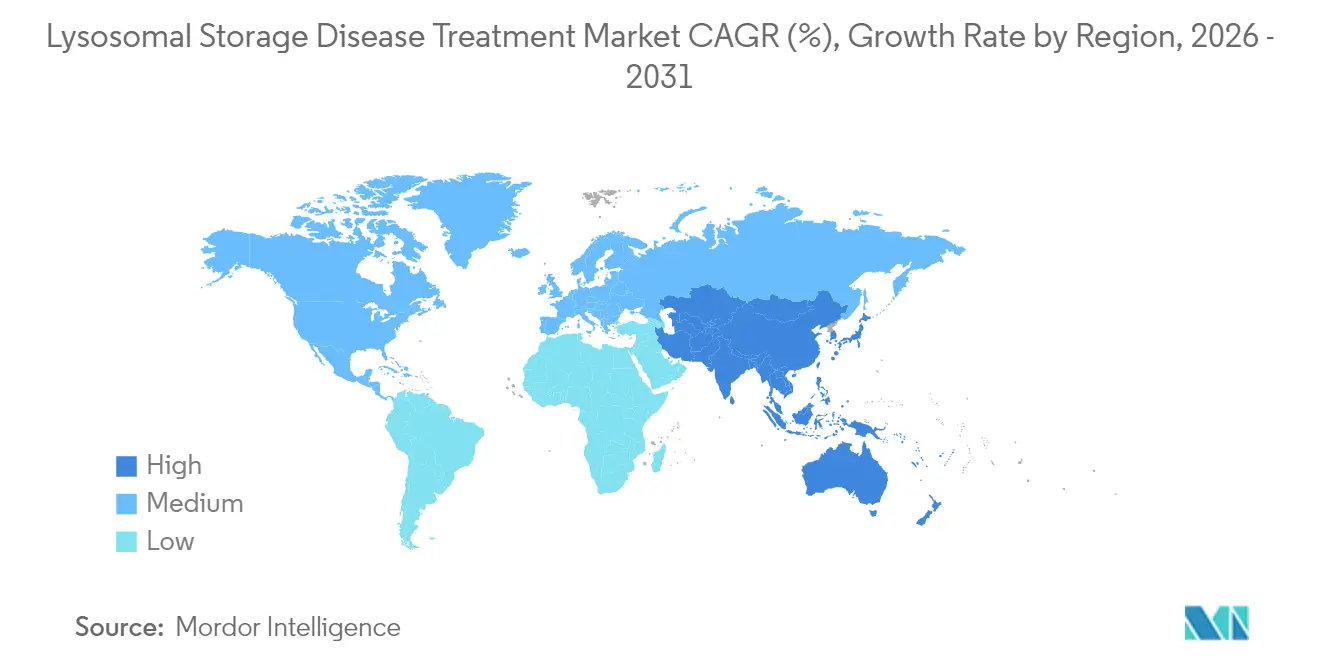

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lysosomal Storage Disease Treatment Market Analysis by Mordor Intelligence

The lysosomal storage disease treatment market size was valued at USD 4.76 billion in 2025 and estimated to grow from USD 5.12 billion in 2026 to reach USD 7.39 billion by 2031, at a CAGR of 7.65% during the forecast period (2026-2031). Accelerating approvals for single-dose gene therapies, broader enzyme-replacement indications, and newborn genomic screening programs have shifted treatment initiation to presymptomatic stages, expanding the addressable population. Competitive intensity is rising as legacy enzyme players face challengers advancing blood-brain-barrier-penetrant vectors and oral small-molecule substrates. Manufacturing scale-up of viral vectors remains a bottleneck even as capital flows to contract development organizations. Parallel growth in home-infusion services, which cut administration costs by 25-50%, is re-shaping care delivery models.

Key Report Takeaways

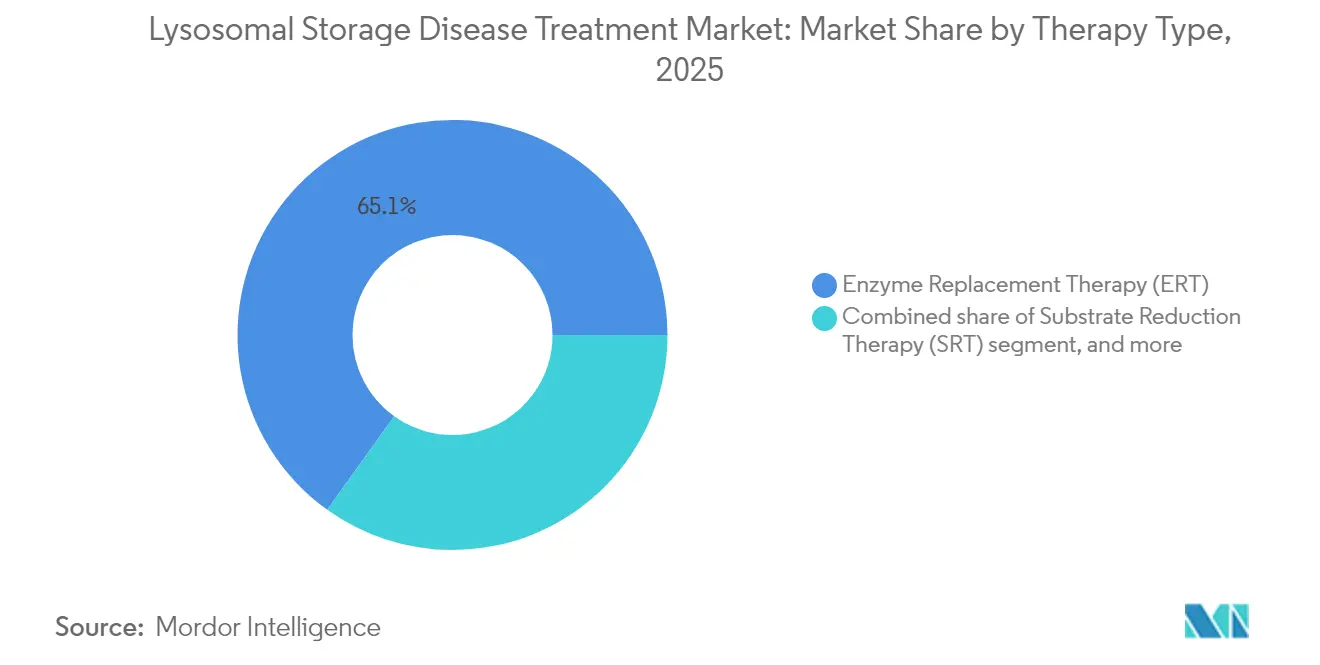

- By therapy type, enzyme replacement therapy led with 65.10% of the lysosomal storage disease treatment market share in 2025; gene therapy is projected to expand at a 10.22% CAGR through 2031.

- By modality, intravenous biologics accounted for 55.20% share of the lysosomal storage disease treatment market size in 2025, while oral small-molecule therapy is forecast to grow at a 10.12% CAGR to 2031.

- By disease type, Gaucher disease commanded 28.10% share of the lysosomal storage disease treatment market size in 2025; Niemann-Pick disease is advancing at a 10.35% CAGR through 2031.

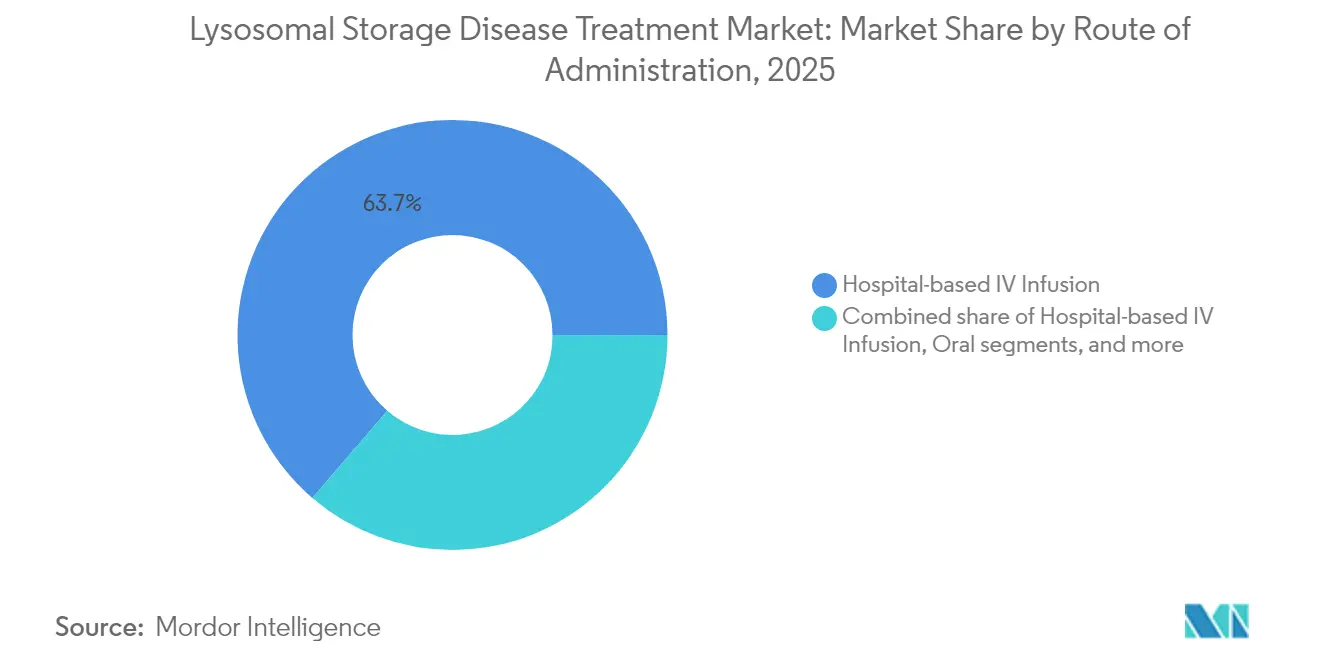

- By route of administration, hospital-based IV infusion held 63.70% of the lysosomal storage disease treatment market share in 2025, whereas home-infusion IV is projected to post an 11.05% CAGR up to 2031.

- By end user, tertiary hospitals captured 65.60% revenue share in 2025, while home-care settings are forecast to grow at an 11.20% CAGR through 2031.

- By geography, North America captured 42.10% revenue share in 2025, while Asia-Pacific are forecast to grow at a CAGR of 9.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lysosomal Storage Disease Treatment Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global prevalence of lysosomal storage disorders | +1.2% | Global – highest detection in developed markets | Medium term (2-4 years) |

| Increasing orphan drug designations and incentives | +1.0% | North America & EU leadership; adoption expanding worldwide | Short term (≤ 2 years) |

| Advancements in diagnostic technologies and early screening | +1.8% | North America & EU leading; rapid rollout in APAC | Short term (≤ 2 years) |

| Expansion of enzyme replacement therapy product approvals | +1.3% | Global, strongest in North America & EU | Medium term (2-4 years) |

| Emerging gene and cell therapies for neuropathic LSDs | +2.1% | Global, concentrated in major pharmaceutical hubs | Long term (≥ 4 years) |

| Strategic collaborations and rare-disease investment surge | +1.5% | North America & EU core; spill-over to emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Lysosomal Storage Disorders

Newborn genomic screening in Shanghai identified LSD incidence of 1 in 1,856 live births, materially above historical estimates and confirming the value of proactive testing. The Chinese National Medical Products Administration’s CARE program encourages orphan-drug filings and has increased investigational new drug submissions by 32% since 2024. Similar prevalence up-ticks are appearing in South Korea’s national registry, underscoring the shift from anecdotal diagnosis to population-wide screening. As registries expand, demand for early-stage intervention grows, shortening diagnostic delay from six years to fewer than six weeks in leading tertiary centers. Therapeutic pipelines are therefore recalibrated toward infant-onset indications where clinical benefit is most pronounced.

Advancements in Diagnostic Technologies and Early Screening

Second-generation tandem mass spectrometry now screens for up to eight LSDs in a single assay with under 0.5% false positives, outperforming enzyme-activity panels. Integration of next-generation sequencing confirms pathogenic variants and guides precision therapy, such as selecting migalastat for Fabry patients with amenable mutations. Turn-around times for confirmatory genotyping have fallen below seven days, enabling treatment initiation during neonatal intensive-care stays. Health-system adoption is fastest in Canada and Germany where government reimbursement covers both biochemical and genomic assays. Early diagnosis is catalyzing payer acceptance of high-value gene therapies by evidencing long-term cost offsets from avoided disability.

Emerging Gene and Cell Therapies for Neuropathic LSDs

Lenmeldy’s single-dose autologous stem-cell therapy produced motor milestone retention in 90% of treated metachromatic leukodystrophy patients versus 30% historically observed in untreated cohorts[1]U.S. FDA, “Rare Pediatric Disease Priority Review Voucher Program,” fda.gov. RGX-121 lowered cerebrospinal heparan-sulfate by 85% and enabled 80% of patients to discontinue weekly infusions. AAV9 capsids penetrate the blood–brain barrier more efficiently than earlier vectors, sustaining enzyme expression for at least 36 months in Gaucher and GM1 gangliosidosis trials. Manufacturing yields, once limited to 1e15 vector genomes per batch, have doubled with suspension HEK293 technologies, trimming cost of goods by 38%. Regulatory agencies are instituting rolling-review mechanisms that have cut approval timelines by nine months on average, intensifying competitive velocity.

Strategic Collaborations and Rare-Disease Investment Surge

REGENXBIO’s USD 110 million licensing deal with Nippon Shinyaku for MPS programs exemplifies a pivot toward regional co-commercialization structures that spread risk and accelerate market entry. BioMarin’s USD 270 million purchase of Inozyme secures a late-stage ERT for ENPP1 deficiency, cementing cross-pathway portfolio breadth. Venture funding remains resilient, with Glycomine securing USD 115 million Series C to advance glycosylation-disorder therapeutics. Partnerships now concentrate on blood-brain-barrier shuttle platforms and modular capsid engineering, fields projected to attract more than USD 2 billion in fresh capital by 2027. Such alliances compress R&D timelines while granting smaller biotech access to established manufacturing and regulatory expertise.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs and reimbursement challenges | −1.8% | Global – most acute in emerging markets | Long term (≥ 4 years) |

| Limited blood–brain barrier penetration of current therapies | −1.2% | Global – impacts neuronopathic forms | Medium term (2-4 years) |

| Manufacturing scalability and supply constraints | −1.4% | Global, centered on gene-therapy production hubs | Medium term (2-4 years) |

| Long-term safety and immunogenicity concerns | −1.0% | Global, affecting all advanced modalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Reimbursement Challenges

Lenmeldy lists at USD 4.25 million, positioning it as the world’s most expensive therapy and forcing payers to adopt outcomes-based contracts tying reimbursement to motor-function end-points[2]Thomas Mueller et al., “Cost Burden of Enzyme Replacement Therapy in Germany,” Orphanet Journal of Rare Diseases, ojrd.biomedcentral.com. In Germany, mean annual enzyme-replacement expenditure for Fabry disease is EUR 369,047 (USD 405,952) per patient, 94% of which is drug acquisition cost. Medicaid programs are carving out gene-therapy bundles from capitation payments to mitigate one-time financial shocks. Private insurers restrict coverage to genetically confirmed cases and require longitudinal biomarker data, prolonging access in 17 U.S. states. Innovative annuity-style payment models are progressing slowly due to unresolved regulatory guidance on multi-year amortization.

Limited Blood–Brain Barrier Penetration of Current Therapies

Intravenous imiglucerase fails to cross the blood–brain barrier, leaving neuronopathic Gaucher disease unmanaged despite somatic symptom control. Receptor-mediated transcytosis using transferrin ligands demonstrated four-fold enzyme uptake in preclinical Pompe models but still awaits phase 2 confirmation. Intrathecal cerliponase alfa extends survival in CLN2 patients yet requires quarterly neurosurgical catheter access, limiting broad uptake. Gene vectors show superior CNS tropism, although neutralizing antibodies to AAV9 exclude up to 25% of adults from trial enrollment. Manufacturing constraints for high-titer vectors persist despite dual-plasmid producer lines that raise yield by 30%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Sustained ERT Leadership Meets Rapid Gene-Therapy Upswing

The lysosomal storage disease treatment market size for enzyme replacement therapy stood at USD 3.1 billion in 2025, equal to 65.10% of total revenue, and remains pivotal for Gaucher, Fabry, and Pompe care. Competitive positioning centers on second-generation enzymes such as avalglucosidase alfa, which offers higher muscle uptake versus predecessor alglucosidase. However, gene therapy’s 10.22% CAGR reflects its one-time-dose value proposition. Lenmeldy’s approval showcases durable neurologic benefit, while Ultragenyx’s UX111 heads the 2025 FDA review queue for Sanfilippo syndrome. Substrate reduction and pharmacological chaperones deliver incremental gains for mutation-specific cohorts, reinforcing precision-medicine trajectories within the lysosomal storage disease treatment market. Pipeline convergence toward combination regimens, such as Pombiliti plus Opfolda, aims to amplify intracellular trafficking and prolong treatment intervals.

By Modality: Oral Regimens Gain Ground on Parenteral Standards

Intravenous biologics retained 55.20% revenue in 2025, anchored by weekly infusions of imiglucerase, agalsidase beta, and alglucosidase alfa. Oral small-molecule substrate reducers—venglustat, lucerastat, and the approved Cerdelga—record the highest growth at 10.12% CAGR, driven by adherence benefits and absence of infusion reactions. The modality mix is tilting further as oral chaperone migalastat expands into additional Fabry genotypes. Intrathecal and intracerebroventricular deliveries are reserved for neuronopathic syndromes; devices such as SmartFlow Neuro enable precise cannula placement for Kebilidi gene transfer. PEGylation and Fc-fusion technologies extend half-life of ERTs like ELFABRIO, trimming infusion frequency to monthly. Patient-centric dosing aligns with home-infusion expansion and underscores payers’ focus on total-cost-of-care reduction within the lysosomal storage disease treatment market.

By Disease Type: Entrenched Gaucher Portfolio Versus Rapid Niemann-Pick Momentum

Gaucher disease remains the largest submarket, holding 28.10% of 2025 revenue, supported by three commercial ERTs and one oral agent that diversify pricing pressure. Competition spurs periodic price rebates and expanded compassionate-use programs. Niemann-Pick disease typifies the future high-growth cohort with 10.35% CAGR through 2031 after dual FDA approvals of Miplyffa (oral) and AQNEURSA (IV) ended decades of therapeutic void. Fabry and Pompe sustain mid-single-digit expansion, thanks to chaperone therapy uptake and next-gen enzymes showing superior renal and pulmonary endpoints. Mucopolysaccharidoses drive gene-therapy innovation; RGX-111 for MPS IIB could deliver durable CNS correction, challenging chronic intrathecal ERT. Emerging pipelines in GM1 gangliosidosis and alpha-mannosidosis illustrate white-space potential as early-stage data show >70% reduction in storage substrates.

By Route of Administration: Home-Infusion Redraws Care Pathways

Hospital-based IV centers delivered 63.70% of doses in 2025, but payer steering toward lower-cost sites of care is accelerating shift to home settings, now posting 11.05% CAGR. Real-world evidence from German Fabry cohorts shows parity in adverse-event rates between home and clinic infusions, while cutting non-drug costs by 42%. Oral regimens push decentralization further, enabling self-administration and reducing travel burdens for rural families. Intrathecal routes, despite surgical requirements, are increasingly offered at satellite neurosurgery centers to broaden access. Gene therapies, administered once in specialized hospitals, may subsequently obviate chronic infusion needs, accentuating the disruptive impact on delivery infrastructure within the lysosomal storage disease treatment market.

By End User: Tertiary Centers Lose Exclusivity to Community-Based Care

Tertiary hospitals still manage 65.60% of treated patients given complex diagnostic and monitoring demands. Yet home-care programs, bolstered by telemedicine, display 11.20% CAGR as nurse-led infusion teams expand geographic reach. Specialty rare-disease clinics, often university affiliated, preserve relevance through access to investigational protocols and multidisciplinary expertise. Gene therapy’s one-time dosing compresses long-term hospital revenue streams, triggering institutions to seek value-based contracts and ancillary genomic-counseling services. Payers are piloting integrated-care bundles that reimburse genetic testing, counseling, and drug delivery under a single code, realigning incentives toward community management in the lysosomal storage disease treatment market.

Geography Analysis

North America delivered 42.10% of 2025 revenue, guided by the FDA’s Rare Pediatric Disease Priority Review Voucher program and expansive commercial insurance coverage. More than 20 active gene-therapy trials are recruiting across the United States, cementing the region’s innovation dominance. State-level disparity persists: California covers travel and lodging for out-of-state Lenmeldy recipients, whereas six Midwestern states limit gene therapies to Medicaid carve-outs, elongating access timelines. Canada’s universal system reimburses five ERTs on a designated orphan-drug list, although approval-to-funding lags average 14 months.

Asia-Pacific is the fastest-growing territory at 9.15% CAGR. China’s updated Rare Disease List, now 207 conditions, has cut regulatory review time for imported agents to 9 months, down from 24 months pre-2023. Shanghai’s genomic screening pilot uncovered LSD incidence far above global averages, prompting national scale-up grants. Japan leverages its Sakigake fast-track to draw foreign biotech filings, while South Korea’s National Health Insurance captures over 90% Fabry treatment coverage, demonstrating advanced payer readiness. India’s rare-disease policy subsidizes up to INR 2 million (USD 2.2 million) per patient for gene therapy, though disbursement remains sporadic.

Europe holds a stable share driven by the European Reference Network for Hereditary Metabolic Disorders that coordinates cross-border care. Germany validates home-infusion cost parity and supports monthly prescription refills to minimize clinic visits. Italy’s Lombardy region mandates LSD newborn screening, expanding early-diagnosis uptake. France favors outcome-linked reimbursement models for high-cost gene therapies, piloting five-year warranty clauses. The U.K.’s NHS is negotiating subscription payments modeled on its antimicrobial “Netflix” contract, aiming to cap annual LSD therapy spend while guaranteeing supplier volume.

Competitive Landscape

Sanofi’s Genzyme unit anchors enzyme-replacement leadership with Cerezyme, Fabrazyme, and Myozyme franchises exceeding USD 1.8 billion combined 2024 sales. Takeda sustains depth across mucopolysaccharidoses, while BioMarin’s VIMIZIM and NAGLAZYME generated USD 2.4 billion in 2023 revenue, funding pipeline expansion into gene therapy. Market incumbents are reformulating first-wave enzymes with PEGylation and glyco-engineering to counter biosimilar pressure.

Orchard Therapeutics achieved first-mover advantage in CNS-targeted gene therapy with Lenmeldy, pricing at USD 4.25 million amid value-based agreement rollouts. Ultragenyx’s UX111 heads the 2025 regulatory calendar with FDA priority review for Sanfilippo syndrome. REGENXBIO is co-developing RGX-121 in Japan through a USD 110 million pact with Nippon Shinyaku, illustrating globalization of commercialization strategies.

Blood-brain-barrier-crossing platforms are a hotbed of partnership activity; Chiesi licensed Aliada’s antibody-mediated shuttle to fuse with lysosomal enzymes for neuronopathic indications. Viral-vector manufacturing capacity is emerging as a strategic differentiator: companies with in-house 2,000 L bioreactor suites report 35% lower COGS than CDMO-reliant peers. White-space indications such as GM1 gangliosidosis attract early-stage investment; GC Biopharma’s preclinical gene therapy reduced GM1 levels by over 70%, signaling pipeline breadth beyond the traditional “big three” diseases.

Lysosomal Storage Disease Treatment Industry Leaders

Pfizer Inc

Takeda Pharmaceutical Company Limited (Shire Plc)

Sanofi (Genzyme Corporation)

BioMarin

Johnson & Johnson (Actelion Pharmaceuticals Ltd)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BioMarin closed its USD 270 million acquisition of Inozyme, adding late-stage ENPP1 deficiency enzyme therapy INZ-701 to its rare-disease portfolio.

- February 2025: Ultragenyx received FDA priority review for UX111 gene therapy targeting Sanfilippo syndrome type A, with PDUFA date set for Aug 18 2025.

- January 2025: REGENXBIO and Nippon Shinyaku announced USD 110 million partnership to co-develop RGX-121 and RGX-111 for MPS disorders in Japan.

- November 2024: FDA approved Kebilidi, the first gene therapy for AADC deficiency, administered via SmartFlow Neuro cannula system.

- September 2024: FDA cleared Miplyffa and AQNEURSA as the first treatments for Niemann-Pick disease type C, inaugurating dual-modality therapy options.

- May 2024: FDA authorized Lenmeldy for metachromatic leukodystrophy, pricing it at USD 4.25 million, and awarding a Priority Review Voucher to Orchard Therapeutics.

Global Lysosomal Storage Disease Treatment Market Report Scope

As per the scope of the report, lysosomal storage diseases (LSDs) are inborn errors of metabolism characterized by the accumulation of substrates in excess in various organs' cells due to the defective functioning of lysosomes. They cause dysfunction of those organs where they accumulate and contribute to great morbidity and mortality. The Lysosomal Storage Disease Treatment Market is Segmented By Therapy Type (Enzyme Replacement Therapy, Substrate Reduction Therapy), By Application (Gaucher disease, Cystinosis, Pompe Disease, Fabry Disease, and Other Applications), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers the value (in USD million) for the above segments.

| Enzyme Replacement Therapy (ERT) |

| Substrate Reduction Therapy (SRT) |

| Gene Therapy |

| Pharmacological Chaperone Therapy |

| Hematopoietic Stem-Cell Transplantation |

| Intravenous Biologics |

| Oral Small-molecule |

| Intrathecal/ICV Delivery |

| Gaucher Disease (Type I–III) |

| Fabry Disease |

| Pompe Disease |

| Mucopolysaccharidoses (I, II, III, IV, VI, VII) |

| Niemann-Pick Disease (Type A/B & C) |

| Other Disease Types |

| Hospital-based IV Infusion |

| Home-infusion IV |

| Oral |

| Intrathecal/ICV |

| Tertiary Hospitals |

| Specialty/Rare-disease Clinics |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Enzyme Replacement Therapy (ERT) | |

| Substrate Reduction Therapy (SRT) | ||

| Gene Therapy | ||

| Pharmacological Chaperone Therapy | ||

| Hematopoietic Stem-Cell Transplantation | ||

| By Modality | Intravenous Biologics | |

| Oral Small-molecule | ||

| Intrathecal/ICV Delivery | ||

| By Disease Type | Gaucher Disease (Type I–III) | |

| Fabry Disease | ||

| Pompe Disease | ||

| Mucopolysaccharidoses (I, II, III, IV, VI, VII) | ||

| Niemann-Pick Disease (Type A/B & C) | ||

| Other Disease Types | ||

| By Route of Administration | Hospital-based IV Infusion | |

| Home-infusion IV | ||

| Oral | ||

| Intrathecal/ICV | ||

| By End-user | Tertiary Hospitals | |

| Specialty/Rare-disease Clinics | ||

| Home-care Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the lysosomal storage disease treatment market?

The lysosomal storage disease treatment market size reached USD 5.12 billion in 2026 and is projected to grow to USD 7.39 billion by 2031.

Which therapy type holds the largest market share?

Enzyme replacement therapy maintained 65.10% of global revenue in 2025, making it the dominant treatment approach.

Why is gene therapy considered disruptive in this space?

Gene therapy offers single-dose, potentially curative benefit and is growing at a 10.22% CAGR, outpacing all other modalities.

Which region is expanding the fastest?

Asia-Pacific is forecast to post a 9.15% CAGR to 2031, driven by regulatory modernization and newborn screening expansion.

How are high treatment costs being managed?

Payers are adopting outcome-based contracts, subscription models, and annuity payments to spread the financial impact of therapies priced above USD 4 million.

Page last updated on: