Lymphoma Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

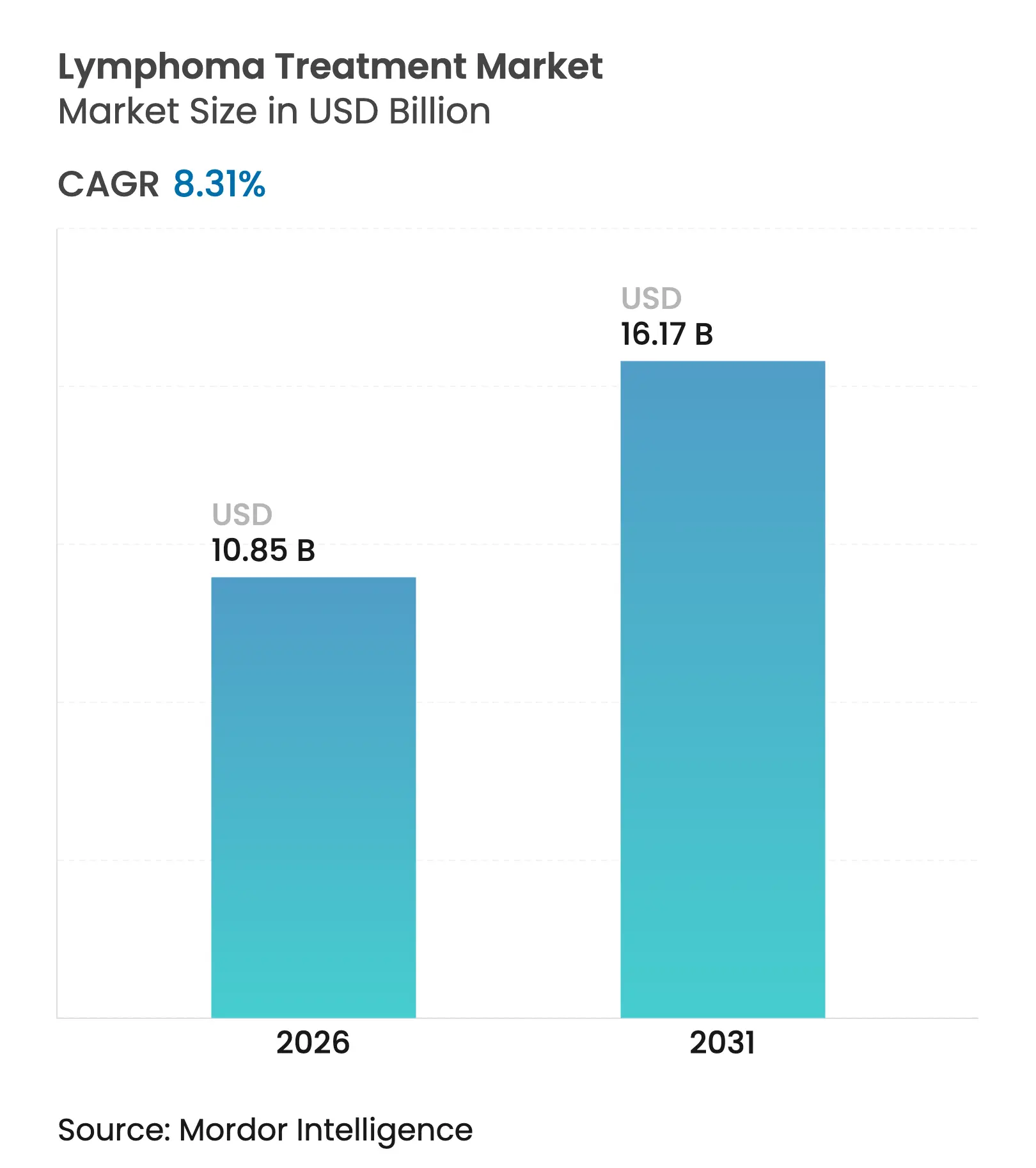

| Market Size (2026) | USD 10.85 Billion |

| Market Size (2031) | USD 16.17 Billion |

| Growth Rate (2026 - 2031) | 8.31 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Lymphoma Treatment Market Analysis by Mordor Intelligence

The lymphoma treatment market size is expected to grow from USD 10.02 billion in 2025 to USD 10.85 billion in 2026 and is forecast to reach USD 16.17 billion by 2031 at 8.31% CAGR over 2026-2031. Growth is driven by surging disease incidence, rapid immunotherapy approvals, and widening treatment access in emerging economies. The US FDA’s expedited reviews for CAR-T cells, bispecific antibodies, and subcutaneous checkpoint inhibitors shorten launch timelines and accelerate revenue capture. Asia Pacific adds momentum as local manufacturers lower costs, exemplified by Brazil’s USD 35,000 locally produced CAR-T program versus the USD 500,000 reference price in mature markets. Meanwhile, manufacturers are scaling capacity—Legend Biotech doubled Carvykti output in 2025—to relieve supply constraints and match rising demand.

Key Report Takeaways

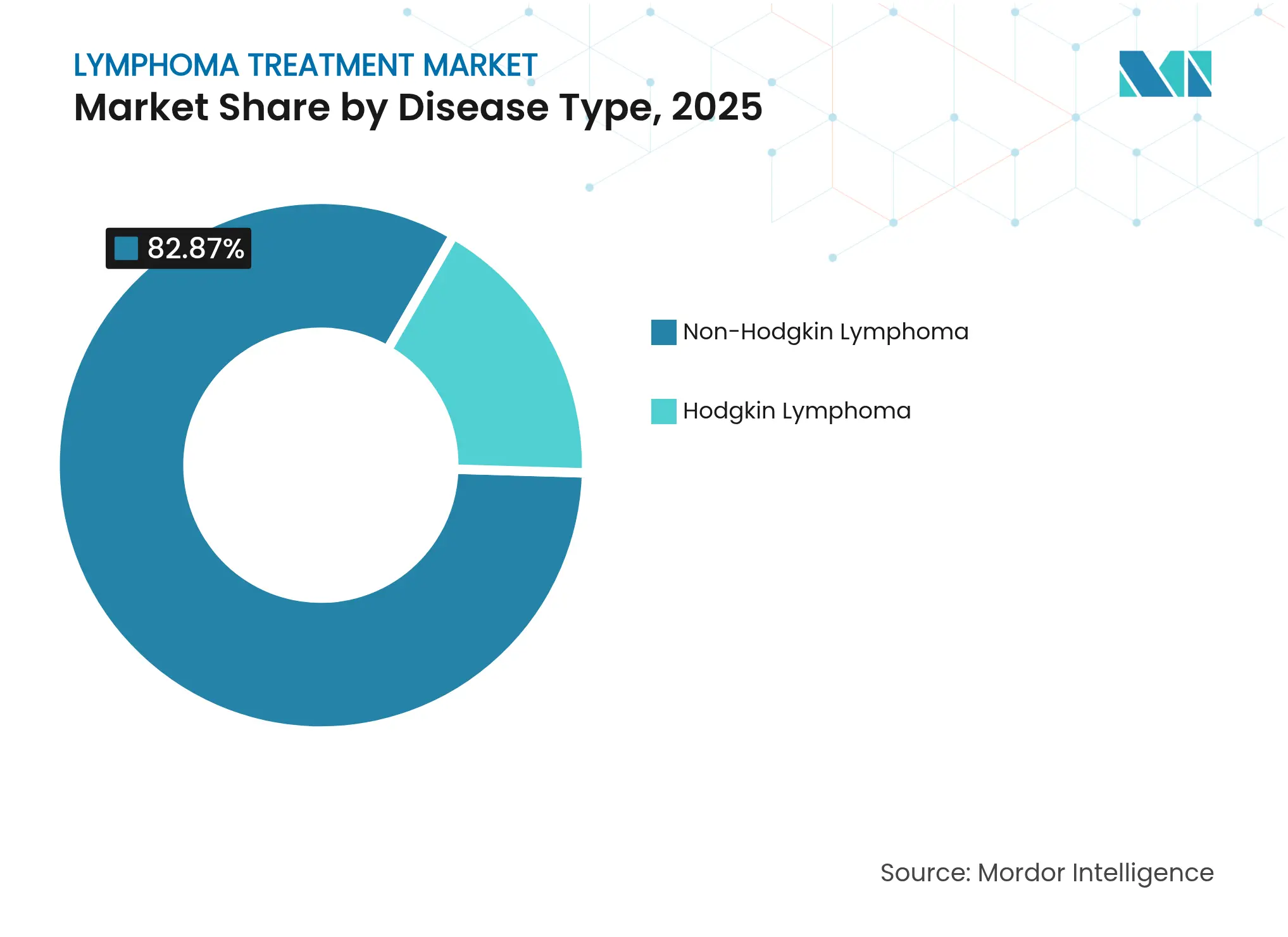

- By disease type, non-Hodgkin lymphoma led with 82.87% revenue share in 2025.

- By type of therapy, immunotherapy held 36.05% share in 2025, while CAR-T cell therapy is poised to expand at a 12.05% CAGR through 2031.

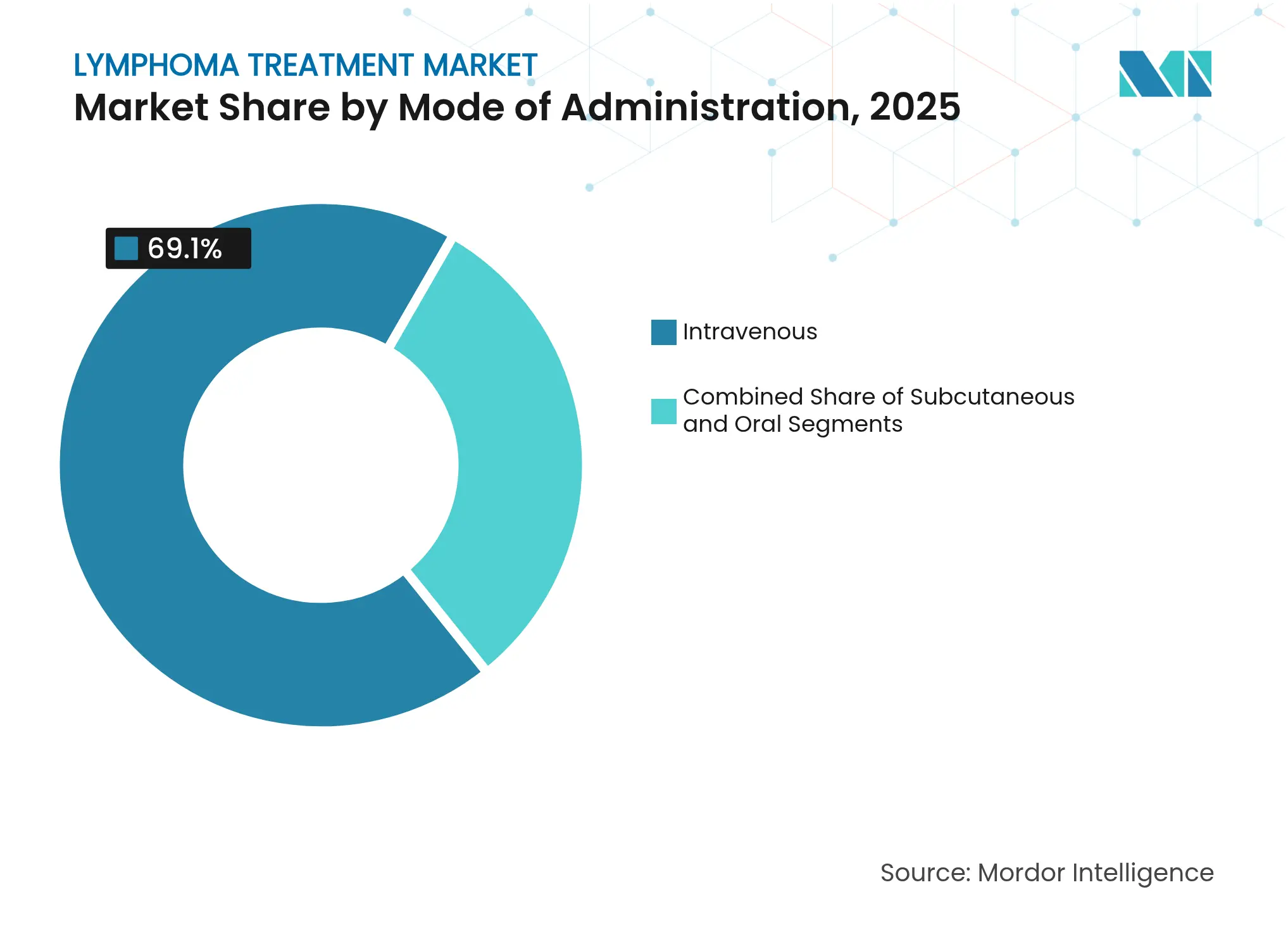

- By mode of administration, intravenous delivery accounted for 69.10% of the lymphoma treatment market share in 2025 and subcutaneous delivery is forecast to grow at an 10.62% CAGR to 2031.

- By end user, hospitals captured 60.74% share of the lymphoma treatment market size in 2025, but home-care settings are advancing at a 9.92% CAGR through 2031.

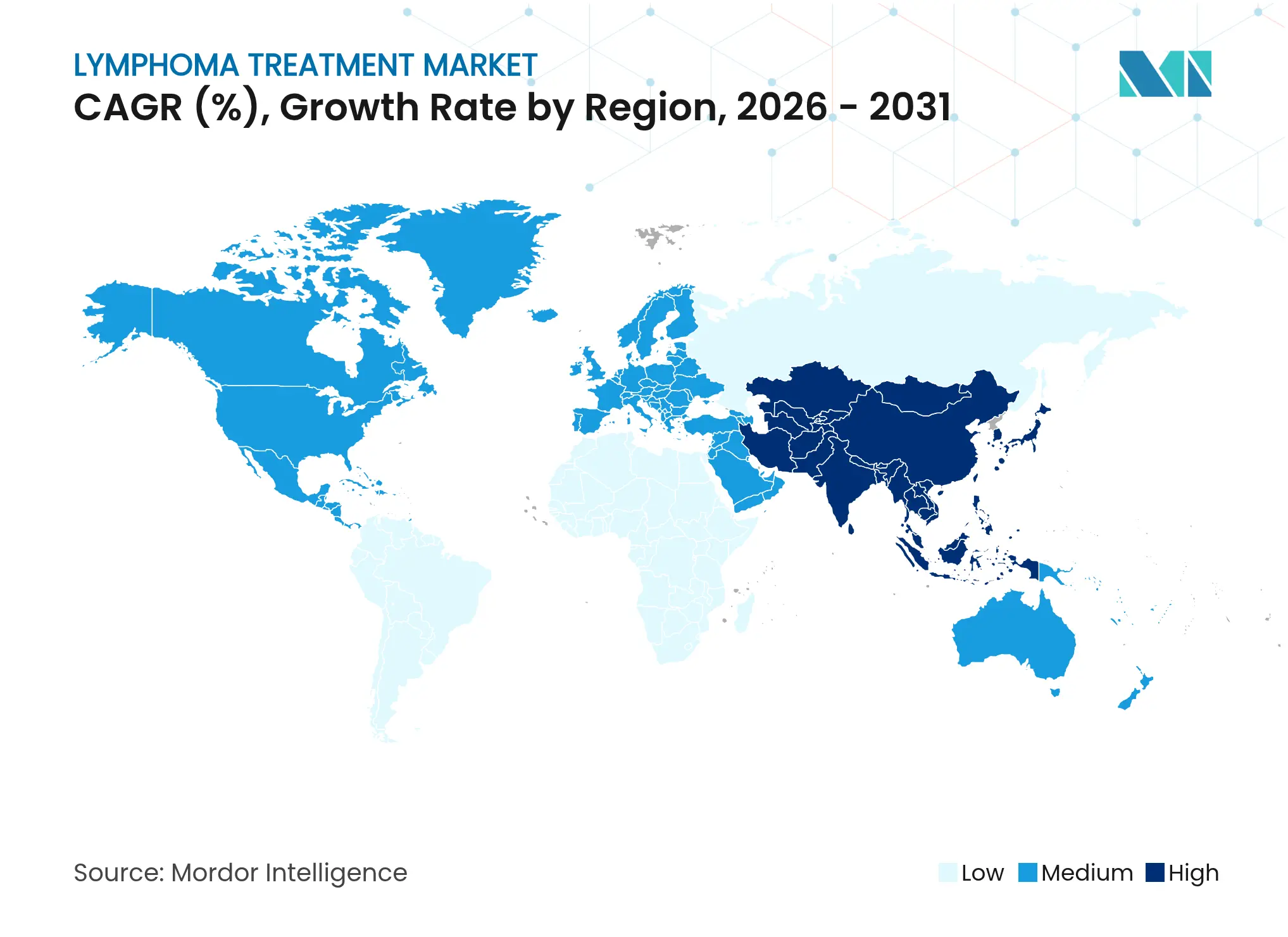

- By geography, North America dominated with 34.20% revenue share in 2025, whereas Asia Pacific is projected to post the fastest 10.54% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lymphoma Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Incidence Of Lymphoma

Rising Incidence Of Lymphoma

| 1.2% | Global, with highest impact in aging populations of North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

1.2%

|

Geographic Relevance

:

Global, with highest impact in aging

populations of North America & Europe

|

Impact Timeline

:

Long term (≥ 4 years)

|

Expanding Approvals For Novel

Immunotherapies

Expanding Approvals For Novel

Immunotherapies

| 1.8% | North America & EU leading, expanding to APAC | Medium term (2-4 years) | |||

Ageing Population & Improved

Diagnostics

Ageing Population & Improved

Diagnostics

| 1.5% | Global, with accelerated impact in developed markets | Long term (≥ 4 years) | |||

AI-Enabled Histopathology

Stratification

AI-Enabled Histopathology

Stratification

| 1.1% | North America & EU core, spill-over to APAC | Medium term (2-4 years) | |||

Decentralised Clinical-Trial

Enrolment

Decentralised Clinical-Trial

Enrolment

| 0.9% | Global, with early gains in North America, Europe, Australia | Short term (≤ 2 years) | |||

Commercialization Of Off-The-Shelf

Bispecific T-Cell Engagers

Commercialization Of Off-The-Shelf

Bispecific T-Cell Engagers

| 0.7% | North America & EU, expanding to emerging markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Incidence of Lymphoma

Lymphoma cases continue to climb as populations age and diagnostic reach broadens, especially in North America and Europe where individuals over 60 represent the fastest-growing demographic.[1]Raquel Aguiar-Ibáñez, “Differences Between Intravenous and Subcutaneous Modes of Administration in Oncology From the Patient, Healthcare Provider, and Healthcare System Perspectives: A Systematic Review,” PubMed, pubmed.ncbi.nlm.nih.govAdvanced imaging and molecular assays uncover earlier-stage disease, enlarging the treatment-eligible cohort and supporting sustained expansion of the lymphoma treatment market. Non-Hodgkin subtypes dominate new diagnoses, reinforcing demand for targeted CD19 and CD20 agents. Hospital networks respond by adding hematology services and training specialists to cope with escalating patient volume. This demand underpins long-term revenue visibility for drug makers and device suppliers.

Expanding Approvals for Novel Immunotherapies

Regulators granted odronextamab conditional European clearance in 2024 and scheduled a final US decision for July 2025, underscoring synchronized agency support for bispecific antibodies. Clinical data showing 80% overall and 73% complete response rates highlight strong therapeutic value, accelerating uptake once commercial supply stabilizes. The FDA’s Regenerative Medicine Advanced Therapy designation for LYL314 further boosts confidence in next-wave CAR-T constructs. Faster approvals shorten development cycles and lift the lymphoma treatment market by expanding the arsenal of high-value assets.

Ageing Population & Improved Diagnostics

AI-assisted digital pathology platforms automate subtype identification, shaving days off diagnostic turnaround and guiding precise therapy choices. Coupled with longer life expectancy, earlier detection increases the treated population. Developed markets feel the greatest effect as seniors now comprise more than 20% of total residents, translating into sustained demand for oncology services. Better diagnostics also support clinical-trial screening, enriching datasets and hastening label expansions that feed market growth.

AI-Enabled Histopathology Stratification

Machine-learning algorithms now recognize subtle morphologic patterns that previously required expert hematopathologists, democratizing high-level diagnostics across community settings. Validated tools deliver accuracy gains and reduce interpretation variability, promoting standardized treatment pathways that elevate outcomes and reinforce confidence in advanced modalities. Emerging economies stand to benefit as AI compensates for specialist shortages, further widening lymphoma treatment market penetration.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost Of Advanced Therapies

High Cost Of Advanced Therapies

| -0.8% | Global, with highest impact in emerging markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-0.8%

|

Geographic Relevance

:

Global, with highest impact in

emerging markets

|

Impact Timeline

:

Long term (≥ 4 years)

|

Safety Concerns (CRS,

Neuro-Toxicity)

Safety Concerns (CRS,

Neuro-Toxicity)

| -1.2% | Global, with regulatory focus in North America & EU | Medium term (2-4 years) | |||

Lengthy Regulatory & HTA

Processes

Lengthy Regulatory & HTA

Processes

| -0.9% | EU & emerging markets primarily | Medium term (2-4 years) | |||

Cell-Therapy Manufacturing

Bottlenecks

Cell-Therapy Manufacturing

Bottlenecks

| -0.6% | Global, with acute impact in North America & EU | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Advanced Therapies

Personalized CAR-T procedures routinely exceed USD 500,000 per patient, and total care costs can climb to USD 1 million when hospitalization and adverse-event management are included. Budget pressures trigger strict reimbursement criteria and elongated health-technology assessments that delay access. Emerging economies grapple with affordability despite initiatives such as Brazil’s USD 35,000 domestic CAR-T program, which aims to close the cost gap. Long-term economic headwinds temper the growth runway for premium-priced regimens and compel payers to favor cost-effective alternatives.

Safety Concerns (CRS, Neuro-Toxicity)

Cytokine-release syndrome affects more than half of CAR-T and bispecific recipients, necessitating intensive monitoring and adding hospital stay days. Neurotoxicity risks further complicate protocols and limit use in frail populations. Physicians in community settings often defer referrals to specialized centers, creating under-treatment pockets. Persistent safety vigilance elevates operating costs for providers and slows full-fledged diffusion of otherwise efficacious modalities.

Segment Analysis

By Disease Type: Non-Hodgkin Lymphoma Retains Dominance

Non-Hodgkin lymphoma held 82.87% of the lymphoma treatment market share in 2025, supported by the broad availability of CD19- and CD20-directed agents alongside diverse clinical-trial pipelines. The lymphoma treatment market size for this segment is set to widen at an 11.02% CAGR through 2031 on the back of highly active bispecific antibodies that deliver 80% response rates in relapsed settings. B-cell subtypes drive bulk revenue, while T-cell variants attract intensified R&D to close therapy gaps. Hodgkin lymphoma remains smaller but benefits from brentuximab vedotin combinations that boost survival metrics and reinforce established protocols. Future growth for both disease segments rides on earlier-line integration of novel agents and adaptive dosing regimens that improve tolerability.

Emerging precision tools, including molecular classifiers and minimal residual disease monitoring, facilitate subtype-specific care pathways. These enhancements raise cure prospects for aggressive disease and expand maintenance strategies for indolent forms. As a result, payer value perception strengthens, backing broader reimbursement and supporting steady volume gains across mature and nascent markets alike.

Note: Segment shares of all individual segments available upon report purchase

By Type of Therapy: CAR-T Leads Growth, Immunotherapy Holds Scale

Immunotherapy preserved a 36.05% slice of 2025 revenue, anchored by rituximab and checkpoint inhibitors whose label breadth spans multiple lines. Biosimilar entry, such as Rixathon, injects cost competition and widens reach without eroding overall spend given elastic demand curves. In contrast, CAR-T therapies, though representing a smaller baseline, are forecast to climb at 12.05% CAGR as constructs like LYL314 post 88% response rates in large B-cell lymphoma. The lymphoma treatment market size attached to CAR-T could nearly triple by 2031 if manufacturing hurdles ease and payers adopt outcome-based contracts.

Targeted kinase inhibitors and antibody-drug conjugates round out the portfolio, offering oral or single-agent alternatives for patients ineligible for intensive therapy. Chemotherapy remains the backbone in frontline combinations, yet its share gradually tapers as biologics displace cytotoxics in first-line and maintenance settings.

By Mode of Administration: Subcutaneous Convenience Gains Ground

Intravenous infusions commanded 69.10% lymphoma treatment market share in 2025 because many complex regimens require controlled delivery and close monitoring. The lymphoma treatment market size attached to intravenous formats continues to grow, though at a slower pace as subcutaneous options capture preference-driven demand. Subcutaneous nivolumab’s regulatory progress spotlights the trend toward quick clinic visits and eventual home dosing. Clinical parity with IV formulations, plus reduced chair time, drives hospital efficiency and patient satisfaction.

Oral agents cater to chronic kinase-inhibitor therapy, particularly in relapsed scenarios where outpatient management dominates. Device innovators refine on-body injectors capable of tolerating large-volume biologics, positioning subcutaneous delivery for double-digit expansion through 2031.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Stay Core While Home-Care Accelerates

Hospitals remain the principal venue, absorbing 60.74% of spending in 2025 due to the need for intensive care resources when adverse events such as CRS arise. Academic centers strengthen this dominance by integrating clinical trials and advanced imaging that community practices may lack. Nonetheless, home-care services are projected to log a 9.92% CAGR as subcutaneous biologics and remote monitoring technologies mature. Payers encourage at-home infusions to cut facility fees, spurring dedicated oncology-nursing networks and digital adherence solutions that bolster safety.

Specialty cancer centers emerge as hybrid models, combining advanced capabilities with outpatient workflow efficiency. They attract referrals for cutting-edge therapies while alleviating bed pressure on tertiary hospitals.

Geography Analysis

North America retained a 34.20% revenue share in 2025, underpinned by integrated payer systems, numerous certified CAR-T centers, and strong clinical-research funding. The region’s streamlined FDA pathways allow median 6-month review times for breakthrough submissions, offering manufacturers early cash-flow realization. NICE’s subsequent endorsement of lisocabtagene maraleucel shows cross-Atlantic policy alignment that speeds post-approval diffusion.

Europe houses robust academic networks and a cohesive regulatory bloc, yet variable HTA timelines lengthen full market rollout. Conditional approvals, like odronextamab’s, demonstrate commitment to therapeutic innovation even as payers scrutinize cost-effectiveness. Partnerships between national health services and manufacturers pilot outcome-based payment models to reconcile high list prices with budgetary prudence.

Asia Pacific is projected to chart a 10.54% CAGR on the back of demographic expansion, heightened disease awareness, and capacity investments such as BeiGene’s USD 800 million biologics plant. Government insurance schemes in China and India broaden coverage while local trial networks cut development costs and accelerate enrolment. South America and the Middle East & Africa show early-stage momentum; Brazil’s low-cost CAR-T blueprint exemplifies inventive approaches to affordability that could inspire neighboring markets.

Competitive Landscape

Market Concentration

Roughly 20 sizable competitors vie across therapy classes, rendering the space moderately fragmented. Gilead’s Kite Pharma and Novartis anchor the CAR-T category, backed by deep manufacturing footprints and global logistics. Pfizer and Regeneron lead the antibody segment, advancing next-generation bispecifics and subcutaneous formats. Mid-cap biotechs provide innovation influx, as illustrated by Lyell Immunopharma’s purchase of ImmPACT Bio that delivers dual-antigen CAR-T capability.[3]Lyell Immunopharma, “Lyell Immunopharma to Acquire ImmPACT Bio,” ir.lyell.com

Capacity scale-up remains a strategic imperative: Legend Biotech’s doubling of Carvykti production exemplifies the race to secure supply and margin advantages. Subcutaneous formulation know-how forms another competitive axis, with device collaborations delivering proprietary injection systems. White-space opportunities persist in T-cell lymphoma, pediatric settings, and maintenance regimens, prompting joint-development pacts between large pharma and diagnostics start-ups.

Regulatory agility and payer engagement differentiate leaders from laggards. Companies that package real-world evidence and flexible pricing into submissions win earlier reimbursements, accelerating adoption curves. Digital-pathology partnerships strengthen companion-diagnostic locks that protect market share by hard-wiring drug selection to proprietary tests.

Lymphoma Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lyell Immunopharma secured FDA RMAT designation for LYL314 after a 94% response rate in large B-cell lymphoma patients.

- April 2025: NICE approved brentuximab vedotin plus chemotherapy for advanced Hodgkin lymphoma, benefitting an estimated 800 UK patients annually.

- February 2025: The US FDA accepted Regeneron’s BLA resubmission for odronextamab in relapsed/refractory follicular lymphoma; action date set for Jul 30 2025.

- February 2025: NICE recommended lisocabtagene maraleucel for large B-cell lymphoma patients unresponsive to frontline therapy, aiding roughly 600 English patients each year.

Table of Contents for Lymphoma Treatment Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence Of Lymphoma

- 4.2.2Expanding Approvals For Novel Immunotherapies

- 4.2.3Ageing Population & Improved Diagnostics

- 4.2.4AI-Enabled Histopathology Stratification

- 4.2.5Decentralised Clinical-Trial Enrolment

- 4.2.6Commercialization Of Off-The-Shelf Bispecific T-Cell Engagers

- 4.3Market Restraints

- 4.3.1High Cost Of Advanced Therapies

- 4.3.2Safety Concerns (CRS, Neuro-Toxicity)

- 4.3.3Lengthy Regulatory & HTA Processes

- 4.3.4Cell-Therapy Manufacturing Bottlenecks

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Disease Type

- 5.1.1Hodgkin Lymphoma

- 5.1.2Non-Hodgkin Lymphoma

- 5.1.2.1B-cell NHL

- 5.1.2.2T-cell NHL

- 5.2By Type of Therapy

- 5.2.1Chemotherapy

- 5.2.2Immunotherapy

- 5.2.3Targeted Therapy

- 5.2.4CAR-T Cell Therapy

- 5.2.5Radiotherapy

- 5.2.6Stem-Cell Transplantation

- 5.3By Mode of Administration

- 5.3.1Intravenous

- 5.3.2Sub-cutaneous

- 5.3.3Oral

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Specialty Cancer Centres

- 5.4.3Academic & Research Institutes

- 5.4.4Home-care Settings

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1AstraZeneca

- 6.3.2Bayer AG

- 6.3.3Biogen Inc.

- 6.3.4Bristol Myers Squibb

- 6.3.5Johnson & Johnson

- 6.3.6Merck & Co.

- 6.3.7Seagen Inc.

- 6.3.8Takeda Pharmaceutical

- 6.3.9Teva Pharmaceutical

- 6.3.10F. Hoffmann-La Roche Ltd

- 6.3.11Novartis AG

- 6.3.12Gilead Sciences

- 6.3.13AbbVie Inc.

- 6.3.14Pfizer Inc.

- 6.3.15Amgen Inc.

- 6.3.16Eli Lilly & Co.

- 6.3.17Incyte Corp.

- 6.3.18BeiGene Ltd.

- 6.3.19Legend Biotech

- 6.3.20Allogene Therapeutics

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Lymphoma Treatment Market Report Scope

As per the scope of the report, Lymphoma is a type of cancer that affects the lymphatic system, a key part of the body's immune system. The lymphatic system includes lymph nodes, spleen, thymus gland, and bone marrow, which work together to help the body fight infections and diseases. The lymphoma treatment market is segmented as diseases type into hodgkin lymphoma, and non-hodgkin lymphoma. By type of therapy, the lymphoma treatment market is segmented into chemotherapy, immunotherapy, targeted therapy, and others. By geography the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.