Luxury Shuttle Bus Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

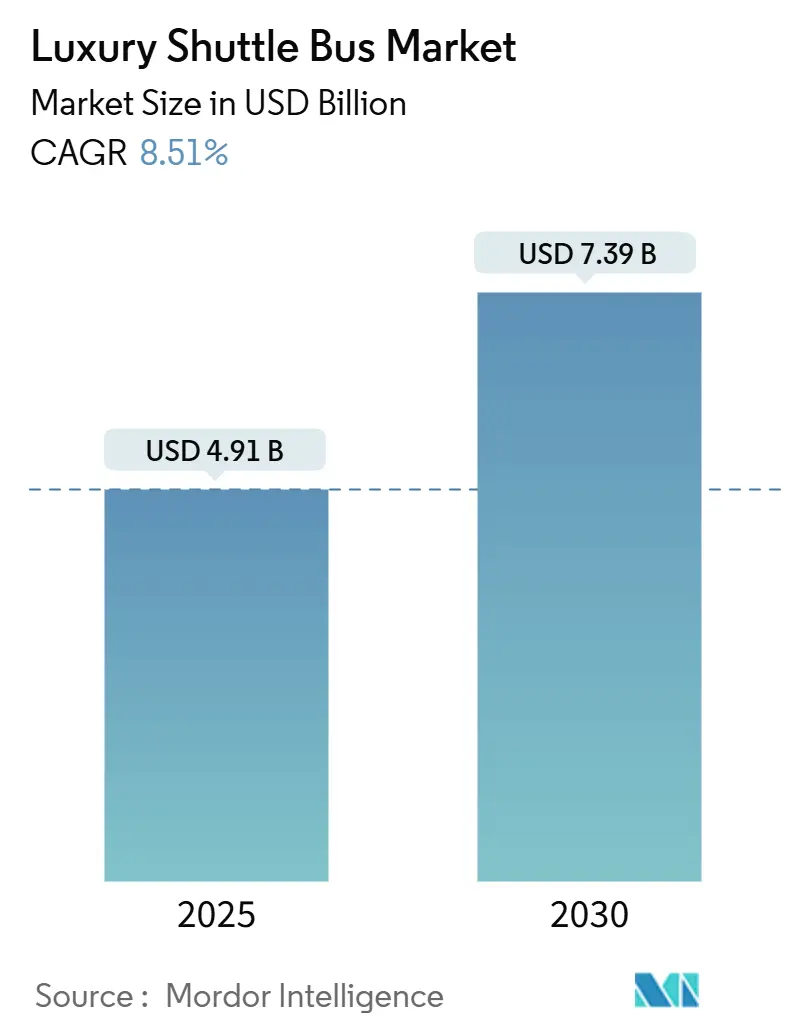

| Market Size (2025) | USD 4.91 Billion |

| Market Size (2030) | USD 7.39 Billion |

| Growth Rate (2025 - 2030) | 8.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

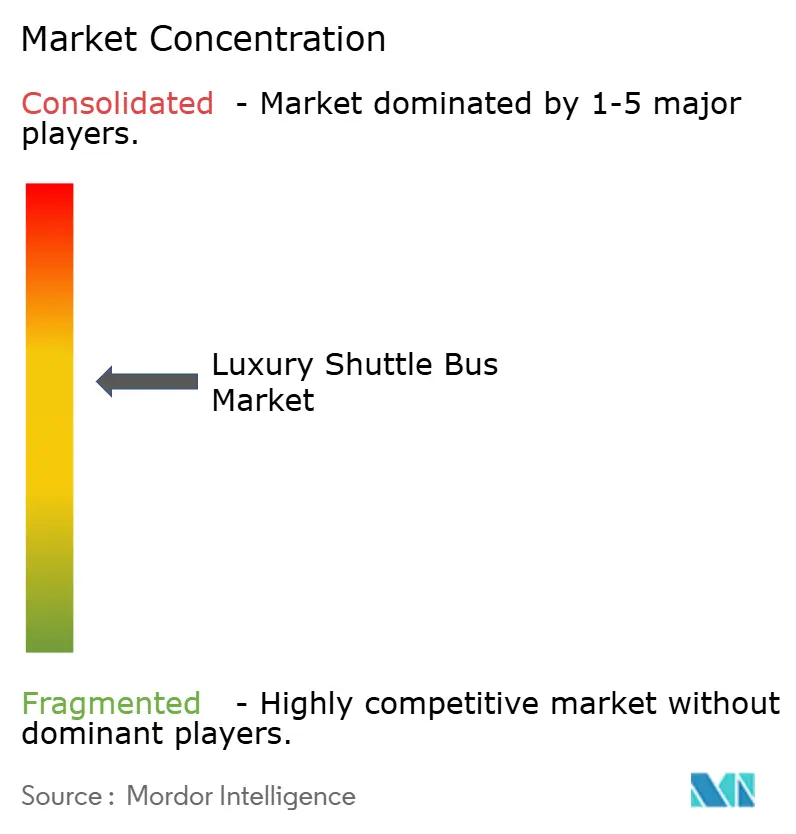

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Shuttle Bus Market Analysis by Mordor Intelligence

The luxury shuttle bus market size stood at USD 4.91 billion in 2025 and is forecast to reach USD 7.39 billion by 2030, registering an 8.51% CAGR over 2025-2030. This growth trajectory reflects sustained corporate sustainability mandates, the rebound of premium tourism, and generous electrification incentives that reshape fleet economics across the luxury shuttle bus market. Asia-Pacific is witnessing rapid expansion, fueled by substantial infrastructure investments and a manufacturing scale, all driven by urban mobility demands and government-supported transport modernization. As the industry pivots towards sustainability and low-emission solutions, battery-electric propulsion emerges as the favored powertrain. In response, fleet operators are strategically consolidating. By acquiring complementary services and platforms, they achieve efficiencies in route planning, data integration, and capital deployment. This consolidation boosts their negotiating power with OEMs and suppliers and strengthens a cycle of competitiveness driven by scale.

Key Report Takeaways

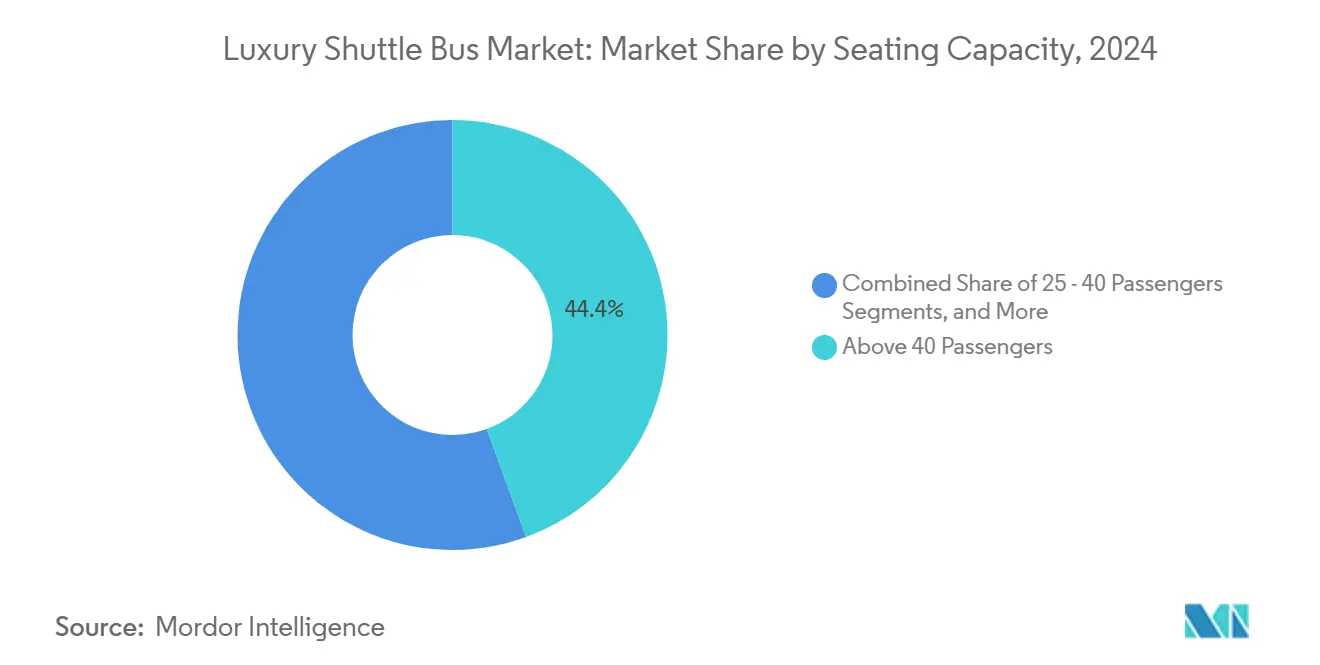

- By seating capacity, coaches with more than 40 seats commanded a 44.42% share of the luxury shuttle bus market in 2024. Sub-25-seat shuttles are forecast to grow at a 9.26% CAGR to 2030.

- By propulsion type, diesel and gasoline powertrains accounted for 34.32% of the luxury shuttle bus market size in 2024. Battery-electric models are advancing at a 12.41% CAGR through 2030.

- By application, tourist coach services held 34.72% of the luxury shuttle bus market share in 2024. Corporate transport is projected to expand at a 9.88% CAGR through 2030.

- By end-user, Private operators captured a 44.23% share of the luxury shuttle bus market in 2024. Hospitality and tourism providers registered the highest 9.12% CAGR over 2025-2030.

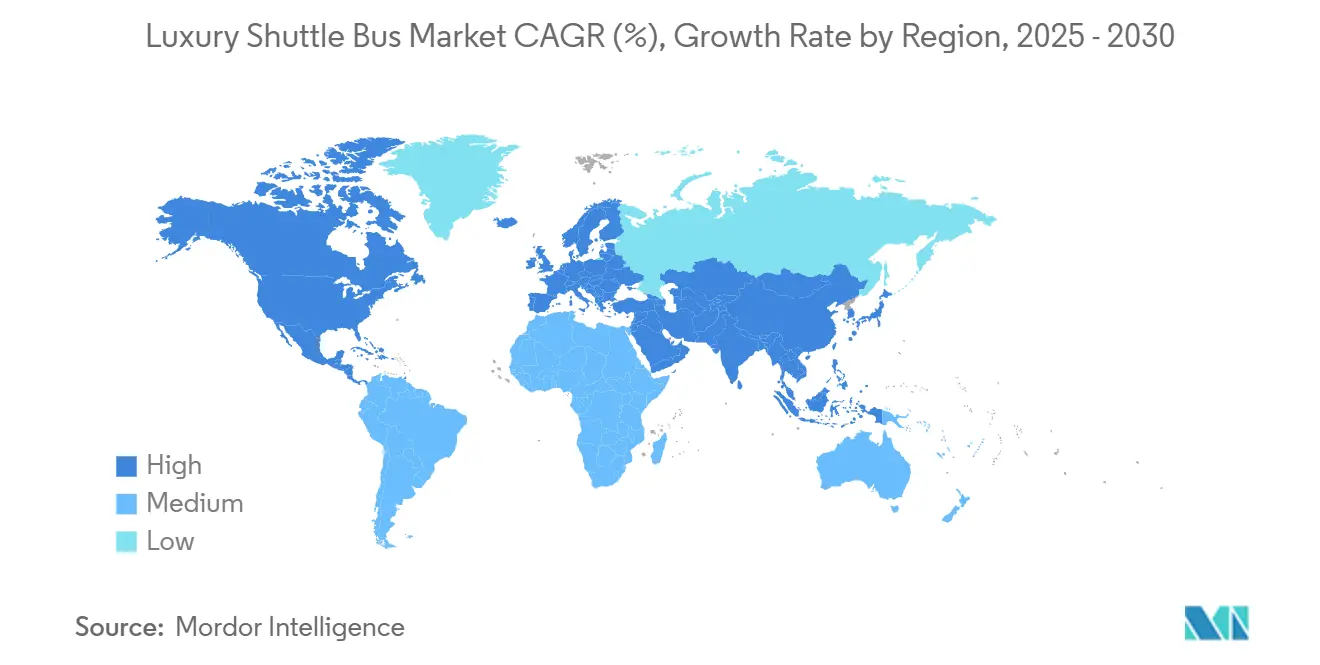

- By geography, Asia-Pacific led with a 45.28% luxury shuttle bus market share in 2024. Asia-Pacific is also set for the quickest 9.28% CAGR during the forecast period.

Global Luxury Shuttle Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Incentives Lowering TCO | +2.3% | North America, Europe, China leading adoption | Medium term (2-4 years) |

| Rising Demand for Premium and Inter-City Travel | +2.1% | Global, with early gains in Asia-Pacific, North America | Medium term (2-4 years) |

| Sustainability-Driven Corporate Shuttle Programs | +1.8% | North America and Europe, spill-over to Asia-Pacific core | Short term (≤ 2 years) |

| Airport Growth Boosting Landside Connectivity | +1.5% | Global, concentrated in major hub airports | Long term (≥ 4 years) |

| Luxury Commuter Clubs via Subscription Models | +0.7% | North America urban centers, expanding to Europe | Long term (≥ 4 years) |

| Hygiene-Focused Shift to Amenity-Rich Hospital Shuttles | +0.8% | Global, with regulatory influence in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electrification Incentives Lowering TCO

Regions such as California, the European Union, and specific Asian markets provide significant subsidies, sometimes reaching 30% of vehicle purchase prices. These government incentives are crucial in promoting the adoption of Class-C electric coaches, aiming to electrify fleets and cut public and private transport emissions. OEMs such as Prevost and Daimler have collectively invested in dedicated R&D and factory tooling for luxury battery-electric buses. Falling battery pack costs allow operators to reach five-year payback periods even on premium configurations.

Corporate Employee-Shuttle Sustainability Programs

Companies are integrating zero-emission shuttle programs into their ESG scorecards to enhance environmental impact and employee mobility. These programs support contract renewals, route expansions, and reduce Scope-3 emissions by replacing individual vehicles with shared electric transport.

Beyond sustainability, improved campus accessibility and reduced parking demands enhance employee experience. Digital platforms now provide real-time attendance tracking and carbon dashboards, offering HR teams metrics for ESG disclosures. This model is gaining traction globally, especially in Europe, where tax credits incentivize collective mobility solutions. Zero-emission shuttles are central to corporate transport strategies, aligning environmental goals with operational efficiency and regulatory support.

Growing Premium Tourism and Inter-City Travel Demand

Premium tourism is reviving swiftly as travelers prioritize spacious seating, onboard connectivity, and higher hygiene standards. Operators are retrofitting fleets with Wi-Fi, reclining leather seats, and concierge-grade service, helping the tourist-coach application maintain a significant share of the luxury shuttle bus market in 2024. Rising executive travel in India and Southeast Asia has further widened the revenue base, allowing fleet managers to cross-utilize vehicles between tourist and corporate contracts during shoulder seasons. Longer-haul point-to-point services also benefit, as high-income customers seek a quieter alternative to low-cost airlines.

Airport Infrastructure Boom and Landside Connectivity

Modernization programs such as LAX’s USD 5.5 billion Landside Access Modernization Project allocate curbside priority and exclusive staging areas for premium shuttles[1]“2025 Landside Access Modernization Project Overview,”, California Energy Commission, energy.ca.gov. Coordinated flight-arrival APIs allow fleet operators to synchronize dispatch times, raising load factors and improving passenger dwell time. As airports mandate lower-emission ground fleets, luxury shuttle providers gain first-mover advantages by deploying electric or hybrid coaches compliant with stringent particulate-matter limits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition and Customization Costs | -1.4% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Competition from Ride-Hailing & Premium Rail | -1.1% | North America & Europe, expanding to urban Asia | Medium term (2-4 years) |

| Chauffeur Shortage Driving Wage Inflation | -0.9% | Global, most severe in developed markets | Long term (≥ 4 years) |

| Limited Curb/Station Access in Dense CBDs | -0.6% | Urban centers globally, regulatory influence varies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition From Ride-Hailing and Premium Rail

Ride-hail apps offer business travelers instant availability, while high-speed trains in Europe and Asia compress intercity travel times. Luxury shuttle operators counter by bundling door-to-door transfers and offering loyalty programs that cap monthly out-of-pocket expenses for frequent travelers. Regulatory changes granting shuttles access to bus-priority lanes in select cities offset lost dwell-time advantages and restore timetable reliability.

Limited Curb/Station Slots in Dense CBDs

Street-level loading areas in financial districts are heavily contested among taxis, delivery vans, and ride-hail pickups, forcing luxury shuttles to cycle around blocks or shift to off-peak slots[2]“San Francisco Commuter Shuttle Permit Program,", San Francisco Municipal Transportation Agency, sfmta.com. While useful in San Francisco, municipal permitting schemes are not yet widely replicated elsewhere, compelling operators to negotiate private-property staging at premium hourly fees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Seating Capacity: Compact Solutions Drive Urban Adoption

Vehicles carrying 40 or more passengers retained a 44.42% share of the luxury shuttle bus market in 2024, serving high-volume tourist corridors and airport routes. Yet the sub-25-seat class is scaling faster at 9.26% CAGR through 2030, propelled by companies that need multiple departures per hour rather than a single large coach. Compact units cut curb-side dwell times and navigate narrow downtown streets without sacrificing premium fittings such as calf-support loungers or full-width infotainment screens.

OEMs have responded with purpose-built micro-coaches featuring low-floor access, modular luggage racks, and Bluetooth-enabled seat controls. For operators, the smaller footprint reduces depot space and shortens charging cycles, improving asset turns. Mid-range 25-40 seat shuttles remain the workhorse for corporate campuses that balance density with comfort, aided by lightweight composites that trim energy use.

By Propulsion Type: Electric Transition Accelerates Premium Positioning

Internal-combustion models commanded a 34.32% share of the luxury shuttle bus market in 2024. Yet battery-electric units are outpacing every other powertrain at 12.41% CAGR through 2030, helped by back-to-base operating profiles that simplify overnight charging. Several transit authorities now stipulate zero-tailpipe requirements in bid documents, nudging group-travel organizers toward electric charters.

Hybrid and alternative-fuel coaches fill regional niches where charging infrastructure remains sparse. LNG and CNG see uptake on 400-km intercity corridors, while bio-diesel blends allow existing diesel fleets to meet interim carbon thresholds. Electric-first designs also enable panoramic cabin layouts freed from floor-mounted engine bays, enhancing the luxury ambience.

By Application: Corporate Transport Leads Growth Through Sustainability Mandates

Tourist-coach services kept a 34.72% share of the luxury shuttle bus market in 2024; however, corporate transport is sprinting ahead at 9.88% CAGR through 2030, as firms hard-wire commuter shuttles into decarbonization roadmaps. Employee satisfaction surveys show reduced turnover when staff enjoy predictable, Wi-Fi-enabled commutes. Carbon-tracking APIs feed into ESG dashboards, helping CFOs secure green finance lines at lower coupon spreads.

Airport shuttles remain a resilient niche, buoyed by passenger-service contracts embedded in terminal-expansion projects. School and medical coaches gain momentum as districts and hospitals raise safety and hygiene specifications, justifying premium pricing.

By End User: Private Operators Leverage Flexibility Advantages

Private fleets owned by mobility start-ups or hospitality groups held a 44.23% share of the luxury shuttle bus market in 2024. Their agility permits dynamic timetables and premium add-ons such as seat-side catering or concierge baggage service. Hotel chains increasingly bundle shuttle passes within loyalty tiers, boosting occupancy during shoulder seasons. Hospitality and tourism providers are projected to grow at a CAGR of 9.12% through 2030.

Public-sector entities partner with these private specialists to outsource niche or variable-demand routes, minimizing taxpayer exposure to under-utilized assets. Technology-led players integrate booking engines, live ETAs, and fleet telemetry onto a single screen, raising the barrier to entry for smaller rivals.

Geography Analysis

Asia-Pacific dominated the luxury shuttle bus market with a 45.28% revenue contribution in 2024 and is projected to expand at a 9.28% CAGR through 2030. The region benefits from fast-growing premium tourism in China, Japan, and Indonesia, combined with domestic OEM depth that accelerates product iteration cycles. Chinese manufacturers leverage vertical integration to price electric luxury coaches below imported equivalents, spurring fleet replacement across Southeast Asia.

North America remains a lucrative arena as corporate-campus shuttles flourish in tech hubs and entertainment destinations. California’s Innovative Clean Transit rule and San Francisco’s structured shuttle permits underpin early adoption of battery-electric premium coaches. Federal funding for EV infrastructure further sweetens operator economics, ensuring steady contract renewals.

Europe displays a balanced mix of legacy coach builders and aggressive electrification policies. Low-emission zones in London, Paris, and Berlin incentivize operators to upgrade aging diesel fleets, while EU taxonomy rules grant loan-rate discounts for zero-emission assets. Scandinavian tour operators are piloting subscription-based luxury commuter clubs to smooth seasonality and maintain utilization during winter.

Competitive Landscape

Major OEMs and service providers dominate the luxury shuttle bus market, capturing a notable portion of global revenues. This indicates a competitive landscape, albeit with a degree of consolidation, allowing top firms to leverage brand recognition, expansive distribution networks, and economies of scale. Manufacturers like Daimler, Volvo, and BYD lead the charge, each rolling out next-gen electric coaches boasting extended ranges and rapid-charging features.

On the service front, consolidation is gaining momentum: Transportation Charter Services bolstered its West Coast presence by acquiring Royal Coach Tours, and Celebrity Coaches expanded its offerings by purchasing BandWagon RV Rentals. These strategic acquisitions pave the way for back-office efficiencies—from unified dispatch systems to collective procurement—reducing operating costs per mile.

Digital pioneers like Zeelo and Swoop are adopting asset-light strategies, partnering with regional operators for capacity while retaining customer engagement. Their extensive data on rider habits and carbon metrics offer valuable insights to corporate clients, granting them a strategic edge even with limited physical assets. The luxury shuttle bus sector showcases a moderate concentration, with the top five OEMs and service providers commanding a notable slice of global revenues. This landscape hints at a competitive yet somewhat consolidated arena, where dominant players reap rewards from brand prestige, expansive distribution channels, and scale economies.

Luxury Shuttle Bus Industry Leaders

-

Daimler Truck AG

-

King Long United Automotive Industry Co. Ltd.

-

Yutong Bus Co., Ltd.

-

BYD Company Limited

-

AB Volvo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Celebrity Coaches, a leading provider of luxury transportation services tailored for the entertainment sector, acquired BandWagon RV Rentals. BandWagon specializes in mid-tier RV solutions for touring. This merger empowers Celebrity Coaches to present an expanded fleet and tailored offerings, catering to the dynamic needs of its clientele.

- March 2024: Volvo Buses expanded its global electric mobility portfolio by introducing services for intercity transportation. The Volvo BZR Electric platform supports city, intercity, and commuter operations. The platform offers multiple configurations to help operators worldwide implement efficient and sustainable transportation services.

Global Luxury Shuttle Bus Market Report Scope

| Below 25 Passengers |

| 25 - 40 Passengers |

| Above 40 Passengers |

| Diesel / Gasoline |

| Alternate Fuels (CNG, LNG, LPG) |

| Battery Electric Buses |

| Hybrid Electric Buses |

| Corporate Transport |

| Government Use |

| School Coach |

| Airport Shuttle |

| Hospital & Medical Coach |

| Tourist Coach |

| Others |

| Private Operators |

| Public Transit Authorities |

| Hospitality & Tourism Providers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Seating Capacity | Below 25 Passengers | |

| 25 - 40 Passengers | ||

| Above 40 Passengers | ||

| By Propulsion Type | Diesel / Gasoline | |

| Alternate Fuels (CNG, LNG, LPG) | ||

| Battery Electric Buses | ||

| Hybrid Electric Buses | ||

| By Application | Corporate Transport | |

| Government Use | ||

| School Coach | ||

| Airport Shuttle | ||

| Hospital & Medical Coach | ||

| Tourist Coach | ||

| Others | ||

| By End User | Private Operators | |

| Public Transit Authorities | ||

| Hospitality & Tourism Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current revenue size of the luxury shuttle bus market?

The luxury shuttle bus market size reached USD 4.91 billion in 2025 and is on track to hit USD 7.39 billion by 2030.

Which region leads growth in premium shuttle demand?

Asia-Pacific commands the largest share at 45.28% and posts the fastest 9.28% CAGR owing to manufacturing scale and infrastructure investment.

How fast are battery-electric luxury coaches growing?

Battery-electric models are forecast to expand at a 12.41% CAGR through 2030, the highest among all propulsion types.

Why are corporate shuttles gaining traction?

The companies integrate employee shuttle programs into ESG targets, driving the segment’s 9.88% CAGR over 2025-2030.

What challenges do luxury shuttle operators face in urban centers?

Intense competition for curb space and limited station slots in dense downtowns constrain scheduling efficiency and heighten permit costs.

Page last updated on: