Luxury Yacht Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

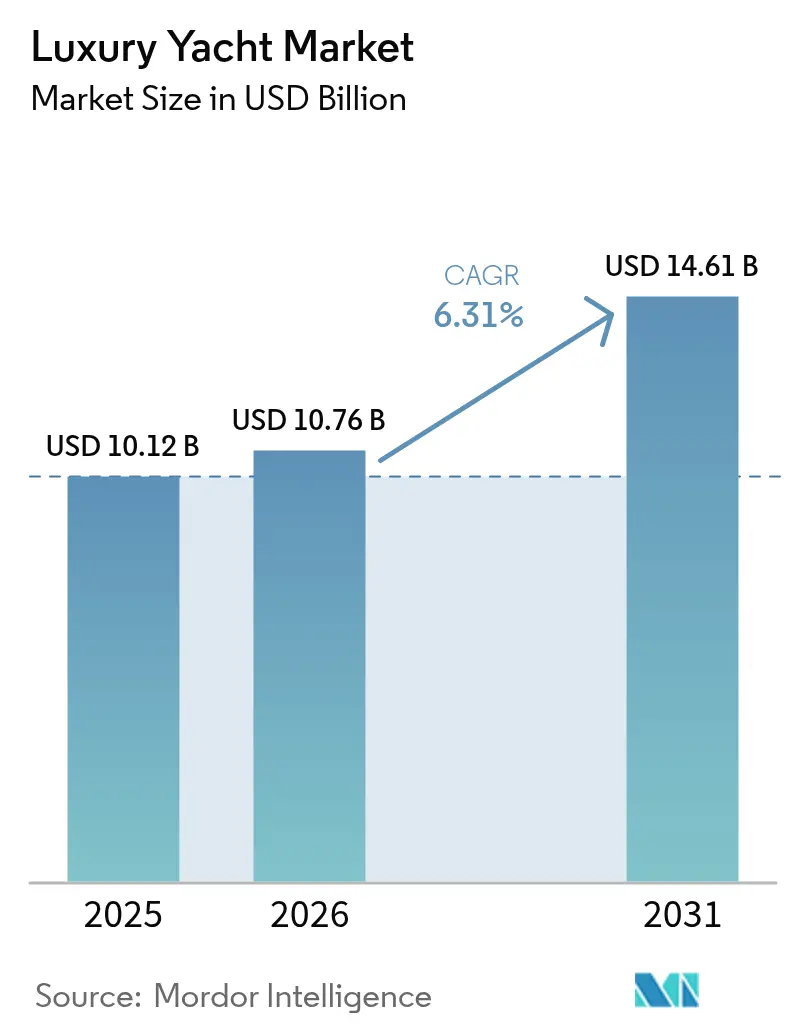

| Market Size (2026) | USD 10.76 Billion |

| Market Size (2031) | USD 14.61 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

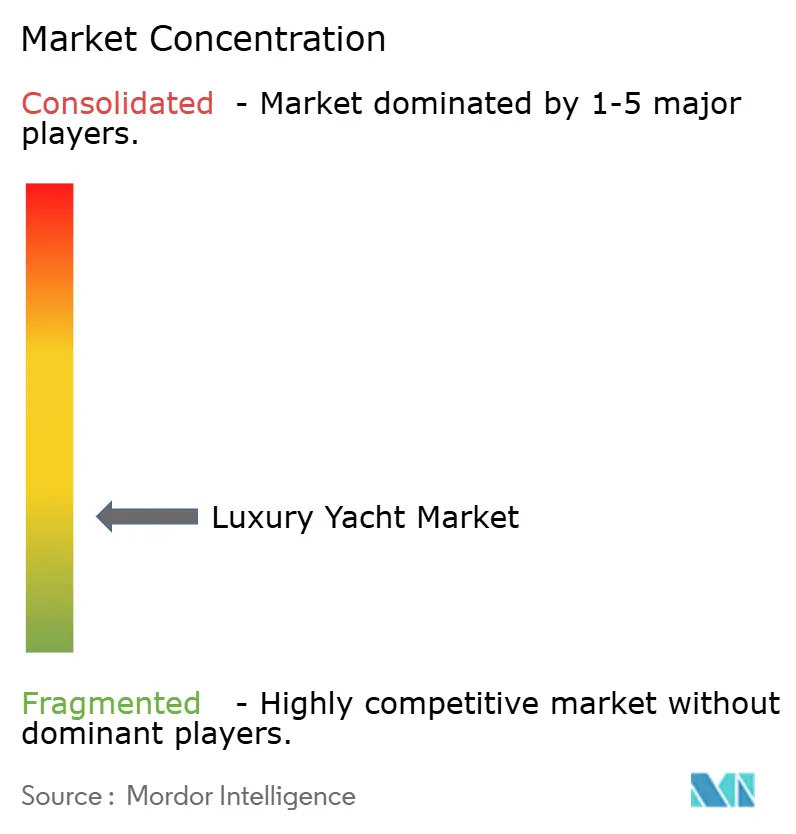

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Yacht Market Analysis by Mordor Intelligence

Luxury yacht market size in 2026 is estimated at USD 10.76 billion, growing from 2025 value of USD 10.12 billion with 2031 projections showing USD 14.61 billion, growing at 6.31% CAGR over 2026-2031. Current momentum stems from the rise in ultra-high-net-worth individuals (UHNWIs), rapid propulsion innovation, and a cultural shift toward experiential assets. Hybrid and electric systems gain traction as builders seek compliance with future IMO greenhouse-gas rules, while expedition-style yachts broaden cruising grounds beyond the Mediterranean. Consolidation among builders and marina operators intensifies, with private-equity funds targeting infrastructure that secures berth availability. Meanwhile, tariffs on European, Chinese, and Taiwanese vessels create a near-term pricing advantage for U.S. yards and could prompt regional reshoring in the luxury yacht market.

Key Report Takeaways

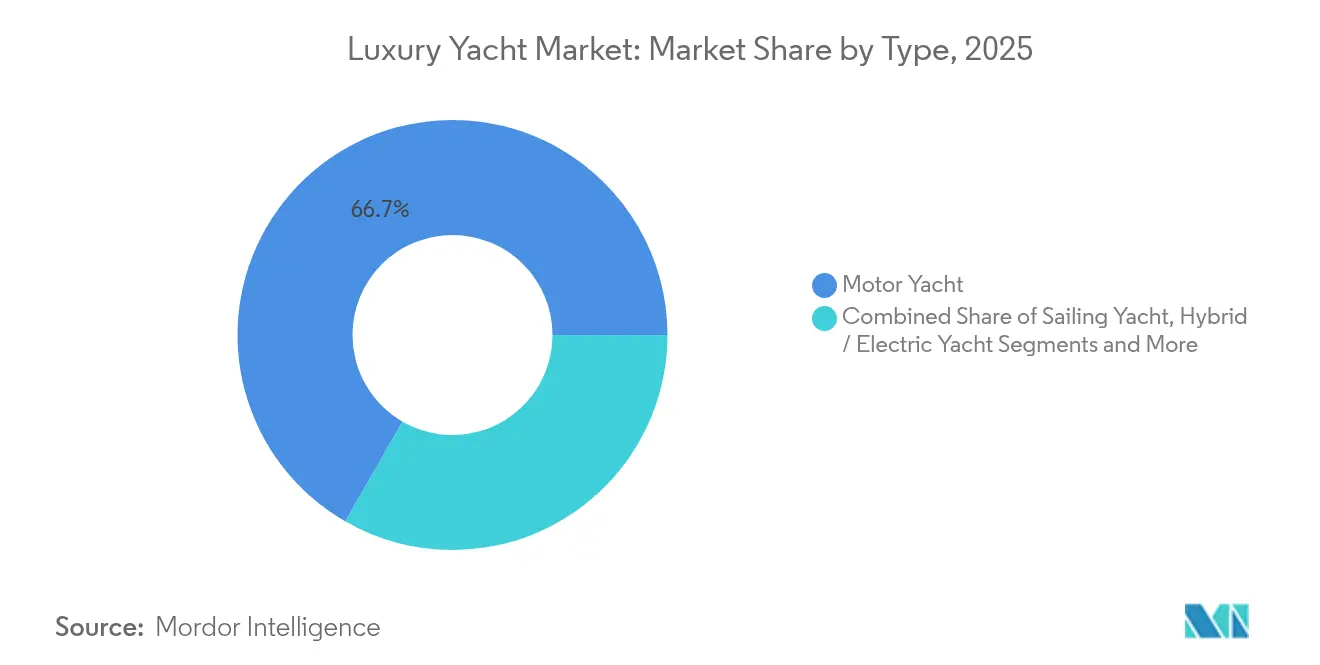

- By type, motor yachts held 66.68% of the luxury yacht market share in 2025, whereas hybrid-electric yachts are projected to post a 10.09% CAGR through 2031.

- By size, vessels measuring 20 to 40 m accounted for 43.62% of the luxury yacht market size in 2025, while yachts above 80 m are forecast to expand at 11.74% CAGR to 2031.

- By hull material, fiberglass/composite commanded a 55.68% share of the luxury yacht market in 2025; carbon-fiber hulls are set to grow at a 12.98% CAGR through 2031.

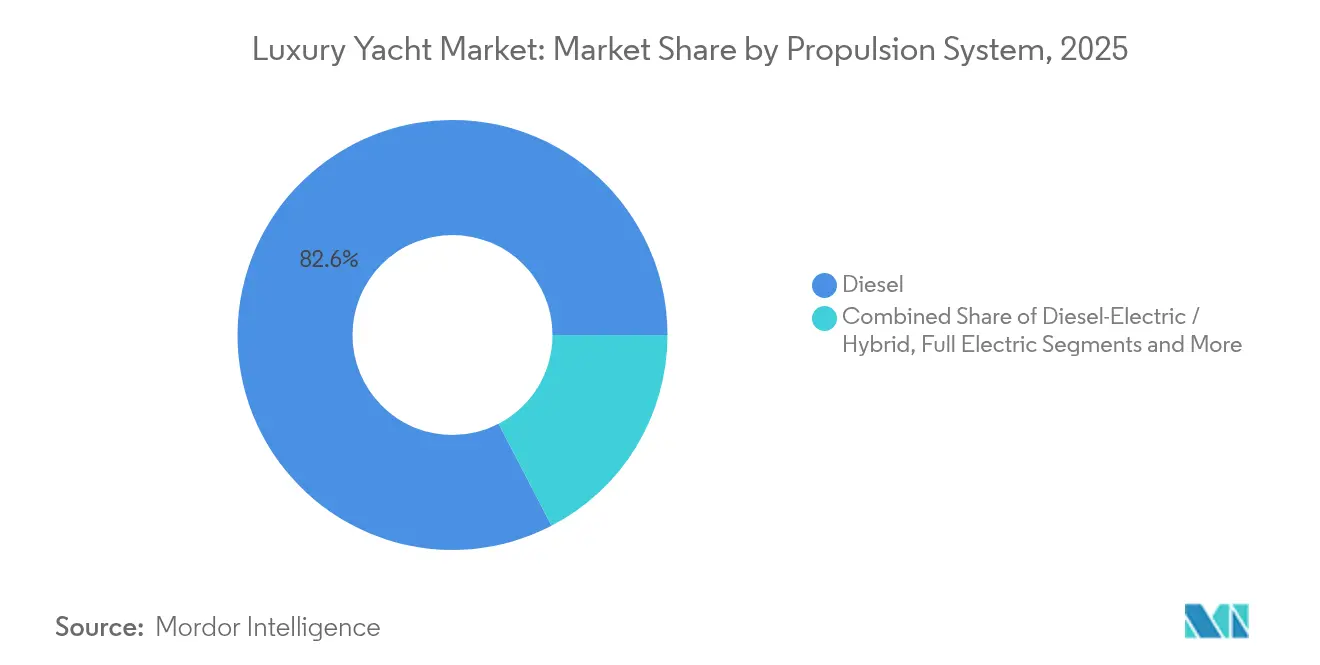

- By propulsion system, diesel retained an 82.62% share of the luxury yacht market in 2025, yet diesel-electric/hybrid systems will accelerate at a 9.12% CAGR through 2031.

- By end user, private individuals held a 60.74% share of the luxury yacht market in 2025, whereas fractional-ownership clubs are on track for an 11.08% CAGR to 2031.

- By geography, Europe led with a 42.62% share in 2025, while Asia-Pacific is expected to record the fastest 11.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury Yacht Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Yacht-Tourism Boom | +1.2% | Global, with concentration in Mediterranean, Caribbean, Asia-Pacific | Medium term (2-4 years) |

| Rising UHNWIs in Emerging Markets | +1.8% | Asia-Pacific core, spill-over to Middle East and South America | Long term (≥ 4 years) |

| Growing Demand for Expedition/Explorer Yachts | +0.9% | Global, with early gains in Northern Europe, North America | Medium term (2-4 years) |

| Shift Toward Hybrid and Electric Propulsion | +0.7% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Private-Island and Remote-Marina Build-Out | +0.6% | Caribbean, Pacific Islands, Mediterranean | Medium term (2-4 years) |

| Rise of Fractional-Ownership Platforms | +0.8% | North America and Europe, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Yacht-Tourism Boom

Yacht tourism will demonstrate healthy growth, accounting for 26% of the marine economy by 2030. Yacht tourists spend approximately USD 287 daily, nearly double conventional tourists, significantly impacting local economies. The sector benefits from post-pandemic travel preferences favoring private, controlled environments, with overcrowded destinations. Charter companies increasingly invest in larger, more luxurious vessels to capture this premium spending, with yacht sailing programs emerging as the most valued attribute among tourists. Safety training and accessible locations within one hour of transport represent optimal combinations that tourists prefer, driving infrastructure development in emerging cruising destinations.

Rising UHNWIs in Emerging Markets

The ultra-wealthy population is projected to grow considerably by 2028, reaching over 587,000 individuals with a net worth exceeding USD 30 million. Emerging markets drive disproportionate growth, with Vietnam forecasting 95% centi-millionaire growth, India 80%, and Mauritius 75%. These new wealth centers prioritize experiential luxury over traditional assets, with yachts representing passion investments that combine status, privacy, and lifestyle benefits. The shift toward sustainable investments among 20% of UHNW investors creates demand for hybrid and electric propulsion systems. Younger generations increasingly drive wealth mobility and investment decisions, favoring technologically advanced vessels with environmental credentials.

Growing Demand for Expedition/Explorer Yachts

Expedition yachts address evolving owner preferences for remote cruising and adventure experiences beyond traditional Mediterranean and Caribbean circuits. 58 new explorer yachts launched in 2025, including notable vessels like REV Ocean (194.9m) equipped for scientific research and Shackleton (107m) featuring ice-classed hulls for polar cruising[1]"The largest explorer yachts hitting the water in 2025", Boat International, boatinternational.com.. These vessels incorporate hybrid propulsion systems and self-sufficiency features for extended autonomous cruising. The segment benefits owners seeking unique experiences in sensitive marine environments, driving demand for environmentally compatible designs. Damen Yachting's Xplorer 60 represents the first in their luxury expedition range, capable of autonomous cruising and designed for high-latitude regions.

Shift Toward Hybrid and Electric Propulsion

Environmental regulations accelerate the adoption of alternative propulsion systems, with the IMO approving new greenhouse gas requirements taking effect from 2028[2]"IMO MEPC 83: GHG requirements approved, taking effect from 2028", DNV, dnv.com.. EU Emissions Trading System expansion and FuelEU Maritime regulations impact vessels over 5,000 gross tons calling at EU ports, requiring emissions reporting and compliance with greenhouse gas intensity limits. Hybrid systems offer operational flexibility, reduced noise and vibration, and improved fuel efficiency during cruising. Rolls-Royce launched integrated hybrid ship propulsion systems suitable for yachts, with power ranges from 1,000 to 4,000 kilowatts. The world's largest sailing yacht, Sailing Yacht A, demonstrates hybrid system application in luxury vessels, showcasing technology maturation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Ownership and Maintenance Costs | -1.4% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Supply-Chain Bottlenecks for Specialized Components | -0.8% | Global, with concentration in European and North American shipyards | Medium term (2-4 years) |

| Stringent Environmental Emission Regulations | -0.6% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Shortage of Skilled Crew Inflating Operating Costs | -0.9% | Global, particularly acute in Mediterranean and Caribbean | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Ownership and Maintenance Costs

Rising operational expenses strain yacht ownership economics, with Princess Yachts reporting a GBP 61 million loss in 2022 on revenues of GBP 315 million amid challenging market conditions. The company announced 250 workforce reductions due to rising operational costs and challenging global market conditions. Marina costs escalate as premium facilities command higher rates, with Safe Harbor Marinas' USD 5.65 billion valuation reflecting 21 times the estimated 2024 Funds from Operations. Interest rate increases compound financing costs for yacht purchases, while insurance premiums rise due to increased claims and replacement values. These factors drive owners toward fractional ownership models and charter arrangements to distribute costs across multiple users.

Supply-Chain Bottlenecks for Specialized Components

Post-COVID supply chain disruptions persist in yacht manufacturing, with specialized components experiencing extended lead times and cost inflation. The recreational boating market stabilizes after a 40% pandemic surge, creating inventory challenges and production bottlenecks. European shipyards report that 95% currently use or plan to use composite materials, primarily fiberglass and polyester resin, but face procurement challenges for advanced materials. Trade tensions exacerbate supply issues, with President Trump's universal 10% tariff on yacht imports and higher rates for specific countries creating pricing pressures. Chinese-built yachts face 54% tariffs, while EU brands encounter 20% duties, potentially reshaping global supply chains and forcing buyers toward domestic alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Motor Yachts Dominate Despite Electric Surge

In 2025, motor yachts dominated the luxury yacht market, securing a commanding 66.68% share, reflecting established consumer preferences for spacious layouts, extended range capabilities, and proven reliability across diverse cruising conditions. Hybrid/electric yachts emerge as the fastest-growing segment at 10.09% CAGR through 2031, driven by environmental regulations and technological advancements. Sailing yachts maintain steady demand among purist owners seeking traditional experiences, while catamaran yachts gain traction for charter operations due to stability and space efficiency. Explorer yachts represent a specialized but rapidly expanding niche, with 58 new vessels launching in 2025 targeting adventure-oriented owners.

The electrification trend accelerates as manufacturers integrate hybrid systems offering reduced noise, improved fuel efficiency, and modular powertrains allowing easy upgrades. Ferretti Group unveiled the Riva El-Iseo, their first full-electric model in the E-Luxury segment, combining traditional design with modern electric technology. Solar energy integration and AI-powered energy management systems optimize power consumption, enhancing the luxury experience while addressing environmental concerns. Motor yacht manufacturers increasingly offer hybrid variants across their model ranges to capture environmentally conscious buyers without sacrificing performance expectations.

By Size: Superyachts Drive Premium Growth

The 20 to 40-meter segment emerged as the frontrunner, holding 43.62% of the market share in 2025, striking a balance between space, operational complexity, and marina accessibility, making it the prime choice for private ownership. Vessels above 80 meters achieve the highest growth rate at 11.74% CAGR through 2031, reflecting ultra-wealthy buyers' preference for floating estates with comprehensive amenities. The up to 20-meter segment serves entry-level luxury buyers and charter operations, while 40 to 60-meter yachts cater to established owners seeking enhanced capabilities. The 60-to-80-meter range targets experienced owners transitioning to larger vessels with expanded crew and guest accommodations.

Superyacht construction increasingly incorporates advanced materials and technologies, with carbon composites moving beyond racing applications into luxury vessels for weight reduction and performance optimization. The Scheherazade exemplifies this trend, incorporating carbon composites in masts, rigging, and deck structures. Larger vessels benefit from economies of scale in hybrid propulsion integration, with Rolls-Royce's systems ranging from 1,000 to 4,000 kilowatts suitable for various yacht sizes. The size escalation reflects owners' desire for self-sufficiency during extended cruising, driving demand for vessels with enhanced range, storage, and onboard facilities.

By Hull Material: Carbon Fiber Gains Momentum

In terms of hull materials, fiberglass and composites led the way, accounting for 55.68% of the market share in 2025, offering proven durability, cost-effectiveness, and established manufacturing processes across global shipyards. Carbon fiber is the fastest-growing segment at 12.98% CAGR through 2031, driven by weight reduction benefits and performance optimization demands. Aluminum maintains relevance for larger vessels requiring structural strength, while steel serves specialized applications, including ice-classed expedition yachts. Other materials encompass innovative solutions, including biocomposites and recycled materials, addressing sustainability concerns.

European shipyards report that nearly 95% currently use or plan to use composite materials, with manufacturing processes evolving toward vacuum infusion and automated techniques. Chomarat's C-PLY noncrimp fabrics demonstrate carbon fiber applications in Arcona Yachts' models 435 and 465, enhancing structural integrity while reducing weight. Technology enables high-speed racing and low-speed cruising capabilities without customization, with the Arcona 435 winning the European Yacht of the Year award in 2019. Carbon fiber construction allows achieving high strength with fewer layers, making it increasingly cost-effective for luxury yacht manufacturing while supporting environmental goals through weight reduction and fuel efficiency improvements.

By Propulsion System: Diesel Dominance Faces Electric Challenge

Diesel propulsion maintains 82.62% of the Luxury Yacht Market's market share in 2025, reflecting established infrastructure, proven reliability, and extensive service networks supporting global cruising operations. Diesel-Electric/Hybrid systems accelerate at 9.12% CAGR through 2031, driven by environmental regulations and technological maturation. Full electric propulsion targets specific applications, including harbor operations and short-range cruising, while hydrogen fuel cells represent emerging technology for zero-emission operations. Diesel-electric hybrid configurations offer transitional solutions combining range capabilities with environmental benefits.

The IMO's new greenhouse gas requirements, taking effect from 2028, accelerate alternative propulsion adoption. EU regulations, including the Emissions Trading System expansion and FuelEU Maritime requirements, impact vessels over 5,000 gross tons, necessitating emissions reporting and compliance with greenhouse gas intensity limits. Hybrid systems provide operational flexibility, enabling silent running for wildlife observation, reduced vibration for guest comfort, and improved fuel efficiency during displacement cruising. Technology integration supports luxury positioning while addressing regulatory compliance, creating competitive advantages for early adopters in environmentally sensitive markets.

By End-User: Fractional Ownership Disrupts Traditional Models

Private individuals were the primary stakeholders, representing 60.74% of the luxury yacht market in 2025, maintaining dominance through direct ownership of luxury yachts for personal use and family enjoyment. Fractional-ownership clubs emerge as the fastest-growing segment at 11.08% CAGR through 2031, addressing high ownership costs and utilization challenges. Charter companies serve growing yacht tourism demand, while corporate and events usage provide steady revenue streams. Government and naval VIP applications represent specialized requirements for official transportation and representation.

The fractional ownership model addresses cost barriers preventing yacht ownership, with platforms enabling shared access to luxury vessels without full ownership responsibilities. This trend aligns with UHNW investors' shift toward sustainable investments and experiential luxury over traditional asset accumulation. Charter companies increasingly invest in larger, more luxurious vessels to capture premium spending, with yacht tourists paying approximately USD 287 per day compared to USD 150 for conventional tourists. The model evolution reflects changing generational preferences, with younger wealthy individuals favoring access over ownership and prioritizing experiences over possessions.

Geography Analysis

Europe commanded 42.62% of the luxury yacht market in 2025 on the strength of enduring shipbuilding clusters in Italy, the Netherlands, and Germany. Italian yards delivered half of all 24 m-plus vessels globally, with Azimut-Benetti aiming for EUR 1.5 billion turnover by 2025 despite soft luxury-goods sentiment. EU climate legislation spurs R&D in hybrid propulsion, allowing builders to market compliance as a competitive edge to carbon-conscious buyers. However, 20% U.S. import tariffs on EU yachts may divert some American orders to domestic brands, potentially trimming Europe’s share over the forecast horizon.

Asia-Pacific is the fastest-growing region at an 11.24% CAGR. The 2025 Hong Kong Superyacht Summit drew 250 executives who outlined marina expansions in Hainan, Cebu, and Langkawi. Chinese registrations increase as the easing of coastal cruising permits streamlines itineraries. India’s coastline modernization plan earmarks eleven new marinas, positioning Goa as a charter springboard for the Maldives. Nevertheless, bureaucratic clearance protocols and limited deep-water berths still inhibit full exploitation of regional demand in the luxury yacht market.

North America remains a mature yet expanding arena. The U.S. marina sector booked USD 6.7 billion in 2023 revenue with occupancy above 90% in many hubs. Blackstone’s record purchase of Safe Harbor Marinas grants the fund 138 properties and underscores the strategic value of berth infrastructure. Universal 10% import tariffs, escalating to 20-54% by source country, buttress domestic builders such as Westport and Christensen. Skill shortages, however, increase crew wages by double-digit percentages, nudging some owners toward less labor-intensive displacement yachts, a trend reverberating across the luxury yacht market.

Mordor Intelligence provides coverage of the luxury yacht market across other key regional markets, including Europe and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The luxury yacht market exhibits moderate concentration with established European builders maintaining leadership through brand heritage, technological innovation, and manufacturing scale. Industry consolidation accelerates through strategic acquisitions, exemplified by Sanlorenzo's EUR 48.5 million purchase of 60% of Nautor Swan, positioning the combined entity as a leader in sustainable yachting technologies. Blackstone Infrastructure's USD 5.65 billion acquisition of Safe Harbor Marinas demonstrates private equity interest in marine infrastructure, potentially reshaping competitive dynamics through operational improvements and network expansion.

Competition intensifies technological differentiation, with manufacturers investing heavily in hybrid propulsion, advanced materials, and digital integration to capture environmentally conscious buyers. White-space opportunities emerge in fractional ownership platforms, expedition yacht segments, and emerging market penetration where traditional builders lack presence. The Red Ensign Group's revised Yacht Code, effective July 2024, establishes enhanced safety and design standards while supporting innovation, creating competitive advantages for compliant manufacturers.

Technology adoption patterns favor builders integrating AI-powered energy management, modular propulsion systems, and sustainable materials to differentiate offerings. Smaller contenders leverage specialized expertise in expedition yachts and electric propulsion to challenge incumbents, while established players expand through acquisitions to capture emerging segments and geographic markets.

Luxury Yacht Industry Leaders

-

Fincantieri Yachts

-

Feadship

-

Lürssen Werft

-

Azimut-Benetti Group

-

Sanlorenzo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The IMO approved new greenhouse gas requirements during MEPC 83, taking effect from 2028, establishing stricter emissions standards for maritime vessels including luxury yachts. These regulations will drive technological innovation in hybrid and electric propulsion systems across the industry.

- February 2025: Blackstone Infrastructure completed its USD 5.65 billion acquisition of Safe Harbor Marinas, the largest marina and superyacht services business in the U.S., operating 138 facilities across North America and Puerto Rico. The transaction reflects strong investor confidence in marina infrastructure and positions Blackstone to enhance operational efficiency while expanding the network.

- February 2025: OneWater Marine completed its USD 75 million acquisition of American Yacht Group, enhancing its presence in the Southeastern U.S. and securing exclusive dealership rights for HCB Yachts in Alabama, Florida, New York, and North Carolina. The deal strengthens OneWater's position in the luxury marine market.

Global Luxury Yacht Market Report Scope

A luxury yacht, often known as a superyacht or megayacht, is a big and opulent pleasure vessel used for recreation. These yachts are either rented or purchased by the ultra-rich or by a firm for its employees.

The luxury yacht market is segmented by type (sailing luxury yachts, motorized luxury yachts, and other types), by size (up to 20 meters, 20 to 50 meters, and above 50 meters), by application (commercial and private use), and by geography (North America, Europe, Asia-Pacific, and the Rest of the World).

The report offers market size and forecasts for the luxury yacht market in value (USD) for the above segments.

| Motor Yacht |

| Sailing Yacht |

| Hybrid / Electric Yacht |

| Catamaran Yacht |

| Explorer / Others |

| Up to 20 m |

| 20 to 40 m |

| 40 to 60 m |

| 60 to 80 m |

| Above 80 m |

| Fiberglass / Composite |

| Aluminum |

| Steel |

| Carbon Fiber |

| Others |

| Diesel |

| Diesel-Electric / Hybrid |

| Full Electric |

| Hydrogen Fuel Cell (Emerging) |

| Private Individuals |

| Charter Companies |

| Corporate and Events |

| Fractional-Ownership Clubs |

| Government and Naval (VIP) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Italy |

| Germany | |

| United Kingdom | |

| France | |

| Netherlands | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Australia | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Motor Yacht | |

| Sailing Yacht | ||

| Hybrid / Electric Yacht | ||

| Catamaran Yacht | ||

| Explorer / Others | ||

| By Size | Up to 20 m | |

| 20 to 40 m | ||

| 40 to 60 m | ||

| 60 to 80 m | ||

| Above 80 m | ||

| By Hull Material | Fiberglass / Composite | |

| Aluminum | ||

| Steel | ||

| Carbon Fiber | ||

| Others | ||

| By Propulsion System | Diesel | |

| Diesel-Electric / Hybrid | ||

| Full Electric | ||

| Hydrogen Fuel Cell (Emerging) | ||

| By End-User | Private Individuals | |

| Charter Companies | ||

| Corporate and Events | ||

| Fractional-Ownership Clubs | ||

| Government and Naval (VIP) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Italy | |

| Germany | ||

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Australia | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the luxury yacht market?

The luxury yacht market stands at USD 10.76 billion in 2026 and is forecast to reach USD 14.61 billion by 2031.

Which yacht type is most popular?

Motor yachts dominate with 66.68% market share in 2025, but hybrid-electric motor yachts are the fastest-growing sub-segment.

Which region will grow the fastest through 2031?

Asia-Pacific is expected to expand at an 11.24% CAGR, driven by rising UHNWIs and new marina infrastructure.

How are environmental regulations influencing yacht design?

IMO and EU greenhouse-gas rules, effective from 2028, will propel the adoption of hybrid and electric propulsion and stimulate R&D in lightweight materials.

Which region has the biggest share in Luxury Yacht Market?

Europe hold the largest market share of 42.62% in the Luxury Yacht market in 2025

Page last updated on: