Market Overview

| Study Period | 2021 - 2031 |

|---|---|

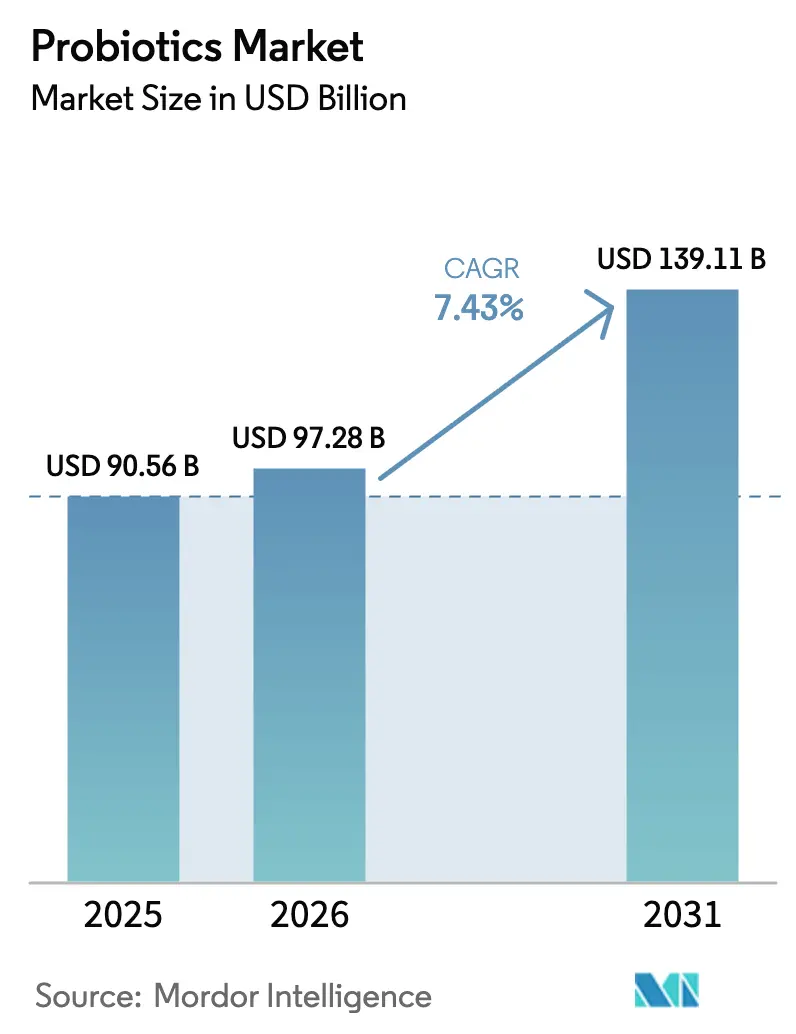

| Market Size (2026) | USD 97.28 Billion |

| Market Size (2031) | USD 139.11 Billion |

| Growth Rate (2026 - 2031) | 7.43% CAGR |

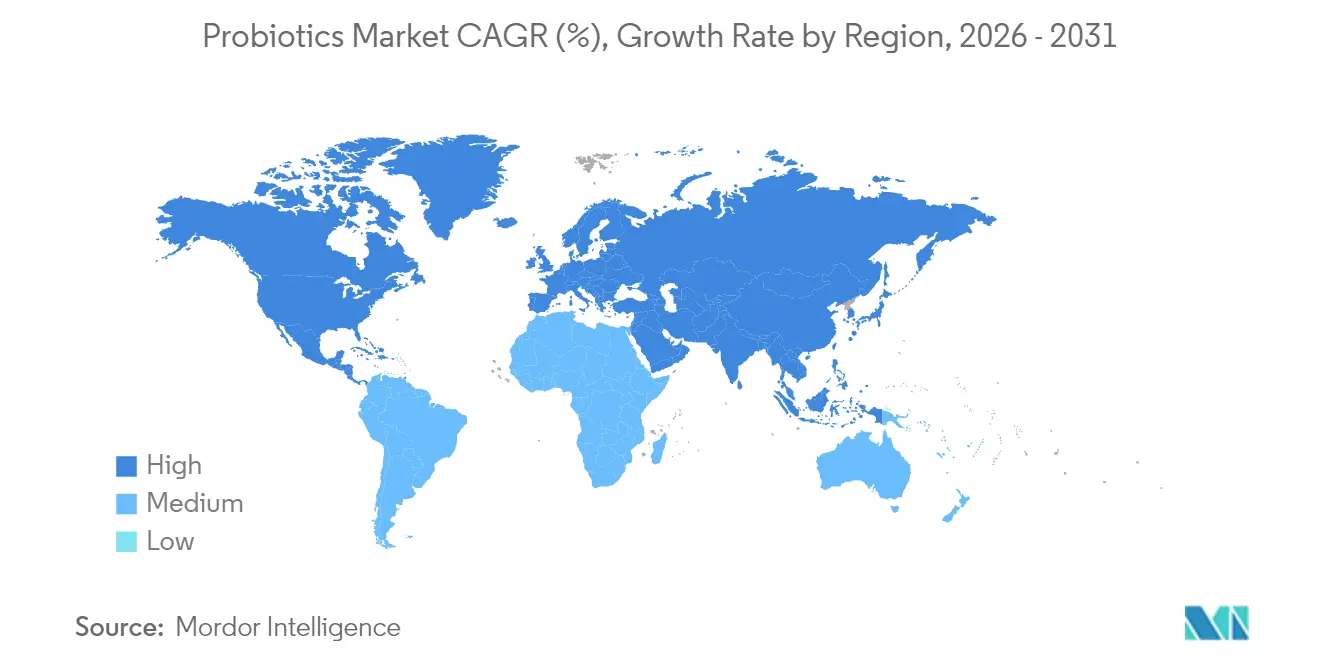

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Probiotics Market Analysis by Mordor Intelligence

The probiotics market size was valued at USD 90.56 billion in 2025 and estimated to grow from USD 97.28 billion in 2026 to reach USD 139.11 billion by 2031, at a CAGR of 7.43% during the forecast period (2026-2031). Heightened consumer focus on preventive health, the FDA’s 2024 qualified health claim for yogurt, and rapid advances in precision microbiome research are propelling adoption across food, supplement, and clinical channels. Manufacturers in the probiotics market are shifting investment toward strain-specific R&D, AI-enabled personalization platforms, and e-commerce fulfillment efficiencies to capture premium margins. Multinational consolidation, led by the Chr Hansen–Novozymes merger, is reshaping competitive structures and accelerating technology diffusion. Regionally, the probiotics market in North America benefits from progressive regulatory signals, while Asia-Pacific’s 9.23% CAGR reflects rising middle-class spending and regulatory harmonization. Strategic opportunities center on next-generation therapeutic formats, organic and non-GMO certification, and livestock antibiotic-reduction policies that widen the probiotics market addressable base.

Key Report Takeaways

- By product type, probiotic foods held 53.88% of probiotics market share in 2025, whereas dietary supplements are advancing at an 7.99% CAGR through 2031.

- By function, digestive and gut health captured 37.10% revenue share in 2025; immunity enhancement is projected to post an 8.39% CAGR to 2031.

- By distribution channel, pharmacies and drug stores commanded 35.02% of the probiotics market size in 2025, while online stores are expanding at a 8.93% CAGR to 2031.

- By geography, North America led with 34.55% share in 2025, yet Asia-Pacific is forecast to accelerate at a 9.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Probiotics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional foods & beverages | +1.2% | Global, higher in North America & Europe | Medium term (2-4 years) |

| Growing incidence of digestive disorders | +1.8% | Global, accelerated in developed markets | Long term (≥ 4 years) |

| Demand for natural, organic, and non-GMO probiotics | +0.9% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Expansion of retail & e-commerce distribution | +1.4% | APAC core, spill-over to emerging markets | Short term (≤ 2 years) |

| Growing research and clinical validation | +1.0% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Microbiome-based personalized nutrition programs | +0.7% | North America & Europe early adoption, APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for functional foods and beverages

The rise in "food-as-medicine" preferences in the probiotics market has prompted fermentation companies to integrate spore-forming probiotic strains into non-dairy products, resulting in shelf-stable offerings across cereals, snacks, and sports beverages. Studies mapping gut microbiome patterns show that specialized probiotic formulations can achieve premium pricing. This development has fostered collaborations between consumer packaged goods (CPG) companies and research institutions for product development. According to market surveys, 85% of U.S. consumers favor probiotic foods over supplements, prompting retailers to expand shelf space for functional products. The increasing prevalence of lactose intolerance and vegan preferences has driven manufacturers to explore plant-based carriers. These innovations in functional foods continue to support the growth of the probiotics market.

Growing Incidence of Digestive Disorders Drives Market Growth

The increasing occurrence of gastrointestinal conditions, inflammatory bowel diseases, and antibiotic-associated complications has expanded the therapeutic applications for probiotics across different age groups. Clinical trials have shown improved efficacy, with multicenter studies demonstrating that high-dose probiotic combinations prevent antibiotic-associated diarrhea in adults, addressing a significant healthcare concern affecting millions of patients each year. In pediatric applications, the combination of omeprazole and probiotics has reduced inflammatory markers and improved symptom scores in children with functional dyspepsia compared to using pharmaceutical treatments alone. The adoption of preventive probiotic treatments has increased due to healthcare cost considerations, as clinical evidence shows their effectiveness in lowering hospitalization rates and reducing dependence on pharmaceuticals for chronic gastrointestinal conditions.

Demand for natural, organic, and non-GMO probiotics

In the probiotics market, the increasing consumer focus on ingredient transparency and sustainable production methods drives demand for certified organic and non-GMO probiotic products. Health-conscious consumers demonstrate willingness to pay higher prices for products with verified sourcing and sustainability credentials. The implementation of the USDA's[1]United States Department of Agriculture, "Strengthening Organic Enforcement", www.fas.usda.gov Strengthening Organic Enforcement rule in March 2024 requires mandatory NOP Import Certificates and enhanced fraud prevention protocols. These regulations create entry barriers for non-compliant suppliers while benefiting certified organic probiotic manufacturers. To maintain organic compliance, manufacturers must source probiotics from non-genetically modified organisms, which affects strain selection and production processes. In European markets, consumers show a strong preference for natural probiotic products, despite strict regulations on health claims. Companies develop alternative marketing approaches to communicate gut health benefits while adhering to EFSA guidelines. Manufacturers who invest in organic certification and supply chain transparency gain competitive advantages, especially as younger consumers consider both environmental impact and health benefits in their purchasing decisions.

Growing Research and Clinical Validation

In the probiotics market, the clinical evidence base for probiotics continues to expand through randomized controlled trials, regulatory submissions, and peer-reviewed publications that demonstrate strain-specific efficacy across various health conditions. The FDA's approval of microbiota-based therapies, including REBYOTA™ and VOWST™ for recurrent Clostridioides difficile infections, establishes a precedent for probiotic drug development and potential prescription applications. Research institutions focus on precision microbiome interventions, with studies showing that AI-driven personalized nutrition programs improve gut microbiome diversity and reduce diet-related health risks over six-week intervention periods. Clinical validation now encompasses sports performance, where studies indicate probiotics enhance endurance capacity, reduce inflammation, and improve recovery metrics in both amateur and professional athletes. The United States Pharmacopeia has developed 14 probiotic ingredient monographs that provide standardized quality parameters and safety guidelines, supporting regulatory acceptance and commercial scalability in pharmaceutical and nutraceutical applications, according to the Food Compliance International[2]Food Compliance International, "USA - A Review of Probiotic Ingredient Safety Supporting Monograph Development Conducted by the United States Pharmacopeia (USP)", www.foodcomplianceinternational.com.

Restraint Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of research and development | -0.8% | Global, particularly impacting smaller companies | Long term (≥ 4 years) |

| Competition from Alternative Health Products | -0.6% | North America & Europe core, expanding globally | Medium term (2-4 years) |

| Lack of consumer awareness in some regions | -0.9% | Emerging markets in APAC, MEA, and South America | Medium term (2-4 years) |

| Regulatory challenges and product claims restrictions | -1.1% | Europe most restrictive, variable across regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of research and development

In the probiotics market, the development of probiotic products requires substantial investments in clinical trials, regulatory compliance, and strain characterization, creating significant barriers for smaller companies. Established companies with robust R&D capabilities and financial resources maintain a competitive advantage. The capital requirements for comprehensive safety evaluations, including toxicological testing and self-GRAS pathway approvals, typically exceed USD 10 million for novel strain development and validation. Microbiome research demands sophisticated analytical capabilities, specialized equipment, and multidisciplinary expertise in microbiology, immunology, and clinical research. Companies without an established research infrastructure face significant operational challenges. The varying regulatory requirements across jurisdictions necessitate multiple studies and separate documentation systems for different markets, increasing development costs and extending time-to-market. Additionally, the complex patent landscape in probiotic applications requires extensive intellectual property research and potential licensing agreements, resulting in additional legal costs and strategic limitations for product development.

Regulatory challenges and product claims restrictions

The regulatory framework for probiotics differs substantially across global probiotics markets, with Europe implementing the most rigorous controls. EFSA's[3]European Food Safety Authority, "Update of the list of qualified presumption of safety (QPS) recommended microbiological agents intentionally added to food or feed as notified to EFSA 20", www.efsa.onlinelibrary.wiley.com revisions to the Qualified Presumption of Safety list demonstrate ongoing regulatory vigilance, including recent exclusions of strains such as Akkermansia muciniphila due to safety considerations. This restricts the innovation of new probiotic products. Divergent regulations among EU member states have created market fragmentation, with nations like the Czech Republic, France, and Italy implementing distinct rules for probiotic terminology and health claims. Although a formal complaint to the European Ombudsman about probiotic classification suggests potential regulatory shifts, the prevailing uncertainty impacts industry investment choices and strategic planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Foods Dominate While Supplements Accelerate

Probiotic foods dominated revenue with a 53.88% of the probiotics market share in 2025, validating consumer desire for health benefits embedded in everyday diets, while supplements are scaling fastest at an 7.99% CAGR. The category’s yogurt cornerstone gained further traction after the FDA diabetes-risk claim, spurring line extensions into low-sugar and plant-based variants. Drinks are diversifying: kefir, kombucha, and oat-based smoothies now incorporate Bacillus spores stable at ambient temperatures, opening non-refrigerated distribution. Supplements ride precision-dose appeal; time-release capsules and spore-based blends attract athletes and seniors seeking targeted outcomes.

The animal nutrition niche, buoyed by EU antibiotic bans, adds incremental volume as poultry and aquaculture producers adopt multi-strain feed additives to improve feed conversion and disease resistance. Collectively, expanding formats underpin resilience of the probiotics market. Functional snacking also rises: chocolate-coated probiotics, shelf-stable baked goods, and chewy gummies serve impulse occasions while delivering viable counts through protective microencapsulation. Private-label innovation in supermarkets puts price pressure on legacy brands yet expands category footprint. In parallel, pharmaceutical-grade synbiotic medical foods enter hospital channels for oncology and critical-care patients requiring microbiome support, further broadening the probiotics market size.

By Function: Digestive health leads, while immunity enhancement accelerates the market

The digestive and gut health applications segment captured 37.10% revenue of the probiotics market in 2025, anchored by extensive clinical validation for diarrhea, IBS, and IBD management. Brand communication focuses on bloat reduction and regularity, resonating across demographics. Immunity products, however, exhibit the highest momentum at an 8.39% CAGR as post-pandemic routines normalize but immune vigilance persists. Controlled studies show certain Lactobacillus strains cut upper-respiratory infection incidence in adults by 25%, reinforcing consumer trust.

Emerging functions include mood modulation; patents on psychobiotics have grown sharply, with early trials indicating anxiety-score improvements. Sports performance benefits, from enhanced VO2max to faster muscle recovery, attract fitness communities, while metabolic support formulations target pre-diabetics using strains linked to glucose homeostasis. Women’s health lines addressing vaginal microbiota imbalance are expanding shelf facings in pharmacies. Such pluralization sustains overall growth of the probiotics market.

By Distribution Channels: Pharmacies Lead Distribution While E-commerce Shows Strongest Growth

Pharmacies and drug stores dominate the distribution landscape with a 35.02% of the probiotics market share in 2025. This leadership stems from healthcare professionals' recommendations and consumer trust in pharmaceutical retail settings. Meanwhile, online stores demonstrate the highest growth trajectory at 8.93% CAGR through 2031. The traditional pharmacy channel maintains its strength through healthcare provider referrals and consumer perception of probiotics as therapeutic products requiring professional guidance, especially for specialized and prescription-adjacent formulations.

Supermarkets and hypermarkets offer extensive consumer access through dedicated refrigerated sections and promotional activities, though they face increasing competition from private label products in terms of pricing and shelf space. Convenience and grocery stores have expanded their probiotic offerings through improved cold-chain management and strategic placement in health sections, benefiting from impulse purchases and regular shopping habits. The online distribution channel has altered market dynamics by establishing direct consumer relationships, implementing subscription models, and offering personalized product recommendations based on health profiles and purchase patterns. E-commerce enables smaller brands to reach specific consumer segments without extensive physical distribution networks, supporting innovation in areas like sports nutrition, pediatric formulations, and condition-specific products. Digital platforms also enhance consumer education through product information, clinical studies, and user reviews, addressing information gaps present in traditional retail environments.

Geography Analysis

North America accounts for 34.55% of the global probiotics market in 2025, underpinned by sophisticated regulatory frameworks, informed consumers, and sustained healthcare provider endorsements. The region sustains growth through high-end product positioning and diversified functional applications. The FDA's recent developments, particularly the March 2024 approval linking yogurt consumption to reduced diabetes risk, strengthen North American manufacturers' competitive position and encourage research investment. In the probiotics market, the United States maintains market dominance through substantial health-related consumer spending, extensive retail distribution, and established research capabilities. Canada contributes through progressive regulations and growing functional food acceptance, while Mexico emerges as a promising probiotics market driven by increased health consciousness and middle-class expansion.

Europe retains substantial market presence despite regulatory restrictions, employing strategic marketing initiatives and product modifications across Germany, the United Kingdom, France, and Italy. EFSA's rigorous health claim requirements demand extensive clinical research investment while restricting marketing flexibility compared to other regions. Nordic countries exhibit strong functional food and probiotic acceptance, reinforced by health-oriented cultural values. Mediterranean markets demonstrate growing interest in digestive health solutions. The ongoing European Ombudsman examination of probiotic classification indicates potential regulatory adjustments that could remove existing market barriers.

Asia-Pacific probiotics market exhibits the strongest growth trajectory at 9.02% CAGR through 2031, fueled by expanding middle-class populations, heightened health awareness, and regulatory standardization across China, India, Japan, and Southeast Asian markets. China offers substantial growth potential, illustrated by Cell Biotech's 12-year leadership in Korean probiotic exports and market penetration into Thailand and Philippines through technological excellence and premium positioning. Japan's comprehensive functional food regulations, including the Foods with Function Claims framework, facilitate evidence-based probiotic development. India's market expands through its substantial population base and rising disposable income, despite infrastructure challenges. South America and Middle East & Africa demonstrate growth potential but require investments in consumer education, distribution networks, and regulatory alignment.

Competitive Landscape

The probiotics market demonstrates a moderate level of concentration. This score reflects a competitive environment where well-established multinational corporations compete alongside agile, specialized players. These companies differentiate themselves through unique positioning strategies and continuous technological advancements. Prominent players in the probiotics industry include Nestlé S.A., Yakult Honsha Co., Ltd, Chobani LLC, Danone S.A., and PepsiCo Inc. To meet the growing demand for probiotic products, these companies are employing a variety of strategies, including launching new products, forming strategic partnerships, expanding their operations, and engaging in mergers and acquisitions.

A notable trend in the market is vertical integration. For instance, Danone's acquisition of The Akkermansia Company has enhanced its capabilities in next-generation probiotics, while ADM's GBP 185 million acquisition of Probiotics International Limited highlights ongoing consolidation within the specialized supplement segment. Significant opportunities are emerging in areas such as precision medicine applications, sports nutrition, and personalized microbiome interventions. In these segments, traditional food companies often face challenges due to a lack of specialized expertise and regulatory experience. The adoption of advanced technologies is accelerating competitive differentiation in the market.

Innovations such as AI-driven personalization platforms, advanced strain characterization techniques, and novel delivery systems are improving product efficacy and enhancing consumer convenience. Additionally, emerging disruptors are reshaping the probiotics industry landscape by leveraging direct-to-consumer models, subscription-based services, and the integration of microbiome testing. These approaches enable them to create unique value propositions that challenge conventional retail-focused strategies. Furthermore, these disruptors are capitalizing on the growing demand for personalized solutions, allowing them to implement premium pricing strategies effectively.

Probiotics Industry Leaders

-

Nestle S.A.

-

Yakult Honsha Co. Ltd

-

Chobani LLC

-

Danone SA

-

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bioma Probiotics launched its flagship product, Bioma Probiotics Supplements. The supplement offers digestive health, immune support, and mental clarity through microbiome balance. The product is a blend of prebiotics, probiotics, and postbiotics.

- May 2025: Florastor expanded its product portfolio with two new products: Her Florastor Digest + De-Stress Probiotics and Digest + Metabolic Support Gummy. The Her Florastor Digest + De-Stress probiotic supplement integrated digestive and vaginal support with L-theanine to address stress management without causing drowsiness.

- March 2025: Nature Made, the largest vitamin and supplement manufacturer in the United States, launched a new product line of probiotic, prebiotic, and fiber supplements for digestive health and wellness requirements. The product portfolio included Nature Made Probiotic + Prebiotic Fiber Gummies and Nature Made Probiotics 1 Billion CFU Capsules.

- September 2024: ZBiotics, a biotechnology company that developed genetically engineered probiotics, announced the launch of its Sugar-to-Fiber Probiotic Drink Mix. This was the company's second product, following its Pre-Alcohol Probiotic Drink, which was engineered to break down specific alcohol byproducts.

Global Probiotics Market Report Scope

Probiotics are a combination of beneficial bacteria and yeasts that help humans and animals maintain intestinal microbial balance. The probiotics market is segmented by type into probiotic foods, probiotic drinks, dietary supplements, and animal feeds. Probiotic food is further sub-segmented into yogurt, bakery/breakfast cereals, baby food and infant formula, and other probiotic foods. Probiotic drinks have been further classified into fruit-based probiotic drinks and dairy-based probiotic drinks. By distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies and health stores, convenience stores, online retail stores, and other distribution channels. The study also involves an analysis of the main regions, including North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Probiotic Foods | Yogurt |

| Bakery & Breakfast Cereals | |

| Infant Formula & Baby Foods | |

| Snacks & Confectionery | |

| Probiotic Drinks | Dairy-based |

| Non-dairy | |

| Dietary Supplements | |

| Animal Feed and Nutrition |

By Function

| Digestive & Gut Health |

| Immunity Enhancement |

| Mental Health & Mood (Gut-brain axis) |

| Sports & Metabolic Performance |

| Others |

By Distribution Channels

| Supermarket/Hypermarkets |

| Pharmacies and Drug Stores |

| Convinience/Grocery Stores |

| Online Stores |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Probiotic Foods | Yogurt |

| Bakery & Breakfast Cereals | ||

| Infant Formula & Baby Foods | ||

| Snacks & Confectionery | ||

| Probiotic Drinks | Dairy-based | |

| Non-dairy | ||

| Dietary Supplements | ||

| Animal Feed and Nutrition | ||

| By Function | Digestive & Gut Health | |

| Immunity Enhancement | ||

| Mental Health & Mood (Gut-brain axis) | ||

| Sports & Metabolic Performance | ||

| Others | ||

| By Distribution Channels | Supermarket/Hypermarkets | |

| Pharmacies and Drug Stores | ||

| Convinience/Grocery Stores | ||

| Online Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the probiotics market in 2026?

The probiotics market size is USD 97.28 billion in 2026 and is on track to reach USD 139.11 billion by 2031.

Which product category leads global sales?

Probiotic foods account for 53.88% of global revenue in 2025.

What segment is growing fastest?

Dietary supplements show the highest product growth at an 7.99% CAGR through 2031, driven by precision dosing and personalization.

Which region is expanding most quickly?

Asia-Pacific leads growth with a projected 9.02% CAGR, propelled by rising middle-class health spending and regulatory harmonization.

Page last updated on: