Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

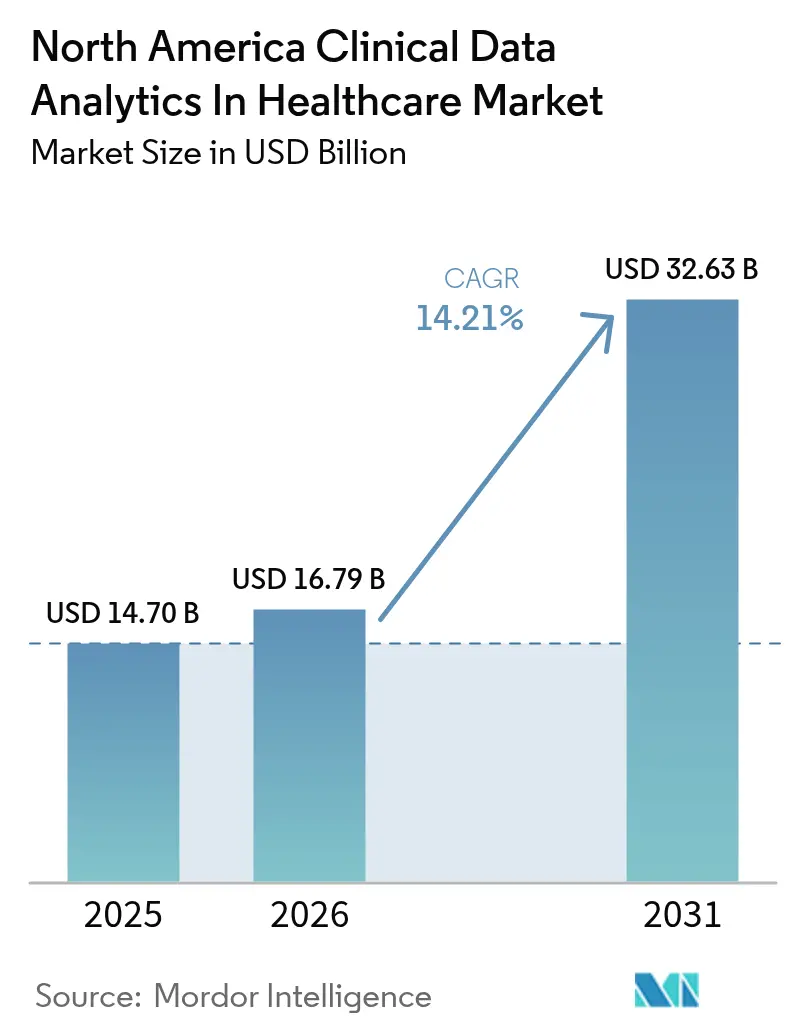

| Base Year Market Size (2025) | USD 14.70 Billion |

| Market Size (2026) | USD 16.79 Billion |

| Market Size (2031) | USD 32.63 Billion |

| Growth Rate (2026 - 2031) | 14.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Clinical Data Analytics In Healthcare Market Analysis by Mordor Intelligence

The North America clinical data analytics in healthcare market size is expected to grow from USD 14.70 billion in 2025 to USD 16.79 billion in 2026 and is forecast to reach USD 32.63 billion by 2031 at 14.21% CAGR over 2026-2031. Heightened demand for real-time insights, accelerated cloud adoption, and value-based reimbursement mandates are steering investment decisions, while artificial intelligence (AI) and advanced interoperability standards redefine competitive positioning. Growing reliance on population-level risk stratification creates fresh revenue streams for health systems that can translate analytics findings into measurable clinical outcomes. At the same time, cyber-insurance requirements elevate data governance to a strategic imperative, prompting many institutions to prioritize analytics maturity ahead of other IT initiatives. Established EHR vendors strengthen their foothold by embedding prescriptive models directly into existing workflows, but smaller, cloud-native firms are winning niche opportunities with agile, AI-first offerings.

Key Report Takeaways

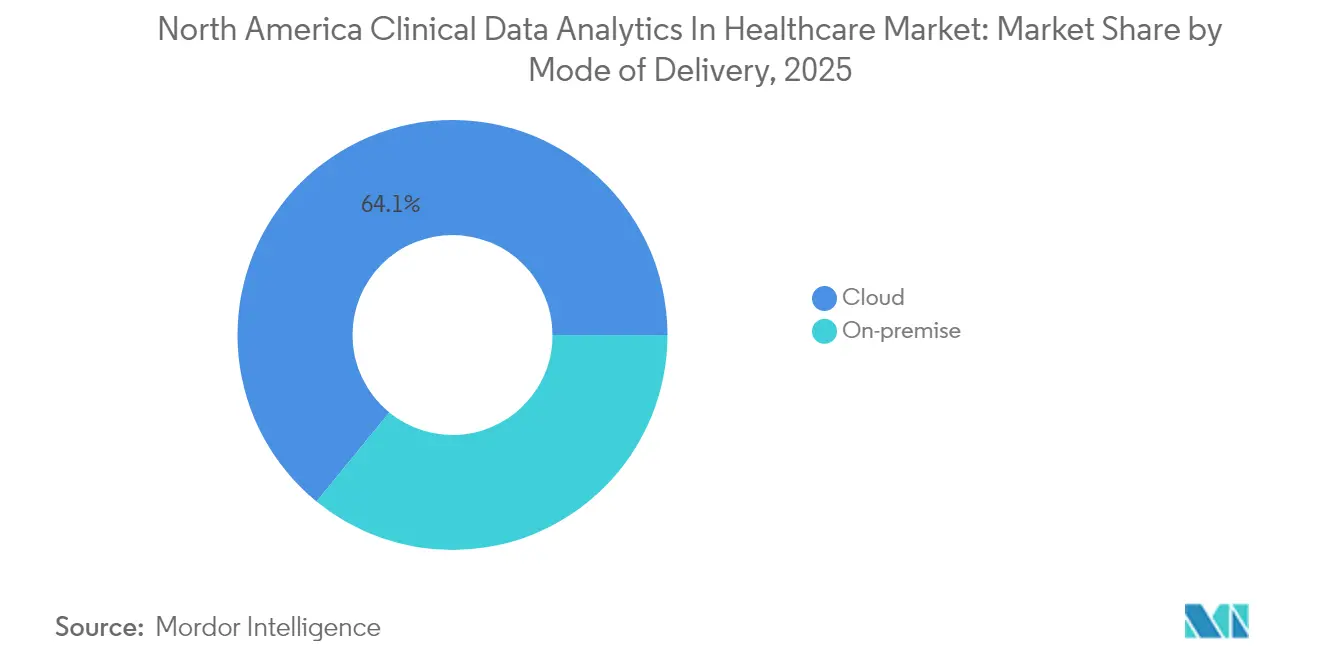

- By mode of delivery, cloud deployment held 64.10% of the North America clinical data analytics in the healthcare market share in 2025.

- By type, prescriptive analytics is forecast to advance at a 15.20% CAGR through 2031.

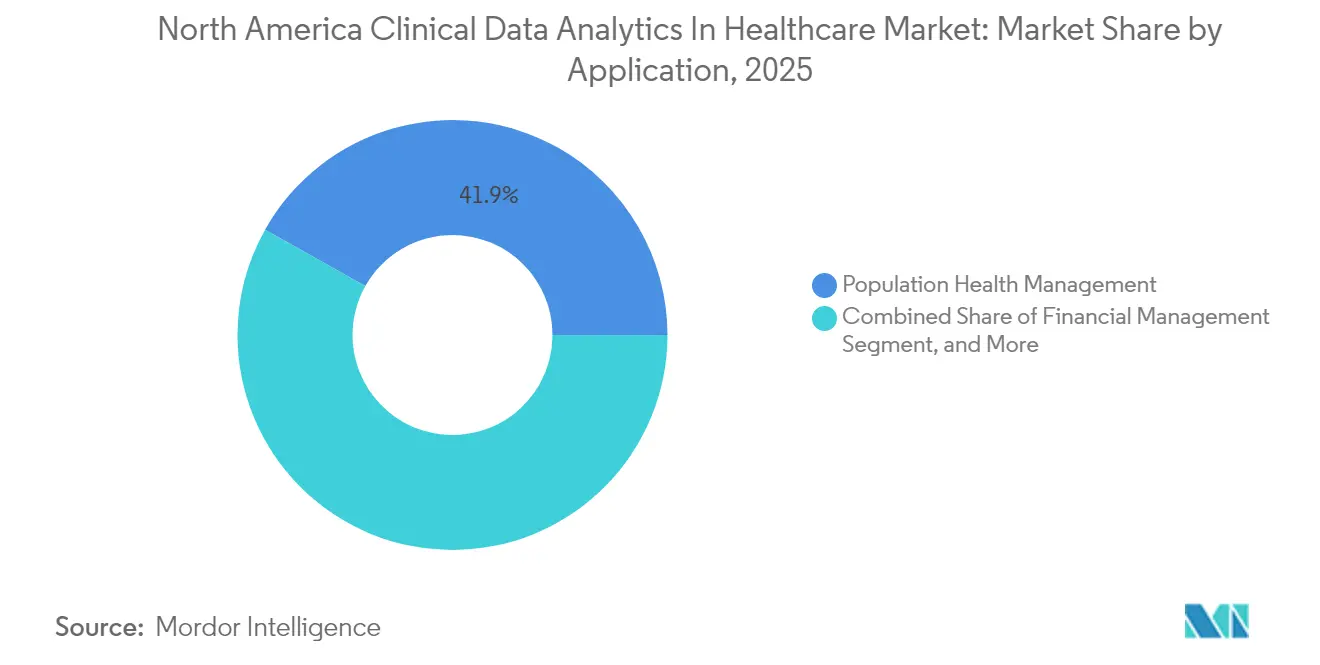

- By application, population health management commanded 41.85% of the North America clinical data analytics in the healthcare market size in 2025.

- By end-user, payers exhibit the highest projected growth, moving at a 15.85% CAGR to 2031.

- By country, the United States retained 78.12% of 2025 regional revenue, while Mexico is expected to grow fastest at a 15.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Clinical Data Analytics In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first EHR modernization initiatives | +3.2% | United States and Canada, with Mexico following | Medium term (2-4 years) |

| AI-assisted clinical decision support demand | +2.8% | North America core, strongest in urban markets | Short term (≤ 2 years) |

| Value-based-care reimbursement mandates | +2.1% | United States primarily, Canada selective adoption | Long term (≥ 4 years) |

| Rapid growth of real-world-evidence trials | +1.9% | Global, with North America hubs | Medium term (2-4 years) |

| Rise of retail-health entrants leveraging analytics | +1.7% | United States concentrated, urban | Short term (≤ 2 years) |

| Escalating cyber-insurance premiums tied to analytics maturity | +1.4% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-first EHR Modernization Initiatives

Large-scale migrations to cloud-based EHRs shorten analytics deployment cycles, shifting capital expenses to operational budgets that better align with fluctuating healthcare revenues. The Veterans Health Administration’s USD 16 billion Oracle Cerner rollout moved data processing from 18–24 months to 6–9 months, producing 40% faster queries and 60% lower data-prep overhead. [1]Department of Veterans Affairs, “EHR Modernization Program Update,” va.gov Centralized data lakes emerging from such projects enable regional health systems to benchmark outcomes across multiple facilities, accelerating evidence-based practice adoption. Vendors with HIPAA-compliant cloud templates capture a disproportionate share as buyers favor turnkey security controls over custom builds. This dynamic magnifies the addressable market for prescriptive analytics and reinforces the appeal of hybrid architectures that retain sensitive data on-premise while performing compute-intensive tasks in the public cloud.

AI-assisted Clinical Decision Support Demand

Clinical decision support tools powered by AI improve diagnostic accuracy and reduce adverse events, catalyzing rapid uptake among tertiary centers and community hospitals alike. Mayo Clinic’s sepsis risk model trimmed mortality by 18% and shortened average stays by 1.5 days, generating USD 1.5 million in annual savings per 100-bed unit. [2]Mayo Clinic, “AI-Enabled Sepsis Model Outcomes,” mayoclinic.org Emergency departments deploying AI-driven triage cut door-to-provider times 23%, an early indicator of improved throughput. The FDA’s clearance of 521 AI-enabled devices by 2024 provides regulatory confidence, yet adoption varies by specialty: surgeons and radiologists embrace algorithmic support at 73%, whereas family physicians lag at 41%. Vendors that address integration pain points-single-sign-on, structured data capture, and liability protections—earn faster renewals and larger enterprise deals.

Value-based-Care Reimbursement Mandates

As Medicare ties half of its payments to quality measures in 2025, analytics platforms transform from optional reporting tools into revenue-critical infrastructure. Accountable Care Organizations using advanced analytics achieved 15% higher shared-savings payouts and 22% stronger quality scores than peers relying on basic reporting. Geisinger reduced readmissions by 44% and garnered USD 2.8 million in bonuses through analytics-guided care management. [3]Geisinger Health System, “Analytics-Driven Population Health Results,” geisinger.org Commercial payers now require similar capabilities, driving providers to operationalize predictive models for risk adjustment and utilization management. Analytics vendors that embed payer-specific quality metrics directly into clinical workflows gain a strategic edge, converting compliance into competitive differentiation.

Rapid Growth of Real-world Evidence Trials

Pharmaceutical demand for real-world data fuels partnerships that monetize de-identified patient records and boost analytics funds within health systems. The FDA incorporated real-world evidence in 34 approvals during 2024, lowering trial costs 30–40%. An Epic-backed research network pools 280 million patient records, enabling hospitals to earn USD 50,000–200,000 annually per 1,000 specialized cases shared with drug sponsors. Privacy safeguards, notably consent management and de-identification techniques, become procurement deal-breakers, giving technically advanced vendors a pricing premium and shortening sales cycles among research-oriented institutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-quality and interoperability gaps | -2.3% | North America widespread, rural areas most affected | Long term (≥ 4 years) |

| Skills shortage of healthcare data scientists | -1.8% | United States and Canada, non-urban markets | Medium term (2-4 years) |

| Stringent state-level privacy regulations (e.g., CCPA) | -1.2% | California leading, spreading to other states | Short term (≤ 2 years) |

| Capital-budget freezes at rural providers | -0.9% | Rural United States primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data Quality and Interoperability Gaps

Sixty-eight percent of providers cite data inconsistencies-divergent lab units, missing timestamps, or non-standard terminologies-as root causes of analytic inaccuracies. Although the 21st Century Cures Act compels data exchange, semantic interoperability remains elusive, forcing organizations to allocate 60–70% of project budgets to cleansing tasks rather than insight generation. Rural hospitals endure added strain since limited IT staff hinder data governance investments, stretching implementation timelines and dampening returns. Vendors offering pre-mapped vocabularies and automated normalization tools win contracts faster, but overall market penetration slows until system-level data hygiene improves.

Skills Shortage of Healthcare Data Scientists

Demand for domain-literate data scientists outpaces supply by 250%, leaving 73% of rural and community hospitals unable to recruit qualified staff. Salary gaps of up to USD 50,000 compared to technology sector roles escalate turnover. Academic programs embed data science in medical curricula, yet graduates need 2–3 years of field exposure to contribute meaningfully, prolonging maturation curves. Consequently, many providers outsource to consultants, inflating project costs 40–60% and limiting institutional learning. Vendor-managed analytics services provide a stop-gap but may lock organizations into inflexible contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Delivery: Cloud Adoption Reshapes Cost Structures

Cloud deployment captured 64.10% of 2025 revenue, underlining its centrality to the North America clinical data analytics in the healthcare market. The segment is forecast to expand at a 15.78% CAGR through 2031, propelled by elastic compute economics and off-premise security accreditation from hyperscale providers. Hybrid configurations add resilience, storing sensitive data locally while routing high-volume computation to the cloud-an architecture endorsed by 85% of AWS healthcare analytics clients. In contrast, on-premise systems persist in academic research labs requiring ultra-low latency or strict data residency. These dual pathways give vendors a roadmap for modular offerings, supporting incremental migrations rather than rip-and-replace exercises.

Second-wave adopters increasingly evaluate cloud partners on pre-certified compliance artifacts and out-of-the-box interoperability. Analytics providers that layer prescriptive applications atop managed data lakes offer healthcare executives a rapid pathway to clinical ROI, minimizing internal IT lift. As a result, the cloud’s share of the North America clinical data analytics in the healthcare market is projected to cross 70% by 2028, cementing its position as the dominant delivery paradigm.

By Type: Prescriptive Analytics Gains Momentum

Prescriptive analytics recorded the fastest trajectory, advancing at 15.20% CAGR to 2031, though descriptive analytics still accounted for 33.20% of 2025 revenue. Hospitals use descriptive dashboards for compliance but pivot to predictive and prescriptive layers for initiatives tied to financial upside, such as staffing optimization and sepsis prevention. Cleveland Clinic’s prescriptive workload module saved 12% in labor costs without diminishing quality indicators. These successes steer budget re-allocation toward advanced algorithms, boosting segment contribution to the North America clinical data analytics in the healthcare market share over the forecast window.

Investment barriers remain: prescriptive models demand clean data and workflow redesign that not all providers can manage. Vendors incorporating no-code interfaces and real-time explainability features lower adoption hurdles, encouraging mid-tier health systems to leapfrog directly from descriptive reports to action-oriented recommendations.

By Application: Population Health Management Sets the Pace

Population health management accounted for 41.85% of 2025 revenue and advances at 15.31% CAGR, reflecting its synergy with value-based reimbursement structures. Integrated datasets combining claims, clinical, pharmacy, and social determinants of health inform proactive interventions that lower acute episodes. Geisinger’s analytics-guided diabetes program cut emergency visits by 28%. Financial management analytics follow in importance as providers tackle margin compression, whereas operations management tools optimize throughput and bed utilization.

A widening gap emerges between health systems harnessing population health analytics to negotiate risk-based contracts and those limited to retrospective reporting. Payers incentivize adoption with shared-savings bonuses, reinforcing demand across both public and private provider segments. Consequently, population health remains the cornerstone of the North America clinical data analytics in the healthcare market through 2031.

By End-user: Payers Outpace Providers in Growth

Providers retained 70.65% of 2025 spending, yet payer investment grows faster at 15.85% CAGR as insurers deploy analytics for fraud detection, risk scoring, and personalized engagement. Anthem’s platform processes 100 million member interactions annually, flagging early-stage chronic risks and suggesting interventions that reduce total cost of care by double-digit margins. As payers deepen data partnerships with pharmacies and wellness apps, their analytics scope broadens beyond traditional actuarial tasks into preventive care orchestration.

Providers, meanwhile, continue scaling analytics for clinical decision support and capacity management, but capital constraints and staffing shortages slow large-scale transformations. Vendors tailoring offerings to payer workflows-member engagement, network design, and actuarial forecasting-unlock fresh revenue channels, shifting competitive dynamics inside the North America clinical data analytics in the healthcare industry.

Geography Analysis

The United States dominates the North America clinical data analytics in the healthcare market due to sophisticated interoperability frameworks and sizable payer-provider ecosystems. Academic hubs in Boston, San Francisco, and Nashville act as diffusion points for AI-enabled decision support, accelerating adoption across affiliates. Federal initiatives like the CMS Quality Payment Program institutionalize analytics as a compliance necessity, ensuring budgets even in periods of capital restraint.

Canada presents a moderate yet dependable pathway for vendors. Provincial health authorities pursue analytics primarily to reduce emergency department congestion and to manage chronic disease prevalence across sparsely populated regions. Ontario’s centralized data platform simplifies cross-institutional benchmarking, though lengthy procurement cycles can defer go-live dates.

Mexico, while smaller today, offers the region’s highest growth ceiling. Government digitization mandates, combined with rising private-sector interest in medical tourism, foster an environment receptive to analytics. However, standardized data governance remains nascent, compelling suppliers to deliver built-in consent management and Spanish language support. Success in Mexico often hinges on collaborations with local health ministries and in-country system integrators.

Competitive Landscape

Market consolidation continues as providers and payers seek end-to-end platforms instead of point solutions. Epic Systems, Oracle Cerner, and other EHR giants fortify their positions by embedding AI modules that capitalize on existing clinical workflows, generating switching costs that challenge newcomers. Yet cloud-native entrants differentiate through lower total cost of ownership and faster deployment, making inroads at mid-sized hospitals and payer IT departments.

Technology competition centers on algorithm transparency, scalability, and interoperability. Health Catalyst’s patent on predictive deterioration algorithms exemplifies how IP portfolios shape negotiations, especially with health systems pursuing precision medicine. Retail health companies leverage consumer analytics proficiency to craft personalized care pathways, inching into territory once dominated by traditional providers.

Rural healthcare remains an under-penetrated segment but offers volume potential for vendors capable of delivering managed services that circumvent local staffing shortages. Interoperability collaborations and standards advocacy may tilt the field toward suppliers willing to contribute open APIs and participate in industry consortia.

North America Clinical Data Analytics In Healthcare Industry Leaders

Cerner Corporation (Oracle Cerner)

Health Catalyst, Inc.

International Business Machines Corporation

Koninklijke Philips N.V.

McKesson Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Oracle acquired Veracyte’s analytics unit for USD 2.8 billion, bolstering oncology analytics capabilities.

- February 2025: Epic Systems unveiled MyChart Analytics, extending personalized insights directly to patients.

- January 2025: Health Catalyst raised USD 450 million in Series D funding for AI research and global expansion.

- December 2024: AWS launched HealthLake Analytics, a HIPAA-compliant data lake for healthcare customers.

North America Clinical Data Analytics In Healthcare Market Report Scope

Clinical data analytics refers to the use of technology and data-driven techniques to analyze and interpret health-related information, helping healthcare professionals such as physicians, nurses, and public health authorities make informed decisions about patient care. It involves examining various types of clinical data to gain insights into a patient’s health status, identify trends, and improve overall health management. The technology used in clinical data analytics can vary based on the types of data, the intended users of the information, and the actions taken by decision-makers to optimize healthcare outcomes.

The report tracks the revenue generated from providing clinical data analytics in healthcare specific to North America.

North America clinical data analytics in the healthcare market is segmented by mode of delivery (cloud and on-premise), by type (descriptive analysis, diagnostic analysis, predictive analysis, and prescriptive analysis), by application (operations management, financial management, population health management, clinical management), by end-user (payers and providers), country (United States, Canada, Mexico, and Rest of North America). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Mode of Delivery

| Cloud |

| On-premise |

By Type

| Descriptive Analytics |

| Diagnostic Analytics |

| Predictive Analytics |

| Prescriptive Analytics |

By Application

| Operations Management |

| Financial Management |

| Population Health Management |

| Clinical Management |

By End-user

| Payers |

| Providers |

By Country

| United States |

| Canada |

| Mexico |

| By Mode of Delivery | Cloud |

| On-premise | |

| By Type | Descriptive Analytics |

| Diagnostic Analytics | |

| Predictive Analytics | |

| Prescriptive Analytics | |

| By Application | Operations Management |

| Financial Management | |

| Population Health Management | |

| Clinical Management | |

| By End-user | Payers |

| Providers | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How big is the North America clinical data analytics in healthcare market today?

It stands at USD 16.79 billion in 2026 with a forecast to reach USD 32.63 billion by 2031, growing at a 14.21% CAGR over 2026-2031.

Which delivery model is leading adoption among providers?

Cloud deployment leads with 64.10% 2025 revenue and is projected to keep expanding at a 15.78% CAGR over 2026-2031.

What is the fastest-growing application area?

Population health management, advancing at a 15.31% CAGR over 2026-2031 as value-based contracts accelerate analytics demand.

Why are payers increasing their analytics spend?

Insurers use advanced analytics for risk scoring, fraud detection, and personalized member engagement, driving a 15.85% CAGR over 2026-2031.

Which country offers the highest growth potential through 2031?

Mexico, projected to expand at 15.25% CAGR over 2026-2031 thanks to universal coverage initiatives and foreign investment.

What key factor drives AI adoption in clinical decision support?

Demonstrated outcomes like Mayo Clinic’s 18% mortality reduction in sepsis cases foster rapid uptake of AI-powered tools.

Page last updated on: