Low-Intensity Sweeteners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

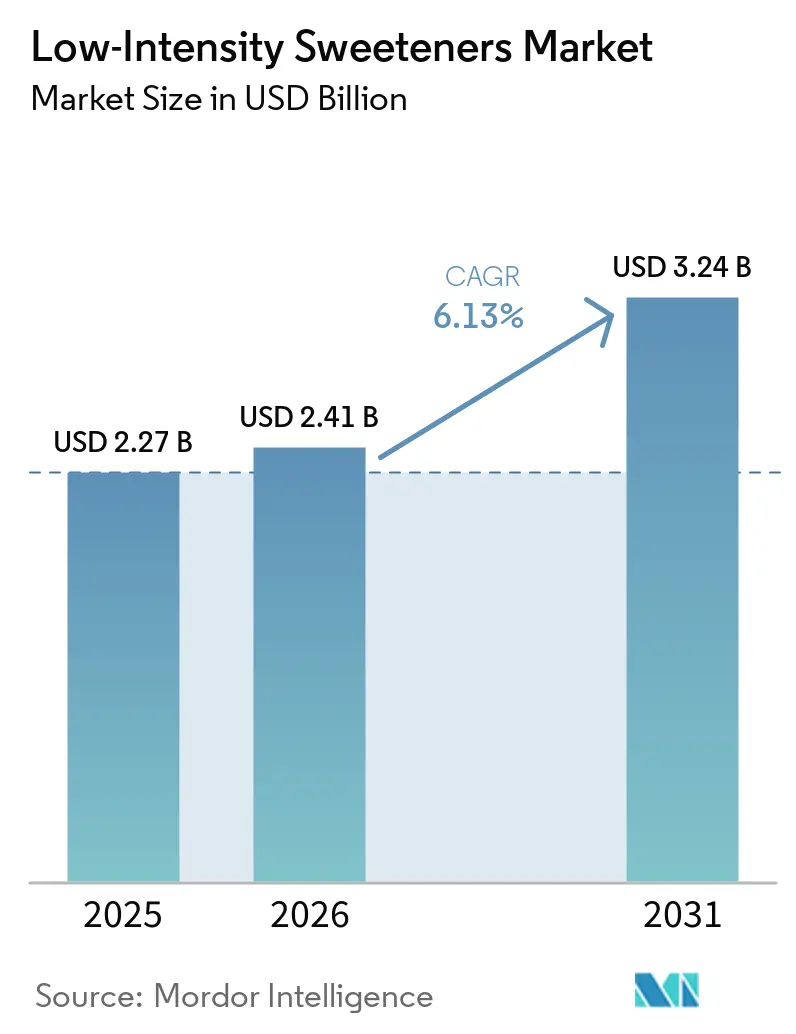

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.24 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

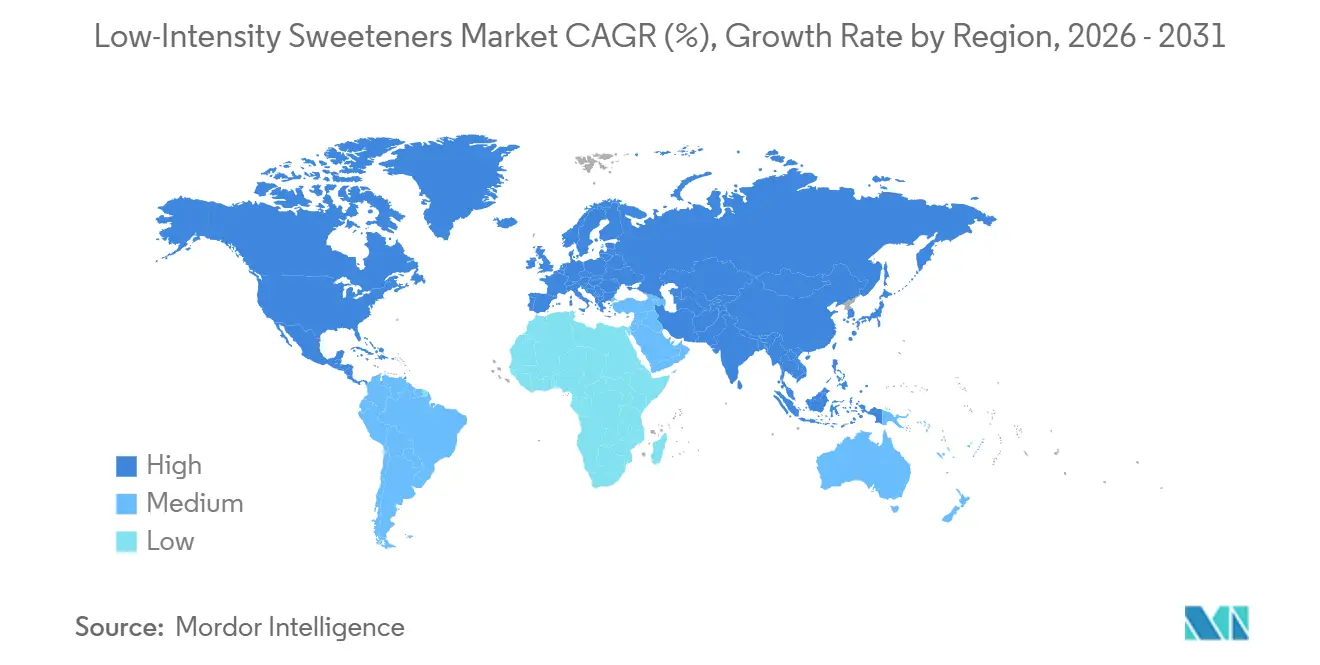

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Low-Intensity Sweeteners Market Analysis by Mordor Intelligence

The Low-Intensity Sweeteners Market size is expected to increase from USD 2.27 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.24 billion by 2031, growing at a CAGR of 6.13% over 2026-2031. This growth momentum is fueled by widespread sugar-reduction mandates, a rising incidence of diabetes, and swift technological advancements that have reduced production costs for polyols and rare sugars. Manufacturers are not only substituting traditional sugars but are also venturing into nutraceuticals, pharmaceuticals, and functional foods. In these sectors, sweeteners serve a dual purpose: enhancing flavor and providing health benefits. Regulatory bodies are converging, as seen with the European Union's swift authorization of erythritol and its ongoing evaluation of D-allulose. This trend is shortening approval timelines and promoting global formulation consistency. Concurrently, there's a growing preference for clean-label products, emphasizing fermentation and enzymatic synthesis. However, trade actions targeting Chinese erythritol have prompted Western buyers to diversify their supply chains.

Key Report Takeaways

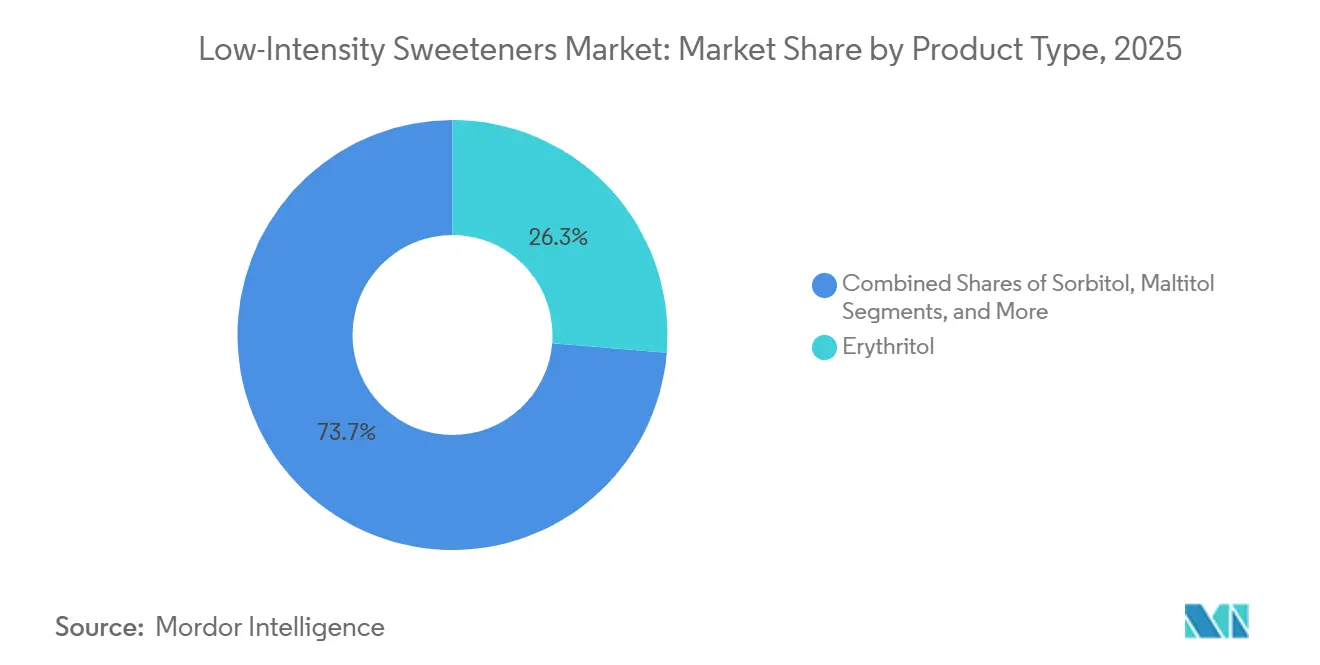

- In 2025, erythritol secured a 26.32% share of the low-intensity sweeteners market and is expected to grow at a 7.76% CAGR from 2026 to 2031.

- In 2025, powder/crystal forms dominated the low-intensity sweeteners market with a 59.89% share, while liquid/syrup variants are projected to grow at a 6.58% CAGR through 2031.

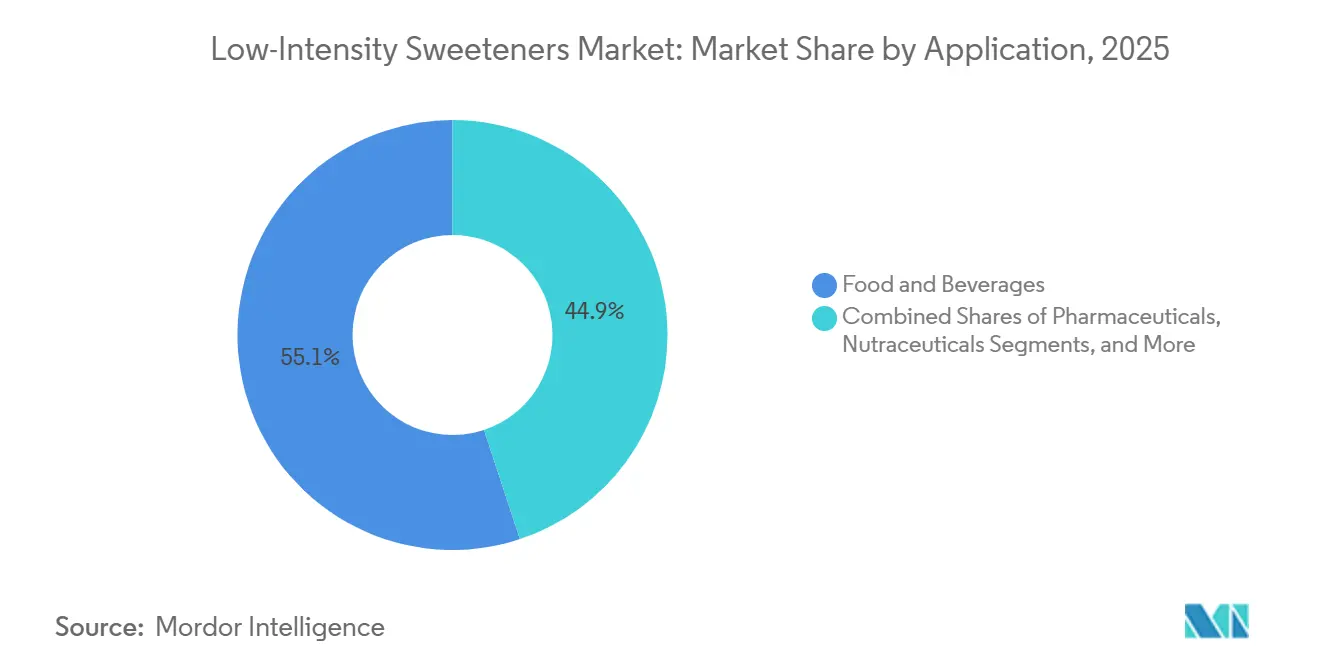

- In 2025, the food and beverage sector led the low-intensity sweeteners market with a 55.09% share, while nutraceuticals and dietary supplements are anticipated to grow at a 6.93% CAGR through 2031.

- In 2025, North America held a commanding 31.87% share of the low-intensity sweeteners market, while Asia-Pacific is forecasted to grow at a 7.06% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low-Intensity Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and sugar reduction goals | +1.2% | Global, with strongest influence in North America and Europe | Medium term (2-4 years) |

| Expansion of clean-label and natural ingredient preferences | +0.9% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Regulatory pressure to lower added sugar levels | +1.5% | North America, Europe, with emerging influence in Asia-Pacific | Short term (≤ 2 years) |

| Technological advancements in sweetener formulation | +0.8% | Global, with innovation hubs in Asia-Pacific and North America | Long term (≥ 4 years) |

| Demand for sugar-free beverage categories | +1.0% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth of keto-friendly and low-carbohydrate diets | +0.7% | North America and Europe, with spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness and Sugar Reduction Goals

Consumers in both developed and emerging markets are becoming more aware of the health impacts of sugar, which is driving changes in their purchasing habits. The International Food Information Council's 2025 Food and Health Survey revealed that 63 percent of Americans are concerned about their sugar intake. Among them, 75 percent are actively reducing or avoiding sugar, and 63 percent are specifically focusing on cutting added sugars[1]Source: International Food Information Council, "2025 IFIC Food & Health Survey: A Focus On Sugars & Sweeteners", ific.org. This shift goes beyond just reading labels. About 30 percent of respondents now use Nutrition Facts panels more often to choose products with less added sugar, up from 23 percent in 2021. Similarly, 25 percent of consumers are buying sugar-free products when available, compared to 21 percent four years ago. The growing use of glucagon-like peptide-1 receptor agonist (GLP-1) medications for weight management is also influencing behavior. A 2024 PwC survey found that over 8 percent of Americans are using GLP-1 drugs, and 57 percent of these users are paying closer attention to added sugar content. These combined trends are pushing low-intensity sweeteners into the mainstream, especially in product categories where it is important to maintain bulk and texture while reducing sweetness.

Expansion of Clean-Label and Natural Ingredient Preferences

Manufacturers are increasingly adopting plant-based fermentation methods to produce polyol sweeteners, driven by the growing demand for simple, minimally processed ingredients. In October 2025, The Humble Co. introduced a COSMOS Natural-certified toothpaste range that uses xylitol as a humectant and sweetener. This toothpaste is marketed as free from PFAS, PTFE, sodium lauryl sulfate, and sugar, reflecting the rising consumer preference for transparent and sustainable oral care products. Roquette has also made significant strides in this area by investing EUR 25 million to expand its liquid and powder polyol production capacity at its Lestrem, France facility. The company focuses on plant-based sources like maize and wheat, positioning polyols as key ingredients in sugar-reduced products such as confectionery, chocolates, chewing gums, and baked goods. The demand for clean-label products is also influencing the pharmaceutical industry, where high-purity polyols are widely used as excipients in directly compressible tablets. These polyols are approved by global drug authorities for use in oral dosage forms, injectable solutions, and dialysis treatments. As food-grade and pharmaceutical-grade quality standards increasingly overlap, suppliers that ensure traceability, non-GMO sourcing, and compliance with ISO and cGMP frameworks are unlocking new opportunities across multiple sectors.

Regulatory Pressure to Lower Added Sugar Levels

Government mandates are accelerating reformulation timelines and enforcing stricter sugar reduction standards across various product categories. In 2024, the U.S. Department of Agriculture required school meals to limit added sugars to 10 percent of total calories by the 2027-2028 school year. This rule impacts breakfast and lunch programs serving about 30 million children daily, driving demand for sugar-reduced products in dairy, baked goods, and beverages. In 2025, the FDA proposed a front-of-package labeling rule introducing a 'high-in' symbol for products exceeding limits on added sugars, sodium, and saturated fat[2]Source: U.S. Food and Drug Administration, "Front-of-Package Labeling," fda.gov.. This penalizes products using sucrose or high-fructose corn syrup while encouraging the use of non-nutritive and low-calorie sweeteners. In Europe, Nutri-Score labeling and quantum satis regulations for polyols require warning labels on products with over 10 percent polyols by weight. While this restricts dosage levels, it also validates polyols as safe and functional within defined limits. The lack of global regulatory alignment creates challenges for multinational manufacturers but offers an edge to suppliers with strong regulatory expertise and the ability to navigate diverse approval processes.

Technological Advancements in Sweetener Formulation

Fermentation is revolutionizing the production of rare sugars, slashing costs and minimizing environmental impacts. This method also bolsters domestic supply chains, mitigating geopolitical risks. Samyang Corporation, having pioneered enzyme technology for liquid allulose in 2016, ramped up to mass production by 2020. That same year, they clinched the FDA's Generally Recognized as Safe status. By September 2024, they unveiled a 13,000-tonne-per-year facility, churning out both liquid and crystalline allulose, now en route to North America, Japan, and Southeast Asia. Baolingbao Biology, in collaboration with Coca-Cola and PepsiCo, is harnessing fermentation to transform glucose into polyols, specifically erythritol and allulose. They're channeling an investment of USD 85 million to establish a similar setup in the U.S., aiming to sidestep countervailing duties on Chinese erythritol imports, a move set for May 2025. Meanwhile, DuPont is pushing the envelope with ion-exchange resin technology, refining liquid sugar syrups. This not only prolongs shelf life but also ensures these syrups, now neutral-colored and low in impurities, are primed for carbonated drinks and fruit juice blends. Thanks to these innovations, the cost disparity between rare sugars and standard polyols is narrowing, paving the way for broader adoption in premium and functional products.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste profile limitations and aftertaste issues | -0.6% | Global, particularly in cost-sensitive and mass-market segments | Medium term (2-4 years) |

| Higher reformulation complexity for manufacturers | -0.4% | Global, with greater friction in small and mid-sized enterprises | Short term (≤ 2 years) |

| Price volatility of natural sweetener raw materials | -0.3% | Global, concentrated in corn-dependent supply chains | Short term (≤ 2 years) |

| Emerging erythritol safety concerns | -0.8% | North America and Europe, with potential spillover to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Taste Profile Limitations and Aftertaste Issues

Polyol sweeteners provide cooling sensations but can cause laxative effects at high doses, making them difficult to use as direct sugar substitutes. The FDA requires warning labels on products exceeding 20 grams of mannitol or 50 grams of sorbitol per day, highlighting potential laxative effects. This restricts their use in confections and reduces acceptance among sensitive consumers. Similarly, the European Union mandates warnings for foods with over 10% added polyols, further limiting their application in chocolate, chewing gum, and baked goods. Maltitol, often used to mask bitterness in high-intensity sweeteners, offers partial sweetness and needs blending with other polyols or rare sugars to mimic sucrose[3]Source: European Union, "Food Additives Regulations", ec.europa.eu.. Xylitol, valued for its anti-cariogenic benefits in oral care, can cause gastrointestinal discomfort, requiring gradual introduction and consumer education. These challenges drive investments in taste-masking technologies and multi-component sweetener systems but create barriers for manufacturers lacking expertise or proprietary blends.

Emerging Erythritol Safety Concerns

In 2024 and 2025, peer-reviewed studies raised concerns about the cardiovascular safety of erythritol, the market's top polyol by volume and revenue. Research in JACC Advances and the European Heart Journal linked high plasma erythritol levels to increased risks of major cardiovascular events, such as heart attacks and strokes. A 2024 study in Arteriosclerosis, Thrombosis, and Vascular Biology suggested erythritol may heighten thrombotic risk by increasing platelet reactivity. Additionally, a 2025 study in the Journal of Applied Physiology associated erythritol with brain endothelial dysfunction, while the European Journal of Preventive Cardiology found a connection between polyol intake and coronary heart disease in women. Despite these findings, the FDA has not revoked erythritol's GRAS status, and no regulatory actions have been taken. However, food and beverage companies are reformulating products cautiously, and health-conscious consumers are showing increased skepticism. This uncertainty is driving interest in rare sugars like allulose and tagatose, which, while lacking extensive safety data, have not shown similar negative signals. Suppliers capable of scaling production and securing regulatory approvals in multiple regions are well-positioned to capitalize on this opportunity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Erythritol Dominates Amid Safety Scrutiny

In 2025, erythritol accounted for 26.32 percent of the Low Intensity Sweeteners Market, with an expected annual growth rate of 7.76 percent through 2031. Its popularity stems from its zero-calorie profile, better digestive tolerance compared to other polyols, and regulatory approvals in key regions like North America, Europe, and Asia-Pacific. Most production is concentrated in China, where Shandong Sanyuan operates a 135,000-tonne annual capacity, holding 32.94 percent of the global market. To counter U.S. duties on Chinese erythritol imports, Baolingbao announced a USD 85 million investment in February 2025 to build a 30,000-tonne plant in the U.S. Jungbunzlauer markets ERYLITE erythritol as a natural, non-GMO polyol made from plant-based materials through yeast fermentation. It is often combined with high-intensity sweeteners like stevia to improve sweetness and mouthfeel in sugar-free beverages.

Rare sugars, such as allulose, tagatose, and isomaltulose, are the fastest-growing segment in the Low Intensity Sweeteners Market, driven by regulatory changes and advancements in fermentation-based production. In November 2025, the FDA allowed D-tagatose to be excluded from total and added sugars on Nutrition Facts labels and assigned it a caloric value of 1.5 kilocalories per gram, providing a labeling advantage over traditional sugars and some polyols. In September 2024, Samyang Corporation opened a KRW 140 billion (USD 105 million) facility in South Korea, quadrupling its annual allulose capacity to 13,000 tonnes and producing liquid and crystalline forms for export to North America, Japan, and Southeast Asia. Allulose, with 70 percent of sucrose's sweetness and negligible calories, caramelizes when heated, making it ideal for baked goods and confectionery.

By Form: Powder Dominance Meets Liquid Innovation

In 2025, powder and crystal forms led the Low Intensity Sweeteners Market with a 59.89% share, driven by their use in pharmaceutical excipients, dry-mix beverages, and confectionery, where flowability, compressibility, and shelf stability are essential. Roquette offers high-purity polyols as excipients for oral dosage forms, including tablets for swallowable, chewable, dispersible, and effervescent formats, as well as active pharmaceutical ingredients approved for injectable solutions and dialysis. In February 2024, Gujarat Ambuja Exports expanded its sorbitol production capacity to 500 tonnes per day across four Indian locations by commissioning a 100-tonne-per-day production line, targeting pharmaceutical-grade and food-grade markets. Mannitol and xylitol are key in tablet formulations for controlling hygroscopicity and ensuring stability, with studies showing their blends improve mechanical strength and dissolution in medicated confectionery and orally disintegrating tablets. Powder forms also dominate keto-friendly baking mixes, protein powders, and dietary supplements, offering free-flowing, easy-to-measure ingredients that dissolve cleanly without residue.

Liquid and syrup formats are expected to grow at 6.58% annually through 2031, driven by beverage manufacturers seeking ready-to-use formulations that simplify processes, reduce energy use, and improve quality control. DuPont’s Amberlite resin technology decolorizes and deashes raw sugar syrups, removing impurities to produce low-impurity liquid sugars with extended shelf life for carbonated beverages, fruit juice blends, and long-distance shipping. Samyang Corporation produces liquid and crystalline allulose at its 13,000-tonne South Korean facility, with liquid formats preferred for export and direct use in beverage production. Jungbunzlauer promotes liquid erythritol for low-calorie drinks, highlighting its ability to enhance mouthfeel while maintaining clarity and stability. The shift to liquid formats is notable in Asia-Pacific, where high-speed bottling lines and just-in-time manufacturing favor pre-dissolved sweeteners that reduce downtime and contamination risks. In North America, beverage companies are reformulating products to meet labeling requirements and growing demand for sugar-free options.

By Application: Beverages Lead, Nutraceuticals Surge

In 2025, food and beverages led the Low Intensity Sweeteners Market, contributing 55.09 percent of the demand. This growth stemmed from reformulations in carbonated soft drinks, sports nutrition, dairy alternatives, confectionery, and baked goods. In March 2026, PepsiCo introduced Gatorade Lower Sugar, reducing sugar by 75 percent and eliminating artificial sweeteners. It also launched Pepsi Prebiotic Cola, a fiber-enriched, reduced-sugar drink, and acquired Poppi, a prebiotic soda brand, for USD 1.95 billion, signaling its focus on functional beverages. In April 2026, Mars Wrigley released Extra Plus chewing gum with three functional variants. The Deep Clean variant, containing xylitol, claims to reduce surface tooth stains in 12 weeks with regular brushing, while the Chill variant, infused with niacin, supports mental well-being.

The nutraceuticals and dietary supplements segment is expected to grow at 6.93 percent annually through 2031, outpacing other applications. This growth is driven by clean-label trends, the popularity of keto and low-carb diets, and rising functional health claims. The IFIC 2025 Food and Health Survey found that 75 percent of Americans are reducing or avoiding sugar, with 63 percent focusing on added sugars. Sugar-free product purchases rose to 25 percent in 2025, up from 21 percent in 2021. The adoption of GLP-1 receptor agonist medications for weight management is also driving this trend, with 57 percent of users monitoring added sugar intake and 44 percent seeking low-sugar, electrolyte-rich supplements for hydration. Beneo promotes Palatinose (isomaltulose) as a low-glycemic carbohydrate that may enhance GLP-1 secretion and provide sustained energy, making it suitable for sports nutrition and weight management.

Geography Analysis

In 2024, North America commands a 32.16% share of the low-intensity sweeteners market, underscoring its status as the industry's most mature and sophisticated hub. This dominance is bolstered by established regulatory frameworks and a robust consumer acceptance of sugar alternatives. The FDA's GRAS (Generally Recognized As Safe) notification system has greenlit a multitude of polyols and rare sugars, fostering an innovative regulatory landscape. Heightened health consciousness, spurred by rising diabetes and obesity rates, fuels the demand for low-calorie alternatives across diverse product categories. A recent investigation by the U.S. Department of Commerce into Chinese erythritol imports underscores North America's dedication to safeguarding its domestic production while championing fair trade practices. Meanwhile, Health Canada's endorsement of various polyols broadens market access, and Mexico's burgeoning middle class, coupled with heightened health awareness, presents lucrative expansion prospects within the NAFTA framework.

Asia-Pacific is set to outpace all regions, boasting an 8.11% CAGR through 2030. This surge is attributed to swift economic growth, urbanization, and a burgeoning health consciousness among its expanding middle class. China's sugar-free beverage market, eyeing a valuation nearing USD 2.78 billion by 2025, epitomizes this growth trajectory as consumers pivot towards healthier choices. Japan's elderly demographic and pronounced diabetes rates bolster the demand for glycemic-friendly sweeteners. South Korea's updated Food Additive Code signals a regulatory evolution, paving the way for market growth. India's vast populace and rising disposable incomes hint at substantial long-term prospects, albeit with regulatory frameworks lagging behind their East Asian counterparts. China's robust manufacturing capabilities offer cost benefits, bolstering global supply chains, yet trade frictions with Western markets are nudging a diversification in these supply chains.

Europe presents a dual-edged sword: its intricate regulatory landscape poses challenges, yet also unveils opportunities. The European Food Safety Authority's stringent evaluations uphold safety standards, albeit at the risk of delaying the market entry of novel sweeteners. Recent EU endorsements of erythritol and the ongoing assessment of D-allulose hint at a regulatory alignment that could hasten market expansion. However, the region's steep anti-dumping duties on Chinese erythritol imports, spanning 34.4% to 233.3%, serve to shield domestic producers, albeit at the potential expense of downstream manufacturers. Germany, the UK, and France spearhead market evolution, driven by a pronounced consumer inclination towards natural and organic offerings. Europe's exacting labeling mandates and discerning consumers cultivate a premium pricing landscape for top-tier products that align with clean-label standards.

Competitive Landscape

The low-intensity sweeteners market, characterized by moderate fragmentation, signals ripe opportunities for consolidation as the industry evolves. Strategic maneuvers reveal a dual approach: Industry giants, Cargill and Ingredion, are not only reaping the benefits of commodity polyols but are also investing heavily in the promising domain of rare sugar technologies. Cargill's strategic edge is highlighted by its GRAS notification for erythritol (GRN No. 789), showcasing its regulatory foresight. Such early investments, especially in alignment with the U.S. Food and Drug Administration, offer significant market access advantages.

Ingredion's acquisition of PureCircle, coupled with its dominant 88% ownership stake, underscores the industry's consolidation trend. This move is further amplified by Ingredion's impressive USD 8.2 billion net sales, with a notable 4% increase in specialty ingredients, particularly low-intensity sweeteners. In this competitive landscape, technological deployment emerges as the pivotal differentiator, especially as enzymatic production capabilities redefine standings in the rare sugar market.

Roquette's partnership with Bonumose for tagatose production underscores the power of strategic alliances in accessing technology and accelerating market penetration. Yet, there's a vast, untapped potential in pharmaceutical excipient applications and customized formulations for diabetic products. Successfully navigating the regulatory landscape in these areas can confer enduring competitive advantages. Moreover, the complex patent landscape surrounding enzyme engineering and fermentation refinement serves as a protective barrier, favoring entities with strong R&D capabilities and astute regulatory insights.

Low-Intensity Sweeteners Industry Leaders

-

Cargill, Incorporated

-

Ingredion Incorporated

-

Roquette Frères S.A.

-

Tate & Lyle PLC

-

Südzucker AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Iranian Company Launched Sorbitol Production, Catering to Pharmaceutical and Food Industries. The newly established sorbitol production facility in Iran, the first of its kind in West Asia, boasts an annual capacity of 7,500 tons of liquid sorbitol at 70% concentration.

- December 2024: Tate & Lyle PLC has teamed up with BioHarvest Sciences in a bid to meet rising consumer demand for healthier, sustainable options. Their joint effort focuses on crafting next-generation, plant-based sweeteners through innovative botanical synthesis technology. The goal is to produce cost-effective, nutritious sugar alternatives that replicate sugar's taste, sans the aftertaste.

- August 2024: RHEWUM's advanced technology has been selected by a leading player in Turkey's starch industry for the production of sorbitol. Sorbitol, a highlight in their product lineup, is a natural sweetener known for its low calorie count and minimal impact on blood sugar levels.

Global Low-Intensity Sweeteners Market Report Scope

| Xylitol |

| Sorbitol |

| Erythritol |

| Maltitol |

| Mannitol |

| Isomalt |

| Rare Sugars (Allulose, Tagatose, Isomaltulose) |

| Powder/Crystal |

| Liquid/Syrup |

| Food and Beverages |

| Pharmaceuticals |

| Dietary Supplements |

| Personal Care and Oral Care |

| Other Industrial Uses |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Xylitol | |

| Sorbitol | ||

| Erythritol | ||

| Maltitol | ||

| Mannitol | ||

| Isomalt | ||

| Rare Sugars (Allulose, Tagatose, Isomaltulose) | ||

| By Form | Powder/Crystal | |

| Liquid/Syrup | ||

| By Application | Food and Beverages | |

| Pharmaceuticals | ||

| Dietary Supplements | ||

| Personal Care and Oral Care | ||

| Other Industrial Uses | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the low-intensity sweeteners market?

The low-intensity sweeteners market size is valued at USD 2.41 billion in 2026.

How fast is the low-intensity sweeteners market expected to grow?

It is forecast to expand at a 6.13% CAGR, reaching USD 3.24 billion by 2031.

Which product segment holds the largest share?

Erythritol leads with 26.32% of 2025 share and records the fastest 7.76% CAGR through 2031.

Which region will grow the quickest?

Asia-Pacific posts the highest projected 7.06% CAGR between 2026-2031 due to expanding health-conscious middle-class consumers.

Page last updated on: