Flavored Syrups Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

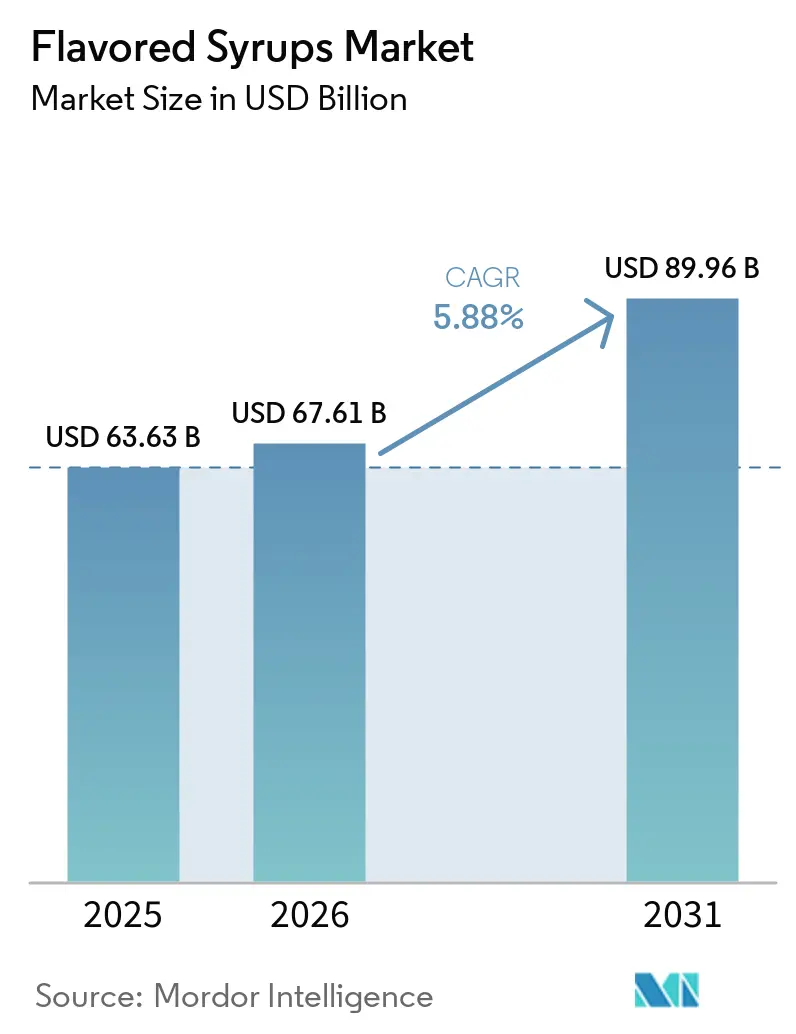

| Market Size (2026) | USD 67.61 Billion |

| Market Size (2031) | USD 89.96 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

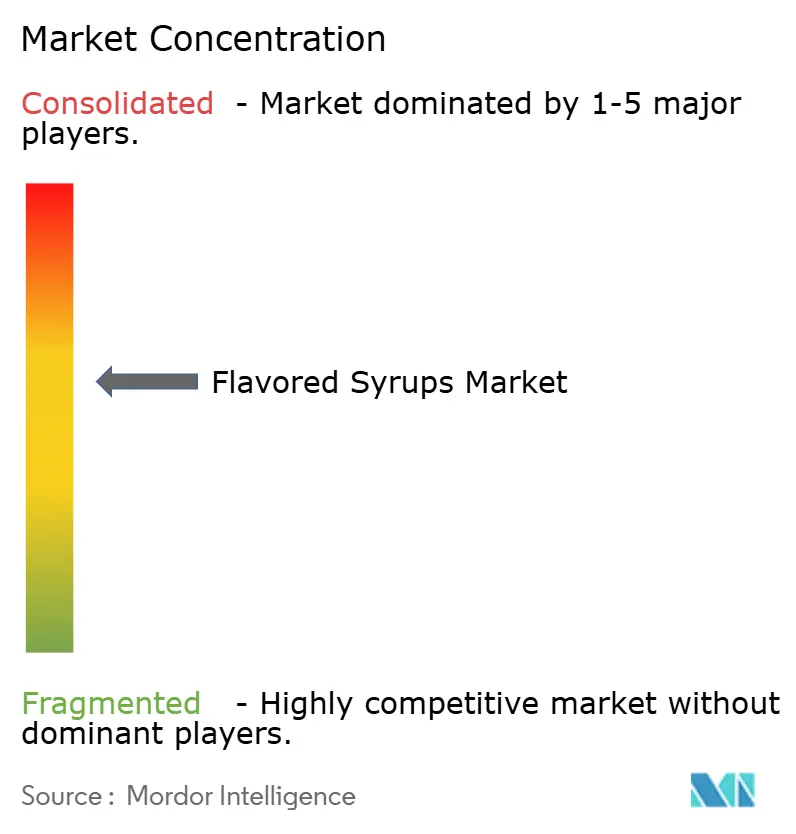

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Flavored Syrups Market Analysis by Mordor Intelligence

The flavored syrups market size was valued at USD 63.63 billion in 2025, is expected to increase to USD 67.61 billion in 2026, and reach USD 89.96 billion by 2031, growing at a CAGR of 5.88% between 2026 and 2031. Growth is being fueled by café expansion, home-mixology habits that took root during pandemic lockdowns, and the shift of flavor customization from a premium perk to an operating necessity for beverage chains. North America led with 35.40% of the flavored syrups market share in 2025, but Asia-Pacific is set to expand at 7.58% CAGR on the strength of rising urban incomes and specialty coffee adoption. Product innovation is splitting into two tracks: indulgent dessert profiles that encourage experiential consumption and botanical or functional blends that align with wellness spending. Parallel pressure from new FDA sugar-and-color rules and vanilla price shocks is accelerating reformulation toward non-nutritive sweeteners and natural colorants, while biotechnology and vertical integration are redrawing competitive fault lines.

Key Report Takeaways

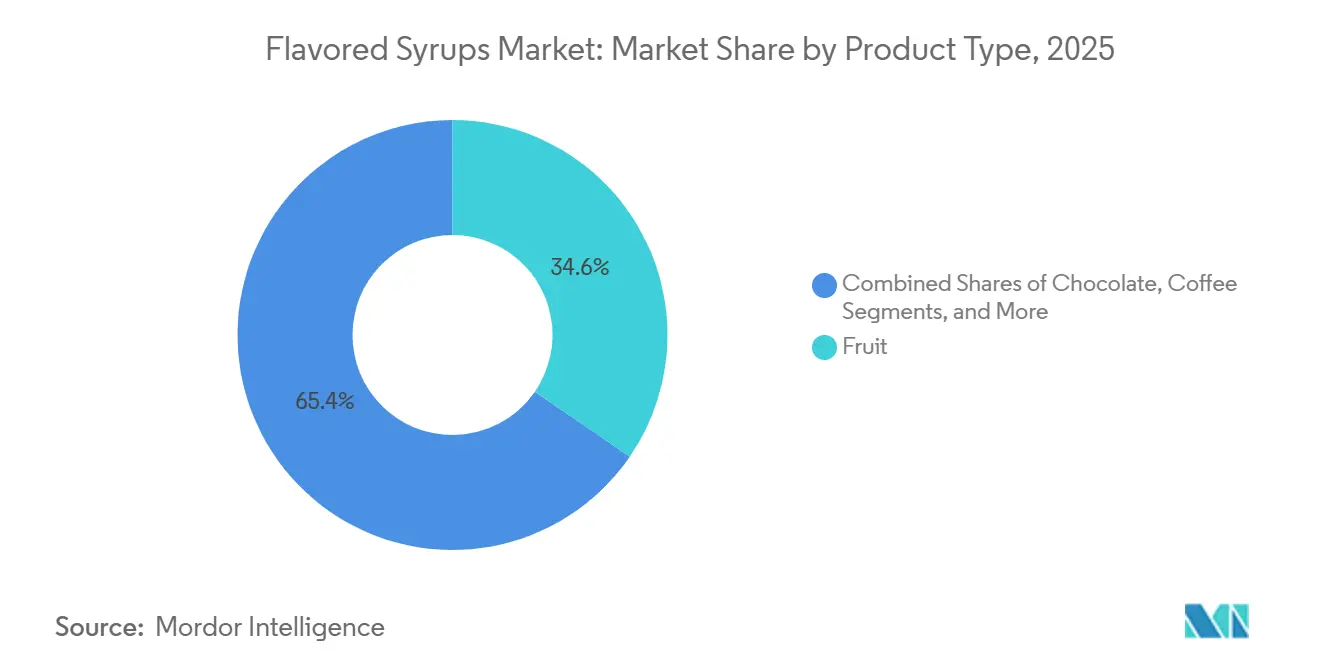

- By product type, fruit syrups led with 34.59% flavored syrups market share in 2025, and herbs and botanicals will be the fastest-growing segment at a 7.48% CAGR through 2031.

- By application, beverages commanded 35.69% of 2025 revenue, whereas functional foods will advance at 6.97% CAGR to 2031.

- By distribution channel, B2B–foodservice held 55.72% share in 2025, while direct-to-consumer e-commerce will expand at 7.70% CAGR on the back of at-home mixology and subscription models.

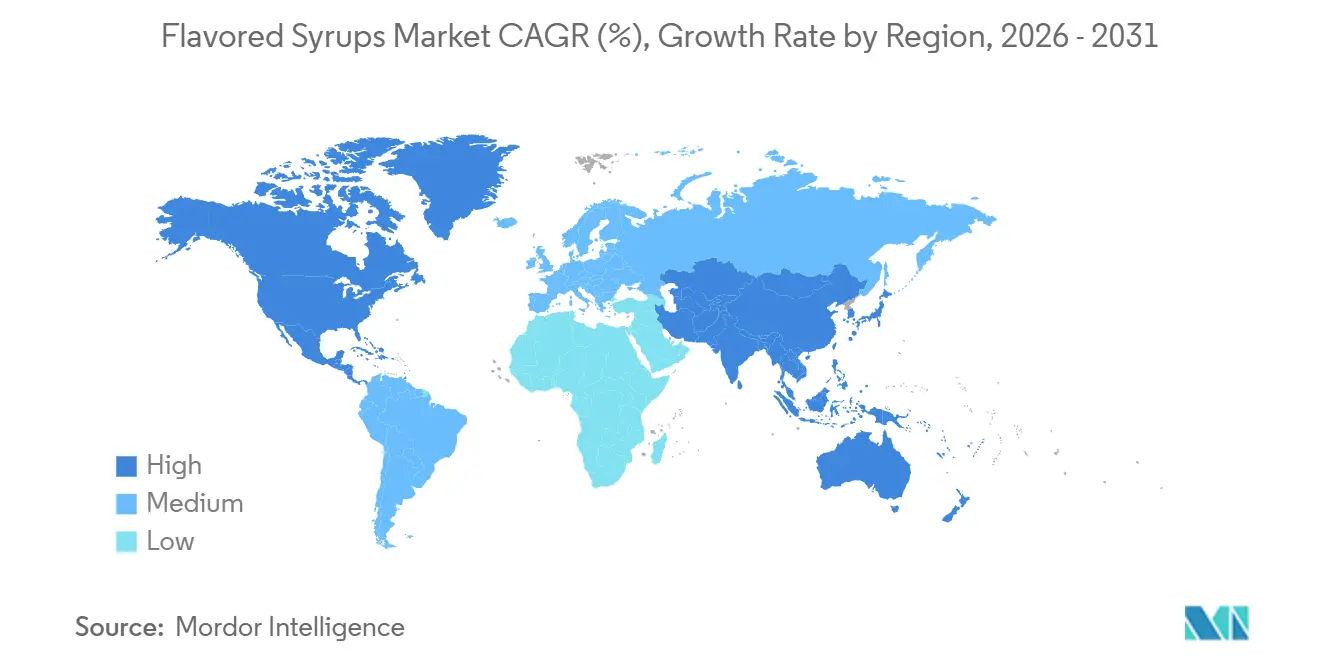

- Geographically, North America remains the largest flavored syrups market, yet Asia-Pacific will represent the fastest-expanding territory with a 7.58% CAGR forecast through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flavored Syrups Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in exotic and global flavor profiles | +1.2% | Global, with accelerated adoption in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Premiumization and artisanal café culture | +1.5% | North America, Europe, and Tier-1 cities in the Asia-Pacific | Medium term (2-4 years) |

| Expansion of RTD beverages using compound syrups | +1.3% | Global, with the strongest growth in Asia-Pacific and North America | Short term (≤ 2 years) |

| Foodservice chains' menu localization drives SKU proliferation | +0.9% | Asia-Pacific, Latin America, and the Middle East and Africa | Medium term (2-4 years) |

| Novel botanical and functional syrup infusions | +1.1% | North America and Europe, spill-over to the Asia-Pacific wellness segments | Long term (≥ 4 years) |

| Versatility in culinary applications | +0.8% | Global, with emphasis on North America and Europe, foodservice innovation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Innovation in Exotic and Global Flavor Profiles

Cross-cultural flavor migration is driving an increase in SKUs and altering regional taste hierarchies. Dragon fruit is set to see a rise in new product launches through 2025, primarily in refreshing beverages, but also branching out into confectionery and alcoholic formats. In the USA, Korean gochujang launches jumped 120% year-over-year. Meanwhile, bulgogi leaped from being an emerging flavor in 2025 to the fourth fastest-growing entry on Kerry's 2026 Meat and Meals chart, highlighting the swift mainstream acceptance of once-niche ethnic flavors. Southeast Asian flavors like ube, black sesame, and pistachio-rose are transitioning from independent cafés to chain menus. Notably, Starbucks debuted an Iced Ube Coconut Macchiato in spring 2026, featuring toasted coconut syrup and ube coconut cream cold foam, underscoring major-chain endorsement of these flavors. Flavor houses are adapting by curating region-specific syrup portfolios. Falmont Flavors noted that 29% of Asia-Pacific consumers are keen on coffee flavor experimentation, with about one-third favoring sweet variants. This cross-cultural flavor exchange presents two avenues for syrup suppliers: they can either curate a diverse portfolio spanning various ethnic cuisines or focus on authenticated single-origin extracts, which fetch premium prices in specialty markets.

Premiumization and Artisanal Café Culture

As specialty coffee enters its third wave, it's reshaping syrup formulation standards and profit margins. Asia is on track to lead the global coffee market, with regional demand surging. Notably, China has overtaken Japan as the region's second-largest coffee market. The number of branded coffee outlets in China has also surpassed the U.S., reflecting the growing demand for unique flavor profiles. Premiumization is splitting into two paths: one emphasizes authenticity, showcasing single-origin vanilla or fair-traded cocoa, while the other leans into innovation. For example, Torani plans to launch a Zero Calorie Beverage Sauce in February 2025, tailored for cold drinks and priced at USD 6.99 for a 12.8-ounce bottle. Artisanal brands are prioritizing traceability; Madagascar vanilla is adapting to the EU's 2024/1211 regulation, which mandates blockchain documentation covering farm location, harvest date, curing method, and worker pay verification. While this adds USD 18-25 per kilogram to production costs, it bolsters premium claims. Independent cafés are differentiating from chains by crafting syrups and using freeze-dried fruit garnishes, driving demand for bespoke concentrates and artisanal formulation services, which flavor houses can monetize through technical collaborations.

Expansion of RTD Beverages Using Compound Syrups

Ready-to-drink formats are shifting from convenience to platforms emphasizing functionality and experience, increasing the complexity of compound syrups. While the global non-alcoholic beverage market is growing, many U.S. alcohol consumers find non-alcoholic alternatives overpriced, driving demand for cost-effective flavor solutions that convey value[1]Source: Graphic Packaging International, “Beverage Trends Report,” graphicpkg.com . The rising popularity of prebiotic sodas offers flavored syrup suppliers an opportunity to create prebiotic-compatible formulations that mask fiber off-notes and emphasize gut health. Protein fortification is expanding into ready-to-drink (RTD) coffee and flavored water, requiring syrups that enhance mouthfeel and mask chalky amino-acid flavors. Sensient’s BioSymphony, a natural flavor portfolio, uses biotransformation to mask off-notes, reduce chalkiness in high-protein drinks, and enhance vanilla and cocoa flavors. The "dirty soda" trend – fountain sodas with creams, syrups, and add-ins – gained over 70 million TikTok views in summer 2025 under #DirtySoda, prompting retailers to explore soda bars and remix kits. These position syrups as tools for modular customization rather than fixed formulations. This modular approach benefits suppliers offering texture-stabilizing formulations and functional syrup blends that perform consistently across carbonation, cold foam, and high-protein applications.

Foodservice Chains' Menu Localization Drives SKU Proliferation

Quick-service restaurants (QSRs) are moving away from standardized menus, opting for hyperlocal flavor adaptations. In Mumbai, global chains like McDonald's, Domino's, and Starbucks are investing in research and development to create India-specific menus featuring items like masala chai, filter coffee, and regional spice profiles. Homegrown operators are exploring Pan-Asian and Middle Eastern formats tailored to local spice tolerances and vegetarian preferences. Delivery platforms Zomato and Swiggy provide outlet-level data, guiding seasonal and location-specific offerings. This enables suppliers to propose region-specific or limited-run syrup SKUs based on point-of-sale analytics. Localization also extends to formulation, with rising demand for plant-based, low-sugar, and portion-controlled options. Syrup manufacturers are responding with modular add-ons and clean-label formulations. In China, regulations like the "Three Red Lines" policy limit high-sugar drinks near schools, while proposed beverage taxes target products with over 5 grams of sugar per 100 milliliters. These measures are driving reformulation toward low- or no-sugar concentrates. Suppliers leveraging data-driven SKU planning and rapid pilot-to-scale capabilities are well-positioned to capture market share in this fragmented demand environment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and labeling regulations | -0.7% | Global, with heightened enforcement in North America and Europe | Short term (≤ 2 years) |

| Concerns over artificial additives, preservatives, and sweeteners | -0.9% | North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Supply chain disruptions are affecting the sourcing of specialty ingredients | -0.6% | Global, with an acute impact on Madagascar vanilla and West African cocoa sourcing | Short term (≤ 2 years) |

| Risk of flavor fatigue and oversaturation | -0.4% | Mature markets in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Food Safety and Labeling Regulations

Regulatory tightening is compressing reformulation timelines and escalating compliance costs. The FDA's updated "healthy" claim rule, effective February 2025 with compliance by February 2028, imposes strict food-group-equivalent requirements and added sugar limits, barring most high-sugar syrups unless reformulated with non-nutritive sweeteners[2]Source: U.S. Food and Drug Administration, “Guidance on Added Sugars and Colorants,” fda.gov. The FDA's Human Foods Program 2026 priorities include mandatory notification for all substances claimed as Generally Recognized as Safe (GRAS), with a draft rule under OMB review since December 2025, creating uncertainty for syrup manufacturers relying on self-affirmed GRAS status. Additionally, the FDA is reviewing chemicals deemed "most concerning to consumers," such as phthalates, propylparaben, BHA, and BHT, and plans to release a Systematic Post-Market Assessment. The FDA is also monitoring industry commitments to eliminate petroleum-based certified color additives, including FD and C Green No. 3, Red No. 40, and Yellow Nos. 5 and 6, by the end of 2027. Major buyers like Walmart aim to remove these colors from private-brand foods by January 2027, forcing suppliers to reformulate or risk losing distribution. Manufacturers face rising reformulation costs, longer lead times for natural-color approvals, and legal risks if "no artificial colors" claims are deemed misleading under ambiguous "petroleum-based" definitions.

Concerns Over Artificial Additives, Preservatives, and Sweeteners

In 2025, most consumers prioritized ingredient transparency, with Gen Z and Millennials willing to pay premiums for clean-label products. Research in the International Journal of Environmental Research and Public Health linked artificial sweeteners to gut microbiome issues and nitrates/nitrites to colorectal cancer, increasing distrust of synthetic ingredients despite regulatory approval. In China's beverage market, reduced-sugar drinks gained popularity, "zero-sugar" searches surged on Meituan, and consumers paid more for eco-friendly packaging while tracking nutrition via QR codes. Reformulating products poses challenges, requiring natural alternatives like fruit and vegetable extracts, plant-based antioxidants, and fermentation-derived stabilizers, all while maintaining stability and shelf-life. These alternatives often increase costs and variability, creating technical and economic hurdles. While FDA guidelines affirm the safety of sweeteners like aspartame and sucralose, consumer perception pressures companies to act. Syrup producers face a strategic choice: invest in natural reformulations for clean-label demand or retain cost-effective synthetic formulations for price-sensitive markets, straining research and development resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Botanicals Disrupt Fruit Dominance

In 2025, fruits held a 34.59% share of the product-type market, highlighting their consumer appeal and versatility in beverages, bakery, and dairy. Herbs and botanicals are growing at a 7.48% CAGR through 2031, driven by wellness trends and premiumization. Botanical syrups like lavender honey, hibiscus, and orange blossom are emerging as "Future Flavors" in US and Asia-Pacific beverages, offering low-sugar alternatives. Chocolate syrups remain stable in mature markets but face reformulation as cocoa prices stabilize. London cocoa futures dropped 11% in September 2025 due to improved West African weather and Ecuador's expansion, leading to a 308,000 metric ton surplus for 2025/26, easing raw material costs[3]Source: International Cocoa Organization, "Cocoa Prices", icco.org. Coffee syrups are gaining traction with cold-brew innovations; in spring 2026, Starbucks launched Iced Ube Coconut Macchiato, while Dunkin' introduced a Banana Cold Foam line, signaling major-chain adoption of coffee-compatible flavors.

Other flavors, including malt, vanilla, almond, and coconut, form a fragmented but vital segment. Madagascar vanilla prices reached USD 450-620 per kilogram in early 2026 as yields dropped from 220 kg/ha in 2019 to 98 kg/ha in 2026 due to cyclones and labor shortages. EU Regulation 2024/1211 mandates blockchain traceability, adding USD 18-25 per kilogram in compliance costs. Suppliers are blending origins and investing in direct farm relationships to secure supply and reduce premiums. Coconut syrups are growing in dairy-free and Southeast Asian iced coffee formats, optimized for plant-based matrices. Almond syrups face competition from nut-based alternatives like pistachio and hazelnut, which are driving premiumization in European snacks and coffee. Kerry's 2026 Taste Charts highlighted Manchego and Pecorino as premiumization drivers, suggesting opportunities for nut-forward profiles. The product-type landscape is bifurcating into volume-driven fruit and chocolate segments and margin-rich botanical and specialty segments prioritizing traceability and functional claims.

By Application: Functional Foods Outpace Beverage Growth

In 2025, beverages held a 35.69% application market share, driven by RTD coffee, cold brew, specialty tea, and carbonated soft drinks. Functional foods are growing at a 6.97% CAGR through 2031, fueled by protein beverages, supplement bars, and wellness-focused dairy alternatives using flavor-masking syrups to counter bioactive off-notes. Sensient's BioSymphony platform reduces chalkiness in high-protein drinks, enhances vanilla and cocoa flavors, extends sweetener effects, and lowers alcohol burn in functional cocktails, positioning syrups as essential technologies. Givaudan's Zensera, a patent-pending lemon balm extract, supports cognitive performance under stress at 300 milligrams, offering good solubility and mild taste for beverages and nutraceuticals. Protein fortification is expanding into RTD coffee and flavored water, with high-protein beverages growing 22% among fitness consumers in Tier-1 Chinese cities, driving demand for syrups that mask amino-acid notes without adding sugar.

Bakery and confectionery applications remain stable but face margin pressures from clean-label reformulations. Dessert-inspired flavors like cookie dough, butter pecan, and cheesecake are boosting sales in cafés and QSRs, creating opportunities for syrup suppliers to develop indulgent bases for coffee, milkshakes, and frozen desserts. The dairy segment is evolving as plant-based alternatives like coconut, oat, and almond milk demand syrups optimized for non-dairy matrices to maintain stability and mouthfeel without dairy fat. Emerging opportunities in sauces, dressings, and savory applications highlight syrup versatility. Sensient's BioSymphony masks sourness in sauces, enhances tomato and umami flavors, and creates creamier textures in Alfredo dishes. The application landscape is shifting from beverage-centric volumes to functional and cross-category margins, rewarding suppliers investing in bioactive-compatible formulations and technical support.

By Distribution Channels: E-Commerce Disrupts B2B Dominance

In 2025, B2B/Foodservice held 55.72% of the distribution share, driven by strong ties with QSR chains, specialty cafés, and institutional buyers. B2C, however, is growing at 7.70% CAGR through 2031, supported by e-commerce, at-home mixology, and direct-to-consumer models. China's beverage sector reflects this shift, with niche beverage brands seeing a 50% rise in DTC sales on Tmall and live-streaming e-commerce generating RMB 12 billion (USD 1.7 billion) in 2023. Torani reported 20% annual growth over 34 years, adding USD 150 million in revenue in 2025 and expanding its workforce by 26%. The company aims for USD 1 billion in revenue by 2030. Subscription models and O2O beverage delivery are growing, while vending machines, expanding at 15% CAGR through 2028, and convenience stores create new touchpoints for single-serve syrup formats.

Supermarkets and hypermarkets remain the largest B2C channels but are losing share to specialty stores and online platforms. Specialty stores cater to premiumization with artisanal syrups commanding higher margins, exemplified by Torani's Diamond Syrup, priced at USD 11.99 and sold exclusively on Torani.com and World Market. Online platforms enable direct consumer engagement, subscription models, and rapid SKU testing without slotting fees. In China, 58% of consumers track nutrition via QR codes, and 45% are willing to pay premiums for eco-friendly packaging, highlighting the role of transparency and sustainability in conversions. Urban centers see growth in convenience stores, vending machines, smart fridges, and subway retail, driven by impulse purchases. The distribution landscape is fragmenting, with B2B focusing on cost and consistency, while B2C emphasizes innovation, transparency, and brand storytelling, requiring distinct go-to-market strategies.

Geography Analysis

In 2025, North America leads the market with a 35.40% share, buoyed by its entrenched coffee culture, a well-established foodservice infrastructure, and consumers' readiness to pay a premium for tailored flavor experiences. Canada and Mexico bolster the region's growth, thanks to their expanding foodservice sectors and robust cross-border trade ties. Additionally, efforts to harmonize regulations are smoothing the path for established players to access the market.

Key European markets, including Germany, France, the UK, the Netherlands, Belgium, and Poland, are reaping the benefits of their expansive food industries. Growing health consciousness among consumers is fueling the demand for clean-label products. With a heightened focus on sustainability, manufacturers showcasing environmental responsibility find ample opportunities. Trends like a preference for locally sourced ingredients and a push to minimize packaging waste are shaping purchasing choices. A notable move in this landscape is Argos Wityu's acquisition of Groupe Routin, a premium syrup maker from France, underscoring the industry's tilt towards premium positioning and a focus on natural ingredients.

Asia-Pacific stands out as the region with the fastest growth rate, projected at a 7.58% CAGR from 2025 to 2030. This surge is largely attributed to a burgeoning middle class, a shift towards Western beverage preferences, and swift urbanization. In China, the market is thriving on a surge in coffee consumption and the embrace of Western café culture. Meanwhile, Japan's established market is pioneering innovations in premium and functional beverage applications. The region's booming functional beverage sector, led by a surge in immune-support drinks, presents a golden opportunity for syrup producers. Trends in Australia reveal a shift: 79% of consumers are cutting back on meat, and there's a rising fascination with Southeast Asian flavors. This evolution leans towards plant-based preferences and a taste for exotic flavors. Meanwhile, South America, the Middle East, and Africa are emerging as regions of interest, each charting its own growth path, shaped by economic progress, urbanization, and a warming up to Western beverage styles.

Competitive Landscape

The flavored syrups market showcases a balanced competition. This indicates a tug-of-war between established multinationals and niche regional players. Recent moves, like Glanbia's USD 300 million takeover of Flavor Producers and Tate & Lyle's eyeing of CP Kelco with a proposed USD 1.8 billion deal, spotlight strategic trends. Players are leaning into vertical integration, carving out premium market positions, and emphasizing natural ingredients. Companies are also differentiating through innovation. For instance, Givaudan, with a reported USD 9.30 billion in 2024 sales, attributes its success to robust research and development and collaborative customer engagements. Meanwhile, DSM-Firmenich is channeling merger-derived synergies, aiming for an annual USD 409.98 million boost to fuel its innovation drive.

There's a budding interest in functional applications and sustainable sourcing. Monin's 74-acre biodynamic yuzu orchard is a testament to vertical integration, ensuring top-notch ingredients while championing sustainability. Tech is reshaping the landscape, with AI at the helm for flavor crafting and streamlining operations. Notably, 40% of consumers now prioritize taste in vegan offerings, and there's a 23% uptick in product launches spotlighting 'fantasy' flavors. These trends highlight the growing importance of aligning product development with evolving consumer preferences and sustainability narratives.

New-age disruptors are carving niches via direct-to-consumer models and tailored experiences. In contrast, industry stalwarts are leveraging their scale and regulatory know-how to fortify their market positions, creating hurdles for smaller entrants. As the competitive terrain shifts, the winners will be those who adeptly juggle innovation with operational savvy, all while steering through supply chain challenges and regulatory mazes. Companies that can balance these factors effectively are likely to maintain a competitive edge in the evolving flavored syrups market.

Flavored Syrups Industry Leaders

-

Monin Inc.

-

Torani Co.

-

Maison Routin 1883

-

Sensient Technologies Corp.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Eggo launched a line of syrups in five different options, including original, buttery, blueberry, sweet and spicy, and cinnamon with application capabilities in a wide range of food products. The company launched these syrups in collaboration with syrup supremo Golding.

- June 2025: Food Service India Pvt Ltd (FSIPL), a prominent player in India's B2B food solutions market, launched a new range of syrups through its brand Marimbula: Jallab, Aam Panna, and Kala Katta. These new syrups are designed to enhance FSIPL's seasonal offerings for hotels, restaurants, cafés, and cloud kitchens nationwide.

- March 2025: Monin Americas, a frontrunner in premium flavor solutions, has introduced its newest creation: Yuzu Pineapple Syrup. Crafted from fruits cultivated by Monin, this syrup melds the distinctive tart and floral notes of yuzu with the sweet and tangy essence of pineapple. The result is a premium tropical flavor, perfect for enhancing cocktails, teas, and culinary dishes.

Global Flavored Syrups Market Report Scope

Flavored syrups are concentrated, viscous liquid additives composed of a simple syrup base, typically sugar or sugar substitutes dissolved in water, infused with natural or artificial flavoring agents. The flavored syrups market is segmented by product type, application, distribution channel, and geography. By product type, the market is segmented into fruits, chocolate, herbs and botanicals, coffee, and others. By application, the market is segmented into beverages, bakery and confectionery, dairy products, functional foods, and others. By distribution channels, the market is segmented into B2B/Foodservice and B2C. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. Market Forecasts are Provided in Terms of Value (USD and Volume (Liters).

| Fruits |

| Chocolate |

| Herbs and Botanicals |

| Coffee |

| Others (Malt, Vanilla, Almond, Coconut) |

| Beverages |

| Bakery and Confectionery |

| Dairy Products |

| Functional Foods |

| Others |

| B2B/Foodservice | |

| B2C | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Channels | |

| Other Distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Fruits | |

| Chocolate | ||

| Herbs and Botanicals | ||

| Coffee | ||

| Others (Malt, Vanilla, Almond, Coconut) | ||

| Application | Beverages | |

| Bakery and Confectionery | ||

| Dairy Products | ||

| Functional Foods | ||

| Others | ||

| Distribution Channels | B2B/Foodservice | |

| B2C | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Channels | ||

| Other Distribution channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the flavored syrups market in 2026?

The flavored syrups market size stands at USD 67.61 billion in 2026.

Which product category holds the highest share?

Fruit-based syrups lead with 34.59% flavored syrups market share in 2025.

What region is growing fastest?

Asia-Pacific is expected to log a 7.58% CAGR between 2026 and 2031.

Which application segment shows the strongest future growth?

Functional foods are projected to expand at 6.97% CAGR through 2031.

Page last updated on: