Loan Servicing Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

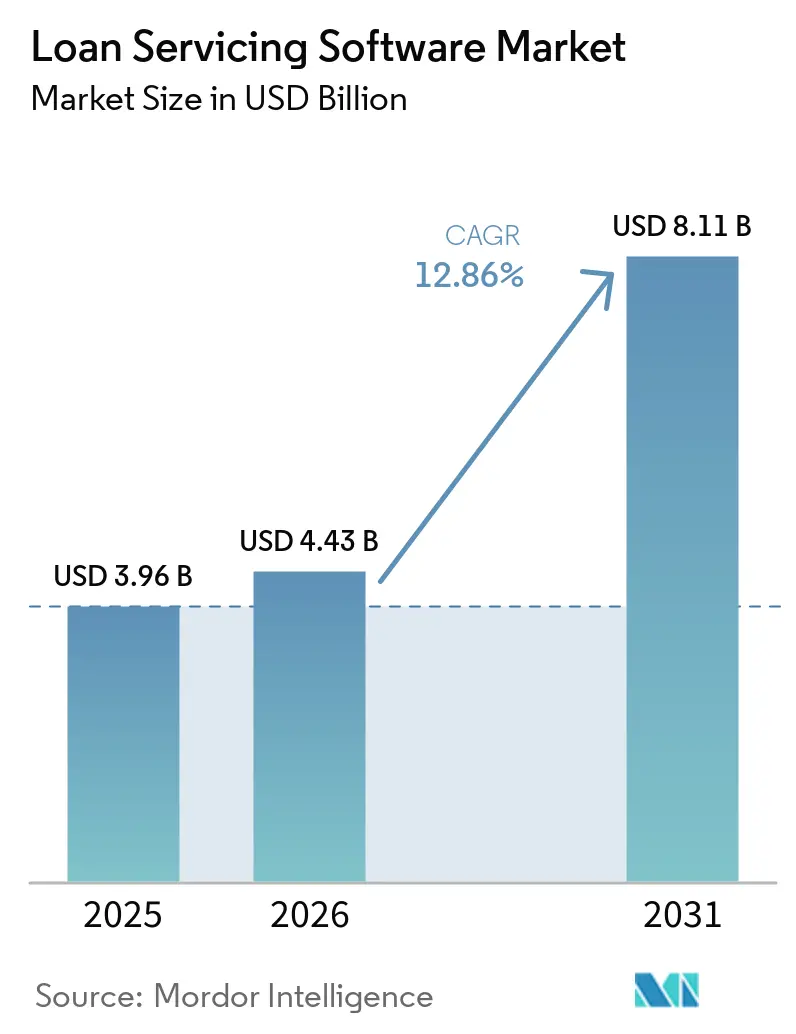

| Market Size (2026) | USD 4.43 Billion |

| Market Size (2031) | USD 8.11 Billion |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Loan Servicing Software Market Analysis by Mordor Intelligence

The loan servicing software market size is expected to increase from USD 3.96 billion in 2025 to USD 4.43 billion in 2026 and reach USD 8.11 billion by 2031, growing at a CAGR of 12.86% over 2026-2031. This expansion reflects rising pressure on lenders and servicers to automate post-origination work such as payment processing, escrow management, investor reporting, delinquency handling, and loss mitigation, while also keeping pace with a compliance framework that has become broader and more detailed. The loan servicing software market is also being driven by replacement demand rather than just first-time software spending, as institutions move away from legacy platforms that cannot support real-time reporting, stronger audit trails, and modern integration requirements. Borrower expectations are reinforcing that shift, as mobile-first service, faster response times, and self-service workflows now shape platform selection alongside efficiency and compliance. Competitive activity remains active as vendors differentiate through cloud-native design, AI governance controls, and stronger real-time data architecture, while expanded service accountability for technology-enabled decisions raises the value of platforms that can produce audit-ready documentation. The result is a loan servicing software market in which regulatory pressure, operating efficiency, and borrower experience are pointing buyers toward the same modernization path.

Key Report Takeaways

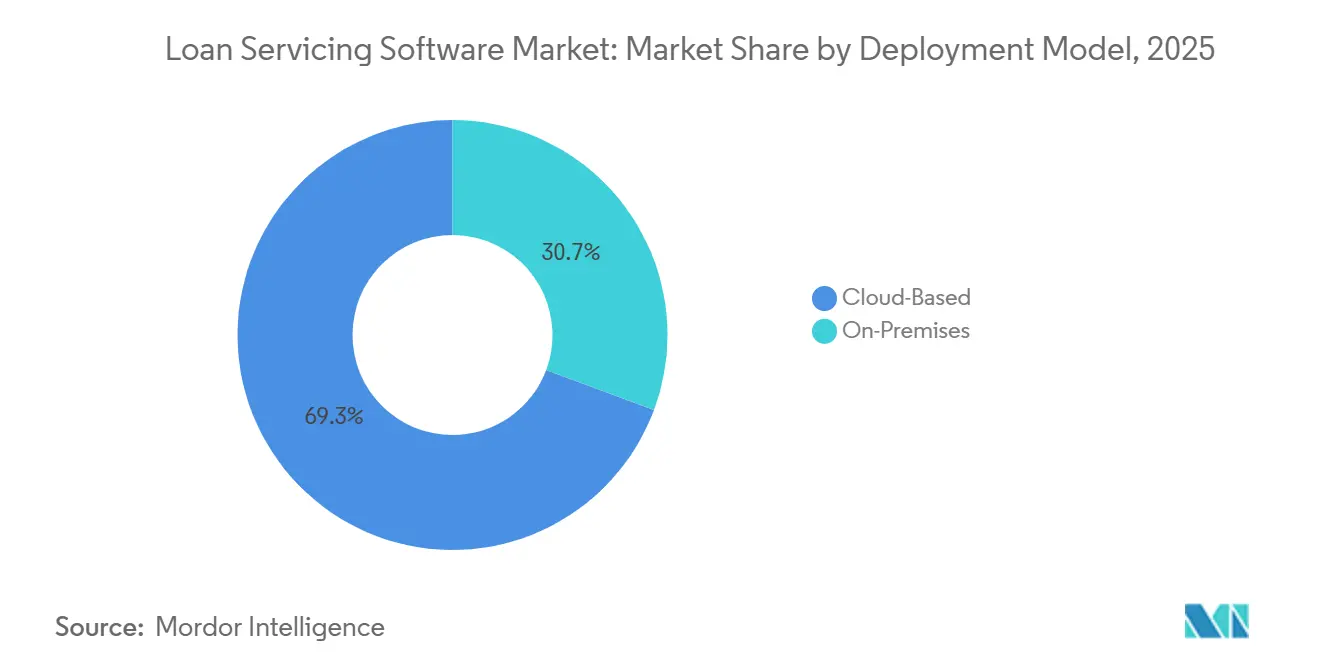

- By deployment model, cloud-based platforms held 69.32% share of the loan servicing software market in 2025, and this same segment is projected to expand at a 13.26% CAGR through 2031.

- By loan type, mortgage loans led with 41.84% share in 2025, while commercial loans are projected to expand at a 14.06% CAGR through 2031.

- By end user, banks held 38.73% share in 2025, while non-bank financial institutions and fintech lenders are projected to grow at a 13.84% CAGR through 2031.

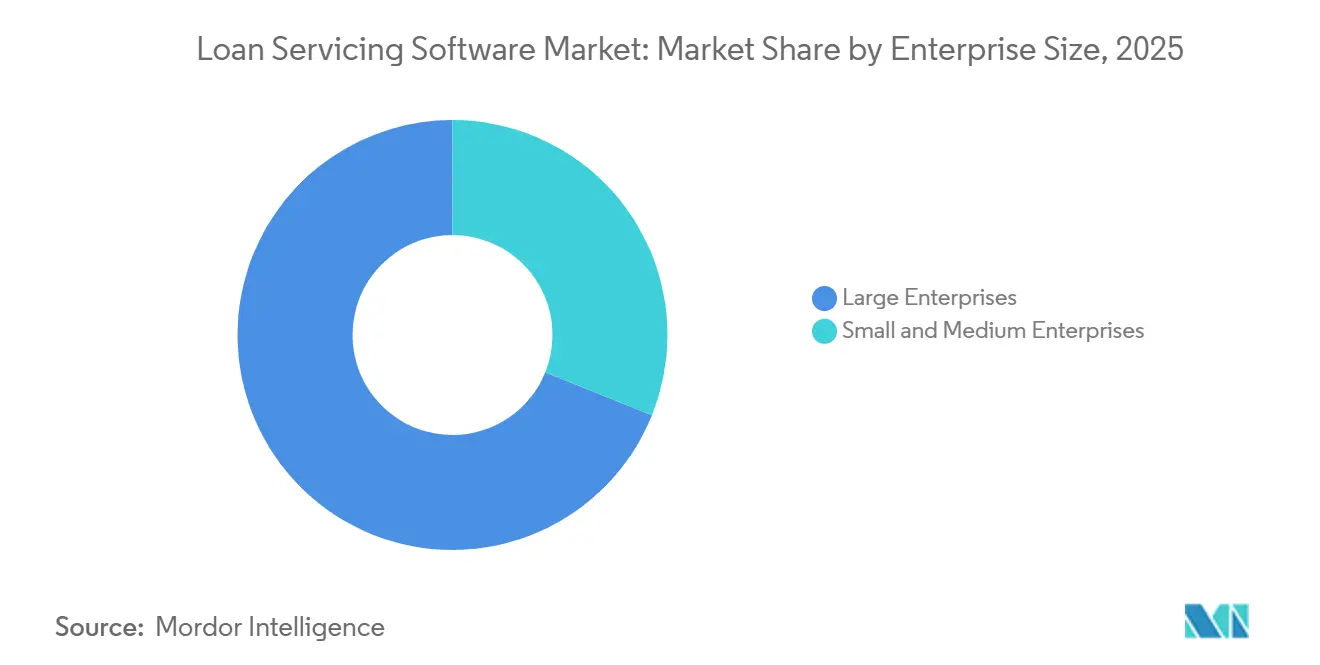

- By enterprise size, large enterprises accounted for 68.91% of the market share in 2025, while SMEs are projected to expand at a 13.21% CAGR through 2031.

- By functionality, payment and collection management accounted for 36.32% share of the loan servicing software market size in 2025, while customer self-service and engagement is projected to expand at a 14.01% CAGR through 2031.

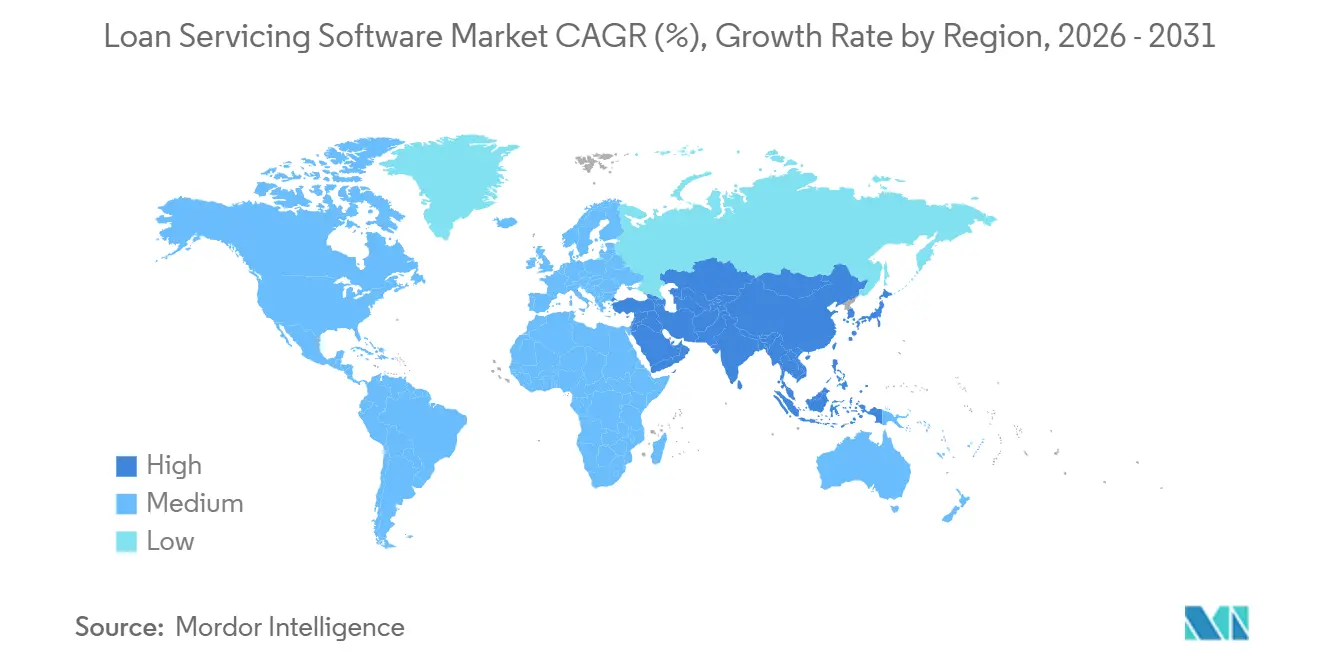

- By geography, North America accounted for 39.74% share of the loan servicing software market size in 2025, while Asia-Pacific is projected to expand at a 13.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Loan Servicing Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation of Complex Post-Origination Workflows | +2.8% | Global, with concentrated demand in North America and Europe | Short term (≤ 2 years) |

| Cloud Migration Across Lenders and Servicers | +2.2% | North America, Europe, and Asia-Pacific core, with spill-over to Middle East and Africa | Medium term (2-4 years) |

| Borrower Demand for Digital Self-Service | +1.6% | Global, with early adoption leadership in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising Regulatory and Audit Burden | +1.3% | North America and Europe, expanding to Australia and India | Medium term (2-4 years) |

| GSE API Mandates for Default and Escrow Reporting | +0.9% | United States primarily, with secondary effect on lenders servicing US-originated loans | Short term (≤ 2 years) |

| AI-Governed Servicing for Government and Distressed Loans | +0.7% | United States and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Automation of Complex Post-Origination Workflows

Automation of complex post-origination workflows remains a primary demand driver in the loan servicing software market, as servicing operations still involve a large number of repetitive, yet tightly regulated, actions across payments, escrow, delinquency, investor reporting, and lien administration. Many of these events are structured and recurring, yet they still consume significant staff time when managed through fragmented systems, manual review queues, and disconnected communication tools. Shaw Systems said in March 2026 that loan servicing platforms are moving from systems of record toward systems of intelligence and orchestration, where AI agents handle first-pass analysis, highlight risks, and prepare communication drafts for human teams to review and finalize. In 2024, Infinite Computer Solutions reported that a large US mortgage fintech reduced delinquency mitigation processing time by 33%, lowered effort by 60%, and automatically processed 98% of borrower payments after modernizing its cloud-native platform across more than 200 business functions. When policy rules are embedded directly into workflow triggers, automation also becomes a compliance control that reduces variation in servicing treatment, improves audit consistency, and lowers the operational burden of proving that required actions were completed in the correct sequence.

Cloud Migration Across Lenders and Servicers

Cloud migration across lenders and servicers is another major growth driver in the loan servicing software market, as institutions now view hosted delivery as a way to improve regulatory responsiveness and operating efficiency. The move is being accelerated by reporting timelines and update cycles that are harder to sustain in heavily customized on-premises environments, especially when institutions rely on manual patching and isolated infrastructure teams. Fannie Mae's LL-2025-02 introduced event-based reporting requirements that require key loan-level servicing events to be reported the same day they are processed and no later than 3:00 a.m. ET on the next business day. Finastra said in 2025 that migration of its LaserPro platform to the cloud delivered a 50-65% reduction in total cost of ownership and a 15-20% improvement in staff productivity by reducing infrastructure overhead and enabling automated update deployment. Cloud environments also make it easier to standardize on encrypted audit trails, security controls, and recurring regulatory updates, which is why modernization roadmaps are translating into multi-year procurement activity rather than one-time replacement projects. As a result, the loan servicing software market continues to benefit from a replacement cycle in which cloud delivery has become the preferred operating model for both scale and compliance.

Borrower Demand for Digital Self-Service

Borrower demand for digital self-service is changing product priorities across the loan servicing software market because customer expectations are now shaped by real-time, mobile-first financial experiences rather than branch or call-center norms. Servicers that cannot support fast account access, simple payment paths, and clear issue resolution face higher service costs and weaker customer retention, even when their underlying servicing controls remain compliant. ACI Worldwide reported that mobile bill payment preference reached 26% in 2024, up from 11% in 2019, while Gen Z preference rose to 47%, which shows how quickly borrower interaction habits are shifting toward handheld and self-directed channels. Tavant said in February 2026 that its TOUCHLESS Servicing Portal was achieving over 80% deflection of routine servicing inquiries in live deployments, providing lenders with a direct, measurable operating case for borrower-facing automation. This matters because self-service is no longer just a convenience layer on top of core servicing; it is becoming part of the core economics of servicing through lower contact-center load, faster issue resolution, and more consistent communication workflows. That is why the loan servicing software market is increasingly rewarding vendors that embed digital engagement into the platform architecture rather than treating it as a portal extension.

Rising Regulatory and Audit Burden

The rising regulatory and audit burden continues to support spending in the loan servicing software market, as servicers are being pushed toward systems that can deliver faster reporting, stronger controls, and clearer documentation under changing rule sets. The challenge is not only the number of requirements, but also the timing, granularity, and traceability now expected across payment events, escrow changes, delinquency movement, and foreclosure workflows. Fannie Mae's LL-2025-02 requires loan-level events such as payments, curtailments, delinquency status changes, and escrow adjustments to be reported on the same day they are processed, with foreclosure events due by the next business day after processing. Sagent said in March 2026 that its Dara platform uses continuous AI scanning of CFPB, Fannie Mae, Freddie Mac, and FHA rule changes to compress regulatory review cycles from weeks to hours, illustrating how compliance work is increasingly being built into the servicing architecture rather than managed outside it.[1]Sagent, “Land Home Financial Services Will Deploy Dara by Sagent to Modernize End-to-End Mortgage Servicing,” Sagent, sagent.com The American Bankers Association stated in May 2026 that mortgage regulatory reform and technology investment should move in tandem, which reinforces the case for configurable platforms that can absorb ongoing change rather than assuming rule intensity will decline. The loan servicing software market, therefore, continues to gain support from compliance pressure, as institutions increasingly see technology replacement as the practical path to keeping pace with regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Core Integration Complexity | -1.4% | Global, with acute impact in North America and Europe where mainframe-era cores remain in active use | Long term (≥ 4 years) |

| High Implementation and Change-Management Costs | -1.0% | Global, with disproportionate impact on community banks, credit unions, and SME-segment lenders | Medium term (2-4 years) |

| AI Governance Liability Shifting to Servicers | -0.7% | United States, Europe | Short term (≤ 2 years) |

| Open-Source and Low-Code Substitution Pressure | -0.5% | North America, Europe, and Asia-Pacific among fintech lenders and digitally mature credit unions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Core Integration Complexity

Legacy core integration complexity remains the most entrenched restraint on the loan servicing software market because many institutions still run servicing operations through long-standing core systems, custom interfaces, and historical data structures that are difficult to unwind cleanly. The challenge goes well beyond system connectivity, since a platform change often requires rebuilding data flows across credit bureaus, custodians, payment processors, escrow processes, and investor reporting layers that were not designed for real-time coordination. This makes modernization slower and more expensive because servicers are not only replacing software but also reworking the surrounding architecture that supports compliant day-to-day servicing. Finastra said in 2025 that architectural reconfiguration is a foundational part of modernization, and that simply moving old structures into a cloud wrapper can preserve the same operating constraints that institutions were trying to remove.[2]Julian Lee, “Finastra's Lending Cloud Service Supporting the Digital Transformation of the Global Corporate Banking Sector,” Finastra, finastra.com LendFoundry noted in 2026 that portfolio migrations require at least three months of prior bureau report alignment before a new servicing system can generate compliant forward-looking reports, which extends the effective switching cost well beyond licensing and deployment fees alone. This long migration runway slows replacement decisions across the loan servicing software market, even when servicers accept that their legacy environment is no longer fit for future requirements.

High Implementation and Change-Management Costs

High implementation and change-management costs remain a significant drag on the loan servicing software market because platform replacements affect both budget planning and ongoing operating capacity. User input indicates that implementation can range from USD 500,000 to USD 2 million for mid-sized servicers, while full deployment can take 6-12 months, even at institutions with dedicated project resources and active modernization plans. The financial burden is only part of the issue, since servicing teams must retrain staff, validate migrated loan data, test compliance workflows, and maintain service quality on live portfolios during transition. In January 2026, Biz2X reported that Central Pacific Bank expanded its partnership for SMB lending automation, demonstrating how modular SaaS models are beginning to lower adoption barriers for smaller institutions that cannot support enterprise-scale rollouts. Even with that progress, community banks, credit unions, and smaller lenders still face a sharper cost-to-value decision because they need better servicing control without the disruption of long transformation programs. Vendors that can reduce deployment time, training effort, and internal process strain will therefore be better placed to capture the next wave of SME demand in the loan servicing software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Architecture Becomes The Compliance Baseline

Cloud-based platforms held 69.32% of the loan servicing software market share in 2025, indicating that new deployments and renewal decisions have shifted strongly toward hosted environments. The segment leads because cloud delivery fits the current need for faster regulatory updates, stronger audit trails, and easier integration with modern servicing workflows. It also supports real-time processing more effectively than heavily customized on-premises environments that were designed around delayed or batch-oriented operating cycles. Fannie Mae's event-based reporting timetable has raised the cost of keeping older servicing stacks aligned with current operational expectations, especially where same-day data movement is required across multiple servicing events. In the loan servicing software industry, deployment choice has therefore moved beyond infrastructure preference and become part of a broader governance and reporting decision.

On-premises systems remain relevant for institutions with data sovereignty constraints, internal hosting requirements, or legacy integration systems that are too costly to unwind quickly. Some government-linked entities, internationally active institutions, and long-established commercial banks still fit this profile because they must balance modernization with internal control and migration risk. Finastra said in 2025 that fully managed cloud platforms automate regulatory update deployments on bi-weekly cycles, reducing maintenance drag and shortening the lag between rule changes and software responses. SAP Fioneer reported in April 2026 that its cloud-native mortgage servicing platform reduced the full-time equivalents needed to process loans by 88% and cut manual data handling by 80%, highlighting the productivity gap between newer architectures and manual-heavy legacy environments. Those differences suggest cloud will keep widening its lead across the loan servicing software market as compliance pressure and operating cost discipline continue to shape buying decisions.

By Loan Type: Mortgage Workflows Lead While Commercial Use Cases Accelerate

Mortgage loans held 41.84% of the loan servicing software market in 2025, and that lead came from the structural complexity of residential servicing rather than simple loan volume alone. Mortgage servicing requires escrow reconciliation, investor reporting, delinquency management, loss mitigation evaluation, and strict communication sequencing, all of which create sustained demand for purpose-built systems with robust documentation and deep control. These workflows are difficult to manage accurately on fragmented platforms because even routine servicing actions can have downstream implications for borrowers, investors, and compliance teams. Commercial loans are projected to expand at a 14.06% CAGR through 2031, making them the fastest-growing loan type in the loan servicing software market. Growth in this category is being supported by lenders that need better control over covenant tracking, borrowing base calculations, and syndicated servicing administration, areas where spreadsheet-led processes are becoming harder to justify.

Consumer, auto, and student loan portfolios each add their own servicing needs, especially around payment cadence, hardship handling, and borrower communication patterns. ACI Worldwide said mobile bill payment preference rose to 26% in 2024 from 11% in 2019, while Gen Z preference reached 47%, which supports continued investment in mobile-first servicing experiences across retail loan categories. The loan servicing software industry is therefore expanding across both high-complexity mortgage operations and faster-moving consumer credit use cases that demand a different style of interaction and workflow design. Vendors that can support multiple loan categories on a common architecture will be better positioned as institutions seek to reduce system fragmentation and manage multiple post-close processes on a single operating base.

By End User: Banks Anchor Current Spending While Fintechs Push Platform Design

Banks held 38.73% of the loan servicing software market in 2025, reflecting their broader product portfolios, larger modernization budgets, and stronger capacity to support complex implementation programs. Their lead also reflects the fact that service quality is closely aligned with core operating performance for large banking institutions, as it affects compliance, cost-per-loan, borrower retention, and investor reporting. In April 2025, United Wholesale Mortgage selected ICE Mortgage Technology's MSP loan servicing system and related digital servicing modules to support its in-house servicing strategy, which illustrates the scale of procurement that keeps large institutional buyers central to category revenue. Large bank and mortgage servicing buyers also shape vendor road maps because they demand stronger APIs, better loss mitigation tools, and more formal governance documentation. That keeps banks important to the loan servicing software market even as other customer groups influence where the next wave of innovation goes.

Non-bank financial institutions and fintech lenders are projected to grow at a 13.84% CAGR through 2031, which makes them the fastest-growing end-user group in the loan servicing software market. These buyers often prefer API-first and composable architectures because they want more freedom to design borrower journeys, connect third-party tools, and avoid the operational rigidity of traditional subservicing structures. Dark Matter said in February 2026 that its Elevate servicing platform gained new signings and deeper integration with the Empower origination system, underscoring how end-to-end workflow continuity remains a strong purchase theme for lenders seeking tighter control of the handoff from origination to servicing. This means banks continue to anchor present revenue, while fintech and non-bank customers increasingly influence the feature direction and architectural priorities of the loan servicing software market.

By Enterprise Size: Large Institutions Dominate While SMEs Open A Wider Buying Base

Large enterprises commanded 68.91% of the loan servicing software market in 2025 because their operating scale, product diversity, and compliance exposure favor established enterprise platforms with deeper governance and integration support. These institutions also have more capacity to absorb long implementation cycles, large migration programs, and the internal testing effort required to modernize live servicing operations without disrupting customer service. For many of them, servicing technology is treated as infrastructure rather than a departmental tool because servicing performance affects funding, customer outcomes, audit quality, and operational costs simultaneously. That has helped preserve a solid enterprise revenue base even as vendor selection criteria become more demanding and more tied to AI governance and real-time data architecture. The size and complexity of enterprise programs also make them the most likely to test advanced servicing automation within formal control frameworks before wider rollout.

SMEs are projected to grow at a 13.21% CAGR through 2031, underscoring how SaaS delivery is widening access to capabilities once concentrated among the largest institutions. LoanPro said its platform serves more than 600 financial organizations, including community banks, credit unions, and fintechs, and that WaFd Bank removed 39 manual servicing steps through modernization on the platform. That example shows why smaller institutions are becoming more active buyers, as they can now target workflow automation and service control without incurring the same capital burden as older enterprise deployments. As this buyer base expands, the loan servicing software market is becoming less dependent on only the largest institutions, even though enterprise customers still dominate current spending and procurement size.

By Functionality: Self-Service Engagement Outgrows Traditional Servicing Modules

Payment and collection management accounted for a 36.32% share of the loan servicing software market in 2025, reflecting the central role of payment accuracy in the economics and compliance profile of servicing. This function touches every active account and has direct consequences for borrower treatment, investor reporting, and regulatory complaint risk, which is why it continues to hold the largest share of functionality. It also remains a part of servicing where breakdowns become most visible, since errors in payment allocation or collection handling can immediately affect both customer experience and operational control. Customer self-service and engagement are projected to expand at a 14.01% CAGR through 2031, which makes it the fastest-growing functionality segment in the loan servicing software market. That growth signals that borrower-facing tools are now being valued not only for convenience, but also for measurable operating efficiency and more consistent interaction management.

Tavant said in February 2026 that its TOUCHLESS Servicing Portal was supporting more than 400,000 borrowers and deflecting over 80% of routine servicing inquiries in live deployments, which gives clear weight to the economic case for self-service. Goal Solutions said in March 2026 that Simplify 2.0 delivered 60% faster response times and client-specific policy isolation for support teams, demonstrating how workflow support and decision guidance are converging. These launches show that payment operations, compliance monitoring, analytics, and borrower interaction are increasingly converging into connected intelligence layers instead of remaining in separate tools. That shift should keep self-service and decision support near the center of competitive differentiation as the loan servicing software market continues to evolve.

Geography Analysis

North America held 39.74% of the loan servicing software market share in 2025, which makes it the largest regional segment in the current revenue mix. The region led because the United States has a dense base of regulated mortgage servicers and a compliance-led replacement cycle shaped by GSE reporting, audit, and governance expectations. Fannie Mae's LL-2025-02 set same-day and next-business-day reporting expectations for key servicing events, which continues to support platform replacement across US servicers that cannot meet those timelines with legacy batch environments. Canada remains a smaller but relevant secondary market as lenders and credit unions modernize older systems under stronger technology resilience expectations and broader digital transformation programs. Europe also remains an established part of the loan servicing software market, led by the United Kingdom, Germany, and France, where data accuracy, auditability, and multi-product lending support continue to shape platform selection, and Finastra highlighted this direction in its 2025 lending cloud work with European corporate banking institutions.

Asia-Pacific is projected to expand at a 13.72% CAGR through 2031, making it the fastest-growing regional segment in the loan servicing software market. India stands out because digital lending rules and the expansion of the NBFC base are pushing more lenders toward standardized servicing platforms rather than spreadsheet-led, manually coordinated post-close processes. China, Japan, and South Korea also support regional growth through modernization programs that focus on stronger data quality, better control depth, and more unified post-merger or multi-entity servicing environments. ACI Worldwide said 88% of global digital lending transactions were initiated on mobile devices in 2025, reinforcing the mobile-first servicing design logic that has become especially evident among Asia-Pacific lenders.[3]Darcy Locke, “2025 Auto Lending Trends Mobile Payments and Self-Service Revolutionize Customer Experiences,” ACI Worldwide, aciworldwide.com

South America, the Middle East, and Africa remain early-stage regions in the loan servicing software market, but they are becoming more relevant as financial inclusion programs, fintech expansion, and digital infrastructure investments drive new demand for post-close systems. Brazil leads South America because open finance standards encourage API-based architectures that align more naturally with modern servicing platforms than older siloed systems. The Middle East is also gaining traction through banking digitization programs, and Biz2X said in February 2026 that Deem Finance partnered with it to support the expansion of embedded finance for SMEs in the UAE, underscoring regional demand for composable, data-driven lending infrastructure. Africa remains at an earlier adoption stage, with demand centered on mobile-first lenders and microfinance institutions that need lightweight, cloud-hosted servicing tools rather than long, costly enterprise implementations.

Competitive Landscape

The loan servicing software market remains moderately fragmented in 2026, with several scaled platform vendors competing alongside a longer tail of specialized or regionally focused providers across mortgage, consumer, and commercial servicing use cases. Competitive positioning is moving away from broad feature counts toward governance controls, real-time data handling, integration depth, and implementation speed, as these factors now matter more directly to both compliance and borrower experience. Sagent has strengthened its position by building out the Dara suite around cloud-native, end-to-end mortgage servicing and continuous regulatory monitoring, which closely aligns with the current preference for platforms that combine workflow automation with audit readiness. ICE Mortgage Technology reinforced its scale in April 2025 when United Wholesale Mortgage selected MSP and related digital servicing modules for its in-house servicing strategy, showing that established vendors still benefit when large lenders want proven servicing depth and broad module coverage. The loan servicing software market, therefore, continues to reward vendors that can combine operational depth with stronger control documentation rather than relying solely on feature breadth.

Newer challengers are trying to win on architecture rather than size, which keeps the loan servicing software market dynamic even without a single dominant vendor setting the rules for the entire category. LoanPro said in October 2025 that its Model Context Protocol created a model-agnostic AI gateway with programmatic compliance guardrails and full audit trails for both AI and human actions, directly addressing the growing demand for accountable automation in servicing environments.[4]Jackson Stone, “LoanPro Unveils First-of-Its-Kind AI Gateway to Enable Safe, Compliant Agentic Loan Servicing,” LoanPro, loanpro.io Tavant also moved deeper into post-close servicing in February 2026 with its TOUCHLESS portal and MAYA agentic AI assistant, demonstrating how borrower engagement and servicing automation are converging within a single operating layer. Vendors that can tie AI features to audit-ready governance are likely to gain more attention as servicers become more cautious about accountability for automated decision support.

Another competitive theme is the effort to connect origination, servicing, analytics, and borrower support on a shared operating layer across the loan servicing software market. Dark Matter has emphasized tighter integration between Elevate and Empower, while Goal Solutions has focused on faster, policy-specific support workflows through Simplify 2.0, demonstrating that vendors are trying to reduce system handoffs and make servicing actions easier to control and document. This direction favors providers that can demonstrate live production performance and clear operating control,s rather than only product roadmaps. The open opportunity remains strongest among community banks, credit unions, and smaller lenders seeking modern servicing capabilities without the enterprise-scale costs, long deployment cycles, or heavy reliance on internal technology.

Loan Servicing Software Industry Leaders

Financial Industry Computer Systems, Inc.

Nortridge Software, LLC

Shaw Systems Associates, LLC

LoanPro Software, LLC

The Mortgage Office

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Carrington Mortgage Services announced a partnership with Valon Technologies to adopt ValonOS as its core servicing platform and to acquire Valon Mortgage, adding approximately 800,000 loans with an unpaid principal balance of approximately USD 197 billion to Carrington's portfolio. The transaction positions ValonOS as the AI-native infrastructure for Ginnie Mae loan modernization, with Valon pivoting entirely to a servicing software and infrastructure company.

- March 2026: Sagent announced that Land Home Financial Services will deploy the full Dara platform suite, including Dara Core, Dara Consumer, Dara Default, Dara Analytics, Dara Claims, Dara Invoice, and AI Docs, to modernize its end-to-end mortgage servicing operations. Dara is described as the industry's first cloud-native, real-time, end-to-end mortgage servicing platform with open API connectivity.

- March 2026: Concord, a credit administration and software provider, acquired Finley Technologies, whose Credit Management System automates borrowing base calculations, covenant compliance monitoring, and portfolio analytics for credit facilities and warehouse lines. The combined entity now administers more than USD 60 billion in assets and supports over 5 million accounts.

- February 2026: Tavant launched its TOUCHLESS Servicing Portal with the MAYA agentic AI assistant, extending its platform from loan origination to post-close servicing. The portal supports over 400,000 borrowers nationwide and achieves over 80% deflection of routine servicing inquiries in current live deployments, with 24/7 AI-assisted self-service and built-in compliance controls.

Global Loan Servicing Software Market Report Scope

The Loan Servicing Software Market comprises software platforms and digital solutions that automate, manage, and optimize loan administration throughout the lifecycle after origination. These solutions enable financial institutions, lenders, and loan servicers to handle key servicing activities, including payment processing, escrow management, interest calculation, collections, delinquency management, customer communications, regulatory compliance, reporting, and portfolio analytics. Loan servicing software improves operational efficiency, reduces manual errors, enhances borrower experience, and supports compliance with evolving regulatory requirements.

The Loan Servicing Software Market Report is Segmented by Deployment Model (Cloud-Based, and On-Premises), Loan Type (Mortgage Loans, Consumer Loans, Commercial Loans, Auto Loans, Student Loans, and Other Loan Types), End User (Banks, Credit Unions, Mortgage Lenders and Servicers, Non-Bank Financial Institutions and Fintech Lenders, and Other End-Users), Enterprise Size (Large, and Small and Medium-Sized Enterprises), Functionality (Payment and Collection Management, Loan Management, Compliance and Risk Management, Reporting and Analytics, Customer Self-Service and Engagement, and Other Functionalities), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premises |

| Mortgage Loans |

| Consumer Loans |

| Commercial Loans |

| Auto Loans |

| Student Loans |

| Other Loan Types |

| Banks |

| Credit Unions |

| Mortgage Lenders and Servicers |

| Non-Bank Financial Institutions and Fintech Lenders |

| Other End Users |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Payment and Collection Management |

| Loan Management |

| Compliance and Risk Management |

| Reporting and Analytics |

| Customer Self-Service and Engagement |

| Other Functionalities |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| By Loan Type | Mortgage Loans | |

| Consumer Loans | ||

| Commercial Loans | ||

| Auto Loans | ||

| Student Loans | ||

| Other Loan Types | ||

| By End User | Banks | |

| Credit Unions | ||

| Mortgage Lenders and Servicers | ||

| Non-Bank Financial Institutions and Fintech Lenders | ||

| Other End Users | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Functionality | Payment and Collection Management | |

| Loan Management | ||

| Compliance and Risk Management | ||

| Reporting and Analytics | ||

| Customer Self-Service and Engagement | ||

| Other Functionalities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the loan servicing software market and what is the growth outlook?

The loan servicing software market was valued at USD 3.96 billion in 2025, stands at USD 4.43 billion in 2026, and is projected to reach USD 8.11 billion by 2031 at a 12.86% CAGR.

Why is cloud adoption rising so quickly in loan servicing platforms?

Cloud-based deployment held 69.32% share in 2025 and is projected to grow at a 13.26% CAGR because it supports faster updates, better auditability, and easier real-time reporting.

Which loan category creates the most software demand today?

Mortgage loans led with 41.84% share in 2025 because escrow reconciliation, investor reporting, delinquency management, and loss mitigation create high servicing complexity.

Which customer group is growing fastest among software buyers?

Non-bank financial institutions and fintech lenders are the fastest-growing end users with a projected 13.84% CAGR through 2031, driven by preference for API-first and composable platforms.

What functionality is expanding fastest in servicing platforms?

Customer self-service and engagement is projected to grow at a 14.01% CAGR, helped by live examples such as Tavant's portal, which reported over 80% deflection of routine inquiries.

Which region leads current demand and which region grows fastest?

North America led with 39.74% share in 2025, while Asia-Pacific is projected to expand at a 13.72% CAGR through 2031 as digital lending infrastructure and mobile-first servicing models deepen.

Page last updated on: