United States Core Banking Software Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

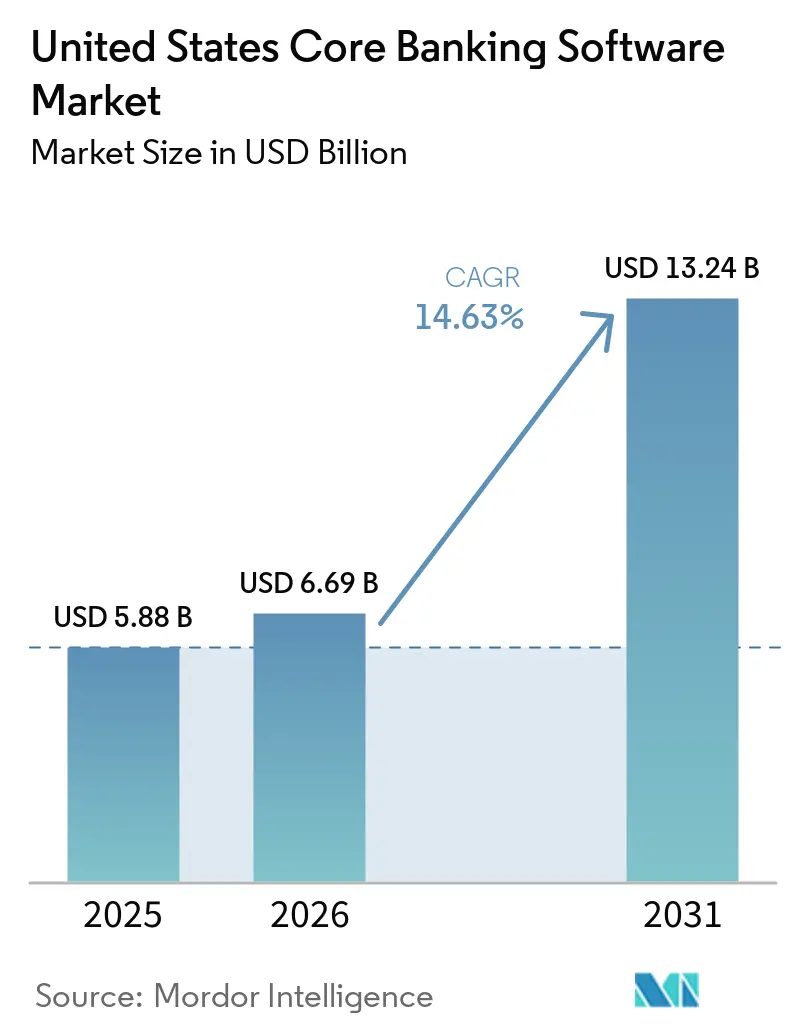

| Base Year Market Size (2025) | USD 5.88 Billion |

| Market Size (2026) | USD 6.69 Billion |

| Market Size (2031) | USD 13.24 Billion |

| Growth Rate (2026 - 2031) | 14.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Core Banking Software Market Analysis by Mordor Intelligence

The United States core banking software market size was valued at USD 5.88 billion in 2025 and estimated to grow from USD 6.69 billion in 2026 to reach USD 13.24 billion by 2031, at a CAGR of 14.63% during the forecast period 2026-2031. The growth path reflects a structural replacement cycle rather than a routine wave of feature upgrades, because many institutions are now reaching the limit of what legacy core extensions can support. FedNow enrollment growth and the retirement of COBOL-era talent are tightening the decision window for banks that had delayed full core replacement for years. Real-time payment volumes moving through FedNow and The Clearing House RTP network are also exposing the limits of batch-based processing, which was not built for continuous event-driven settlement at this scale. Demand is concentrating in large financial centers and in mid-market community banking corridors at the same time, which is creating different spending patterns by institution size and operating model. Vendor competition is therefore being shaped by both architecture depth and delivery confidence, with incumbents defending installed relationships while cloud-native providers target new builds, sponsor-bank programs, and institutions ready for full modernization.

Key Report Takeaways

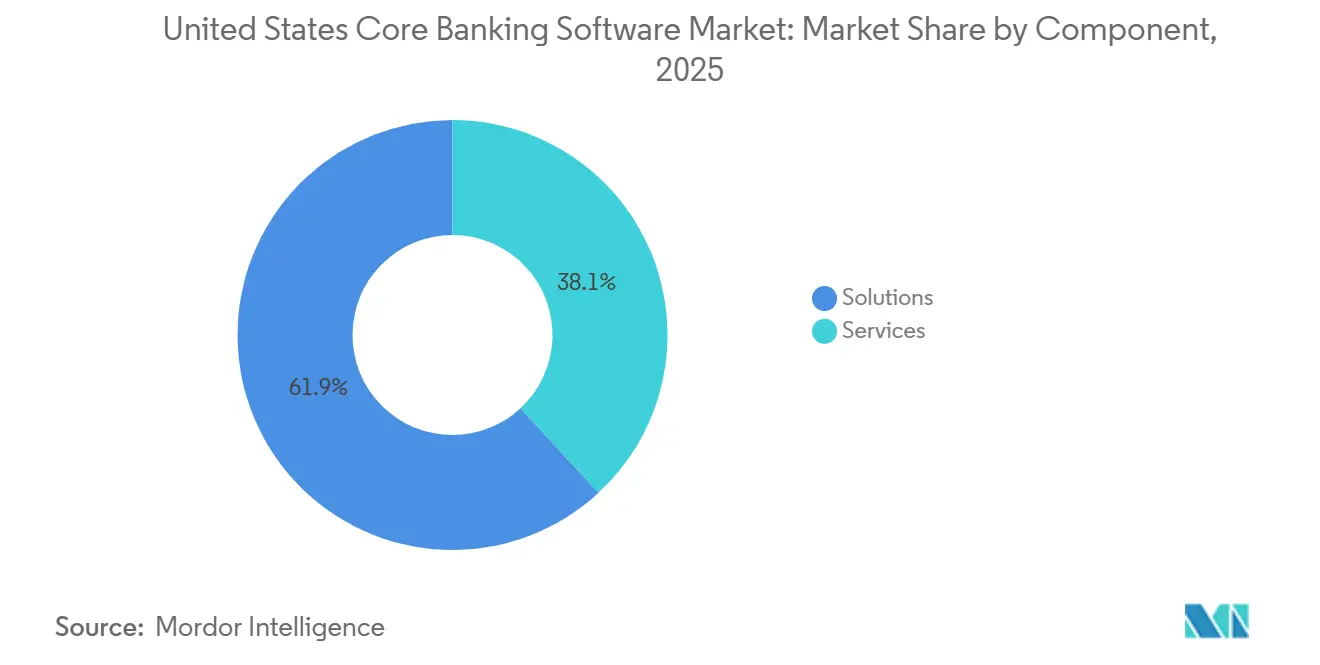

- By component, solutions held a 61.89% share of the United States core banking software market in 2025, while services are projected to expand at a 14.98% CAGR through 2031.

- By deployment mode, cloud accounted for a 57.11% share of the United States core banking software market in 2025 and also remained the fastest-growing deployment model in the US core banking software market.

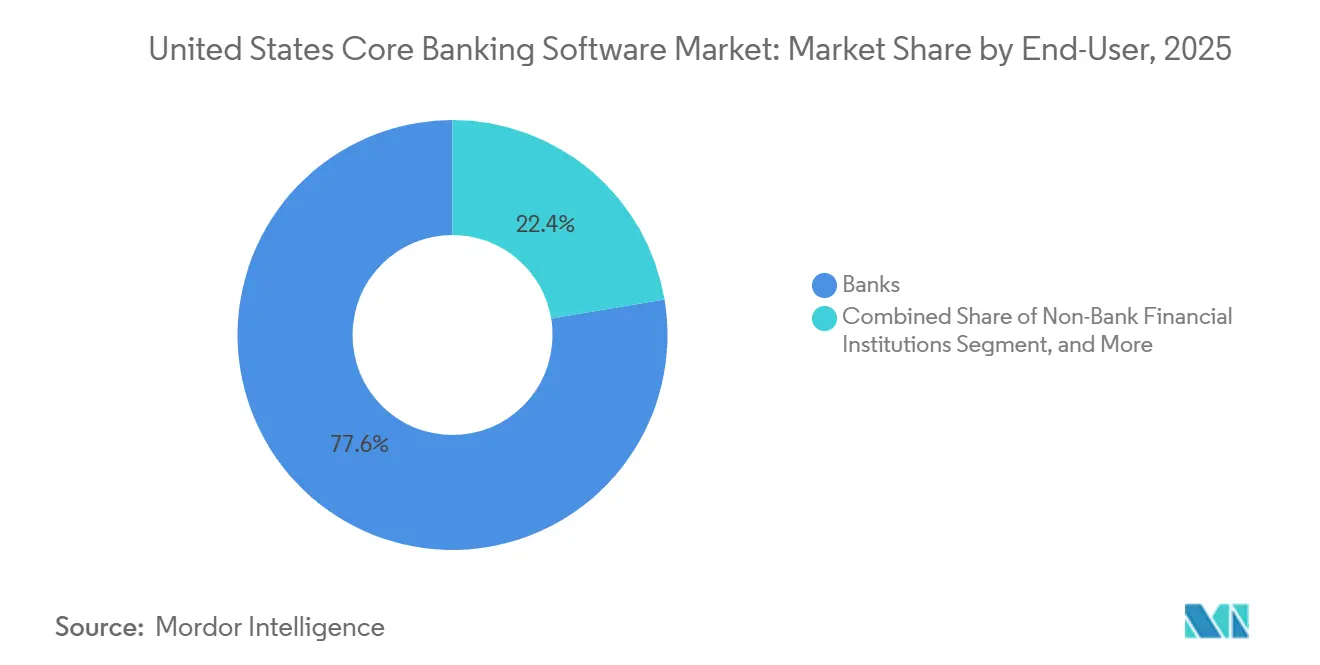

- By end-user, banks held the largest share in 2025, while non-bank financial institutions are projected to grow at a 15.68% CAGR through 2031 in the US core banking software market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Core Banking Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Native Migration Lowering Cost And Release Cycles | +3.2% | National, with concentrated activity in Northeast financial hubs and Southeast community banking corridors | Short term (≤ 2 years) |

| FedNow And RTP Adoption Driving Real-Time Core Upgrades | +2.8% | National, strongest in mid-tier regional banks with USD 1 billion to USD 50 billion in assets across all 50 states | Short term (≤ 2 years) |

| Agentic AI Programs Requiring Event-Driven Core Data | +2.4% | National, with early concentration at large commercial banks and sponsor-bank programs in the Northeast and Southeast | Medium term (2-4 years) |

| Mainframe Talent Attrition Accelerating Core Renewal | +2.1% | National, most acute at community banks in the Midwest and smaller regional banks with limited IT scale | Medium term (2-4 years) |

| Open Banking And API Ecosystem Expansion | +1.6% | National, with early compliance pressure on the largest banks and spillover to mid-tier institutions | Medium term (2-4 years) |

| Sponsor-Bank Program Controls Pulling Payments Closer To The Core | +1.1% | National, concentrated in institutions running banking-as-a-service programs, especially in the Southeast and West Coast fintech corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Migration Lowering Cost And Release Cycles

Cloud-native architectures are reducing release cycles from quarters to weeks, and that speed gap is turning into a commercial disadvantage for banks still running monolithic cores. U.S. Bank expanded its collaboration with AWS in May 2026 across payment processing, wealth management, and commercial banking applications that support approximately 1.4 million businesses, showing that modernization now spans mission-critical workloads rather than side systems.[1]Amazon Web Services, “U.S. Bank Expands Collaboration With AWS to Accelerate Progressive Technology Transformation and AI-Driven Customer Experience Innovation,” AWS Press Center, press.aboutamazon.com PeoplesBank completed its move to a modern cloud-native core in September 2025, finished a day ahead of schedule, and re-enrolled more than 19,000 customers in online banking within 24 hours, which gave community institutions a live example of low-disruption conversion execution. These cases show that cloud migration is no longer limited to pilot programs, because both national and community institutions are using it to reset operating models and delivery timelines. Consumption-based infrastructure also changes the cost equation by reducing the fixed overprovisioning that sat inside long-lived mainframe environments. In the United States core banking software market, that combination of faster releases and cleaner cost visibility is making migration timing part of competitive planning rather than a back-office technology decision.

FedNow And RTP Adoption Driving Real-Time Core Upgrades

Real-time payment growth is moving faster than many replacement budgets expected, and the gap between receiving transactions and sending them in real time is exposing weaknesses in batch-oriented core designs. FedNow processed more than USD 850 billion in 2025 and the network had reached around 1,700 financial institutions by April 2026, which shows how quickly the operating baseline has shifted for banks of different sizes. The RTP network also raised its transaction cap from USD 1 million to USD 10 million in February 2025, widening commercial and treasury use cases that require immediate ledger visibility and faster reconciliation. Metropolitan Commercial Bank completed the retirement of its legacy ACH mainframe in February 2026 and moved to Finzly's cloud-native, API-first payment platform, which showed that full decommission is possible and that hybrid workarounds are not the only path. As instant payment throughput rises, banks that still rely on batch-ledger updates face rising operating strain in payments, exception handling, and customer-facing service response. In the US core banking software market, the market keeps real-time readiness tied closely to core replacement timing rather than to standalone payments upgrades.

Agentic AI Programs Requiring Event-Driven Core Data

Agentic AI depends on current and accessible ledger data, and that requirement is changing the business case for modernization at large commercial banks and platform-led institutions. Fiserv launched agentOS in May 2026 with OpenAI and AWS Bedrock so financial institutions could run AI agents natively across core, payments, issuer processing, and servicing workflows, including production use cases at First Interstate Bank and Boulder Dam Credit Union.[2]Fiserv, Inc. and Amazon Web Services, “Fiserv Launches agentOS, The Operating System for Agentic AI in Banking,” AWS Press Center, press.aboutamazon.com Oracle Financial Services extended its Agentic AI Platform to corporate banking in April 2026 with pre-built agents across treasury, trade finance, credit, and lending, which shows that AI enablement is moving directly into banking workflow design rather than staying at the edge.[3]Oracle, “Oracle Financial Services Extends Agentic AI Platform to Corporate Banking,” Oracle, oracle.com These releases matter because AI agents cannot act safely on stale batch data when tasks involve onboarding, fraud review, AML triage, or report generation. Banks with API-first cores are better positioned to deploy those capabilities at scale, while banks wrapping older systems in middleware face a larger data freshness and control challenge. The United States core banking software market is therefore starting to separate providers that built real-time data access into the platform from those still treating it as an add-on layer.

Mainframe Talent Attrition Accelerating Core Renewal

COBOL talent scarcity has moved from a planning issue into an operating issue, because the same teams maintaining legacy systems are also needed to support migration design and cutover preparation. A late-2025 survey found that 71% of mainframe teams at financial institutions were understaffed and 54% were underfunded, which shows that legacy support capacity is already thinning inside the sector. That shortage matters because old core environments usually depend on undocumented business logic, exception handling rules, and data transformations that only a small number of experienced staff still understand. When those people retire or move, banks lose the internal knowledge needed to document interfaces, validate historical data behavior, and stage a safe cutover. The staffing issue also raises the cost of delay, because waiting does not preserve optionality when the pool of legacy expertise keeps shrinking. In the US core banking software market, core renewal is turning from a strategic choice into an operational necessity for many community and regional institutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Conversion Risk And Legacy Integration Complexity At Regional Banks | -2.3% | National, sharpest at mid-tier regional banks in the Midwest and Southeast with complex multi-core environments | Long term (≥ 4 years) |

| Vendor Lock-In And Long Renewal Cycles Slowing Switching | -1.5% | National, concentrated at community banks with limited IT procurement leverage | Medium term (2-4 years) |

| Third-Party And Fourth-Party Scrutiny Raising Due-Diligence Burden | -1.0% | National, most pronounced for sponsor banks operating banking-as-a-service programs in all regions | Short term (≤ 2 years) |

| Cyber-Resilience And Severe-Outage Recovery Requirements Increasing Migration Scope | -0.8% | National, with heightened examiner focus on institutions with more than USD 100 billion in assets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Conversion Risk And Legacy Integration Complexity At Regional Banks

Conversion risk is most acute at regional institutions in the USD 1 billion to USD 50 billion asset range, where operating complexity is high but IT scale is still limited. A 2025 industry survey found that 35% of banks were dissatisfied with their core processor and 19% were likely to convert at the next renewal date, which shows that demand to switch exists even when execution remains difficult. The challenge usually sits beyond the core itself, because banks often have to remap 30 to 50 or more ancillary systems across payments, treasury, compliance, cards, and digital channels before a cutover can happen. Legacy environments also carry years of undocumented data transformations, and those issues often appear late in validation when timelines are already tight. Longer parallel runs can reduce operational risk, but they also increase program cost, control overhead, and internal fatigue during migration. In the United States core banking software market, that keeps many regional banks cautious even when the long-term case for modernization is already clear.

Vendor Lock-In And Long Renewal Cycles Slowing Switching

Vendor lock-in remains a material brake on switching because many US core contracts run for 7 to 10 years and carry high exit friction. Deconversion fees, data migration work, staff retraining, and dual-running expenses can make the economics of a move difficult to justify inside a single budget cycle. That slows access to newer capabilities such as native real-time payment orchestration, open API exposure, and AI-ready workflow tools when they are not available on the incumbent platform. It also weakens buyer leverage during renewal discussions, especially for community institutions that have small procurement teams and fewer integration alternatives. Every extended contract term widens the gap between institutions that modernize earlier and those that keep layering fixes onto older platforms. This leaves part of the US core banking software market moving on a slower clock even as the demand signal for core replacement keeps strengthening.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals An Execution Economy

Solutions held 61.89% of the United States core banking software market share in 2025, which kept software subscriptions and platform licenses as the largest revenue base for vendors and buyers. Within the US core banking software market size outlook, services are projected to expand at a 14.98% CAGR through 2026-2031, which makes delivery work the faster-growing revenue stream. This mix shows that banks still commit large budgets to the platform itself, but they increasingly need outside help to execute conversion, integration, testing, and control design safely. The demand pressure does not come from one workstream alone, because API exposure, data mapping, payments integration, and compliance preparation often run together during the same replacement program. As a result, implementation capacity has become a constraint that shapes deal timing, vendor selection, and migration sequencing across the US core banking software market.

The services layer is also becoming more recurring as vendors and partners add managed migration, cloud operations, and AI workflow support around the core. That shift improves the economics of service delivery because the relationship continues after go-live instead of ending once the platform is installed. It also changes how buyers assess vendor quality, since delivery depth now affects not only speed but also operating stability and examination readiness. In the United States core banking software industry, certified platform expertise is becoming more valuable because institutions want fewer handoffs across separate advisory, integration, and operations teams. This leaves services positioned as the segment that absorbs the execution demands created by modernization, even while solutions remain the larger base of spending.

By Deployment Mode: Cloud Leads With Architecture Depth

Cloud accounted for 57.11% of the United States core banking software market share in 2025 and also carried the fastest growth profile among deployment modes. That lead reflects architectural fit as much as hosting cost, because real-time payments and agent-based workflows depend on event-driven ledgers and fast core data access. The May 2026 partnership between Thought Machine and US Senate Federal Credit Union illustrated this standard with Vault Core and Vault Payments deployed as one integrated real-time stack built around ISO 20022-native rails. In practice, buyers are separating true cloud-native systems from older applications that were only lifted onto remote infrastructure without redesign. That distinction matters because it changes configuration flexibility, release speed, data availability, and the amount of middleware needed to support new product or payment use cases.

On-premises deployments still retained a meaningful role at larger institutions with bespoke recovery, data control, and supervisory requirements in 2025. Hybrid models continued to work as transition paths when banks wanted new digital or payments modules in the cloud while keeping the core ledger on-site during the parallel-run period. Even so, partial migration does not fully solve the architectural gap that appears when instant settlement and AI use cases require consistent, low-latency data from the ledger. In the US core banking software industry, deployment choice increasingly signals how far a bank is willing to redesign operations rather than simply where it hosts applications. This keeps cloud at the center of new buying activity in the US core banking software market, while on-premises and hybrid remain important mainly for staged replacement strategies.

By End-User: Non-Bank Financial Institutions Drive Structural Expansion

Banks represented the largest end-user base in 2025, while non-bank financial institutions are projected to expand at a 15.68% CAGR through 2026-2031. Within the United States core banking software market size outlook, the growth rate shows demand is broadening beyond traditional chartered banks and into platform-led financial models. Sponsor-bank programs, fintech lenders, payments firms, and embedded finance operators now need ledger, payments, and compliance capabilities that older point solutions cannot provide in an integrated way. The April 2025 consent action against Community Federal Savings Bank highlighted how control gaps in sponsor-bank models can pull payment oversight back toward the core system and away from fragmented peripheral tools. This makes core selection more important for institutions that support partner ecosystems, because the ledger increasingly sits at the center of control design, exception management, and audit evidence.

Other end-users, including fintechs and payment institutions, are also raising demand for core-adjacent infrastructure that can support multi-rail settlement, faster onboarding, and program-level controls. Thread Bank's August 2025 decision to use Finxact from Fiserv with Infinant's Interlace Platform showed how embedded banking programs can scale on a modern core without forcing a full retail platform reset. That model is drawing attention because it gives community institutions a route into program banking revenue while preserving existing customer-facing business lines. In the US core banking software industry, this widens the addressable customer base beyond banks replacing aging processors on renewal cycles. It also means the US core banking software market is gaining growth from new operating models, not only from incumbent bank modernization budgets.

Geography Analysis

The Northeast carried the highest concentration of enterprise spending in the US core banking software market in 2025 because it houses many of the largest US bank headquarters and technology decision centers. New York, Boston, and Philadelphia remain the main hubs for large commercial core discussions, especially where banks are balancing modernization with complex operating environments and large product sets. Large institutions in this corridor are moving on multi-cloud modernization paths, as shown by U.S. Bank's expanded AWS collaboration in May 2026 to migrate hundreds of mission-critical applications across core banking and adjacent functions. FedNow and RTP adoption have also raised the performance baseline in markets where larger institutions shape customer expectations and peer response times. This makes the Northeast the region where architecture depth, payment readiness, and vendor delivery quality are tested earliest.

The Southeast and Midwest represented the broadest pool of active replacement evaluations in the US core banking software market because community banks and credit unions are densely represented across both regions. Many of these institutions sit in the USD 250 million to USD 5 billion asset range, where lean IT teams make legacy upkeep harder to sustain alongside modernization planning. A late-2025 survey found that 71% of mainframe teams were understaffed, and that condition weighs heavily on smaller institutions trying to run old environments while preparing for migration. PeoplesBank's September 2025 conversion to the Nymbus cloud-native core has circulated as a live proof point that mid-sized institutions can complete cutovers without service interruption. These regions therefore show strong demand from institutions modernizing because of staffing limits and operating pressure rather than because of optional innovation budgets alone.

The West Coast showed the strongest pull from sponsor-bank programs, embedded finance operators, and digital-asset-adjacent institutions entering the United States core banking software market. These buyers usually need API-first, multi-rail, and real-time ledger capabilities from the start, which favors cloud-native providers over heavily customized legacy stacks. The USSFCU partnership with Thought Machine in May 2026 and Thread Bank's Finxact decision in August 2025 reflect the type of architecture now being evaluated for program banking and embedded finance expansion. Credit unions and fintech-facing institutions in this region are therefore widening the addressable demand base beyond traditional retail bank replacements.

Competitive Landscape

The United States core banking software market remained moderately concentrated in 2026, with Fiserv, FIS, and Jack Henry anchoring a large share of installed relationships across chartered institutions. That installed base continues to matter because conversion cost, integration depth, and operating familiarity make renewal decisions conservative even when dissatisfaction is visible. Cloud-native challengers such as Thought Machine, Mambu, Finxact, and Nymbus are still smaller, but they are winning a larger portion of greenfield deployments and sponsor-bank programs than their current scale alone would suggest. FIS reported 45% GAAP Banking Solutions revenue growth in Q1 2026, helped in part by acquired businesses, which showed that incumbent vendors still bring material financial strength to modernization cycles. The result is a market where incumbents defend scale while challengers compete on architecture, speed, and clearer modernization narratives.

Fiserv used product strategy to reinforce its position when it launched agentOS in May 2026 with OpenAI and AWS Bedrock for native deployment across core and payments workflows. FIS advanced a different agenda in April 2026 through Project Keystone, which it developed with 6 US financial institutions to support tokenized money movement on bank-controlled infrastructure. Thought Machine strengthened its US profile in May 2026 through the USSFCU replatforming project, which paired core and payments modernization in one program and highlighted the appeal of unified real-time architecture. Jack Henry also showed continued relevance with larger institutions in 2026 through its Woodforest National Bank core win, even as cloud-native vendors targeted fresh replacements. These moves show that product breadth alone is no longer enough, because vendors now need credible positions around AI readiness, real-time processing, and execution control.

The largest open opportunity remains the USD 1 billion to USD 50 billion asset band, where replacement need is clear but failed cutovers are hardest to absorb. Vendors that combine software with migration services, integration support, and managed controls are better aligned with how these institutions buy and how boards review execution risk. That is why the US core banking software market is separating more clearly between providers that rebuilt around APIs and those still depending on middleware wrapped around older cores. Competitive advantage is increasingly tied to proof of safe production cutovers, live real-time payment performance, and operational governance after conversion.

United States Core Banking Software Industry Leaders

Fiserv, Inc.

Jack Henry & Associates, Inc.

Fidelity National Information Services, Inc.

Computer Services, Inc.

Finastra Group Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Jack Henry and Associates announced Woodforest National Bank, with over USD 9 billion in assets and more than 740 branches across 17 states, selected its modern, integrated core platform, the largest new core signing in Jack Henry's history by number of accounts, marking a significant win among larger institutions.

- May 2026: Fiserv launched agentOS, an agentic AI operating system developed with OpenAI and AWS Bedrock, enabling financial institutions to deploy and scale AI agents natively across core, payments, issuer processing, and servicing workflows. 6 financial institutions co-developed the platform, with broad availability planned for August 2026.

- May 2026: U.S. Bank expanded its collaboration with AWS to migrate hundreds of mission-critical banking applications, including payment processing, wealth management, and commercial banking systems, in one of the largest banking modernization initiatives in the US financial sector.

- May 2026: Temenos announced new AI Agents, Copilots, and Conversational Studio capabilities embedded across its core and digital banking products at Temenos Community Forum 2026, building on its 2025 Copilot for Core launch, which enables natural-language interaction with core banking systems.

United States Core Banking Software Market Report Scope

The Core Banking Software Market in the United States refers to the market for banking platforms that manage a bank’s central operations, including deposits, loans, payments, account servicing, and transaction processing. It covers on-premises, cloud, and hybrid systems that help banks modernize legacy infrastructure, improve real-time processing, and support digital banking services.

The United States Core Banking Software Market Report is Segmented by Component (Solutions and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), and End-User (Banks, Non-Bank Financial Institutions, and Other End-users (FinTechs and Payment Institutions)). The market forecasts are provided in terms of value (USD).

| Solutions |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Banks |

| Non-Bank Financial Institutions |

| Other End-users (FinTechs, Payment Institutions) |

| By Component | Solutions |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By End-User | Banks |

| Non-Bank Financial Institutions | |

| Other End-users (FinTechs, Payment Institutions) |

Key Questions Answered in the Report

What is the current size and growth outlook for the United States core banking software?

The United States core banking software market was valued at USD 5.88 billion in 2025, is projected at USD 6.69 billion in 2026, and is forecast to reach USD 13.24 billion by 2031 at a 14.63% CAGR.

Why are banks replacing legacy core platforms now?

Real-time payments growth, cloud-native operating advantages, and the retirement of COBOL-era talent are making delay harder to justify for both large and mid-sized institutions.

Which deployment model leads adoption in the United States?

Cloud led with a 57.11% share in 2025 and was also the fastest-growing deployment mode, largely because it better supports real-time processing and AI-enabled workflows.

Which customer group is expanding fastest?

Non-bank financial institutions are projected to grow at a 15.68% CAGR through 2031 as sponsor-bank programs, fintech lenders, and payment firms require ledger and compliance capabilities.

Why are services growing faster than solutions?

Solutions remained larger with a 61.89% share in 2025, but services are growing faster at 14.98% CAGR because migration, integration, compliance, and managed support work are rising with each conversion program.

What makes vendor selection more difficult for regional banks?

Regional banks often face conversion risk across 30 to 50 or more ancillary systems, plus long contracts, data migration costs, and limited internal technical capacity during cutover planning.

Page last updated on: