LED Backlight Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

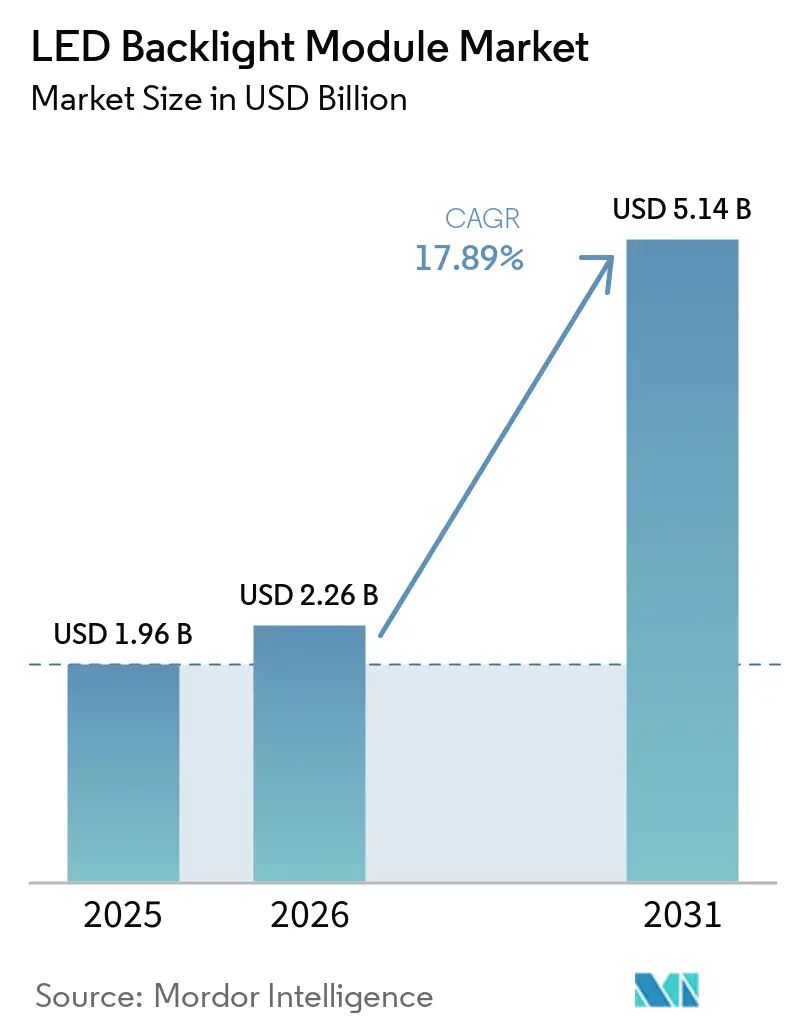

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 5.14 Billion |

| Growth Rate (2026 - 2031) | 17.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LED Backlight Module Market Analysis by Mordor Intelligence

The LED backlight module market size is expected to increase from USD 1.96 billion in 2025 to USD 2.26 billion in 2026 and reach USD 5.14 billion by 2031, growing at a CAGR of 17.89% over 2026-2031. Premium television brands are standardizing Mini-LED arrays with thousands of dimming zones to compete directly with OLED, while tier-1 automotive suppliers deploy 2,000-nit backlights that satisfy ISO 15008 legibility requirements. Localization incentives in China and India have begun to pull final assembly onshore, compressing lead times and insulating panel makers from tariff exposure. At the same time, energy-efficiency mandates in the United States and the European Union reward high-efficacy modules that integrate quantum-dot enhancement films. These converging forces support double-digit growth for the LED backlight module market even as OLED captures some flagship smartphone and tablet volumes.

Key Report Takeaways

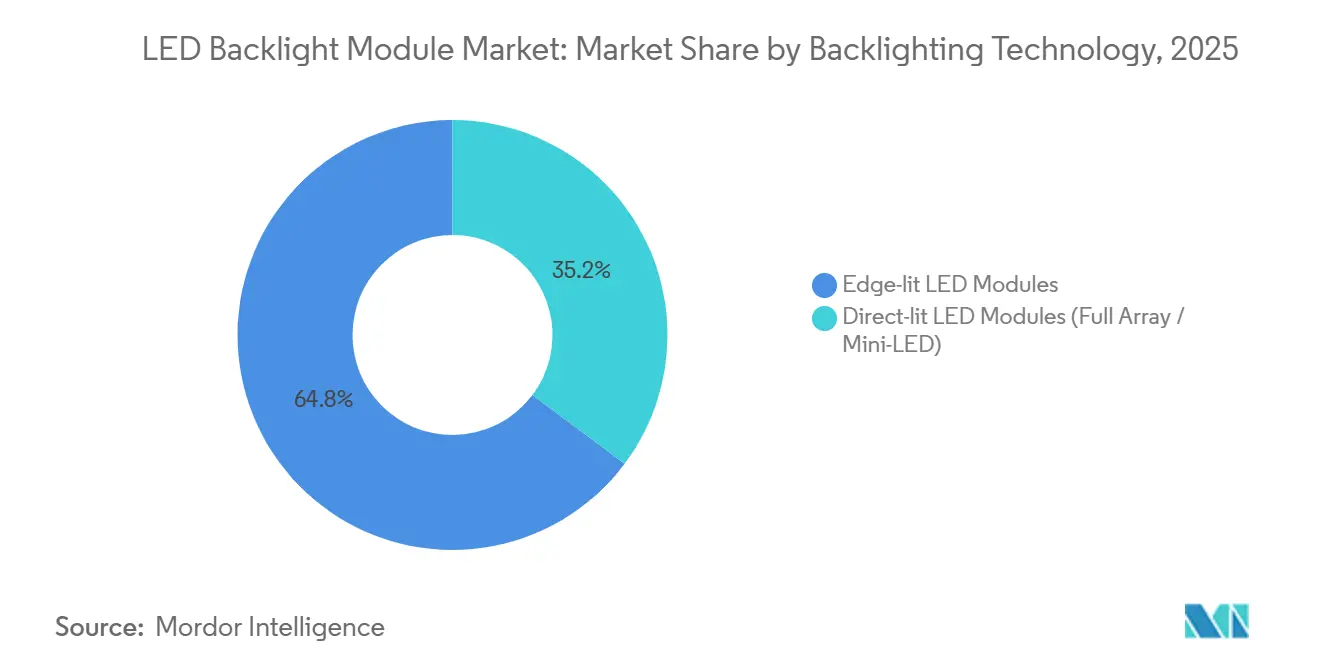

- By backlighting technology, edge-lit architectures led the LED backlight module market with 64.77% market share in 2025, whereas direct-lit Mini-LED solutions are projected to expand at an 18.23% CAGR through 2031.

- By panel size, large-size panels retained 44.94% of revenue in 2025, while medium-size panels are forecast to post the highest growth at an 18.55% CAGR over 2026-2031.

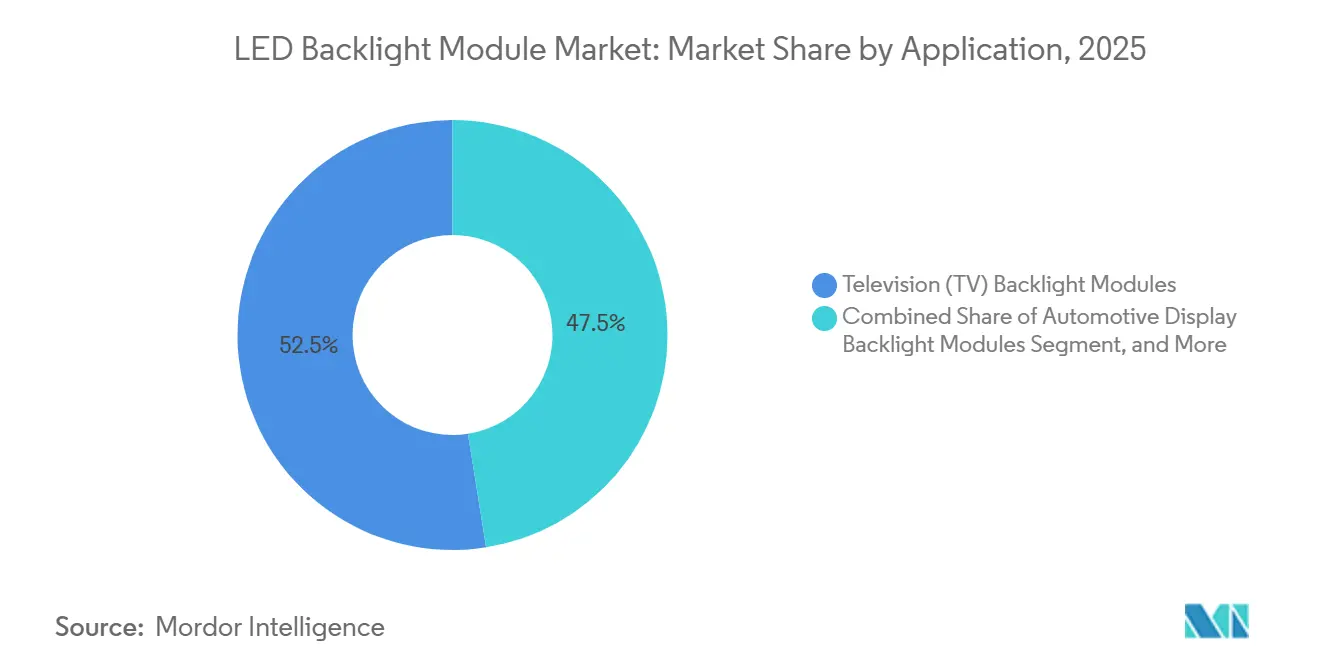

- By application, television retained 52.49% of revenue in 2025, while automotive displays are forecast to post the highest growth at an 18.43% CAGR over 2026-2031.

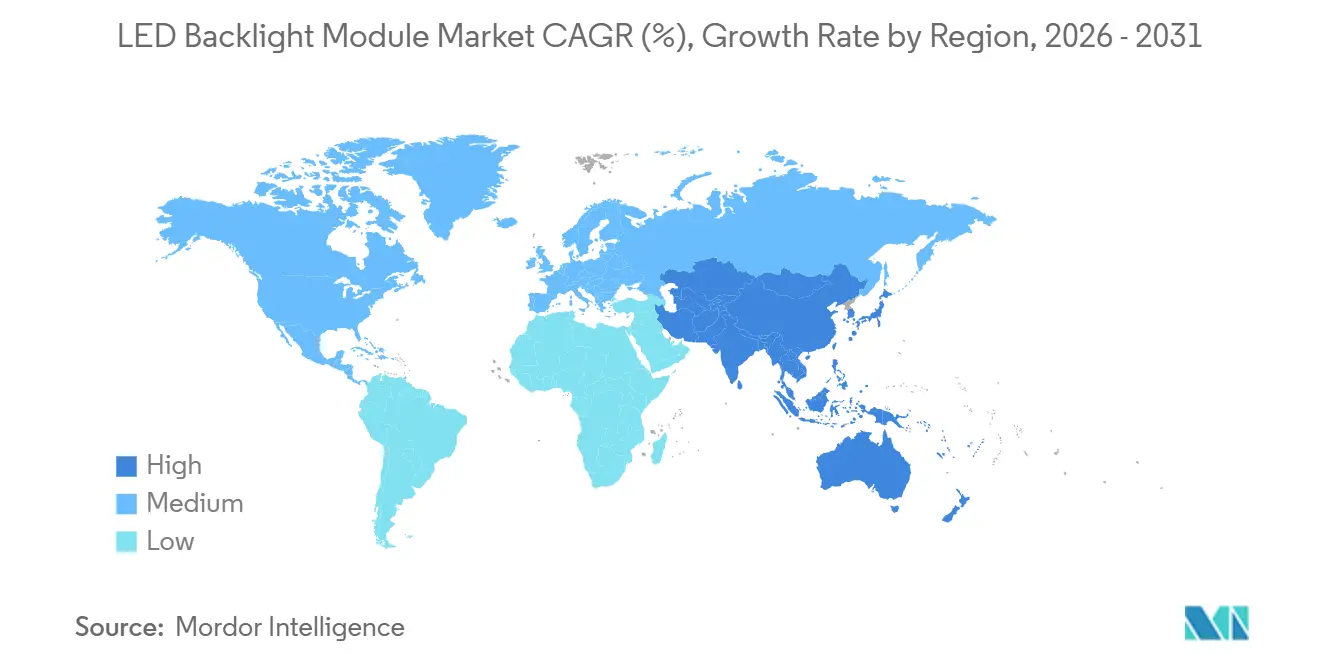

- By geography, Asia Pacific dominated with 67.82% revenue share in 2025 and is set to advance at an 18.35% CAGR, consolidating its leadership in the LED backlight module market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LED Backlight Module Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing Penetration of Mini-LED Backlighting in Premium TVs | +4.2% | Global (North America, Asia Pacific) | Medium term (2-4 years) |

| Rising Demand for High-Brightness Automotive Displays | +3.8% | North America, Europe, China | Medium term (2-4 years) |

| Supply-Chain Localisation Incentives in China and India | +3.1% | Asia Pacific | Long term (≥ 4 years) |

| Cost Advantages of Edge-Lit Architectures for Thin Notebooks | +2.9% | Asia Pacific, North America | Short term (≤ 2 years) |

| Energy-Efficiency Regulations Favouring LED Backlight Retrofits | +2.3% | North America, Europe | Medium term (2-4 years) |

| Integration of Quantum-Dot Enhancement Films in LCD Panels | +1.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of Mini-LED Backlighting in Premium TVs

Samsung’s Neo QLED and LG’s QNED lineups now ship with 1,000-plus dimming-zone Mini-LED modules that deliver peak brightness beyond 1,500 nits and 100% DCI-P3 gamut. Retail price compression 65-inch sets selling below USD 1,000 in North America broadens adoption beyond early enthusiasts. Each Mini-LED backlight employs 5,000-25,000 chips, driving demand for advanced driver ICs with per-zone pulse-width modulation.[1]BASF, “Quantum-Dot Enhancement Film Technology Brief,” basf.com The resulting bill-of-materials uplift underpins a multiyear revenue tailwind for direct-lit suppliers and accelerates the LED backlight module market’s migration toward premium configurations.

Rising Demand for High-Brightness Automotive Displays

Electric-vehicle cockpit redesigns mandate 2,000-3,000 nit backlights for daytime readability. HARMAN’s Ready Display platform integrates redundant LED strings and over 1,000 dimming zones to satisfy both ISO 15008 legibility and ISO 26262 functional-safety rules.[2]HARMAN International, “Mini-LED Cockpit Integration,” harman.com Automotive tiers now pay 10-15% module premiums for this capability, locking in multiyear design wins and lifting average selling prices across the LED backlight module market.

Supply-Chain Localization Incentives in China and India

China’s provincial subsidies and India’s Electronics Components and Semiconductors program exempt domestically integrated sub-assemblies from a 20% customs levy. BOE Technology Group Co., Ltd., Tianma Microelectronics Co., Ltd., and Radiant Opto-Electronics Corporation have responded with new capacity in China, Vietnam, and India, reinforcing Asia Pacific's position and ensuring long-term visibility for growth in the LED backlight module market.[3]Press Information Bureau, “Electronics Components and Semiconductors Scheme Details,” pib.gov.in This localization push is also improving supply chain resilience by reducing reliance on cross-border components and shortening OEM lead times. Additionally, it enables manufacturers to better align with regional demand cycles while benefiting from policy-driven cost efficiencies.

Cost Advantages of Edge-Lit Architectures for Thin Notebooks

Ultrabook chassis under 15 millimeters utilize perimeter-mounted LED strips, achieving uniform luminance with fewer chips. This innovation results in cost savings and extends battery life compared to direct-lit alternatives.[4]U.S. Department of Energy, “Final Rule for Television Efficiency,” energy.gov Although edge-lit architectures fall short of HDR performance standards, their cost-efficiency and compatibility with slim form factors make them a strong presence in price-sensitive notebook segments. This ongoing adoption not only ensures a steady volume demand for edge-lit configurations but also supports consistent production throughput, cementing their foundational role in the LED backlight module market throughout the forecast period.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Intensifying Competition from OLED and Micro-LED Displays | -2.7% | Global (Premium Segments) | Medium term (2-4 years) |

| IP Royalty Disputes Elevating BOM Costs | -1.9% | Asia Pacific Manufacturing Hubs | Short term (≤ 2 years) |

| Supply Volatility of High-Performance Phosphors | -1.4% | Global | Long term (≥ 4 years) |

| Environmental Scrutiny on Rare-Earth Extraction | -0.8% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from OLED and Micro-LED Displays

OLED panels dominate flagship smartphones and tablets priced above USD 800, displacing conventional backlights. Micro-LED pilots promise OLED-like contrast without organic degradation and could enter large-screen production once mass transfer yields stabilize. These self-emissive technologies siphon premium share, trimming the attainable ceiling for the LED backlight module market.

IP Royalty Disputes Elevating BOM Costs

IP royalty disputes are elevating BOM costs across the LED backlight module value chain. Settlements, such as those between Everlight Electronics Co., Ltd. and Seoul Semiconductor Co., Ltd., and ongoing litigation involving BOE Technology Group Co., Ltd. and Samsung Electronics Co., Ltd., underscore the complexity of royalty stacking tied to phosphor technologies and local-dimming algorithms. Each additional licensing layer can increase component costs, placing pressure on margins and raising barriers to entry. This environment challenges smaller manufacturers, limiting their ability to scale competitively within the LED backlight module market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Backlighting Technology: Mini-LED Direct-Lit Gains Momentum

Direct-lit Mini-LED modules are projected to post an 18.23% CAGR, reflecting rising adoption in televisions and gaming monitors. The LED backlight module market for edge-lit designs will expand more slowly, yet its lightweight profile and sub-USD 20 bill of materials keep it vital for notebooks and budget TVs. Manufacturers continue to refine dual-edge configurations and reflective cavities to defend share, but the contrast advantage of thousands of dimming zones positions Mini-LED as the long-term growth engine.

Production cost curves reinforce this split. Falling driver-IC prices and improved LED binning yields reduced Mini-LED television street prices from USD 3,000 in 2022 to nearly USD 1,200 in 2025. Conversely, edge-lit lines enjoy higher utilization and low capital intensity, enabling manufacturers to profit even as average selling prices decline, ensuring balanced growth across the LED backlight module market.

By Panel Size: Medium Panels Accelerate Growth

Medium-size panels measuring 10-32 inches are forecast to expand at an 18.55% CAGR through 2031, the fastest rate among all size tiers. They benefit from electric-vehicle clusters, esports monitors, and all-in-one desktops that need high refresh rates, localized dimming, and wide color gamut. Manufacturers combine Mini-LED backlighting with curved glass and quantum-dot films to achieve 2,000-nit peak brightness and 100% DCI-P3 coverage without sacrificing cabinet depth.[5]Illumi Electric, “Edge-Lit Backlight Cost Structure Whitepaper,” illumielectric.com This feature set positions the tier to command a rising share of the LED backlight module market, even though average selling prices remain below premium television levels. Battery-powered medical carts and rugged industrial tablets also migrate into the 10-14-inch bracket, adding incremental volume and creating cross-industry demand for automotive-grade thermal management and redundant LED strings.

Large panels above 32 inches still accounted for 44.94% of 2025 revenue. Replacement cycles for living-room televisions have stretched past five years, prompting brands to chase margin with Mini-LED upgrades rather than pure volume gains. Edge-lit designs defend low-cost 43-inch and 55-inch sets, while direct-lit Mini-LED modules dominate 75-inch and 85-inch premium SKUs, pulling in thousands of chips and sophisticated driver ICs. At the opposite extreme, small panels under 10 inches retreat as OLEDs capture flagship smartphones, leaving price-sensitive handsets, barcode scanners, and basic infotainment screens to sustain residual demand. Collectively, the divergence across size classes forces suppliers to run mixed production lines that balance thin-edge-lit notebooks, high-zoned Mini-LED gaming monitors, and cost-optimized television modules to keep utilization high and margins stable.

By Application: Automotive Leads Growth, TV Retains Scale

Television remained the largest application, accounting for 52.49% of 2025 revenue. Brands combat this plateau by embedding 1,000-zone Mini-LED engines, HDR10+ Adaptive metadata, and slim form factors that fit sub-30 millimeter cabinets. Even so, entrance-level edge-lit models priced below USD 400 keep volumes high but compress margins. Gaming monitors and creator-class laptops sit between the budget and premium ends, demanding 144-240 Hz refresh rates, 1,000-nit peaks, and wide-gamut performance that justifies a USD 150-USD 300 backlight premium. Energy-efficient signage and medical imaging panels provide steady retrofit income as hospitals and retailers replace fluorescent backlights to meet updated IEC and ENERGY STAR standards.

Automotive displays are projected to log an 18.43% CAGR, making them the fastest-growing segment in the forecast period. Cockpit digitization in electric vehicles places 2,000-nit, 15-inch-plus curved screens across instrument panels, center stacks, and passenger entertainment zones, each qualifying under ISO 15008 for daylight readability and ISO 26262 for functional safety. This complexity raises the bill of materials by 10-15% but locks suppliers into multi-year vehicle programs, supporting premium pricing and predictable loadings on Mini-LED assembly lines. Industrial and rugged tablets, medical carts, and avionics also lean on the same high-brightness architectures, widening the automotive supply base to adjacent verticals. Smartphones and tablets continue their secular decline within LED backlighting as OLED scales, leaving mid-tier handsets and educational tablets the last refuge for edge-lit solutions.

Geography Analysis

Asia Pacific contributed 67.82% of revenue in 2025 and is projected to sustain an 18.35% CAGR, underpinned by BOE, Tianma, and TCL CSOT expansions, as well as supportive incentives in China, Vietnam, and India. Localization programs reduce landed costs by exempting domestic sub-assemblies from import duties, driving internal investment into module integration lines. Capacity corridors in Guangdong and Jiangsu now combine LED epitaxy, phosphor synthesis, and quantum-dot film production, fortifying the regional supply chain.

North America and Europe collectively register outsized growth in automotive displays. Stricter power-consumption limits accelerate the transition to high-efficiency backlights across commercial signage and hospitality displays. Proposed reshoring projects, such as Japan Display’s USD 13 billion fab in the United States, could diversify supply away from the Asia Pacific while maintaining momentum for the LED backlight module market.

South America, the Middle East, and Africa remain nascent, with local integrators assembling modules for retail signage and price-sensitive televisions. Volumes in these regions are insufficient to challenge Asia Pacific dominance, yet tariff barriers and regional content rules could spur incremental localized assembly over the forecast horizon.

Competitive Landscape

In the LED backlight module market, a moderate concentration is evident. Through vertical integration, encompassing LED packaging, driver-IC fabrication, and final assembly, Samsung Display, LG Display, and BOE command a combined share. Meanwhile, specialized suppliers like Radiant Opto-Electronics, Seoul Semiconductor, Nichia, and ams OSRAM carve out their niche with proprietary dimming algorithms, cadmium-free quantum-dot materials, and a focus on automotive-grade reliability. Notably, ams OSRAM’s expansion in Austria is set to double its filter capacity and quadruple it's through-silicon-via capacity, bolstering the supply of optoelectronic components for both automotive and medical displays.

Patent portfolios serve as pivotal competitive assets. Nichia’s foundational, white-LED intellectual property and Seoul Semiconductor’s packaging patents generate royalty income, providing a buffer against commoditization pressures. The automotive sector offers lucrative opportunities; here, ISO 26262 certification and redundant LED architectures yield higher gross margins than in television modules. As legacy LCD panel makers offload older fabs, evidenced by Innolux’s divestiture of Fab 2 and Fab 5, capital is increasingly funneled towards higher-value optics and advanced packaging.

New market entrants are focusing on driver-IC integration and quantum-dot enhancement films. Companies like Nanosys, a subsidiary of Shoei Chemical, and BASF are pioneering organic light-conversion materials. These innovations enable extending the LCD color gamut to 100% DCI-P3 without requiring a redesign of LED arrays, thereby increasing the relevance of LED backlighting. Such advancements not only highlight the potential of LED technology but also offer panel makers a viable upgrade path amidst the rising prominence of OLED and Micro-LED technologies.

LED Backlight Module Industry Leaders

Samsung Electronics Co., Ltd.

BOE Technology Group Co., Ltd.

LG Display Co., Ltd.

AU Optronics Corp.

Innolux Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Innolux announced plans to sell its Fab 2 and Fab 5 facilities, enabling semiconductor packagers to repurpose the cleanrooms for advanced optics and meta-lens production.

- March 2026: Japan Display and the Japanese government began evaluating a USD 13 billion advanced display plant in the United States to diversify critical supply chains.

- February 2026: Taiwan-based panel makers fast-tracked sales of legacy fabs, with Powertech investing USD 220 million to acquire an AU Optronics site for fan-out panel-level packaging.

- September 2025: BASF introduced an upgraded cadmium-free QDYES film that boosts light efficiency by 10% and achieves 100% DCI-P3 color.

Global LED Backlight Module Market Report Scope

The LED Backlight Module Market Report is Segmented by Backlighting Technology (Edge-lit LED Modules and Direct-lit LED Modules), Panel Size (Small-size Panels, Medium-size Panels, and Large-size Panels), Application (Television, Monitor/Laptop, Smartphone/Tablet, Automotive Display, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Edge-lit LED Modules |

| Direct-lit LED Modules (Full Array / Mini-LED) |

| Small-size Panels (Less Than or Equal To 10 inches) |

| Medium-size Panels (Less Than 10 to Greater Than or Equal to 32 inches) |

| Large-size Panels (Less Than 32 inches) |

| Television (TV) Backlight Modules |

| Monitor / Laptop Backlight Modules |

| Smartphone / Tablet Backlight Modules |

| Automotive Display Backlight Modules |

| Other Application – Display Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Backlighting Technology | Edge-lit LED Modules | |

| Direct-lit LED Modules (Full Array / Mini-LED) | ||

| By Panel Size | Small-size Panels (Less Than or Equal To 10 inches) | |

| Medium-size Panels (Less Than 10 to Greater Than or Equal to 32 inches) | ||

| Large-size Panels (Less Than 32 inches) | ||

| By Application | Television (TV) Backlight Modules | |

| Monitor / Laptop Backlight Modules | ||

| Smartphone / Tablet Backlight Modules | ||

| Automotive Display Backlight Modules | ||

| Other Application – Display Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the LED backlight module market be by 2031?

It is projected to reach USD 5.14 billion by 2031 at a 17.89% CAGR over 2026-2031.

Which segment is driving growth in LED backlighting technologies?

Mini-LED direct-lit modules are forecast to grow at an 18.23% CAGR, outpacing edge-lit designs.

Why is automotive demand critical for future revenue?

Electric-vehicle cockpits require 2,000-nit displays that integrate redundant LED strings and functional-safety features, driving an 18.43% CAGR in automotive applications.

What region dominates production and consumption?

Asia Pacific accounted for 67.82% of 2025 revenue and is set to grow at an 18.35% CAGR, driven by aggressive capacity expansion and localization incentives.

How do energy regulations influence module design?

Updated U.S. and EU efficiency standards favor high-efficacy LED backlights that integrate quantum-dot films, accelerating retrofits in televisions and signage.

What competitive strategies sustain margins amid commoditization?

Vertical integration, robust patent portfolios, and specialization in high-growth niches such as automotive and gaming enable suppliers to defend 15-20% gross margins.

Page last updated on: