Automotive LED Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

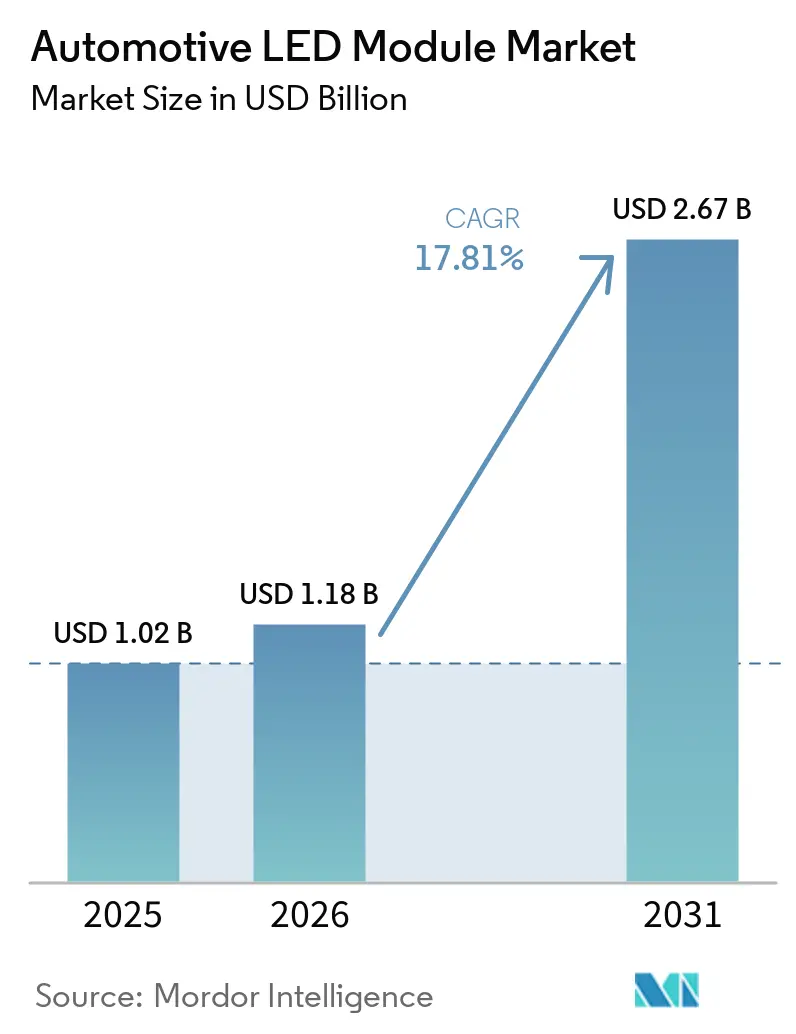

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 2.67 Billion |

| Growth Rate (2026 - 2031) | 17.81% CAGR |

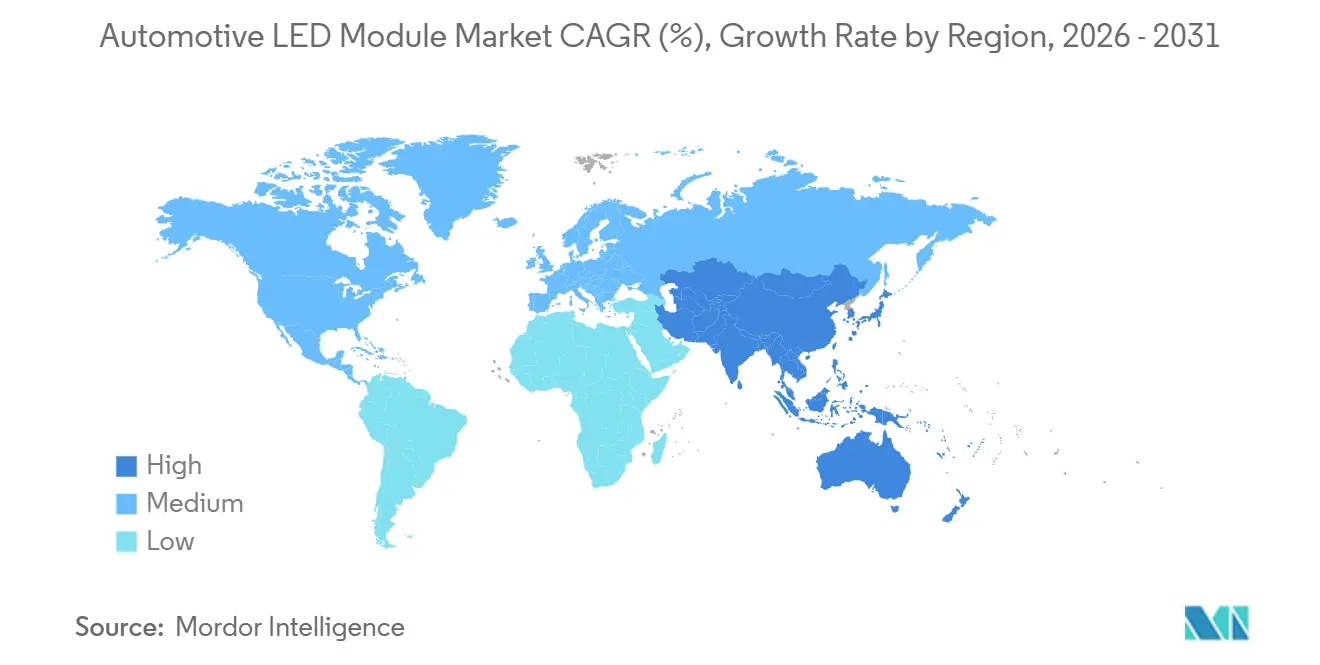

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

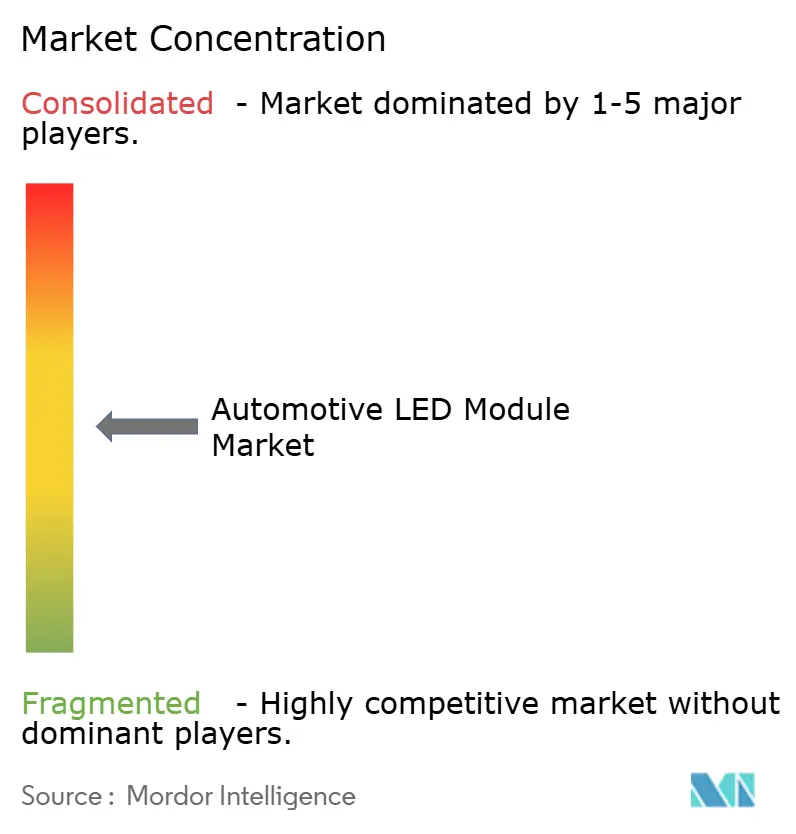

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive LED Module Market Analysis by Mordor Intelligence

The Automotive LED Module market size is projected to be USD 1.18 billion in 2026 and reach USD 2.67 billion by 2031, growing at a CAGR of 17.81% from 2026 to 2031. Demand is accelerating as adaptive driving beam systems enter mid-price models, electric vehicles impose tighter energy budgets, and pixel-addressable modules fall below USD 15 per headlamp assembly. Automakers are expanding software-defined lighting functions that project navigation cues and dynamic safety symbols onto the road surface. Suppliers that deliver chip-to-module solutions with integrated driver ICs and thermal management are gaining share, while pure assemblers face margin pressure. Asia Pacific dominates volume thanks to China’s new-energy-vehicle boom and deep Mini LED fabrication capacity, and passenger vehicles remain the innovation epicenter as premium features migrate into mass-market trims.

Key Report Takeaways

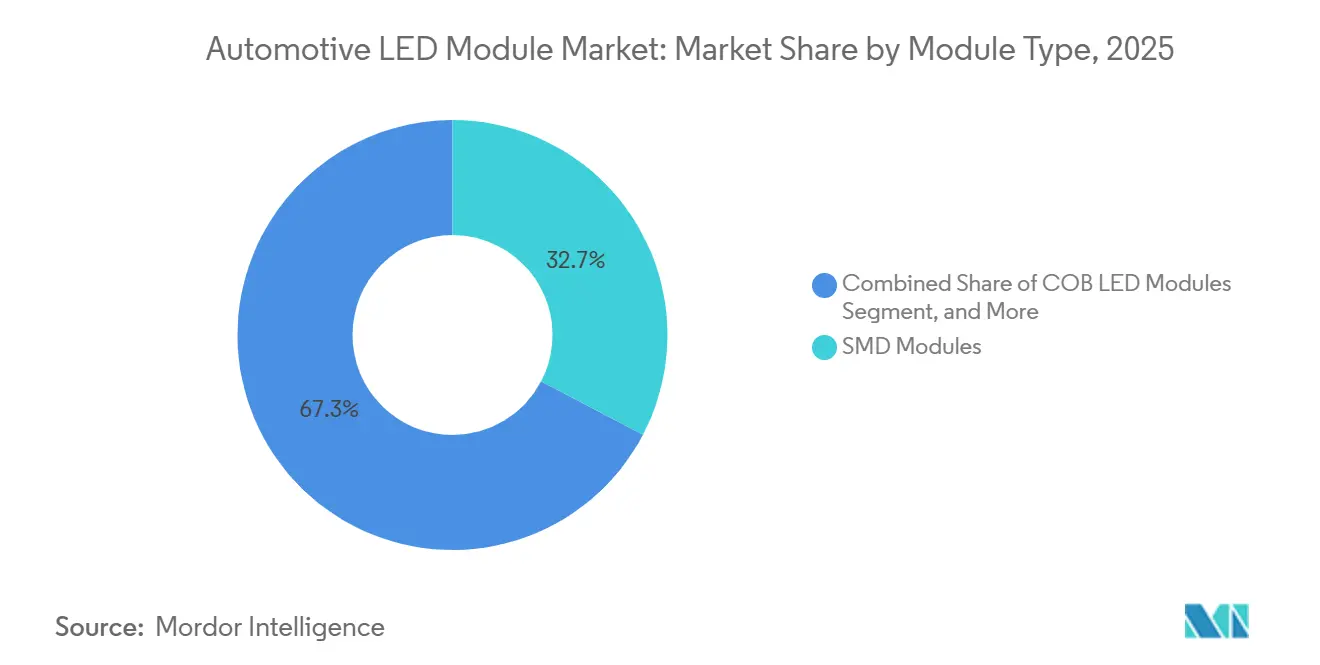

- By module type, SMD LED modules held 32.67% of the Automotive LED Module market share in 2025, while pixel and matrix arrays are forecast to grow at an 18.47% CAGR through 2031.

- By lighting function, exterior systems accounted for 67.39% of 2025 revenue; interior ambient lighting is advancing at a 18.33% CAGR through 2031.

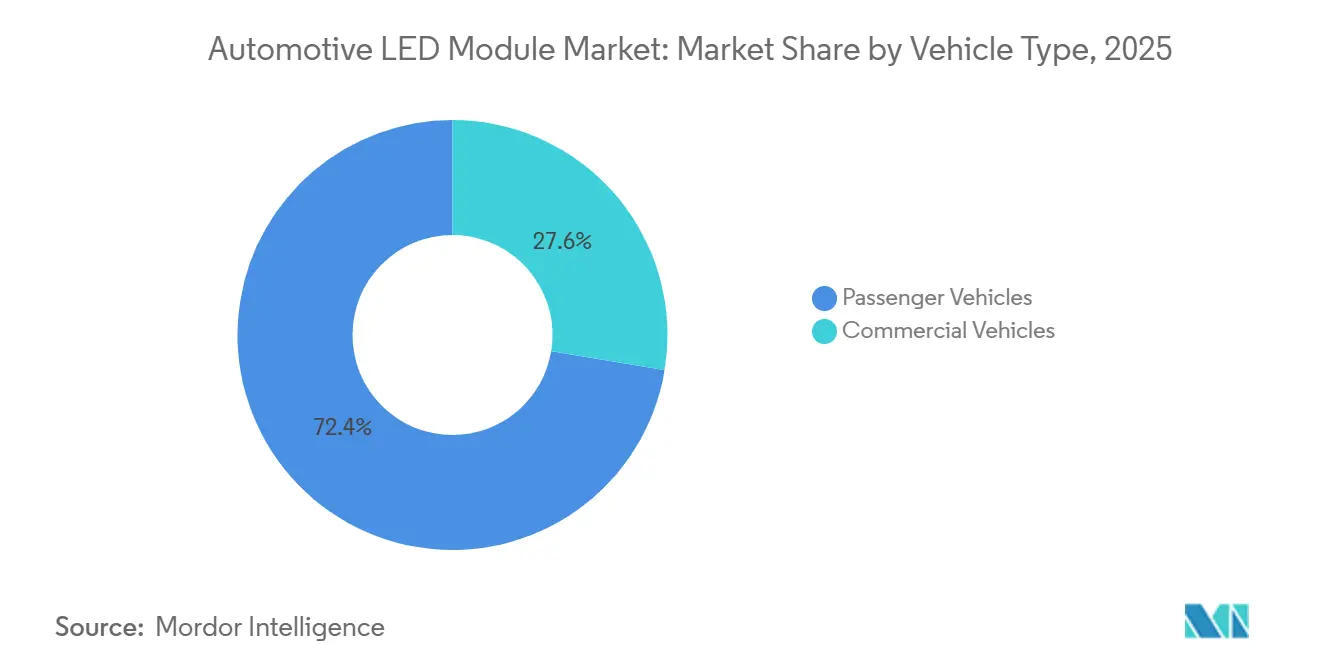

- By vehicle type, passenger models accounted for 72.39% of 2025 sales and are projected to grow at an 18.58% CAGR through 2031.

- By geography, Asia Pacific commanded 68.73% of 2025 revenue and is set to grow at a 17.97% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive LED Module Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing Adoption of Advanced Driver-Assistance Systems (ADAS) | +4.2% | Global, led by Asia Pacific and Europe | Medium term (2-4 years) |

| Shift Toward Electric Vehicles Requiring Energy-Efficient Lighting | +3.8% | Global, concentrated in China, Europe, and North America | Medium term (2-4 years) |

| OEM Preference for Modular, Scalable Lighting Architecture | +2.9% | Global, early traction in Asia Pacific and Europe | Short term (≤ 2 years) |

| Declining LED Cost per Lumen Boosting Penetration | +2.6% | Global, benefiting cost-sensitive Asia Pacific markets | Short term (≤ 2 years) |

| Integration of Dynamic Pixel Lighting for Vehicle-to-X Communication | +1.9% | Europe, North America, select Asia Pacific cities | Long term (≥ 4 years) |

| Regional Subsidies for Night-time Road-Safety Technologies | +1.4% | North America, Europe, the Middle East, and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Advanced Driver-Assistance Systems (ADAS)

Pixel-level beam control prevents camera and LiDAR wash-out, so OEMs are installing high-definition modules with more than 25,000 addressable points.[1]Audi AG, “Q3 Adaptive Matrix Lighting Specifications,” audi.com Selective illumination cuts energy use by up to 30% and extends lifetime by reducing thermal stress.[2]Infineon Technologies, “Automotive Micro-LED Driver IC Family,” infineon.com Software-programmable beams also enable left- and right-hand-drive compliance without mechanical parts, thereby shortening development cycles. As Level 3 and Level 4 features appear, lighting that communicates vehicle intent to pedestrians becomes essential, further entrenching pixel arrays as the default headlamp technology.

Shift Toward Electric Vehicles Requiring Energy-Efficient Lighting

LED modules draw 40-60 watts versus 110-130 watts for halogens, adding 2-4 kilometers of range per charge in compact EVs. Premium ambient systems now operate at 30% lower power while maintaining color-rendering indices above 95, easing load on battery cooling loops. Every watt saved in lighting is reallocated to drivetrain or climate control, so OEMs specify LEDs on nearly all new electric platforms, pushing both volume and content per vehicle higher.

OEM Preference for Modular, Scalable Lighting Architecture

Common mechanical interfaces let automakers offer entry-level halogen-replacement, matrix, and pixel options from a single housing. Flexible circuit boards conform to curved grilles and two-meter light bars, cutting assembly steps by about 40% in new high-tonnage molding facilities. Firmware reconfiguration supports different regional regulations across a single hardware set, helping tier-one suppliers capture multiple trim levels and markets with a single modular family.

Declining LED Cost per Lumen Boosting Penetration

Cost-per-lumen has dropped annually as Mini LED oversupply and chip-scale packaging yields have squeezed prices. Vertical integration across wafer, package, and module stages reduces manufacturing costs, enabling suppliers to offer fixed-price contracts that protect OEMs from volatility. Lifespans of 49,999 hours eliminate mid-life bulb changes, making LEDs cost-neutral for commercial fleets within a short period.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Thermal Management Challenges in High-Power LED Modules | -2.3% | Global, acute in the Middle East and South Asia | Short term (≤ 2 years) |

| High Up-Front Tooling Cost for Matrix/Pixel Platforms | -1.9% | Global, constraining smaller OEMs and tier-twos | Medium term (2-4 years) |

| Supply-Chain Volatility of Key Phosphor and Epitaxy Materials | -1.2% | Global, concentrated in the Asia Pacific rare-earth supply | Medium term (2-4 years) |

| Regulatory Uncertainty Around Adaptive Beam Standards | -0.8% | North America, select Asia Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thermal Management Challenges in High-Power LED Modules

Currents above 1 ampere push junction temperatures past 150 °C, accelerating lumen loss and shortening life below the 50,000-hour target. Advanced substrates, carbon-nanotube fluids, and active cooling reduce heat but add USD 8-12 per module and increase warranty complexity. Hot climates intensify the problem, forcing premium cars to adopt liquid plates or micro-fans that remain uneconomic for mass models, thereby slowing pixel adoption in volume segments.

High Up-Front Tooling Cost for Matrix/Pixel Platforms

Pixel programs often exceed USD 50 million in molds, alignment jigs, and driver IC design. Only platforms with more than 100,000 units justify such spend, so smaller brands and tier twos struggle to bid. Rapid pixel-count doubling renders last-generation tooling obsolete before full amortization, raising financial risk. Universal assembly lines that handle multiple pixel densities help spread costs, but capital barriers still deter new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: Pixel Arrays Challenge SMD Incumbency

SMD LED modules accounted for 32.67% of the Automotive LED Module market share in 2025, thanks to mature supply chains and reliable thermal performance. The Automotive LED Module market size for pixel and matrix systems is projected to expand at an 18.47% CAGR, supported by software-defined beams that satisfy UN ECE R149 and NHTSA adaptive rules without mechanical parts. Pixel engines with more than 16,000 micro-LEDs now monitor current and temperature per emitter, enabling predictive maintenance and extending service life. COB packages serve high-intensity spot and fog functions, especially in commercial vehicles where vibration resistance matters more than cost. Laser-assisted hybrids remain niche until phosphor stability and cooling costs improve, with series production slated beyond 2027.

Pixel architectures advance partly because they enable firmware updates that add new animations or communication symbols post-sale, a feature SMD arrays cannot deliver. Suppliers offering integrated driver ICs and sub-0.5 K/W thermal resistance win premium EV programs, while pure SMD assemblers defend volume ICE models but face price compression. The transition timeline hinges on thermal breakthroughs and further cost declines, but the direction toward high-pixel-count modules is clear.

By Lighting Function: Interior Ambient Systems Outpace Exterior Growth

Exterior systems accounted for 67.39% of revenue in 2025, driven by headlamps adopting adaptive driving beams and daytime running lights evolving into signature animations. The Automotive LED Module market size tied to interior ambient arrays is expanding at an 18.33% CAGR as per-pixel RGB control and CRI > 95 become standard in electric crossovers. Mini LED foils enable full-width rear lamps that flash dynamic turn patterns, while interior lighting spreads across dashboards, seat wings, and roof liners to support personalized cabin moods.

Headlamp volumes still dictate overall demand, but interior content per car is rising faster because ambient zones multiply from less than 10 in 2024 to more than 64 in premium 2026 launches. Regulatory harmonization between UN ECE R149 and Transport Canada photometric codes simplifies exterior approvals, allowing designers to invest more effort in interior differentiation.[3]Transport Canada, “TSD 108 Amendments for Adaptive Driving Beams,” tc.canada.ca Ambient modules also integrate with driver-monitoring cameras and wellness functions, tying lighting to biometric cues such as heart rate or drowsiness.

By Vehicle Type: Passenger Segment Drives Volume and Innovation

Passenger vehicles contributed 72.39% of 2025 revenue and are forecast to grow at an 18.58% CAGR, reflecting the segment’s appetite for styling, ADAS, and brand signatures. The Automotive LED Module market size in commercial vehicles grows more slowly but benefits from 50,000-hour lifespans that reduce bulb-change downtime. Electric and hybrid passenger vehicles use LED technology extensively, as every saved watt extends their range. Combustion platforms, while currently at a lower level of LED adoption, are steadily increasing their usage due to styling considerations.

Ultra-slim 17 mm headlamps launch first in passenger EVs, where aerodynamic gains translate into range, then trickle to light-duty trucks. Long-haul trucks prioritize durable COB arrays with standardized connectors that technicians can swap in under 30 minutes. Fleet safety targets are nudging the adoption of adaptive beams that lower wildlife collisions, gradually narrowing the technology gap with passenger models.

Geography Analysis

Asia Pacific commanded a 68.73% share in 2025 and will advance at a 17.97% CAGR through 2031, as China, Japan, and India together exceed a large amount of global output. Concentrated fabrication of Mini and Micro LED wafers shortens lead times and lowers package costs, reinforcing the region’s dominance. Subsidies tied to China’s 25% new-energy-vehicle penetration catalyze gains in LED content per car. Japan scales application-processor modules, positioning local plants as hubs for driver ICs and Mini LED backlights used in both interior lighting and cockpit displays. India accelerates tool-heavy rear-lamp programs thanks to new high-tonnage presses capable of two-meter light bars.

North America is catalyzed by consumer appetite for customizable cabins and software-defined vehicle platforms. NHTSA’s cautious enforcement of its adaptive-beam rule slows ultra-high pixel counts but ensures stable demand for matrix arrays. Supplier investments cluster near Mexico and the United States to mitigate tariff and logistics risk while serving domestic assembly plants.

Europe sets the regulatory pace with UN ECE R149, allowing matrix beams across the continent under unified testing, encouraging OEMs to fit LEDs even on entry trims to meet CO₂ and safety targets. South America and the Middle East show smaller bases but above-average gains, as exporters align with EU lighting standards and regional premium buyers specify LED daytime running lights. Africa remains nascent; premium segments in South Africa adopt LEDs, while mass models still rely on halogen to keep vehicle prices down.

Competitive Landscape

Sector concentration is moderate; the top five lighting integrators account for a significant share of 2025 revenue. Strategic paths diverge: tier-ones pursue vertical integration, exemplified by OPmobility’s plan to acquire Hyundai Mobis’s lighting arm for over EUR 1 billion (USD 1.13 billion), expanding captive access to Hyundai and Kia platforms. Semiconductor houses circumvent integrators by marketing full-light engines; ams OSRAM’s 2026 Open System Protocol links 1,000 addressable LEDs on a differential bus, slashing PCB costs and positioning the firm as a turnkey supplier.[4]BusinessKorea, “LG Innotek Expands Gwangju Plant,” businesskorea.co.kr

White-space innovation targets circular-economy compliance. Replaceable light-source cartridges that fit service-category rules reduce end-of-life waste and unlock remanufacturing revenue. Chinese entrants leverage wafer-to-module vertical stacks to undercut incumbents by 20-30% while meeting AEC-Q standards, prompting established players to differentiate through pixel density, thermal resistance, and integrated health monitoring. Patent filings on 16,000-plus-pixel micro-LED arrays signal a defensive moat around high-definition adaptive beams, constraining latecomers to licensing or lower-spec offerings.

Automotive LED Module Industry Leaders

Nichia Corporation

ams-OSRAM AG

Stanley Electric Co., Ltd.

Seoul Semiconductor Co., Ltd.

Lumileds Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Marelli-Motherson Lighting India inaugurated a second plant in Sanand, Gujarat, equipped with presses forming two-meter light bars and 17 mm headlamps, introducing heavy-tooling capacity to India.

- January 2026: Valeo secured a major interior lighting contract and installed an in-mold structural electronics line using TactoTek technology, contributing to nearly EUR 1 billion (USD 1.13 billion) in orders since 2024.

- January 2026: OPmobility signed an MoU to explore the acquisition of Hyundai Mobis’s lighting division, potentially adding EUR 1 billion (USD 1.13 billion) annual revenue, with closing targeted in 2026.

- January 2026: LG Innotek expanded its Gwangju facility with a 9,000 m² automotive application-processor module line, investing KRW 100 billion (USD 75 million) and tripling capacity.

Global Automotive LED Module Market Report Scope

The Automotive LED Module Market Report is Segmented by Module Type (COB LED Modules, SMD LED Modules, Matrix/Pixel LED Modules, and Other Module Type), Lighting Function (Exterior Lighting: Headlamps, Tail Lamps, Daytime Running Lights, Other Exterior Lighting; and Interior Lighting; Other lighting functions), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| COB LED Modules |

| SMD LED Modules |

| Matrix / Pixel LED Modules |

| Other Module Type (laser-assisted, adaptive modules) |

| Exterior Lighting | Headlamps |

| Tail Lamps | |

| Daytime Running Lights (DRL) | |

| Others Exterior Lighting | |

| Interior Lighting | |

| Others Interior Lighting (ambient signature, logo projection) |

| Passenger Vehicles |

| Commercial Vehicles |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Module Type | COB LED Modules | |

| SMD LED Modules | ||

| Matrix / Pixel LED Modules | ||

| Other Module Type (laser-assisted, adaptive modules) | ||

| By Lighting Function | Exterior Lighting | Headlamps |

| Tail Lamps | ||

| Daytime Running Lights (DRL) | ||

| Others Exterior Lighting | ||

| Interior Lighting | ||

| Others Interior Lighting (ambient signature, logo projection) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Automotive LED Module market by 2031?

The market is expected to reach USD 2.67 billion by 2031.

How fast is the market expected to grow between 2026 and 2031?

It is forecast to grow at a 17.81% CAGR during the period.

Which region leads global demand today?

Asia Pacific accounts for about 68.73% of 2025 revenue and continues to lead.

Why are pixel LED modules gaining traction?

They enable adaptive beams without mechanical parts, support software updates, and align with ADAS sensor requirements.

What is the main restraint to high-power LED adoption?

Managing junction temperatures above 150 °C increases costs and complexity, slowing mass-market segment rollout.

Which vehicle segment shows the highest growth rate?

Passenger models are advancing at an 18.58% CAGR through 2031, outpacing commercial vehicles.

Page last updated on: