Leaf-Spine Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.42 Billion |

| Market Size (2031) | USD 35.32 Billion |

| Growth Rate (2026 - 2031) | 16.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Leaf-Spine Switch Market Analysis by Mordor Intelligence

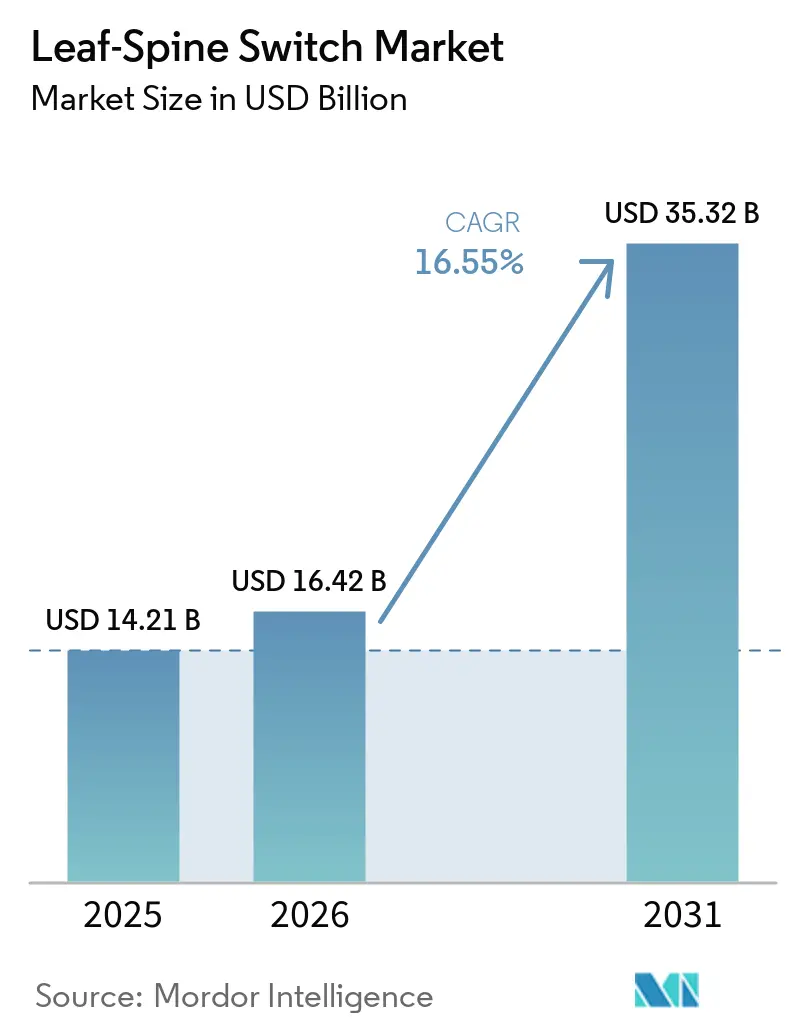

The leaf-spine switch market size is expected to increase from USD 14.21 billion in 2025 to USD 16.42 billion in 2026 and reach USD 35.32 billion by 2031, growing at a CAGR of 16.55% over 2026-2031. The leaf-spine switch market is being lifted by a rare overlap of two upgrade cycles, as data center operators shift to two-tier fabrics at the same time that they move from 400Gbps to 800Gbps and from 51.2Tbps to 102.4Tbps silicon. That overlap is changing purchasing behavior because fewer, denser systems now carry more traffic, which raises revenue per deployed platform even when switch counts fall in the largest AI clusters. Demand remains centered on hyperscalers and colocation operators, where non-blocking east-west bandwidth, tenant isolation, and faster provisioning directly affect cluster output and site monetization. The leaf-spine switch market is also opening up for ODMs and open networking stacks as hardware and software disaggregation gains traction, while established vendors defend margins through modular platforms, integrated management, and deeper silicon partnerships. Sovereign cloud mandates across Europe, the Middle East, and Southeast Asia are adding a second build cycle that is less tied to hyperscaler spending and gives the leaf-spine switch market a broader geographic demand floor through the forecast period.

Key Report Takeaways

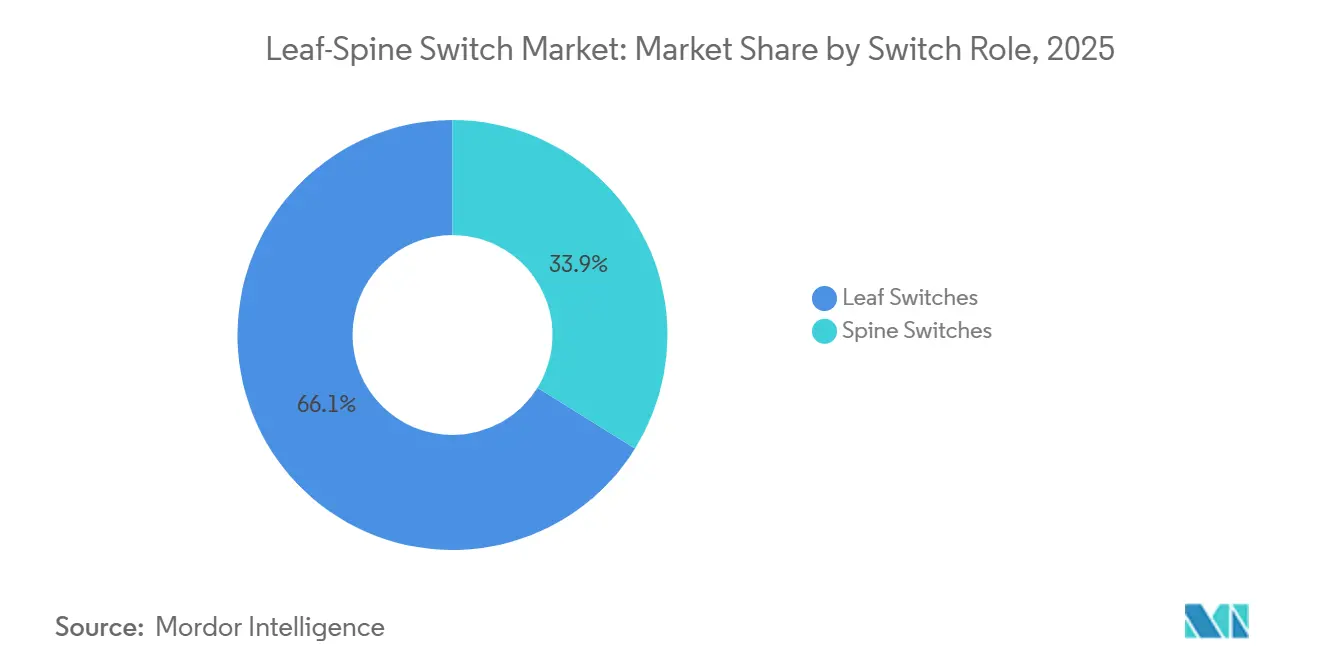

- By switch role, leaf switches led with 66.14% of revenue in 2025 in the leaf-spine switch market, while spine switches recorded the highest projected CAGR at 18.45% through 2031.

- By product type, fixed configuration switches held 72.43% of revenue in 2025, while modular switches are forecast to expand at a 18.12% CAGR through 2031.

- By port speed, the 25-100 GbE segment accounted for 38.62% of revenue in 2025, while the 800 GbE and above segment is advancing at a 17.83% CAGR through 2031.

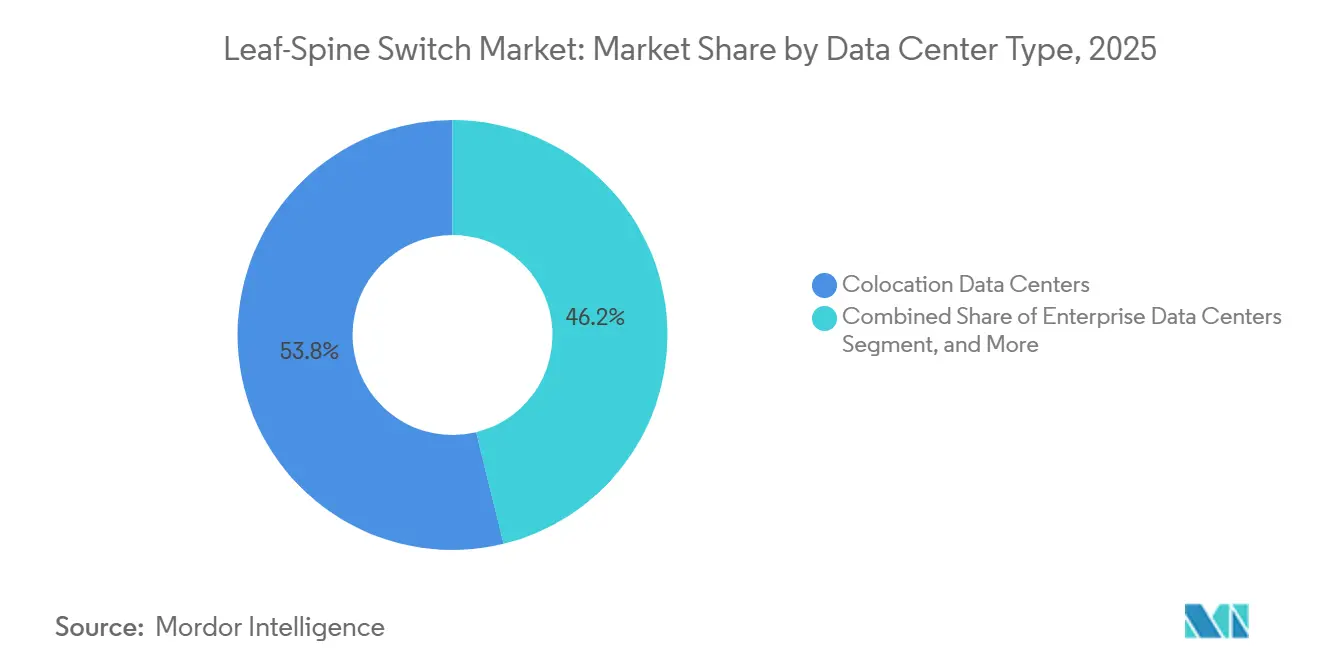

- By data center type, colocation data centers captured 53.81% of revenue in 2025, while hyperscale and cloud service provider data centers are projected to grow at a 17.11% CAGR through 2031.

- By end user, cloud service providers accounted for 44.32% of revenue in 2025 and remained the fastest-growing end-user category through the forecast period at a 17.23% CAGR through 2031.

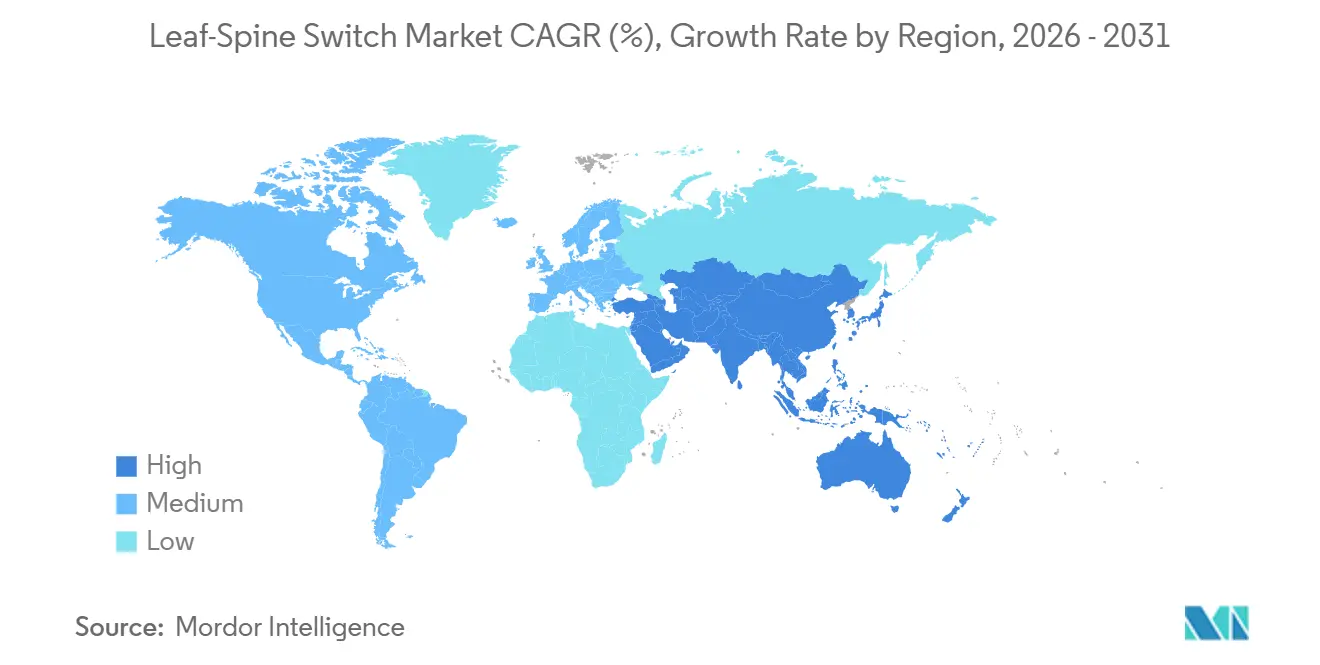

- By geography, North America held 41.43% of revenue in 2025, while Asia-Pacific is projected to expand at an 16.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Leaf-Spine Switch Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hyperscaler AI Cluster 400G and 800G Fabric Rollouts | +4.8% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| East-West Traffic Growth and Data Center Fabric Modernization | +3.2% | Global, with highest intensity in North America, Asia-Pacific, and Europe, the Middle East, and Africa | Medium term (2-4 years) |

| 51.2T Switch Silicon Enabling Flatter Topologies | +2.6% | Global, driven by hyperscaler and Tier-1 colocation deployments | Short term (≤ 2 years) |

| Colocation Expansion and Tenant-Ready EVPN-VXLAN Fabrics | +2.0% | North America and Europe, expanding into Asia-Pacific | Medium term (2-4 years) |

| Ethernet Replacing InfiniBand in AI Scale-Out Networks | +1.5% | Global, primary impact in North America and East Asia | Short term (≤ 2 years) |

| Sovereign Cloud Zones Multiplying Local Fabric Builds | +1.2% | Middle East, Europe, Southeast Asia, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscaler AI Cluster 400G And 800G Fabric Rollouts

Hyperscaler spending is setting the pace for the leaf-spine switch market because AI clusters cannot scale without large volumes of low-latency east-west bandwidth. Operators are now buying fabrics around 400G and 800G as standard design points instead of treating them as premium edge cases. Google disclosed Virgo in April 2026 as a flat, two-layer network linking 134,000 TPU chips with 47 petabits per second of bisectional bandwidth, which shows how large AI fabrics are moving deeper into purpose-built accelerator environments. Arista stated in May 2026 that it had surpassed 100 cumulative 800G Ethernet customers and raised its 2026 AI networking revenue target to USD 3.5 billion, which confirms that commercial demand is already broadening beyond a handful of early deployments.[1]Arista Networks, “AI Networking Revenue Target and 800G Customer Update,” Arista Networks, arista.com This is also changing product boundaries inside the leaf-spine switch market, because high-radix 800G systems are increasingly serving as both AI back-end aggregation layers and conventional east-west spines. That shift raises revenue density per chassis and favors vendors that can supply dense platforms without adding operational complexity.

East-West Traffic Growth And Data Center Fabric Modernization

East-west traffic now dominates virtualized and AI-oriented data center environments, which keeps the leaf-spine switch market tied to fabric modernization rather than to simple port replacement. The architectural move from three-tier switching to two-tier leaf-spine design reduces latency, simplifies pathing, and supports the 1:1 non-blocking ratios that AI training environments require. The cost logic also matters because 400G delivers materially lower cost-per-bit than 100G, which makes it the default step for operators that need bandwidth growth without taking on a full 800G migration. The oversubscription change is equally important because many legacy enterprise designs ran at 3:1, while GPU clusters demand non-blocking behavior and therefore need far more active switching capacity for the same compute footprint. As a result, the leaf-spine switch market is gaining from both greenfield AI deployments and brownfield refresh programs that replace hierarchical designs with flatter fabric architectures. The underlying opportunity is wide because modernization now serves performance, power, and operational goals at the same time, which is why the upgrade case is harder for operators to delay.

51.2T Switch Silicon Enabling Flatter Leaf-Spine Topologies

The arrival of 51.2T and 102.4T switching platforms is one of the clearest hardware accelerators for the leaf-spine switch market because it allows operators to flatten networks while lifting traffic per system. Cisco introduced Silicon One G300 in February 2026 at 102.4T, and the platform was presented as enabling a 128,000-GPU fabric with 750 switches instead of the 2,500 that would have been required on a comparable 25.6T generation.[2]Cisco, “Silicon One G300 and AI Networking Platform Announcements,” Cisco Newsroom, cisco.com That reduction changes both capital intensity and operating models because the network carries similar or higher traffic with fewer elements to power, cool, cable, and manage. It also changes competition because lower switch counts move more value into a smaller number of high-radix systems, especially in modular spine tiers. In the leaf-spine switch market, that means vendors with credible chassis road maps can capture a larger share of budget even as unit volumes compress at the top end of cluster design. The result is a winner-take-more pattern in premium deployments, where performance per chassis now matters more than the older equation of simple port accumulation.

Colocation Expansion And Tenant-Ready EVPN-VXLAN Fabrics

Colocation operators remain central to the leaf-spine switch market because shared facilities concentrate tenant density, routing complexity, and pressure for faster provisioning. EVPN-VXLAN has become the standard framework for multi-tenant isolation because it lets operators create independent Layer 2 and Layer 3 environments without physical re-cabling. Equinix launched Fabric Geo Zones in May 2026 across 77 metro markets, showing how data sovereignty controls are now being built into the interconnection layer rather than treated as a separate compliance overlay. That move matters for switching demand because tenant readiness is no longer defined only by available ports, it is also defined by how quickly compliant virtual domains can be turned up and managed. This pushes operators toward pre-provisioned EVPN-VXLAN templates, zero-touch workflows, and software-linked switching environments that support faster onboarding. In practical terms, the leaf-spine switch market benefits because more of the value stack now sits inside the fabric itself, not only in the raw hardware footprint.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| 400G and 800G Refresh Capex and Migration Complexity | -3.2% | Global, most acute in North America and Europe, the Middle East, and Africa enterprise segments | Medium term (2-4 years) |

| EVPN-VXLAN and RoCE Operations Talent Shortages | -2.0% | Global, concentrated in North America, Europe, the Middle East, and Africa, and Asia-Pacific tier-2 markets | Long term (≥ 4 years) |

| Power and Thermal Retrofit Burden in Dense AI Pods | -1.4% | North America and Europe, where legacy facilities dominate | Medium term (2-4 years) |

| Merchant Silicon and Optics Supply Concentration | -1.0% | Global, with cascading risk in Southeast Asia manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

400G And 800G Refresh Capex And Migration Complexity

The leaf-spine switch market faces a real spending barrier because 400G and 800G transitions require more than a switch purchase. Fiber compatibility problems, connector mismatches, and trunk rework can add large project costs across thousands of links in active facilities. Power is another constraint because 800G systems can draw 800 to 1,000 watts, which makes it harder for older sites that were not designed for dense AI pods. Many operators, therefore, need network, cabling, and facility teams to move in sequence, which slows deployment even when procurement intent is strong. This creates a split in the leaf-spine switch market, where hyperscalers with dedicated engineering teams can move quickly, while enterprise and mid-market operators often stretch refresh cycles across multiple budget periods. The result is uneven demand timing, not weak demand, which is why order flow can look lumpy even when the medium-term adoption case remains intact.

EVPN-VXLAN And RoCE Operations Talent Shortages

Skills remain a limiting factor for the leaf-spine switch market because advanced fabrics are harder to run than they are to approve on paper. Many organizations can design EVPN-VXLAN architectures, but far fewer can operate them reliably at production scale across multi-tenant or AI-heavy environments. RoCE-based Ethernet fabrics also demand careful congestion and flow-control settings, which raises the cost of operational mistakes when expensive GPU workloads sit behind the network. The gap is most evident among regional cloud operators and mid-market enterprises that lack hyperscaler-scale platform teams. That slows rollouts in customer groups where the fabric transition is still at an early stage and where long-run vendor expansion should be strongest. Until skills, tooling, and day-2 operations improve together, the leaf-spine switch market will continue to see a portion of planned upgrades deferred by execution risk rather than by a lack of strategic need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switch Role: Leaf Dominance Meets Spine Renaissance

Leaf switches held 66.14% of 2025 revenue, which gave them the largest position in the leaf-spine switch market share because every GPU node and most server endpoints still terminate at the top-of-rack layer. That installed logic remains strong because cluster node counts are rising faster than the number of distinct clusters, which keeps the leaf layer broad even as designs become more efficient. The top-of-rack leaf position also benefits from repeatability, since large AI and cloud builds replicate rack-level patterns at scale across halls and campuses. In the leaf-spine switch industry, that means fixed leaf platforms retain a wide deployment base even when value is shifting upward into denser aggregation systems. End-of-row leaf systems still serve enterprise environments where a rack-by-rack build is harder to justify, especially when operators are modernizing only a portion of legacy compute space.

Spine switches are projected to grow at an 18.45% CAGR through 2031, which makes them the fastest-growing role in the leaf-spine switch market size profile for role-based demand. The reason is not switch count alone, it is the revenue concentration created when one chassis aggregates a large number of 800G uplinks and carries a much higher average selling price than a fixed spine unit. Arista launched its 7800R4 modular spine family with up to 576x800G ports per system, which illustrates how the architectural center of gravity is moving toward fewer, larger aggregation systems.[3]Arista Networks, “R4 Series and 7800R4 Modular Spine Platform,” Arista Networks, arista.com This is why spine growth looks stronger than its unit footprint suggests, because scale-out AI traffic rewards vendors that can deliver high-radix platforms with predictable congestion behavior and simpler management. The role balance is therefore not reversing, but it is re-weighting revenue inside the leaf-spine switch market toward premium spine systems that sit at the center of AI training fabrics.

By Product Type: Fixed Form Factors Hold Ground As Modular Scales

Fixed configuration switches accounted for 72.43% of 2025 revenue, which reflects how much of the leaf-spine switch market still depends on the sheer number of leaf positions across new data center builds. That arithmetic is direct because a very large cluster can require thousands of fixed leaf units even when the spine layer can be handled by a much smaller number of chassis systems. The 1U and 2U categories remain important because operators continue to standardize top-of-rack deployment around dense fixed platforms that fit repeatable rack designs. In 2026, fixed configurations with 64x800G and 32x1.6T are entering production environments, which shows that fixed form factors are not a legacy layer, but a still-evolving foundation for AI leaf roles. This keeps fixed systems at the volume center of the leaf-spine switch market even as premium spending migrates elsewhere.

Modular switches are forecast to grow at a 18.12% CAGR through 2031, which gives them the fastest momentum among product types in the leaf-spine switch market. That growth is tied to hyperscale AI clusters where spine refresh cycles require densities and scale characteristics that fixed systems cannot match efficiently. Arista stated that its 7800R4 family delivers 65% lower power consumption than the prior 7800R3 series, which shows how vendor competition in modular systems is expanding beyond port count into energy efficiency and operating cost. Buffer design and congestion control are also becoming clearer differentiators because mixed-speed AI fabrics need systems that can absorb bursty traffic without forcing operators into complex workarounds. Vendors that can pair modular spine products with fixed leaf systems inside one management plane are gaining an advantage, since buyers want fewer operational seams across multi-year refresh programs. That makes modular growth strategically important to the leaf-spine switch market even if fixed platforms continue to dominate total deployment count.

By Port Speed: Installed Base Strength Supports The 800G Push

The 25-100 GbE band held 38.62% of 2025 revenue, which made it the largest single speed tier in the leaf-spine switch market because the enterprise and mid-tier installed base is still substantial. Many operators remain on 25G server links and 100G uplinks, so the existing footprint continues to generate revenue through replacement planning, staged upgrades, and mixed-speed deployments. This installed base matters because it funds a gradual transition path rather than a one-time jump, especially for operators that want to preserve parts of their fiber plant while modernizing AI-ready zones first. The persistence of this tier also shows that the leaf-spine switch market is not moving at one universal speed, as hyperscalers, colocation operators, and enterprises are making different timing choices. That diversity softens the risk of a narrow demand profile and keeps broad-based spending active even while premium attention focuses on 800G.

The 800 GbE and above segment is projected to expand at a 17.83% CAGR through 2031, making it the fastest-growing speed band in the leaf-spine switch market. The formal ratification of IEEE 802.3df in 2024 removed a major interoperability concern around 800G Ethernet, which supports broader multivendor adoption in AI and high-performance data center fabrics. The Ultra Ethernet Consortium published the UEC 1.0 specification in June 2025, and that framework pushed receiver-driven congestion control, packet spraying, and RDMA transport more firmly into the Ethernet roadmap for AI fabrics. The effect is to narrow the gap between open Ethernet and proprietary alternatives in large AI scale-out designs. At the same time, the 100-400 GbE range remains the workhorse for many new enterprise uplink deployments because it balances bandwidth gains with operational familiarity and better fit for existing cabling. This split means the leaf-spine switch market can expand at the top and middle layers simultaneously, rather than relying on one premium tier to carry all growth.

By Data Center Type: Colocation Anchors Revenue While Hyperscale Sets The Pace

Colocation data centers captured 53.81% of 2025 revenue, which gave them the largest position in the leaf-spine switch market size by facility type. Their advantage comes from shared physical infrastructure, tenant isolation requirements, and the need for redundancy across many customer environments inside the same building or metro platform. A multi-tenant fabric often requires more switching depth, more redundant leaf pairs, and stronger automation than a single-tenant network of similar compute scale, which lifts revenue per rack. Colocation operators also turn the network into a commercial feature because provisioning speed and routing flexibility shape how quickly a tenant can go live. That keeps the leaf-spine switch market closely tied to colocation investment cycles, especially in metros where enterprise AI demand is moving faster than in-house facility build-outs.

Hyperscale and cloud service provider facilities are expected to grow at a 17.11% CAGR through 2031, which makes them the fastest-expanding data center type in the leaf-spine switch market. These builds are being pulled by AI training demand, and the timing is notable because major regions are scaling in parallel rather than in the staggered wave pattern seen in earlier cloud infrastructure cycles. Enterprise data centers are still moving more selectively, often deploying 400G fabrics in new AI and machine learning zones while leaving 25G and 100G infrastructure in older compute areas. Edge facilities add a smaller but interesting stream of demand because compact leaf-spine pods can support real-time inference where centralized sites cannot meet latency needs. That edge case is not yet a revenue center on the same scale as colocation or hyperscale, but it expands the deployment map of the leaf-spine switch market into more distributed and repeatable site formats.

By End User: Cloud Service Providers Lead On Scale And Spending Intensity

Cloud service providers held 44.32% of 2025 end-user revenue, which made them the largest buyer group in the leaf-spine switch market. Their role is unusually strong for infrastructure hardware because they buy at both very high volume and very high technical intensity, especially in AI cluster environments where network limits directly reduce model throughput. This combination keeps the vendor landscape tightly focused on a small set of very demanding customers whose design choices influence the rest of the market. Their refresh cycles are also faster than those seen in traditional enterprise environments, which keeps premium product generations moving into production sooner. That is why the leaf-spine switch market responds quickly to hyperscaler architecture changes, whether the trigger is higher port speed, denser silicon, or a different balance between fixed and modular systems.

Cloud service providers remained the fastest-growing end-user segment through 2031, registering a robust CAGR of 17.23% during the period. Telecommunication operators continue to adopt leaf-spine fabrics for 5G core and network slicing environments where EVPN-VXLAN supports multi-tenant network function virtualization on shared infrastructure. Large enterprises form the second-largest user group, but many are still in the early phase of shifting private AI and inference workloads onto modernized Ethernet fabrics. Government demand is becoming more important because sovereign AI projects require in-country fabrics and in some cases impose hardware sourcing constraints that reshape vendor selection. Microsoft confirmed that the Saudi Arabia East Azure region is planned for availability in Q4 2026, which highlights how national cloud and AI programs are turning policy requirements into switching demand.[4]Microsoft, “Saudi Arabia East Azure Region Confirmation,” Microsoft News, microsoft.com Other users, including research institutions and managed service providers, remain smaller in scale, but they add breadth to the leaf-spine switch market as more high-performance environments move toward standards-based Ethernet fabrics.

Geography Analysis

North America held 41.43% of 2025 revenue, which made it the largest regional contributor and the clearest anchor of the leaf-spine switch market share by geography. The region benefits from the heaviest concentration of hyperscale AI training infrastructure, the deepest set of vendor relationships, and the strongest installed base for high-end data center switching. The United States remains the core of that demand because most large procurement programs, platform validations, and AI cluster launches are centered there. It is also the region where Cisco, Arista, NVIDIA, and white-box suppliers compete most directly for hyperscale and enterprise fabric budgets. This concentration keeps North America central to the leaf-spine switch market even as growth begins to broaden geographically.

Asia-Pacific is projected to grow at an 17.52% CAGR through 2031, which gives it the fastest regional growth path in the leaf-spine switch market. The region is being supported by a wide data center build pipeline, sovereign compute programs, and a rising mix of hyperscale, colocation, and enterprise open networking deployments. Malaysia, India, Japan, South Korea, Thailand, and other hubs are attracting parallel investment, which reduces reliance on any single national build cycle. Japan also showed movement toward open networking in 2026 when EXEO Group completed a production deployment of a SONiC-based leaf-spine fabric managed by BE Networks' Verity platform, a sign that software-disaggregated approaches are gaining credibility in the regional enterprise segment.

Europe is growing from a smaller base than North America, but the region is structurally important to the leaf-spine switch market because data sovereignty and regulated workload rules are creating demand for in-country fabrics. Equinix expanded Fabric Geo Zones in 2026 with preview availability in markets including Switzerland and the United Kingdom, which shows how switching and compliance are becoming more closely linked in multi-tenant interconnection environments. South America remains earlier in development, with Brazil as the key market, while the Middle East and Africa are moving faster because sovereign cloud programs in Saudi Arabia and the UAE are turning policy mandates into physical network build-outs. The result is a broader geographic demand base for the leaf-spine switch market, with commercial and policy-driven projects now advancing at the same time across several regions.

Competitive Landscape

Cisco held 27.63% of total Ethernet switch revenue in Q4 2025, while Arista held 12.61% overall and 19% of the data center segment, which shows that the leaf-spine switch market remains consolidated among a small number of vendors at the top. NVIDIA also emerged as the third-largest data center switch vendor in Q4 2025 with a 15.24% share, supported by rapid growth in AI back-end switching built around Spectrum-X silicon. This creates a structure that is concentrated in premium deployments but still contested across the wider field, especially where open networking and ODM supply are gaining traction. Cisco and Arista kept their leading positions in hyperscale and enterprise revenue in 2025, while Celestica and NVIDIA together accounted for 50% of the Ethernet AI back-end switch segment. The competitive landscape in the leaf-spine switch market is therefore not defined by a single dominant company, but by a leading cluster of vendors with distinct strengths in silicon depth, systems design, and software strategy.

Strategic differentiation is now moving away from raw port count alone toward silicon roadmaps, optics integration, power efficiency, and software openness. Arista announced the XPO multi-source agreement in March 2026 for a 12.8 Tbps liquid-cooled pluggable optics module, demonstrating how the company is extending its role from switching hardware into the optical layer of AI fabrics. Cisco expanded its Secure AI Factory with the NVIDIA program in March 2026 to support Spectrum-6 silicon at 102.4T in the Cisco N9100 series, underscoring how strategic partnerships are becoming a direct competitive advantage in premium AI deployments.[5]Cisco, “Secure AI Factory with NVIDIA and N9100 Series,” Cisco Newsroom, cisco.com The Ultra Ethernet Consortium also released UEC 1.0 in June 2025, which supports hardware and software disaggregation, broadening the addressable space for open networking ODMs while putting margin pressure on tightly integrated approaches. In the leaf-spine switch market, that means incumbents need stronger platform integration and ecosystem depth to defend pricing as more buyers evaluate disaggregated stacks.

White-box manufacturers such as Accton, Celestica, Edgecore, and UfiSpace are gaining relevance where hyperscalers prioritize software-hardware separation and large-volume economics over full-stack vendor support. Huawei, H3C, and Ruijie remain important within China, where export controls on 400G and above equipment have reshaped the addressable opportunity for several North American vendors. Supermicro is not a core competitive reference for this market because switching is a secondary business within a broader server and storage portfolio, while Wistron NeWeb Corporation and Inventec Network are more relevant comparables in white-box leaf-spine supply. The deeper supply chain also matters because Broadcom and Marvell together held a very large share of merchant ASIC supply in 2025, keeping silicon concentration a real strategic risk for vendors and buyers alike. The leaf-spine switch market, therefore, combines high concentration in top-tier branded systems with fragmentation across ODMs, regional suppliers, and open networking specialists that are still fighting for the next layer of share.

Leaf-Spine Switch Industry Leaders

Cisco Systems, Inc.

Arista Networks

NVIDIA Corporation

Huawei Technologies Co., Ltd.

Dell Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Google published details of its Virgo data center network, linking 134,000 TPU chips with 47 petabits per second of bisectional bandwidth in a flat two-layer design, marking the first public disclosure of a petabit-scale, two-tier leaf-spine fabric built exclusively for AI accelerator interconnect.

- March 2026: Arista Networks announced the XPO multi-source agreement for a 12.8 Tbps liquid-cooled pluggable optics module delivering 204.8 Tbps per OCP rack unit, a 4x density improvement over 1600G-OSFP, targeting future AI fabric spine ports.

- March 2026: Cisco expanded the Secure AI Factory with NVIDIA program to support NVIDIA Spectrum-6 Ethernet silicon at 102.4T in the new Cisco N9100 series switches, extending AI factory deployments from central data centers to enterprise edge sites.

- October 2025: Arista Networks launched the R4 Series, including the 7800R4 modular spine, up to 576x800G, the 7280R4 fixed 32x800G spine, and the 7020R4 AI leaf switches, marking commercial availability of a full 800G AI fabric portfolio across leaf and spine roles.

Global Leaf-Spine Switch Market Report Scope

The Leaf-Spine Switch architecture is a network design commonly implemented in modern data centers and enterprise AI infrastructures. It ensures high bandwidth, low latency, and reliable performance. This architecture simplifies traffic flow and supports horizontal scaling, effectively addressing the limitations of traditional three-tier network models (core, aggregation, access).

The Leaf-Spine Switch Market Report is Segmented by Switch Role (Leaf Switches, and Spine Switches), Product Type (Fixed Configuration, and Modular Switches), Port Speed (Up to 25 GbE, More than 25 to 100 GbE, More than 100 to 400 GbE, and 800 GbE and Above), Data Center Type (Colocation Data Centers, Hyperscale / Cloud Service Provider Data Centers, Enterprise Data Centers, and Edge Data Centers), End User Industry (Cloud Service Providers, Telecommunication Providers, Large Enterprises, Government and Public Sector, and Other end user Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Leaf Switches | Top-of-Rack Leaf Switches |

| End-of-Row Leaf Switches | |

| Spine Switches | Fixed Spine Switches |

| Chassis-based Spine Switches |

| Fixed Configuration | 1U |

| 2U and Above | |

| Modular Switches | 4-slot to 8-slot |

| 10-slot and Above |

| Up to 25 GbE |

| More than 25 to 100 GbE |

| More than 100 to 400 GbE |

| 800 GbE and Above |

| Colocation Data Centers |

| Hyperscale / Cloud Service Provider Data Centers |

| Enterprise Data Centers |

| Edge Data Centers |

| Cloud Service Providers |

| Telecommunication Providers |

| Large Enterprises |

| Government and Public Sector |

| Other end user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Ireland | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Singapore | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Switch Role | Leaf Switches | Top-of-Rack Leaf Switches | |

| End-of-Row Leaf Switches | |||

| Spine Switches | Fixed Spine Switches | ||

| Chassis-based Spine Switches | |||

| By Product Type | Fixed Configuration | 1U | |

| 2U and Above | |||

| Modular Switches | 4-slot to 8-slot | ||

| 10-slot and Above | |||

| By Port Speed | Up to 25 GbE | ||

| More than 25 to 100 GbE | |||

| More than 100 to 400 GbE | |||

| 800 GbE and Above | |||

| By Data Center Type | Colocation Data Centers | ||

| Hyperscale / Cloud Service Provider Data Centers | |||

| Enterprise Data Centers | |||

| Edge Data Centers | |||

| By End User Industry | Cloud Service Providers | ||

| Telecommunication Providers | |||

| Large Enterprises | |||

| Government and Public Sector | |||

| Other end user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Netherlands | |||

| Ireland | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Singapore | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the leaf-spine switch market size through 2031?

The leaf-spine switch market size stood at USD 14.21 billion in 2025, reached USD 16.42 billion in 2026, and is forecast to reach USD 35.32 billion by 2031 at a 16.6% CAGR.

Which segment leads by switch role and which one grows fastest?

Leaf switches led with 66.14% of 2025 revenue, while spine switches are projected to grow the fastest at an 18.45% CAGR through 2031.

Why are hyperscalers so important to leaf-spine demand?

Cloud service providers held 44.32% of 2025 revenue, and their AI clusters require non-blocking east-west bandwidth, faster refresh cycles, and rapid adoption of 400G, 800G, and higher-density silicon.

Which region is growing fastest for new deployments?

Asia-Pacific is the fastest-growing region at an 17.52% CAGR through 2031, supported by sovereign compute programs, a broad data center pipeline, and rising enterprise open networking activity.

What is holding back wider 800G adoption?

The main barriers are fiber and connector upgrades, higher power draw, facility retrofit costs, and the shortage of teams that can operate EVPN-VXLAN and RoCE-based fabrics at scale.

How competitive is the vendor landscape?

The field is concentrated at the top with Cisco, Arista, and NVIDIA in strong positions, but it is still contested by ODMs, open networking suppliers, and regional vendors, especially in disaggregated environments.

Page last updated on: