Modular Chassis Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.72 Billion |

| Market Size (2031) | USD 21.33 Billion |

| Growth Rate (2026 - 2031) | 9.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modular Chassis Switch Market Analysis by Mordor Intelligence

The modular chassis switch market size is projected to expand from USD 12.56 billion in 2025 and USD 13.72 billion in 2026 to USD 21.33 billion by 2031, registering a CAGR of 9.23% between 2026 to 2031. Refresh cycles are accelerating as buyers treat modularity as a lever to sidestep import tariffs rather than merely a path to higher port density. Tariff exemptions that reward 20% United States content have moved decision-making away from purely technical criteria toward supply-chain and rules-of-origin considerations. Hyperscale operators are replacing fixed-configuration fabrics with liquid-cooled, hot-swappable line-cards that deliver 400G and 800G throughput while avoiding fresh import duty every time a speed bump ships. Meanwhile, enterprises in manufacturing and government hold on to 10 GbE line-cards for legacy equipment but increasingly view chassis modularity as insurance against component embargoes or sudden policy shifts.

Key Report Takeaways

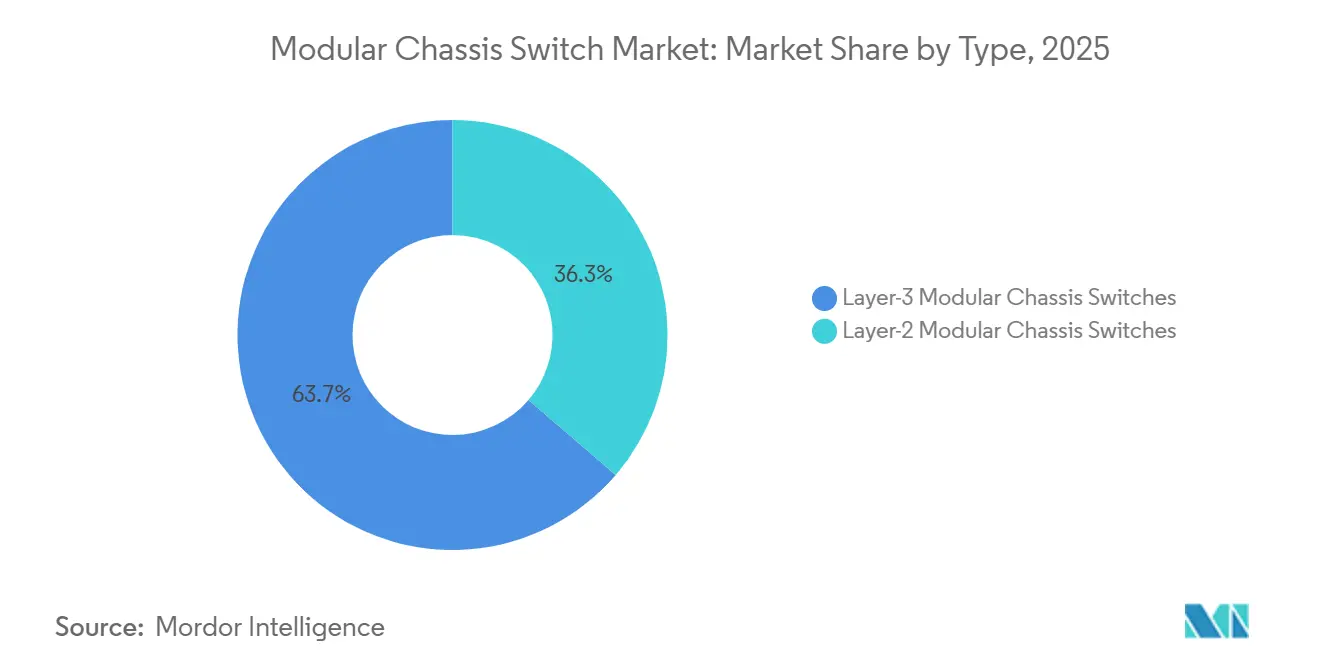

- By modular chassis switch type, Layer-3 platforms commanded 63.72% of 2025 revenue, while Layer-2 equipment is forecast to post a 7.86% CAGR through 2031.

- By port speed, 10 GbE held 36.75% share of 2025 revenue, but 100 GbE and above is projected to advance at a 14.44% CAGR between 2026-2031.

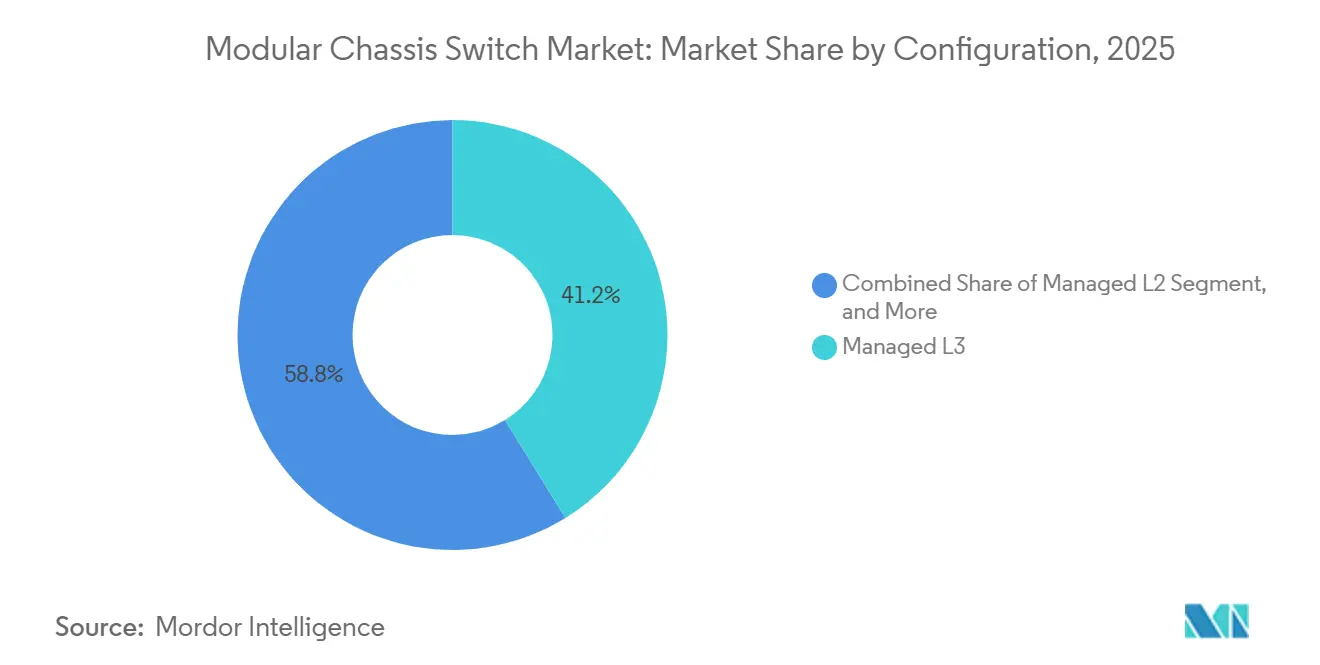

- By configuration, Managed L3 captured 41.20% revenue share in 2025 and is set to grow at an 8.69% CAGR to 2031.

- By end-user industry, manufacturing accounted for 34.00% of 2025 demand, while data centers are anticipated to expand at a 10.11% CAGR through 2031.

- By geography, North America led with 41.20% of 2025 spending, whereas Asia Pacific is estimated to rise at a 9.87% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Modular Chassis Switch Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cloud and 5G‑Driven Need for Scalable Core Switching | +2.8% | Global, concentrated in North America, Europe, Asia Pacific telco markets | Medium term (2-4 years) |

| Industrial 4.0 Retrofits in Harsh Environments | +1.9% | APAC manufacturing hubs, Europe, North America industrial corridors | Long term (≥ 4 years) |

| Hyperscale Data‑Center Migration to 400G/800G Architectures | +3.1% | North America, Asia Pacific, Europe hyperscale regions | Short term (≤ 2 years) |

| Tariff‑Circumvention Via Field‑Replaceable Modules | +0.9% | United States, Canada, European Union | Short term (≤ 2 years) |

| Open‑Network Switch OS Ecosystems Boosting Chassis Refresh | +1.6% | Global hyperscale cloud and telco operators | Medium term (2-4 years) |

| AI/ML Workload Growth is Driving Demand for Deep Buffers, Telemetry, and Low Latency Best Met by Modular Chassis | +0.7% | North America, Asia Pacific, Europe hyperscale regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud and 5G-Driven Need For Scalable Core Switching

Telco operators are moving from discrete packet cores toward cloud-native 5G architectures that require chassis able to grow from metro edge to national hub without forklift upgrades. Three UK tripled its packet-core throughput to 9 Tbps in early 2025 by deploying modular switches that allow in-service line-card insertion, eliminating traffic drains during maintenance.[1]Ericsson Press Office, “Three UK Selects Ericsson to Build Largest Mobile Packet Core in Europe,” ERICSSON.COM Dell and Ericsson later validated a pre-integrated 5G Core running on Dell Telecom Infrastructure Blocks and Cisco Nexus fabrics, shrinking rollout timelines from months to weeks. BT’s plan to consolidate from 5,600 exchanges to roughly 1,000 sites further concentrates switching capacity, favoring high-slot-count chassis with efficient power and cooling.

Industrial 4.0 Retrofits In Harsh Environments

As manufacturing plants transition from legacy fieldbus links to Ethernet, the demand for robust switches capable of withstanding harsh conditions, such as vibration, dust, and extreme temperatures, is driving the growth of modular chassis switches. Moxa’s PT-510 and PT-G510 lines address these needs by offering hot-swappable power supplies and ensuring IEC 61850-3 compliance, making them particularly suitable for substations.[2]Moxa Inc., “PT-510 and PT-G510 Series Industrial Switches,” MOXA.COM Similarly, Phoenix Contact’s FL SWITCH 2708 series, featuring conformal-coated line cards, enhances durability and extends service life, especially in challenging environments like chemical plants. Additionally, Belden’s BRS-5G, introduced in 2026, integrates cellular backhaul capabilities, catering to remote oil-and-gas sites where fixed fiber installations are not cost-effective. These advancements are propelling the adoption of modular chassis switches, as they provide the flexibility, reliability, and scalability required for Industrial 4.0 retrofits in demanding environments.

Hyperscale Data-Center Migration To 400G/800G Architectures

The rapid increase in east-west traffic driven by AI training clusters is accelerating the adoption of 400G and 800G modular chassis in hyperscale data centers, particularly for the spine layer. Arista's 7800R4, integrated with its liquid-cooled XPO optics, delivers a remarkable 204.8 Tbps switching capacity within a compact 1U design, addressing the growing demand for high-performance solutions. Huawei's XH16800, launched in 2025, marked a significant milestone as China's first 800G production chassis, targeting the expansive CNY 226.8 billion local switching market. Additionally, Edgecore's AIS1600-64O, powered by Broadcom's Tomahawk 6, provides a cost-effective alternative with 102.4 Tbps output, appealing to open-network buyers. These advancements in modular chassis technology are enabling hyperscalers to efficiently manage increasing data traffic, reduce latency, and optimize network scalability, thereby driving the growth of this market segment.

Tariff-Circumvention Via Field-Replaceable Modules

U.S. regulations that exempt equipment with 20% domestic content have created opportunities for companies to optimize costs by avoiding tariffs on components such as line-cards, power supplies, and optics. Cisco, for instance, responded to the imposition of 25% tariffs by relocating 80% of its manufacturing operations out of China. This shift, coupled with the ability of modular chassis switch buyers to import chassis under one tariff code while sourcing duty-free, U.S.-made line-cards under another, has significantly reduced costs and enhanced supply chain flexibility. Similarly, in Europe, rules of origin enable cost advantages when chassis are assembled in Poland and integrated with German line-cards and Dutch optics. These factors are collectively driving the adoption of modular chassis switches, as businesses increasingly leverage such regulatory frameworks to optimize production and reduce expenses.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Upfront CAPEX Versus Fixed Switches | -1.2% | Global, acute in Latin America, Africa, Southeast Asia, SMBs worldwide | Short term (≤ 2 years) |

| Rapid Silicon and Optics Obsolescence | -1.6% | North America and Europe hyperscale early adopters | Short term (≤ 2 years) |

| Integration‑Security Risks in Multi‑Vendor Modular Builds | -0.5% | Government, defense, financial services in North America, Europe, APAC | Medium term (2-4 years) |

| Semiconductor Lead Times Over 40 Weeks for High‑End Switch ASICs Cause Procurement Uncertainty and Chassis Upgrade Delays | -0.4% | Global, especially North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX Versus Fixed Switches

The high upfront capital expenditure (CAPEX) associated with modular chassis switches is significantly restraining their market growth. A 48-port 10 GbE modular chassis is priced between USD 40,000 and 60,000, which is approximately three times the cost of a comparable fixed switch. This substantial price difference forces cash-constrained enterprises to delay necessary upgrades, despite the potential for long-term operational expenditure (OPEX) savings. Extreme Networks, in its 2025 Form 10-K, reported a decline in modular revenue as campus buyers increasingly opted for more cost-effective stackable alternatives. Furthermore, while leasing models provide some financial flexibility, they are primarily viable in mature credit markets. Consequently, regions such as Latin America and Africa, where credit markets are less developed, continue to rely on lower-cost fixed gear, further limiting the adoption of modular chassis switches.

Rapid Silicon And Optics Obsolescence

In April 2026, Arista introduced the XPO transceiver, which reduced operating temperatures by 25°C. This innovation immediately diminished the value of air-cooled 400G chassis shipped in 2024, as they became less competitive in terms of efficiency. Similarly, Broadcom's Tomahawk 6 silicon achieved a performance benchmark of 102.4 Tbps in 2025. However, the company has already announced plans for a 204.8 Tbps successor by 2027, significantly shortening the amortization period for existing technologies. These rapid advancements in silicon and optics are creating challenges for the modular chassis switch market. Telcos and government organizations, which typically plan investments over a seven-year horizon, face the risk of stranded assets as their existing infrastructure becomes obsolete faster than anticipated. This accelerated pace of technological evolution is restraining the growth of modular chassis switches, as buyers are increasingly cautious about committing to long-term investments in hardware that may quickly lose its relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Routing-Capable Layer-3 Platforms Dominate Growth

Layer-3 modular chassis switches held 63.72% of global 2025 revenue, reflecting deep reliance on MPLS and BGP for aggregation. This share translates into the single largest slice of the modular chassis switch market share in the base year. Juniper’s QFX5250, now under Hewlett Packard Enterprise, extends Layer-3 reach to AI fabrics with ultra-low-latency telemetry, while Cisco’s IE3500 combines TSN and PTPv2 to converge IT and OT traffic. Vendors are bundling micro-burst buffering, segment routing, and flow-aware hashing to keep latency under one microsecond, a requirement emerging in GPU training clusters.

Layer-2 chassis appeal to industrial and campus buyers who value simplicity over routing scale. Despite representing a smaller portion of the modular chassis switch market size, Layer-2 boxes are forecast for a healthy 7.86% CAGR on the back of Industrial Ethernet migrations. Moxa and Phoenix Contact are shipping fanless, conformal-coated Layer-2 models certified for IEC 61850-3 substations, proving that deterministic Ethernet can thrive without heavyweight routing stacks. Flexible licensing now lets operators unlock Layer-3 features later, blurring boundaries and future-proofing early Layer-2 investments.

By Port Speed: 400G And 800G Drive Triple-Digit Slot Adoption

Hyperscalers are retrofitting 400G leaf-spine fabrics and preparing for 800G, driving the 100 GbE and above band to a projected compound annual growth rate (CAGR) of 14.44% through 2031. Edgecore’s DCS520, featuring 64 × QSFP56-DD ports and delivering 25.6 Tbps, positions its white-box chassis as a cost-effective alternative, priced 30-40% lower than branded competitors.[3]Edgecore Networks, “DCS520,” EDGE-CORE.COM Similarly, Dell’s PowerSwitch, powered by NVIDIA Spectrum-6, achieves an impressive 102.4 Tbps, showcasing that merchant-silicon latency can now compete with proprietary ASICs.[4]Edgecore Networks, “APS800-16O,” EDGE-CORE.COM

Legacy 10 GbE still accounted for 36.75% of 2025 revenue as government and education sectors lag on server-NIC upgrades. This is primarily due to the slower adoption of server-NIC upgrades in sectors such as government and education. These segments play a crucial role in sustaining the modular chassis switch market, as the reuse of existing optics and cabling often outweighs the demand for higher performance. However, with companies like Sumitomo Electric and Fujikura tripling their optical fiber production capacity to support 800G and 1.6T interconnects, the economic viability of sub-100G platforms is expected to diminish before the end of the decade, further influencing the market dynamics.

By Configuration: Managed L3 Sets The Automation Pace

Managed L3 platforms captured 41.20% of 2025 spend and are on track for an 8.69% CAGR as intent-based networking eliminates CLI toil. This growth is fueled by the adoption of intent-based networking, which significantly reduces reliance on CLI-based operations. Products like Edgecore’s APS800-16O, powered by Xsight Labs' X2 silicon, highlight advancements such as P4 programmable data planes that enable real-time weighted dynamic load balancing.[5]Dell Technologies, “PowerSwitch with NVIDIA Spectrum-6,” DELL.COM Additionally, cloud-managed solutions from companies like Extreme and Aruba leverage SaaS subscription models, allowing these platforms to efficiently penetrate branch networks without requiring on-site personnel. These factors position Managed L3 platforms as a critical component in the modular chassis switch market, particularly as enterprises increasingly align their networking strategies with AI and analytics-driven roadmaps.

Managed L2 units maintain a strong foothold in the manufacturing sector, where their ability to deliver deterministic forwarding and IGMP snooping provides a competitive edge over the flexibility offered by BGP. These units are essential for environments requiring precise and reliable network performance. On the other hand, unmanaged and smart-lite chassis, which have traditionally served pop-up retail and small clinics, are witnessing a decline in demand. This is largely due to the growing emphasis on zero-trust security frameworks, which prioritize authenticated ports, thereby reducing the addressable market for these solutions. Consequently, the modular chassis switch market is increasingly shifting toward Managed L3 platforms, as their advanced capabilities and alignment with modern enterprise requirements make them indispensable for future-ready networking infrastructures.

By End-User Industry: Data Centers Eclipse Manufacturing

Manufacturing, driven by advancements in automotive and semiconductor automation, is projected to account significantly of the 2025 demand. However, data centers are expected to grow at a faster pace, fueled by the increasing deployment of GPU clusters. Cushman and Wakefield report a significant shift in the Asia Pacific region, with a 19.4 GW pipeline transitioning from brownfield retrofits to large-scale greenfield hyperscale campuses. India, in particular, is emerging as a key player, planning to expand its capacity from 1.5 GW to an impressive 10 GW by 2030. This expansion is driving substantial demand for 400G and 800G line-card orders, which are critical components in modular chassis switches, enabling high-speed data transmission and scalability.

The government and defense sectors, while smaller in volume, demand highly specialized solutions. For instance, the U.S. Department of Defense's February 2026 tender specifies sub-5 ns latency fabrics, necessitating custom ASICs and FIPS 140-2 certification. These stringent requirements are pushing innovation in modular chassis switches, as they must meet high-performance standards while ensuring security and reliability. Similarly, telecom service providers are playing a pivotal role in the growth of modular chassis switches. By integrating dual-mode 5G cores onto modular chassis, they enable seamless software upgrades, reducing operational costs and eliminating the need for physical interventions like truck rolls. This adaptability and efficiency make modular chassis switches a cornerstone in supporting the evolving needs of these industries.

Geography Analysis

North America accounted for 41.20% of 2025 revenue as hyperscalers clustered in Virginia, Oregon, and Texas ordered 400G liquid-cooled chassis. These regions serve as critical hubs for hyperscale data centers, underscoring their pivotal role in the market. Cisco's strategic decision to relocate 80% of its production to Mexico and Vietnam significantly enhanced operational efficiency by reducing lead times and minimizing tariff exposure, thereby strengthening the advantages of regional sourcing. Additionally, while Canada's multi-tenant colocation growth remains comparatively slower, it holds a strategic position in the market due to its seamless duty-free integration with U.S. component manufacturers, which supports cost-effective and efficient supply chain operations.

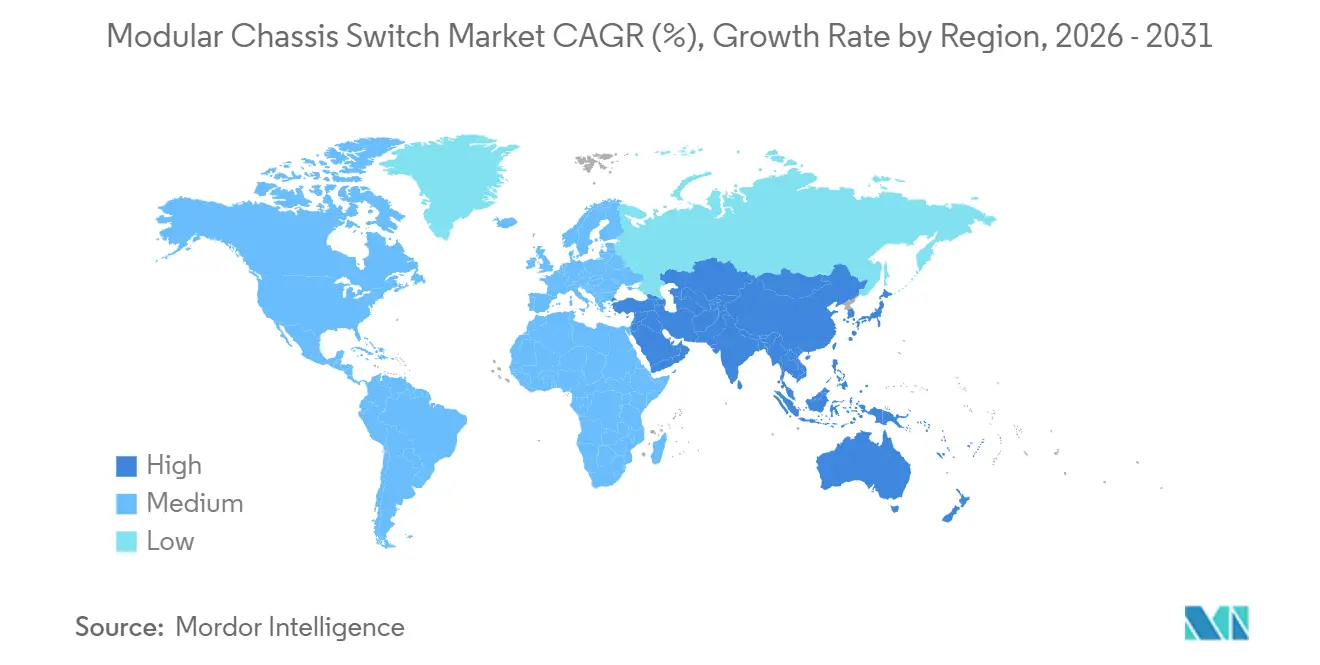

Asia Pacific is projected to register a 9.87% CAGR, the fastest worldwide. China’s CNY 226.8 billion (USD 31.8 billion) data-center switching outlay in 2025 sets a high base, yet India and Malaysia are adding capacity even faster. Mumbai’s projected jump toward 2 GW installed power by 2028 alone underpins sustained chassis orders, while Johor’s 124% pipeline growth in 2025 cements Southeast Asia as an emerging fabrication hub. Sumitomo Electric’s USD 700 million optical-interconnect investment and Fujikura’s USD 2.1 billion fiber expansion position Japanese suppliers to serve the 800G ramp.

Europe sits between legacy and next-gen deployments. Industrial automation in Germany and Italy favors ruggedized Layer-2 chassis, whereas hyperscale data centers in Frankfurt and Amsterdam order 800G spines to match U.S. peers. BT’s exchange consolidation will funnel more traffic into fewer buildings, prompting high-slot-count chassis orders through the 2030s. South America and the Middle East and Africa lag on total spend, but Brazil’s automotive revamp and Saudi Arabia’s NEOM smart-city build-out create spot markets for IEC-compliant modular gear.

Competitive Landscape

In the modular chassis switch market, Cisco, Huawei, and Arista maintain a significant share of the global revenue. A notable shift occurred in 2025 when Hewlett Packard Enterprise (HPE) acquired Juniper Networks for USD 14 billion. This strategic acquisition doubled HPE’s networking revenue and expanded its portfolio with Juniper’s QFX and PTX chassis lines, along with Mist AI capabilities. However, regulatory scrutiny from the U.S. Department of Justice required HPE to divest its Instant On WLAN line and license the Mist AI Ops source code to competitors, ensuring market equilibrium and preventing supply disruptions. Meanwhile, Arista has accelerated its growth through advancements in optics, with its XPO liquid-cooled ecosystem surpassing 100 partners by early 2026. This ecosystem has strengthened Arista’s competitive position in high-performance data center environments, supported by its 204.8 Tbps back-end fabrics.

White-box providers such as Edgecore and Accton are leveraging Broadcom’s Tomahawk 6 silicon and open network operating systems (NOS) like SONiC to deliver chassis solutions priced 30-40% lower than branded incumbents, while maintaining line-rate throughput. This aggressive pricing strategy appeals to hyperscale operators and enterprises seeking cost efficiency without compromising performance. Concurrently, Nokia and Ericsson are strengthening their positions in the telecommunications segment by bundling SR Linux and dual-mode control planes with high-availability chassis to support 5G core deployments. Their focus on carrier-grade reliability and integration with telecom infrastructure makes them preferred partners for operators modernizing their networks. Emerging players such as Xsight Labs are further disrupting the market by introducing P4-programmable silicon capable of offloading congestion-aware load balancing for AI training clusters. This innovation highlights the growing importance of programmable architectures in environments requiring flexibility and real-time optimization.

Certification and compliance are increasingly influencing competitive dynamics in the modular chassis switch market. Vendors achieving standards such as Common Criteria EAL4+, FIPS 140-2, or IEC 61850-3 can command premium margins in government and industrial bids, where supply chain assurance and security compliance outweigh raw port density. These certifications act as trust signals, particularly in sensitive deployments where resilience and regulatory adherence are critical. Conversely, buyers prioritizing open-source flexibility and cost efficiency are gravitating toward vendors like Dell, Edgecore, and Accton, mitigating risk through multi-vendor NOS portability. This bifurcation of demand underscores how the market is dividing between compliance-driven premium buyers and cost-conscious adopters of open ecosystems. Together, these trends illustrate a market landscape where scale, innovation, and certification are as critical as raw performance, shaping the competitive trajectory of the modular chassis switch segment.

Modular Chassis Switch Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Arista Networks, Inc.

Hewlett Packard Enterprise Company

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Arista Networks confirmed that its XPO liquid-cooled optics program surpassed 100 member companies, enabling 1U switches to reach 204.8 Tbps aggregate throughput.

- April 2026: Belden unveiled BRS-5G, the first industrial modular chassis integrating 5G backhaul for remote oil-and-gas sites.

- March 2026: Ericsson announced AI-RAN, a custom ASIC approach that bypasses external GPUs in future radio units.

- July 2025: Hewlett Packard Enterprise closed its USD 14 billion acquisition of Juniper Networks, doubling HPE networking revenue.

Global Modular Chassis Switch Market Report Scope

The Modular Chassis Switch Market refers to the industry focused on high-capacity, scalable network switches designed using modular chassis systems. These systems enable organizations, including large enterprises, telecom providers, and data centers, to achieve flexible port expansion, advanced network management, and dependable performance. Modular chassis switches are particularly valued for their ability to support growing network demands, ensure operational efficiency, and provide robust solutions for complex networking environments.

The Modular Chassis Switch Market Report is Segmented by Modular Chassis Switch Type (Layer-3 Modular Chassis Switches, and Layer-2 Modular Chassis Switches), Port Speed (1 GbE and below, 10 GbE, 25 GbE, 40 GbE, and 100 GbE and above), Configuration (Managed L3, Managed L2, Cloud-Managed, and Unmanaged), End-User Industry (Data Centers, Telecom, Industrial, Government, and Other End-User Industries), and Geography (North America, South America, Europe, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Layer-3 Modular Chassis Switches |

| Layer-2 Modular Chassis Switches |

| 1 GbE and Below |

| 10 GbE |

| 25 GbE |

| 40 GbE |

| 100 GbE and Above |

| Managed L3 |

| Managed L2 |

| Cloud-Managed / Controller-Managed |

| Unmanaged / Smart-Lite |

| Data Centers |

| Telecom Service Providers |

| Industrial and Manufacturing |

| Government and Defense |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of the Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Modular Chassis Switch Type | Layer-3 Modular Chassis Switches | ||

| Layer-2 Modular Chassis Switches | |||

| By Port Speed | 1 GbE and Below | ||

| 10 GbE | |||

| 25 GbE | |||

| 40 GbE | |||

| 100 GbE and Above | |||

| By Configuration / Management | Managed L3 | ||

| Managed L2 | |||

| Cloud-Managed / Controller-Managed | |||

| Unmanaged / Smart-Lite | |||

| By End-User Industry | Data Centers | ||

| Telecom Service Providers | |||

| Industrial and Manufacturing | |||

| Government and Defense | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of the Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will global spending on modular chassis switches be by 2031?

Mordor Intelligence projects the modular chassis switch market size to reach USD 21.33 billion by 2031, growing at a 9.23% CAGR over 2026-2031.

Which switch type currently dominates revenue?

Layer-3 routing-capable chassis commanded 63.72% of 2025 revenue, the highest share according to Mordor Intelligence.

What speed tier is expanding the fastest?

Ports rated at 100 GbE and above are forecast to advance at a 14.44% CAGR through 2031 as AI fabrics migrate to 400G-800G bandwidth, states Mordor Intelligence.

Which end-user sector is set for the quickest growth?

Data centers are expected to post a 10.11% CAGR to 2031, outpacing manufacturing and telecom, per Mordor Intelligence.

Why are operators choosing modular platforms over fixed switches?

Modularity allows hot-swapping of line-cards to bypass evolving tariffs, integrate liquid-cooled optics, and align refresh cycles with ASIC roadmaps, lowering lifetime duty and downtime risk.

Page last updated on: