Layer Feed Additives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.80 Billion |

| Market Size (2031) | USD 6.20 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

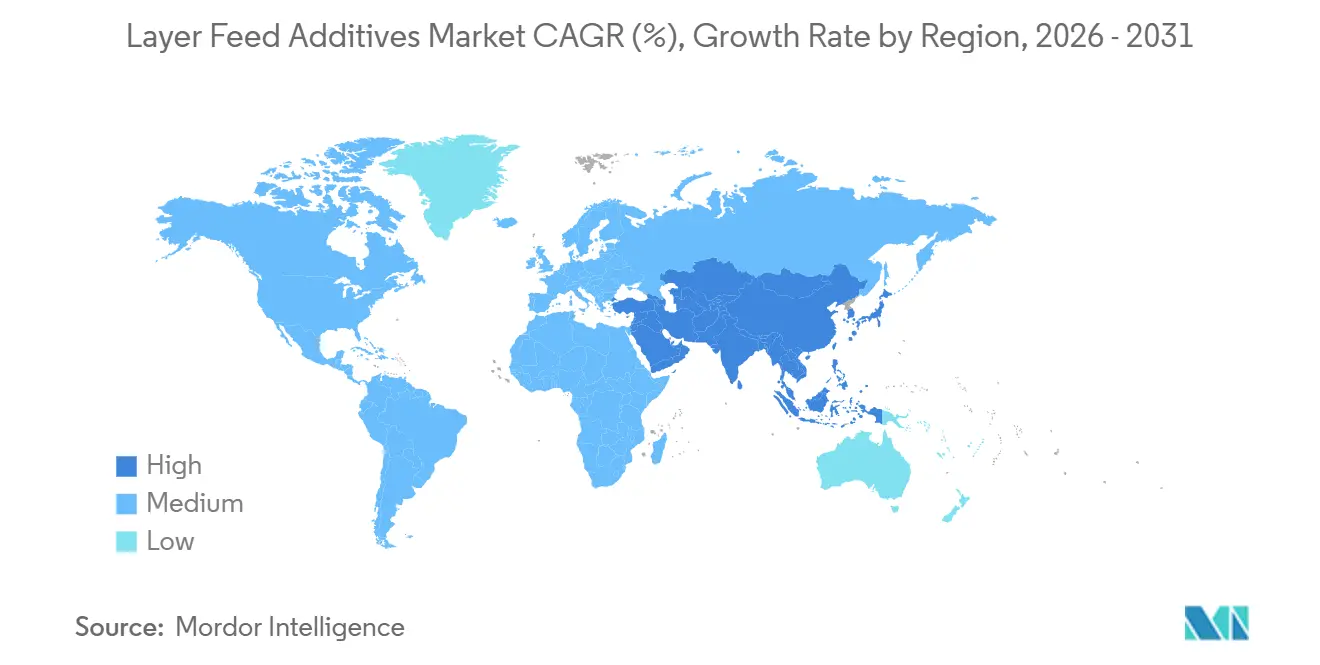

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

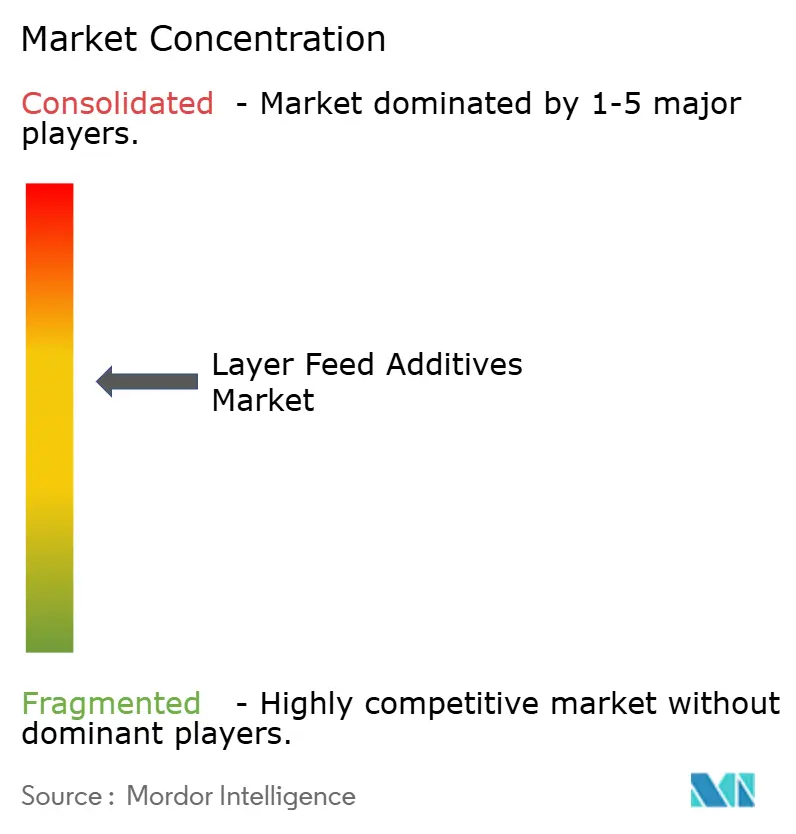

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Layer Feed Additives Market Analysis by Mordor Intelligence

The Layer Feed Additives Market size was valued at USD 4.57 billion in 2025 and is estimated to grow from USD 4.80 billion in 2026 to reach USD 6.20 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031). The market is moving on the back of steady egg demand, wider commercialization of layer farming in emerging countries, and stronger use of science-based nutrition in place of routine antibiotic-led programs. Producers are also spending more on targeted additive programs because longer laying cycles place greater pressure on shell quality, gut stability, liver health, and late-phase bird performance. Premium egg categories, including enriched and deeper-yolk products, are also lifting additive spending per metric ton of feed even in countries where flock growth is modest. The competitive structure of the layer feed additives market remains moderate, with multinational suppliers holding stronger positions in high-value specialties and regional suppliers competing more actively in price-sensitive vitamin and mineral categories. Cost swings in amino acids, disease-related flock disruption, and soy-linked compliance risks can pressure demand in the near term, but they do not change the longer demand pattern supporting the layer feed additives market.

Key Report Takeaways

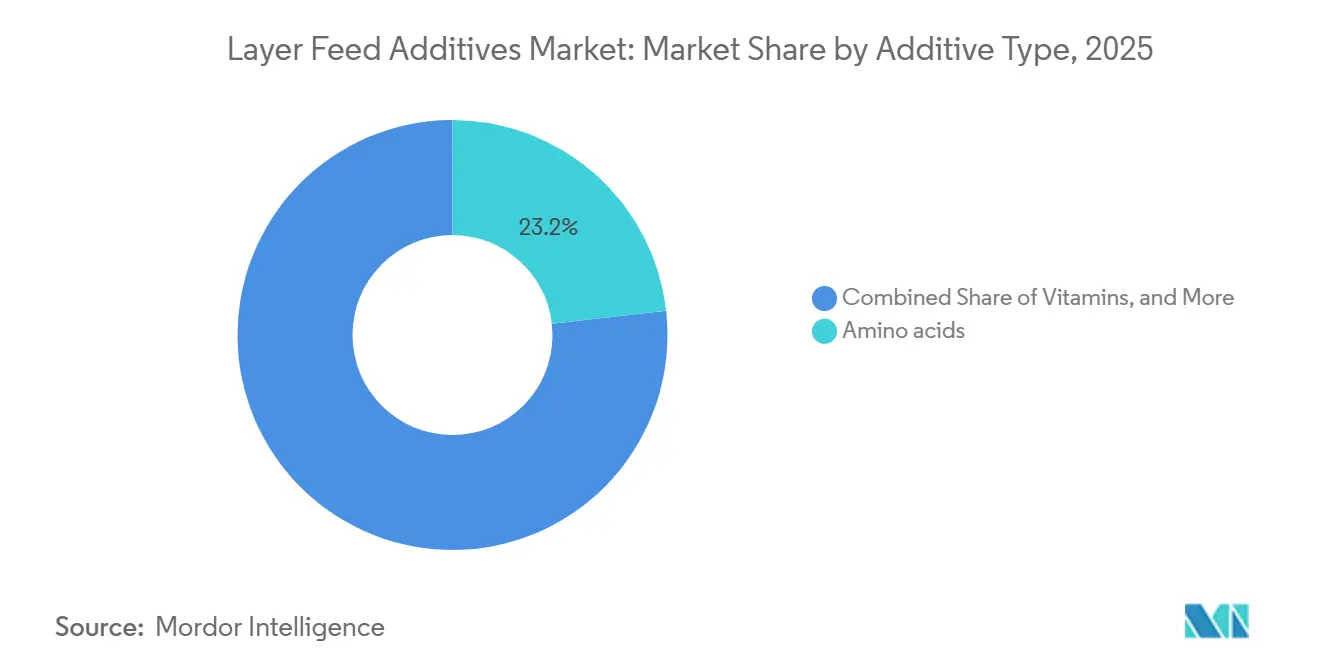

- By additive type, amino acids were the largest segment, accounting for 23.2% of the layer feed additives market in 2025, while acidifiers registered as the fastest-growing segment, with a projected 5.9% CAGR through 2031.

- By geography, Asia-Pacific held the largest share at 40.8% of the layer feed additives market share in 2025, and it is also the fastest-growing regional segment, with a projected 4.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Layer Feed Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global egg consumption and commercial layer flock expansion | +1.6% | Global, with highest intensity in Asia-Pacific and Africa | Medium term (2-4 years) |

| Antibiotic reduction driving probiotic, phytogenic, and organic-acid adoption | +1.3% | Global, with strongest regulatory influence in Europe, North America, and South Korea | Medium term (2-4 years) |

| Precision nutrition focus to improve feed efficiency and laying performance | +1.0% | North America, Europe, and Asia-Pacific core markets | Medium term (2-4 years) |

| Industrialized egg production scaling in emerging markets | +0.9% | Asia-Pacific, Africa, and South America | Long term (≥ 4 years) |

| Longer laying cycles increasing demand for shell, liver, and gut health supplements | +0.7% | Global, with strongest effect in Europe, North America, and China | Medium term (2-4 years) |

| Premium yolk-color and enriched-egg positioning lifting additive value | +0.5% | Europe, North America, Japan, South Korea, and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Egg Consumption and Commercial Layer Flock Expansion

Rising egg consumption continues to support flock expansion, and that directly increases the volume base for the layer feed additives market. The strongest expansion is taking place in countries where poultry systems are moving from dispersed smallholder production toward larger integrated farms that depend on more standardized feed programs. That change matters because commercial layer units use deeper additive stacks than backyard systems, especially in amino acids, enzymes, vitamins, minerals, and gut-health products. It also raises the average value of every metric ton of feed since modern operators focus on consistency, egg quality, and feed efficiency rather than basic survival performance alone. Suppliers that track only bird numbers can miss the larger opportunity because formulation complexity is rising at the same time as flock scale. This combined increase in flock count and additive intensity remains one of the clearest reasons the layer feed additives market is set to expand through 2031.

Antibiotic Reduction Driving Probiotic, Phytogenic, and Organic Acid Adoption

The move away from routine in-feed antibiotic growth promoters has strengthened demand for probiotics, phytogenics, and organic acids across the layer feed additives market. The European Commission authorized a preparation containing Bacillus subtilis DSM 32324, Bacillus subtilis DSM 32325, and Bacillus amyloliquefaciens DSM 25840 for all poultry species for laying or breeding in December 2025, which shows that the regulatory framework is still opening room for targeted microbial solutions[1]Source: European Commission, “Commission Implementing Regulation (EU) 2025/2576 of 18 December 2025 Concerning the Authorisation of a Preparation of Bacillus subtilis DSM 32324, Bacillus subtilis DSM 32325 and Bacillus amyloliquefaciens DSM 25840 as a Feed Additive for All Poultry Species for Laying or for Breeding,” eur-lex.europa.eu. The commercial effect is not limited to simple one-for-one replacement because flocks at peak lay often need layered programs that combine probiotics, acidifiers, and plant-based actives in the same protocol. That raises additive spending per bird and tends to favor suppliers with broad functional portfolios over single-category companies. Markets in South and Southeast Asia are also moving along this path as residue control, export requirements, and local enforcement become stricter. This shift is helping the layer feed additives market move toward higher-value multifunctional blends rather than isolated ingredient sales.

Precision Nutrition Focus to Improve Feed Efficiency and Laying Performance

Precision nutrition is making performance outcomes easier to measure, and that is improving the value case for premium products in the layer feed additives market. Nutritionists now rely more heavily on digital formulation tools, ingredient testing, and flock-level production data, which allows amino acid and enzyme programs to be adjusted more tightly to actual bird needs. Methionine and lysine remain central to this shift because they affect egg mass, feed conversion, and cost control in large layer operations. Novus International, Incorporated presented 5 poultry nutrition studies in January 2026 showing that replacing inorganic trace minerals with bis-chelated sources improved egg quality measures such as egg and yolk weights during peak lay[2]Source: Novus International, Incorporated, “Five New Studies at IPSF 2026 Show How Targeted Nutrition Helps Poultry Producers Get More from Feed,” novusint.com. As these tools spread, lower-grade commodity inputs become easier to benchmark and easier to replace when they fail to deliver repeatable outcomes. This keeps the layer feed additives market tied closely to measurable return on feed efficiency and laying performance rather than simple ingredient cost.

Industrialized Egg Production Scaling in Emerging Markets

Industrialized egg production is expanding across several emerging economies, and that is widening the customer base for the layer feed additives market. Producers in India, Indonesia, Nigeria, and parts of South America are moving toward controlled housing, more consistent feed management, and tighter flock monitoring. This transition usually starts with better premix use, but it often widens into full programs that include enzymes, organic acids, pigments, toxin-control products, and performance-support blends. The commercial opportunity is strongest early in the modernization cycle because suppliers that win the first technical relationship often stay embedded in the formulation process for years. Tropical feed conditions also create room for tailored products that handle heat, storage stress, microbial pressure, and variable ingredient quality more effectively. For that reason, the layer feed additives market is benefiting not only from rising scale in emerging regions but also from a durable upgrade in formulation discipline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexity and fragmented approval frameworks | -0.5% | Global, with compliance pressure most visible in Europe, China, and South and Southeast Asia | Long term (≥ 4 years) |

| Volatility in raw material prices across key feed additive categories | -0.8% | Global, especially North America and Europe | Short term (≤ 2 years) |

| European Union Deforestation Regulation (EUDR)-linked compliance costs and soy supply chain disruption | -0.4% | Europe and South American exporting countries, with spillover into the United Kingdom and Switzerland | Medium term (2-4 years) |

| Import constraints and tariff-driven supply chain risks | -0.3% | North America and Europe, with secondary effects in Asia-Pacific export corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity and Fragmented Approval Frameworks

Regulatory complexity remains a drag on the layer feed additives market because new ingredients do not move through global approval systems at the same speed. A product that is established in one country can still face a separate registration path, additional data requests, or delayed commercial use in another. That slows the launch of newer bioactive and functional products, especially in categories where long safety histories are still being built. The burden is heavier for smaller suppliers because dossier preparation, regulatory staffing, and follow-up testing require time and capital that many regional companies do not have. It also creates an advantage for large multinational players that can carry longer approval cycles without pulling back innovation spending. The result is a layer feed additives market where premium growth remains attractive, but route-to-market timing can still limit how quickly new concepts scale.

Volatility in Raw Material Prices Across Key Feed Additive Categories

Raw material price volatility continues to pressure the layer feed additives market, especially in amino acids, vitamins, and other categories with concentrated supply chains. The United States Department of Agriculture's Economic Research Service noted continued feed market pressure and changing cost conditions in its January 2026 feed outlook, reinforcing broader concerns about input volatility in animal nutrition chains. Methionine is particularly exposed because its production depends on petrochemical inputs and complex synthetic routes rather than solely on fermentation economics. When those costs rise sharply, additive manufacturers cannot always pass the full increase through to customers, particularly in price-sensitive emerging markets. That squeezes suppliers' margins and can lead feed producers to delay upgrades or reformulate toward lower-cost combinations. Even so, the long-term structure of the layer feed additives market still favors precision use rather than broad pullback, which is why volatility slows growth more than it changes direction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive Type: Amino Acids Anchor Formulations but Specialty Categories Are Accelerating

Amino acids held the largest market share of 23.2% in 2025 in the layer feed additives market, confirming their central role in commercial layer diet formulation. Methionine and lysine remain the core volume drivers because they directly affect feed efficiency, egg mass, and cost discipline in large flocks. Vitamins and minerals follow as a broad spending base because eggshell quality, calcium utilization, and late-cycle bird stability depend on dependable micronutrient support. Enzymes are also gaining greater prominence in routine formulations as producers seek better phosphorus use and improved nutrient release from raw materials. Probiotics, prebiotics, phytogenics, organic acids, antioxidants, pigments, and toxin-control products round out a category set that is now used more often in combination than in isolation across the layer feed additives market.

Acidifiers are the fastest-growing segment with a 5.9% CAGR through 2031. The layer feed additives market size linked to specialty categories is expanding faster in value than in physical volume because many functional products carry higher prices per kilogram than core amino acids. The European Commission authorized the preparation of 6-phytase produced with Aspergillus oryzae DSM 33737 for poultry for laying or reproduction in May 2026, reinforcing continued confidence in enzyme-led efficiency programs. Pigments and carotenoids hold premium pricing because yolk color remains a visible quality marker in many egg markets, especially where premium differentiation matters at retail level. Mycotoxin binders and detoxifiers show a more episodic pattern because demand strengthens when grain quality risk rises and contamination control becomes urgent. This mix means the largest segment by share still supports the commercial base, while specialty lines increasingly shape value capture across the layer feed additives industry.

Geography Analysis

Asia-Pacific held the largest 40.8% of the layer feed additives market share in 2025 and is also the fastest regional segment, with the layer feed additives market size for the region projected to advance at a 4.7% CAGR through 2031. China remains the biggest national demand center because of its very large layer base and its wide spread between highly advanced integrated farms and smaller regional producers. India is also moving deeper into the use of enzymes, organic acids, and precision nutrition as large operators modernize housing systems and extend productive cycles. Indonesia, Vietnam, and Thailand are still less advanced in additive sophistication, but adoption is rising quickly as export-linked supply chains tighten residue and drug-use standards. Japan and South Korea remain important high-value markets where enriched eggs and premium yolk standards support elevated per-bird additive spending.

Europe plays a crucial role in the layer feed additives market due to its intensive, technically advanced, and highly regulated layer industry. The region's production base drives strong demand for additives that enhance shell quality, gut health, and flock stability, particularly as housing systems continue to develop. The shift towards alternative housing systems, such as cage-free and free-range setups, has further increased the need for specialized feed additives to maintain productivity and animal welfare standards. However, stringent regulatory requirements, while potentially delaying the introduction of new products, enable premium pricing for validated and compliant solutions. These regulations also ensure that products meet high safety and efficacy standards, fostering trust among producers and consumers.

North America remains strategically important to the layer feed additives market because scale, biosecurity concerns, and commercial feed discipline all support regular additive use. As per United States Department of Agriculture National Agricultural Statistics Service (USDA NAS), the United States layer flock averaged 365 million birds in 2025, down 3% from the prior year, which reflected the disruption caused by Highly Pathogenic Avian Influenza. Mexico remains a valuable egg-producing country with strong demand for yolk-color and gut-health solutions, while Brazil and Argentina offer rising opportunity as retailer standards and export requirements lift formulation quality. Africa is still smaller in present value, but Nigeria, South Africa, and Egypt continue to build commercial layer capacity that should deepen demand for full additive programs through 2031.

Competitive Landscape

The layer feed additives market is moderately concentrated in premium specialties, but less consolidated in broader commodity categories, where regional suppliers remain active. Multinational companies maintain a stronger presence in areas where registration, fermentation, extraction, and technical service requirements create significant barriers to entry. This is particularly evident in segments such as amino acids, enzymes, carotenoids, and advanced functional blends, where factors like scale and thorough documentation are as critical as production costs. In contrast, commodity vitamins and minerals provide greater opportunities for regional blenders to leverage local relationships and compete on price. As a result, the layer feed additives market is characterized by a balance between global dominance in high-value niches and local competition in more standardized product categories.

The most important strategic shift came in February 2026, when DSM-Firmenich announced an agreement to divest its Animal Nutrition and Health business to CVC Capital Partners at a total enterprise value of EUR 3.7 billion (USD 4.0 billion), including the earlier sale of the Feed Enzyme Alliance stake for EUR 1.5 billion (USD 1.62 billion)[3]Source: dsm-firmenich, “dsm-firmenich Announces Agreement to Divest Animal Nutrition and Health to CVC Capital Partners,” live.euronext.com. In March 2026, Denkavit Ingredients and Adisseo France SAS expanded their collaboration in the Benelux region, adding more than 40 Adisseo products across gut health, feed preservation, and functional nutrition categories. In April 2026, Kemin Industries, Incorporated, introduced EDIE Generation 2, a precision chlorine dioxide application system designed for water quality monitoring and enhanced biosecurity in poultry operations. These moves show that consolidation, portfolio expansion, and on-farm systems support are all shaping the next phase of competition in the layer feed additives market.

The next competitive battleground is likely to center on suppliers that can connect products with technical service, performance data, and formulation support. Novus International, Incorporated, reinforced that model in January 2026 by presenting poultry studies linking targeted mineral strategies to measurable improvements in egg quality at peak lay. DSM-Firmenich also strengthened its manufacturing position in Brazil through its Sete Lagoas facility, inaugurated in October 2024, which added local production depth in a major poultry country. Even with these moves, the layer feed additives market is unlikely to become tightly concentrated across all categories, as regional suppliers still hold ground in simpler products, and customer relationships remain local.

Layer Feed Additives Industry Leaders

Cargill, Incorporated

Archer Daniels Midland Company

BASF SE

DSM-Firmenich AG

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Denkavit Ingredients and Adisseo France SAS expanded their collaboration in the Benelux region by introducing over 40 Adisseo products. These products span advanced additive categories, including gut health, feed preservation, and functional nutrition for poultry and laying hens.

- February 2026: DSM-Firmenich has agreed to sell its Animal Nutrition and Health division to CVC Capital Partners for EUR 3.7 billion (USD 4.0 billion), including the earlier Feed Enzyme Alliance sale to Novozymes. This move is anticipated to impact the global competitive landscape for vitamins, premixes, and functional feed additives, affecting layer additive supply chains in key regions.

- May 2024: Innovad Group has acquired Oligo Basics, a Brazilian manufacturer specializing in prebiotic and organic acid solutions, for an undisclosed amount exceeding USD 15 million. This acquisition strengthens Innovad's feed additive portfolio by integrating Oligo Basics' expertise in prebiotic and organic acid solutions for layers, creating a more comprehensive offering.

Global Layer Feed Additives Market Report Scope

A feed additive is a specialized ingredient or micro-substance intentionally added to animal feed in small quantities to enhance its overall nutritional value, flavor, and digestibility. Its primary purpose is to boost livestock health, support gut immunity, and improve overall growth and efficiency of meat or milk production.

The Layer Feed Additives Market Report is Segmented by Additive Type (Amino Acids, Vitamins, Minerals, Enzymes, Pigments, Probiotics, Prebiotics, Yeasts, Binders, Antioxidants, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Acidifiers | By Sub Additive | Fumaric Acid |

| Lactic Acid | ||

| Propionic Acid | ||

| Other Acidifiers | ||

| Amino Acids | By Sub Additive | Lysine |

| Methionine | ||

| Threonine | ||

| Tryptophan | ||

| Other Amino Acids | ||

| Antibiotics | By Sub Additive | Bacitracin |

| Penicillins | ||

| Tetracyclines | ||

| Tylosin | ||

| Other Antibiotics | ||

| Antioxidants | By Sub Additive | Butylated Hydroxyanisole (BHA) |

| Butylated Hydroxytoluene (BHT) | ||

| Citric Acid | ||

| Ethoxyquin | ||

| Propyl Gallate | ||

| Tocopherols | ||

| Other Antioxidants | ||

| Binders | By Sub Additive | Natural Binders |

| Synthetic Binders | ||

| Enzymes | By Sub Additive | Carbohydrases |

| Phytases | ||

| Other Enzymes | ||

| Flavors and Sweeteners | By Sub Additive | Flavors |

| Sweeteners | ||

| Minerals | By Sub Additive | Macrominerals |

| Microminerals | ||

| Mycotoxin Detoxifiers | By Sub Additive | Binders |

| Biotransformers | ||

| Phytogenics | By Sub Additive | Essential Oil |

| Herbs and Spices | ||

| Other Phytogenics | ||

| Pigments | By Sub Additive | Carotenoids |

| Curcumin and Spirulina | ||

| Prebiotics | By Sub Additive | Fructo Oligosaccharides |

| Galacto Oligosaccharides | ||

| Inulin | ||

| Lactulose | ||

| Mannan Oligosaccharides | ||

| Xylo Oligosaccharides | ||

| Other Prebiotics | ||

| Probiotics | By Sub Additive | Bifidobacteria |

| Enterococcus | ||

| Lactobacilli | ||

| Pediococcus | ||

| Streptococcus | ||

| Other Probiotics | ||

| Vitamins | By Sub Additive | Vitamin A |

| Vitamin B | ||

| Vitamin C | ||

| Vitamin E | ||

| Other Vitamins | ||

| Yeast | By Sub Additive | Live Yeast |

| Selenium Yeast | ||

| Spent Yeast | ||

| Torula Dried Yeast | ||

| Whey Yeast | ||

| Yeast Derivatives |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Australia | |

| Philippines | |

| Rest of Asia-Pacific | |

| Middle East | Iran |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | Egypt |

| Kenya | |

| South Africa | |

| Rest of Africa |

| Additive | Acidifiers | By Sub Additive | Fumaric Acid |

| Lactic Acid | |||

| Propionic Acid | |||

| Other Acidifiers | |||

| Amino Acids | By Sub Additive | Lysine | |

| Methionine | |||

| Threonine | |||

| Tryptophan | |||

| Other Amino Acids | |||

| Antibiotics | By Sub Additive | Bacitracin | |

| Penicillins | |||

| Tetracyclines | |||

| Tylosin | |||

| Other Antibiotics | |||

| Antioxidants | By Sub Additive | Butylated Hydroxyanisole (BHA) | |

| Butylated Hydroxytoluene (BHT) | |||

| Citric Acid | |||

| Ethoxyquin | |||

| Propyl Gallate | |||

| Tocopherols | |||

| Other Antioxidants | |||

| Binders | By Sub Additive | Natural Binders | |

| Synthetic Binders | |||

| Enzymes | By Sub Additive | Carbohydrases | |

| Phytases | |||

| Other Enzymes | |||

| Flavors and Sweeteners | By Sub Additive | Flavors | |

| Sweeteners | |||

| Minerals | By Sub Additive | Macrominerals | |

| Microminerals | |||

| Mycotoxin Detoxifiers | By Sub Additive | Binders | |

| Biotransformers | |||

| Phytogenics | By Sub Additive | Essential Oil | |

| Herbs and Spices | |||

| Other Phytogenics | |||

| Pigments | By Sub Additive | Carotenoids | |

| Curcumin and Spirulina | |||

| Prebiotics | By Sub Additive | Fructo Oligosaccharides | |

| Galacto Oligosaccharides | |||

| Inulin | |||

| Lactulose | |||

| Mannan Oligosaccharides | |||

| Xylo Oligosaccharides | |||

| Other Prebiotics | |||

| Probiotics | By Sub Additive | Bifidobacteria | |

| Enterococcus | |||

| Lactobacilli | |||

| Pediococcus | |||

| Streptococcus | |||

| Other Probiotics | |||

| Vitamins | By Sub Additive | Vitamin A | |

| Vitamin B | |||

| Vitamin C | |||

| Vitamin E | |||

| Other Vitamins | |||

| Yeast | By Sub Additive | Live Yeast | |

| Selenium Yeast | |||

| Spent Yeast | |||

| Torula Dried Yeast | |||

| Whey Yeast | |||

| Yeast Derivatives | |||

| Region | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| Italy | |||

| Netherlands | |||

| Russia | |||

| Spain | |||

| Turkey | |||

| United Kingdom | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Vietnam | |||

| Australia | |||

| Philippines | |||

| Rest of Asia-Pacific | |||

| Middle East | Iran | ||

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | Egypt | ||

| Kenya | |||

| South Africa | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of layer feed additives in 2026?

The layer feed additives market stands at USD 4.8 billion in 2026 and is projected to reach USD 6.2 billion by 2031 at a 5.22% CAGR.

Which additive type leads spending in layer nutrition?

Amino acids are the largest additive type, holding 23.2% share in 2025 because they remain essential for feed efficiency and egg mass control.

Which source segment is growing fastest in feed additives for laying hens?

Acidifiers additives are the fastest-growing source segment, with a projected 5.9% CAGR from 2026 to 2031, supported by clean-label and sustainability demand.

Why is Asia-Pacific the key growth region for this space?

Asia-Pacific is the largest regional segment with 40.8% share in 2025 and the fastest one through 2031, supported by expanding commercial layer systems in China, India, and Southeast Asia.

How are longer laying cycles changing additive demand?

Longer productive cycles raise demand for shell-quality minerals, liver-support products, and gut-health additives because older birds need tighter nutritional support to sustain output.

What is shaping competition among leading suppliers?

Competition is being shaped by portfolio consolidation, technical service depth, regulatory capability, and strategic moves such as DSM-Firmenich's divestment and Denkavit Ingredients' expanded collaboration with Adisseo France SAS.

Page last updated on: