LASIK Eye Surgery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

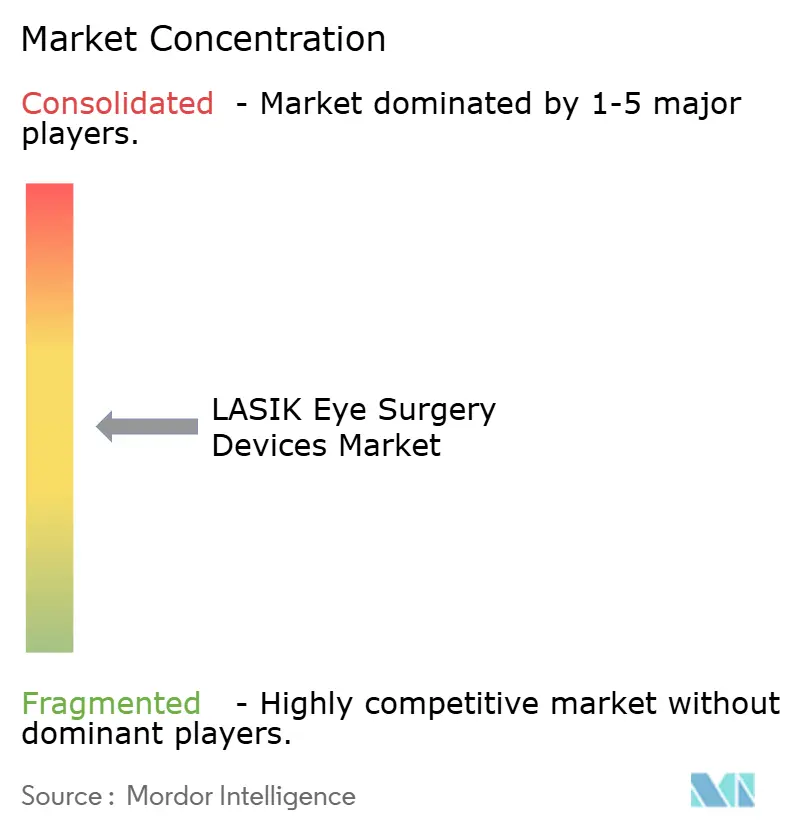

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LASIK Eye Surgery Devices Market Analysis by Mordor Intelligence

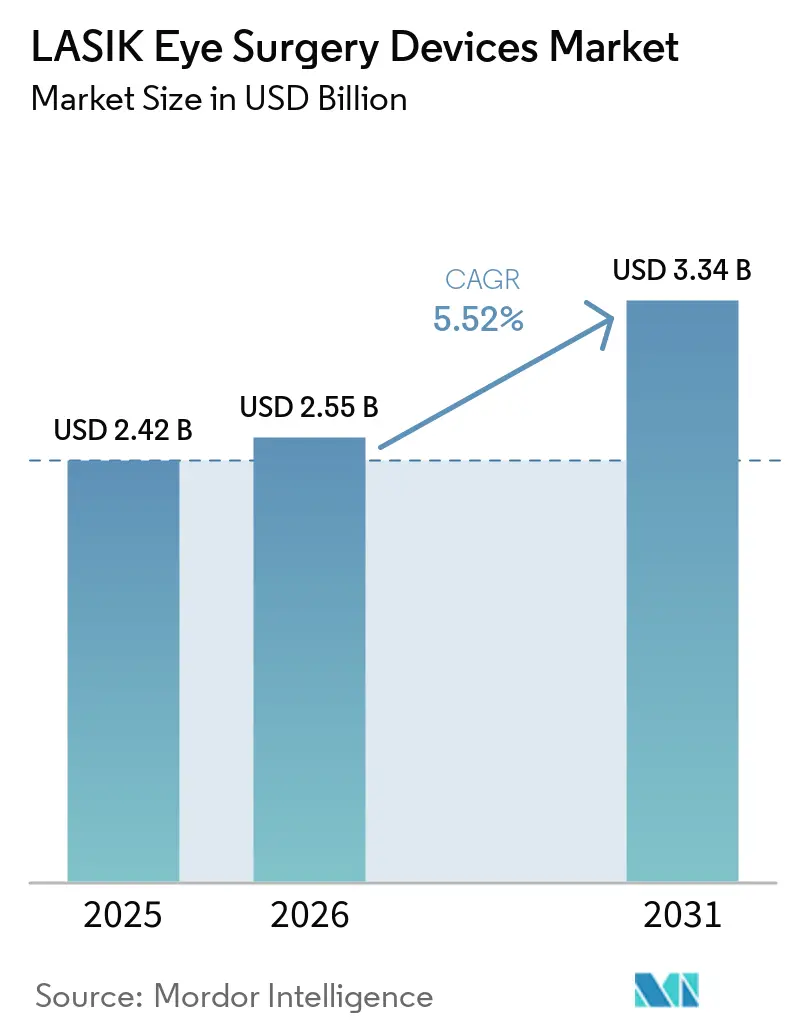

The LASIK Eye Surgery Devices Market size is expected to increase from USD 2.42 billion in 2025 to USD 2.55 billion in 2026 and reach USD 3.34 billion by 2031, growing at a CAGR of 5.52% over 2026-2031.

The market is being supported by a rising global pool of treatment-eligible patients as myopia and astigmatism continue to expand across younger populations, especially in urban Asia. Demand is also shifting toward integrated all-laser systems as refractive surgery centers look for better workflow consistency, stronger clinical outcomes, and tighter compatibility between diagnostics, planning software, and treatment platforms. Competitive activity remains focused on platform upgrades rather than basic device replacement, which is raising the importance of software-linked differentiation and premium treatment positioning. At the same time, insurance exclusions and stronger lens-based alternatives in high-myopia cases continue to limit full conversion of clinical need into procedure demand. The result is a market where growth is steady, premiumized, and increasingly concentrated around centers that can support advanced refractive workflows and higher patient throughput.

Key Report Takeaways

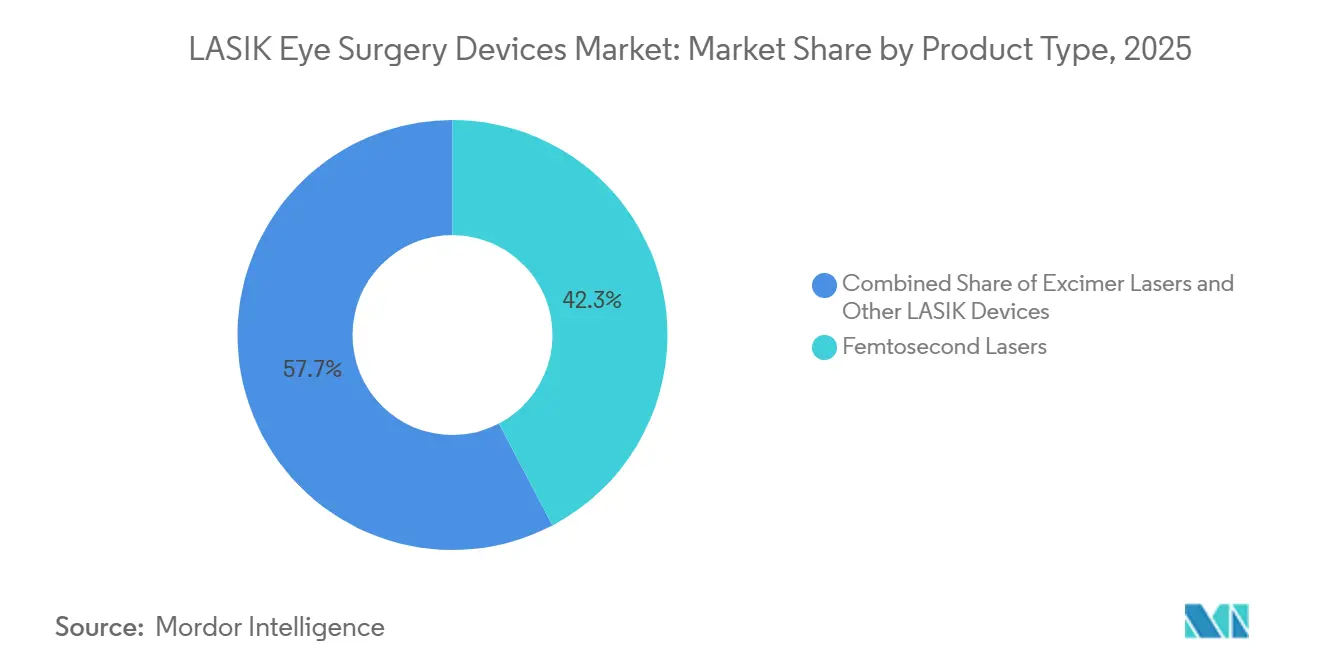

- By product type, femtosecond lasers held 42.31% revenue share in 2025, while excimer lasers are projected to grow at 7.38% through 2031.

- By technology, wavefront-guided LASIK accounted for 43.24% of revenue in 2025, while topography-guided LASIK is projected to expand at 6.52% through 2031.

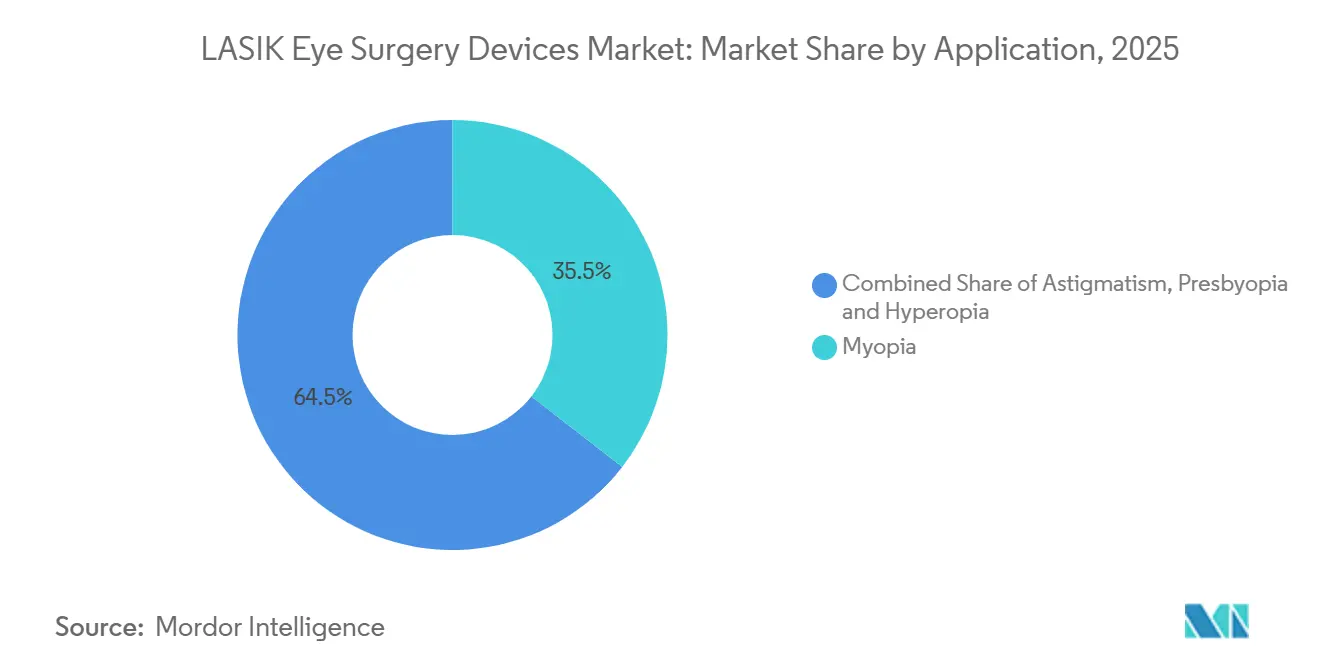

- By application, myopia correction represented 35.52% of revenue in 2025, while astigmatism correction is projected to grow at 7.25% through 2031.

- By end user, eye clinics held 38.22% revenue share in 2025, while ambulatory surgical centers are projected to expand at 7.65% through 2031.

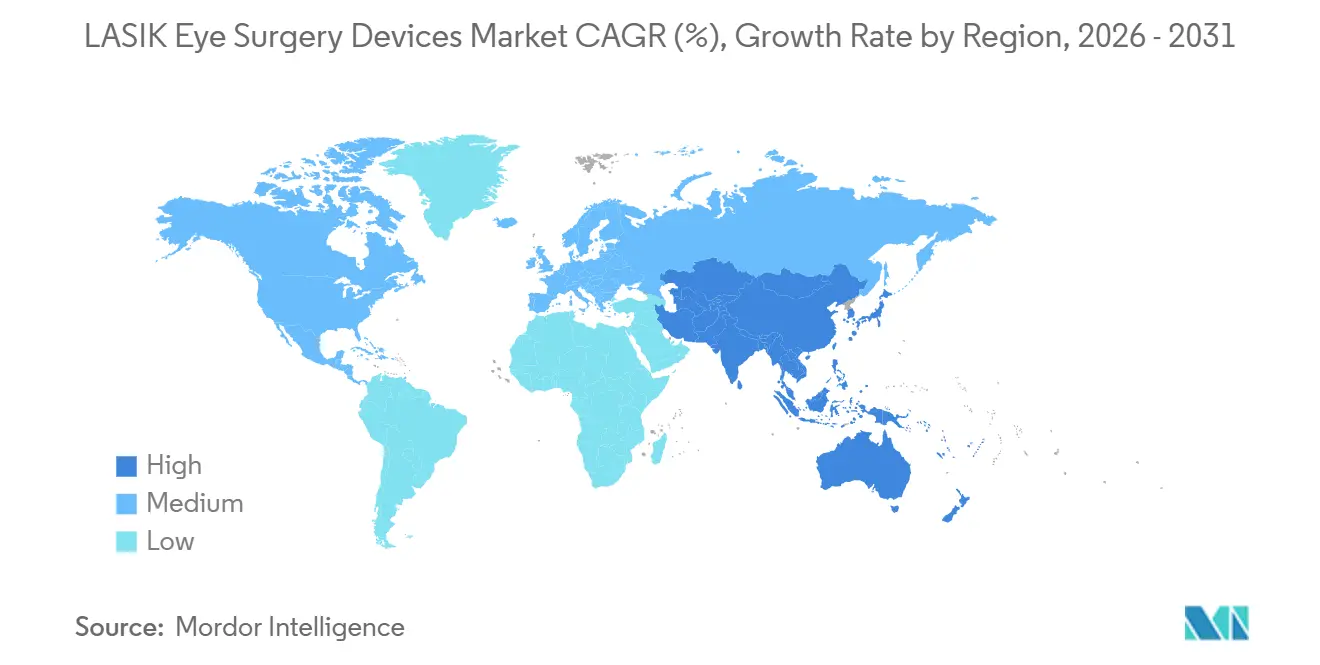

- By geography, North America accounted for 45.52% revenue share in 2025, while Asia-Pacific is projected to grow at 7.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LASIK Eye Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Myopia and Astigmatism Burden | +1.9% | Global, most acute in East Asia, with spillover to South Asia and MEA | Long term (≥ 4 years) |

| Shift From Blade-Based to All-Laser LASIK | +1.3% | North America and Europe leading, APAC accelerating | Medium term (2-4 years) |

| Expansion of High-Volume Refractive Surgery Centers | +0.9% | APAC core, with spillover to South Asia and MEA | Medium term (2-4 years) |

| Higher Upgrade Cycles for Wavefront and Topography-Guided Platforms | +0.7% | North America, Europe, Tier-1 APAC cities | Short term (≤ 2 years) |

| Specialty Gas and Optics Supply Chain Localization Risk | +0.4% | Global, concentrated in East Asia and EU manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Myopia and Astigmatism Burden

The LASIK eye surgery devices market is drawing long-term support from the steady rise in myopia and related refractive conditions across children, adolescents, and young adults. A 2025 meta-analysis covering 276 studies and more than 5.4 million participants found that global myopia prevalence among children and adolescents rose from 24.32% in 1990 to 35.81% in 2023. The same body of evidence points to a much larger future treatment pool as these patients move into the age band where refractive surgery becomes clinically suitable. East Asia remains the most intense pressure point, with WHO regional data showing adolescent myopia rates approaching 80% in some China and Singapore cohorts[1]World Health Organization Western Pacific Regional Office, “Myopia at Epidemic Levels,” WHO WPRO Data Platform, data.wpro.who.int. Astigmatism often appears alongside myopia, which means rising case volumes are not limited to simple spherical correction and increasingly favor platforms with stronger cylinder management. That pattern is helping the LASIK eye surgery devices market move toward systems that can treat more complex visual profiles rather than only high-volume routine cases.

Shift From Blade-Based to All-Laser LASIK

The LASIK eye surgery devices market is also being lifted by the continued move away from blade-based procedures and toward all-laser treatment workflows. In March 2025, the US FDA approved the WaveLight EX500 Laser System with INNOVEYES Sightmap, the first ray-tracing personalized LASIK system to receive that clearance[2]U.S. Food and Drug Administration, “Premarket Approval P020050/S043, WaveLight EX500 Laser System With INNOVEYES Sightmap,” U.S. Food and Drug Administration, fda.gov. Alcon later reported real-world results from 200 patients and 400 eyes treated with wavelight plus, with 100% of myopic eyes reaching 20/20 uncorrected distance visual acuity at 3 months and 89% reaching 20/16. A 2025 study in BMC Ophthalmology also found that ray-tracing-guided LASIK reduced overcorrection ratios relative to standard approaches. These results are pushing patient expectations upward at premium centers and raising pressure on older installations that cannot deliver the same planning depth or treatment precision. The LASIK eye surgery devices market is therefore seeing replacement demand shaped as much by outcome expectations and software capability as by hardware age.

Expansion of High-Volume Refractive Surgery Centers

The LASIK eye surgery devices market is being reshaped by the steady concentration of procedure volumes inside larger refractive surgery networks and multi-site outpatient care models. This shift changes procurement from surgeon-led decisions into institution-led capital planning, where service contracts, workflow standardization, and training support carry more weight. Larger center formats also support stronger equipment utilization, which improves the economics of premium platform adoption and makes advanced systems easier to justify. The same shift favors vendors that can install, maintain, and support multiple devices across networks rather than only sell a single laser into a single clinic. It also reduces the commercial strength of smaller suppliers that compete mainly on standalone hardware features. As this procurement model expands, the LASIK eye surgery devices market is becoming more dependent on enterprise relationships and less dependent on isolated device placements.

Higher Upgrade Cycles for Wavefront and Topography-Guided Platforms

The LASIK eye surgery devices market is seeing a shorter replacement cycle as refractive centers increasingly position clinical differentiation as part of their patient acquisition strategy. Wavefront-guided LASIK held the largest technology share at 43.24% in 2025, while topography-guided LASIK is projected to grow faster at 6.52% through 2031. Alcon’s FDA-approved Contoura Topo-G pivotal study reported 93% of eyes at 20/20 uncorrected distance visual acuity or better and 32% at 20/12.5 or better. A 2025 prospective contralateral-eye comparison found that wavefront-guided LASIK produced a statistically significantly higher proportion of 20/12.5 outcomes than topography-guided LASIK at 12 months. These findings show that the two technologies are addressing different patient needs rather than competing as direct substitutes. That dynamic is increasing the value of dual-technology ownership and pushing the LASIK eye surgery devices market toward more frequent platform refreshes in centers that compete on premium outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Device and Maintenance Cost | -0.8% | Global, most acute in South Asia, Southeast Asia, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Limited Insurance Coverage for Elective Vision Correction | -0.7% | North America, Europe, Gulf markets | Short term (≤ 2 years) |

| Surgeon Training Depth and Case-Volume Requirements | -0.4% | Global, concentrated in South Asia, MEA, and Latin America | Medium term (2-4 years) |

| Regulatory Friction for New Ablation Profiles and Software Updates | -0.3% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device and Maintenance Cost

High capital cost remains 1 of the clearest adoption limits for the LASIK eye surgery devices market, especially outside major urban care clusters. Premium femtosecond and excimer systems usually require initial spending from USD 300,000 to more than USD 700,000 per unit, with annual service contracts of USD 40,000 to USD 80,000. That cost base is difficult for lower-volume centers to absorb and often pushes purchasing decisions toward delayed upgrades or second-hand systems. The burden is not limited to initial purchase price because excimer systems also depend on specialty gases and optics support that add recurring operating expense. This makes utilization rates critical, since centers with weaker procedure density have less room to recover capital and service costs over time. The result is a slower placement pace for new platforms in cost-sensitive regions even when clinical demand for refractive correction is rising.

Limited Insurance Coverage for Elective Vision Correction

Limited reimbursement remains a direct demand ceiling for the LASIK eye surgery devices market in high-income health systems where elective vision correction is usually excluded from routine insurance coverage. In the United States, the 2025 Federal Employee Vision Plan administered by VSP offered a discount of 15% at contracted facilities rather than direct reimbursement[3]U.S. Office of Personnel Management, “2025 VSP FEHBP Brochure,” Office of Personnel Management, opm.gov. Priority Health’s 2025 policy also classified refractive procedures for myopia, hyperopia, astigmatism, and presbyopia as not medically necessary. Humana stated average out-of-pocket LASIK costs near USD 2,200 per eye, which keeps bilateral treatment in the mid-four-digit range for many households. While FSA and HSA eligibility provides some relief, that route mainly shifts timing of procedures rather than creating a broad reimbursement foundation. This keeps the LASIK eye surgery devices market exposed to consumer affordability and discretionary spending patterns even in otherwise mature regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Femtosecond Leadership Supports Premium Platform Economics

Femtosecond lasers held 42.31% of the LASIK eye surgery devices market share in 2025, making them the largest product segment in the LASIK eye surgery devices market. Their lead reflects the established role of bladeless flap creation in premium refractive workflows and the strong preference for reproducible incision geometry. Surgeons also value the ability to control flap thickness more precisely and reduce epithelial complications compared with mechanical systems. A Harvard review traced the evolution of femtosecond lasers from LASIK-specific tools into broader corneal surgery platforms, which strengthens utilization economics for each installed system. That broader use case supports higher capital justification and helps maintain premium pricing even when procedure competition intensifies. The LASIK eye surgery devices industry therefore continues to treat femtosecond placement as both a refractive asset and a wider ophthalmic capability investment.

Excimer lasers are the fastest-growing product segment, with the LASIK eye surgery devices market size for this segment projected to expand at a 7.38% CAGR from 2026 to 2031. Recent regulatory clearances widened their addressable use and improved the case for dual-platform adoption. Bausch + Lomb received FDA approval for the TENEO Excimer Laser Platform for myopia and myopic astigmatism LASIK vision correction surgery in January 2024. The FDA also lists the MEL 90 among approved lasers for LASIK, reinforcing the broader indication expansion underway in the category. As these approvals expand treatment flexibility, centers that once relied on limited refractive setups are moving toward combined femtosecond and excimer ownership. That transition supports incremental excimer demand even when overall procedure growth is steady rather than abrupt.

By Technology: Clinical Differentiation Is Increasing Segment Separation

Wavefront-guided LASIK accounted for 43.24% of revenue in 2025, giving it the leading technology position within the LASIK eye surgery devices market. Its large installed base and long clinical track record continue to support demand at high-volume refractive centers. A 2025 prospective contralateral-eye study reported that wavefront-guided LASIK delivered a statistically significantly higher rate of 20/12.5 visual outcomes than topography-guided LASIK at 12 months. That supports its role in standard myopia cases where corneal irregularity is limited and precision consistency matters most. Wavefront-optimized systems also retain an efficiency advantage in busy centers that value shorter treatment planning and throughput discipline. The LASIK eye surgery devices industry still depends on this installed base for a large part of current technology revenue.

Topography-guided LASIK is the fastest-growing technology segment, with a projected CAGR of 6.52% from 2026 to 2031 in the LASIK eye surgery devices market. The segment is benefiting from stronger surgeon comfort, more visible patient-facing differentiation, and better fit in irregular or complex astigmatic cases. Alcon’s Contoura Topo-G pivotal study showed 93% of eyes reaching 20/20 uncorrected distance visual acuity or better and 32% reaching 20/12.5 or better. A 2024 expanded cohort study found that wavefront-guided and topography-guided platforms both achieved close to 90% of eyes at 20/20 or better, showing that multiple technology paths can remain clinically credible. The next layer of competition is already emerging through ray-tracing systems, which connect diagnostic depth more tightly to ablation planning. That means technology competition in the LASIK eye surgery devices market is shifting from simple treatment categories into outcome-specific workflow design.

By Application: Myopia Provides Scale While Astigmatism Drives Premium Growth

Myopia correction represented 35.52% of revenue in 2025 and remained the largest application in the LASIK eye surgery devices market. Its lead reflects the condition’s broad prevalence and the long-established fit of LASIK for myopia within the clinically accepted correction range. WHO Western Pacific data continue to show particularly intense pressure in East Asian urban populations, where adolescent prevalence remains extremely high in some cohorts. This gives the LASIK eye surgery devices market a large future pool of patients who may seek surgical correction once refractive stability is reached. Hyperopia remains a smaller but stable niche that gained support from broader platform approvals. FDA approval pathways have therefore widened the practical addressable range for application demand even without changing the central weight of myopia.

Astigmatism correction is the fastest-growing application segment, with the LASIK eye surgery devices market size for this segment projected to grow at a 7.25% CAGR through 2031. Growth is linked to better axis-specific treatment capability and stronger recognition of mild to moderate astigmatism as a meaningful surgical target. A 2025 Ophthalmology study found that ray-tracing-guided LASIK improved astigmatic correction predictability and reduced overcorrection ratios compared with wavefront-optimized LASIK. Another 2025 study in the Journal of Southern Medical University showed Toric-ICL outperforming femtosecond LASIK in moderate-to-high myopia with astigmatism, which underscores why more advanced LASIK planning is becoming important at the clinical margin. Because astigmatism and myopia frequently appear together, product selection is increasingly influenced by how well a platform handles combined cases rather than single-condition correction. That makes astigmatism management a major competitive lever inside the LASIK eye surgery devices market even though myopia still brings the largest volume.

By End User: Outpatient Expansion Is Changing How Vendors Win Contracts

Eye clinics held 38.22% of revenue in 2025, which kept them as the largest end-user group in the LASIK eye surgery devices market. Their lead reflects the fact that many LASIK consultations, diagnostic assessments, and surgeon-patient relationships still begin in clinic settings rather than hospital departments. High-volume dedicated LASIK centers also sit within this group and remain important targets for premium system placement because stronger annual case loads improve payback on expensive platforms. Clinics often have more flexibility than hospitals in scheduling elective procedures and designing patient pathways around refractive surgery. That supports continued demand for integrated diagnostic and treatment suites that reduce workflow friction from evaluation to surgery. The LASIK eye surgery devices market therefore still relies heavily on clinic-led demand even as the care setting continues to evolve.

Ambulatory surgical centers are the fastest-growing end-user segment, with a projected CAGR of 7.65% from 2026 to 2031 in the LASIK eye surgery devices market. MedPAC’s March 2025 report to Congress identified ophthalmology as 1 of the 2 most common single-specialty ASC categories in the United States. That outpatient alignment fits LASIK well because the procedure does not need hospital-scale infrastructure and benefits from lower overhead and faster case turnover. As more ophthalmology capacity shifts toward ASC-linked models, purchasing decisions are moving toward network committees that evaluate service support, training, and remote monitoring along with laser performance. This favors manufacturers that can support repeated installations across multiple sites and maintain uptime at scale. As a result, the LASIK eye surgery devices industry is seeing the procurement model move away from single-site preference and toward system-wide operating logic.

Geography Analysis

North America held 45.52% of the LASIK eye surgery devices market share in 2025, which made it the largest regional market. The region combines high procedure awareness, dense refractive surgery infrastructure, and an active approval environment for new devices and treatment upgrades. Between January 2024 and March 2025, major platforms such as TENEO and the personalized WaveLight EX500 with INNOVEYES Sightmap received U.S. regulatory clearance or approval, reinforcing the pace of premium system renewal. The LASIK eye surgery devices market in the region also benefits from a large base of outpatient eye care providers that can absorb high-end capital equipment. South America remains smaller, with Brazil and Argentina as the most active procedure centers in the region, supported by private eye care concentration and medical travel patterns.

Europe remained the second-largest regional block in the LASIK eye surgery devices market, supported by mature refractive surgery activity in Germany, the United Kingdom, and Spain. Germany continues to support demand for advanced capability platforms through specialty clinics and academic refractive centers. The United Kingdom also maintains stable private-pay LASIK demand outside public reimbursement, which supports consistent procedure volumes. Across the region, stricter EU Medical Device Regulation requirements are extending commercialization timelines for new ablation profiles and software updates, which favors larger companies with stronger regulatory infrastructure.

Asia-Pacific is the fastest-growing regional segment, with the LASIK eye surgery devices market size in the region projected to advance at 7.45% CAGR from 2026 to 2031. China and India remain the main growth engines because both markets combine expanding private eye care capacity with a large future treatment pool. WHO Western Pacific data show very high adolescent myopia prevalence in several East Asian settings, which keeps the long-term patient pipeline structurally strong. South Korea also supports regional growth through a strong domestic refractive surgery base and cost-competitive appeal for cross-border patients. The Middle East and Africa continue to develop from a smaller base, led by Saudi Arabia and the UAE where medical tourism, higher disposable incomes, and specialist care investment are supporting procedure demand. Across emerging regions, growth remains real, but it is moderated by capital cost, regulatory entry requirements, and the need for trained refractive surgery teams.

Competitive Landscape

The LASIK eye surgery devices market is moderately consolidated among tier-1 suppliers, but it remains fragmented beyond the leading group. Alcon Inc., Carl Zeiss Meditec AG, Bausch + Lomb, and Johnson & Johnson Vision Care continue to shape premium platform competition through broader refractive workflow offerings. Their strength comes from combining diagnostics, treatment planning, and lasers into connected systems that are harder for centers to replace step by step. This structure raises switching costs at the provider level and gives larger vendors more control over service, training, and software-linked upgrades. The LASIK eye surgery devices market is therefore becoming more centered on ecosystem strength than on single-device specifications alone.

Alcon provided the clearest recent example of this direction when it launched wavelight plus in the United States and Canada in September 2025 after earlier commercialization in China and Europe. The system combines ray-tracing guidance with the WaveLight EX500 and an advanced diagnostic layer, which supports fully personalized treatment planning. Carl Zeiss Meditec has also been extending its refractive workflow position through the VISUMAX 800 and MEL 90 combination, which the company highlighted as part of its broader ophthalmic care offering in 2025. Bausch + Lomb strengthened its presence after FDA approval of the TENEO platform, which broadened its competitive standing in excimer-based LASIK. These moves show that leading companies are not only defending installed bases, they are also trying to lock centers into broader clinical workflows that can support future upgrades.

A second competitive layer is forming around new treatment delivery models and white-space applications within the LASIK eye surgery devices market. iVIS Technologies demonstrated fully remote-controlled LASIK surgery in 2025, connecting a surgeon in Bangalore with a patient in Bari through its iRes2 laser and Remote Control Station. This shows how specialized expertise could be extended into locations that lack high-end refractive surgeons on site. Presbyopia-focused laser correction remains another open area because no single platform has established clear dominance. That combination of tier-1 platform control and open niches leaves the market structured, but not closed.

LASIK Eye Surgery Devices Industry Leaders

Alcon Inc.

Carl Zeiss Meditec AG

Johnson & Johnson Vision Care, Inc.

Bausch + Lomb Incorporated

NIDEK CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: OVO LASIK + LENS, a well-known provider of advanced vision correction, completed over 1,500 WaveLight Plus LASIK procedures, making it the top-performing clinic in the U.S. for this treatment.

- September 2025: Alcon launched WaveLight Plus, the first-ever fully personalized LASIK treatment guided by ray-tracing technology, in the U.S. and Canada.

Global LASIK Eye Surgery Devices Market Report Scope

As per the scope of the report, LASIK eye surgery devices are specialized medical instruments and equipment used to perform Laser-Assisted In Situ Keratomileusis (LASIK), a popular refractive surgery procedure to correct vision problems such as myopia, hyperopia, and astigmatism.

The LASIK eye surgery devices market is segmented by product type, technology, application, end user, and geography. By product type, the market includes femtosecond lasers, excimer lasers, and other LASIK devices. By technology, it is categorized into wavefront-guided LASIK, wavefront-optimized LASIK, topography-guided LASIK, and other technologies. By application, the market covers myopia, hyperopia, astigmatism, and presbyopia. By end user, it is segmented into eye clinics, hospitals, ambulatory surgical centers, and other end users. By geography, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Femtosecond Lasers |

| Excimer Lasers |

| Other LASIK Devices |

| Wavefront-Guided LASIK |

| Wavefront-Optimized LASIK |

| Topography-Guided LASIK |

| Other Technologies |

| Myopia |

| Hyperopia |

| Astigmatism |

| Presbyopia |

| Eye Clinics |

| Hospitals |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Femtosecond Lasers | |

| Excimer Lasers | ||

| Other LASIK Devices | ||

| By Technology | Wavefront-Guided LASIK | |

| Wavefront-Optimized LASIK | ||

| Topography-Guided LASIK | ||

| Other Technologies | ||

| By Application | Myopia | |

| Hyperopia | ||

| Astigmatism | ||

| Presbyopia | ||

| By End User | Eye Clinics | |

| Hospitals | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of the LASIK eye surgery devices space?

The LASIK eye surgery devices market size was USD 2.42 billion in 2025, rises to USD 2.55 billion in 2026, and is forecast to reach USD 3.34 billion by 2031 at a 5.52% CAGR.

Which product segment leads revenue generation?

Femtosecond lasers led with 42.31% revenue share in 2025 because they remain the standard for bladeless flap creation and support premium refractive workflows.

Which technology is growing the fastest through 2031?

Topography-guided LASIK is the fastest-growing technology segment, with a projected 6.52% CAGR through 2031, supported by stronger performance in complex corneal and astigmatic cases.

Which application is expanding the fastest?

Astigmatism correction is projected to grow at 7.25% through 2031 as ray-tracing and topography-guided systems improve axis-specific ablation accuracy.

Which region leads demand and which region grows fastest?

North America held 45.52% share in 2025, while Asia-Pacific is the fastest-growing region with a projected 7.45% CAGR through 2031.

What is the biggest commercial barrier for vendors and providers?

The main barrier is the combination of high equipment cost and limited insurance coverage, which slows new system placement and keeps LASIK dependent on out-of-pocket spending.

Page last updated on: