Vitreoretinal Surgery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

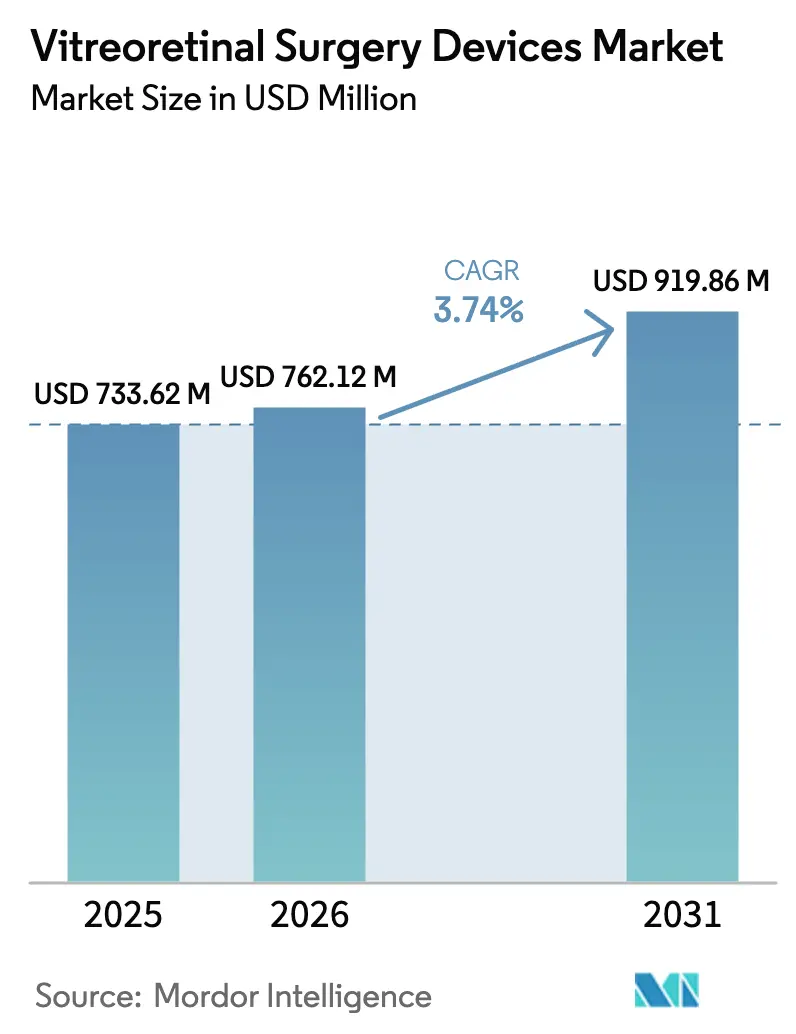

| Market Size (2026) | USD 762.12 Million |

| Market Size (2031) | USD 919.86 Million |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vitreoretinal Surgery Devices Market Analysis by Mordor Intelligence

The Vitreoretinal Surgery Devices Market size is expected to increase from USD 733.62 million in 2025 to USD 762.12 million in 2026 and reach USD 919.86 million by 2031, growing at a CAGR of 3.74% over 2026-2031.

Growing caseloads of diabetic retinopathy and age-related macular degeneration, combined with a pivot toward micro-incision platforms and single-use consumables, are expanding procedure volumes while reshaping revenue mix. Device makers are grappling with infection-control mandates that favor disposables, reimbursement ceilings that cap system prices, and an increasing shift of cases to ambulatory surgical centers (ASCs). Competitive strategies, therefore, emphasize pre-sterilized instrument kits, integrated digital visualization, and modular consoles that lower entry costs for emerging markets. At the same time, regulatory bodies in the United States, the European Union, and China are tightening evidence and traceability requirements, raising the bar for new entrants but widening opportunities for incumbents with strong quality systems.

Key Report Takeaways

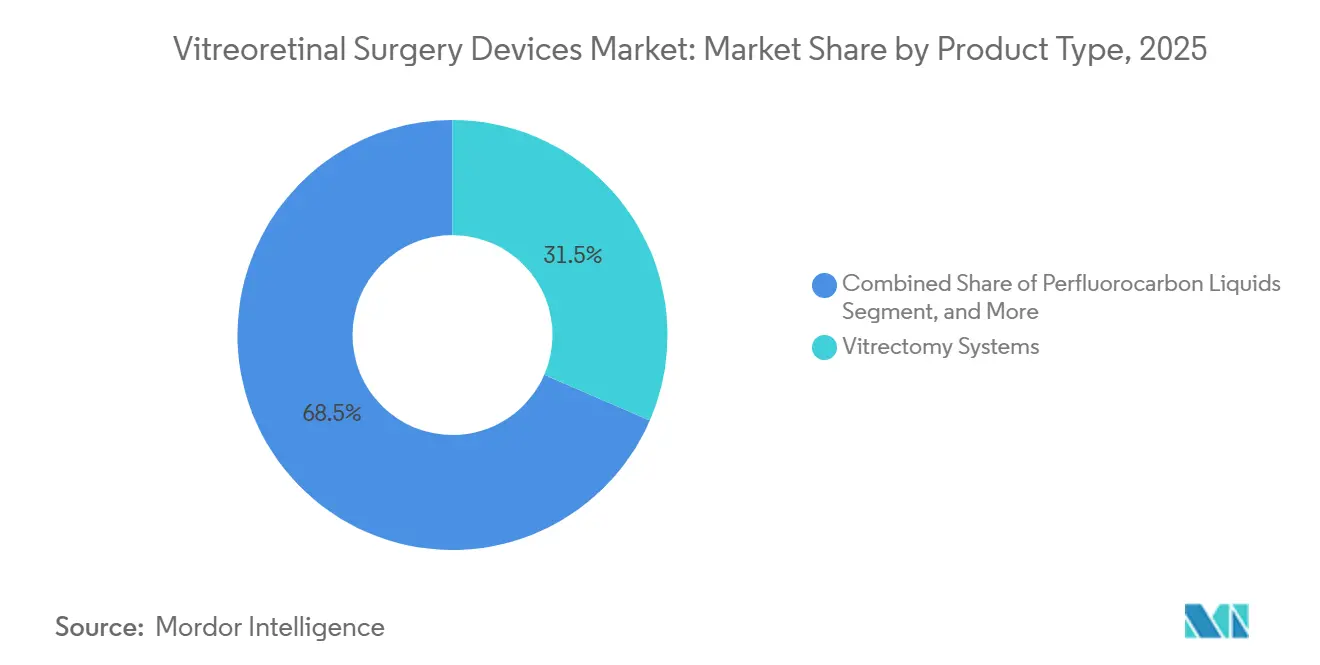

- By product type, vitrectomy systems led with 34.81% of vitreoretinal surgery devices market share in 2025, while single-use consumables are expanding at a 6.76% CAGR through 2031.

- By surgery type, posterior procedures accounted for 69.03% of vitreoretinal surgery devices market size in 2025, yet anterior procedures are advancing at a 7.20% CAGR to 2031.

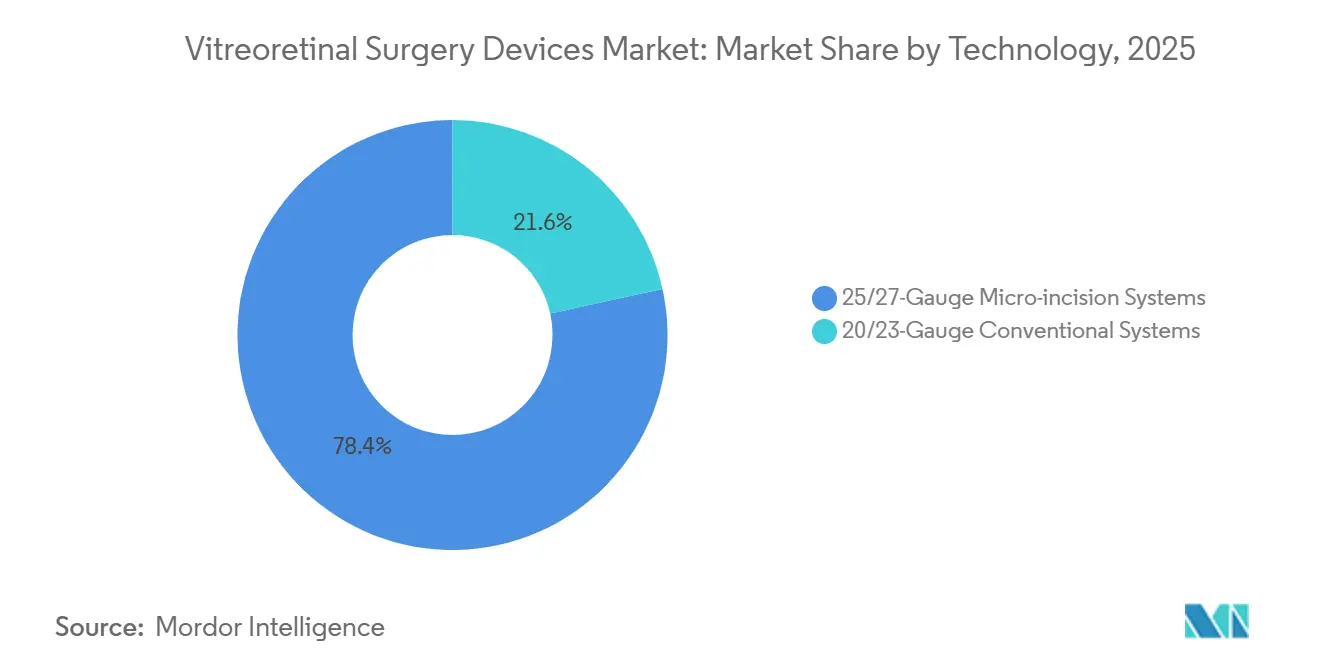

- By technology, 25-gauge and 27-gauge micro-incision platforms commanded 78.43% of segment revenue in 2025; conventional 20-/23-gauge systems are growing at 5.91% annually in cost-sensitive regions.

- By end user, hospitals held 42.46% of segment revenue in 2025, whereas ASCs are the fastest-growing channel, expanding at an 8.52% CAGR during the forecast horizon.

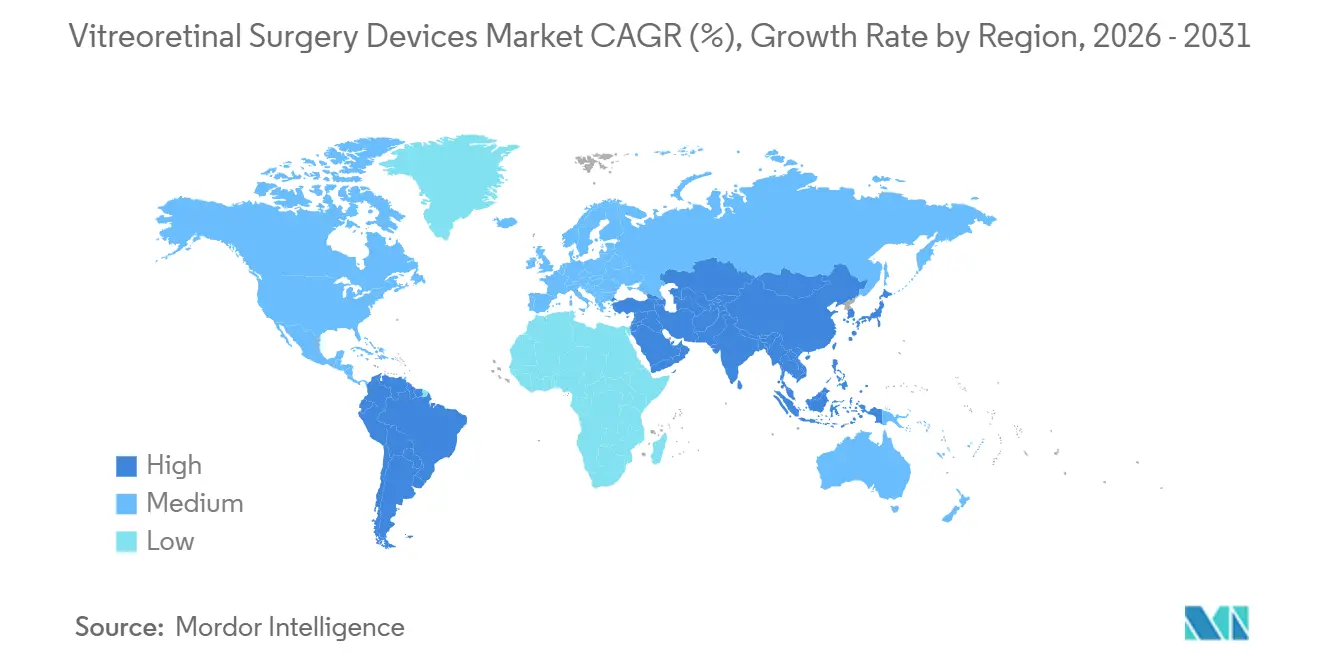

- By geography, North America retained a 39.16% revenue share in 2025, but Asia-Pacific is poised to grow at 7.74% CAGR to 2031, driven by medical tourism and public-sector capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vitreoretinal Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetic retinopathy & AMD | +1.2% | APAC, North America | Long term (≥ 4 years) |

| Growing geriatric population worldwide | +0.8% | Japan, Europe, North America | Long term (≥ 4 years) |

| Shift toward single-use instruments | +0.9% | North America, EU, urban APAC | Medium term (2-4 years) |

| Expansion of outpatient/ASC procedures | +1.1% | North America, Western Europe, GCC | Short term (≤ 2 years) |

| Intra-operative OCT & digital visualization | +0.6% | North America, Germany, Japan | Medium term (2-4 years) |

| APAC medical-tourism-led growth | +0.7% | Thailand, Singapore, India, Malaysia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetic Retinopathy & AMD

Diabetic retinopathy affected 103.12 million adults in 2025, while age-related macular degeneration reached 195.92 million cases, creating a durable pipeline for complex retinal procedures. China’s Healthy China 2030 program increased rural retinal screening coverage to 54% by 2025, resulting in a 22% boost in newly diagnosed proliferative cases.[1]National Health Commission China, “Healthy China 2030 Screening Update,” nhc.gov.cn India’s National Programme for Control of Blindness reported that diabetic eye disease prevalence climbed to 21.3 % among known diabetics in 2025, lengthening specialist wait times in tier-2 cities. In North America, rising obesity rates sustain incident diabetes, keeping procedure backlogs elevated. These epidemiological trends are driving the expansion of the vitreoretinal surgery devices market, as hospitals and ASCs invest in additional consoles and consumables to meet the growing demand.

Shift Toward Single-Use Ophthalmic Instruments Driven by Strict Infection-Control Mandates

The 2024 CDC guideline reclassified reusable endo-illuminators as critical devices that require sterilization between cases, a standard many sterile-processing departments struggle to meet. U.S. retina services responded by shifting to pre-sterilized disposable light pipes and cutters, prompting a 41% surge in Alcon’s disposable sales during Q3 2025. The EU Medical Device Regulation’s traceability rules added paperwork for reusables, accelerating the adoption of single-use products in high-volume centers in Germany and France. Bausch + Lomb’s Stellaris Elite platform capitalized on the trend by bundling 25-gauge disposable packs that eliminate reprocessing liability, capturing 18% of the U.S. ASC segment in 2025. As urban APAC hospitals emulate Western infection-control standards, the penetration of single-use products is rising in Singapore, Seoul, and tier-1 Chinese cities.

Expansion of Outpatient/ASC Vitreoretinal Procedures

Medicare removed multiple vitrectomy codes from the inpatient-only list in 2025, allowing ASCs to bill at 58% of hospital outpatient rates while retaining higher margins.[2]Centers for Medicare & Medicaid Services, “Physician Fee Schedule 2025,” cms.gov ASC vitrectomy volume in the United States jumped 27% year-over-year through Q1 2026, with SCA Health opening 14 retina-focused centers outfitted for 90-minute turnovers. Saudi Arabia licensed 22 private day-surgery units in 2025, mirroring the U.S. shift. However, European ASC penetration remains below 15% because of licensing hurdles and bundled hospital contracts. The migration concentrates volume in high-throughput facilities that favor standardized, disposable kits, thereby expanding the addressable demand for vitreoretinal surgery devices.

Intra-Operative OCT & Digital Visualization Uptake

Carl Zeiss Meditec’s RESCAN 700 and Leica’s EnFocus Ultra, cleared in 2024, integrated spectral-domain OCT into surgical microscopes, reducing repeat membrane-peel rates by 23% in complex proliferative cases. Alcon’s NGENUITY 3D display reached 22% penetration in U.S. academic centers by late 2025, cutting surgeon neck strain by 40% during 8-hour lists. Japan’s aging ophthalmologist workforce values ergonomic heads-up display, supporting early adoption. High capital premiums, ranging from USD 150,000 to USD 200,000 above standard scopes, remain a barrier; however, leasing models and bundled service contracts are helping to improve affordability. The technology’s ability to shorten operative time and avoid re-interventions reinforces its pull on the vitreoretinal surgery devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & consumable costs | -0.9% | Emerging APAC, Latin America, MEA | Medium term (2-4 years) |

| Post-operative complications | -0.3% | Global | Short term (≤ 2 years) |

| Patchy reimbursement for premium kits | -0.7% | North America, select European markets | Medium term (2-4 years) |

| Lengthy regulatory approval cycles | -0.5% | EU post-MDR, China NMPA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Consumable Costs

A fully configured vitrectomy suite costs USD 250,000 to USD 450,000, a figure that excludes 68% of U.S. independent retina practices from ownership.[3]American Society of Retina Specialists, “Practice Survey 2025,” asrs.org Single-use packs add USD 800 to USD 1,200 per case, versus USD 200 to USD 300 for reusables after reprocessing labor, straining margins in low-income markets. In India, consumables account for 42% of procedure costs, which limits adoption in tier-2 and tier-3 cities, where out-of-pocket payments dominate. DORC’s EVA NEXUS, launched at USD 180,000, aims to bridge the gap with modular upgrades but commands slow uptake, as surgeons prioritize entrenched Alcon and Bausch ecosystems. While leasing models, such as Alcon’s OptiLease, spread costs over 36 months, only 10% of practices have adopted them due to the perceived risk of obsolescence.

Patchy Reimbursement for Premium Kits

The 2025 Medicare ASC payment for CPT 67036 is USD 1,847, barely covering basic micro-incision disposables and leaving no room for intra-operative OCT add-ons. Private U.S. insurers frequently classify disposable light pipes as bundled supplies, denying separate payment. Germany’s DRG pays EUR 2,100 (USD 2,289) but requires onerous documentation to bill for 27-gauge upgrades. The United Kingdom’s flat GBP 1,620 (USD 2,041) tariff has frozen since 2024, forcing National Health Service trusts to ration advanced visualization tools. Manufacturers have begun to implement value-based contracts; Bausch + Lomb, for example, cuts 15% off the list price in exchange for shared savings on readmissions to overcome payor resistance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Gain as Systems Mature

Single-use consumables expanded their share of the vitreoretinal surgery devices market in 2025 and are forecast to grow at a 6.76% annual rate through 2031, while vitrectomy consoles accounted for 34.81% of the revenue. Prefilled silicone-oil syringes trimmed eight minutes of prep time per case and cut contamination risk, propelling adoption among ASCs focused on fast turnover. Endo-illumination is shifting toward disposable LED light pipes, with 58% of Bausch’s 2025 sales projected to come from single-use units. Perfluorocarbon liquids remain a niche but steady earner; Vitreq’s extended-duration formulation, CE Marked in 2024, lengthened tamponade dwell time and postponed follow-up surgeries.

The momentum of consumables hinges on infection-control mandates and the economics of ASCs, where reprocessing space is at a premium. The vitreoretinal surgery devices market for disposables is projected to expand further as CDC and EU regulators scrutinize validation data for reusable devices. Meanwhile, console vendors stress backward compatibility; Alcon’s Unity system allows legacy Constellation owners to migrate gradually by adding disposable gauge-specific cassettes. Carl Zeiss Meditec bundles microscopes with OCT modules to secure long-term consumable revenue, mirroring the printer-ink razor model that stabilizes cash flow.

By Surgery Type: Anterior Segment Work Accelerates

Posterior procedures continued to dominate, accounting for 69.03% of the revenue in 2025; however, anterior vitrectomy volumes increased by 7.20% annually due to pediatric trauma and cataract-related complications. The vitreoretinal surgery devices market size for anterior cases benefits from cross-utilizing the same 27-gauge cutters used posteriorly, minimizing inventory SKUs for ASCs. A 27-gauge anterior approach cut surgical time by 12 minutes compared to a 20-gauge approach, lowering anesthesia exposure in children and aligning with ASC session economics. Posterior cases, although slower-growing, account for 82% of consumable spend, as they require more forceps, scissors, and retinal tamponades.

Medicare’s 2025 site-neutral reforms further erased inpatient-outpatient divides, encouraging same-day discharge even for posterior repairs. Ophthalmologists increasingly refer complex anterior complications to retina specialists, concentrating volume in high-throughput centers that specify disposable kits. BVI and Katalyst Surgical now offer sub-USD 400 anterior vitrectomy packs that align with payor bundles, reinforcing consumable tailwinds for the vitreoretinal surgery devices market.

By Technology: Micro-Incision Dominance Masks Conventional Resurgence

Micro-incision 25-gauge and 27-gauge platforms hold 78.43% share in 2025, prized for sutureless closures and rapid recovery. However, lower-cost 20-/23-gauge consoles are rebounding, with prices up 5.91% in price-sensitive APAC and Latin American sites. A meta-analysis showed that 27-gauge vitrectomy reduced hypotony to 1.2% compared with 3.8% for 20-gauge vitrectomy, yet the latter remains essential for thick membrane manipulation and large foreign-body removal. Indian eye-care chains deploy 20-gauge systems in rural satellites, where reusable instruments align with budget constraints. The vitreoretinal surgery devices market continues to prioritize hybrid consoles; Alcon’s Unity offers interchangeable gauge cassettes, allowing clinics to tailor costs to case complexity.

EU regulators have slowed the introduction of ultra-small-gauge products, those with 30-gauge and narrower diameters, as manufacturers must demonstrate non-inferiority to 27-gauge. This regulatory drag could prolong revenue for established gauges, giving suppliers time to amortize R&D. Meanwhile, robotic trocar placement systems from Preceyes promise to standardize port alignment across gauges, potentially flattening the learning curve and expanding addressable demand.

By End User: ASCs Capture Margin-Conscious Volume

Hospitals retained a 42.46% share in 2025, but ASC volumes are expanding at an 8.52% annual rate, driven by a 28%-34% lower cost per case and surgeon equity incentives. SCA Health and Surgery Partners added 31 retina-dedicated centers in 2025, each configured for 12-16 daily cases and stocked exclusively with pre-sterilized instrument packs. The vitreoretinal surgery devices market size associated with ASCs is, therefore, the fastest-growing channel. In Europe and Japan, restrictive licensing maintains hospital dominance, but policy debates are intensifying as payers scrutinize U.S. savings benchmarks.

Ophthalmology clinics remain a niche but noteworthy end-user: portable systems, such as MedOne’s Photon, priced at USD 120,000, enable in-office floaterectomies. Reimbursement uncertainty, however, caps growth. Alcon’s 36-month lease at USD 6,500 per month aims to bridge capital barriers, yet adoption lags amid concerns about technological obsolescence. Nonetheless, any acceleration in clinic-based procedures would open an additional front in the vitreoretinal surgery devices market.

Geography Analysis

North America accounted for 39.16% of 2025 revenue, anchored by Medicare’s willingness to reimburse digital visualization and high ASC penetration. The United States alone placed 230 new vitrectomy consoles in 2025, with 64% of these going to ASCs. Canada continues to favor hospital outpatient departments but is trialing bundled-payment pilots that could speed ASC licensing by 2027.

Asia-Pacific is the fastest-growing territory, advancing at a 7.74% CAGR through 2031. Medical tourism drew 47,200 inbound ophthalmic cases to Thailand in 2025, while India’s National Health Mission funded 140 district-hospital vitrectomy systems that same year. China’s NHSA cataloged 12 reimbursable retinal codes in 2025, reimbursing 85% of the patient's cost and igniting demand for consoles in tier-2 urban clusters. Collectively, these initiatives expand the vitreoretinal surgery devices market and shift unit placement growth toward APAC.

Europe’s growth is hindered by flat DRG tariffs and stringent EU MDR rules, which extend approval timelines and delay the launch of new-gauge and single-use products. Backlog pressures in Germany, the United Kingdom, and France are pushing clinics in Eastern Europe to adopt lower-cost 23-gauge systems, which could moderate regional ASPs. The Middle East and Africa are growing at a rate of 6.2% per year, buoyed by the Gulf Cooperation Council's hospital privatization and South Africa’s expansion of its private-hospital network. South America faces currency volatility; Brazil’s public SUS system reimburses only basic 20-gauge kits, shifting premium demand to self-pay urban clinics. Australia, while minor, approved intra-operative OCT for reimbursement in 2025, underscoring its early-adopter profile.

Competitive Landscape

The vitreoretinal surgery devices market exhibits moderate concentration, with the top five suppliers, Alcon, Bausch + Lomb, Carl Zeiss Meditec, DORC, and BVI, collectively accounting for significant revenue in 2025; however, none of these suppliers exceeded 20%. Alcon’s Unity platform integrates real-time pressure sensing into a disposable 27-gauge cutter, lowering hypotony rates by 19%. Bausch + Lomb’s Stellaris Elite bundles a 25-gauge console with single-use instrument packs, capturing 18% of the U.S. ASC niche by eliminating reprocessing liability. Carl Zeiss Meditec leverages its microscope base to cross-sell RESCAN 700 intra-operative OCT, achieving 12% penetration among U.S. retina practices in 2025.

White-space entrants focus on cost-disruptive disposables and robotics. Katalyst Surgical’s 27-gauge cutter launched 40% below incumbent ASPs, appealing to turnover-obsessed ASCs. Vitreq’s extended-duration perfluorocarbon liquids cut follow-up surgeries and gained traction in Europe. Preceyes secured the CE Mark for a robotic vitrectomy assistant that stabilizes instrument motion with 10 μm precision, potentially broadening surgeon access. Patent activity related to AI-assisted membrane segmentation and robotic trocar placement increased by 34% between 2024 and 2025, foreshadowing a possible inflection point in automation over the next decade.

Regulatory headwinds are stiffening. The FDA’s 2025 guidance tightens validation for single-use reprocessing claims, advantaging incumbents with ISO 13485-certified plants. EU MDR traceability rules add cost but heighten entry barriers. Collectively, these dynamics preserve margin for market leaders yet leave strategic gaps, particularly in low-cost disposables, where nimble players can thrive.

Vitreoretinal Surgery Devices Industry Leaders

Dutch Ophthalmic Research Center International BV

Bausch & Lomb, Inc

Alcon, Inc.

MedOne Surgical, Inc

Carl Zeiss Meditec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: EssilorLuxottica signed its acquisition of Optegra Eye Health Care, a European network of ophthalmic clinics, with backing from investment firm MidEuropa. Optegra operated clinics in five European nations: the United Kingdom, the Czech Republic, Poland, Slovakia, and the Netherlands.

- April 2025: At the 2025 American Society of Cataract and Refractive Surgery (ASCRS) Annual Meeting, Microsurgical Technology (MST) presented groundbreaking advancements in vitreoretinal surgery. Central to their showcase was the Vista 1-Step, a 27-gauge, 14.5 mm needle-point vitrector designed for seamless scleral introduction without the need for MVR blades or trocars.

- April 2025: Alcon launched its latest innovations, the UNITY Vitreoretinal Cataract System (VCS) and the UNITY Cataract System (CS). This versatile platform comes in two configurations: a combined console (VCS) and a standalone cataract system (CS). Engineered for optimal efficiency, this platform enhances both vitreoretinal and cataract surgeries, ensuring outstanding patient outcomes.

- September 2024: Microsurgical Technology (MST) established an exclusive global partnership with Vista Ophthalmics to introduce the Vista line, featuring revolutionary products such as the Vista 1-Step. The Vista 1-Step, a 27-gauge, 14.5 mm needle-point vitrector, is designed to streamline scleral entry by removing the need for microvitreoretinal (MVR) blades or trocars.

Global Vitreoretinal Surgery Devices Market Report Scope

As per the scope of the report, vitreoretinal surgery devices are used to conduct surgeries for diseases like macular degeneration, retinal detachment, uveitis, vitreous hemorrhage, macular hole and epiretinal membrane, retinal detachment, and complications related to diabetic retinopathy. The Vitreoretinal Surgery Devices Market is segmented by Product Type (Perfluorocarbon Liquids, Endoillumination Instrument, Vitreoretinal Prefilled Silicone Oil Syringes, Vitrectomy System, and Other Product Types), Surgery Type (Anterior Vitreoretinal Surgery and Posterior Vitreoretinal Surgery), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Perfluorocarbon Liquids |

| Endo-illumination Instruments |

| Vitreoretinal Prefilled Silicone-Oil Syringes |

| Vitrectomy Systems |

| Single-use Consumables |

| Other Product Types |

| Posterior Vitreoretinal Surgery |

| Anterior Vitreoretinal Surgery |

| 20/23-Gauge Conventional Systems |

| 25/27-Gauge Micro-incision Systems |

| Hospitals |

| Ambulatory Surgical Centers |

| Ophthalmology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Perfluorocarbon Liquids | |

| Endo-illumination Instruments | ||

| Vitreoretinal Prefilled Silicone-Oil Syringes | ||

| Vitrectomy Systems | ||

| Single-use Consumables | ||

| Other Product Types | ||

| By Surgery Type | Posterior Vitreoretinal Surgery | |

| Anterior Vitreoretinal Surgery | ||

| By Technology | 20/23-Gauge Conventional Systems | |

| 25/27-Gauge Micro-incision Systems | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Ophthalmology Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the vitreoretinal surgery devices market?

The global vitreoretinal surgery devices market size is worth USD 762.12 million in 2026.

How fast is the vitreoretinal surgery devices market expected to grow?

It is forecast to expand at a 3.74% CAGR, reaching USD 919.86 million by 2031.

Which region is projected to be the fastest-growing for vitreoretinal devices?

Asia-Pacific is set to grow at a 7.74% CAGR through 2031, driven by medical tourism and public-sector investment.

Why are single-use consumables gaining traction in retinal surgery?

Stricter infection-control mandates and ASC workflow needs favor pre-sterilized disposable cutters, light pipes, and cannulas.

Which technology dominates current vitreoretinal procedures?

Micro-incision 25-gauge and 27-gauge platforms hold 78.43% share, prized for sutureless closures and rapid recovery.

Page last updated on: