Ocular Trauma Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

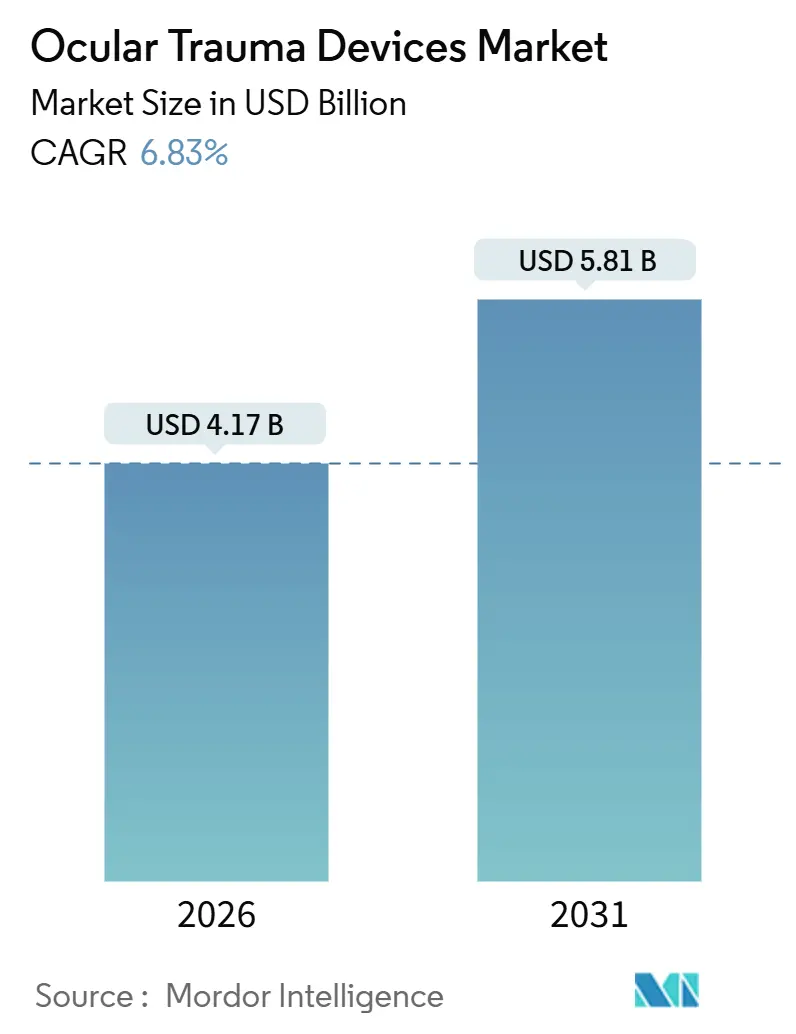

| Market Size (2026) | USD 4.17 Billion |

| Market Size (2031) | USD 5.81 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

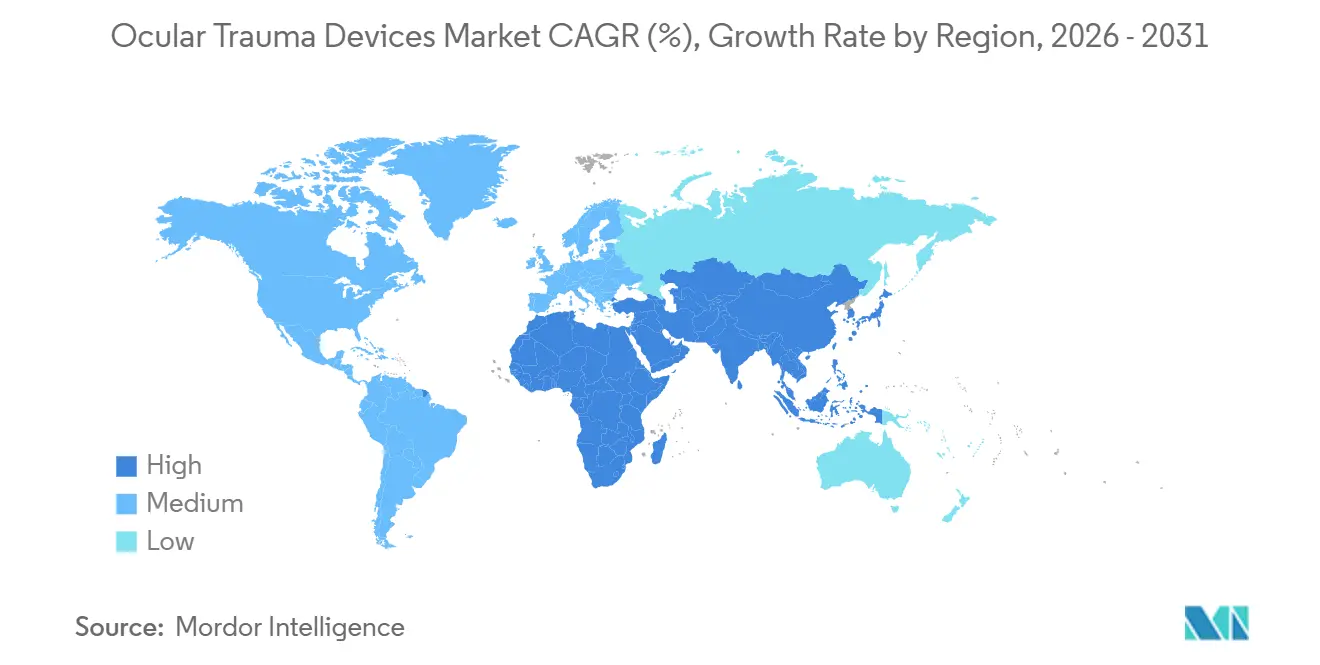

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ocular Trauma Devices Market Analysis by Mordor Intelligence

The Ocular Trauma Devices Market size is estimated at USD 4.17 billion in 2026, and is expected to reach USD 5.81 billion by 2031, at a CAGR of 6.83% during the forecast period (2026-2031).

Rising adoption of micro-invasive surgical platforms, military procurement of rapid-deployment repair kits, and AI-enabled triage systems are widening both civilian and defense demand curves. Hospitals still anchor purchasing, yet ambulatory surgical centers are absorbing a growing share as payers steer moderate cases toward lower-cost venues. Material substitution is under way: silicone remains dominant, but biodegradable polymers are winning surgeon confidence by eliminating follow-up removal procedures. Supply-chain fragility for specialty silicone grades and tightening reimbursement for premium implants constrain near-term margins, but device makers that demonstrate functional-outcome gains continue to command pricing power.

Key Report Takeaways

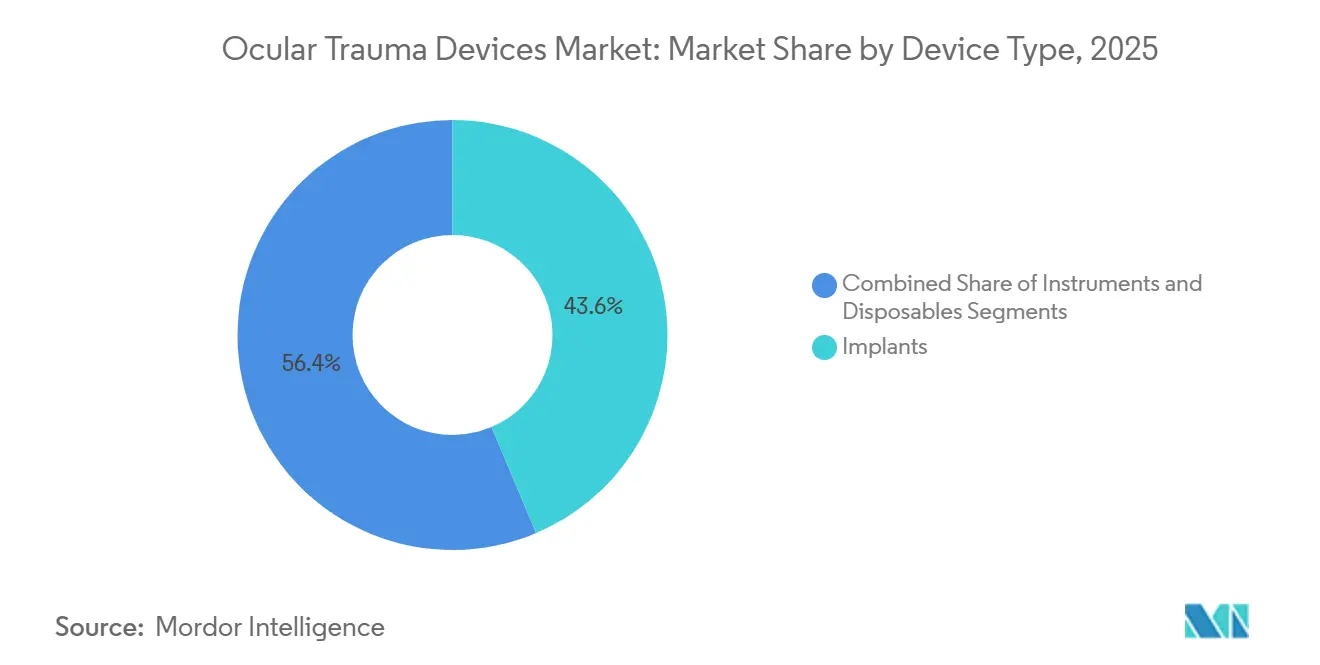

- By device type, implants led with a 43.63% share of the ocular trauma devices market size in 2025, while disposables are forecast to expand at a 9.36% CAGR through 2031.

- By indication, penetrating injuries accounted for 44.72% of ocular trauma devices market share in 2025; chemical injuries are poised to grow fastest at an 8.79% CAGR to 2031.

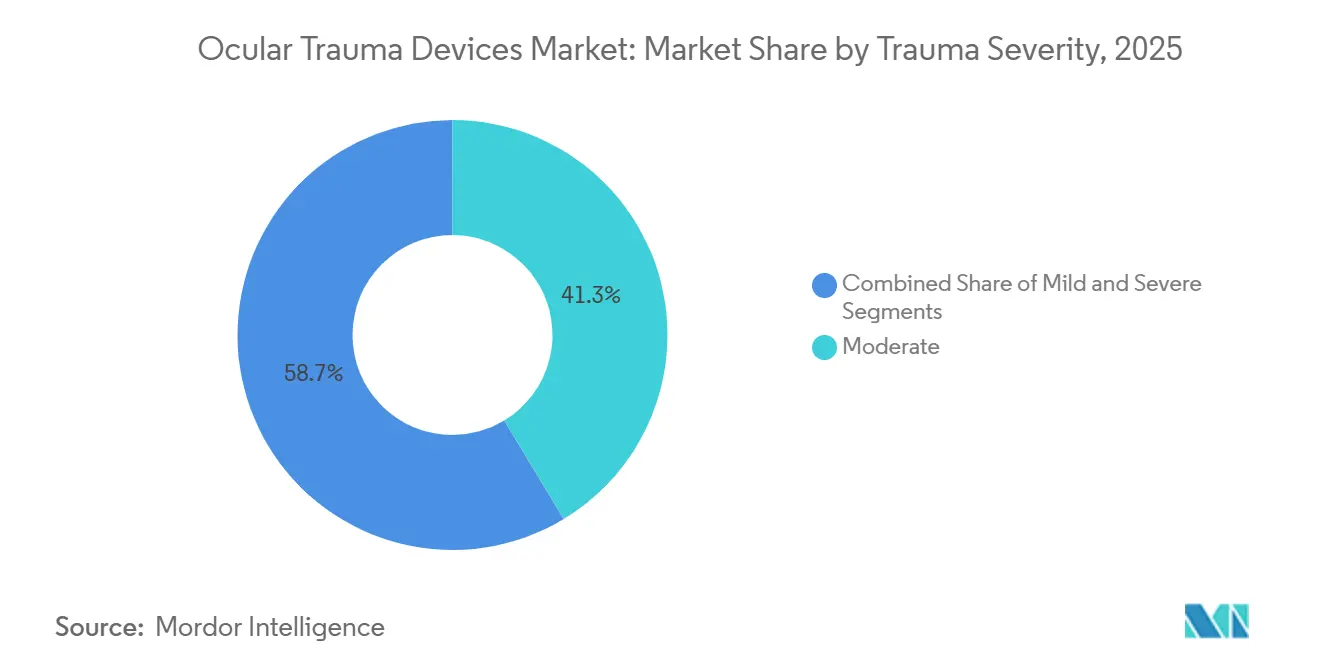

- By trauma severity, moderate cases delivered 41.34% revenue in 2025, whereas severe injuries will record the highest CAGR at 9.22% through 2031.

- By material, silicone held 56.84% of segment revenue in 2025; biodegradable polymers are projected to rise at a 10.35% CAGR to 2031.

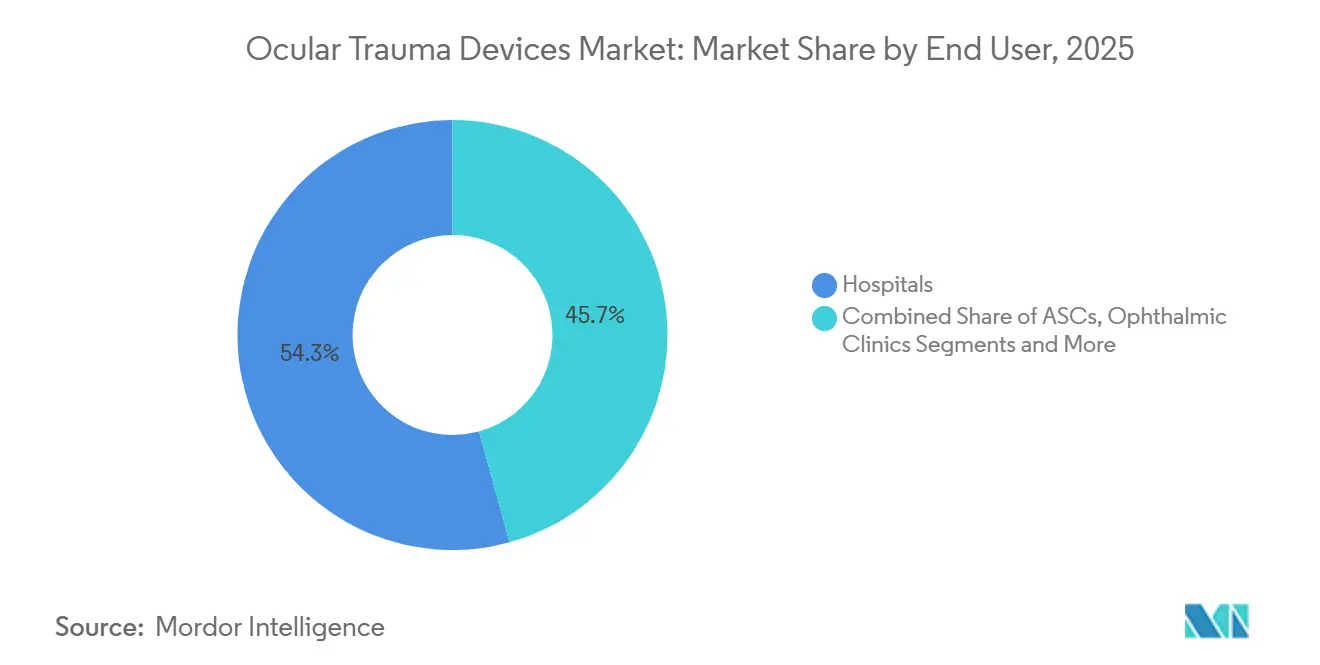

- By end user, hospitals captured 54.27% revenue in 2025, yet ambulatory surgical centers will advance at an 8.74% CAGR through 2031.

- By geography, North America led with 34.44% revenue in 2025, while Asia-Pacific will post the fastest 9.37% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ocular Trauma Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Ocular Injuries | +1.2% | Global, strongest in APAC and MEA | Medium term (2-4 years) |

| Technological Advances in Micro-Invasive Surgical Tools | +1.4% | North America, EU spillover to APAC | Short term (≤ 2 years) |

| Expansion of Road-Traffic & Sports-Related Trauma Cases | +0.9% | APAC core, Latin America emerging | Medium term (2-4 years) |

| Smart Biosensor-Embedded Implants for Real-Time IOP Monitoring | +0.7% | North America & EU, pilots in APAC | Long term (≥ 4 years) |

| Defense Demand for Rapid-Deployment Repair Kits | +0.5% | North America, EU, Middle East | Short term (≤ 2 years) |

| AI-Enabled Handheld Diagnostics for Low-Resource Triage | +0.6% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Ocular Injuries

Industrial hubs across China, India, and Southeast Asia report a disproportionate surge in high-energy penetrating wounds, a trend attributed to inconsistent enforcement of eye-safety protocols.[1]World Health Organization, “World Health Organization Vision Report 2024,” World Health Organization, who.int Recreational trauma is also escalating: U.S. emergency rooms treated more basketball-related eye injuries in 2024 than in any prior year, a pattern the American Academy of Ophthalmology linked to lax protective-eyewear adoption.[2]American Academy of Ophthalmology, “Workforce Analysis 2024,” American Academy of Ophthalmology, aao.org Motorcycle crashes without visor-equipped helmets add a continual stream of blunt and penetrating injuries in emerging Asian economies. These dynamics enlarge the addressable pool for both implants and disposables.

Technological Advances in Micro-Invasive Surgical Tools

Robotic platforms such as the PRECEYES Surgical System achieve sub-100-micron precision that minimizes collateral tissue loss during foreign-body extraction. Heads-up 3-D visualization, exemplified by Alcon’s NGENUITY system, is installed in more than 3,000 operating rooms, improving ergonomics and supporting real-time remote consultation. Integrated optical-coherence-tomography (OCT) guidance in Carl Zeiss Meditec’s ARTEVO 800 enables surgeons to confirm retinal re-attachment without stopping to access external imaging. Together, these technologies shorten average procedure time by up to 20%, a compelling value proposition for hospitals facing operating-room bottlenecks.

Expansion of Road-Traffic & Sports-Related Trauma Cases

India reported more than 460,000 road-traffic accidents in 2024; ophthalmic injuries are rising in tandem with two-wheeler ownership. Combat sports such as mixed martial arts gained mainstream popularity in Asia-Pacific, yet protective face shields remain optional despite International Olympic Committee data showing that combat events accounted for 12% of all Olympic eye injuries at the 2025 Paris Games.[3] International Olympic Committee, “Paris 2025 Injury Surveillance Data,” International Olympic Committee, olympic.org Recreational leagues lag in adopting safety standards, ensuring a persistent pipeline of moderate-severity trauma cases that benefit the ocular trauma devices market.

Smart Biosensor-Embedded Implants for Real-Time IOP Monitoring

FDA-cleared eyemate PLUS sensors provide round-the-clock intraocular-pressure data, enabling clinicians to detect post-traumatic glaucoma before optic-nerve damage occurs. Bausch + Lomb is evaluating a disposable contact lens with embedded microelectronics that records diurnal IOP fluctuations, a non-surgical alternative for patients reluctant to accept implants. Early adopters report fewer secondary surgeries because pressure spikes are managed proactively, reinforcing the case for premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Costs & Uneven Reimbursement | -0.8% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Stringent Multi-Region Regulatory Pathways | -0.7% | Global, most burdensome in EU & North America | Medium term (2-4 years) |

| Shortage of Trauma-Trained Ophthalmic Surgeons | -0.5% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Supply-Chain Fragility in Specialty Silicone & Fluorosilicone Materials | -0.4% | Global, concentrated in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Costs & Uneven Reimbursement

Alcon’s NGENUITY 3-D console lists at roughly USD 300,000, while annual service contracts add up to USD 40,000, presenting budget hurdles for community hospitals – especially after Medicare trimmed complex-vitrectomy fees by 3% in 2025. Private insurers demanding prior authorization for premium intraocular lenses delay procedures and nudge surgeons toward lower-priced alternatives. European health-technology-assessment agencies tighten quality-adjusted life-year thresholds, further dampening uptake.

Stringent Multi-Region Regulatory Pathways

The EU Medical Device Regulation, fully enforced in 2024, has created application backlogs surpassing 18 months, forcing smaller manufacturers to prioritize U.S. markets where 510(k) reviews still take 8-10 months. ISO 13485 audits and FDA Part 820 quality-system requirements impose ongoing compliance costs that thin margins for emerging innovators. These delays slow global rollout of novel ocular trauma devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Implants Anchor Revenue, Disposables Surge

In 2025, implants generated 43.63% of ocular trauma devices market revenue, reflecting their central role in globe reconstruction. Vitreous tamponades such as silicone oil feature in over 60% of post-traumatic retinal detachment repairs. In contrast, single-use vitrectomy packs and pre-loaded suture systems underpin a 9.36% CAGR for disposables, as ambulatory surgical centers favor pre-sterilized kits that negate reprocessing costs. Instruments, although vital, have 3-5-year replacement cycles that temper unit growth. Capital-intensive systems like Alcon’s Constellation dominate the reusable segment, yet smaller facilities gravitate to lower-cost disposable alternatives that align with lean budgets.

Disposables’ momentum is structural rather than cyclical. Post-COVID infection-control mandates elevate demand for one-time-use drapes and cannulas. Bausch + Lomb’s Stellaris Elite, launched with modular disposable cassettes, illustrates how OEMs monetize consumables even when capital sales flatten. Implants will retain the revenue crown through 2031, but disposables’ faster clip signals a shift toward throughput-driven purchasing behavior, a theme echoing across the ocular trauma devices market.

By Indication: Penetrating Injuries Lead, Chemical Burns Accelerate

Penetrating wounds commanded 44.72% ocular trauma devices market share in 2025, owing to foreign-body extractions and corneal repairs that consume high-value consumables. Workplace accidents and combat injuries create unpredictable but high-acuity demand spikes. Chemical injuries, however, will expand at an 8.79% CAGR as governments tighten industrial-safety mandates, forcing factories to install decontamination stations stocked with specialized irrigation kits. The U.S. Occupational Safety and Health Administration’s 2024 hazardous-materials update elevated employer liability, triggering equipment upgrades.

Blunt-force injuries from sports and traffic account for a steady baseline, often treated with staged interventions that spread device usage over multiple visits. Thermal burns and radiation exposure remain niche but stimulate innovation in amniotic-membrane grafts and shield designs. The differential growth rates underline a regulatory feedback loop: stricter prevention rules surface previously underreported cases, paradoxically driving higher device sales.

By Trauma Severity: Moderate Cases Dominate, Severe Injuries Grow Fastest

Moderate cases accounted for 41.34% of 2025 revenue, typically managed in outpatient centers that favor cost-effective kits and disposables. These facilities prize simplicity and quick turnover, aligning with manufacturers that bundle single-use vitrectomy packs. Severe trauma, often arising from high-velocity projectiles or blast injuries, will post a 9.22% CAGR as geopolitical flashpoints persist. Tertiary hospitals invest in integrated-OCT microscopes and robotic platforms to tackle these complex repairs, sustaining demand for premium capital equipment.

Mild injuries generate negligible device revenue, yet they channel follow-up monitoring that may escalate into surgical intervention if complications emerge. Vendors must segment go-to-market strategies: value-engineered disposables for high-volume moderate cases versus feature-rich systems for severe-trauma centers. Such bifurcation enlarges total accessible revenue within the ocular trauma devices market.

By Material Type: Silicone Dominates, Biodegradables Gain Traction

Silicone captured 56.84% of 2025 revenue due to its optical clarity and proven biocompatibility. Medical-grade silicone oil remains the gold standard for tamponade despite concerns over emulsification. Biodegradable polymers, however, will rise at a 10.35% CAGR, propelled by resorbable scleral plugs that remove the need for explant surgery. PMMA and legacy acrylics continue to cede ground to hydrophobic acrylics and new copolymers that reduce postoperative inflammation.

Metallic alloys retain niche relevance for scleral buckles and retinal tacks, where tensile strength outweighs optical properties. Johnson & Johnson Vision’s Tecnis Eyhance lens, crafted from a next-generation hydrophobic acrylic, exemplifies competitive differentiation via material science. Regulatory hurdles for new biomaterials remain high, but surgeon demand for leave-nothing-behind solutions ensures ongoing R&D investment across the ocular trauma devices market.

By End User: Hospitals Lead, Ambulatory Centers Rise

Hospitals held 54.27% revenue in 2025, underpinned by 24/7 operating-room access and multidisciplinary trauma teams. Academic centers act as regional hubs, concentrating severe cases and justifying investments in million-dollar robotic systems. Ambulatory surgical centers will log an 8.74% CAGR as payers extend reimbursement for moderate-complexity procedures and patients prefer same-day discharge. MedOne Surgical’s portable vitrectomy systems, priced under USD 120,000, target this fast-growing segment.

Ophthalmic clinics handle postoperative care, suture removal, and laser touch-ups, creating aftermarket demand for small-form-factor lasers and diagnostic probes. Military field hospitals and humanitarian missions buy rugged, battery-operable kits, a modest but strategic niche. The shifting site-of-service landscape compels manufacturers to offer modular portfolios that scale from austere deployments to flagship academic theaters, broadening reach within the ocular trauma devices market.

Geography Analysis

North America generated 34.44% revenue in 2025 thanks to more than 2,000 Level I and II trauma centers and robust defense procurement of rapid-deployment kits. U.S. facilities routinely integrate 3-D visualization and intraoperative OCT, reinforcing premium-device penetration, while Canada balances universal access with budget limits that slow high-end purchases. Mexico’s trauma burden is climbing, yet reimbursement gaps impede device uptake, creating a latent demand pool.

Asia-Pacific will record a 9.37% CAGR through 2031, driven by China’s plan to deploy 200 regional eye-trauma hubs and India’s USD 1.2 billion Vision 2030 investment. Japan and South Korea act as testbeds for robotic surgery and AI diagnostics, while medical tourism funnels complex trauma cases to private centers in Singapore and Thailand. Workforce deficits linger in Indonesia and the Philippines, tempering device adoption outside tier-one metros.

Europe’s strict Medical Device Regulation stretches launch timelines, yet Germany, France, and the United Kingdom sustain steady demand owing to well-funded public systems. Austerity in Southern Europe curbs capital budgets, pushing hospitals toward refurbished equipment. The Middle East shows a bifurcated pattern: Gulf states import cutting-edge devices and hire expatriate surgeons, whereas sub-Saharan Africa relies on donor-funded basic kits. South America remains opportunity-rich but volatile; Brazil’s expanding private-insurance base contrasts with Argentina’s currency headwinds that delay imports.

Competitive Landscape

The market is moderately consolidated. Key players include Alcon, Bausch + Lomb, Johnson & Johnson Vision, and Carl Zeiss Meditec, each offering broad portfolios that bundle implants, instruments, and disposables. Their vertical integration secures long-term purchasing contracts and after-sales revenue. Niche companies – MedOne Surgical, BVI Medical, Vitreq – compete on specialization, supplying portable vitrectomy consoles or custom micro-forceps tailored for trauma cases.

Technology remains the main battleground. Alcon’s NGENUITY heads-up display and Carl Zeiss Meditec’s OCT-integrated ARTEVO 800 command premium prices but risk obsolescence if next-gen platforms leapfrog current functionality. Patent trends reveal strategic divergence: Alcon filed 14 trauma-focused patents between 2024-2025, targeting autonomous suturing and hemostatic sealants, whereas Johnson & Johnson emphasizes smart-lens sensors. ISO 13485 and FDA Part 820 compliance favor large incumbents, yet the FDA’s Breakthrough Device pathway offers smaller firms expedited review, keeping acquisition pipelines active.

White-space opportunities cluster around biodegradable implants, AI-guided triage, and defense-grade rapid-deployment kits. Expect selective consolidation as dominant players acquire innovators to fortify portfolios, preserving a moderate-concentration structure within the ocular trauma devices market.

Ocular Trauma Devices Industry Leaders

Topcon Corporation

Carl Zeiss Meditec AG

Alcon Inc.

Bausch + Lomb Corp.

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: A Singapore Eye Research Institute licensing deal with Eyexora Global formed Y.ora Vision to commercialize a minimally invasive glaucoma device that performs multiple trabeculotomies.

- September 2025: Alcon committed USD 50 million to expand its Fort Worth, Texas plant, adding 200,000 sq ft of cleanroom space to boost NGENUITY and Constellation Vision System output. Completion is slated for Q3 2026.

- June 2025: The FDA approved ENCELTO (revakinagene taroretcel-lwey), a surgically implanted therapy for macular telangiectasia type 2, originating from a Scripps Research and Lowy Medical partnership.

Global Ocular Trauma Devices Market Report Scope

Ocular trauma devices are tools, implants, and protective equipment used to diagnose, treat, and manage eye injuries caused by blunt, sharp, or chemical trauma, including open-globe and closed-globe injuries.

The Ocular Trauma Devices Market Report is segmented by Device Type, Indication, Trauma Severity, Material Type, End User, and Geography. By Device Type, the market is segmented into Implants, Instruments, and Disposables. By Indication, the market is segmented into Penetrating Trauma, Blunt Trauma, Chemical Trauma, and Other Trauma. By Trauma Severity, the market is segmented into Mild, Moderate, and Severe. By Material Type, the market is segmented into Silicone-Based, PMMA & Acrylic, Biodegradable Polymers, and Metallic Alloys. By End User, the market is segmented into Hospitals, ASCs, Ophthalmic Clinics, and Other. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Implants |

| Instruments |

| Disposables |

| Penetrating Injuries |

| Blunt Injuries |

| Chemical Injuries |

| Other Trauma Types |

| Mild |

| Moderate |

| Severe |

| Silicone-Based |

| PMMA & Acrylic |

| Biodegradable Polymers |

| Metallic Alloys (Titanium, Stainless) |

| Hospitals |

| Ambulatory Surgical Centers |

| Ophthalmic Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Implants | |

| Instruments | ||

| Disposables | ||

| By Indication | Penetrating Injuries | |

| Blunt Injuries | ||

| Chemical Injuries | ||

| Other Trauma Types | ||

| By Trauma Severity | Mild | |

| Moderate | ||

| Severe | ||

| By Material Type | Silicone-Based | |

| PMMA & Acrylic | ||

| Biodegradable Polymers | ||

| Metallic Alloys (Titanium, Stainless) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Ophthalmic Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the ocular trauma devices market?

The market is valued at USD 4.17 billion in 2026, with a projected rise to USD 5.81 billion by 2031.

Which device category is growing fastest?

Disposables, such as single-use vitrectomy packs, are forecast to grow at a 9.36% CAGR through 2031.

Which indication will expand most rapidly?

Chemical injuries are expected to post the highest 8.79% CAGR as industrial-safety regulations tighten.

Why are ambulatory surgical centers important for future growth?

Payers encourage moderate trauma cases to move to lower-cost ASCs, driving an 8.74% CAGR in this setting.

How will defense procurement influence technology trends?

Military demand for rugged, portable repair kits accelerates innovation in multi-function devices suitable for austere environments.

What regions offer the highest growth potential?

Asia-Pacific is projected to lead with a 9.37% CAGR, buoyed by large-scale investments in trauma-care infrastructure.

Page last updated on: