Ophthalmology Surgical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

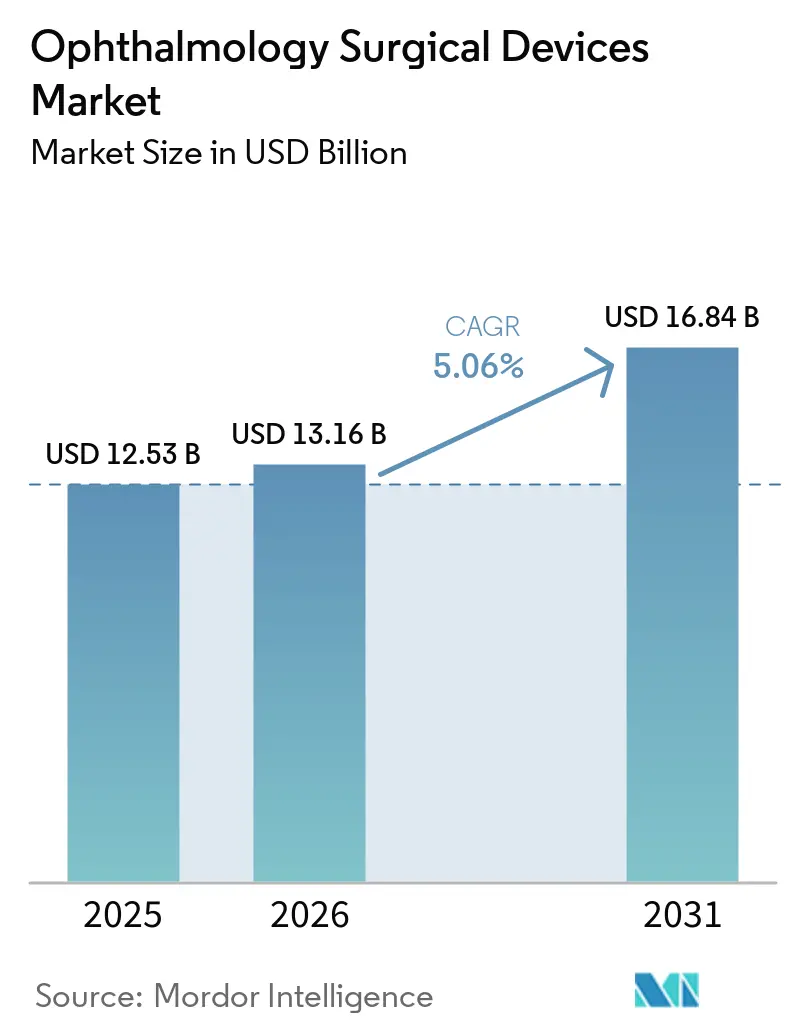

| Market Size (2026) | USD 13.16 Billion |

| Market Size (2031) | USD 16.84 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmology Surgical Devices Market Analysis by Mordor Intelligence

The ophthalmic surgical devices market size was valued at USD 12.53 billion in 2025 and estimated to grow from USD 13.16 billion in 2026 to reach USD 16.84 billion by 2031, at a CAGR of 5.06% during the forecast period (2026-2031). Sustained demand is linked to the global surge in age-related eye disorders, expanding surgical coverage, and steady gains in healthcare spending across emerging economies. Robust product pipelines—especially in phaco systems, image-guided microscopes, and minimally invasive glaucoma implants—are enabling providers to improve outcomes while raising procedure throughput. Rising adoption of ambulatory surgical centers (ASCs) in North America, favorable reimbursement adjustments, and growing availability of purpose-built low-cost platforms in Asia Pacific are further widening access. Meanwhile, consolidation among key manufacturers is yielding integrated digital ecosystems that combine diagnostics, planning, and surgery into a single workflow, enhancing surgeon productivity and differentiating premium offerings.

Key Report Takeaways

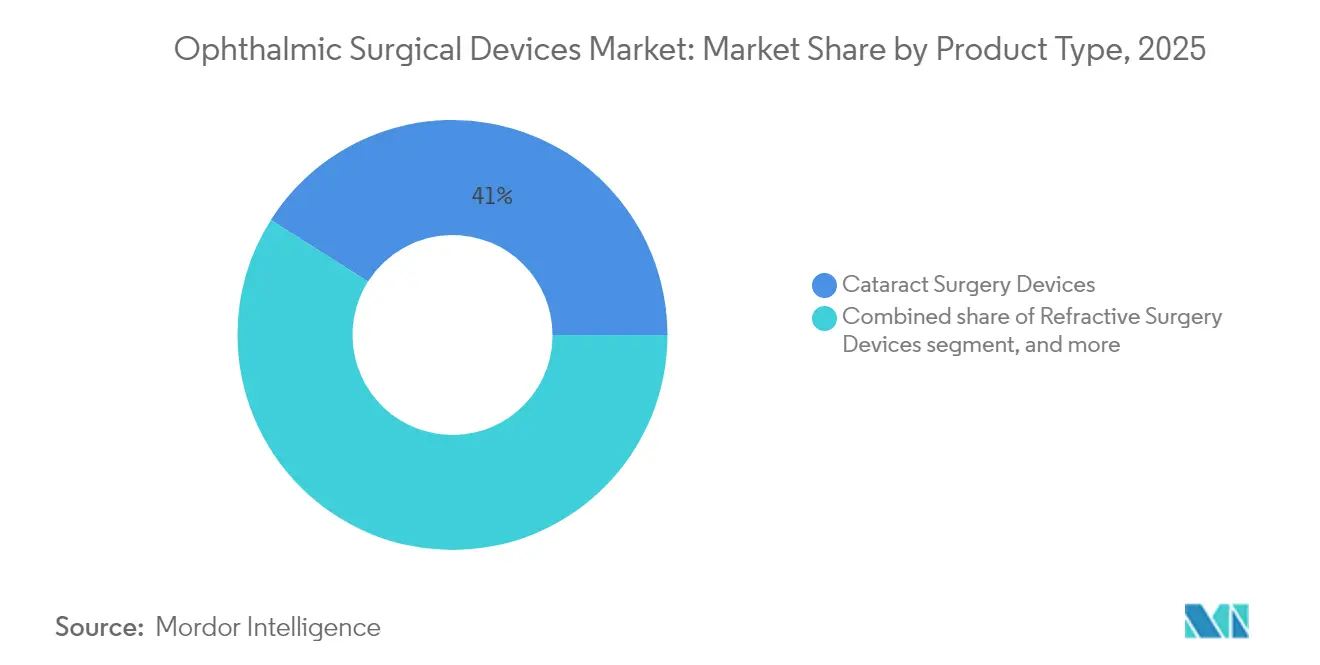

- By product, cataract surgery devices accounted for 41.02% of the ophthalmic surgical devices market share in 2025, whereas glaucoma surgery devices are forecast to expand at an 8.63% CAGR through 2031.

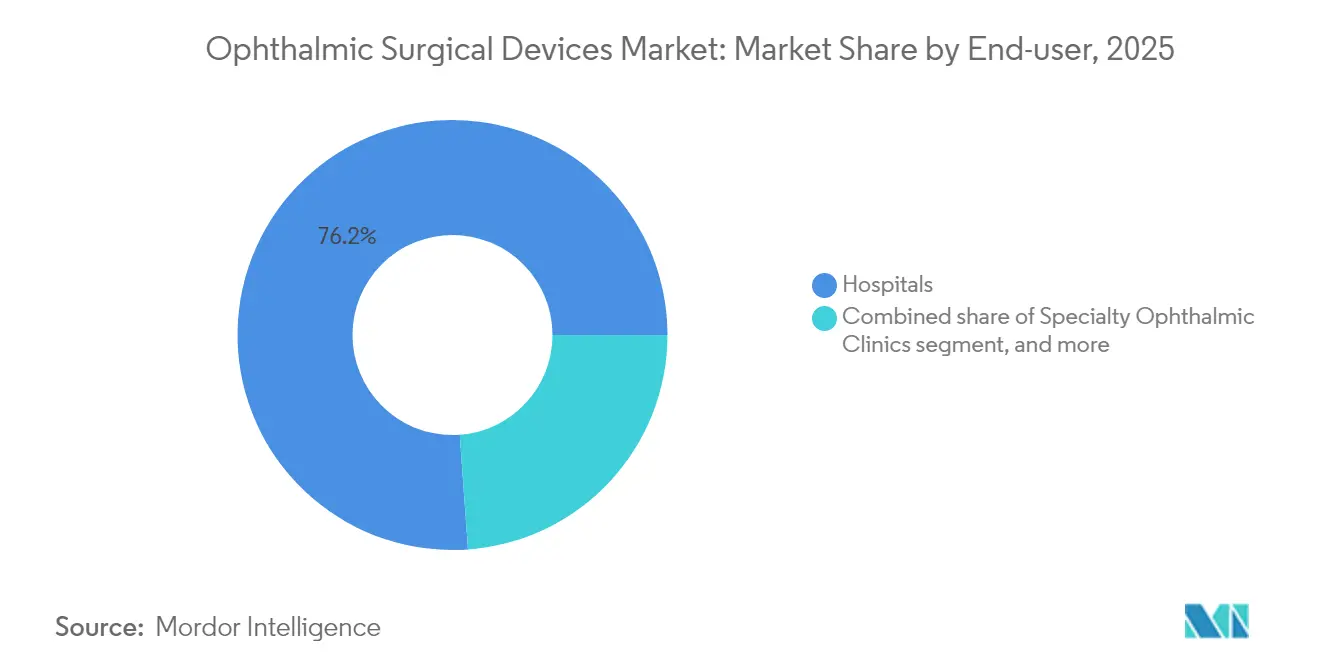

- By end-user, hospitals held 76.15% of the ophthalmic surgical devices market size in 2025, while ASCs are set to grow at a 6.82% CAGR through 2031.

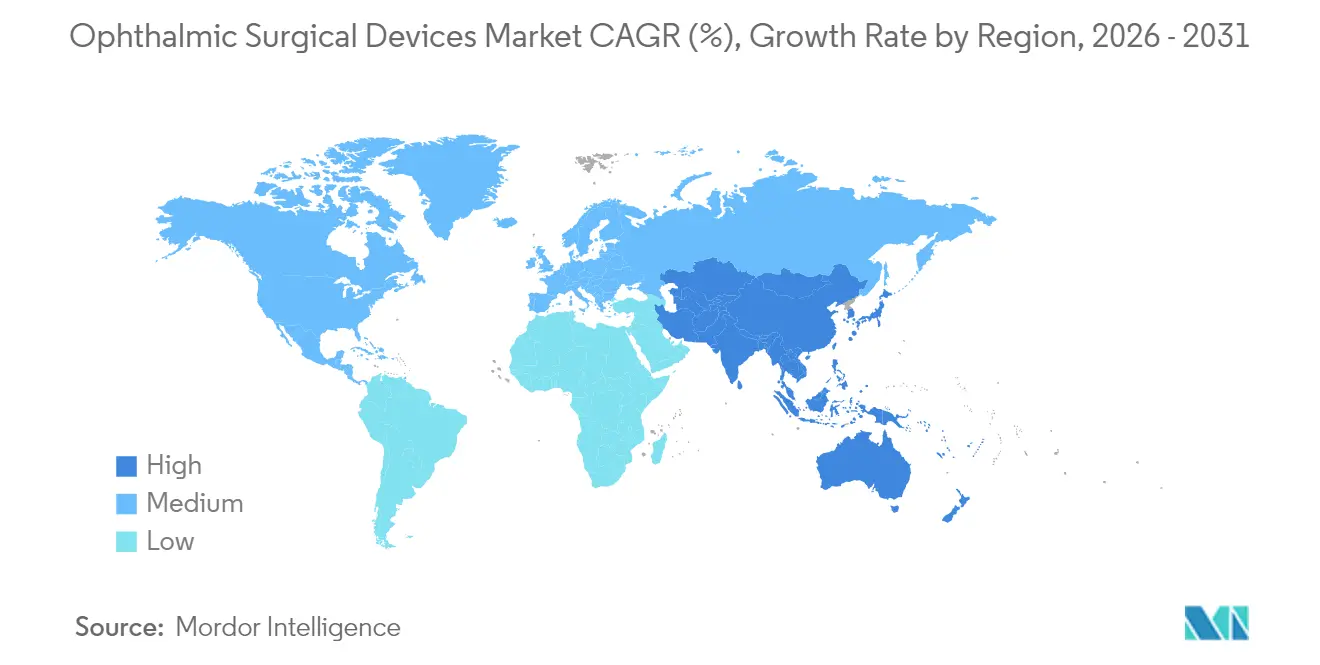

- By geography, North America commanded 31.75% revenue in 2025; Asia Pacific is the fastest-growing region at a projected 5.74% CAGR from 2026 to 2031.

- By company, Alcon Inc., Johnson & Johnson Vision Care, Carl Zeiss Meditec AG, Bausch + Lomb Corp., and Glaukos Corp. collectively controlled about 64.40% of global revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ophthalmology Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global cataract-surgery surge | +1.5% | Global (notably Asia Pacific & North America) | Long term (≥ 4 years) |

| Adoption of MIGS & combination procedures | +0.8% | North America, Europe; rising in Asia Pacific | Medium term (2-4 years) |

| Digital-OR & image-guided technology adoption | +1.2% | North America, Europe, advanced Asian markets | Medium term (2-4 years) |

| Expansion of ASCs & day-care reimbursement models | +0.9% | North America; building in Europe & Australia | Short term (≤ 2 years) |

| Purpose-built low-cost phaco platforms & single-use cataract packs | +0.6% | Asia Pacific (India, China), Latin America, Africa | Medium term (2-4 years) |

| Vision-care initiatives (WHO “Vision 2030”, national blindness-prevention programs) | +0.4% | Global; highest impact in developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Cataract-Surgery Surge Driven by Aging Demographics and Widening Surgical Coverage

Cataract procedure volumes are forecast to rise 128% by 2036, with patients aged 85+ generating the greatest incremental demand. Japan’s elderly population already exceeds 20%, creating broad momentum for surgical capacity expansion. National programs tackling surgical backlogs—from WHO’s Vision 2030 to country-specific blindness-prevention schemes—are improving coverage in many lower-income regions. Persistent disparity is still evident: a 2025 Australian study found Indigenous cataract surgical coverage at 68% versus 88.4% in non-Indigenous groups, underscoring the need for targeted outreach[1]Thais Watt et al., “Prevalence of Visually Significant Cataract and Cataract Surgical Coverage in Indigenous and Non-Indigenous Australians,” BMJ Ophthalmology, bmj.com. Mobile theaters and public-private partnerships are therefore emerging to address underserved communities and sustain growth in the ophthalmic surgical devices market.

Accelerating Adoption of Minimally Invasive Glaucoma Surgeries and Combination Cataract-Glaucoma Procedures

MIGS implants such as iStent and Hydrus deliver 20% intraocular-pressure (IOP) reductions in more than 75% of treated eyes at 24 months, transforming the risk–benefit profile of glaucoma surgery. The INTEGRITY study reported 78.2% of iStent infinite eyes meeting the ≥20% IOP-reduction threshold with a 3.3% complication rate, well below conventional trabeculectomy[2]Iqbal I.K. Ahmed et al., “Six-Month Outcomes from a Prospective, Randomized Study of iStent Infinite Versus Hydrus,” Ophthalmology and Therapy, springer.com. Bundling MIGS with cataract extraction allows surgeons to address two diseases in a single sitting, shortening patient recovery and cutting payor costs. Reimbursement codes covering combination procedures are now standard in the United States and parts of Europe, accelerating MIGS penetration and supporting steady expansion of the ophthalmic surgical devices market.

Digital-OR and Image-Guided Technologies Raising Premium-Procedure Uptake

4K digital microscopes, heads-up displays, and AI-powered planning tools have dramatically improved visualization, depth perception, and IOL calculation accuracy. The ZEISS ARTEVO 850 platform raises depth of field by 60%, while the Hill-RBF and Kane formulas outperform legacy biometry methods in refractive predictability. Alcon’s SMARTCataract suite trims pre-operative planning by 13.8 minutes per case, unlocking additional daily slots in high-volume centers. These data-centric ecosystems enhance outcomes and justify premium pricing, reinforcing digital differentiation across the ophthalmic surgical devices market.

Expansion Of ASCs And Day-Care Reimbursement Models Lowering Procedure Costs and Boosting Volume

ASCs now conduct 72.0% of U.S. ophthalmic surgeries at 45-60% lower cost than hospitals and with 20% shorter waits . The Centers for Medicare & Medicaid Services granted a 2.9% ASC fee increase for 2025, widening the economic advantage over inpatient sites[3]Centers for Medicare & Medicaid Services, “Hospital Outpatient Prospective Payment and ASC Systems for CY 2025,” federalregister.gov. High-performing ASCs also post 54% fewer severity-weighted complications. Greater payer acceptance of same-day discharge, combined with miniaturized equipment footprints, is catalyzing a sustained outpatient shift that underpins revenue gains for the ophthalmic surgical devices market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance costs | −0.7% | Global; strongest in emerging markets | Medium term (2-4 years) |

| Divergent & tightening regulatory regimes | −0.5% | Europe, China, other regulated markets | Short term (≤ 2 years) |

| Limited pool of fellowship-trained ophthalmic surgeons | −0.4% | Asia Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Reimbursement compression & pricing caps on premium IOLs and adjunct devices | −0.6% | North America, Japan, China, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital and Maintenance Costs for Advanced Laser and Phaco Systems Challenging ROI for Mid-Size Providers

State-of-the-art femtosecond lasers and digital microscopes command outlays beyond USD 500,000, with annual service contracts topping USD 50,000. Mid-size clinics face stretched payback horizons as downward reimbursement pressure erodes margins, especially where case volumes are modest. Staffing costs compound the burden; shortages of certified technicians force centers to offer premium wages and invest in lengthy training, delaying profitability. Limited capital access in rural territories widens geographic inequality and tempers installation rates, placing a brake on the ophthalmic surgical devices market.

Divergent and Tightening Regulatory Regimes Prolonging Approval Timelines and Compliance Costs

The European Union’s Medical Device Regulation amplifies clinical-evidence demands for both legacy and new products, lengthening time-to-market. China’s NMPA similarly requires full local trials for many imported innovations. Parallel post-market evidence commitments add expense and risk, diverting resources away from R&D and early-stage ventures. Smaller developers often prioritize U.S. pathways—perceived as clearer—before tackling Europe or China, reshuffling global launch sequencing and modestly restraining the ophthalmic surgical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cataract Leadership and Glaucoma Momentum

Cataract systems represented 41.02% of the ophthalmic surgical devices market in 2025, anchored by more than 20 million annual procedures worldwide. Advanced fluidics platforms such as Alcon’s CENTURION Vision System with ACTIVE SENTRY maintain more physiologic intraocular pressure, decreasing endothelial cell loss and expediting recovery. Digital workflow suites bundle biometry, formula calculators, and cloud transfer, elevating throughput and surgeon consistency. Premium femtosecond lasers and toric IOL injectors attract affluent urban centers, whereas purpose-built low-cost phaco packs target volume programs in emerging economies.

Glaucoma surgery devices, especially trabecular micro-bypass stents, are the fastest-growing category with an 8.63% CAGR projected for 2026-2031. Widespread MIGS training, maturing long-term safety data, and pairing with cataract removal expand candidacy. Refractive and vitreo-retinal platforms hold smaller shares yet benefit from innovations such as Zeiss VISUMAX 800 with SMILE pro software, which cuts lenticule creation time below 10 seconds, and dual-mode lasers that bridge cataract and retinal applications. Device makers therefore pursue cross-segment synergies to defend margins and expand the ophthalmic surgical devices market.

By End-User: Hospital Dominance, ASC Acceleration

Hospitals controlled 76.15% of the ophthalmic surgical devices market size in 2025, leveraging full-service infrastructure for complex corneal, retinal, and trauma cases. Many tertiary centers are now investing in heads-up 3D visualization and robotic-assisted cataract surgery device modules to maintain referral flow. However, inpatient growth is tempering as payers encourage site-of-service shifts and surgeons favor streamlined scheduling in specialty centers.

ASCs are climbing at a 6.82% CAGR, supported by CMS fee adjustments and proven clinical quality. Single-specialty ophthalmic facilities post 54% lower severity-weighted complication rates, bolstering patient confidence. Modular room designs permit fast turnover, and high utilization rates shorten equipment payback. Specialty eye clinics and mobile units round out demand, particularly in rural Asia Pacific and sub-Saharan Africa, where nonprofit missions complement public funding to broaden reach for the ophthalmic surgical devices market.

Geography Analysis

North America accounted for 31.75% of global revenue in 2025, underpinned by mature reimbursement frameworks, early adopter surgeon bases, and dense ASC networks. Medicare’s 2.9% ASC fee boost for 2025 and sustained capital budgets at leading academic centers anchor regional stability. Nonetheless, premium IOL reimbursement compression is pressuring pricing, prompting hospitals to renegotiate supply contracts and consolidate purchasing.

Asia Pacific is projected to post a 5.74% CAGR from 2026 to 2031, the fastest pace worldwide. Public blindness-prevention drives in China and India are expanding eligibility, and domestic firms are scaling low-cost phaco units that operate on portable power. Private ophthalmology chains in India secured fresh equity infusions in 2025, earmarked for regional clinic rollouts and training centers. Alongside rising disposable income and urbanization, these factors sustain double-digit unit growth in cataract kits, supporting the broader ophthalmic surgical devices market.

Europe, the Middle East & Africa, and South America collectively represent the remaining share. Europe’s stringent MDR rules have lengthened certification cycles, yet the region continues to innovate in digital microscopes and regenerative corneal implants. Gulf Cooperation Council nations are funding flagship eye institutes that import top-tier systems, whereas many sub-Saharan nations rely on charity-supported mobile theaters to serve remote areas. Brazil and Argentina lead South America in device adoption, but currency swings raise procurement risk and hinder consistent expansion. Across regions, outpatient migration and digital integration remain unifying themes in the ophthalmic surgical devices market.

Competitive Landscape

The top five manufacturers—Alcon Inc., Johnson & Johnson Vision Care, Carl Zeiss Meditec AG, Bausch + Lomb Corp., and Glaukos Corp.—controlled roughly 65.0% of 2024 revenue, signaling a moderately concentrated structure. Carl Zeiss Meditec’s 2025 acquisition of Dutch Ophthalmic Research Center for about EUR 985 million instantly expanded its vitreo-retinal suite and underscores portfolio-driven consolidation. Alcon’s Unity VCS and CS launch integrated vitreoretinal and cataract functions into a common console, advancing workflow synergy and lock-in at high-volume centers.

White-space innovation thrives despite scale advantages. ViaLase’s femtosecond laser image-guided high-precision trabeculotomy (FLigHT) recorded a 34.6% IOP reduction over 24 months without serious adverse events, illustrating nimble entrant differentiation. Regulatory collaboration is also reshaping competition: the FDA validated the Assessment of IntraOcular Lens Implant Symptoms (AIOLIS) tool—co-developed by the American Academy of Ophthalmology, UCLA, Alcon, Bausch + Lomb, Zeiss, and Johnson & Johnson—to quantify patient-reported outcomes in premium IOL trials. Such pre-competitive initiatives streamline study design, accelerating product cycles in the ophthalmic surgical devices market.

Growth strategies blend incremental platform upgrades with selective M&A. Bausch + Lomb’s 2025 CE mark for its LuxLife trifocal IOL fortified its European premium lens lineup, while Glaukos’ 25% year-on-year sales surge to USD 106.7 million in Q1 2025 reflects strong MIGS uptake. Manufacturers are simultaneously localizing supply chains—evident in Alcon’s tariff-mitigation plan—and embedding software subscriptions to create recurring revenue streams across the ophthalmic surgical devices market.

Ophthalmology Surgical Devices Industry Leaders

Alcon Inc

Johnson & Johnson Vision Care

Carl Zeiss Meditec AG

Bausch + Lomb Corp.

Glaukos Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Alcon launched the Unity VCS and CS integrated platforms for vitreoretinal and cataract surgery, enhancing workflow connectivity.

- April 2025: Carl Zeiss Meditec introduced the Micor 700 handpiece in the United States, improving cataract-fluidics control.

- April 2025: Glaukos announced multiple scientific abstracts for the 2025 ASCRS meeting, highlighting second-generation trabecular micro-bypass data and the iDose TR implant.

- May 2025: Bausch + Lomb obtained CE marking for the LuxLife trifocal IOL, expanding its European premium lens range.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the ophthalmology surgical devices market as the value of equipment, implants, and single-use consumables deployed in cataract, glaucoma, refractive, and vitreoretinal surgeries performed in accredited medical facilities worldwide. According to Mordor Intelligence, this definition yielded a 2025 baseline of USD 12.53 billion.

Scope exclusion: Vision-care products (spectacles, contact lenses) and stand-alone diagnostic benches are outside the present scope.

Segmentation Overview

- By Product

- Refractive Surgery Devices

- Glaucoma Surgery Devices

- Cataract Surgery Devices

- Other Surgical Devices

- By End-user

- Hospitals

- Specialty Ophthalmic Clinics

- Ambulatory Surgery Centers (ASCs)

- Other End-users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed ophthalmic surgeons, hospital procurement leads, and regional distributors across North America, Europe, and Asia-Pacific. Their inputs clarified average selling prices, operating-room kit mix, and the pace at which laser-assisted cataract systems replace legacy phaco units, letting us close data gaps flagged during desk work.

Desk Research

We began with structured searches across open datasets such as the WHO blindness registry, the International Agency for the Prevention of Blindness surgery database, and regional procedure logs from bodies like the American Society of Cataract and Refractive Surgery. Trade statistics from UN Comtrade, import alerts posted by the U.S. FDA, and published reimbursement schedules supplied foundational shipment, pricing, and utilization clues.

To ground financial indicators, our analysts tapped company 10-Ks, selected investor decks, and D&B Hoovers for unit revenue splits, then correlated these with peer-reviewed journals that track phacoemulsification uptake and MIGS penetration. Dow Jones Factiva helped us follow real-time plant expansions or recalls that could sway supply. This list is illustrative; many other public and subscription sources supported validation.

Market-Sizing & Forecasting

A top-down model reconstructs global demand from national surgical-volume statistics that are adjusted for day-case conversion, followed by procedure-level device bills of materials. Select bottom-up checks, supplier roll-ups, and sampled ASP × unit probes fine-tune aggregates before finalization. Key variables include cataract prevalence in 60+ cohorts, ASC share of eye surgeries, MIGS adoption curves, phacoemulsification kit ASP trends, hospital capital expenditure cycles, and exchange-rate weighted import values. Forecasts use multivariate regression blended with scenario analysis to reflect population aging, technology diffusion, and reimbursement shifts. Where bottom-up evidence is thin, uplift factors are transparently flagged and revisited once new surveys land.

Data Validation & Update Cycle

Every dataset passes two-step analyst review, then variance checks against external procedure trackers. Anomalies trigger re-contact of sources. Reports refresh annually, with mid-cycle updates when material events, such as major product recalls and guideline changes, occur.

Why Mordor's Ophthalmology Surgical Devices Baseline Commands Dependability

Published estimates often diverge because firms pick different device baskets, price anchors, or refresh cadences.

Key gap drivers here include: some studies fold diagnostic tables and vision-care lenses into 'surgical,' others omit high-value consumables like viscoelastics, while a few apply uniform ASP escalators without regional calibration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.53 B (2025) | Mordor Intelligence | - |

| USD 30.12 B (2024) | Global Consultancy A | Bundles diagnostic and vision-care lines, inflating scope |

| USD 7.70 B (2025) | Trade Journal B | Excludes refractive and vitreoretinal device families |

| USD 8.10 B (2022) | Industry Association C | Older baseline; uses static ASPs, limited geographic coverage |

Taken together, the comparison shows that Mordor's disciplined scope selection, variable-level cross-checks, and yearly refresh deliver a balanced, transparent baseline that decision-makers can replicate and audit.

Key Questions Answered in the Report

What is the current value of the ophthalmic surgical devices market?

The market is valued at USD 13.16 billion in 2026 and is forecast to reach USD 16.84 billion by 2031.

Which product segment leads the ophthalmic surgical devices market?

Cataract surgery devices lead with 41.02% revenue share in 2025 due to high global procedure volumes.

Why are minimally invasive glaucoma surgeries gaining traction?

MIGS implants deliver significant IOP reductions with lower complication rates, and combining them with cataract surgery addresses two conditions in one procedure, boosting adoption.

How is outpatient migration influencing device demand?

ASCs now perform 72% of U.S. ophthalmic surgeries at lower cost and with shorter waits, accelerating equipment purchases tailored to high-throughput outpatient settings.

Which region is growing fastest in the ophthalmic surgical devices market?

Asia Pacific is projected to expand at a 5.74% CAGR from 2026 to 2031, driven by improving healthcare infrastructure and public blindness-prevention initiatives.

What are the main hurdles limiting wider device uptake?

High capital costs for advanced systems and divergent regulatory requirements that prolong approvals are the leading restraints cited by manufacturers and providers.

Page last updated on: