Laser Measuring Instrument Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

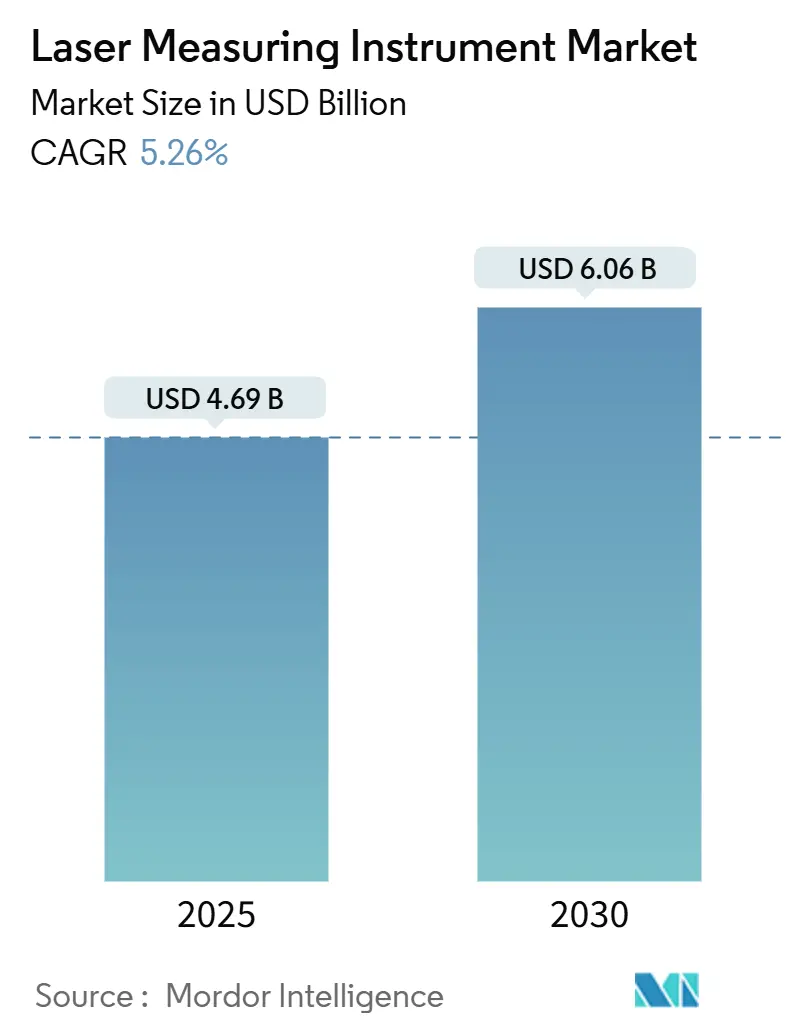

| Market Size (2025) | USD 4.69 Billion |

| Market Size (2030) | USD 6.06 Billion |

| Growth Rate (2025 - 2030) | 5.26% CAGR |

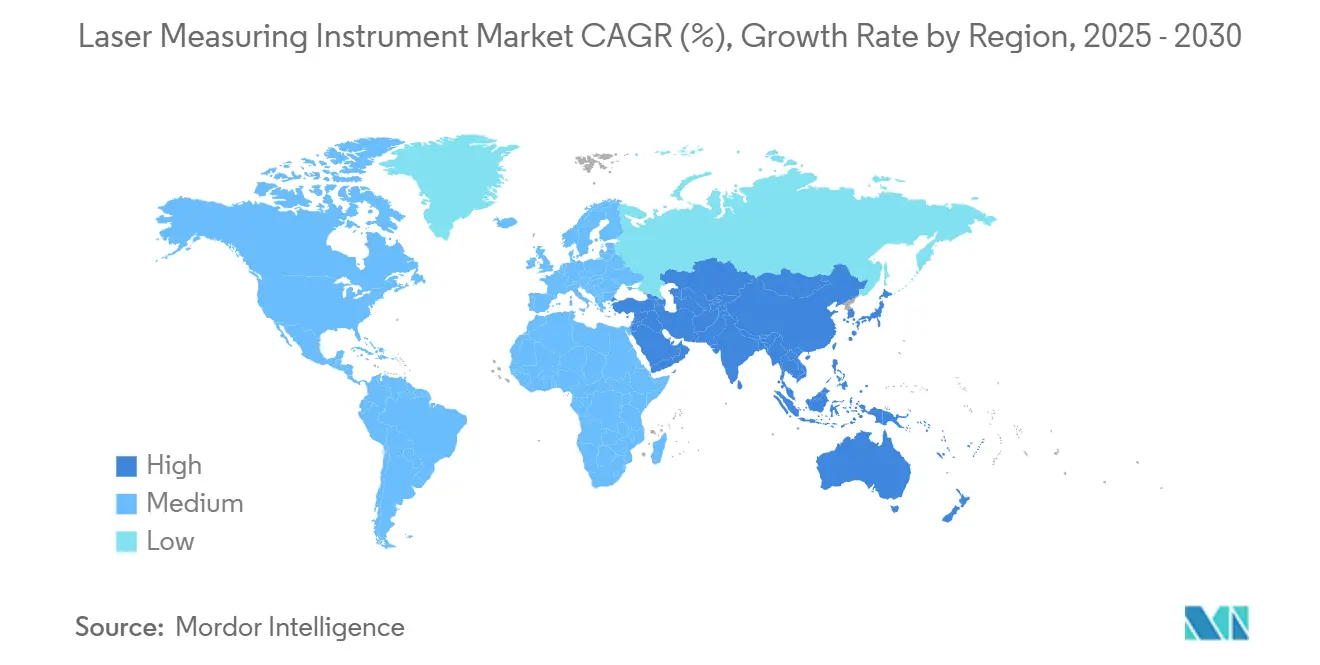

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laser Measuring Instrument Market Analysis by Mordor Intelligence

The laser measuring instrument market size is USD 4.69 billion in 2025 and is forecast to reach USD 6.06 billion by 2030, advancing at a 5.26% CAGR. Systematic integration into construction, manufacturing and smart-city workflows anchors demand, while Building Information Modeling (BIM) mandates, LiDAR-enabled urban planning and tighter automotive quality regulations reinforce steady equipment refresh cycles. Platform strategies that bundle hardware, analytics and cloud subscriptions are reshaping purchasing criteria, helping vendors overcome capital-expenditure hurdles during periods of interest-rate volatility. Supply-chain localization for photonic components is slowly easing lead-time risk, yet the sector must still navigate semiconductor bottlenecks and a widening skills gap for metrology specialists. Competitive advantage is moving toward companies able to fuse laser data with artificial intelligence, creating predictive maintenance and real-time decision support capabilities that justify premium pricing.

Key Report Takeaways

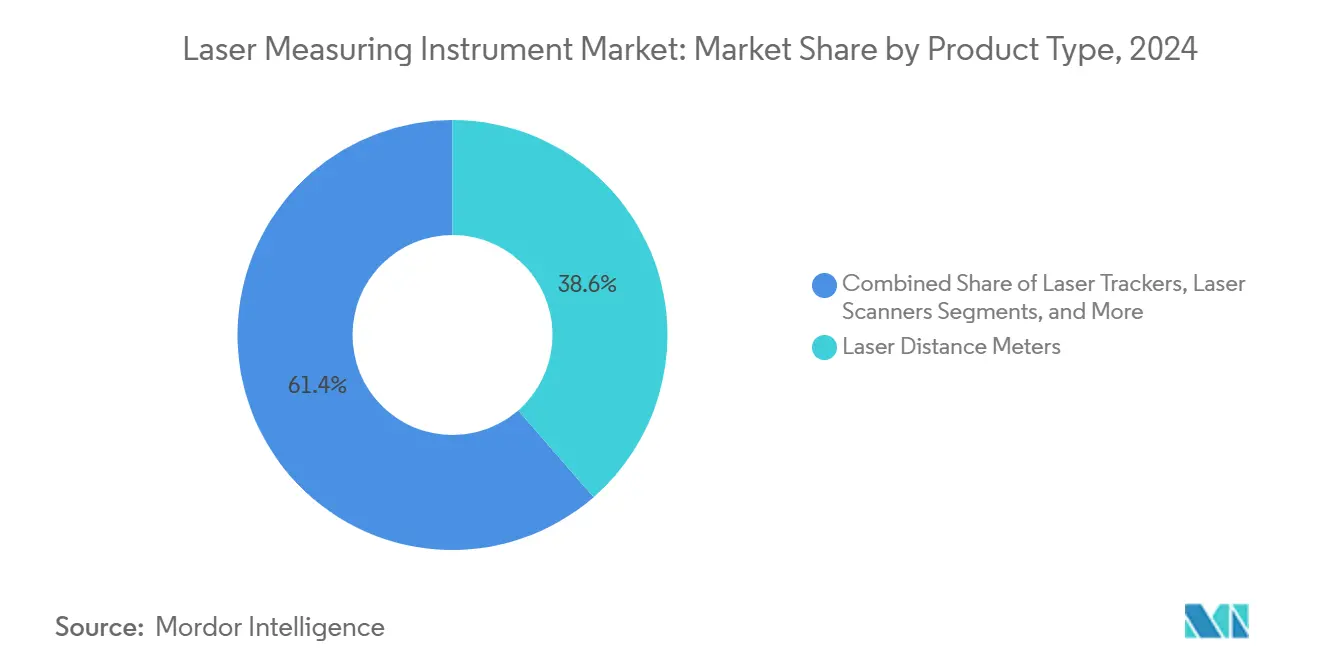

- By product type, laser distance meters accounted for 38.6% of the laser measuring instrument market share in 2024, while laser trackers are projected to expand at a 6.1% CAGR through 2030.

- By technology, time-of-flight held 41.3% share of the laser measuring instrument market size in 2024, whereas triangulation is on course for a 6.5% CAGR to 2030.

- By range, mid-range systems captured 61.2% revenue share in 2024 and long-range devices are forecast to record a 7.1% CAGR over 2025-2030.

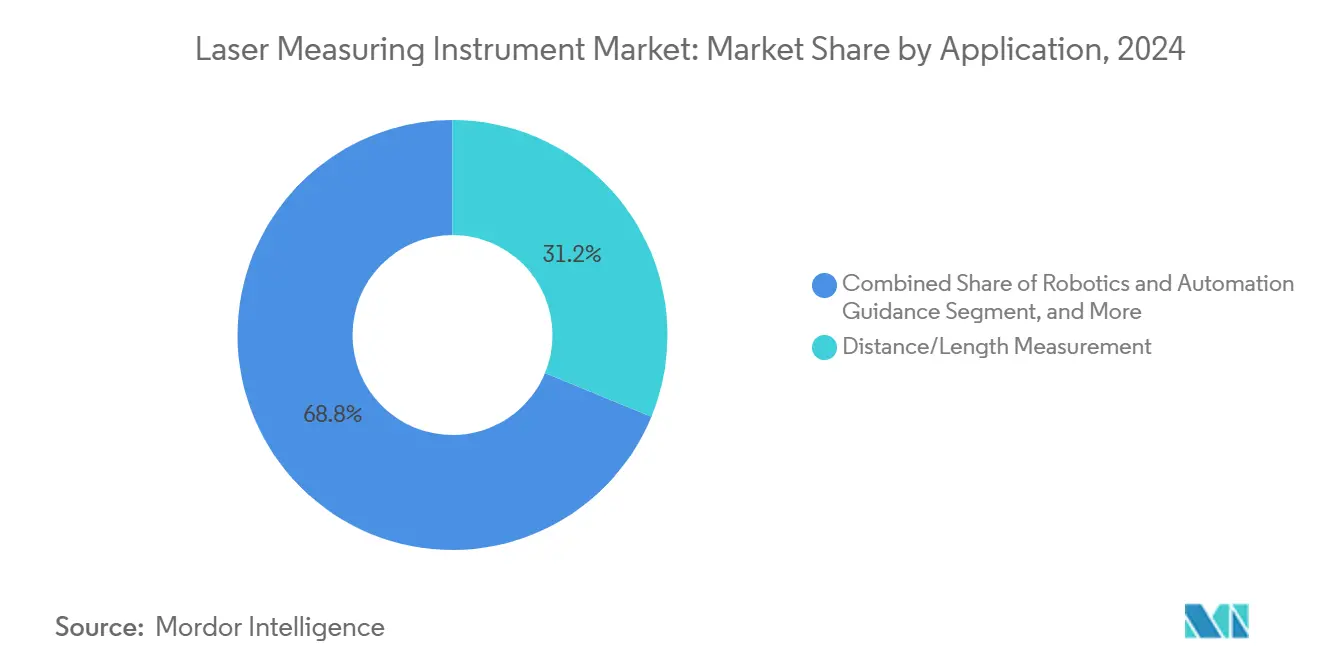

- By application, distance measurement represented 31.2% of the laser measuring instrument market size in 2024; robotics and automation guidance is advancing at a 5.7% CAGR.

- By end-user industry, construction led with 22.5% revenue share in 2024, while manufacturing and industrial automation is projected to grow at a 5.4% CAGR.

- By geography, North America contributed 37.9% revenue in 2024 and Asia-Pacific is poised for a 6.8% CAGR during the outlook period.

Global Laser Measuring Instrument Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of laser distance meters in construction and BIM workflows | +1.1% | Global, with early gains in North America and EU | Medium term (2-4 years) |

| Growing 3-D inspection demand in automotive and aerospace manufacturing | +0.8% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Rising use of laser displacement sensors in robotics and automation | +0.6% | APAC manufacturing hubs, expanding to MEA | Medium term (2-4 years) |

| Expanding LiDAR deployments in surveying and smart-city projects | +0.5% | Global urban centers, government-led initiatives | Long term (≥ 4 years) |

| AR/VR-integrated laser metrology for real-time field measurement | +0.4% | North America and EU early adopters | Long term (≥ 4 years) |

| Consumer-grade fiber-laser ranging modules for smartphones and wearables | +0.3% | Global consumer markets, led by Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Laser Distance Meters in Construction and BIM Workflows

Mandatory BIM compliance is turning laser distance meters into everyday site tools that feed 3-D point-cloud data directly into digital-twin models. Contractors cite project-delay reductions of up to 75% after shifting from manual tape measurements to integrated laser workflows. Autonomous ground robots equipped with LiDAR now patrol sites, overlaying scans against BIM files to flag alignment deviations before concrete cures. These efficiency gains help mid-sized firms justify the capital outlay despite thin construction margins. Equipment suppliers are embedding inertial odometry to maintain accuracy on uneven terrain, and cloud connectors allow architects to visualize progress in near real time. Growing availability of subscription-based software further lowers the entry barrier and accelerates fleet upgrades among regional builders.

Growing 3-D Inspection Demand in Automotive and Aerospace Manufacturing

Automotive body-in-white lines and aerospace MRO shops increasingly specify laser trackers that capture thousands of points per second, slashing inspection cycles by 75% and preventing probe-induced part damage. Smartphone-linked gap-and-flush systems give operators immediate feedback on assembly tolerances and feed dashboards that support Industry 4.0 analytics. As aviation regulators tighten traceability norms, laser coordinate measuring machines are becoming mandatory for turbine blade core checks, driving recurring calibration contracts for OEMs. The resulting data lakes enable predictive quality algorithms that flag drift before defects occur, reinforcing the shift from point tools to connected measurement ecosystems.

Rising Use of Laser Displacement Sensors in Robotics and Automation

Smart factories deploy laser displacement sensors for real-time robot positioning with ±0.001-inch accuracy inside 20-foot work envelopes. Edge-to-cloud architectures route sensor data through fog nodes to machine-learning models that cut cycle times by half and improve first-pass yield above 95%. Labor shortages across aging industrial workforces accelerate adoption, and payback periods under two years keep boardroom support strong even when macro conditions soften. Component miniaturization is extending metrology-grade sensing into collaborative robots, warehouse AGVs and medical‐service robots, widening addressable volume for sensor suppliers.

Expanding LiDAR Deployments in Surveying and Smart-City Projects

Municipal agencies now specify roadside LiDAR for traffic adaptive control, with Utah’s pilot system improving peak-hour throughput by double-digit percentages. Single-photon LiDAR arrays can log more than 14 million points per second, making airborne corridor mapping economical for power utilities and telecoms. IEEE research shows spatiotemporal algorithms boosting static-object discrimination by 10%, enhancing autonomous-vehicle safety on busy downtown grids. Long-range accuracy gains open revenue streams in environmental monitoring and flood-risk modeling, while federal infrastructure grants de-risk early deployments in smaller cities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of precision laser instruments | -0.7% | Global, particularly affecting SMEs | Short term (≤ 2 years) |

| Shortage of skilled operators and training programs | -0.4% | Developed markets with aging workforce | Medium term (2-4 years) |

| Photonic-chip supply bottlenecks causing lead-time volatility | -0.3% | Global, with acute impact on APAC manufacturing | Short term (≤ 2 years) |

| Cyber-security compliance hurdles for connected laser devices | -0.2% | North America and EU regulatory markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Precision Laser Instruments

Enterprise-grade laser trackers list between USD 100,000 and USD 500,000, a hurdle for small manufacturers coping with inflation-driven borrowing costs. Although ROI modeling often shows payback inside three years, CFOs remain cautious when cash flows tighten. Low-cost AR-based systems are emerging but trade range for price, constraining them to lab settings. Vendors respond with leasing and usage-based pricing that convert capex to opex and bundle calibration into multiyear service agreements.

Shortage of Skilled Operators and Training Programs

Retiring baby-boom metrologists leave a void that universities have yet to fill; Purdue Polytechnic’s outreach highlights the scarcity of structured curricula in dimensional measurement. Modern systems require hybrid software-mechanical skill sets, stretching onboarding to 12 months for inexperienced hires. OEM-run academies and augmented-reality training aids are mitigating the gap, but widespread proficiency remains at least two years out, moderating near-term adoption velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Distance Meters Lead Tracker Innovation

Laser distance meters held 38.6% of the laser measuring instrument market size in 2024, underpinned by construction digitization mandates on every continent. Contractors favor the category’s handheld ergonomics and Bluetooth-enabled data transfer that injects measurements directly into BIM software. At the opposite end, laser trackers are registering the fastest 6.1% CAGR as aerospace MRO shops overhaul turbine blades and auto plants monitor body-in-white geometry. Vendors now sell distance meters and trackers on common firmware, unifying user interfaces and shortening operator learning curves. Subscription analytics that compare site scans against design intent lock customers into multi-product ecosystems and lift lifetime value.

A growing mid-tier of displacement sensors and 3-D scanners is addressing robotics, heritage-building documentation and consumer smartphone LiDAR. Leica’s AP20 AutoPole exemplifies the pivot toward edge-intelligent accessories that correct tilt error and auto-record pole height, eliminating re-work for survey crews.[1]Leica Geosystems, “The AP20 AutoPole,” leica-geosystems.com Product roadmaps are converging around modular optics and cloud microservices, enabling companies to push firmware upgrades that add functionality without new hardware. The competitive focus therefore shifts from single-device accuracy to holistic workflow efficiency, reinforcing revenue resilience in the laser measuring instrument market.

By Technology: Time-of-Flight Dominance Faces Triangulation Challenge

Time-of-flight systems accounted for 41.3% laser measuring instrument market share in 2024, prized for their long-range capability and mature supply chain. The architecture remains the default in infrastructure surveying and autonomous-vehicle perception because it balances cost with meter-level precision over hundreds of meters. Triangulation, growing at 6.5% CAGR, is eroding this lead in semiconductor and medical device plants where sub-millimeter tolerances are non-negotiable. Declining laser-diode costs and advances in CMOS sensors make triangulation more affordable, pressing incumbent vendors to hybridize platforms.

Interferometry and phase-shift niches cater to research labs and high-speed inspection cells that value nanometer resolution or microsecond acquisition. Korea’s optical frequency-comb breakthrough promises 0.34-nanometer field precision, hinting that interferometry could vault into mainstream metrology once packaging scales. As customers evaluate accuracy-versus-cost trade-offs, vendors that flexibly integrate multiple methods within unified software stand to capture widening cross-segment opportunities in the laser measuring instrument market.

By Range: Mid-Range Applications Drive Long-Range Growth

Systems covering 30-300 meters delivered 61.2% of 2024 revenue, illustrating how construction, plant maintenance and asset digitization dominate purchase orders. Compact battery packs and ergonomic housings keep weight under 2 kilograms, letting one operator scan multi-story structures in a single shift. Long-range units beyond 300 meters, although only a 14% slice today, will grow at a 7.1% CAGR as smart-city LiDAR corridors, aerospace hangar inspections and offshore wind-farm surveys demand extended throw distances. Battery energy density improvements and single-photon detection efficiencies will ease historic trade-offs between range, weight and scan speed.

Short-range sensors under 30 meters remain vital to robotics arms, pick-and-place machines and medical imaging beds. Chip-scale lasers smaller than a penny underscore a miniaturization pathway that could soon embed metrology-grade rangefinding into consumer devices. Range segmentation is therefore blurring, and future competitive advantage will hinge on firmware that dynamically tunes pulse energy and timing to extend a single device across multiple distance bands, enhancing addressable volume within the laser measuring instrument market.

By Application: Distance Measurement Anchors Robotics Expansion

Distance and length measurement retained 31.2% share of 2024 revenue, proving that simple point-to-point tasks remain the entry gateway for first-time buyers. Real-time data logging into construction management platforms ensures adoption stays sticky. Meanwhile robotics and automation guidance will post the fastest 5.7% CAGR through 2030 as labor shortages accelerate cobot deployments across electronics, warehousing and food processing. Laser displacement sensors mounted on six-axis robots deliver closed-loop calibration mid-cycle, driving scrap rates below 2%.

3-D scanning and modeling benefit from renewed interest in digital twins for predictive maintenance and heritage preservation projects. Quality control and inspection adopt both fixed-station scanners and portable arms that feed statistical process control dashboards. Healthcare, environmental monitoring and consumer electronics form an “edge-application” cluster where miniaturized, lower-power lasers create new revenue micro-pockets, broadening the laser measuring instrument market reach.

By End-User Industry: Construction Leadership Meets Manufacturing Automation

Construction and infrastructure projects produced 22.5% of sales in 2024, as public-sector funding and BIM mandates institutionalized laser metrology on site. Large contractors now bundle equipment rental, data hosting and analytics into single RFPs, stabilizing multiyear demand pipelines. Manufacturing and industrial automation is the fastest-growing end-user at 5.4% CAGR, leveraging continuous in-line measurement to enforce zero-defect policies on automotive body panels and smartphone casings.

Aerospace and defense require periodic laser tracker recalibration for airframe overhaul, generating high-margin service contracts. Energy and utilities rely on LiDAR for pipeline alignment and turbine blade inspection, while mining firms test laser-induced breakdown spectroscopy to grade ore quality in real time. Consumer electronics firms integrate LiDAR in flagship smartphones, exposing a mass-market user base to measurement technology and indirectly boosting professional-grade upgrades, widening the funnel for the laser measuring instrument industry.

Geography Analysis

North America controlled 37.9% of 2024 revenue, sustained by aerospace, defense and precision manufacturing clusters that demand higher-margin, integrated solutions. Vendors are embedding AI and cloud subscriptions, with Trimble’s 17% year-over-year recurring-revenue growth illustrating the model’s stickiness. Currency-adjusted cost pressures, however, are prompting procurement teams to trial lower-priced imports for non-mission-critical tasks.

Asia-Pacific is on a 6.8% CAGR trajectory as China’s smart-manufacturing subsidies, South Korea’s semiconductor boom and Japan’s robotics leadership compound into large-volume instrument orders. Domestic photonics supply chains trim lead times and allow rapid iteration of low-mid price tiers, challenging European and North American incumbents. Regional OEMs such as Kyocera are integrating camera-LIDAR fusion sensors that collapse two bill-of-materials lines into one, compressing costs and paving the way for parallax-free perception in autonomous vehicles.

Europe retains a solid share on automotive and medical-device strengths, and photonics production climbed to EUR 124.6 billion in 2022. Yet geopolitical uncertainty over raw-material sourcing and export controls may temper growth. Hexagon’s five-year roadmap emphasizes single-photon LiDAR and SaaS add-ons that mitigate hardware margin compression.[2]Hexagon AB, “Annual and Sustainability Report 2023,” hexagon.com The continent’s embrace of sustainability regulation also favors devices that offer embedded carbon-footprint tracking, nudging niche growth in environmental monitoring within the laser measuring instrument market.

Competitive Landscape

Market concentration sits in the mid-range, with the top five vendors holding roughly 40% combined revenue-enough to wield scale, but far from monopoly control. Hexagon’s Leica Geosystems, FARO Technologies and Bosch occupy the premium tier, bundling hardware with analytics suites that lock customers into multiyear licenses. AMETEK’s Virtek pickup extends its projection and inspection offerings deeper into aerospace and industrial automation niches. MKS’s USD 5.1 billion Atotech merger links laser processing with electro-plating, creating a “one-stop” electronics-manufacturing platform.

Asian challengers are closing feature gaps by leapfrogging into camera-LiDAR sensor fusion, as Kyocera’s 2025 launch shows. Local Chinese firms leverage cluster economics in Shenzhen to undercut on price while approaching Western accuracy benchmarks. Meanwhile U.S. vendors push cloud-first roadmaps; FARO reports consecutive double-digit EBITDA margins after pivoting toward subscription-heavy scanners and arms.[3]FARO Technologies Inc., “Third Quarter Financial Results,” faro.comThe competitive narrative therefore revolves around who can monetize data faster, not who can hit the lowest micrometer.

Strategic partnerships with cloud hyperscalers, machine-vision specialists and robotics integrators accelerate ecosystem building. Vendors increasingly expose APIs, letting third parties insert task-specific apps into measurement workflows. This “app store” dynamic echoes smartphone economics and could tilt bargaining power toward platform owners, potentially triggering another consolidation wave within the laser measuring instrument market.

Laser Measuring Instrument Industry Leaders

Keyence Corporation

Panasonic Holdings Corporation

Fluke Corporation

OMRON Corporation

Teledyne Technologies Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kyocera unveiled the world’s first camera-LiDAR fusion sensor that eliminates parallax and boosts long-distance detection accuracy for autonomous vehicles.

- January 2025: ams OSRAM introduced an eight-channel 915 nm pulsed laser delivering 1,000 W peak optical power, the first AEC-Q102 qualified device for long-range LiDAR in robo-taxis.

- October 2024: AMETEK closed its acquisition of Virtek Vision International, adding 3-D laser projection and smart-camera inspection to its automation portfolio.

- September 2024: Leica Geosystems launched the 0.75 kg GS05 GNSS Smart Antenna with calibration-free tilt, integrating UHF, 4G, Wi-Fi and Bluetooth for survey efficiency.

Global Laser Measuring Instrument Market Report Scope

| Laser Distance Meters |

| Laser Trackers |

| Laser Displacement Sensors |

| Laser Scanners |

| Other Product Types |

| Time-of-Flight |

| Triangulation |

| Interferometry |

| Phase-Shift |

| Other Technologies |

| Short-Range (Less than 30 m) |

| Mid-Range (30-300 m) |

| Long-Range (Greater than 300 m) |

| Distance / Length Measurement |

| Alignment and Leveling |

| 3-D Scanning and Modeling |

| Quality Control and Inspection |

| Robotics and Automation Guidance |

| Other Applications |

| Construction and Infrastructure |

| Manufacturing and Industrial Automation |

| Automotive |

| Aerospace and Defense |

| Energy and Utilities |

| Mining and Geology |

| Consumer Electronics |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Laser Distance Meters | ||

| Laser Trackers | |||

| Laser Displacement Sensors | |||

| Laser Scanners | |||

| Other Product Types | |||

| By Technology | Time-of-Flight | ||

| Triangulation | |||

| Interferometry | |||

| Phase-Shift | |||

| Other Technologies | |||

| By Range | Short-Range (Less than 30 m) | ||

| Mid-Range (30-300 m) | |||

| Long-Range (Greater than 300 m) | |||

| By Application | Distance / Length Measurement | ||

| Alignment and Leveling | |||

| 3-D Scanning and Modeling | |||

| Quality Control and Inspection | |||

| Robotics and Automation Guidance | |||

| Other Applications | |||

| By End-User Industry | Construction and Infrastructure | ||

| Manufacturing and Industrial Automation | |||

| Automotive | |||

| Aerospace and Defense | |||

| Energy and Utilities | |||

| Mining and Geology | |||

| Consumer Electronics | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 value of the laser measuring instrument market?

The market stands at USD 4.69 billion in 2025.

How quickly is Asia-Pacific demand expected to grow?

Asia-Pacific revenue is projected to expand at a 6.8% CAGR through 2030.

Which product category currently holds the largest share?

Laser distance meters lead with 38.6% share of 2024 revenue.

Which application will expand fastest by 2030?

Robotics and automation guidance is forecast to grow at a 5.7% CAGR.

What factor most limits small-company adoption?

High upfront cost of precision instruments remains the primary barrier, trimming forecast CAGR by 0.7%.

Which technology leads long-range infrastructure projects?

Time-of-flight systems dominate because they balance cost with reliable accuracy over hundreds of meters.

Page last updated on: