Ultraviolet Analyzer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.48 Billion |

| Market Size (2030) | USD 2.01 Billion |

| Growth Rate (2025 - 2030) | 6.31% CAGR |

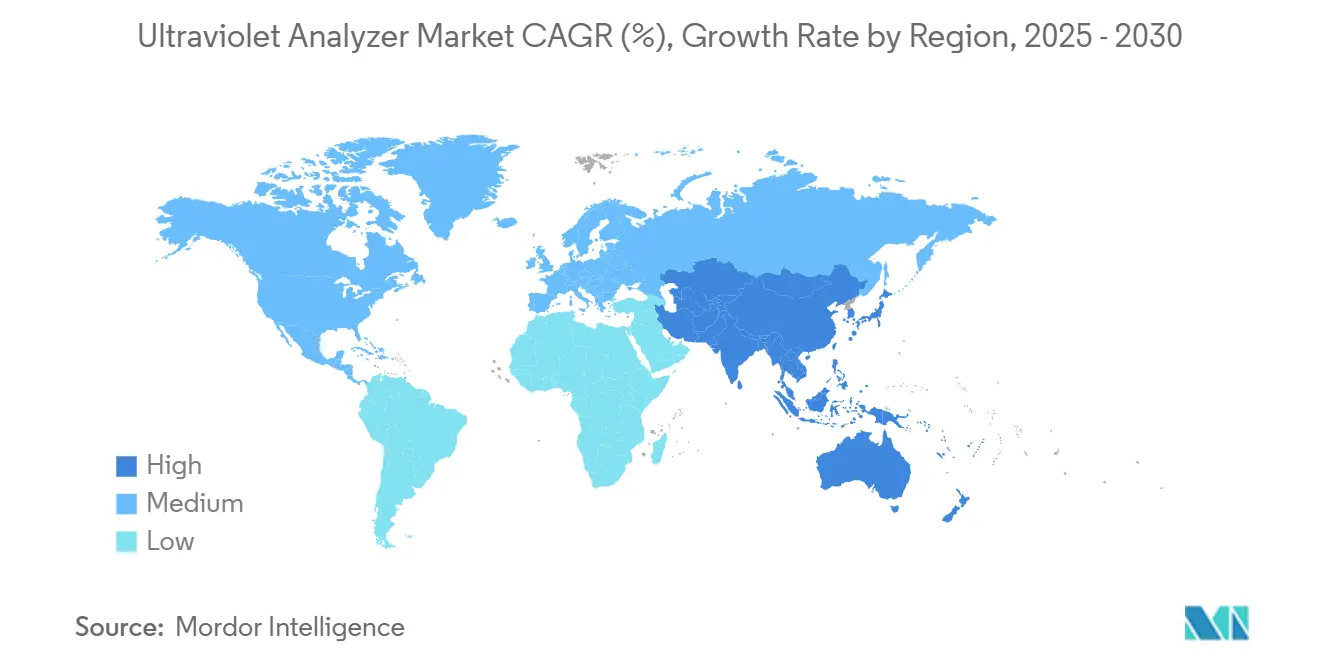

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

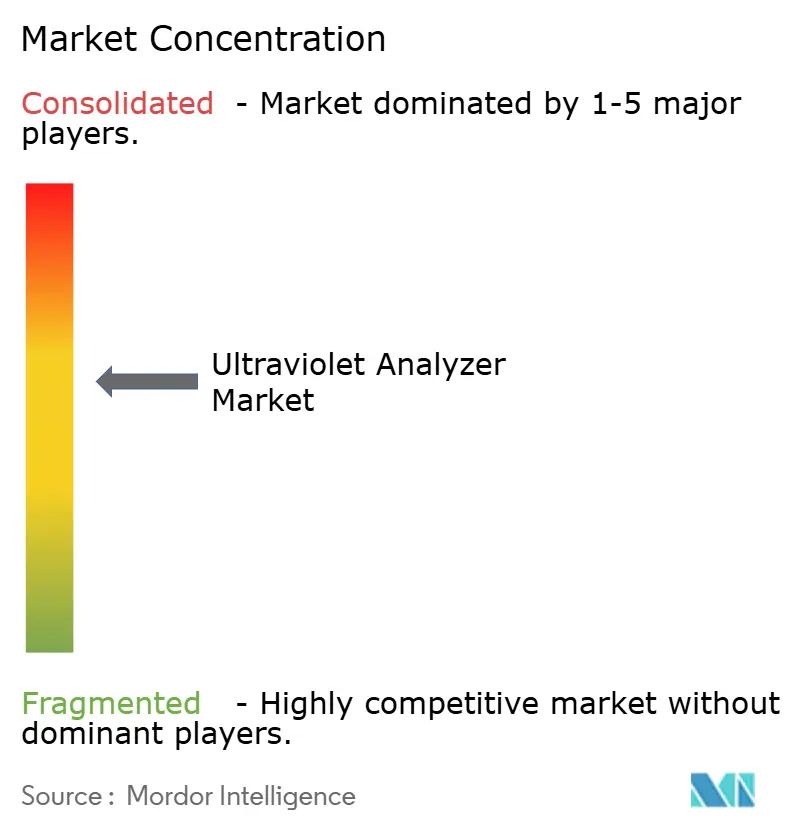

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultraviolet Analyzer Market Analysis by Mordor Intelligence

The Ultraviolet analyzer market size was USD 1.48 billion in 2025 and is projected to reach USD 2.01 billion by 2030, growing at a 6.31% CAGR during the forecast period. Regulatory pressure from the U.S. Environmental Protection Agency, the European Union, and several Asian governments is compelling utilities and industrial facilities to install real-time spectroscopic instruments that verify water, air, and process streams for compliance. Digitalization programs in process industries demand instruments that integrate with supervisory control and data acquisition systems, which reinforces demand for network-ready analyzers. The accelerating rollout of advanced wastewater treatment plants in the Asia-Pacific, combined with the widespread adoption of Process Analytical Technology in North American and European pharmaceutical plants, is further expanding the application base. Edge-enabled platforms that combine ultraviolet sensing with artificial intelligence are transitioning from pilot trials to commercial scale, marking a strategic shift toward autonomous quality decisions at the point of use. Parallel miniaturization initiatives have cut analyzer footprint and power draw, thereby opening sizable opportunities in field testing and remote environmental monitoring.

Key Report Takeaways

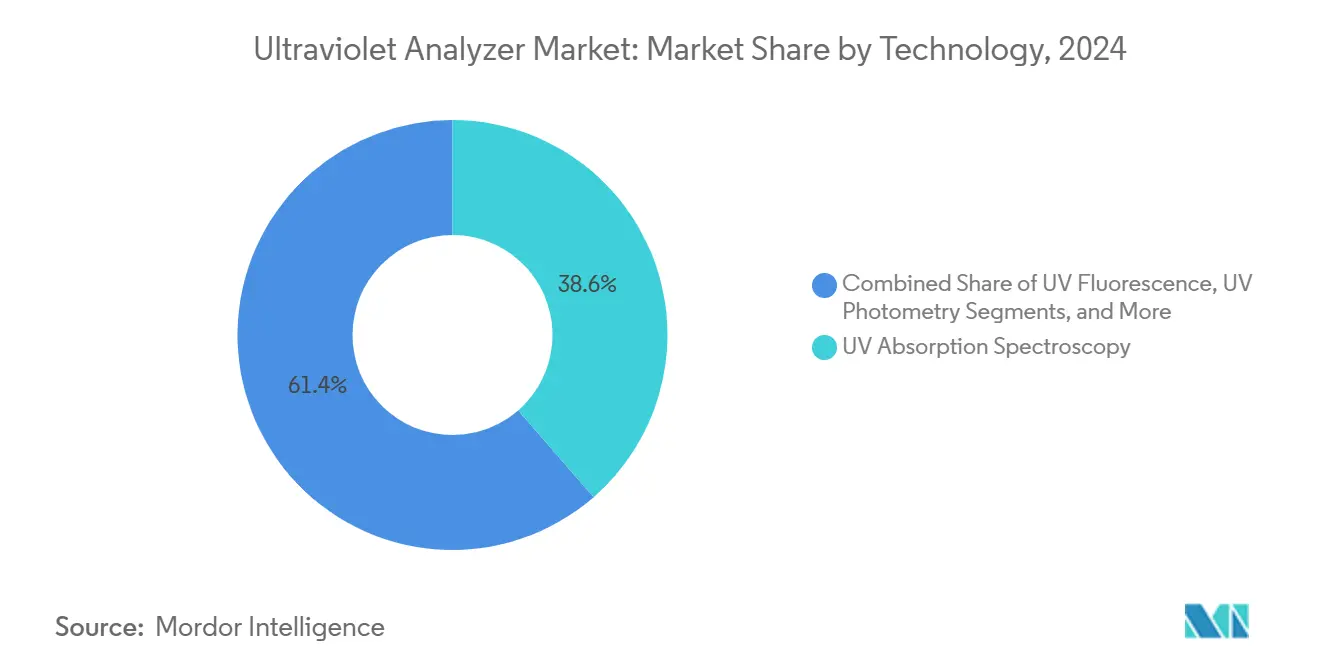

- By technology, ultraviolet absorption spectroscopy led the ultraviolet analyzer market with a 38.60% market share in 2024, whereas hybrid and multi-wavelength systems are forecast to expand at a 7.50% CAGR through 2030.

- By end-user industry, municipal utilities accounted for 31.20% of the ultraviolet analyzer market size in 2024, while the oil and gas sector is projected to record the fastest growth, with a 7.20% CAGR from 2024 to 2030.

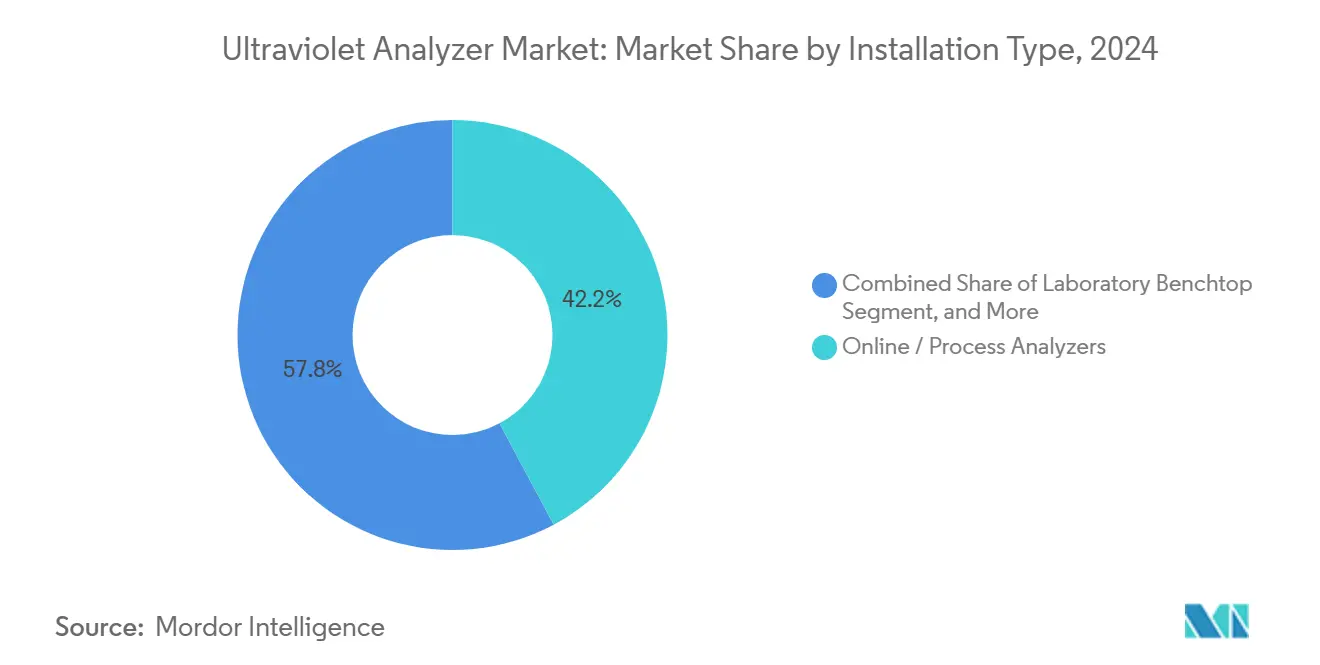

- By installation type, online process analyzers accounted for 42.20% of the revenue ultraviolet analyzer market in 2024, and portable handheld units are projected to grow at a 7.90% CAGR over the same horizon.

- By geography, the Asia-Pacific region captured a 31.10% revenue share ultraviolet analyzer market in 2024 and is advancing at a leading 8.10% CAGR toward 2030.

Global Ultraviolet Analyzer Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent Environmental Regulations on Water Quality Monitoring | +1.8% | North America, the European Union, and global influence | Long term (≥ 4 years) |

| Growing Adoption of Process Analytical Technology in Pharmaceuticals | +1.2% | North America and the European Union, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Expansion of Municipal Wastewater Treatment Infrastructure | +0.9% | Asia-Pacific core, rising in the Middle East and Africa | Long term (≥ 4 years) |

| Increasing Industrial Focus on Emission Control Compliance | +0.8% | Global, the earliest uptake in developed markets | Medium term (2-4 years) |

| Rapid Miniaturization Enabling Portable UV Analyzer Deployment | +0.7% | Global, with particular strength in field applications | Short term (≤ 2 years) |

| Integration of UV Analyzers with Edge AI for Real-Time Quality Decisions | +0.6% | North America and Europe leading, Asia-Pacific following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Regulations on Water Quality Monitoring

Governments are enlarging the list of regulated contaminants, which keeps the Ultraviolet analyzer market on a multiyear procurement cycle. The EPA mandate covering 460 nitrogen dioxide monitoring sites, the Mercury and Air Toxics Standards for fossil plants, and gasoline distribution rules that target benzene and toluene have all raised analytical performance thresholds.[1]U.S. Environmental Protection Agency, “Air Quality Analysis for NO2 NAAQS Review,” epa.gov Facilities that deploy continuous UV-based systems reduce unplanned shutdowns and demonstrate superior environmental performance on their scorecards to investors and communities. Municipalities benefit from automated correlation between ultraviolet absorbance at 254 nm and total organic carbon, which enables rapid adjustments to disinfection. Early adopters translate compliance into competitive advantages, measured through lower fines, faster permitting, and stronger environmental, social, and governance ratings. The resulting demand pull stabilizes revenues for suppliers and drives incremental innovation, such as self-cleaning optical paths that cut downtime.

Growing Adoption of Process Analytical Technology in Pharma

The U.S. Food and Drug Administration's Quality by Design framework has enabled ultraviolet spectroscopy to transition from the lab bench to production suites.[2]U.S. Food and Drug Administration, “Pharmaceutical cGMPs,” fda.gov Inline ultraviolet probes now verify active pharmaceutical ingredient concentration and impurity levels in real-time, which reduces batch rejection by as much as 30% compared to legacy offline sampling. Short analytical cycles also enable continuous manufacturing lines, which reduce work-in-progress inventory and expedite product release. European regulators have mirrored the FDA stance, pushing manufacturers in Germany, the United Kingdom, and France to invest in integrated sensors. Vendors offering validated chemometric libraries gain a defensible position because pharmaceutical plants require pre-approved methods. The ongoing expansion of biologics and personalized therapies further amplifies demand for ultraviolet analyzers that can detect low-concentration species without complex sample preparation.

Expansion of Municipal Wastewater Treatment Infrastructure

Rapid urbanization in China, India, Indonesia, and Vietnam has led to the development of large build-operate-transfer projects for advanced wastewater treatment plants. Each facility specifies multichannel ultraviolet systems to monitor biochemical oxygen demand, chemical oxygen demand, and UV transmittance in a single optical head. Operators rely on continuous data streams to maintain pathogen inactivation targets while reducing energy use in ultraviolet disinfection lines, which often account for 15-25% of a plant's electricity load.[3]National Institute of Standards and Technology, “Ultraviolet Spectral Comparator Facility,” nist.gov Combined measurement of dissolved organic carbon and nitrate allows tighter nutrient removal control that supports zero-liquid-discharge initiatives. Multiyear funding vehicles from the Asian Development Bank stabilize capital outlays, while similar infrastructure grants in the Middle East are driving first-time adoption. Vendors that bundle cloud dashboards with predictive maintenance add tangible value for municipalities facing skills shortages.

Increasing Industrial Focus on Emission Control Compliance

The automotive, chemical, and metal industries face overlapping emission caps for nitrogen oxides, sulfur oxides, and volatile organic compounds that will come into force between 2027 and 2032. The Ultraviolet analyzer market benefits from ultraviolet absorption, which detects multiple pollutants at sub-ppm levels, and fluorescence modules, which add selectivity for aromatic compounds. Integration with distributed control systems enables operators to adjust combustion settings in real-time, reducing fuel consumption and minimizing catalyst degradation. Suppliers that offer ruggedized probes capable of withstanding high temperatures and corrosive gases secure long-term service agreements. The same hardware addresses refinery flare stacks and petrochemical vent streams, giving vendors cross-sector leverage that supports economies of scale. These compliance-driven installs lay the groundwork for future edge-AI retrofits that automate alarm thresholds.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Initial Capital and Maintenance Costs | -0.7% | Global, pronounced among small and midsize enterprises | Short term (≤ 2 years) |

| Limited Skilled Personnel for Ultraviolet Spectroscopy Operation | -0.5% | Global, acute in developing regions | Long term (≥ 4 years) |

| Interference from Emerging Disinfection Chemicals Affecting Accuracy | -0.4% | North America and Europe primarily | Medium term (2-4 years) |

| Cybersecurity Concerns in Networked Process Analyzers | -0.3% | Global, with heightened concerns in the critical infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Capital and Maintenance Costs

Advanced multi-wavelength analyzers with automatic cleaning and sampling modules cost USD 50,000-200,000, which strains the budgets of small utilities and mid-tier manufacturers. Annual service contracts add 10-15% of capital value and cover calibration, lamp replacement, and software upgrades. Many operators underestimate the integration expenses, including fiber-optic runs, sample conditioning, and compliance documentation. Unexpected downtime during maintenance interrupts production and inflates the total cost of ownership. Leasing and performance-based agreements offer partial relief, yet accounting rules in several jurisdictions still classify them as capital commitments, which prolongs approval cycles and delays adoption.

Limited Skilled Personnel for Ultraviolet Spectroscopy Operation

The National Science Board's survey of analytical laboratories revealed a persistent shortage of spectroscopy technicians. Training in method development, chemometrics, and compliance documentation remains limited, particularly in emerging markets. Although vendors provide web-based tutorials and remote diagnostics, complex troubleshooting often requires on-site expertise. Pharmaceutical and petrochemical plants compete for the same constrained talent pool, resulting in higher wage costs and increased staff turnover. These skill shortages extend project commissioning timelines and hinder the deployment of new ultraviolet systems, especially in regions where universities have yet to advance in applied spectroscopy education.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Spectroscopic Diversity Drives Innovation

Ultraviolet absorption systems retained a 38.60% market share in the ultraviolet analyzer market in 2024, due to their proven reliability in water treatment and pharmaceutical settings. Hybrid and multi-wavelength platforms are forecast to register a 7.50% CAGR through 2030 as users demand simultaneous monitoring of organic contaminants and disinfection efficacy. The Ultraviolet analyzer market size for hybrid designs is projected to expand steadily, as one unit can replace multiple sensors for parallel absorption, fluorescence, and photometric measurements. Vendors such as TU Graz have demonstrated broadband near-ultraviolet dual-comb spectrometers that capture the dynamics of formaldehyde and nitrogen oxides with high temporal resolution.[4]Graz University of Technology, “Novel UV Broadband Spectrometer Revolutionizes Air Pollutant Analysis,” tugraz.at Flexible firmware upgrades enable new analytes to be added without hardware swaps, which lengthens product life and aligns with sustainability goals.

Growing interest in predictive maintenance is fueling the development of self-diagnosing optical benches that track lamp intensity, stray light, and fouling in real-time. These features lower total lifecycle cost and enhance data integrity, two priorities for regulated sectors. Open-protocol communication standards, such as OPC UA, simplify enterprise resource planning integration and support remote audits. The Ultraviolet analyzer market, therefore, rewards suppliers that balance core optical performance with digital attributes such as encrypted data transmission and containerized firmware updates. of

By End-User Industry: Municipal Leadership Meets Energy Sector Growth

Municipal utilities accounted for 31.20% of the Ultraviolet analyzer market size in 2024, as every disinfection train relies on precise ultraviolet transmittance measurement to ensure pathogen kill rates. Continuous absorbance monitoring also validates advanced oxidation processes that target emerging contaminants. Oil and gas installations are set to expand at a 7.20% CAGR as upstream operators measure hydrogen sulfide, benzene, and other hazardous vapors at the wellhead. The Ultraviolet analyzer market is experiencing incremental tailwinds in the chemicals and petrochemicals sectors, where ultraviolet probes confirm reaction endpoints and product purity.

Pharmaceutical plants amplify demand by embedding inline ultraviolet sensors in continuous manufacturing skids, which supports real-time release testing. Power generation facilities deploy ultraviolet mercury monitors to comply with Mercury and Air Toxics Standards, creating service revenue for suppliers. Manufacturing sectors such as food and beverage adopt handheld analyzers for rapid sanitation checks, expanding visibility beyond core water treatment users. Diversification across industries disperses economic risk and cushions suppliers from cyclical spending in any single vertical.

By Installation Type: Process Integration Balances Portability Trends

Online process instruments captured 42.20% of the revenue in 2024 because they feed data directly into distributed control systems, allowing operators to adjust chemical dosing, combustion parameters, or disinfection intensity without manual intervention. Integration projects often span multiple analyzer types, which delivers scale benefits and longer service agreements for vendors. Portable handheld units, although smaller in revenue today, are forecasted to have a 7.90% CAGR to 2030. Miniaturized spectrometers, such as Hamamatsu’s C16767MA, extend ultraviolet coverage down to 190 nm while fitting into battery-powered casings, thereby enhancing field diagnostics capabilities.

Laboratory benchtop systems remain essential for method development and regulatory reference checks. Ultraviolet sensors are now being embedded inside membrane bioreactors, cooling towers, and point-of-entry drinking water systems. This convergence of form factors forces suppliers to maintain broad portfolios. Successful brands package identical analytical cores across online, portable, and benchtop designs, which lowers inventory costs and simplifies user training. End users can then standardize calibration protocols and spare parts across facilities, reinforcing vendor lock-in and long-term support contracts.

Geography Analysis

Asia-Pacific generated 31.10% Ultraviolet analyzer market revenue in 2024 and is forecast to grow at 8.10% CAGR to 2030. China’s Five-Year Plan includes thousands of new wastewater plants that each specify closed-loop ultraviolet control for advanced oxidation and the removal of micro-pollutants. India’s Jal Jeevan Mission encourages the use of smart water grids that incorporate compact ultraviolet photometers at network nodes to verify residual chlorine surrogates. Southeast Asian governments are tightening palm oil effluent rules and requiring real-time organic carbon tracking, which adds to the instrument count. Japanese and South Korean semiconductor fabs utilize ultraviolet tools to verify the quality of ultrapure water, generating high-margin sales.

North America ranks second in value as the EPA raises monitoring frequencies for nitrogen oxides, mercury, and volatile organic compounds. Replacement cycles in municipal utilities average eight to ten years, which supports steady aftermarket revenue. Pharmaceutical investments in continuous production drive demand for validated ultraviolet platforms that comply with 21 CFR Part 11 regulations. Canadian resource projects and Mexican manufacturing corridors increase regional adoption, yet overall growth remains moderate due to a large installed base.

Europe maintains strong momentum, fueled by the Green Deal's objectives that reward low-carbon and circular economy technologies. Germany, France, and the United Kingdom are retrofitting aging treatment plants with intelligent optical systems to reduce energy consumption without compromising effluent quality. The Ultraviolet analyzer market size in Eastern Europe is increasing as EU cohesion funds finance municipal upgrades, while Mediterranean desalination plants are specifying corrosion-resistant ultraviolet sensors. The Middle East and Africa are registering an accelerating uptake in large-scale desalination, mining, and oil refining projects, although market penetration is hindered in lower-income economies where credit availability and skilled labor remain scarce.

Competitive Landscape

The ultraviolet analyzer market remains moderately fragmented. Established brands such as Hach, HORIBA, and Teledyne balance broad portfolios with deep service networks. ABB strengthened its position by acquiring Real Tech Inc. and introducing the UviTec line, which combines spectrophotometric and fluorescence capabilities. Mid-tier specialists focus on niche strengths, such as biofouling-resistant optical paths or deep UV coverage for semiconductor rinse verification. Start-ups backed by research institutes introduce dual-comb and quartz-enhanced photo-acoustic variants that promise higher selectivity.

Intense competition centers on digital features rather than core optics alone. Vendors embed AI chips at the sensor edge to enable outlier detection and to push maintenance alerts before failure. Open MQTT and OPC UA protocols are now standards, which simplify connections to industrial Internet of Things frameworks. Cybersecurity, once an afterthought, has become a key consideration in vendor selection criteria, following the exposure of vulnerabilities in ransomware events at water utilities. Suppliers differentiate through encrypted firmware, role-based access, and signed updates that meet IEC 62443 standards.

Ultraviolet Analyzer Industry Leaders

Hach Company

Teledyne FLIR LLC

HORIBA Ltd.

AMETEK Process Instruments Inc.

Swan Analytical Instruments AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Hach launched the NH6000sc ammonium analyzer, adding high sensitivity and auto-calibration to its online water portfolio.

- October 2024: ABB introduced the UviTec optical water analyzer family, merging Real Tech spectrophotometric and fluorescence techniques for five-second total organic carbon readings.

- July 2024: NIST upgraded its Ultraviolet Spectral Comparator Facility to extend germicidal coverage to 200-300 nm, strengthening U.S. calibration infrastructure.

- May 2024: DeNovix unveiled the DS-7 Spectrophotometer, a budget 1 µL instrument that targets teaching labs with full 190-840 nm coverage.

Global Ultraviolet Analyzer Market Report Scope

| UV Absorption Spectroscopy |

| UV Fluorescence |

| UV Photometry |

| Hybrid and Multi-wavelength Systems |

| Municipal Utilities |

| Chemicals and Petrochemicals |

| Power Generation |

| Oil and Gas |

| Manufacturing and Others |

| Online / Process Analyzers |

| Laboratory Benchtop |

| Portable / Hand-held |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa |

| By Technology | UV Absorption Spectroscopy | |

| UV Fluorescence | ||

| UV Photometry | ||

| Hybrid and Multi-wavelength Systems | ||

| By End-user Industry | Municipal Utilities | |

| Chemicals and Petrochemicals | ||

| Power Generation | ||

| Oil and Gas | ||

| Manufacturing and Others | ||

| By Installation Type | Online / Process Analyzers | |

| Laboratory Benchtop | ||

| Portable / Hand-held | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Ultraviolet analyzer market?

The market is valued at USD 1.48 billion in 2025 and is projected to reach USD 2.01 billion by 2030.

Which region contributes the most revenue?

Asia-Pacific generated 31.10% of global revenue in 2024 and is also the fastest-growing region.

Which end-user segment leads adoption?

Municipal utilities hold 31.20% share due to mandatory disinfection verification and organic contaminant tracking requirements.

Which technology segment is expanding the fastest?

Hybrid and multi-wavelength ultraviolet analyzers are forecast to post a 7.50% CAGR to 2030.

What are the primary barriers to wider deployment?

High capital expenditure and ongoing maintenance costs, along with a shortage of skilled spectroscopy personnel, remain the most significant restraints.

How are vendors differentiating their offerings?

Suppliers embed edge AI for predictive maintenance and provide encrypted connectivity that satisfies rising cybersecurity expectations.

Page last updated on: