Laser Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

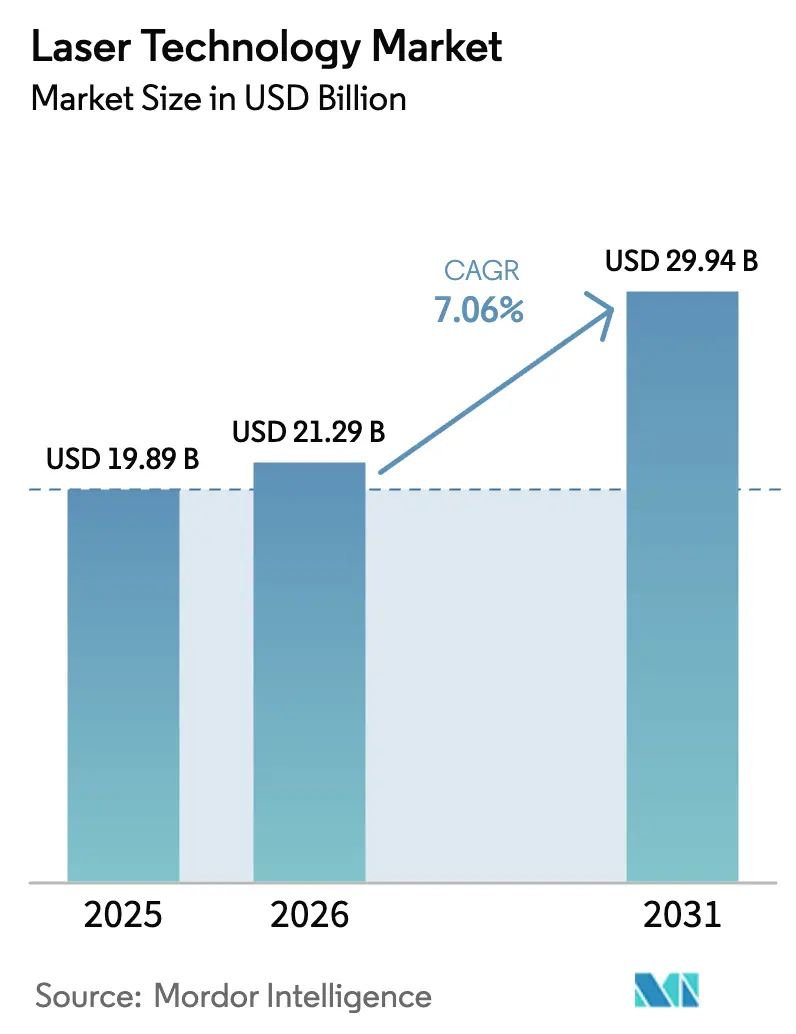

| Market Size (2026) | USD 21.29 Billion |

| Market Size (2031) | USD 29.94 Billion |

| Growth Rate (2026 - 2031) | 7.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laser Technology Market Analysis by Mordor Intelligence

The laser technology market size in 2026 is estimated at USD 21.29 billion, growing from 2025 value of USD 19.89 billion with 2031 projections showing USD 29.94 billion, growing at 7.06% CAGR over 2026-2031. Demand continues to widen from precision metal processing and advanced semiconductor packaging to directed-energy defense systems, aesthetic medicine, and autonomous-vehicle LiDAR. The shift from CO₂ platforms to fiber and semiconductor architectures underpins this expansion, because manufacturers value the combination of high wall-plug efficiency, compact form factors, and nanometer-scale accuracy. Adding impetus, decarbonization efforts in steelmaking, fast-evolving electric-vehicle battery designs, and government incentives for domestic photonics foundries keep capital spending on high-power lasers buoyant. In parallel, rising adoption of eye-safe solid-state LiDAR in China and the United States firmly links laser demand to the global electrification and autonomy story. Together, these dynamics reinforce the long-term growth profile of the laser technology market.

Key Report Takeaways

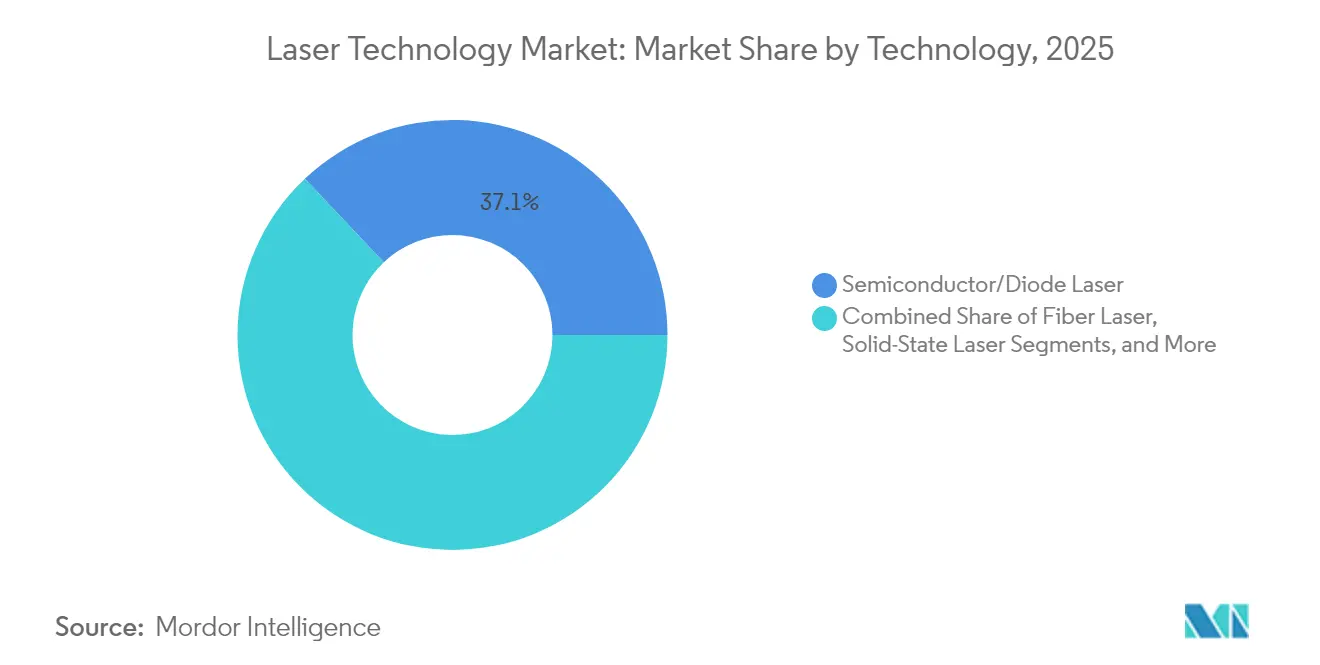

- By technology, semiconductor and diode lasers led with 37.05% revenue share in 2025, while fiber lasers are projected to advance at a 7.58% CAGR through 2031.

- By power output, medium-power systems (1-5 kW) held 40.15% of the laser technology market share in 2025; ultra-high-power platforms above 10 kW are set to grow fastest at 7.95% CAGR to 2031.

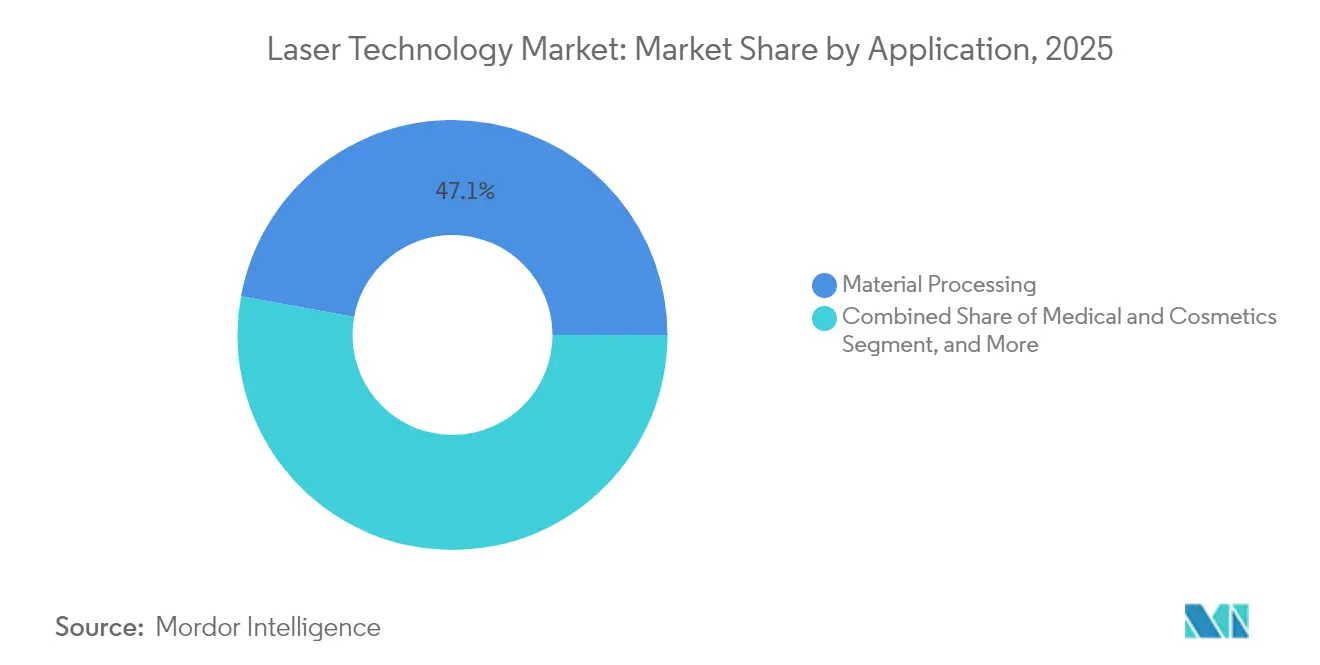

- By application, material processing represented 47.12% of the laser technology market size in 2025, whereas automotive LiDAR is forecast to expand at a 8.75% CAGR during 2026-2031.

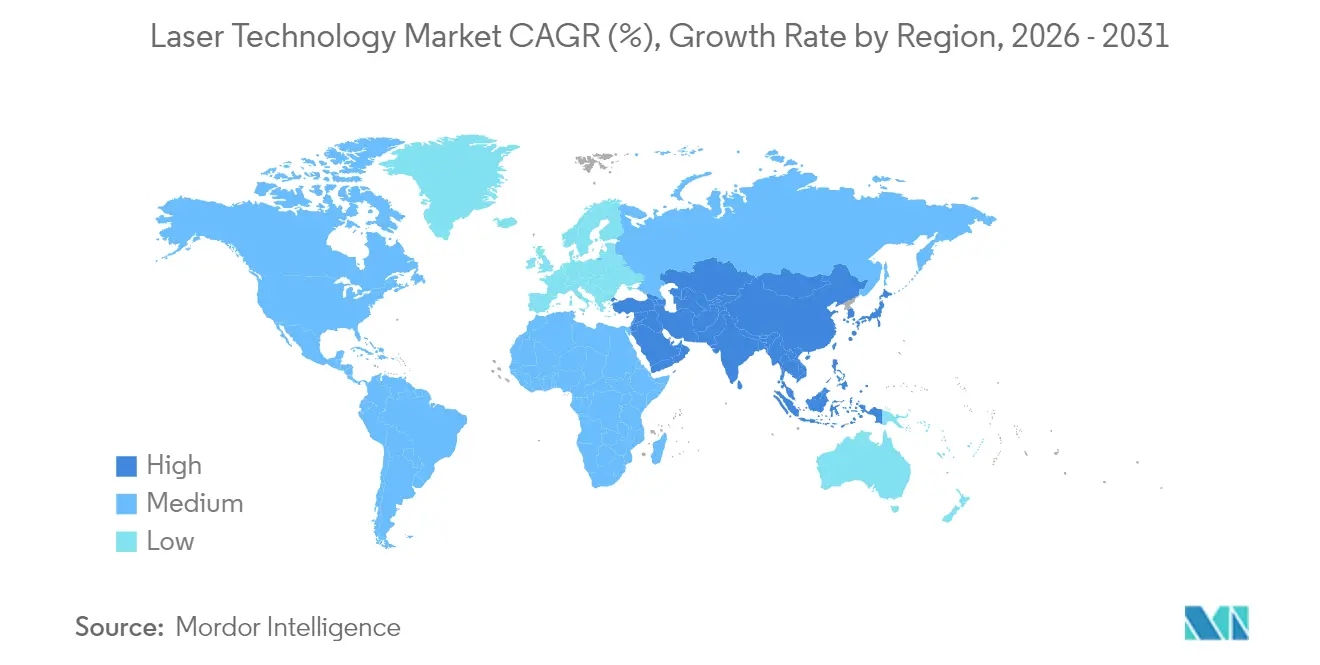

- By geography, Asia-Pacific commanded 42.05% of 2025 revenue, while the Middle East & Africa segment is expected to post the quickest 7.85% CAGR.

- By end-use industry, electronics retained leadership with a 26.65% share in 2025, and healthcare shows the highest projected growth, estimated at about 10.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laser Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiber lasers enabling high-precision micromachining in consumer-electronics plants | +1.2% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) |

| Rising demand for laser-based aesthetic procedures among millennials | +0.8% | North America & Europe | Short term (≤ 2 years) |

| High-power industrial lasers supporting green-steel and EV-battery manufacturing | +1.0% | Europe core, spillover to APAC | Long term (≥ 4 years) |

| Eye-safe LiDAR lasers for autonomous vehicles | +1.5% | China & USA core, global expansion | Medium term (2-4 years) |

| Incentives for domestic photonics foundries in South Korea | +0.6% | South Korea national, regional spillover | Long term (≥ 4 years) |

| Defense modernization programs fueling directed-energy laser procurement | +0.9% | Middle East core, NATO expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fiber lasers enabling high-precision micromachining in consumer-electronics plants

Fiber-laser beam quality of 1 M² and wall-plug efficiency near 40% sharply reduce power consumption and maintenance downtime compared with legacy CO₂ equipment. Asian smartphone and wearables makers now specify positional tolerances of 1-20 nm, which fiber lasers deliver without secondary finishing. TRUMPF’s partnership with SCHMID Group on glass-interposer drilling illustrates how the approach shortens production cycles for AI accelerator chips while lowering defect rates. China’s fiber-laser revenue is expected to touch USD 1.79 billion in 2024, rising 10.2% year on year, supported by provincial tax rebates that favor domestically built photonics subsystems. Expanded in-line sensors and AI-driven process control further reinforce adoption, making fiber technology the backbone of next-generation electronic-device factories across the region.

Rising demand for laser-based aesthetic procedures among millennials

The United States outpatient clinics report double-digit procedure growth as millennials choose non-invasive laser treatments for resurfacing, body contouring, and tattoo removal—a segment valued near USD 400-500 million in 2024 and scaling quickly toward multi-billion status. CO₂, Er:YAG, and picosecond platforms offer sub-50 µm ablation precision and minimal thermal damage, translating to shorter recovery windows favored by younger demographics. In Europe, harmonized reimbursement codes and less-restrictive advertising rules accelerate clinic rollouts of multi-application workstations. Parallel innovation in consumer-grade IPL and low-power laser devices broadens addressability beyond medical offices, although safety standards remain tightly regulated. Social-media visibility and rising disposable income across urban cohorts sustain this consumption runway, delivering incremental tailwinds to the laser technology market.

High-power industrial lasers supporting green-steel and EV-battery manufacturing

Europe’s push toward net-zero requires heavy industry to switch from gas-fired to hydrogen-based direct-reduction furnaces. Ultra-high-power fiber and diode lasers provide deep-penetration welding and rapid drying of cathode slurry coatings, thereby cutting energy use by up to 30%. Projects such as Blastr Green Steel’s 2.5 million-ton Finnish mill illustrate the commercial viability of integrating >10 kW laser welding lines into hot-strip halls. Likewise, TRUMPF’s TruHeat VCSEL solution speeds electrode drying by 300%, trimming battery cell costs for European gigafactories.[1]TRUMPF, “Battery Show Europe: TRUMPF TruHeat VCSEL Drying Solutions,” trumpf.com As automakers localize supply chains, demand for high-output lasers that guarantee micron-level seam consistency grows, further benefiting the laser technology market.

Eye-safe LiDAR lasers for autonomous vehicles

China filed more than 25,000 LiDAR patents since 2000, enabling cost downs that dropped unit prices below USD 500 in 2024. RoboSense alone shipped 256,000 eye-safe 905 nm units last year, supporting Level-3 autonomy launches by multiple domestic EV brands.[2]Liu Chang, “Chinese LiDAR Companies Take the Lead in Autonomous Driving Innovation,” Xinhua, english.news.cn US efforts center on silicon-photonics-based solid-state designs, as exemplified by Mobileye, which integrate lasers, photodetectors, and drive ASICs on a single wafer to enhance reliability. Transition from mechanical scanning to MEMS and flash architectures removes moving parts, pushing overall sensor MTBF beyond 25,000 hours. Regulators in both markets now finalize safety standards that cap maximum permissible exposure, unlocking volume adoption and contributing to sustained double-digit growth for the laser technology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gallium-nitride and rare-earth shortages inflating semiconductor-laser costs | -1.8% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Stringent EU laser safety directives raising SME compliance burden | -0.7% | Europe core, spillover to export markets | Medium term (2-4 years) |

| Power-grid instability limiting ultrafast-laser uptake in emerging Asia | -0.5% | Southeast Asia | Medium term (2-4 years) |

| Capital-intensive cooling infrastructure hindering >10 kW deployment in Africa | -0.3% | Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gallium-nitride and rare-earth shortages inflating semiconductor-laser costs

Chinese export restrictions raised gallium prices more than 150% and germanium 26% in 2024, putting immediate cost pressure on blue-diode production critical for EV-battery welding and free-space optical communications.[3]US Geological Survey, “China Ban on Gallium and Germanium Exports Could Cost USD 3.4 Billion in US GDP,” semiconductor-today.com USGS models suggest that a complete ban could erase USD 3.4 billion of US GDP. Stop-gap measures include LightPath Technologies’ BDNL4 glass as a germanium alternative and accelerated recycling initiatives, yet meaningful diversification into non-Chinese feedstock likely needs 3-5 years. Until then, pricing volatility squeezes margins for Western suppliers, slightly dampening growth within the laser technology market.

Stringent EU laser safety directives raising SME compliance burden

Revised EN 60825-1/A11 and EN 50689 standards demand explicit product marking, extended technical files, and mandatory CE labels, pushing administrative costs up by double-digit percentages for smaller firms. Economic Operators now share legal liability for misuse, forcing distributors to verify documentation throughout the supply chain.[4]UL Solutions, “Understand the New Laser Product Safety Standards for Europe,” ul.com Moreover, the Personal Protective Equipment Regulation (EU) 2016/425 obliges laser-goggle vendors to specify lifetime ratings and harmonized test reports. Cumulative digital- and green-transition compliance for European SMEs could reach EUR 53 billion, placing strain on R&D budgets and slowing product refresh cycles. Although safety gains are clear, the timing coincides with inflationary component prices, amplifying near-term hurdles for market entrants inside the laser technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Semiconductor dominance faces fiber-laser disruption

Semiconductor and diode platforms held a commanding 37.05% share of the laser technology market in 2025, anchored by telecom transceiver, optical-storage, and consumer-electronics demand. Their direct electrical pumping and nanosecond modulation capability enable high-bit-rate data links and barcode scanners. Fiber systems, however, are scaling fastest at a 7.58% CAGR through 2031, buoyed by superior beam quality (M² < 1.2) and up-to-40% electrical efficiency, which slash operational costs in industrial cutting lines. The laser technology market size for fiber architectures is expected to eclipse legacy CO₂ installations before 2028. Ultrafast femtosecond variants add momentum, because they ablate transparent materials without heat-affected zones, matching semiconductor roadmap needs for sub-10 nm vias. CO₂ lasers maintain niche relevance in signage and packaging, whereas excimer and quantum-cascade units fulfill lithography and chemical-sensing roles, respectively. Taken together, technology choice increasingly reflects application-specific trade-offs between capex, feature size, and electrical efficiency across the broader laser technology market.

The transition is also spurring hybrid architectures that co-package diode pumps with doped-fiber gain media inside temperature-regulated modules. Suppliers emphasize vertical integration to secure epitaxial wafer capacity and minimize gallium-based material disruptions. Collaborative R&D programs between European photonics hubs and Asian contract manufacturers shorten design cycles, allowing quarterly power-density upgrades. As a result, competitive advantage is shifting from pure wattage metrics toward integrated software suites that optimize pulse shape and in-situ process metrology, a trend likely to define the competitive landscape of the laser technology industry over the next decade.

By Power Output: Medium-power systems lead while ultra-high-power gains momentum

Systems rated 1-5 kW captured 40.15% of the laser technology market share in 2025, because they straddle versatility and total cost of ownership for sheet-metal, furniture, and automotive-tier suppliers. These mid-range platforms deliver 20 mm mild-steel cuts at 30 m/min while burning less than 12 kW wall power, translating to attractive ROI for job shops. Ultra-high-power rigs exceeding 10 kW, although niche, show the quickest 7.95% CAGR, driven by heavy-plate processing for shipbuilding and emerging hydrogen-ready steel mills. Fraunhofer’s HICLAD demonstrated additive-cladding deposition rates of 18 kg/h on a 12 kW diode source-evidence that throughput scales almost linearly with optical power.

Cooling needs escalate sharply beyond 8 kW, pushing integrators to adopt direct-diode or segmented-fiber designs with proprietary thermal-management loops. Installation complexity limits uptake in power-constrained regions, yet European utilities offer preferential tariffs for green-steel initiatives, partially offsetting opex. Below 1 kW, low-power units dominate surface-microstructuring and medical-device texturing. Vendors progressively bundle AI-driven beam-delivery heads that auto-compensate focus shift, enhancing uptime. Consequently, the laser technology market size distribution by output band is expected to widen, reflecting diverging end-user performance thresholds.

By Application: Material processing dominates while LiDAR accelerates

Material-processing tasks-from 6 mm aluminum chassis cutting to selective-laser melting of aerospace brackets-generated 47.12% of 2025 revenue, underscoring lasers’ entrenchment across manufacturing value chains. Pulse-on-demand controls now enable weld-seam widths under 50 µm, minimizing post-machining. Concurrently, automotive LiDAR revenue is expanding at a 8.75% CAGR, stoked by China’s subsidy-driven EV boom and the United States’ push for autonomous-vehicle safety validation. The laser technology market size dedicated to LiDAR is forecast to eclipse medical-aesthetics revenue before 2030.

Beyond the headline segments, photolithography remains cyclically robust, tied to advanced-node semiconductor output. Medical lasers address dermatology and ophthalmology, supported by demographics and reimbursement coverage. Additive-manufacturing platforms capitalize on 3D-printed turbine and orthopedic implants, embedding multi-laser arrays to enhance build volume. Environmental sensing, quantum-computing infrastructure, and fusion-energy prototypes round out emerging use cases, creating optionality for diversified suppliers inside the laser technology industry.

By End-Use Industry: Electronics leadership challenged by healthcare growth

Electronics and semiconductor fabs accounted for 26.65% of the laser technology market in 2025, reflecting ongoing transition to heterogeneous integration and chiplet packaging that rely on deep-ultraviolet excimer and femtosecond-UV drilling heads. Yet healthcare is forecast to register the fastest double-digit CAGR through 2031, powered by laser cataract surgery, aesthetic dermatology, and minimally invasive oncology procedures. Hospitals increasingly prefer femtosecond platforms for flap-free LASIK and mid-IR ablation tools for tumor debulking, lifting capital-equipment budgets.

Automotive OEMs allocate capital toward LiDAR sensor integration and next-generation battery pack assembly, while aerospace primes invest in laser-welded titanium and nickel superalloy components to lighten airframes. Energy-sector demand—from battery recycling to solar-cell doping—adds resilience. Cross-industry synergies, evident in photonics foundries servicing medical and telecom clients alike, diversify revenue streams and hedge against single-sector slowdowns, reinforcing the long-term outlook for the laser technology market.

Geography Analysis

Asia-Pacific retained a 42.05% share of the laser technology market in 2025, propelled by China’s vertically integrated photonics ecosystem and state-subsidized LiDAR rollouts. Beijing’s five-year plan earmarks multi-billion renminbi packages for on-shore gallium-nitride epi capacity, while South Korea’s KRW 471 trillion semiconductor mega-cluster anchors regional optics demand. Japanese toolmakers concentrate on ultrafast-pulse innovations for advanced packaging, and India’s PLI incentives lure backend-assembly suppliers. Coupled with ASEAN cost advantages, the region covers the entire value chain, from laser-diode chips to five-axis cutting tables, sustaining its dominance in the laser technology market. North America, a mature yet innovation-centric arena, focuses on directed-energy defense prototypes, advanced medical systems, and high-throughput additive manufacturing. Pentagon contracts exceed USD 400 million annually for DEW demonstrators, while elective aesthetic clinics dot urban centers, absorbing dermatology workstations. Canada’s photonics corridor in Ontario partners with universities on mid-IR gas-sensing chips, and Mexico’s maquiladora plants retrofit fiber cutters for automotive housings. Fierce price competition from Asian imports compresses margins in commodity cutters but encourages US firms to climb the value curve through vertical integration and software-defined motion control, keeping the laser technology market resilient. Europe combines regulatory strictness with green-manufacturing ambition. Stringent CE norms raise entry hurdles but ensure harmonized safety benchmarks. Simultaneously, carbon-border-adjustment mechanisms accelerate deployment of laser-enabled hydrogen steelmaking, positioning the bloc at the forefront of clean-industry applications. German, Italian, and Finnish integrators spearhead >10 kW shipyard lasers, while French and UK labs trial fusion-energy pump sources. The Middle East & Africa segment, although starting from a smaller base, exhibits the quickest 7.85% CAGR on the back of defense modernization-Israel’s USD 500 million Iron Beam expansion is emblematic-and infrastructure megaprojects that need precision-cut steel. Limited grid stability in parts of Africa tempers ultra-high-power uptake, yet collaborative financing with Gulf investors signals future capacity. South America remains nascent, showing patchy adoption tied to mining equipment refurbishment and renewable-energy installations, but technology transfer programs with European OEMs lay groundwork for medium-term demand growth, collectively contributing to the global laser technology market expansion.

Competitive Landscape

The laser technology market displays moderate fragmentation: the top five vendors account for an estimated 55-60% of combined revenue, suggesting room for both global majors and agile regional specialists. TRUMPF, Coherent, and IPG Photonics safeguard their leadership via 5-10% annual R&D ratios, forward-integrated service programs, and in-house epi-wafer lines. Coherent’s new 6-inch indium-phosphide fab in Texas and Sweden halves internal die cost and insulates supply chains against gallium disruptions.

Chinese challengers such as Acme and MAX Photonics leverage scale economics and state credit lines to undercut Western pricing by up to 35%, swiftly gaining share in fiber-cutter kits and automotive LiDAR. Their local sourcing mitigates tariff exposure, though patent-infringement litigation remains an overhang in US and European courts. Strategic trajectories show a pivot toward platform ecosystems: vendors bundle motion-control software, AI-powered process monitors, and cloud-based predictive maintenance, locking in recurring service revenue.

M&A activity underscores portfolio consolidation. Alcon moved to acquire LENSAR for USD 356 million, reinforcing its ophthalmic-laser footprint. Teledyne’s USD 710 million purchase of select Excelitas electronics businesses adds the Qioptiq optical-systems brand, extending defense penetration. Thorlabs snapped up Praevium Research to deepen VCSEL know-how for OCT diagnostics. These bolt-ons reveal how acquirers seek application-specific IP rather than pure wattage gains, anticipating cross-selling opportunities into vertical markets and solidifying positions within the laser technology industry.

Laser Technology Industry Leaders

Trumpf SE + Co. KG

Coherent Corp.

Han's Laser Technology Industry Group Co., Ltd.

IPG Photonics

Jenoptik AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: University of Tokyo researchers achieved laser-machining speeds one-million-fold faster than conventional methods, promising transformative semiconductor through-glass-via drilling.

- May 2025: QinetiQ secured a GBP 160 million UK MoD extension to accelerate DragonFire high-energy laser systems.

- May 2025: Coherent Corp. posted USD 1.50 billion Q3 FY 2025 revenue, up 24% YoY, buoyed by AI datacenter optics

- March 2025: Alcon agreed to acquire LENSAR for USD 356 million, adding the ALLY robotic cataract laser platform

- March 2025: University of Adelaide launched an AUD 8.2 million project to commercialize ultra-short-pulse lasers for fusion-energy research.

Global Laser Technology Market Report Scope

Laser technology excites atoms or molecules to emit light at specific wavelengths, amplifying it to produce a focused radiation beam. This emission is usually confined to a narrow spectrum, spanning visible, ultraviolet, or infrared wavelengths.

The study offers an in-depth analysis of laser technology trends and dynamics, covering aspects like technological evolution and demand fluctuations. It monitors the revenue generated from the sales of laser systems based on different technologies by leading global market players as a foundation for market estimations. In addition, macroeconomic factors have been taken into account to fine-tune these figures in light of evolving market dynamics.

The laser technology market is segmented by technology (CO2 laser, fiber laser, solid-state laser (SSL), semiconductor laser, excimer laser, and others), application (material processing, medical and cosmetics, photolithography, communication, sensing and instrumentation, consumer electronics, military and defense, and other applications), and geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| CO2 Laser |

| Fiber Laser |

| Solid-State Laser |

| Semiconductor/Diode Laser |

| Excimer Laser |

| Ultrafast (Femtosecond/Picosecond) Laser |

| Quantum Cascade Laser |

| Hybrid and Other Technologies |

| Low-Power (Less than 1 kW) |

| Medium-Power (1-5 kW) |

| High-Power (5-10 kW) |

| Ultra-High-Power (Above 10 kW) |

| Material Processing | Cutting |

| Welding and Cladding | |

| Marking and Engraving | |

| Additive Manufacturing | |

| Medical and Cosmetics | Surgical Lasers |

| Dermatology and Aesthetics | |

| Ophthalmology | |

| Photolithography and Semiconductor Manufacturing | |

| Optical Communication | |

| Sensing and Instrumentation | |

| Consumer Electronics | |

| Military and Defense | |

| Automotive LiDAR | |

| Research and Academia |

| Automotive |

| Aerospace and Defense |

| Healthcare |

| Electronics and Semiconductor |

| Industrial Machinery |

| Energy (Battery and Solar) |

| Telecom and IT |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Technology | CO2 Laser | ||

| Fiber Laser | |||

| Solid-State Laser | |||

| Semiconductor/Diode Laser | |||

| Excimer Laser | |||

| Ultrafast (Femtosecond/Picosecond) Laser | |||

| Quantum Cascade Laser | |||

| Hybrid and Other Technologies | |||

| By Power Output | Low-Power (Less than 1 kW) | ||

| Medium-Power (1-5 kW) | |||

| High-Power (5-10 kW) | |||

| Ultra-High-Power (Above 10 kW) | |||

| By Application | Material Processing | Cutting | |

| Welding and Cladding | |||

| Marking and Engraving | |||

| Additive Manufacturing | |||

| Medical and Cosmetics | Surgical Lasers | ||

| Dermatology and Aesthetics | |||

| Ophthalmology | |||

| Photolithography and Semiconductor Manufacturing | |||

| Optical Communication | |||

| Sensing and Instrumentation | |||

| Consumer Electronics | |||

| Military and Defense | |||

| Automotive LiDAR | |||

| Research and Academia | |||

| By End-Use Industry | Automotive | ||

| Aerospace and Defense | |||

| Healthcare | |||

| Electronics and Semiconductor | |||

| Industrial Machinery | |||

| Energy (Battery and Solar) | |||

| Telecom and IT | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the laser technology market?

The laser technology market is valued at USD 21.29 billion in 2026 and is projected to reach USD 29.94 billion by 2031.

Which technology segment is expanding the fastest?

Fiber lasers are expanding most rapidly at a 7.58% CAGR through 2031, driven by superior beam quality and energy efficiency.

Which power-output category dominates industry revenue?

Medium-power systems rated 1-5 kW held 40.15% of 2025 revenue because they balance throughput with manageable capex and opex.

Why is Asia-Pacific so important to laser suppliers?

Asia-Pacific accounts for 42.05% of global revenue thanks to China’s large LiDAR and consumer-electronics base, South Korea’s semiconductor investments, and a fully integrated photonics supply chain.

What major risk could slow near-term growth?

Restricted exports of gallium-nitride and rare-earth materials have already lifted diode-laser costs and could trim the global CAGR by about 1.8% if shortages persist.

How fragmented is competition in the industry?

The top five vendors command roughly 55-60% of revenue, yielding a moderate concentration level that still leaves room for regional specialists and niche innovators.

Page last updated on: