Laser-based Gas Analyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

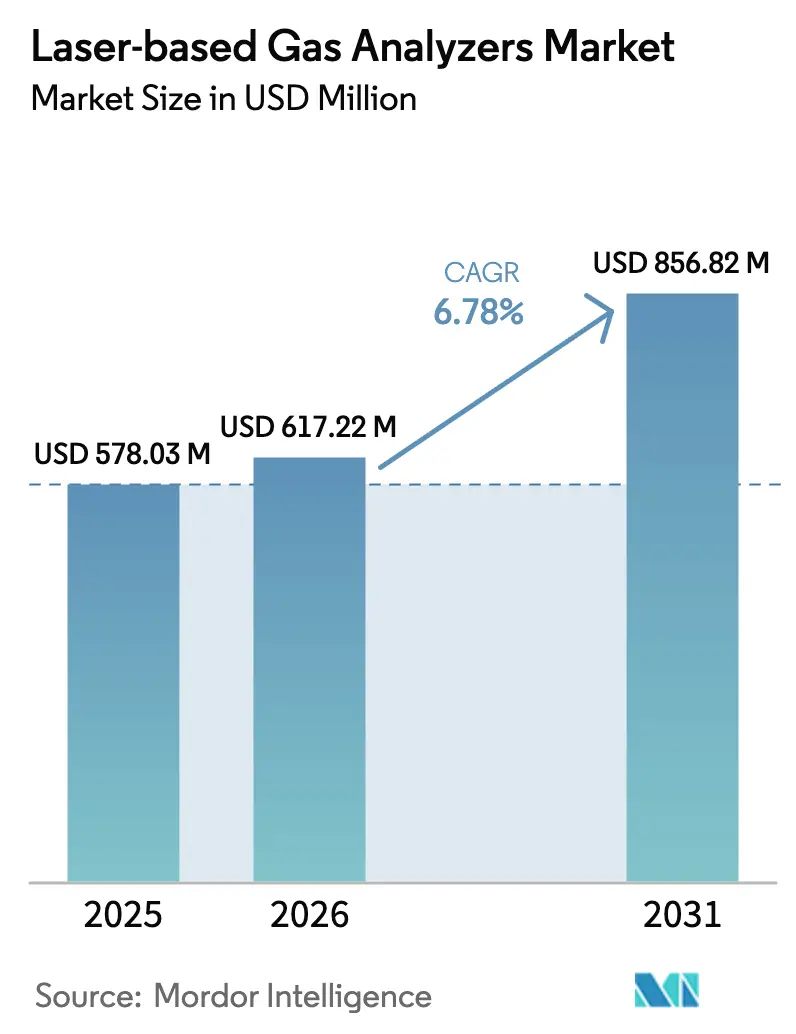

| Market Size (2026) | USD 617.22 Million |

| Market Size (2031) | USD 856.82 Million |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

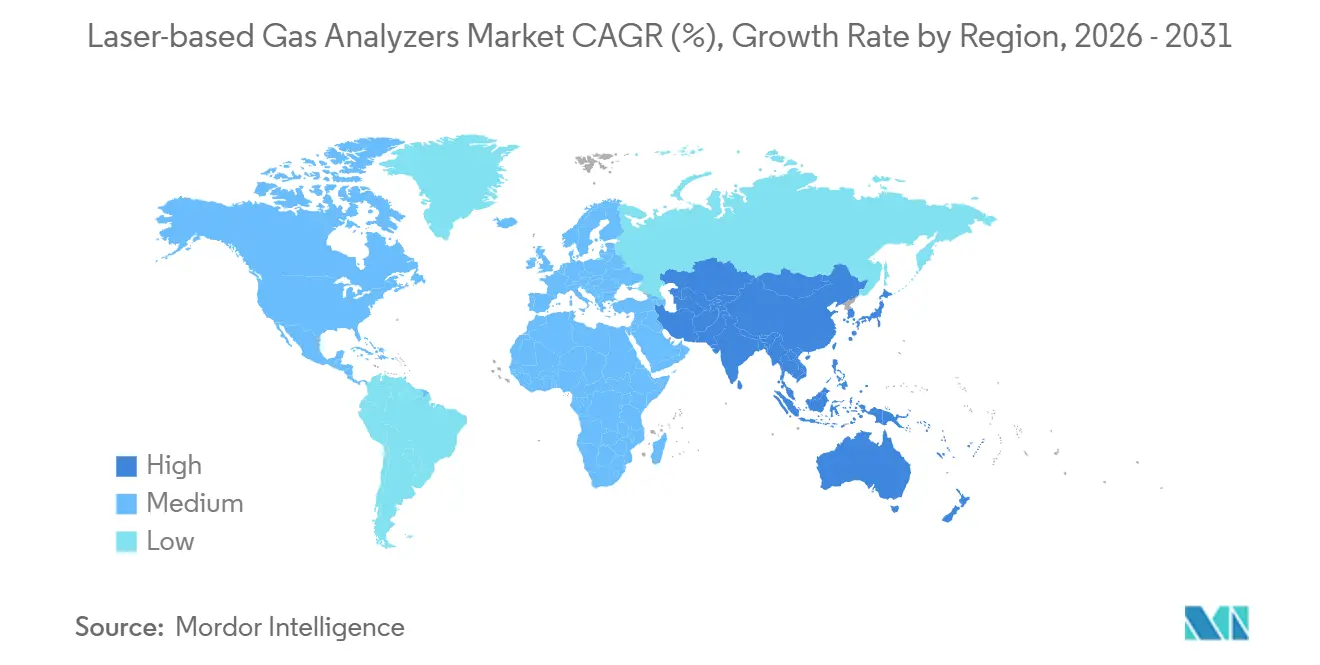

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

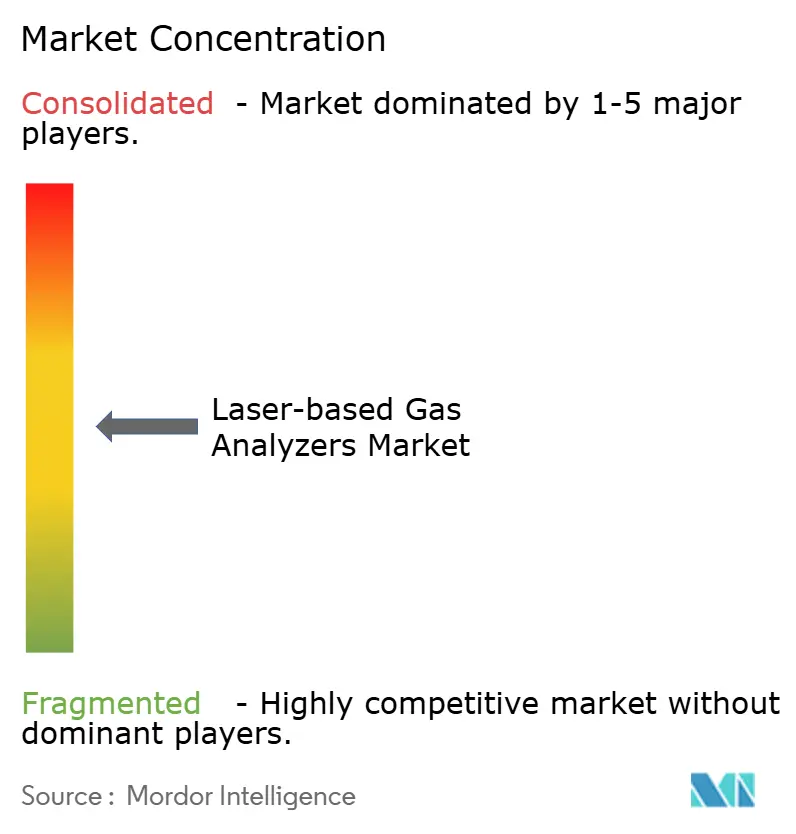

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laser-based Gas Analyzers Market Analysis by Mordor Intelligence

The Laser-based Gas Analyzers Market size is expected to increase from USD 578.03 million in 2025 to USD 617.22 million in 2026 and reach USD 856.82 million by 2031, growing at a CAGR of 6.78% over 2026-2031.

Stringent multi-pollutant rules in emerging economies, rising coal-to-hydrogen co-firing activity, and the build-out of small modular reactors support steady capital spending on continuous off-gas monitoring. Vendors that integrate cloud analytics with hardware are lowering operating costs for plants that lack on-site spectroscopy skills, while supply-chain workarounds for gallium arsenide wafers are easing recent lead-time pressures. Procurement also benefits from mid-infrared quantum cascade laser modules that resolve trace ammonia and volatile organic compounds in petrochemical streams. Growth opportunities remain strongest where subsidies, such as China’s air-quality budget and the United States Department of Energy capture hubs program, offset the capital-cost premium of laser platforms.

Key Report Takeaways

- By process, in-situ configurations led with 58.73% revenue share in 2025 of the laser-based gas analyzers market, whereas extractive systems are advancing at a 7.66% CAGR through 2031.

- By technology, tuneable diode laser spectroscopy retained 41.63% revenue share in 2025 of the laser-based gas analyzers market, while quantum cascade laser systems are expanding at a 7.33% CAGR to 2031.

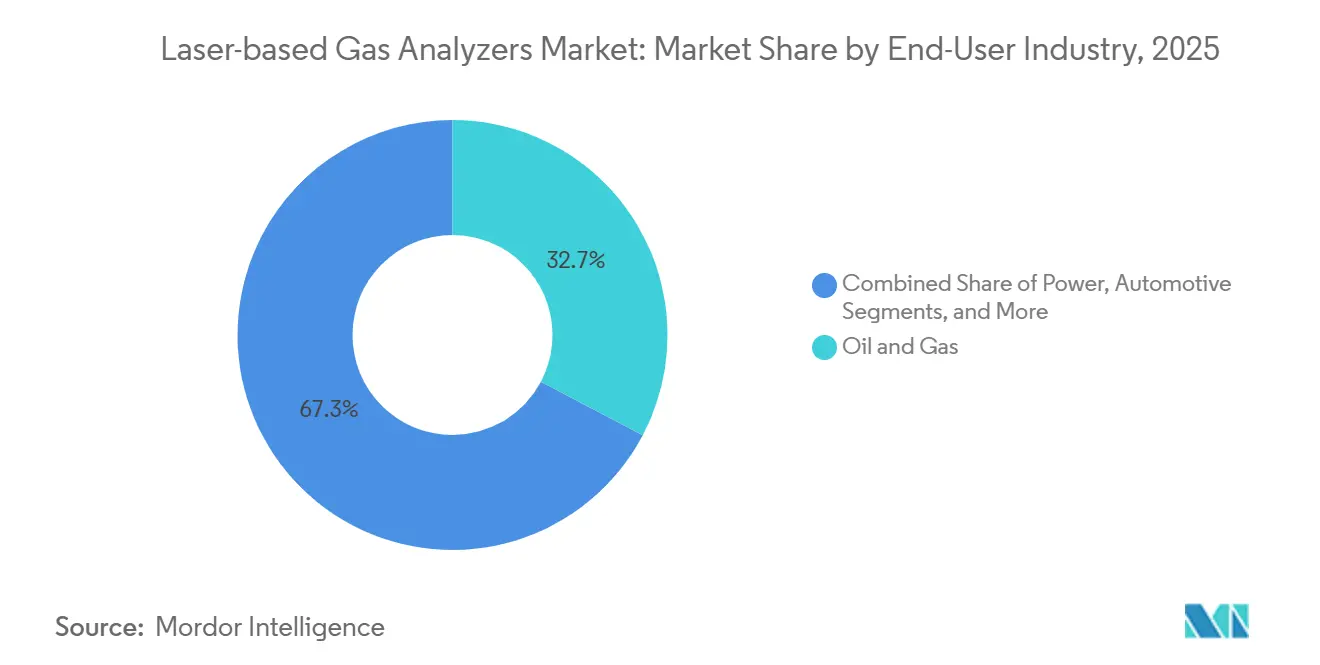

- By end-user industry, oil and gas contributed 32.73% revenue share in 2025 of the laser-based gas analyzers market; healthcare and pharmaceuticals record the fastest 6.99% CAGR to 2031.

- By application, emissions monitoring accounted for 41.74% of the laser-based gas analyzers market size in 2025 and laboratory and research analysis is growing at a 7.44% CAGR through 2031.

- By geography, North America held 38.73% of geographic revenue in 2025 of the laser-based gas analyzers market; Asia-Pacific is forecast to post the highest 7.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laser-based Gas Analyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-pollutant emissions regulations post-2025 in emerging economies | +1.2% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Accelerated coal-to-hydrogen co-firing retrofits requiring real-time combustion analytics | +0.9% | Europe and Asia-Pacific, selective North America sites | Medium term (2-4 years) |

| Rapid expansion of small modular reactor projects needing continuous off-gas monitoring | +0.7% | North America and Europe, early Asia-Pacific deployments | Long term (≥4 years) |

| Rising adoption of CCUS with laser inline CO₂ purity checks | +1.1% | Global, concentrated in North America and Middle East | Medium term (2-4 years) |

| Petrochemical shift to green ammonia driving in-situ NH₃ leak detection systems | +0.8% | Middle East, Asia-Pacific, selective Europe hubs | Medium term (2-4 years) |

| Growth of hospital negative-pressure isolation rooms mandating trace anesthetic gas analysis | +0.5% | Global, accelerated in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Pollutant Emissions Regulations Post-2025 in Emerging Economies

Vietnam, Kenya, and India enacted rules between 2024 and 2025 that oblige thermal power plants and cement kilns to install continuous analyzers for nitrogen oxides, sulfur dioxide, and particulate matter. Vietnam’s Circular 45/2024 demands real-time monitoring for units above 30 MWth, capturing nearly 180 coal-fired boilers. Kenya’s 2024 air-quality update reduced the nitrogen-oxide cap to 150 mg/m³ and tightened quarterly reporting, while India extended its 2015 norms to about 400 captive generators. Near-infrared tuneable diode laser and mid-infrared quantum cascade laser systems outperform electrochemical cells in these dusty high-moisture stacks, reinforcing demand across the laser-based gas analyzers market.

Accelerated Coal-to-Hydrogen Co-Firing Retrofits Requiring Real-Time Combustion Analytics

European and Asian utilities are blending up to 20% hydrogen or ammonia with coal, altering flame chemistry and increasing unburned-fuel slip. Mitsubishi Heavy Industries measured 15 ppm ammonia slip at a 20% co-fire setting and recommended sub-5 ppm detection thresholds, achievable with modern tuneable diode laser analyzers.[1]Mitsubishi Heavy Industries, “Ammonia Co-firing Technology for Coal-Fired Power Plants: Combustion Characteristics and Emissions Control,” mhi.com The EU Innovation Fund awarded EUR 150 million (USD 169.5 million) to demonstration plants in late 2024, each specifying continuous laser-based combustion analytics.[2]European Commission, “Innovation Fund: Large-Scale Projects Call Results,” climate.europa.eu Japan targets 1 GW ammonia co-firing by 2030, with early projects at JERA facilities adopting quantum cascade laser platforms for simultaneous ammonia and nitrous-oxide monitoring. These actions amplify opportunity across the laser-based gas analyzers market.

Rapid Expansion of Small Modular Reactor Projects Needing Continuous Off-Gas Monitoring

The United States Nuclear Regulatory Commission approved NuScale’s 77 MWe module in 2023, with Idaho construction permits expected by 2026. Off-gas systems must detect krypton-85, xenon-133, and iodine-131 at sub-ppb levels. Pacific Northwest National Laboratory reported that cavity ring-down spectroscopy attains detection limits 10 times lower than beta-gamma counters while eliminating sample conditioning. IAEA Technical Document 1991, published in 2025, endorses continuous laser-based noble-gas tracking in Generation IV designs.[3]International Atomic Energy Agency, “Continuous Off-Gas Monitoring for Generation IV Reactors,” iaea.org Growing reactor fleets thus expand the laser-based gas analyzers market.

Rising Adoption of CCUS with Laser Inline CO₂ Purity Checks

CO₂ streams require ≥95% purity before pipeline injection to curb corrosion. The United States Department of Energy directs regional capture hubs to verify purity in real time, favoring laser platforms that bypass dilution and desiccant steps. Norway’s Northern Lights project rejected two cargoes in early 2025 due to nitrogen contamination detected by laser analyzers. Draft ISO 27919-3, expected in 2026, names tuneable diode laser spectroscopy for sulfur dioxide and hydrogen sulfide trace measurement. Implementation momentum boosts the laser-based gas analyzers market worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital cost premium versus electrochemical sensors in cost-sensitive mid-tier plants | -0.8% | Asia-Pacific, South America, Africa | Short term (≤2 years) |

| Skill shortage to interpret high-resolution spectral data in developing regions | -0.6% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Laser source supply-chain constraints due to GaAs wafer shortages | -0.5% | Global, acute in North America and Europe | Short term (≤2 years) |

| Standardization gaps across global regulatory methods hindering procurement decisions | -0.4% | Global, pronounced in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital Cost Premium Versus Electrochemical Sensors in Cost-Sensitive Mid-Tier Plants

Laser analyzers cost 2-3 times more than electrochemical arrays. An Asian Development Bank study estimated 18-24 months payback in Southeast Asian plants, exceeding the 12-month hurdle many managers apply. Where enforcement remains uneven, operators delay upgrades, especially when single-gas non-dispersive infrared devices suffice. The premium tempers short-term uptake in parts of Asia-Pacific, South America, and Africa, restraining the laser-based gas analyzers market.

Skill Shortage to Interpret High-Resolution Spectral Data in Developing Regions

Only 15% of technicians in India, Indonesia, and Nigeria possess laser spectroscopy training versus 40% in Germany, according to a 2025 ISA survey. The gap creates commissioning delays and mis-alarms. Cloud analytics mitigate the problem, yet bandwidth limits and data-sovereignty rules hinder adoption in remote or regulated plants. The talent deficit therefore reduces near-term growth potential in several high-priority regions of the laser-based gas analyzers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process: Extractive Systems Widen Adoption in Harsh Environments

Extractive systems are gaining ground even though in-situ units delivered 58.73% of 2025 revenue in the laser-based gas analyzers market. Power plants that retrofit pre-2000 continuous emissions monitoring hardware favor extractive probes that sit outside the flue, shielded from acid rain precursors and dust. Extractive modules deliver 7.66% CAGR through 2031 as coal, waste-to-energy, and biomass boilers exceed optical path fouling limits that hamper cross-stack tuneable diode laser probes. The United States Environmental Protection Agency Performance Specification 18 update in 2024 legitimized extractive tuneable diode laser reporting provided transfer lines stay above the acid dew point. Calibration is straightforward because certified gas blends can be injected directly, a convenience embraced by ISO 14001-certified facilities.

Hybrid architectures are emerging in refineries that use an in-situ probe for combustion trim and an extractive loop for trace hydrogen sulfide. The European Industrial Emissions Directive mandates continuous reporting of 12 pollutants at integrated refinery sites, an obligation most cost-effectively met with multi-point extractive networks feeding central spectrometers. As maintenance teams gain experience, extractive installations in cement kilns and glass furnaces are also climbing. Altogether, growing retrofit activity enlarges the share of extractive solutions within the laser-based gas analyzers market.

By Technology: Mid-Infrared QCLS Accelerates Trace-Gas Detection

Tuneable diode laser spectroscopy delivered 41.63% of technology revenue in 2025, supported by mature supply chains for 1.3 µm to 1.6 µm distributed-feedback lasers that measure water vapor, methane, and hydrogen chloride. Quantum cascade laser spectroscopy, however, records the highest 7.33% CAGR, driven by its 2 µm–12 µm wavelength coverage, which probes the fundamental vibrational modes of ammonia, nitrous oxide, and volatile organic compounds. When Thorlabs introduced a room-temperature module below USD 15,000 in 2025, entry barriers for mid-sized petrochemical plants fell sharply.

Cavity ring-down spectroscopy is gaining traction in isotopic CO₂ verification for carbon accounting, as cited in the NIST Standard Reference Material 2820, released in 2025. Raman analyzers remain mainly in laboratories due to fluorescence interference from aromatics, although new chemometric libraries are improving field viability. The International Electrotechnical Commission is drafting IEC 61508 functional-safety guidance specific to quantum cascade analyzers in hazardous areas, with publication expected in late 2026. Together, these advances diversify technology preferences inside the laser-based gas analyzers market.

By End-User Industry: Healthcare Gains Momentum

Oil and gas contributed 32.73% of 2025 revenue, anchored by methane leak rules under the United States EPA Subpart W and Canadian federal mandates. Healthcare and pharmaceuticals now post a 6.99% CAGR through 2031, reflecting hospital expansions of negative-pressure isolation rooms that require continuous anesthetic-gas monitoring under ASHRAE 170-2021. Real-time volatile-organic-compound tracking also helps pharmaceutical manufacturers comply with ICH Q3C residual-solvent limits.

In power generation, high-dust coal units favor laser analyzers because electrochemical cells drift under particulate loading. Automotive paint booths rely on perimeter laser monitoring to ensure 95% destruction of volatile organic compounds, as mandated by the European Solvent Emissions Directive. Pulp and paper mills outfit recovery boilers with tunable diode laser units to maintain total reduced sulfur levels below odor thresholds. Food processors installing renewable natural gas equipment verify that methane purity is above 97% and hydrogen sulfide is below 4 ppm. Such diverse use cases broaden the laser-based gas analyzers market across end-user verticals.

By Application: Laboratory Analysis Records Fastest Uptick

Emissions monitoring retained 41.74% revenue share in 2025, rooted in mandatory continuous emissions monitoring systems at approximately 1,200 North American power plants alone. Laboratory and research analysis, however, exhibits a 7.44% CAGR to 2031, boosted by academic adoption of cavity ring-down spectroscopy for carbon isotopics and breath analysis. NIST’s 2025 isotopic standards closed a traceability gap and sparked instrument purchases for voluntary carbon market verification.

Process optimization gains ground in petrochemical crackers where real-time ethylene and propylene readings enhance olefin yields. Safety and leak detection rollouts at liquefied natural gas terminals rely on sub-ppm hydrogen and methane thresholds to preempt explosive conditions. Environmental compliance testers value portable tuneable diode laser instruments weighing under 10 kg that simplify multi-site sampling. Cumulatively, expanding laboratory, safety, and optimization tasks enrich the laser-based gas analyzers market application mix.

Geography Analysis

North America generated 38.73% of laser-based gas analyzers market revenue in 2025. United States power plants covered by the Acid Rain Program and the Regional Greenhouse Gas Initiative must submit continuous emissions data, and the 2024 Performance Specification 18 revision further entrenched laser absorption methods. Canadian upstream operators comply with quarterly methane leak surveys, while new carbon capture hubs require inline CO₂ purity checks, driving additional analyzer orders.

Asia-Pacific posts the fastest 7.55% CAGR through 2031. China’s Ministry of Ecology and Environment directed CNY 1.2 trillion (USD 169 billion) toward air-quality upgrades during the 14th Five-Year Plan, subsidizing laser deployments in steel and non-ferrous smelters. India’s National Clean Air Programme, updated in 2025, compels 1,500 industrial sources to install continuous monitoring by 2027. Southeast Asian power stations adopt laser systems as Vietnam and Indonesia enforce new stack limits. Mid-sized chemical plants remain cost sensitive, yet rising enforcement and falling module prices are closing the gap.

Europe’s share stabilizes as Western sites near saturation, yet Eastern member states, including Poland and Romania, accelerate installations to meet Industrial Emissions Directive best-available-technique notes. The Middle East builds new petrochemical complexes committed to Zero Routine Flaring goals, prompting orders for hydrogen sulfide and moisture analyzers. South American growth centers on Brazilian ethanol distilleries and Argentine shale projects, while South Africa’s draft 2024 rules could spark demand at 12 Eskom coal units. Collectively, regulatory divergence and investment cycles shape geographic prospects for the laser-based gas analyzers market.

Competitive Landscape

Top Companies in Laser-based Gas Analyzers Market

Five global automation conglomerates, ABB, Emerson, Siemens, Yokogawa, and Endress+Hauser, controlled about half of 2025 revenue by bundling service contracts with tuneable diode laser, quantum cascade laser, and Raman offerings. High installed-base switching costs safeguard their positions. Mid-tier chemical plants in Southeast Asia and Latin America represent white-space where price sensitivity and skill shortages have slowed conversions, but cloud-enabled analyzers promise to simplify adoption.

Specialists such as Tiger Optics, SpectraSensors, and Gasera focus on sub-ppb detection of moisture and ammonia in semiconductor fabs and pharmaceutical cleanrooms. Chinese firms Focused Photonics and Hangzhou Zetian gained domestic ground through localized production priced 20-30% below Western equipment, though European and United States certification hurdles limit exports. Patent activity concentrates on wavelength-modulation noise suppression. Siemens filed EP4012400 in 2024 for a second-harmonic normalization algorithm that cuts drift by 40%.

Technology strategies diverge, as incumbents push tunable diode lasers due to mature supply chains, while venture-backed firms emphasize quantum cascade lasers and cavity ring-down spectroscopy for green ammonia and isotopic CO₂ niches. The International Electrotechnical Commission is drafting IEC 61508 laser-specific safety rules that will advantage companies with certified design processes. Overall, moderate concentration prevails in the laser-based gas analyzers market.

Laser-based Gas Analyzers Industry Leaders

ABB Ltd

Opsis AB

Emerson Electric Co.

HORIBA Ltd

Servomex Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Emerson allocated USD 45 million to expand its Solingen facility, tripling quantum cascade laser module capacity and adding indium phosphide wafer processing.

- November 2025: Yokogawa won a USD 38 million, 5-year deal with Saudi Aramco to supply tuneable diode laser analyzers for 12 liquefied natural gas trains at Jafurah, with commissioning in 2027.

- October 2025: ABB partnered with NuScale Power to embed cavity ring-down spectroscopy into small modular reactor off-gas systems for the Carbon Free Power Project.

- September 2025: Siemens launched the Sitrans SL300 tuneable diode laser analyzer with a modular optical bench covering 1.3 µm–10 µm and Zone 1 hazardous-area certification.

Global Laser-based Gas Analyzers Market Report Scope

The Laser-based Gas Analyzers Market Report is Segmented by Process (In Situ, Extractive), Technology (TDLS, Raman Spectroscopy, CRDS, QCLS), End-user Industry (Power, Oil and Gas, Mining and Metals, Chemical and Petrochemical, Automotive, Pulp and Paper, Healthcare and Pharmaceuticals, Other End-user Industries), Application (Emissions Monitoring, Process Optimization and Control, Safety and Leak Detection, Environmental Compliance Testing, Laboratory and Research Analysis), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| In Situ |

| Extractive |

| Tuneable Diode Laser Spectroscopy (TDLS) |

| Raman Spectroscopy (RA) |

| Cavity Ring-Down Spectroscopy (CRDS) |

| Quantum Cascade Laser Spectroscopy (QCLS) |

| Power |

| Oil and Gas |

| Mining and Metals |

| Chemical and Petrochemical |

| Automotive |

| Pulp and Paper |

| Healthcare and Pharmaceuticals |

| Other End-user Industries |

| Emissions Monitoring |

| Process Optimization and Control |

| Safety and Leak Detection |

| Environmental Compliance Testing |

| Laboratory and Research Analysis |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Process | In Situ | ||

| Extractive | |||

| By Technology | Tuneable Diode Laser Spectroscopy (TDLS) | ||

| Raman Spectroscopy (RA) | |||

| Cavity Ring-Down Spectroscopy (CRDS) | |||

| Quantum Cascade Laser Spectroscopy (QCLS) | |||

| By End-user Industry | Power | ||

| Oil and Gas | |||

| Mining and Metals | |||

| Chemical and Petrochemical | |||

| Automotive | |||

| Pulp and Paper | |||

| Healthcare and Pharmaceuticals | |||

| Other End-user Industries | |||

| By Application | Emissions Monitoring | ||

| Process Optimization and Control | |||

| Safety and Leak Detection | |||

| Environmental Compliance Testing | |||

| Laboratory and Research Analysis | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the Laser-based Gas Analyzers Market?

The laser-based gas analyzers market size reached USD 617.22 million in 2026 and is projected to climb to USD 856.82 million by 2031.

Which segment is growing fastest within this market?

Quantum cascade laser technology shows the quickest adoption, expanding at a 7.33% CAGR through 2031 due to its mid-infrared trace-gas capabilities.

How are emissions regulations influencing demand?

Post-2025 rules in Asia-Pacific and Africa require multi-pollutant continuous monitoring, adding roughly +1.2% to the overall CAGR.

Why are healthcare facilities investing in laser analyzers?

Hospitals need continuous anesthetic-gas and volatile-organic-compound tracking to meet ASHRAE 170-2021 and occupational exposure limits.

Which region will post the highest growth rate?

Asia-Pacific is expected to register a 7.55% CAGR through 2031, driven by Chinese and Indian air-quality mandates and subsidy programs.

Page last updated on: